Equine Supplement Products Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 91.88 Million |

| Market Size (2031) | USD 104.42 Million |

| Growth Rate (2026 - 2031) | 2.59% CAGR |

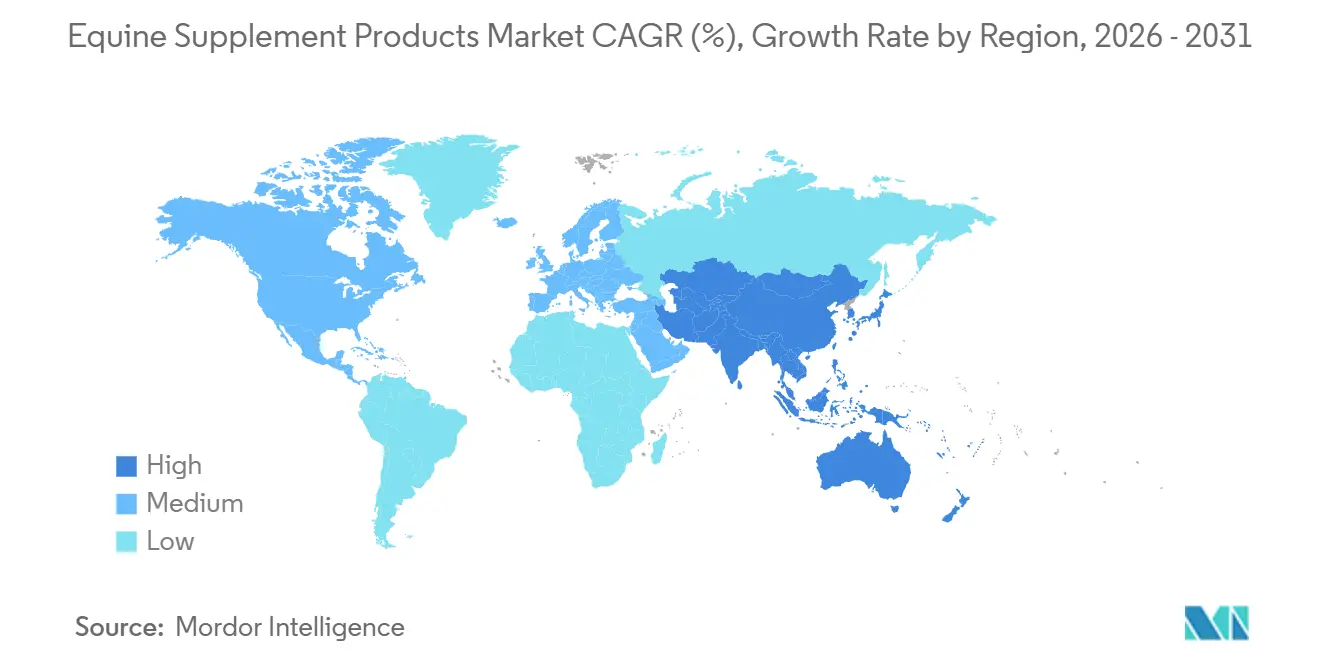

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Equine Supplement Products Market Analysis by Mordor Intelligence

The Equine Supplement Products Market size is projected to be USD 90.49 million in 2025, USD 91.88 million in 2026, and reach USD 104.42 million by 2031, growing at a CAGR of 2.59% from 2026 to 2031.

Structural shifts are visible as regulatory clarification in North America accelerates commercialization of botanical feed ingredients alongside pharmaceutical-grade actives, which shortens product development cycles and broadens innovation in joint and gastric care. Asia-Pacific’s demand is led by expanding participation in equestrian sports and sustained racing infrastructure, and the region is forecast to post the highest growth rate in the period. North America remains the anchor geography by revenue share, reflecting the United States’ mature base of breeding, training, and competition-oriented consumption. Digital channels are reshaping route-to-market dynamics, as subscription and tele-veterinary models lower initial access costs and simplify repeat purchase behavior. Ingredient science is transitioning from commodity vitamins to precision bioactives supported by peer-reviewed studies, strengthening claims around mobility, hoof integrity, and gut health.

Key Report Takeaways

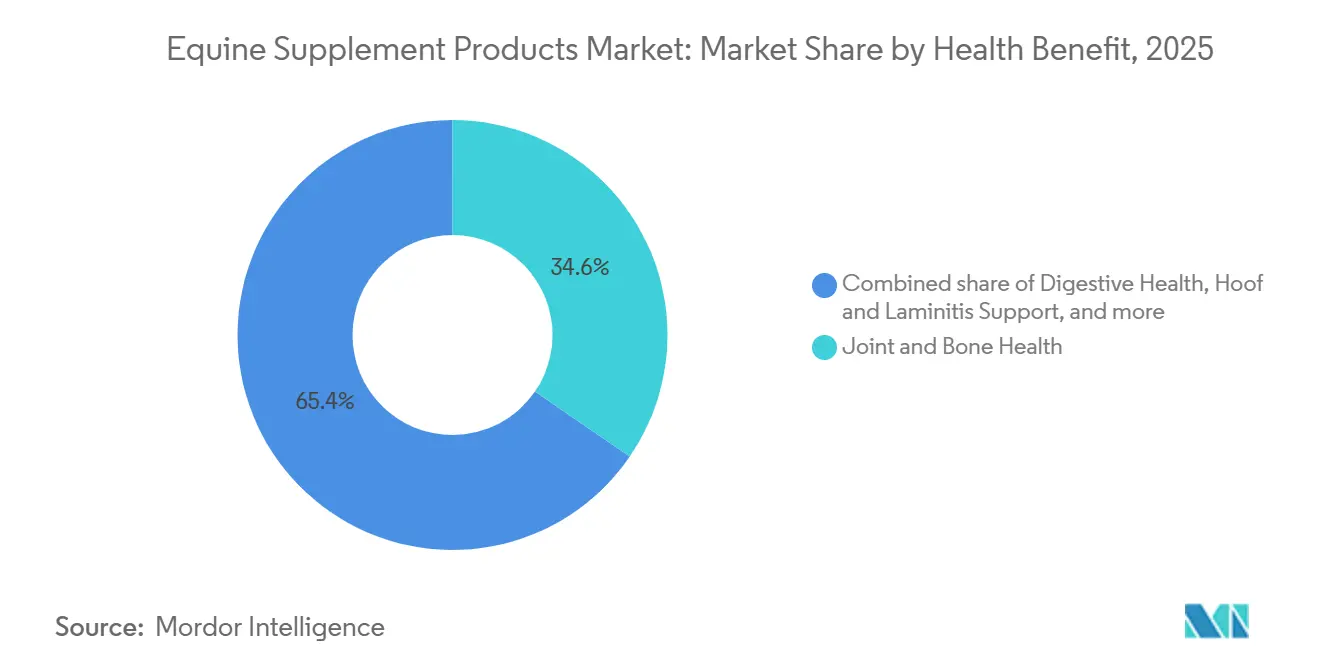

- By application, Joint & Bone Health led with 34.56% revenue share in 2025, while Hoof & Laminitis Support is projected to advance at a 4.51% CAGR through 2031.

- By ingredient type, Proteins & Amino Acids held 41.24% share in 2025, and Herbal, Botanical, and Nutraceutical ingredients are expected to grow at a 4.14% CAGR over 2026-2031.

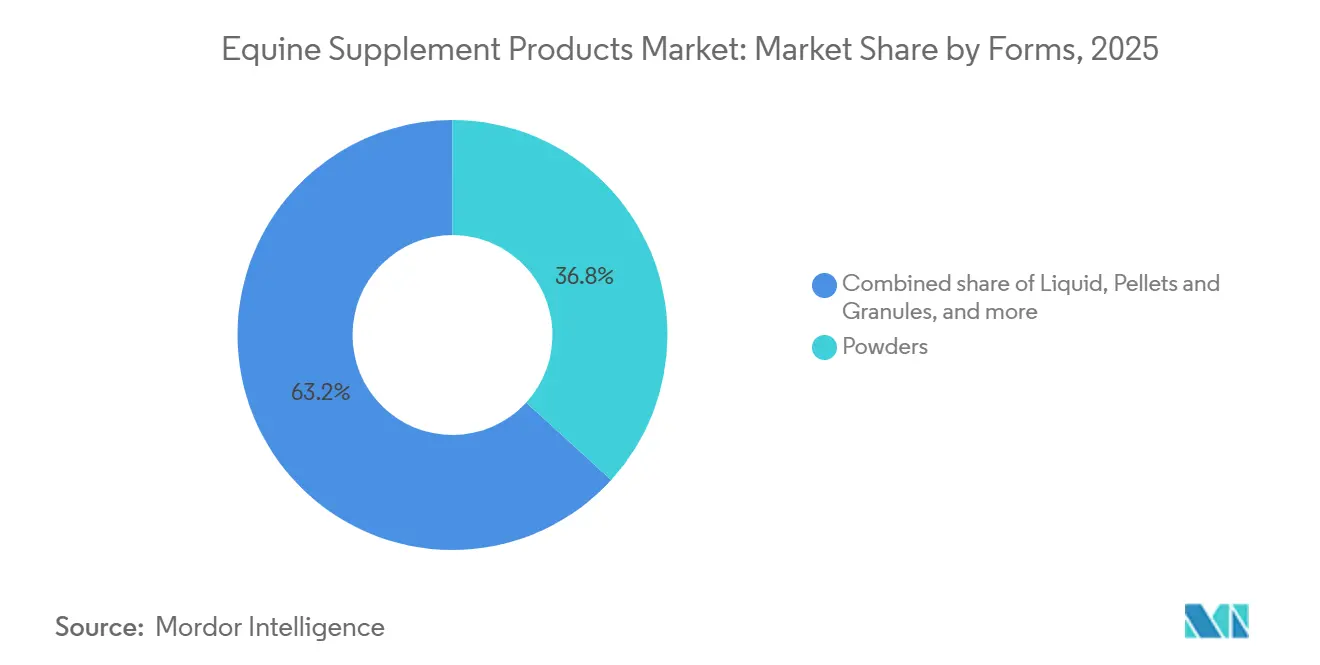

- By form, Powders accounted for a 36.78% share in 2025, and Liquids are forecast to expand at a 4.65% CAGR through 2031.

- By distribution channel, Veterinary Hospitals & Clinics captured 33.67% share in 2025, while Online Retail is projected at a 4.96% CAGR over 2026-2031.

- By geography, North America commanded a 42.67% share in 2025, and Asia-Pacific is set to grow at a 5.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Equine Supplement Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Online retail and D2C penetration reshapes access and assortment | +0.6% | Global, with early gains in North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Rising joint and bone health management in performance and aging horses | +0.5% | North America & Europe, with spill-over to Latin America and Asia-Pacific | Medium term (2-4 years) |

| Preventive veterinary care and owner nutrition awareness | +0.4% | North America, EU core, Australia, expanding in urban Asia | Medium term (2-4 years) |

| Evidence-based nutraceuticals, probiotics, and clean-label innovation | +0.5% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Personalized programs and subscription nutrition tied to tele-vet insights | +0.4% | North America (mature telehealth infrastructure), Western Europe, Australia | Short term (≤ 2 years) |

| Regulatory approvals for novel feed additives improve efficacy claims | +0.3% | North America (FDA GFI #293), Europe (EFSA pathways), Asia-Pacific (emerging frameworks) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Online Retail and D2C Penetration Reshapes Access and Assortment

The equine supplement products market continues to benefit from rapid e-commerce adoption, as online channels scale assortment beyond the constraints of local vet clinics and tack stores, with online retail identified as the fastest-growing distribution route in the forecast period. Direct-to-consumer programs that bundle diet analysis, subscription auto-ship, and curated formulations improve convenience and trust, exemplified by Mad Barn’s integrated content and service model that includes free ration analysis for horse owners. Digital tools such as ration calculators and telehealth tie-ins are becoming table stakes, helping brands reduce friction at the point of decision while reinforcing compliance with feeding protocols over time.

Regulatory clarity in the United States supports this channel shift, since FDA’s final guidance on AAFCO-defined ingredients enables interstate commerce for listed feed ingredients, reducing uncertainty for compliant online sellers [1]“FDA’s Final Guidance for AAFCO-Defined Ingredients,” Association of American Feed Control Officials, aafco.org. Online approaches also allow rapid education on clean-label positioning and formulation science, which has become a determinant of conversion in higher value segments such as joint support and digestive health. As consumers diversify sourcing from physical retail to marketplaces and first-party sites, repeat purchase reliability and transparent ingredient disclosure are emerging as core differentiators.

Rising Joint and Bone Health Management in Performance and Aging Horses

Application-level demand in the equine supplement products market remains anchored by mobility and structural support, as owners seek to sustain performance and extend working lifespans in aging sport and leisure horses. Beyond legacy glucosamine-chondroitin and hyaluronic acid combinations, new multi-modal bioactives are entering clinician and trainer toolkits and are being validated with relevant functional endpoints in recent trials.

A 12-week prospective study published in February 2026 reported that natural eggshell membrane supplementation improved rider-reported function and altered joint-angle kinematics in Warmblood horses with chronic lameness, which signals potential synergy from collagen, glycosaminoglycans, and hyaluronic acid components within a single matrix.

Cross-species findings in 2025 that combined curcumin C3 Complex with glucosamine and chondroitin to reduce osteoarthritis severity and inflammatory markers in canine models have influenced equine product development strategies for inflammatory modulation. Clean sport compliance remains a threshold requirement for elite use cases, and brands emphasize third-party quality systems and transparent labeling to navigate stringent competition rules in Europe and global federations. The combination of broader evidence, sport-specific nutrition demands, and regulatory diligence reinforces sustained demand for mobility-focused formulas.

Preventive Veterinary Care and Owner Nutrition Awareness

The equine supplement products market is being shaped by preventive nutrition behaviors as owners adopt structured diet planning to preempt issues related to weight, metabolic stress, and subclinical deficiencies. Industry programs that educate on body condition scoring, forage testing, and targeted supplementation reinforce earlier intervention and more consistent feeding adherence throughout the year.

Purina Animal Nutrition’s 2024 education effort around achieving and maintaining optimal body condition demonstrates how supplier-backed initiatives can raise awareness on weight management strategies that integrate feed and supplements. Veterinary-led guidance is an important factor in brand and product selection, especially when owners weigh clean-label preferences against the need for measurable outcomes in performance and recovery. Digital education hubs also heighten product literacy and can improve compliance as owners apply ration calculators and structured feeding schedules with ongoing feedback loops. Over time, these educational and clinical touchpoints support stable category spend and help migrate buyers from commodity inputs to evidence-backed formulations.

Evidence-Based Nutraceuticals, Probiotics, and Clean-Label Innovation

Evidence generation is accelerating in the equine supplement products market as research teams publish microbiome and nutraceutical studies that inform product design for gut, immune, and musculoskeletal support. A February 2026 peer-reviewed paper identified Akkermansia muciniphila as inversely correlated with small-intestinal colic, pointing to targeted prebiotic strategies that aim to support mucosal integrity and reduce inflammation in at-risk horses.

At the same time, randomized work in 2025 found no significant change in secretory IgA or microbiota composition from a commercial Lactobacillus blend in healthy adult horses, underscoring the need to match strains and delivery conditions to specific physiological states. Clean-label demand continues to pivot brands toward botanicals and minimally processed actives, supported by company-backed product launches that emphasize natural sourcing and the avoidance of synthetic preservatives.

Category participants must also navigate organic compliance challenges, as a 2024 report from USDA’s National Organic Program highlighted the heavy reliance on genetically modified microorganisms for certain vitamins like riboflavin, which complicates organic labeling without transparent disclosures. These scientific and regulatory dynamics are influencing claims, formulation architecture, and sourcing policies across premium ranges.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented regulation and inconsistent labeling/quality standards | -0.7% | Global, acute in U.S., Europe, Asia-Pacific | Long term (≥ 4 years) |

| Premium pricing constrains adoption in price-sensitive cohorts | -0.5% | Latin America, Southeast Asia, rural North America | Medium term (2-4 years) |

| Input-cost and supply volatility for specialty ingredients | -0.4% | Global, particularly marine oils (Asia-Pacific sourcing), herbal botanicals (supply concentration), shellfish-derived actives | Medium term (2-4 years) |

| Cost-of-living pressure reduces discretionary spend | -0.3% | Global, acute in inflation-hit regions (UK, EU periphery, Latin America) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Regulation and Inconsistent Labeling/Quality Standards

Regulatory structures for animal supplements sit between feed and drug frameworks, which creates ambiguity in claims, labeling, and interstate commerce, particularly in the United States. FDA’s final guidance acknowledging AAFCO-defined feed ingredients provides a clearer path for compliant use of listed inputs in feeds, yet products that imply therapeutic intent can still be scrutinized under new animal drug rules. Labeling rules for approved or conditionally approved new animal drugs remain stringent, which makes botanical multi-constituent blends challenging to position if claims drift into treatment territory that would otherwise require drug pathways.

These compliance considerations are magnified for companies that export across jurisdictions, since national implementations of feed hygiene and quality systems vary and can increase documentation and verification workloads. Competitive-sport requirements in Europe also drive manufacturers to invest in quality assurance schemes and supplier audits to mitigate contamination and meet clean-sport standards. Collectively, these regulatory and labeling complexities raise barriers for smaller entrants and contribute to uneven product consistency across markets.

Premium Pricing Constrains Adoption in Price-Sensitive Cohorts

Price sensitivity in emerging and value-conscious segments can limit uptake of premium formulations, particularly where ownership costs already constrain discretionary spend on supplements. Brands with strong clean-label positioning and clinical backing command price premiums that are justified for performance and recovery use cases, but these price points can be a hurdle for broader adoption in non-elite populations.

Company portfolios often include high-potency antioxidant or omega-3 products that signal premium positioning, which can be attractive to competition-focused owners while remaining out of reach for casual owners. Education on targeted use, transparent dosing, and visible performance outcomes can help buyers frame value, but macro affordability constraints persist in rural and developing markets. As digital commerce scales, subscription models that smooth monthly outlays may lessen price hurdles for some owners, yet pricing remains a gating factor for mass-market penetration in lower-income contexts. Suppliers therefore balance depth of evidence and quality controls with formulation strategies that keep core SKUs accessible to a wider base.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Health Benefit / Application: Hoof Support Gains as Farriers and Nutritionists Align

Joint & Bone Health accounted for the largest slice of the equine supplement products market in 2025 at 34.56%, reflecting the ongoing need to maintain soundness in both performance and aging horses. The equine supplements industry is adding multi-modal support inputs that complement traditional glucosamine-chondroitin and hyaluronic acid matrices with targeted anti-inflammatory and connective tissue support.

Natural eggshell membrane has moved into the discussion after a February 2026 clinical study in Warmblood horses showed functional improvements over a 12-week schedule, which has helped expand formulator interest in collagen-rich complexes[2]Young-Sam Kwon et al., “Natural Eggshell Membrane Supplementation for Chronic Lameness in Warmblood Horses,” Frontiers in Veterinary Science, frontiersin.org. Separate evidence in companion animals where curcumin C3 Complex combined with glucosamine and chondroitin reduced osteoarthritis severity has supported cross-species ingredient screening for equine joint health. Sports integrity is a parallel focus, and brands that operate in Europe emphasize quality systems and third-party testing frameworks to meet clean-sport expectations around competition eligibility. These trends are creating a more evidence-aware buyer who weighs ingredient provenance and trial endpoints when selecting joint formulas.

Hoof & Laminitis Support is the fastest-growing sub-application with a 4.51% CAGR forecast, and its momentum reflects closer coordination between farriers, veterinarians, and nutritionists targeting preventive lameness. Research into methylated tirilazad has reported reductions in laminar matrix metalloproteinase activity in experimental models, and although not yet approved for equine use, this work informs anti-inflammatory strategies that developers are tracking for future formulations. Biotin remains a staple of hoof support, and company guidance around sustained dosing supports owner compliance and farrier recommendations over extended time frames.

Digestive and gut health applications have expanded due to rising microbiome awareness, with attention to prebiotics that may support mucosal health in horses vulnerable to colic. As early evidence grows, application-level portfolios are tilting toward precision approaches rather than broad-spectrum blends, which can translate into clearer use cases at the point of care. These shifts reinforce the premium tier while also pushing formulators to document outcomes for owner-facing education and veterinary collaboration.

By Ingredient Type: Herbal Formulations Outpace Synthetics

Proteins & Amino Acids led ingredient demand with a 41.24% share in 2025, supported by lysine, methionine, and threonine to aid topline development, hoof keratin quality, and reproductive function. The equine supplement products market continues to incorporate these building blocks in balanced rations, often anchored by essential amino acid combinations within broader feed and supplement regimens. Botanical and nutraceutical inputs are the fastest-growing at a 4.14% CAGR, supported in the United States by regulatory clarity that AAFCO-listed feed ingredients can move across state lines, which reduces uncertainty for compliant ingredient use in commercial products.

Clean-label strategies are gaining prominence, including the use of wild-harvested or minimally processed actives and transparent supply chains, as shown by company announcements that emphasize natural sourcing and formula simplicity. This momentum increases the need for validated dosing protocols and supporting data so owners and clinicians can line up ingredients with intended outcomes across metabolic and performance profiles. As ingredient portfolios broaden, product developers are also addressing carrier systems and stability to protect bioactive integrity through the digestive tract.

Vitamins present a mixed picture due to organic compliance challenges that stem from widespread use of genetically modified microorganisms in industrial production of certain B vitamins. The 2024 USDA National Organic Program report highlighted riboflavin and other vitamins as typically produced through GMO fermentation, which complicates organic claims for equine feeds and supplements without transparent disclosures or alternative sourcing.

Enzymes, probiotics, and synbiotics remain active areas for development, though studies in healthy horses show that not all commercial probiotic blends produce measurable immunological or microbiota shifts, encouraging more targeted strain selection and context-specific use. Electrolytes and minerals, including chelated forms of copper, zinc, and manganese, continue to be staples due to their roles in thermoregulation and musculoskeletal function in training and competition settings. With a growing body of microbiome and nutraceutical evidence, brands are adopting tighter documentation practices for both raw material credentials and finished-product testing. This combination of scientific discipline and quality control underpins the premiumization visible across leading ingredient segments.

By Form: Liquids Surge on Bioavailability and Ease of Administration

Powders held the largest form factor at 36.78% share in 2025, a function of manufacturing efficiency, shelf stability, and practicality when top-dressed on grain rations. The equine supplements industry leverages powders for multi-nutrient blends and daily ration fortification, with pelletized versions used to reduce sorting and improve consistency in shared feeding environments.

Liquids are the fastest-growing form at a 4.65% CAGR as owners prioritize ease of administration, better palatability for picky eaters, and precise dosing with pump systems. Rapid uptake is most pronounced in use cases where timing and absorption matter, such as electrolyte replacement around training or competition and calming formulas during travel or show schedules.

Formulators also continue to apply microencapsulation and controlled-release technologies to protect sensitive actives and extend delivery profiles, which can benefit B vitamins or amino acids under sustained workloads. As the portfolio of liquid and pellet options broadens, decision drivers include dosing accuracy, storage considerations, and horse acceptance, each of which directly influences compliance and outcomes.

Pastes and gels retain a role in acute scenarios where targeted delivery is critical, such as short-duration electrolyte support or specific gastric applications. Chewable and treat-like formats have a smaller footprint relative to companion-animal categories, but they continue to capture niche behavioral or training use cases for owners who prioritize convenience.

Across all forms, the equine supplement products market size associated with faster-acting or precision-delivery products is expected to expand in line with the increasing use of digital coaching and veterinarian-directed protocols that emphasize timing and dose adherence. Brands are responding with clearer feeding directions and online calculators that map body weight, work level, and diet composition to daily dosing plans. As owners look to reduce waste and ensure intended intake, packaging ergonomics and dosing aids have become part of the overall value proposition in premium form factors. Collectively, these product and user-experience adjustments support the fastest growth rates in liquids and reinforce powder leadership for daily foundational nutrition.

By Distribution Channel: Online Platforms Disintermediate Traditional Gatekeepers

Veterinary Hospitals & Clinics represented 33.67% of channel share in 2025, due to professional credibility, in-clinic merchandising, and point-of-diagnosis recommendations. This channel remains central for clinical and performance use cases, especially where veterinarians align feeding protocols with diagnostic insights and follow-up schedules. Online retail is the fastest-growing route with a 4.96% CAGR, propelled by D2C and multi-brand marketplaces that combine auto-ship, content, and telehealth services to reinforce adherence and simplify replenishment.

As these platforms expand, they absorb discovery and education functions that used to sit with specialty retailers, although local tack stores continue to provide hands-on advice and regional stocking tailored to discipline and climate. Feed and farm stores hold ground in mixed-animal operations, with cross-species SKUs that meet basic equine needs but may lack the depth of sport-specific expert advice. Over time, the equine supplement products market is likely to see a stable coexistence between veterinary-led recommendations and digital-first subscription models that build direct relationships and recurring revenue.

Specialty brands are refining channel strategies to maximize their advantages in content, service, and trust-building. Company-backed guarantees, professional education modules, and free services such as ration analysis can drive conversion and retention without heavy discounting, which is attractive for premium portfolios. In competitive and regulated environments, manufacturers also time online releases around updated compliance guidance so that label and claim frameworks are synchronized across state and national boundaries.

As virtual consultations become part of routine nutrition management in many barns, platforms that connect diet analysis with product selection and delivery are positioned to gain share. This pattern elevates the importance of transparent ingredient lists and batch-level quality disclosures that can be referenced in remote clinical conversations. The net effect is a channel mix where online, veterinary, and specialty retail each maintain roles, while the fastest growth accrues to integrated digital experiences.

Geography Analysis

North America led the equine supplement products market with a 42.67% share in 2025, reflecting a deep base of competition disciplines, breeding programs, and sport-adjacent infrastructure that supports specialized nutrition demand. Regulatory clarification on AAFCO-defined ingredients has improved predictability for interstate commerce and online fulfillment, which aligns with the region’s strong adoption of D2C and marketplace channels. In Canada, suppliers with equine-specialist manufacturing and integrated education services contribute to regional growth by pairing science-based content with practitioner support.

Within the United States, labeling guidance for new animal drugs reinforces the need for clear label claims and careful separation between feed and drug positioning for any product that edges into therapeutic territory[3]“Labeling Requirements for Approved or Conditionally Approved New Animal Drugs,” Federal Register, federalregister.gov. With a large installed base of performance horses and a well-developed veterinary ecosystem, North America remains central to early adoption of innovation and to scaling clinically guided product lines. Overall, the region’s regulation, channel maturity, and customer education form a stable foundation for premiumization.

Europe displays steady growth under stricter pharmacovigilance and feed hygiene oversight, which encourages investments in quality systems and clean-sport validation. Brands that operate in the United Kingdom have retooled distribution relationships following post-Brexit trade changes, and a notable 2026 partnership for exclusive distribution has strengthened channel alignment for a leading sport-nutrition brand.

Asia-Pacific is projected to be the fastest-growing region with a 5.01% CAGR, a reflection of expanding equestrian participation and entrenched racing cultures that prioritize performance nutrition. Product development in Japan tends to emphasize microencapsulation and fermentation-derived inputs in line with local preferences for biotech-enabled nutrition, while Australia’s regulatory environment facilitates timely market access for compliant formulations. The equine supplement products market size in this region is influenced by a rising base of urban and peri-urban riders in select countries and by coaching ecosystems that encourage structured nutrition management across disciplines.

Competitive Landscape

The competitive structure features a mix of animal health conglomerates and specialist nutrition brands, with moderate fragmentation and intensifying differentiation through clinical validation, clean-label commitments, and integrated digital services. Specialist brands invest in education-led commerce that combines ration analysis, content, and responsive customer support, building credibility beyond price positioning. Product and marketing narratives are increasingly anchored to peer-reviewed evidence, visible quality systems, and sport eligibility to meet buyer expectations in performance contexts where compliance and efficacy are scrutinized.

Sponsorships embedded in racing and sport calendars deepen engagement with professional users and signal long-term brand commitment to horse welfare and competitive integrity. European distribution realignments underscore the importance of local partners that can scale brand presence while meeting national labeling and certification nuances. The outcome is a landscape where trusted science, channel fluency, and transparent sourcing become key levers for share gain.

Strategic moves illustrate this shift toward value creation through verified inputs and delivery. A 2026 exclusive distribution agreement expanded a leading European brand’s access to the UK specialty channel, reflecting an emphasis on specialist retail reach and sport-aligned positioning. Racing sponsorships across 2024 and 2025 in Ireland provided brand touchpoints with trainers and stable staff, alongside awards programs that recognize industry contributions, creating trust and loyalty at the heart of the racing supply chain.

Company-backed launches at the premium end continue to highlight clean-label sourcing and functional claims aligned to immune and cellular vitality. In North America, product portfolios that surface antioxidant strategies and targeted nutrient support maintain relevance for owners who want focused outcomes without drug-like claims. Collectively, these actions reinforce competitive intensity as brands seek to own distinct functional spaces and deepen relationships with veterinarians, farriers, and trainers.

Equine Supplement Products Industry Leaders

Cavalor

NAF (Natural Animal Feeds)

TRM (Thoroughbred Remedies Manufacturing)

Foran Equine

Mad Barn

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Gilad & Gilad, the sole provider of nutraceuticals featuring the neuroprotective ingredient G-Agmatine, proudly announced AgmaVet for Horses. This innovative product was designed to bolster nerve function resilience and ease joint discomfort.

- November 2025: Gerosynth Labs launched Mytulin EQ, an advanced equine nutritional supplement derived from wild-harvested Alaskan chaga mushrooms, targeting immune health, cellular vitality, and mitochondrial rejuvenation. The introductory pricing and formula positioning signaled a premium clean-label approach aimed at performance and senior cohorts.

- October 2025: Chewy enhanced its equine category presence by acquiring SmartEquine from Covetrus. This acquisition integrated subscription-based horse supplements, personalized nutrition plans, and a therapeutic product portfolio into Chewy's e-commerce platform. By capitalizing on SmartEquine's established customer base and veterinary partnerships, Chewy strategically expanded into the higher-margin health and wellness verticals.

Global Equine Supplement Products Market Report Scope

As per the scope of the report, equine supplement products are designed to support horse health, optimize performance, and promote longevity, with popular options addressing joint care, digestion, calming, and coat health. The equine supplement products market is segmented by health benefit/application, ingredient type, form, distribution channel, and geography. By health benefit/application, the market is segmented as joint & bone health, digestive/gut health, hoof & laminitis support, vitamins & minerals (general health & immunity), skin & coat, calming & nervous system, respiratory & immune support, performance & energy/recovery, and senior/metabolic support. By ingredient type, the market is segmented as proteins & amino acids, vitamins, enzymes / probiotics / synbiotics, electrolytes & minerals, and herbal/botanical / nutraceutical. By form, the market is segmented as powders, liquids, pellets & granules, pastes & gels, and chewables/treats. By distribution channel, the market is segmented as veterinary hospitals & clinics, pharmacies & drug stores, equine specialty & tack stores, feed & farm supply stores, online retail (marketplaces & D2C), and supermarkets & hypermarkets. By geography, the market is segmented as North America, Europe, Asia-Pacific, Middle-East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Joint & Bone Health |

| Digestive / Gut Health |

| Hoof & Laminitis Support |

| Vitamins & Minerals (General Health & Immunity) |

| Skin & Coat |

| Calming & Nervous System |

| Respiratory & Immune Support |

| Performance & Energy / Recovery |

| Senior / Metabolic Support |

| Proteins & Amino Acids |

| Vitamins |

| Enzymes / Probiotics / Synbiotics |

| Electrolytes & Minerals |

| Herbal / Botanical / Nutraceutical |

| Powders |

| Liquids |

| Pellets & Granules |

| Pastes & Gels |

| Chewables / Treats |

| Veterinary Hospitals & Clinics |

| Pharmacies & Drug Stores |

| Equine Specialty & Tack Stores |

| Feed & Farm Supply Stores |

| Online Retail (Marketplaces & D2C) |

| Supermarkets & Hypermarkets |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Health Benefit / Application | Joint & Bone Health | |

| Digestive / Gut Health | ||

| Hoof & Laminitis Support | ||

| Vitamins & Minerals (General Health & Immunity) | ||

| Skin & Coat | ||

| Calming & Nervous System | ||

| Respiratory & Immune Support | ||

| Performance & Energy / Recovery | ||

| Senior / Metabolic Support | ||

| By Ingredient Type | Proteins & Amino Acids | |

| Vitamins | ||

| Enzymes / Probiotics / Synbiotics | ||

| Electrolytes & Minerals | ||

| Herbal / Botanical / Nutraceutical | ||

| By Form | Powders | |

| Liquids | ||

| Pellets & Granules | ||

| Pastes & Gels | ||

| Chewables / Treats | ||

| By Distribution Channel | Veterinary Hospitals & Clinics | |

| Pharmacies & Drug Stores | ||

| Equine Specialty & Tack Stores | ||

| Feed & Farm Supply Stores | ||

| Online Retail (Marketplaces & D2C) | ||

| Supermarkets & Hypermarkets | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the equine supplement products market?

The equine supplement products market size is projected at USD 90.49 million in 2025, moving to USD 91.88 million in 2026, and reaching USD 104.42 million by 2031 at a 2.59% CAGR from 2026 to 2031.

Which applications lead demand and which are growing fastest?

Joint & Bone Health led with 34.56% in 2025, and Hoof & Laminitis Support is the fastest-growing with a 4.51% CAGR through 2031.

Which regions contribute the most and where is growth strongest?

North America held 42.67% in 2025, while Asia-Pacific is expected to grow fastest with a 5.01% CAGR through 2031.

What channels are most important for purchasing equine supplements?

Veterinary Hospitals & Clinics led with 33.67% in 2025, and Online Retail is the fastest-growing channel at a 4.96% CAGR due to subscription and D2C models.

Which ingredient categories are most prominent in equine supplements?

Proteins & Amino Acids led at 41.24% in 2025, while Herbal, Botanical, and Nutraceutical ingredients are projected to grow at a 4.14% CAGR over 2026-2031.

What forms are most used, and which are increasing fastest?

Powders held 36.78% in 2025 for daily foundational feeding, and Liquids are growing fastest at a 4.65% CAGR due to dosing ease and palatability.

Page last updated on: