Ergonomic Office Furniture Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

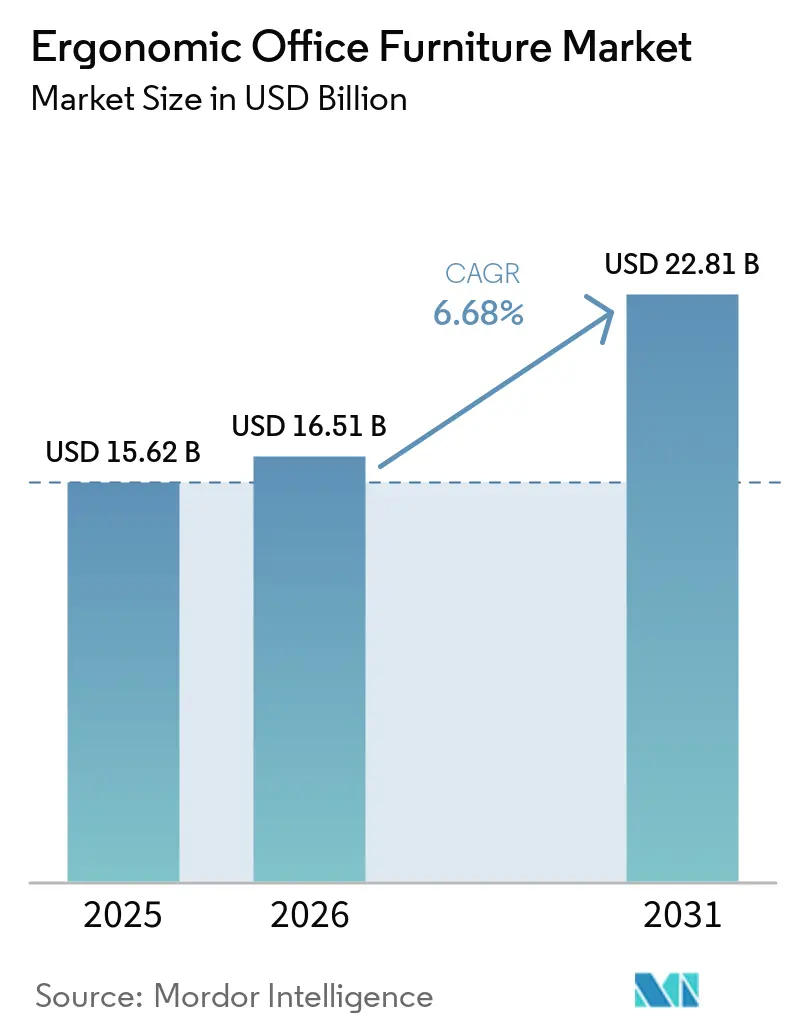

| Market Size (2026) | USD 16.51 Billion |

| Market Size (2031) | USD 22.81 Billion |

| Growth Rate (2026 - 2031) | 6.68% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ergonomic Office Furniture Market Analysis by Mordor Intelligence

The ergonomic office furniture market size is projected to be USD 15.62 billion in 2025, USD 16.51 billion in 2026, and reach USD 22.81 billion by 2031, growing at a CAGR of 6.68% from 2026 to 2031. The ergonomic office furniture market is also supported by a more structured return-to-office pattern, as 62% of organizations now mandate fixed in-office days, which sustains replacement demand for better chairs, desks, and shared workstations. The ergonomic office furniture market is gaining another layer of support from hybrid employees, as Gensler found that 1 in 4 workers still relies on do-it-yourself fixes for ergonomics, temperature, or privacy, which leaves a clear unmet need in both employer-funded and self-funded purchases. At the same time, actual global office utilization remained at 56% against a 74% target in 2026, so the ergonomic office furniture market still faces delays when facility managers extend asset lifecycles rather than authorizing full refresh cycles[1]JLL, “Structured Hybrid Work Becomes the Global Norm as Strategic Focus Shifts to AI-Readiness,” JLL, jll.com.

Key Report Takeaways

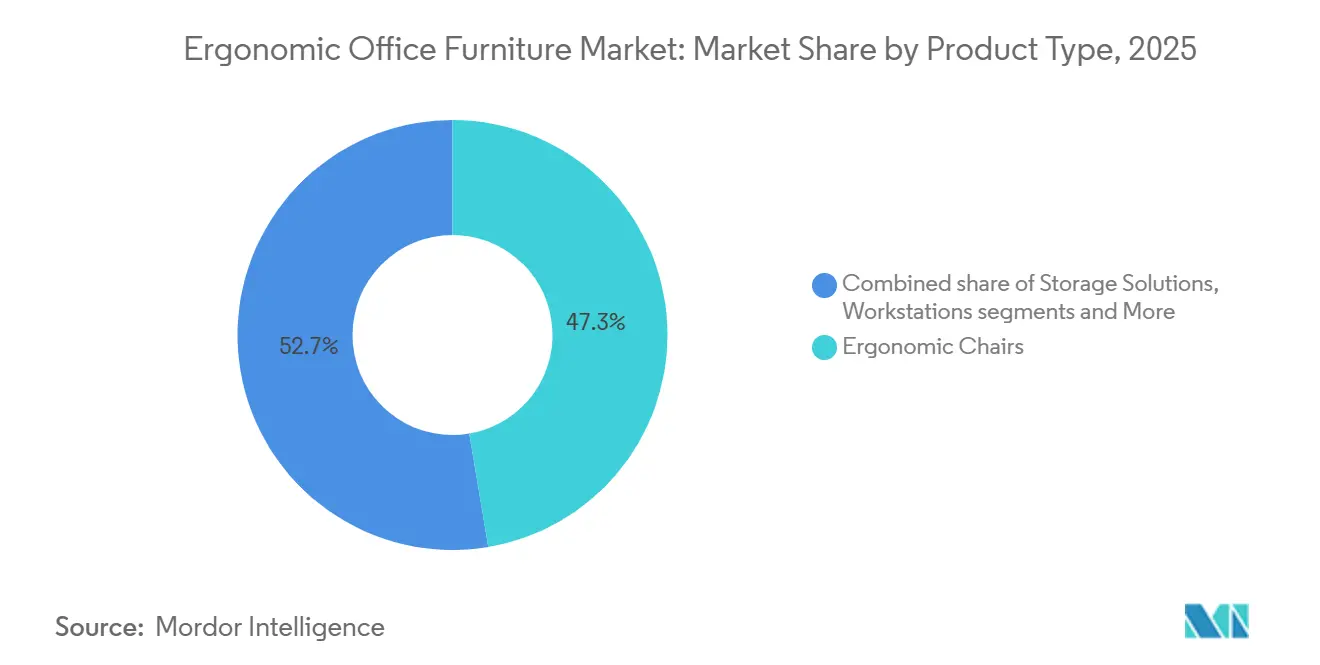

- By product type, ergonomic chairs led with 47.34% of the ergonomic office furniture market share in 2025, while height-adjustable desks and tables are projected to expand at an 8.45% CAGR through 2031.

- By material, wood held 46.11% of the ergonomic office furniture market share in 2025, whereas metal is forecast to grow at a 7.26% CAGR through 2031.

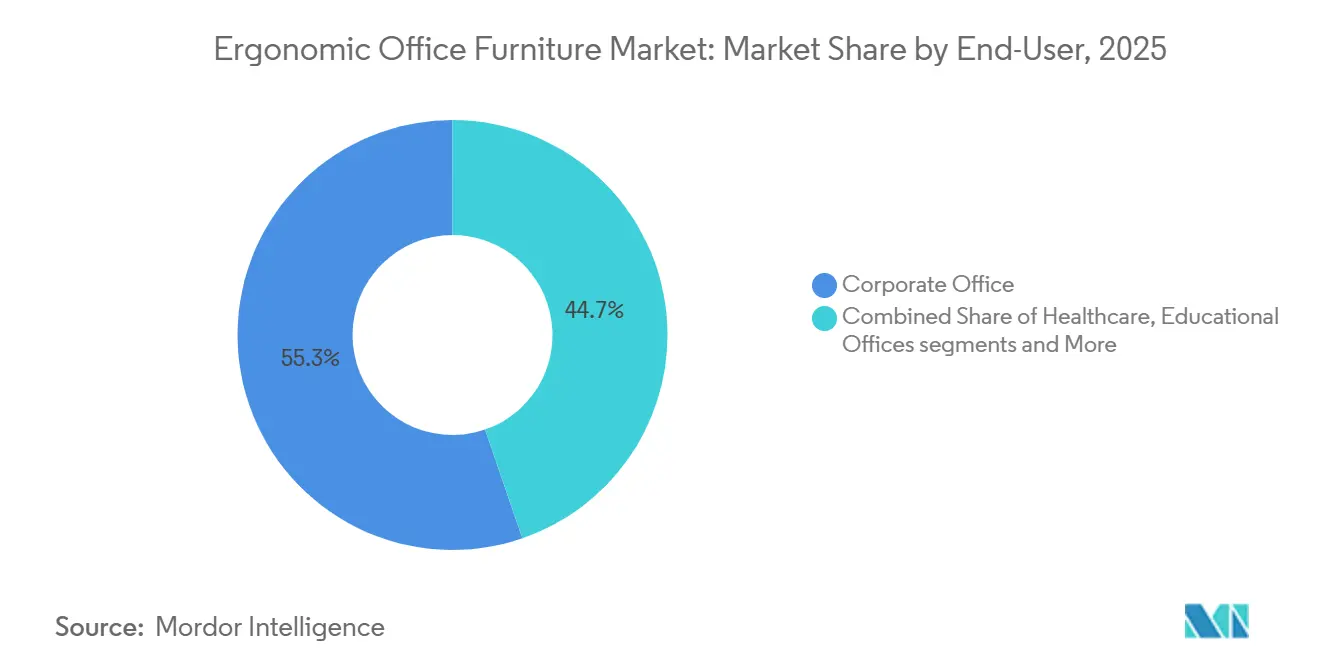

- By end-user, corporate offices captured 55.28% of the ergonomic office furniture market share in 2025, while hospitality and retail back-offices are expected to advance at an 8.32% CAGR through 2031.

- By distribution channel, B2B/project sales accounted for 67.01% of the ergonomic office furniture market share in 2025, while B2C/retail is projected to grow at a 7.51% CAGR through 2031.

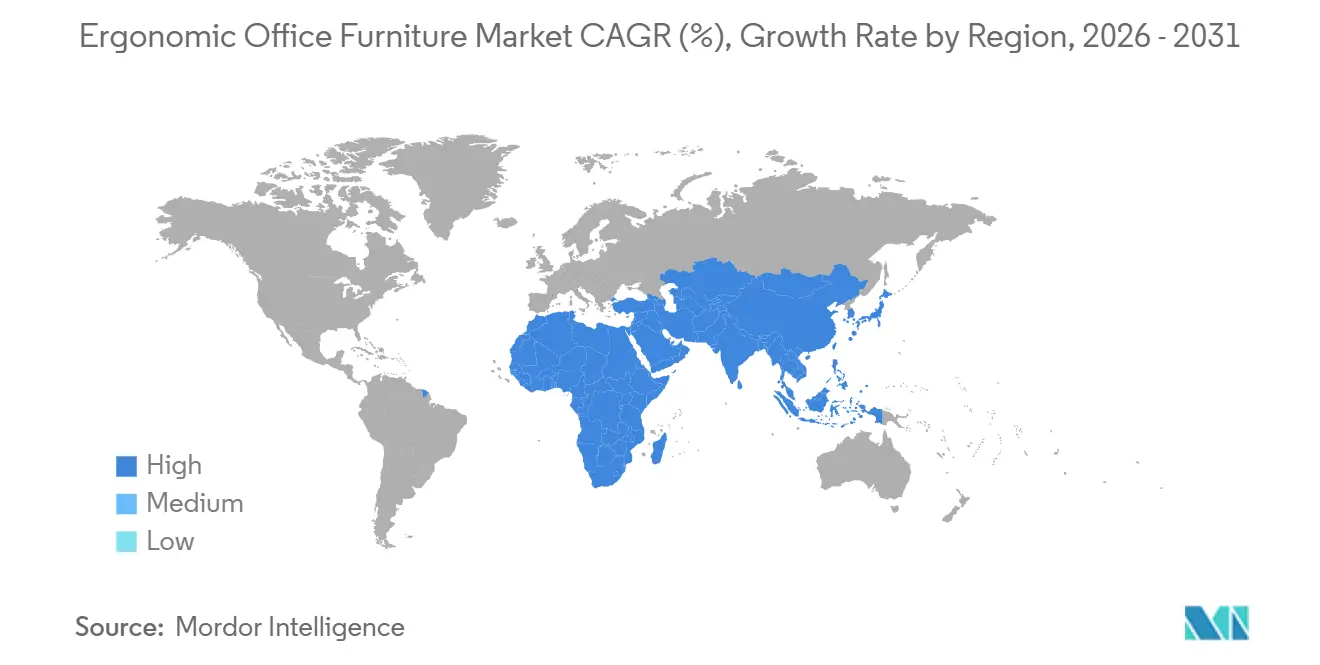

- By geography, North America accounted for 37.52% of the ergonomic office furniture market share in 2025, whereas Asia-Pacific is forecast to expand at a 8.26% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ergonomic Office Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Workplace Ergonomics and Musculoskeletal Risk Reduction | +1.4% | Global, with the highest intensity in developed occupational health markets | Medium term (2-4 years) |

| Corporate Wellness and Productivity Investment | +1.6% | North America and Europe, with early spillover into Asia-Pacific enterprise hubs | Medium term (2-4 years) |

| Hybrid Work and Hybrid Office Refits | +1.0% | North America and Europe, expanding into a structured hybrid Asia-Pacific markets | Short term (≤ 2 years) |

| Smart Furniture and Sensor-Enabled Workstation Adoption | +0.5% | Global, concentrated in North America and Northern Europe | Medium term (2-4 years) |

| Sustainable Procurement and Circular Furniture Demand | +0.7% | Europe-led, with growing adoption in North America and Asia-Pacific | Medium term (2-4 years) |

| Growth in Flexible and Hot-Desking Office Models | +1.2% | Global, strongest in North America and the United Kingdom | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Workplace Ergonomics and Musculoskeletal Risk Reduction

The ergonomic office furniture market is increasingly tied to measurable health outcomes rather than general workplace aesthetics. In 2024 and 2025, the United Kingdom Health and Safety Executive recorded 511,000 workers with work-related musculoskeletal disorders, resulting in 7.1 million working days lost and 14 days of absence per case on average[2]Health and Safety Executive, “Work-Related Musculoskeletal Disorders Statistics in Great Britain, 2025,” HSE, hse.gov.uk. Those disorders accounted for 27% of all work-related ill health cases in Great Britain, and back disorders alone accounted for 43% of all musculoskeletal cases, keeping seating posture and workstation setup at the center of employer attention. The ergonomic office furniture market also benefits from workforce aging, as HSE data show a musculoskeletal prevalence of 2,540 per 100,000 among males aged 55 and above, supporting a longer replacement cycle for higher-support seating and adjustable desks in mature labor markets.

Corporate Wellness and Productivity Investment

The ergonomic office furniture market is increasingly being funded through workforce wellbeing priorities rather than only through facilities budgets. Research cited by the Global Wellness Institute showed that companies embedding wellbeing into leadership and organizational design reported productivity increases of 20% to 25%, providing ergonomic procurement with a more direct business case in large enterprises[3]Global Wellness Institute, “Workplace Wellbeing Initiative Trends for 2026,” Global Wellness Institute, globalwellnessinstitute.org. The same 2026 report noted that musculoskeletal disorders account for more than USD 2 trillion in global economic losses each year, underscoring the need for prevention-oriented spending in human capital planning. Willis Towers Watson’s 2024 wellbeing survey, as cited there, also pointed to 46% of global employers making wellbeing foundational to strategy by 2027, suggesting the ergonomic office furniture market will continue to attract attention from HR and finance teams together. The ergonomic office furniture market is also supported by repeat buying behavior, as companies that made early wellness-led purchases are now entering their first planned refresh cycle with higher specifications and larger budgets.

Hybrid Work and Hybrid Office Refits Redefine The Fitout Brief

The ergonomic office furniture market is now shaped by hybrid work as a steady operating model rather than a short-lived post-pandemic adjustment. JLL reported in 2026 that 62% of organizations mandate fixed in-office days, up from 49% a year earlier, while the gap between actual and target utilization narrowed from 25 percentage points in 2025 to 18 percentage points in 2026. That pattern means fewer desks in some locations. Still, it also means the desks that remain are being specified to a higher ergonomic standard, so employees see value in returning to the office. Haworth’s 2026 YourPlace Flex shows how suppliers are responding, with height-adjustable workstations and personalized sit-stand controls built for shared users in hot-desk environments[4]Haworth, “YourPlace Flex Brochure, Asia-Pacific, 2026,” Haworth, haworth.com. Gensler also found that flexible furniture and updated technology were among the design features most closely linked with employees rating a workplace as effective for learning, which supports continued hybrid-office refits in the ergonomic office furniture market.

Smart Furniture And Sensor-Enabled Workstation Adoption Reshapes The Product Roadmap

The ergonomic office furniture market is moving closer to workplace technology as connected desks and occupancy-aware workstations gain relevance. Steelcase’s Workplace Advisor platform uses Microsoft Azure IoT to collect anonymous occupancy data, helping clients connect furniture use to future planning decisions rather than relying solely on occasional manual audits. Gensler reported that utilization data now informs 90% of planning decisions globally, up from 70% in 2025, which increases the appeal of workstations that generate continuous usage signals. Haworth’s 2026 launch of YourPlace Flex in Asia-Pacific further shows that smart controls and posture reminders are moving into mainstream product design rather than staying limited to niche premium concepts. The ergonomic office furniture market may also see higher vendor stickiness over time, because data platforms tied to connected furniture make single-brand ecosystems more practical for large occupiers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost Versus Conventional Furniture | -1.2% | Global, most acute in SMEs in APAC and South America | Short term (≤ 2 years) |

| Corporate Footprint Consolidation Reducing Seat Density | -0.9% | North America and Europe, especially where hybrid mandates are established | Medium term (2-4 years) |

| Retrofit Complexity in Legacy Workplaces | -0.6% | Europe’s older building stock and parts of the Middle East and Africa | Long term (≥ 4 years) |

| Price Pressure From Low-Cost And Regional Manufacturers | -0.8% | Asia-Pacific, South America, and price-sensitive segments globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Versus Conventional Furniture

The ergonomic office furniture market still faces a clear cost barrier in small and mid-sized organizations. A mid-range ergonomic task chair from a leading manufacturer typically carries a list price of USD 800 to USD 1,500, compared with USD 100 to USD 300 for a conventional office chair, which makes full replacement difficult without a proven return case. HSE data also showed that workplaces with fewer than 50 employees had the highest musculoskeletal disorder prevalence rates, indicating that many of the firms with the greatest need still have the weakest capacity to fund premium ergonomic upgrades. That cost gap often pushes buyers toward accessories such as monitor arms, lumbar supports, and keyboard trays instead of core furniture replacement. The ergonomic office furniture market may ease this barrier over time through furniture-as-a-service and circular rental models, but adoption outside North America and Northern Europe remains limited.

Corporate Footprint Consolidation Reducing Seat Density

The ergonomic office furniture market faces a volume constraint, as many occupiers are reducing seat counts rather than fitting every legacy desk with newer ergonomic products. JLL reported actual global office utilization at 56% against a 74% target in 2026, which continues to put pressure on facility managers to shrink desk footprints before they launch full-scale refresh programs. This creates a mixed outcome for the ergonomic office furniture market, because premium brands can still raise value per workstation even while total units shipped grow more slowly. The strongest pressure is centered in North America and Europe, which are also the regions with the highest ergonomic spend per workstation and the deepest installed base. Once major occupiers complete footprint rationalization, the ergonomic office furniture market is likely to see a later synchronized replacement wave from the smaller but higher-quality workstation base that remains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Chairs Lead, Height-Adjustable Desks Drive the Next Growth Phase

Ergonomic chairs held 47.34% of the ergonomic office furniture market share in 2025, which kept seating as the core purchase in most commercial fitouts. Chairs remain the most established category because they are directly associated with posture support, daily comfort, and musculoskeletal risk reduction in desk-based work. The ergonomic office furniture market for height-adjustable desks and tables is projected to expand at a 8.45% CAGR through 2031, making them the fastest-growing product type in the forecast period. That growth reflects a shift in buyer expectations, as sit-stand capability is moving from a wellness add-on to a standard feature in many hybrid and hot-desk layouts.

Herman Miller’s February 2025 launch of the Spout Sit-to-Stand Table showed how the category is moving beyond simple adjustment into premium design and stronger mechanical performance, with 4 in-line motor actuators and a 400 lb lift capacity. Workstations and benching systems hold a smaller but important place in the ergonomic office furniture market because they support open-plan layouts that need density, cable discipline, and easier reconfiguration. Accessories such as monitor arms, laptop stands, and lumbar supports are gaining traction in the B2C channel, where many hybrid workers prefer smaller-step purchases rather than full furniture replacements. A 24-month study published in the International Journal of Behavioral Nutrition and Physical Activity found that sit-stand interventions sustained 60 minutes of reduced sitting during an 8-hour workday, which continues to reinforce buying decisions in this part of the ergonomic office furniture industry.

By Material: Wood Anchors Aesthetics, Metal Gains Through Institutional Durability Requirements

Wood accounted for 46.11% of the ergonomic office furniture market in 2025, which reflected its established role in executive offices, educational settings, and higher-end interiors that value visual warmth. Buyers continue to favor wood in spaces where furniture is expected to support both ergonomic function and a polished design language. Metal is the fastest-growing material segment at a 7.26% CAGR through 2031, and the ergonomic office furniture market for metal-based products is being boosted by durability, traceability, and lower lifecycle replacement needs in public and large-enterprise contracts. Plastic and polymer components still keep a meaningful role in seating shells and accessories, where lower weight and design flexibility remain useful.

The ANSI/BIFMA e3-2024 Furniture Sustainability Standard, approved by ANSI on April 21, 2025, and required for new certifications from April 22, 2026 onward, has materially raised expectations around material transparency, chemical disclosure, and supply chain traceability. That shift is changing procurement behavior in the ergonomic office furniture market, especially in public sector and enterprise accounts that link qualification to sustainability certifications. Steelcase said at its June 2025 Chicago WorkLife Center opening that it had doubled recycled content in high-performance seating, using recycled plastics from water bottles and carpet scraps, which shows how major suppliers are aligning product claims with traceable materials narratives. Within the ergonomic office furniture industry, this raises the quality threshold for smaller suppliers that still compete mainly on price but cannot yet match the same documentation depth.

By End-User: Enterprise Office Dominates, Hospitality Back-Office Accelerates

Corporate offices accounted for 55.28% of the ergonomic office furniture market in 2025, keeping enterprise fitouts as the largest source of demand. Large companies continue to dominate because they buy at the system level, refresh across full floors, and often align procurement with wellness, facilities, and risk management goals. Hospitality and retail back offices are advancing at an 8.32% CAGR through 2031, and the ergonomic office furniture market tied to this cohort is growing as operators pay closer attention to repetitive-task conditions, retention pressure, and staff comfort. This shift matters because the buying logic is changing from front-of-house design value to back-of-house productivity and injury prevention.

Humanscale’s January 2026 NexPoint launch demonstrated how suppliers are developing products specifically for this space, including a fully ADA-compliant ergonomic point-of-sale solution for retail, hospitality, and healthcare settings. Healthcare offices remain important but are more constrained, as infection-control needs narrow material choices and limit some specification options common in general corporate environments. Educational and government offices move more slowly because purchasing cycles are longer and tender rules are stricter, yet they still give the ergonomic office furniture market a stable demand base. European Commission material on Helsinki’s circular furniture tender also shows that public procurement is gradually raising expectations for durability, reuse, and traceability, rather than buying only on initial price.

By Distribution Channel: B2B/Project Scale Holds, B2C/Retail Captures the Hybrid Dividend

B2B and project channels accounted for 67.01% of the ergonomic office furniture market in 2025, reflecting the scale, logistics, and specification complexity of corporate and government buying. The contract channel remains dominant because large projects require dealer networks, installation support, space planning coordination, and compliance documentation that standard retail channels cannot easily replicate. B2C and retail are projected to grow at a 7.51% CAGR through 2031, making them the fastest-growing distribution channels in the ergonomic office furniture market. That growth is closely tied to hybrid workers and small firms buying directly through online stores, brand websites, and specialty retailers.

Online retail is the strongest sub-channel inside B2C because it shortens the buying journey and lets users compare features, configure desks, and review ergonomic accessories without involving contract intermediaries. Gensler’s 2026 survey found that 1 in 4 employees is making do-it-yourself fixes to improve ergonomics or related workplace conditions, indicating a large consumer pool already self-solving and ready to be converted into branded purchases. Direct-to-consumer brands such as FlexiSpot, UPLIFT Desk, and Autonomous have gained traction by offering faster delivery, simpler price points, and digital-first comparison tools. The ergonomic office furniture market is also seeing some channel overlap, because companies with fewer than 100 employees often buy through retail pathways even when the end use still resembles a small commercial fitout.

Geography Analysis

North America held 37.52% of the ergonomic office furniture market share in 2025, making it the largest regional contributor by revenue. The United States remains the anchor market because employers, insurers, and risk managers can point to direct injury costs when justifying better chairs, desks, and shared workstations. Canada adds steady demand through large employers in finance and technology that continue to run structured ergonomic programs aligned with occupational health expectations. Mexico is also becoming more relevant to the ergonomic office furniture market as nearshoring supports investment in compliant workplace facilities for multinational manufacturers.

Europe represents a mature part of the ergonomic office furniture market, where sustainability rules, circular procurement, and supplier documentation strongly shape buyer standards. The region’s institutional demand is increasingly filtering out vendors that cannot meet stricter expectations on materials, traceability, and lifecycle thinking. The Nordics remain the most developed ergonomic procurement environment in Europe because workstation standards, labor structures, and long-standing office design practices reinforce demand quality. Germany, France, the United Kingdom, Italy, Spain, and the BENELUX countries still account for the largest regional volumes, supported by a strong contract furniture base and established local manufacturing capacity.

Asia-Pacific is advancing at a 8.26% CAGR through 2031, making it the fastest-growing geography in the ergonomic office furniture market. The region is benefiting from new commercial real estate supply, first-time ergonomic adoption in enterprise offices, and an industrial base that serves both export and domestic demand. Steelcase’s June 2026 dealer showroom opening in Chennai signaled how global brands are positioning for demand from India’s corporate technology and back-office hubs. China remains the largest production base in the region, while Vietnam and Indonesia continue to gain attention as alternative supply locations for cost-sensitive manufacturing. The Middle East and Africa are supported by commercial development tied to diversification programs, and South America is led by Brazil, with additional growth coming from formalizing office demand in Argentina, Chile, and Peru.

Competitive Landscape

The ergonomic office furniture market remains moderately fragmented, with MillerKnoll, Steelcase, Haworth, HNI Corporation, and KOKUYO holding meaningful but not dominant positions in global revenue. The premium contract tier is more concentrated in North America and Europe, where long dealer networks, design reputation, and ergonomic research credentials still shape specification wins. In this part of the ergonomic office furniture market, suppliers compete less on single products and more on full workplace systems that combine seating, height-adjustable desks, storage, and accessories into one coordinated offer. That systems approach gives larger vendors an advantage because architects, dealers, and workplace planners often prefer a smaller set of integrated suppliers for multi-floor projects.

Technology and sustainability now define much of the competitive agenda in the ergonomic office furniture market. Steelcase’s Workplace Advisor platform uses occupancy data to support space-planning decisions, turning connected furniture into a planning input rather than just a purchased asset. MillerKnoll’s Sustainability without Compromise presentation at Clerkenwell Design Week 2026 showed how material transparency and circular design are now part of mainstream competitive positioning rather than side initiatives. Humanscale’s Re-Freshed program, launched in August 2024, further showed that suppliers are building second- and third-life product cycles into their commercial narratives as institutional buyers place greater weight on circularity. These moves are raising the entry threshold in the ergonomic office furniture market for smaller firms that lack the capital to support connected platforms, showroom expansion, and traceable sustainability claims.

Challenger brands still have room to grow in the mid-market of the ergonomic office furniture market, where buyers want better ergonomics but cannot absorb premium contract pricing. Direct-to-consumer companies such as FlexiSpot, UPLIFT Desk, and Autonomous are gaining with online-first distribution, simpler price ladders, and faster product cycles. KI’s June 2026 launch of the Kiaura Collection with Cognetic Technology showed how mid-tier competitors are trying to widen the value proposition from injury prevention to focus, conferencing, and broader human performance. Geographic expansion is also becoming a practical growth lever, as brands push into South Asia, hospitality back-offices, and other underpenetrated demand pockets where premium incumbents have historically had lighter coverage.

Ergonomic Office Furniture Industry Leaders

Herman Miller, Inc.

Steelcase Inc.

Haworth Inc.

HNI Corporation

KOKUYO Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: At Chicago Design Days, the Aeron Chair was introduced in 2 new colorways with advanced 8Z Pellicle material. This update is considered a significant revision to the Aeron in recent years, incorporating advancements in biomechanical research and sustainable design principles to address a broader range of body types and user preferences.

- June 2026: At Chicago Design Week, the Spring 2026 portfolio was showcased, featuring the Migration Desking Collection with expanded basic height options for cost-effective ergonomic projects. The Ocular Frame was also presented, designed for AV connectivity in hybrid spaces. The showcase focused on research highlighting the connection between workspace cognitive design and improved employee productivity.

- June 2026: KI introduced the Kiaura Collection, built with Cognetic Technology. This collection, referred to as Human Performance Seating, is designed for focus, conferencing, and lounge environments, emphasizing cognitive performance through cohesive ergonomic and visual design.

- May 2026: At Clerkenwell Design Week 2026 in London, MillerKnoll brands launched several new products. These included Knoll's Konzert private office system by Paolo Dell'Elce and Colebrook Bosson Saunders' Lana laptop stand, which received an award. The event highlighted MillerKnoll's focus on circular design and material innovation, demonstrated through the Sustainability without Compromise exhibit.

Global Ergonomic Office Furniture Market Report Scope

| Ergonomic Chairs |

| Height-Adjustable Desks and Table |

| Workstations and Benching Systems |

| Storage Solutions |

| Ergonomic Accessories (monitor arms, laptop stands, lumbar & seat cushions, etc.) |

| Others |

| Wood |

| Metal |

| Plastic & Polymers |

| Other Materials |

| Corporate Office |

| Healthcare Offices |

| Educational Offices |

| Government and Public Offices |

| Hospitality and Retail Back-Offices |

| Other End-Users |

| B2B/Project | |

| B2C/Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Local Workshops | |

| Other Distribution Channels |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and the Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of the Middle East and Africa |

| By Product Type | Ergonomic Chairs | |

| Height-Adjustable Desks and Table | ||

| Workstations and Benching Systems | ||

| Storage Solutions | ||

| Ergonomic Accessories (monitor arms, laptop stands, lumbar & seat cushions, etc.) | ||

| Others | ||

| By Material | Wood | |

| Metal | ||

| Plastic & Polymers | ||

| Other Materials | ||

| By End-User | Corporate Office | |

| Healthcare Offices | ||

| Educational Offices | ||

| Government and Public Offices | ||

| Hospitality and Retail Back-Offices | ||

| Other End-Users | ||

| By Distribution Channel | B2B/Project | |

| B2C/Retail | Home Centers | |

| Specialty Furniture Stores | ||

| Online | ||

| Local Workshops | ||

| Other Distribution Channels | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and the Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of the Middle East and Africa | ||

Key Questions Answered in the Report

What is driving growth in ergonomic office furniture through 2031?

Growth is being supported by rising employer focus on musculoskeletal risk, structured hybrid office refits, and higher adoption of adjustable and sensor-enabled workstations. The market is projected to reach USD 22.81 billion by 2031 at a 6.68% CAGR.

Which product category leads current demand?

Chairs led demand with a 47.34% share in 2025 because they remain the most direct and widely adopted ergonomic upgrade across office environments.

Which product area is growing the fastest?

Height-adjustable desks and tables are forecast to grow at an 8.45% CAGR through 2031 as sit-stand capability becomes a more standard feature in enterprise and hybrid layouts.

Why does North America remain the largest regional contributor?

North America held 37.52% share in 2025 because it has mature corporate wellness programs, higher ergonomic spend per workstation, and stronger risk-based justification for preventive workplace investment.

Why is Asia-Pacific expanding faster than other regions?

Asia-Pacific is projected to grow at an 8.26% CAGR through 2031 due to new commercial real estate, first-time ergonomic adoption by enterprise buyers, and localized expansion by global and regional suppliers.

How concentrated is competition among leading brands?

Competition is moderate rather than tight. Large suppliers such as MillerKnoll, Steelcase, Haworth, HNI Corporation, and KOKUYO are influential, but the broader field still includes mid-market and online-first challengers.

Page last updated on: