Enterprise Service Management Store Apps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

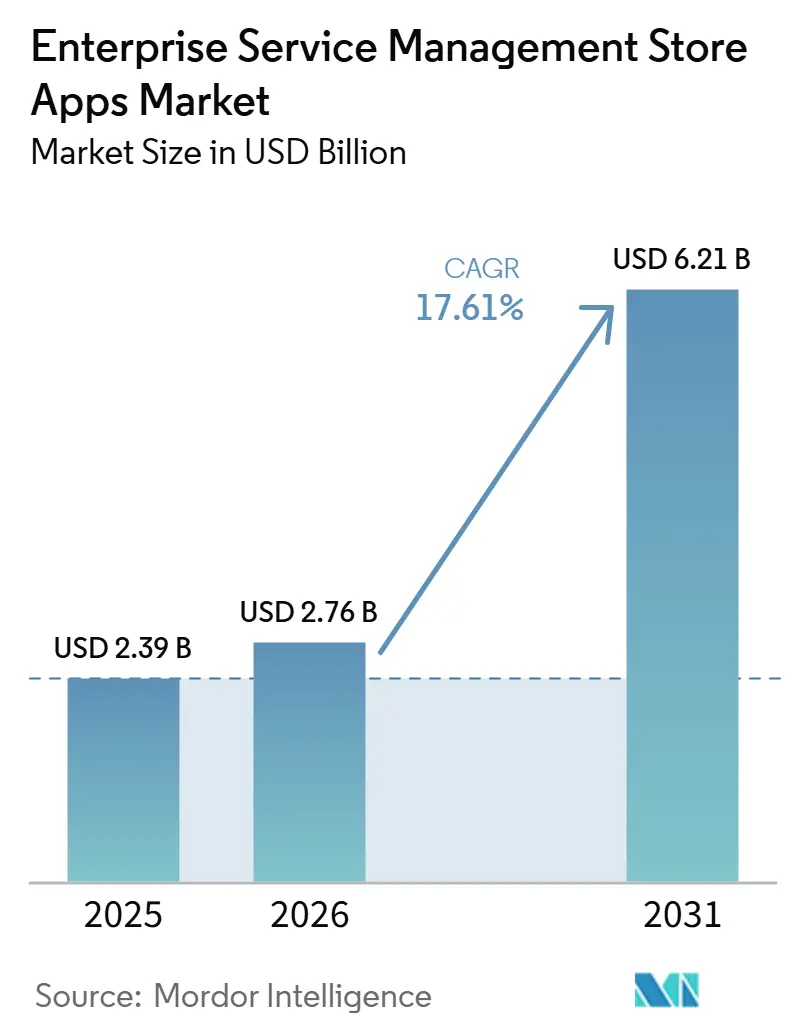

| Market Size (2026) | USD 2.76 Billion |

| Market Size (2031) | USD 6.21 Billion |

| Growth Rate (2026 - 2031) | 17.61% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

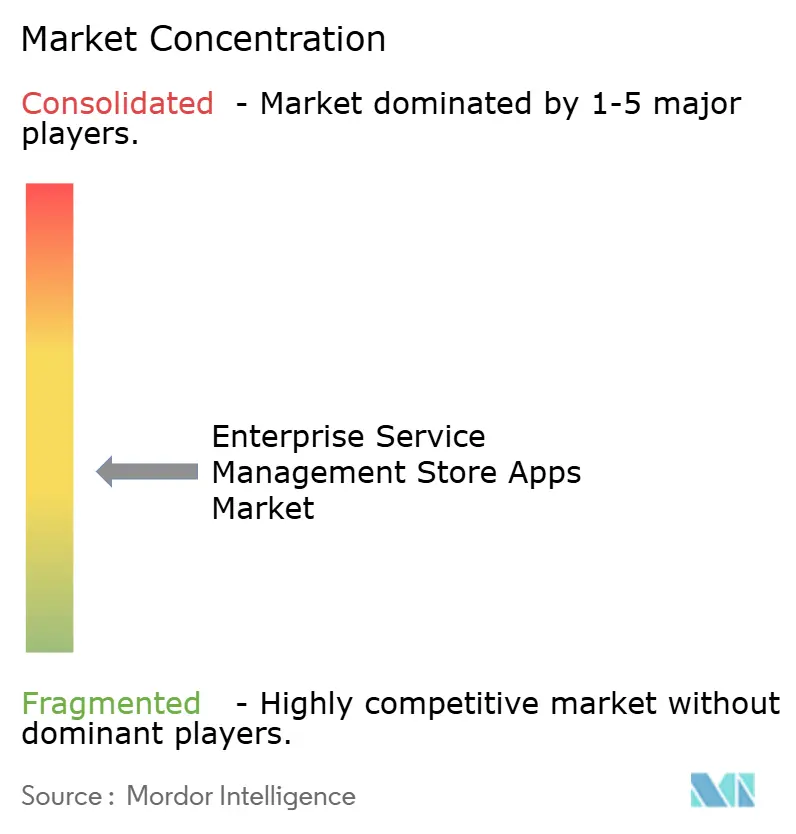

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Service Management Store Apps Market Analysis by Mordor Intelligence

The Enterprise Service Management Store Apps Market size is projected to be USD 2.39 billion in 2025, USD 2.76 billion in 2026, and reach USD 6.21 billion by 2031, growing at a CAGR of 17.61% from 2026 to 2031. The 2026 base already reflects a faster adoption cycle, as buyers move away from stand-alone software licenses toward certified marketplace extensions that can be added to a broader workflow stack with less implementation friction. Demand is also being shaped by the shift toward unified AI-enabled operating environments, where buyers want one platform to coordinate service delivery, automation, and governance across multiple business functions. Low-code and no-code tools are widening the buyer base by allowing nontechnical teams to adopt prebuilt extensions without funding large custom development programs. Certified marketplace apps are also benefiting from stronger compliance expectations, as buyers increasingly prefer governed, auditable extensions over custom builds that are harder to validate and maintain. Competition remains active at the module level even as platform control remains concentrated, leaving room for growth in security, identity, and cross-functional workflow extensions that address urgent operational gaps.

Key Report Takeaways

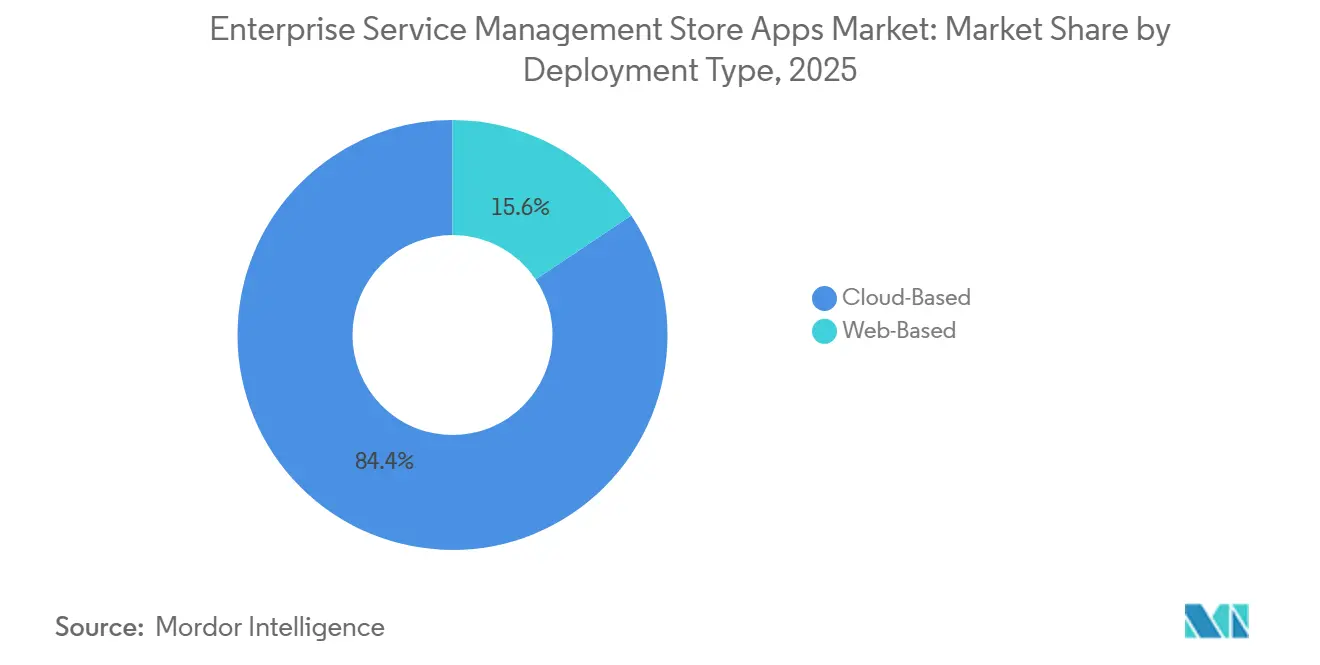

- By deployment type, cloud-based apps accounted for 84.37% of the enterprise service management store apps market size in 2025, and are projected to expand at a 18.64% CAGR through 2031.

- By enterprise size, large enterprises held 71.84% of the enterprise service management store apps market share in 2025, while small and medium enterprises are projected to grow at a CAGR at 19.88% through 2031.

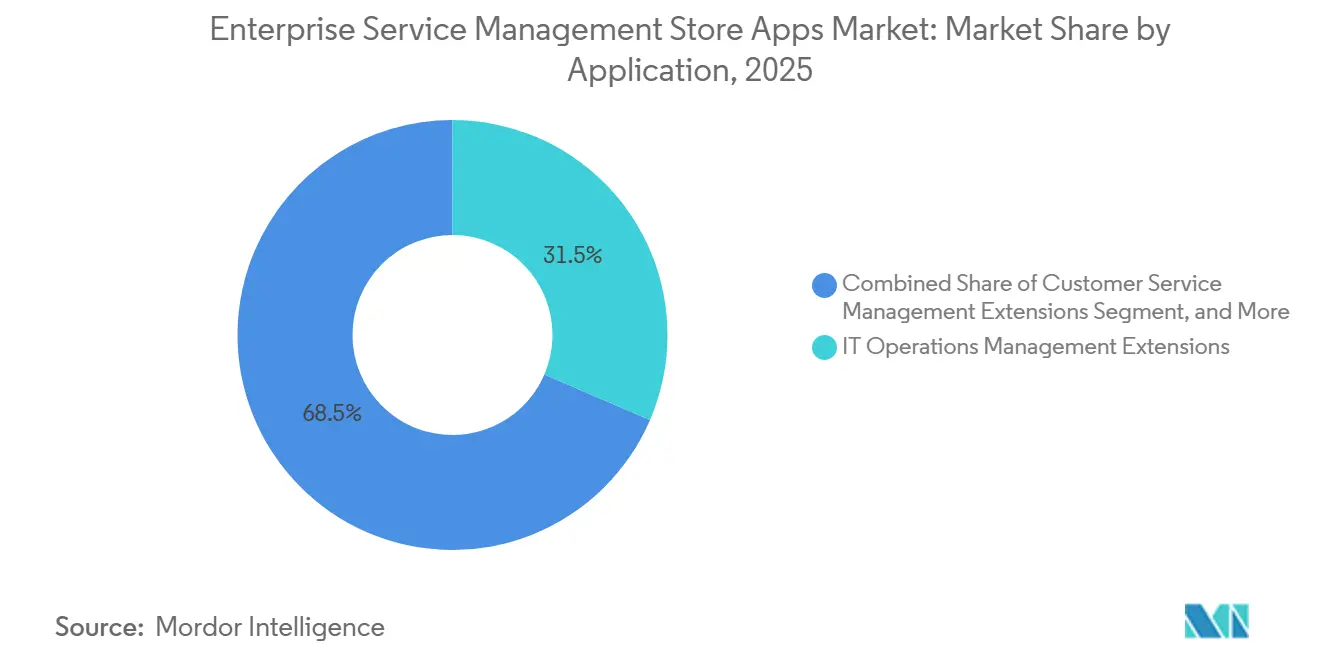

- By application, IT operations management accounted for 31.46% of the enterprise service management store apps market size in 2025, while security operations and identity are projected to advance at a 20.82% CAGR through 2031.

- By geography, North America held 41.28% of the enterprise service management store apps market share in 2025, while Asia-Pacific is projected to expand at a 20.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Enterprise Service Management Store Apps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased Adoption of Cloud-First Enterprise Workflow Ecosystems | +4.5% | Global | Short term (≤ 2 years) |

| AI-Assisted Workflow Automation in Enterprise Service Management | +3.8% | Global | Medium term (2-4 years) |

| Rapid Expansion of Cross-Functional Service Orchestration | +2.9% | North America and Europe | Medium term (2-4 years) |

| Rising Demand for Low-Code and No-Code Store Apps | +2.1% | Global, with high concentration in APAC and North America | Short term (≤ 2 years) |

| Growing Preference for Certified Marketplace Extensions Over Custom Builds | +1.4% | North America and Europe | Medium term (2-4 years) |

| Compliance-Driven Demand for Governed App Distribution | +0.9% | North America, Europe, and APAC core | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased Adoption of Cloud-First Enterprise Workflow Ecosystems

Cloud-first operating models are turning the enterprise service management store apps market into a core distribution layer rather than an optional add-on environment. When enterprises standardize on cloud-native service platforms, they often adopt the platform marketplace as the default route for deploying new workflow features, thereby elevating the role of store apps in day-to-day operations. ServiceNow reported USD 3,466 million in subscription revenue in Q4 2025, with 21% year-over-year growth, and that expansion was tied to broader workflow adoption across functions beyond core IT use cases.[1]ServiceNow, “ServiceNow Reports Fourth Quarter and Full-Year 2025 Financial Results,” ServiceNow Newsroom, servicenow.com The enterprise service management store apps market is also benefiting from lower installation friction because platform operators now streamline entitlement, acceptance, and app surfacing steps that previously delayed adoption after purchase. This matters commercially because every new cloud platform customer becomes a recurring buyer of adjacent extensions, upgrades, and workflow enhancements distributed through the same marketplace channel. The result is that cloud migration no longer only supports software deployment; it also shapes how vendors monetize the enterprise service management store apps market through repeat app purchases and growing partner participation.

AI-Assisted Workflow Automation in Enterprise Service Management

AI-assisted workflow automation is changing, which extensions attract spending across the enterprise service management store apps market, because buyers now expect automation features to be embedded into service tools rather than added later. ServiceNow disclosed that its Marketplace grew 67% year over year, while Now Assist surpassed USD 600 million in annual contract value in 2025 and targeted more than USD 1 billion in 2026. That momentum shows that buyers are not only adopting AI at the platform level but are also paying for packaged AI functions sold as certified store extensions. The governance pressure is also rising because a 2026 C1 survey found that 95% of organizations now run AI agents that autonomously perform IT or security tasks, underscoring the need for validated identity and security controls for machine-led actions. ServiceNow also repositioned its Build Program in early 2026 to use the Store as a route to market for partner-built AI agents, which ties agentic automation directly to marketplace distribution economics. As a result, the enterprise service management store apps market is moving from basic extension sales toward higher-value automation bundles that reduce deployment time and align more easily with existing governance rules.

Rapid Expansion of Cross-Functional Service Orchestration

Cross-functional service orchestration is expanding the enterprise service management store apps market by pulling new business functions into platform-based service models that were once centered on IT. Departments such as HR, legal, finance, and facilities now need use-case-specific workflow tools, which increases demand for extensions built around departmental processes rather than only technical incident handling. This widens the addressable buyer set inside the enterprise service management store apps market, because purchase decisions are now influenced by operational leaders outside the central IT function. Dynatrace and ServiceNow deepened their strategic collaboration in 2025, and the scope expanded beyond IT operations into HR Service Delivery and Asset Management workloads, demonstrating how connected service models are replacing standalone functional tools. That shift changes what app publishers must offer, because point solutions with narrow task coverage become less attractive than extensions that support orchestration across multiple business teams. In practical terms, the enterprise service management store apps market is growing in volume from broader internal platform adoption and gaining value from more complex cross-departmental workflow packages.

Rising Demand for Low-Code and No-Code Store Apps

Low-code and no-code development patterns are broadening participation in the enterprise service management store apps market by lowering the technical barrier for both buyers and app creators. The commercial effect is clear, because workflow owners in HR, finance, and shared services can now adopt certified extensions without waiting for large custom engineering projects or specialized developer teams. ServiceNow has been reducing installation and deployment friction within its app experience, enabling faster activation of prebuilt extensions and encouraging wider use by nontechnical teams. ServiceNow also linked partner-built AI agents to its Build Program and Store distribution model in 2026, strengthening the role of reusable packaged apps over one-off custom builds. This creates a wider on-ramp into the enterprise service management store apps market, because smaller teams can adopt standard bundles first and add deeper automation later. It also puts pressure on established publishers, because simpler visual configuration tools make it easier for newer vendors to reach acceptable feature levels without bearing the full cost of legacy development models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity with Legacy Identity and ITSM Stacks | -3.2% | Global (most acute in large enterprises across North America and Europe) | Short term (≤ 2 years) |

| High Certification, Maintenance, and Licensing Costs | -2.1% | Global, most pronounced for SMEs in APAC and South America | Medium term (2-4 years) |

| Security, Data Sovereignty, And Vendor Lock-In Concerns | -1.4% | Europe, APAC core, with spill-over to MEA | Short term (≤ 2 years) |

| Buyer Resistance to Fragmented App Catalog Governance | -0.8% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity with Legacy Identity and ITSM Stacks

Legacy integration problems continue to slow the enterprise service management store apps market, especially in large organizations that have accumulated years of customization across service, identity, and workflow systems. Older identity frameworks often do not align with the permission models required by newer AI-enabled extensions, which means app deployment can depend on a separate identity modernization effort before buyers can proceed. A 2026 Teleport survey found that 43% of organizations had no formal governance controls or only informal guidelines for AI use, which adds to the caution buyers should exercise when evaluating agentic extensions that require privileged access across multiple systems. This weakens near-term conversion in the enterprise service management store apps market, because buyers often need to validate permissions, workflow dependencies, and data access rules before approving production use. The problem becomes more serious as service management expands beyond IT, since each new department adds additional identity roles, policy checks, and legacy connectors that must be aligned. Even when demand is strong, integration risk can delay app listings, purchases, and go-live schedules across the enterprise service management store.

High Certification, Maintenance, And Licensing Costs

High certification and maintenance costs are creating a two-speed supplier environment in the enterprise service management software market, where larger vendors can sustain ongoing compliance work more easily than smaller publishers. Certified app distribution requires ongoing updates, testing, and alignment with platform release cycles, and those recurring obligations reduce the attractiveness of niche app categories with limited sales potential. The burden is not only on publishers, because buyers also face layered cost decisions once they move beyond the base platform and start adding specialized extensions, AI functions, and service-specific bundles. The International Trade Center highlighted digital infrastructure gaps and skills shortages in its SME Competitiveness Outlook 2025, and these conditions help explain why smaller organizations remain more price-sensitive even when prebuilt software reduces technical effort. This is one reason the enterprise service management store apps market still skews toward large enterprises, even though the SME growth rate is stronger over the forecast period. The result is a catalog that can favor broad, high-volume app classes while leaving narrower compliance and vertical workflow needs underrepresented.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Cloud Dominance Entrenches While Web-Based Retains Transitional Relevance

Cloud-based apps accounted for 84.37% of revenue in 2025 and are projected to grow at an 18.64% CAGR through 2031 in the enterprise service management store apps market. This concentration reflects how platform operators have built certification, entitlement, version control, and distribution processes around cloud delivery rather than around locally managed deployment formats. The enterprise service management store apps market has therefore become structurally aligned with cloud release cycles, because new capabilities now move through centralized marketplaces with fewer installation steps. ServiceNow’s Application Manager changes in 2025 clearly show that direction, as eligible apps can now surface automatically after company-level terms are accepted, reducing repetitive friction in deployment workflows. This operating model also favors faster monetization, because publishers can distribute upgrades and feature additions through the same managed framework that handles initial activation. For buyers, the practical advantage is less manual work around installation, entitlement, and version maintenance, which makes store-based adoption easier to scale across multiple functions.

Web-based deployment still retains a role in the enterprise service management store apps market, especially for organizations that must keep tighter control over jurisdictional hosting, internal data movement, or phased migration plans. Some enterprises remain in transition and prefer web-based formats while they modernize older service management environments or reassess cloud governance requirements. That means web-based models are not disappearing, but their role is shifting toward controlled use cases rather than mainstream growth leadership. The cloud advantage is also becoming harder to challenge as AI agents become more common, because continuous model updates and higher compute need fit cloud-native environments more naturally than constrained deployment setups. As more advanced extensions are designed first for managed cloud stacks, the enterprise service management store apps market is likely to widen the performance gap between cloud and web-based formats over time. Even so, transitional demand for web-based deployment still supports a smaller but durable niche among buyers that value staged change over rapid platform standardization.

By Enterprise Size: Large Enterprises Hold the Revenue Base While SMEs Gain Speed

Large enterprises captured 71.84% of the 2025 market, while SMEs are projected to grow at a 19.88% CAGR through 2031 in the enterprise service management store apps market. Large organizations built much of the early installed base because they had the budget, architecture teams, and governance structures needed to adopt platform ecosystems before smaller firms were ready. That history still matters because deep workflow customizations and long service platform commitments create switching costs that reinforce app spending on the same core environments. In revenue terms, large enterprises continue to anchor the enterprise service management store apps market because they buy more modules, support more departments, and require larger catalogs of certified extensions. Their buying patterns also favor premium workflow packages with tighter compliance, identity, and orchestration requirements. This gives leading platforms a durable commercial floor, even as new customer growth becomes more diversified.

SMEs are entering the enterprise service management store apps market through a different route that depends on prevalidated bundles, lighter implementation paths, and consumption-led purchasing. The International Trade Centre identified digital infrastructure gaps and skills shortages as major barriers for smaller firms, which supports the view that ready-to-use extensions are more attractive than custom development for this buyer group. That is why SME adoption is accelerating even from a smaller base, because certified marketplace apps can reduce both project complexity and the need for scarce internal expertise. The enterprise service management store apps industry also benefits from this pattern, since app bundles and guided configuration lower the cost of expanding service automation into firms that once remained outside the category. Mid-sized buyers are especially important because they want advanced workflow capability without the operational burden of enterprise-scale buildouts. Over the forecast period, faster SME adoption should gradually reduce the current revenue imbalance, even though large organizations are expected to remain the main source of absolute spending.

By Application: Security And Identity Lead Growth While IT Operations Management Anchors Scale

Security Operations and Identity is projected to grow at a 20.82% CAGR through 2031, while IT Operations Management held 31.46% of the enterprise service management store apps market share in 2025. IT Operations Management remains the largest revenue pool because incident management, monitoring, change workflows, and service reliability functions are already embedded across mature enterprise service platforms. That installed base gives the enterprise service management store apps market a stable demand center, since buyers continue to add extensions around proven IT service processes before moving into newer functional categories. At the same time, Security Operations and Identity is growing faster because the rise of machine-led activity is expanding the number of access points that need validation, monitoring, and audit controls. C1 reported in 2026 that 95% of enterprises now run AI agents that autonomously perform IT or security tasks, while only 45% have deployed IAM tools to govern non-human identities.[2]IBM Newsroom, “IBM and ServiceNow Expand Collaboration to Unlock Enterprise Data for AI at Scale,” IBM, ibm.com That gap is pushing buyers toward certified extensions that can secure agent actions inside service workflows without forcing separate, slower governance projects.

The enterprise service management store apps market is also seeing greater interest in Human Resources Service Delivery, as companies seek to handle employee workflows on the same platforms used for internal support operations. Dynatrace and ServiceNow expanded their collaboration across HR Service Delivery, IT operations, and Asset Management, reinforcing the move toward broader service orchestration on a shared platform. Customer Service Management is also gaining traction where organizations want tighter links between internal service processes and external support interactions. Custom workflow and productivity extensions remain important across the long tail of the catalog, because they address vertical use cases that platform vendors have not fully standardized. In that sense, the enterprise service management store apps market combines a mature IT operations core with a newer security and identity growth engine, driven by AI governance needs. This pattern should keep volume centered on IT-led categories while shifting incremental growth toward identity, risk, and cross-functional workflow control.

Geography Analysis

North America accounted for 41.28% of revenue in 2025, making it the largest regional market for enterprise service management store apps. The region benefits from a dense concentration of large enterprise platform deployments, broad alignment with hyperscalers, and a mature supplier ecosystem that supports store-based extension development across many workflow categories. The United States remains the main regional contributor, while Canada and Mexico add demand as multinational organizations extend common service governance models across regional operations. This gives North America a structural lead in the enterprise service management store apps market, because buyers there often adopt new app categories earlier and can scale them across large installed environments. Europe is the second-largest geography and remains especially important for compliance-led demand. Buyers in Germany, the United Kingdom, and France place greater weight on auditable controls, data-handling discipline, and vendor accountability, raising the quality bar for store listings and supporting vendors with stronger governance infrastructure.

Asia-Pacific is projected to expand at a 20.71% CAGR through 2031, which makes it the fastest-growing geography in the enterprise service management store apps market. The regional growth profile is supported by rising enterprise software spending, stronger digital modernization programs, and buyer preference for faster deployment models that reduce dependence on scarce developer resources. India, China, Japan, South Korea, and Australia are central to that expansion, but the underlying demand patterns differ across them, as each market moves at a different pace in cloud readiness, procurement rules, and internal workflow digitization. Japan offers a clear public-sector example, as its Digital Agency formalized the Digital Marketplace in early 2025 to support SaaS procurement across ministries, prefectures, and municipalities.[3]C1, “Future of Identity Security 2026,” C1, c1.ai That move matters for the enterprise service management store apps market because it normalizes a governed marketplace model in public administration and creates a clearer path for certified workflow tools. Across the broader region, prebuilt app bundles are also becoming more attractive where organizations need business process automation but cannot support long custom build cycles. The growth opportunity is therefore tied not only to software budgets, but also to a practical need for simpler deployment and stronger governance.

South America, the Middle East, and Africa still account for a smaller portion of the enterprise service management store apps market, yet they remain strategically relevant because growth is often linked to formal modernization programs and compliance-driven adoption. Brazil leads South American demand, with multinational and public-sector buyers showing greater interest in structured workflow platforms that can support policy consistency and audit readiness. In the Middle East, the United Arab Emirates and Saudi Arabia continue to invest in digital government and enterprise transformation programs that improve the operating environment for certified store apps. Africa remains earlier in its adoption curve, with South Africa and Nigeria standing out where financial services and telecommunications create stronger service management requirements than the broader regional average. Taken together, these geographies represent a smaller revenue pool today, but they offer expansion potential for vendors that can align pricing, compliance, and deployment models to local operating realities within the enterprise service management store apps market.

Competitive Landscape

The enterprise service management store apps market is moderately concentrated at the platform level and more fragmented at the extension level, which creates a split competitive structure. Platform owners control certification, distribution, and installed customer access, so they set the rules that shape how independent publishers participate in the enterprise service management store apps market. That gives leaders a clear advantage in visibility, ecosystem economics, and upgrade timing, even when individual extension categories remain contested. At the same time, buyers still evaluate app quality based on workflow fit, compliance strength, and deployment ease, leaving room for competition among specialized vendors. ServiceNow remains the strongest reference point in this space because its marketplace scale, AI packaging, and platform breadth are already tied together operationally. Atlassian, Freshworks, and BMC still matter in specific workflow areas, keeping the enterprise service management software market active rather than closed.

Strategic moves across the enterprise service management store apps market show that leading companies are expanding through acquisitions, ecosystem building, and tighter control of data and identity capabilities. ServiceNow completed its acquisition of Armis in June 2026, after already closing the Veza acquisition, and that combination strengthened first-party security and identity coverage inside its broader workflow platform. IBM and ServiceNow also expanded their collaboration in June 2026 to address the AI-ready data challenge and the legacy application layer, with joint solutions expected through the ServiceNow Store in the second half of 2026.[4]Japan Digital Agency, “Digital Marketplace Official Version Launch Announcement,” Digital Agency Japan, digital-gov.note.jp Freshworks strengthened its ServiceOps position through the FireHydrant acquisition, which connected IT service management with AI-native incident management and reliability functions. These moves show that competition in the enterprise service management store apps market is increasingly focused on owning adjacent control layers rather than only adding isolated app features.

White-space opportunity remains meaningful in the enterprise service management store apps market, especially in vertical workflow categories that need stronger compliance logic or deeper automation than broad horizontal tools currently provide. Industry-specific HR delivery, compliance-heavy financial workflows, and telecom-oriented incident response still offer room for further specialization. The enterprise service management store apps industry is also under pressure from AI-native entrants that can work within established platform programs while offering simpler pricing and faster deployment. That creates a challenge for legacy publishers, because established customer relationships no longer guarantee product differentiation if buyers can find certified alternatives with a narrower scope and lower friction. Over time, the market is likely to maintain its mixed structure, where a small group of platforms shapes distribution while a broader field of publishers competes for category-level demand within the enterprise service management store apps market.

Enterprise Service Management Store Apps Industry Leaders

ServiceNow, Inc.

IBM Corporation

Microsoft Corporation

Cisco Systems, Inc.

Okta, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: ServiceNow completed its acquisition of Armis for approximately USD 7.75 billion, integrating real-time cyber asset visibility and AI-native identity intelligence, via the previously closed Veza acquisition, into its platform. This positions ServiceNow as a vertically integrated provider of security operations extensions, altering the competitive calculus for independent security app publishers in its Store.

- June 2026: IBM and ServiceNow announced an expanded collaboration to address the AI-ready data problem and legacy application layer. The partnership will deliver joint solutions through the ServiceNow Store in the second half of 2026, extending ServiceNow's Workflow Data Fabric with IBM's enterprise data capabilities to enable autonomous IT operations for the world's largest enterprises.

- June 2026: Everbridge xMatters expanded its collaboration with ServiceNow, extending earlier Emergency Event Management initiatives into AI-driven digital operations and workflow orchestration. XMatters' expanded ServiceNow Store integration adds automated stakeholder communications, dynamic incident routing, and workflow automation capabilities designed to reduce enterprise incident response times.

- March 2026: SailPoint signed a strategic collaboration agreement with AWS to govern agentic AI access, making SailPoint Machine Identity Security and Agent Identity Security available for purchase through AWS Marketplace. The agreement creates a new route to market for identity governance extensions in cloud-native enterprise environments.

Global Enterprise Service Management Store Apps Market Report Scope

Enterprise Service Management Store Apps are applications that enable organizations to manage, automate, and deliver internal business services through a centralized service portal. The scope includes apps used across functions such as IT, human resources, finance, facilities, legal, and other enterprise departments to streamline service requests, approvals, workflows, knowledge management, and employee self-service.

The Enterprise Service Management Store Apps Market Report is Segmented by Deployment Type (Cloud-Based, and Web-Based), Enterprise Size (Small and Medium Enterprises, and Large Enterprises), Application (IT Operations Management Extensions, Human Resources Service Delivery Extensions, Customer Service Management Extensions, Security Operations and Identity Extensions, and Custom Workflow and Productivity Extensions), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Based |

| Web-Based |

| Small and Medium Enterprises |

| Large Enterprises |

| IT Operations Management Extensions |

| Human Resources Service Delivery Extensions |

| Customer Service Management Extensions |

| Security Operations and Identity Extensions |

| Custom Workflow and Productivity Extensions |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Deployment Type | Cloud-Based | |

| Web-Based | ||

| By Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Application | IT Operations Management Extensions | |

| Human Resources Service Delivery Extensions | ||

| Customer Service Management Extensions | ||

| Security Operations and Identity Extensions | ||

| Custom Workflow and Productivity Extensions | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the Enterprise Service Management Store Apps Market?

The Enterprise Service Management Store Apps Market stands at USD 2.76 billion in 2026 and is forecast to reach USD 6.21 billion by 2031, with a 17.61% CAGR over 2026-2031.

What is driving the adoption of enterprise service management store apps?

The main demand drivers are cloud-first workflow ecosystems, wider use of AI-assisted automation, cross-functional service orchestration, and growing interest in low-code and no-code app deployment.

Which deployment model leads this space today?

Cloud-based apps accounted for 84.37% of revenue in 2025 and are projected to grow at an 18.64% CAGR through 2031, keeping cloud as the main commercial format.

Which buyer group is expanding fastest?

Large enterprises still held 71.84% of revenue in 2025, but SMEs are projected to grow faster at a 19.88% CAGR as prevalidated app bundles lower adoption barriers.

Which application area shows the strongest growth outlook?

Security Operations and Identity is projected to grow at a 20.82% CAGR through 2031, supported by the rise of AI agents and the governance gap around non-human identities.

Which region offers the strongest growth opportunity through 2031?

Asia-Pacific is expected to post the fastest regional growth at a 20.71% CAGR, while North America remains the largest revenue contributor with a 41.28% share in 2025.

Page last updated on: