Epidermolysis Bullosa Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

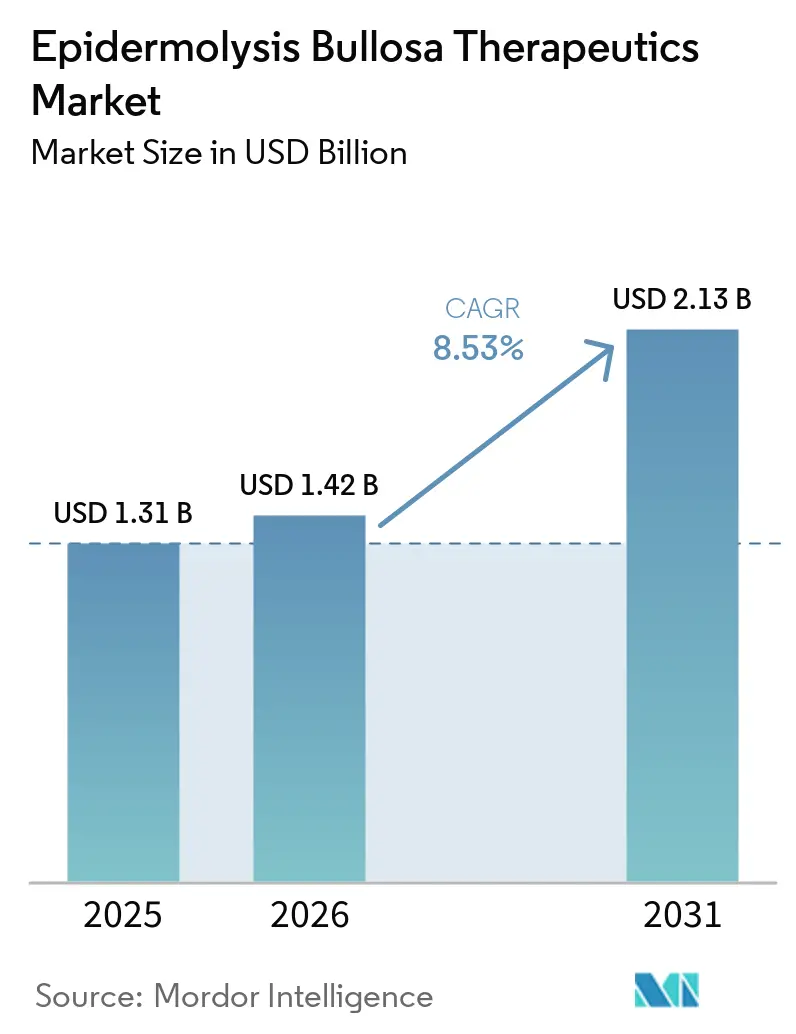

| Market Size (2026) | USD 1.42 Billion |

| Market Size (2031) | USD 2.13 Billion |

| Growth Rate (2026 - 2031) | 8.53% CAGR |

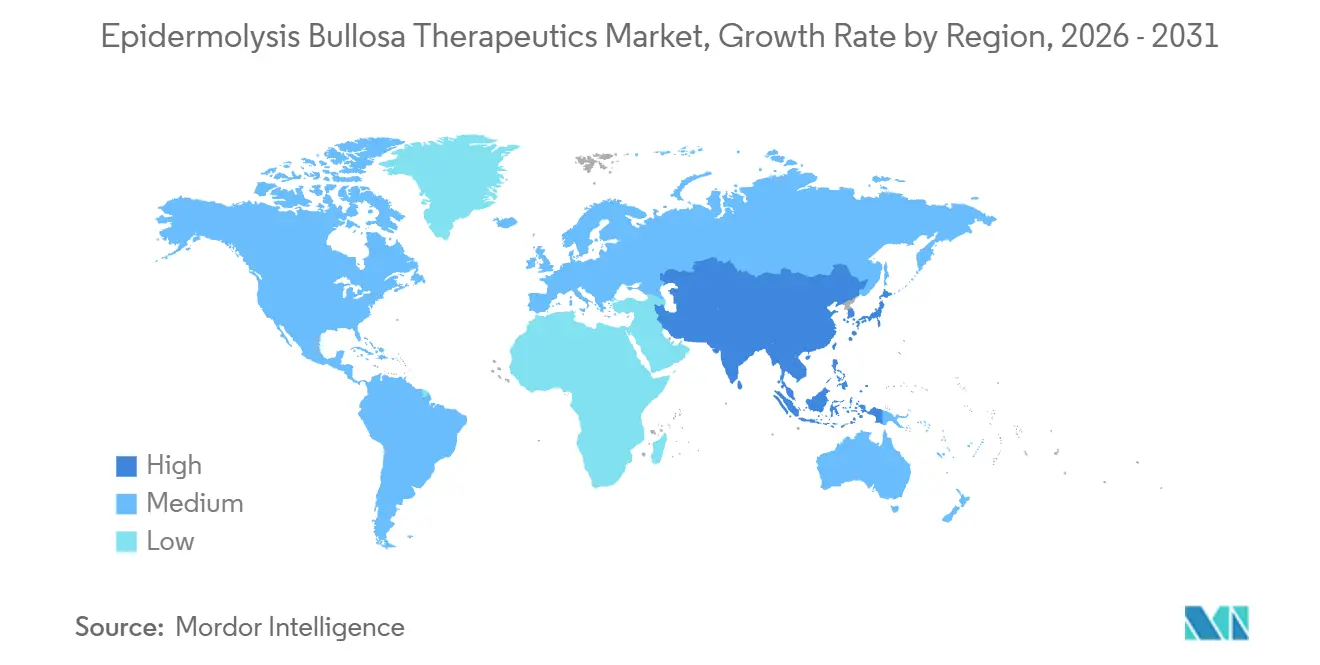

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Epidermolysis Bullosa Therapeutics Market Analysis by Mordor Intelligence

The Epidermolysis Bullosa Therapeutics Market size is projected to be USD 1.31 billion in 2025, USD 1.42 billion in 2026, and reach USD 2.13 billion by 2031, growing at a CAGR of 8.53% from 2026 to 2031.

Rapid regulatory progress for gene and cell therapies in 2024 and 2025 shifted care from symptomatic wound management toward disease-modifying strategies, which is raising expectations for sustained uptake across high-acuity patient cohorts. Orphan-drug incentives, including seven-year exclusivity and Priority Review Vouchers, continue to underpin commercial viability for ultra-rare dermatologic genetics and support premium pricing within payer programs that prioritize reductions in caregiver burden and hospitalizations. Treatment delivery is decentralizing as label updates and remote monitoring expand at-home use for selected therapies, which supports the fastest growth in home-based care over the forecast horizon. Competitive dynamics are intensifying around durability claims and dose frequency, with manufacturers positioning one-time grafts against chronic redosing in response to payer demand for multi-year outcome evidence. Regional outlooks diverge as North America sustains the largest revenue base while Asia Pacific accelerates following Japan’s 2025 launch window, which catalyzes broader diagnostic adoption and access planning across the region.

Key Report Takeaways

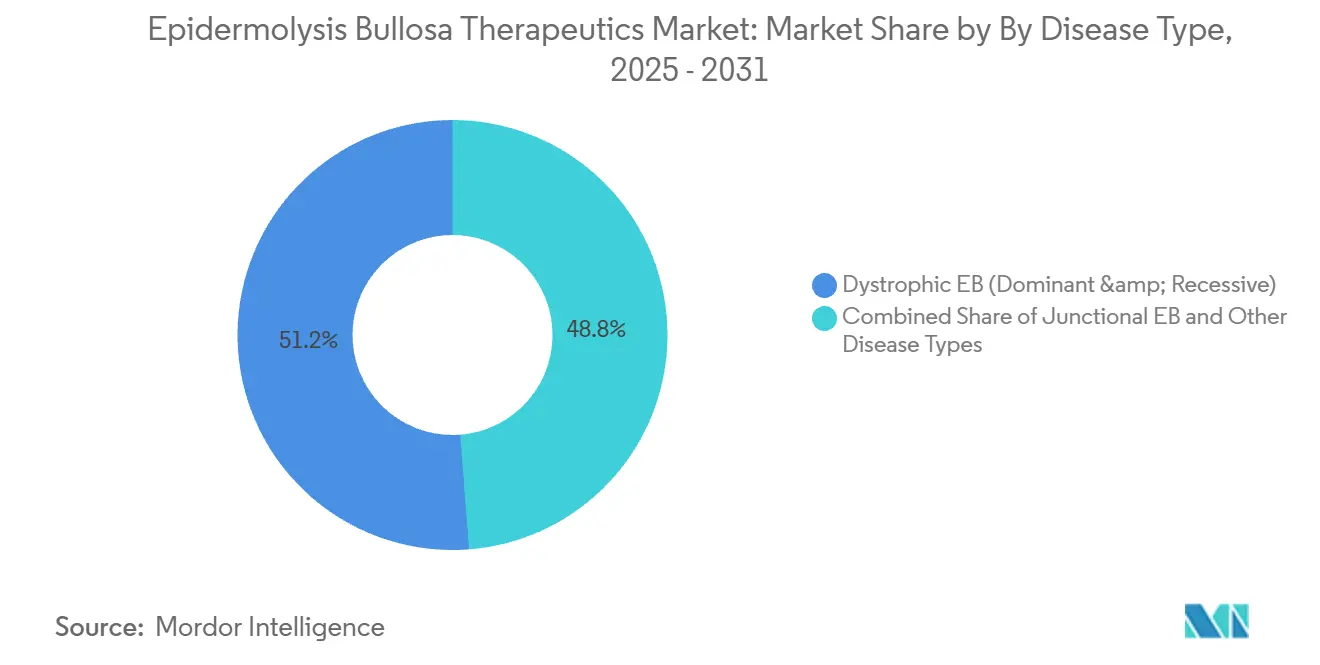

By disease type, Dystrophic EB led with 51.23% revenue share in 2025, while Kindler Syndrome is projected to expand at an 8.91% CAGR through 2031.

By therapeutic modality, Small-Molecule and Topical Agents held 40.92% revenue share in 2025, and Gene Therapy is forecast to grow at a 9.32% CAGR to 2031.

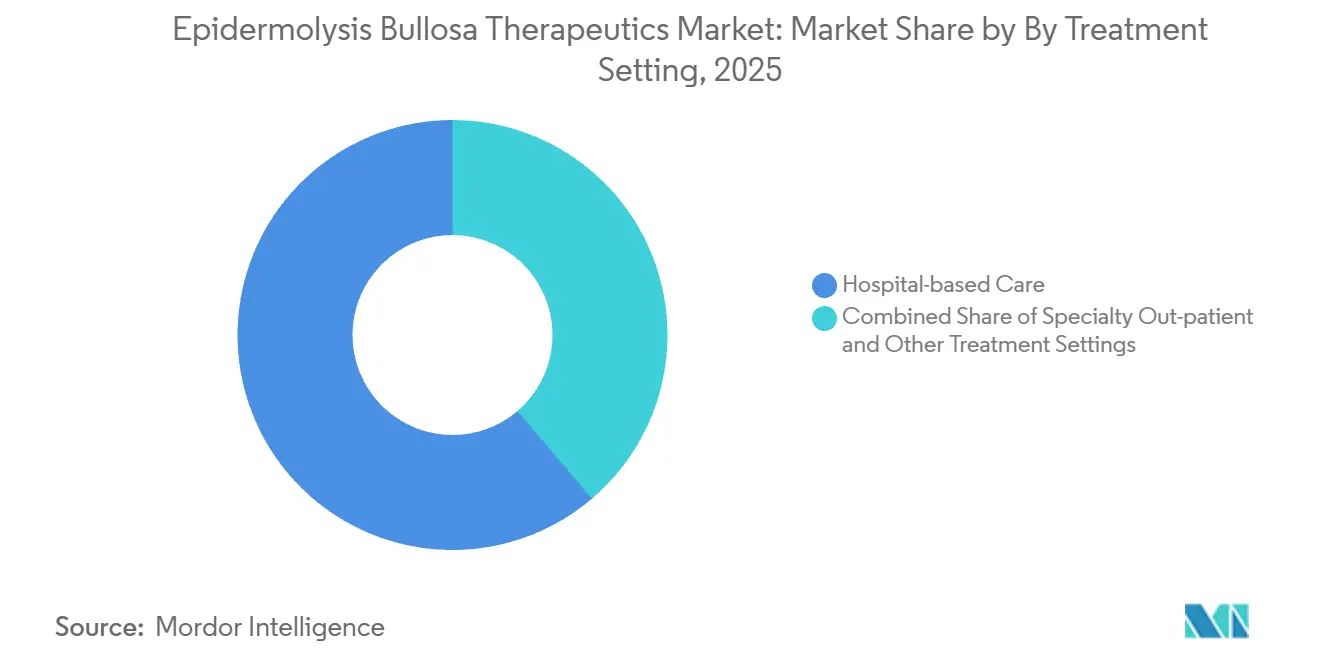

By treatment setting, Hospital-based Care accounted for 61.23% in 2025, while Home-based Care recorded the highest projected CAGR at 9.52% through 2031.

By age group, Pediatric patients commanded 65.47% revenue share in 2025, while the Adult cohort is advancing at a 9.10% CAGR through 2031.

By geography, North America held 45.18% of global revenue in 2025, and the Asia Pacific is the fastest-expanding region at 4.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Epidermolysis Bullosa Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FDA Approval Of VYJUVEK Gene Therapy | +1.8% | Global, with early gains in US, Germany, France, Japan | Medium term (2-4 years) |

| Orphan-Drug Incentives Expanding Commercialization Runway | +1.2% | North America & EU | Long term (≥ 4 years) |

| Increasing Diagnostic Rates Through Genomic Testing | +0.9% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Growing Pipeline Of Gene & Cell Therapies | +1.5% | Global | Long term (≥ 4 years) |

| Tele-Dermatology Platforms For Remote Wound Monitoring | +0.6% | National, with early gains in EU, India | Short term (≤ 2 years) |

| CRISPR-Enabled Ex-Vivo Autografts Nearing Clinical Use | +2.5% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

FDA approval of VYJUVEK gene therapy

Label expansion in September 2025[1]U.S. Food and Drug Administration, “Orphan Drug Designations and Approvalsallowed VYJUVEK use from birth and permitted at-home administration by patients or caregivers under healthcare provider oversight, which widened the eligible population and reduced clinic visit frequency for qualified families Caregiver time in severe dystrophic EB is a significant friction point and has historically reached high weekly hour commitments, so enabling at-home application supports the shift toward home-based care and aligns with payer preferences that favor reduced caregiver burden. VYJUVEK demonstrated strong commercial traction in 2025, with reported quarterly revenue of USD 97.8 million and more than 615 U.S. reimbursement approvals by Q3 2025 as international launches progressed in Germany, France, and Japan. France’s Haute Autorité de Santé assigned an ASMR III designation in October 2025, which validates the therapy’s clinical contribution while channeling access through early-reimbursement programs that balance speed and fiscal discipline. Germany’s benefit assessment and pricing process under AMNOG continued into late 2026, emphasizing evidence standards and patient-relevant outcomes that shape final price negotiations. Japan’s October 2025 launch followed a cost-effectiveness premium approach under national health insurance, providing a framework that supports access while preserving robust manufacturer margins.

Orphan-drug incentives expanding commercialization runway

U.S. orphan-drug policy and the Rare Pediatric Disease pathway continue to anchor investment flows into ultra-rare dermatology and enable multiple value streams, including transferable Priority Review Vouchers that can be sold to extend operating runways or offset capital needs. Sponsors reported monetization outcomes that funded commercialization readiness and next-wave clinical work, reinforcing the financial logic behind first-mover strategies in indications with very small addressable patient pools . Seven-year market exclusivity limits direct price competition in the initial launch window, which creates predictable revenue curves and encourages evidence investments that support label expansion and line extensions. EMA orphan designation confers fee reductions and scientific advice that may compress development timelines, increasing the appeal of EU engagement for EB programs with clear genetic mechanisms. The UK’s Early Access to Medicines Scheme provides managed access for promising therapies before full licensing, which can accelerate real-world data accrual relevant for later pricing rounds and broader rollouts. U.S. tax credits under Internal Revenue Code Section 45C enable sponsors to claim a portion of qualified clinical testing expenses, an incentive that supports late-stage study execution and regulatory preparation for orphan therapies.

Increasing diagnostic rates through genomic testing

Whole-genome sequencing and broad multi-gene panels are increasing diagnostic yields by capturing deep intronic variants that exome-only tests can miss, which is improving patient stratification for targeted therapies across EB subtypes. A February 2025 study resolved 100% of six previously unsolved Junctional EB cases through whole-genome sequencing, including detection of deep intronic COL7A1 and LAMB3 variants that would not be identified with narrow assays. Minigene assays in keratinocyte-relevant cell systems validated the pathogenicity of such variants, underscoring the need for tissue-appropriate functional models when interpreting non-coding changes that affect splicing. Prenatal and perinatal genetic testing access has been expanded through national health systems such as NHS England, enabling earlier, more precise counseling and pathway planning for families with known carrier status. Tele-dermatology in India integrated genomic referrals within pediatric dermatology consults, showing that most initial evaluations can be triaged remotely while channeling complex cases to in-person genetic confirmation. Commercial clinical-grade EB panels reported high sensitivity and expanded coverage of known non-coding variants, and order volumes rose as clinicians adopted comprehensive panels to inform therapy selection and eligibility.

Growing pipeline of gene & cell therapies

Late-stage programs widened the option set in 2025 and 2026, with sponsors advancing gene-modified autologous cell therapies and redosable gene delivery approaches that offer distinct trade-offs among frequency, durability, setting of care, and price. One program is designed for periodic intradermal dosing to complement a topical redosing gene therapy on one side and a one-time autologous graft on the other, a positioning that may suit payers seeking middle-ground budget predictability over multi-year horizons. Systemic mesenchymal stromal cell platforms advanced toward key filings with a pediatric focus, aligning mechanism and administration with high-burden patient populations where unmet needs and utilization costs are most acute. Gene-editing research in EB reached high allele-deletion efficiencies for targeted COL7A1 exons in preclinical human cells, with restored type VII collagen in engineered skin constructs reported in peer-reviewed work, expanding future possibilities for precision correction. While gene editing is not yet in human EB trials as of 2026, the breadth of correctable exons and platform generalizability support strong academic and translational interest in next-generation modalities that could complement current viral vector and autologous approaches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Therapy Cost & Reimbursement Hurdles | -2.1% | Global | Medium term (2-4 years) |

| Limited Patient Pool Complicates Clinical Trials | -1.3% | Global | Long term (≥ 4 years) |

| Regulatory Complexity For Advanced Biologics | -0.8% | Global, with acute challenges in APAC | Medium term (2-4 years) |

| Viral-Vector Manufacturing Capacity Constraints | -1.7% | Global, with production concentrated in North America, EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High therapy cost & reimbursement hurdles

One-time autologous cell-based gene therapies launched with list prices in the multi-million-dollar range, which concentrates payer scrutiny on durability, re-treatment risk, and outcomes-based safeguards that share financial risk over time. Redosing gene therapies priced per vial with annualized dosing plans shift budget impact from a single upfront payment to recurring annual expense, and sponsors have disclosed per-vial pricing and annual caps designed to fit payer budget models for rare diseases. Patient-assistance and warranty constructs have been communicated to address reimbursement barriers and align manufacturer economics with clinical outcomes, though actuarial models still require maturing real-world evidence for long-horizon projections. Baseline care costs for severe RDEB in national health systems[2]Camilla’s Wings Foundation, “Caregiver Burden and Cost of Care in RDEB,” Camilla’s Wings, camillaswings.org such as the UK have been high, including sustained caregiver time and wound supplies, which informs cost-effectiveness judgments for newly approved therapies. Payer frameworks continue to evolve, and U.S. Medicaid pilot models for cell and gene therapies provide a template for milestone-linked rebates and access agreements, even as disease-specific inclusion varies across programs. The combined effect is that price, real-world durability, and measurable reductions in hospitalizations and caregiver time remain pivotal in reimbursement decisions and therapy selection.

Limited patient pool complicates clinical trials

Very small eligible populations at each subtype and genotype level complicate enrollment and prolong timelines to pivotal data, which has pushed sponsors to adopt efficient trial designs and use patients as their own controls where suitable. Pivotal programs in EB have proceeded with low double-digit enrollment while maintaining rigorous wound-level randomization and endpoint definitions that regulators accept for ultra-rare conditions. Geographic dispersion adds operational burden for monthly follow-up and specialized procedures, so qualified centers often cluster in major metropolitan areas, creating travel constraints for families in distant regions. Genotype heterogeneity and exon-level variation add another layer of trial design complexity, as mutation-specific eligibility criteria can further narrow recruitment pools for targeted mechanisms. Regulators have shown flexibility by accepting external natural-history comparators and innovative statistical approaches where appropriate, which helps maintain evidentiary rigor while accommodating the realities of ultra-rare disease trials. These adaptations are essential to sustain the pace of innovation for the Epidermolysis bullosa therapeutics market while meeting safety and efficacy standards that protect patients and caregivers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Type: Dystrophic EB Dominates as Kindler Syndrome Accelerates

Dystrophic EB accounted for 51.23% of 2025 revenue, reflecting higher clinical need and the availability of approved therapies that target COL7A1-confirmed patients within the Epidermolysis bullosa therapeutics market. Junctional EB began to see expanded clinical attention following U.S. approval of a topical therapy that addresses wounds in JEB, which broadened eligible patient access for subtypes with severe early-life manifestations. Epidermolysis bullosa simplex remains the most common form, yet is less penetrated by genetic-correction modalities, which is why wound care and symptomatic management still represent a noteworthy share of care pathways. Kindler Syndrome is a smaller share in 2025 but registers the fastest growth at an 8.91% CAGR through 2031 as FERMT1 gene panel adoption rises in neonatal screening programs across parts of Europe. Labeling for gene therapies ties use to confirmatory genetic testing, which elevates the role of comprehensive genomic diagnostics in earlier life stages and determines eligibility for disease-modifying care.

The therapeutic footprint within Dystrophic EB now spans topical redosing and one-time autologous graft options, giving clinicians flexibility to match mechanism, site-of-wound, and logistics with patient-specific needs in the Epidermolysis bullosa therapeutics market. Confirmed COL7A1 mutations anchor clinical decision-making for these modalities, and continued evidence development is expected to clarify optimal sequences between redosing regimens and surgical autografts. Ongoing surveillance of squamous cell carcinoma risk and chronic infection burden in severe cases influences therapy selection, dosing windows, and supportive care planning for long-term patient safety. As more real-world data accumulates, payers and providers will refine criteria that weigh durability, retreatment probability, and caregiver time alongside wound-closure outcomes, further shaping the Epidermolysis bullosa therapeutics market.

By Therapeutic Modality: Gene Therapy Disrupts Small-Molecule Hegemony

Small-Molecule and Topical Agents held 40.92% of 2025 revenue, supported by broad label coverage across key subtypes and a strong fit with outpatient and home-based settings in the Epidermolysis bullosa therapeutics market. Longitudinal publications reported sustained reductions in wound burden for approved topical agents with consistent use, and national bodies recognized the clinical benefit in health-economic decisions during 2024 and 2025. Gene Therapy is the fastest-growing modality with a 9.32% CAGR through 2031, underpinned by rising adoption of redosable topical gene delivery and initiation of one-time autologous grafts in qualified treatment centers. Platform expansions to ocular and other site-specific indications could broaden the eligible population further as development and regulatory efficiencies are realized. Program-specific safety monitoring and supply planning will continue to define launch pacing as centers gain operational experience with multi-modality workflows.

Cell-based approaches, including autologous grafts and systemically administered cell therapies, form a complementary tier within the Epidermolysis bullosa therapeutics market, with usage concentrated in high-acuity settings that can support complex handling and post-procedure monitoring. As pivotal data matures, payers will have additional anchors to compare long-term durability against recurring topical gene dosing and to evaluate total cost of care under each approach. Protein replacement concepts remain under evaluation and face adherence and pharmacokinetic hurdles that may narrow the target population relative to gene and cell therapies. Hybrid and site-optimized vectors are emerging to serve sub-populations where systemic exposure is insufficient or where local delivery can better match the disease biology and care setting. These dynamics point to a realignment in modality shares over time as evidence deepens and logistics evolve in the Epidermolysis bullosa therapeutics market.

By Treatment Setting: Home-based Care Gains as Caregiver Economics Shift

Hospital-based Care captured 61.23% of 2025 revenue and remained the locus for one-time autologous grafts and first-dose administrations that require intensive monitoring in the Epidermolysis bullosa therapeutics market. Specialty Outpatient centers expanded their role in topical gene therapy dosing and follow-up care as more payers approved coverage and more sites gained operational experience with cryostorage and procedural workflows. Home-based Care posted the fastest growth at a 9.52% CAGR through 2031 as labels permitted patient or caregiver application under defined oversight, which reduced in-person clinic visits and aligned with caregiver burden reduction objectives. Early-adopter countries coupled digital wound monitoring with decentralized dosing to control safety risks while capturing real-world outcomes that supported subsequent pricing rounds. These shifts reflect a wider system preference to move eligible care closer to home without sacrificing monitoring fidelity or safety.

As outpatient and home-based pathways scale, initial-dose supervision and structured training remain essential to minimize adverse events and ensure dosing competence in the Epidermolysis bullosa therapeutics market. Labels distinguish between initial and subsequent dosing rules, and patient support programs help families navigate coordination and documentation with payer and provider teams. In systems such as the UK NHS, shifting qualified patients from hospital-coordinated dressing changes to home-based care with tele-dermatology oversight delivered meaningful savings and informed national recommendations for newly approved therapies. Autologous grafts will remain concentrated in hospitals due to surgical requirements and post-procedure observation windows, reinforcing a two-speed setting dynamic between one-time and redosing modalities. Over 2026 to 2031 the balance of episodes is expected to continue trending toward community and home settings as decentralized protocols and remote assessment tools expand.

By Age Group: Pediatric Predominance Meets Adult Opportunity

Pediatrics represented 65.47% of 2025 revenue, driven by disease onset patterns, intensive caregiver involvement, and a regulatory environment that prioritizes pediatric endpoints and Rare Pediatric Disease incentives in the Epidermolysis bullosa therapeutics market. PRV-linked designations and orphan status have concentrated sponsor focus on children with severe forms of dystrophic and junctional EB, where potential gains in wound closure and infection reduction are largest in budget impact models. Adults are set to grow at a 9.10% CAGR through 2031 as clinical programs demonstrate comparable wound-healing benefits across age groups and as adult-focused access frameworks mature. The cumulative lifetime risk of squamous cell carcinoma in severe recessive dystrophic EB underscores the importance of accelerated wound closure and surveillance in adult care, shaping therapy selection and follow-up. Earlier genetic confirmation supports treatment initiation in neonatal and infant windows where labels allow, reinforcing pediatric shared leadership.

Dosing strategies and vial counts for topical gene therapies scale with wound surface area rather than weight, which guides pediatric planning differently than traditional systemic dosing rules and informs clinician-patient counseling at initiation. Caregiver time commitments have been central to access decisions in several markets, given the documented challenges of frequent dressing changes and the employment impact on families. Adult uptake should also benefit from improved care coordination and the growth of specialized centers capable of supporting autologous grafts and outpatient redosing regimens with consistent monitoring. As longitudinal data accumulates across age cohorts, payers will refine age-specific coverage criteria and measure reductions in infection-related hospitalizations and emergency interventions alongside wound healing. These dynamics collectively sustain the leadership of pediatrics while unlocking an adult opportunity that increases total eligible volumes in the Epidermolysis bullosa therapeutics market.

Geography Analysis

North America maintained 45.18% of global revenue in 2025, supported by early adoption of approved gene and cell therapies and a growing installed base of specialty centers capable of advanced EB care in the Epidermolysis bullosa therapeutics market. The U.S. recorded hundreds of payer approvals within the first two years of gene therapy launch, reflecting the strength of coverage policies that reward demonstrated wound-closure benefits and reduced hospitalization risk. Canadian access moved through province-by-province evaluation and negotiation, which tends to stagger uptake timelines but can still deliver broad access once national and provincial bodies align. Mexico progressed through early planning stages for specialty distribution and site enablement as sponsors expanded networks for 2026, representing a potential medium-term expansion node in North America. In Europe, France’s ASMR III appraisal in 2025 enabled inclusion in early reimbursement channels that speed access while price setting continues, balancing the urgency of severe wound care with stewardship imperatives. Germany’s AMNOG process maintained rigorous comparative benefit assessments through 2026, which will set precedents for subsequent genetic-dermatology evaluations and influence negotiated price bands[3]Federal Joint Committee G-BA, “AMNOG Assessments and Price Negotiations. Italy prepared for a 2026 launch window aligned with regional processes, highlighting how decentralized structures can add several months to timing compared to centralized systems. The UK, which issued positive guidance in early 2024 for a topical therapy covering dystrophic and junctional EB, grounded its decision in demonstrable wound-burden reductions and credible budget impact evidence.

Asia Pacific is the fastest-growing region at a 4.67% CAGR through 2031, catalyzed by Japan’s October 2025 gene therapy launch and supportive reimbursement frameworks designed for severely debilitating conditions in the Epidermolysis bullosa therapeutics market. Japan’s cost-effectiveness premium framework under national insurance enabled timely market entry, with manufacturer communications indicating pricing sufficient to sustain strong margins as site onboarding progressed. China’s diagnostics ramp in tier-1 hospitals identified deep intronic mutations through whole-genome sequencing that older panels could not detect, which enlarged the diagnosed prevalence pool and will be important to future access planning. India advanced a national telemedicine infrastructure with integrated genomic referrals that proved scalable for pediatric dermatology, which provides a platform for decentralized follow-up when therapies require periodic monitoring. Australia’s regulatory pathways allow for provisional approvals referencing European dossiers, which can shorten timelines for EB therapies that are already authorized in the EU. South Korea’s recognition agreements support efficient review of therapies with EU approval histories, reinforcing regional alignment on evidence standards for ultra-rare conditions.

Competitive Landscape

Three approved therapies concentrated most revenue in 2025 and early 2026, with a topical redosing gene therapy, a one-time autologous graft, and a topical agent each addressing distinct clinical and economic use cases in the Epidermolysis bullosa therapeutics market. Manufacturers differentiated on dose frequency versus durability, enabling payers to consider either recurring spend models tied to wound closure trajectories or upfront capital models backed by long-horizon follow-up data. Sponsors also invested in platform strategies, including vector platforms that can be leveraged across additional indications such as ocular manifestations, aiming to reduce development friction and accelerate evidence generation. Vertical integration in manufacturing emerged as a competitive advantage, reducing dependence on constrained external capacity and improving control over release testing and scale-up. Pricing and access strategies included patient-assistance constructs, early-launch distributor agreements, and targeted site activation across North America, Europe, and Japan. These choices positioned incumbents to defend their share while late-stage entrants prepare to broaden the competitive field after 2026.

Strategic moves during 2025 and 2026 included European and Japanese launches by a leading topical gene therapy sponsor following EU authorization in 2025, which signaled readiness for ex-U.S. expansion and deepened payer engagement around early clinical outcomes and label extensions. The first commercial treatment with an autologous cell-based gene therapy outside trial settings occurred in December 2025, marking a key step from pivotal data to routine advanced care at qualified centers. Financing transactions funded Phase 3 development for a competing autologous fibroblast program in 2025, indicating investor confidence in additional gene-modified cell options that could serve different patient profiles or care settings. In parallel, companies pursuing systemic cell-based approaches with pediatric targets outlined plans for near-term filings, setting the stage for broader modality diversity by 2027. Together, these developments reinforce a bifurcated competitive structure in the Epidermolysis bullosa therapeutics market as chronic redosing and one-time procedures vie for therapy selection on evidence strength, logistics, and cost.

Competitive boundaries also sharpened around scope, with several wound-care device and dressing suppliers playing supportive roles rather than offering disease-modifying therapies, which distinguishes the market’s core players from adjacent suppliers of consumables. Academic centers remain important sources of next-generation approaches, including gene-editing concepts that could be licensed or spun out as clinical-stage programs in the next wave. Regulatory expertise and quality systems have become moats in autologous manufacturing, where experience resolving CMC and postmarketing requirements signals organizational depth that newcomers will need to build or acquire. The combination of IP estates for vector platforms and ex-vivo correction adds further barriers that set timeframes for realistic competitive entry. As additional indications such as ocular involvement mature under platform designations, first movers could compound their lead, provided they convert process learning into faster approvals and new segment entry points in the Epidermolysis bullosa therapeutics market.

Epidermolysis Bullosa Therapeutics Industry Leaders

Krystal Biotech, Inc.

Abeona Therapeutics Inc.

Chiesi Group

Castle Creek Biosciences

Smith & Nephew plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Krystal Biotech reported full-year 2025 financial results, with VYJUVEK generating USD 389.1 million in revenue, 34% year-over-year growth, and net income reaching USD 204.8 million. The company maintained 94% gross margins and ended 2025 with USD 955.9 million in cash reserves. Krystal announced plans to launch VYJUVEK in at least one additional major European market and expand its specialty distributor network to over 40 countries by end-2026.

- February 2026: Krystal Biotech executed a commercialization agreement with a regional specialty distributor for VYJUVEK in Israel, part of a broader Middle East and North Africa market-entry strategy targeting 15-20 countries.

- December 2025: Abeona Therapeutics announced the first commercial patient treatment with ZEVASKYN gene therapy at Lucile Packard Children's Hospital Stanford, marking a significant milestone as the therapy entered broader clinical use beyond trial settings.

- December 2025: VYJUVEK received the Prix Galien France award in the Innovative Therapy Medicines category, recognizing the therapy's clinical innovation and impact on patient outcomes. This followed the Prix Galien Italia award in the Advanced Therapy Medicinal Products category received earlier in 2025.

Global Epidermolysis Bullosa Therapeutics Market Report Scope

| Epidermolysis Bullosa Simplex (EBS) |

| Dystrophic EB (Dominant & Recessive) |

| Junctional EB |

| Kindler Syndrome |

| Gene Therapy |

| Cell-based Therapy |

| Protein Replacement |

| Small-Molecule / Topical Agents |

| Hospital-based Care |

| Specialty Out-patient |

| Home-based Care |

| Pediatric (less than17 yrs) |

| Adult (over 18 yrs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disease Type | Epidermolysis Bullosa Simplex (EBS) | |

| Dystrophic EB (Dominant & Recessive) | ||

| Junctional EB | ||

| Kindler Syndrome | ||

| By Therapeutic Modality | Gene Therapy | |

| Cell-based Therapy | ||

| Protein Replacement | ||

| Small-Molecule / Topical Agents | ||

| By Treatment Setting | Hospital-based Care | |

| Specialty Out-patient | ||

| Home-based Care | ||

| By Age Group | Pediatric (less than17 yrs) | |

| Adult (over 18 yrs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

Which care setting is growing the fastest for EB therapies

Home-based Care is the fastest-growing setting with a 9.52% CAGR through 2031 as labels permit at-home application under supervision and as tele-dermatology tools standardize remote wound monitoring.

Which region leads current EB therapy revenues and which region is growing the fastest

North America led with 45.18% of 2025 revenue, while Asia Pacific is the fastest-growing region at a 4.67% CAGR to 2031 following Japans 2025 gene therapy launch.

How are payers evaluating one-time grafts versus redosing gene therapies in EB

Payers focus on multi-year durability, risk-sharing constructs, and reductions in hospitalizations and caregiver time, comparing one-time autologous grafts against chronic redosing models to balance upfront expenditure and ongoing budgets.

What role does genomic testing play in therapy eligibility for EB

Comprehensive genomic testing confirms subtype and mutation status including deep intronic variants, which determines eligibility for gene therapies and informs prenatal and neonatal planning where labels permit from-birth use.

Which disease subtype currently leads revenues in the EB arena

Dystrophic EB leads with 51.23% of 2025 revenue due to higher clinical need, available approved therapies, and increased use tied to COL7A1 genetic confirmation in the Epidermolysis bullosa therapeutics market.

Page last updated on: