Enterprise Agent Infrastructure Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

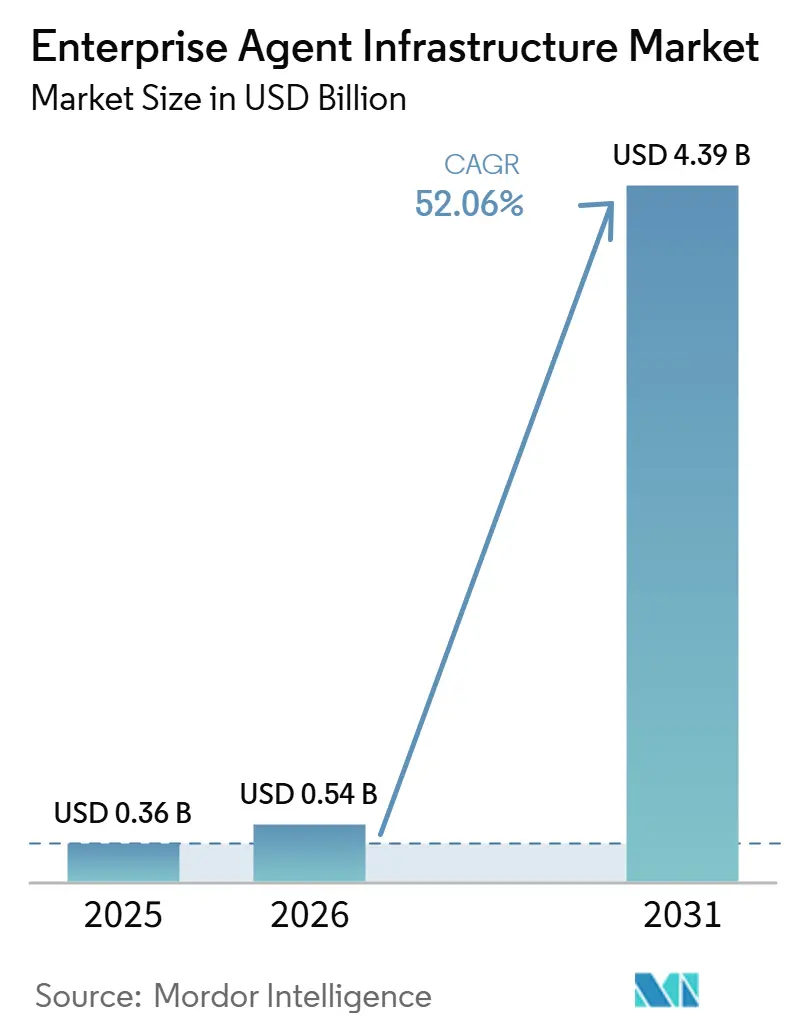

| Market Size (2026) | USD 0.54 Billion |

| Market Size (2031) | USD 4.39 Billion |

| Growth Rate (2026 - 2031) | 52.06% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Agent Infrastructure Market Analysis by Mordor Intelligence

The Enterprise Agent Infrastructure market size is projected to be USD 0.36 billion in 2025, USD 0.54 billion in 2026, and reach USD 4.39 billion by 2031, growing at a CAGR of 52.06% from 2026 to 2031. Surging venture capital, rapid migration from pilot projects to production deployments, and usage-based monetization that scales with inference volume rather than employee headcount are accelerating growth. Enterprises view agentic systems as a pathway to automate complex IT operations, customer engagement, and data-orchestration workflows. Competition is unfolding across three layers, such as foundation models, orchestration frameworks, and vector databases, each racing to lower latency and cost while improving reasoning depth. Demand for integration services, observability tooling, and compliance-ready frameworks is expanding as organizations strive to run agents at scale without jeopardizing data security or regulatory alignment.

Key Report Takeaways

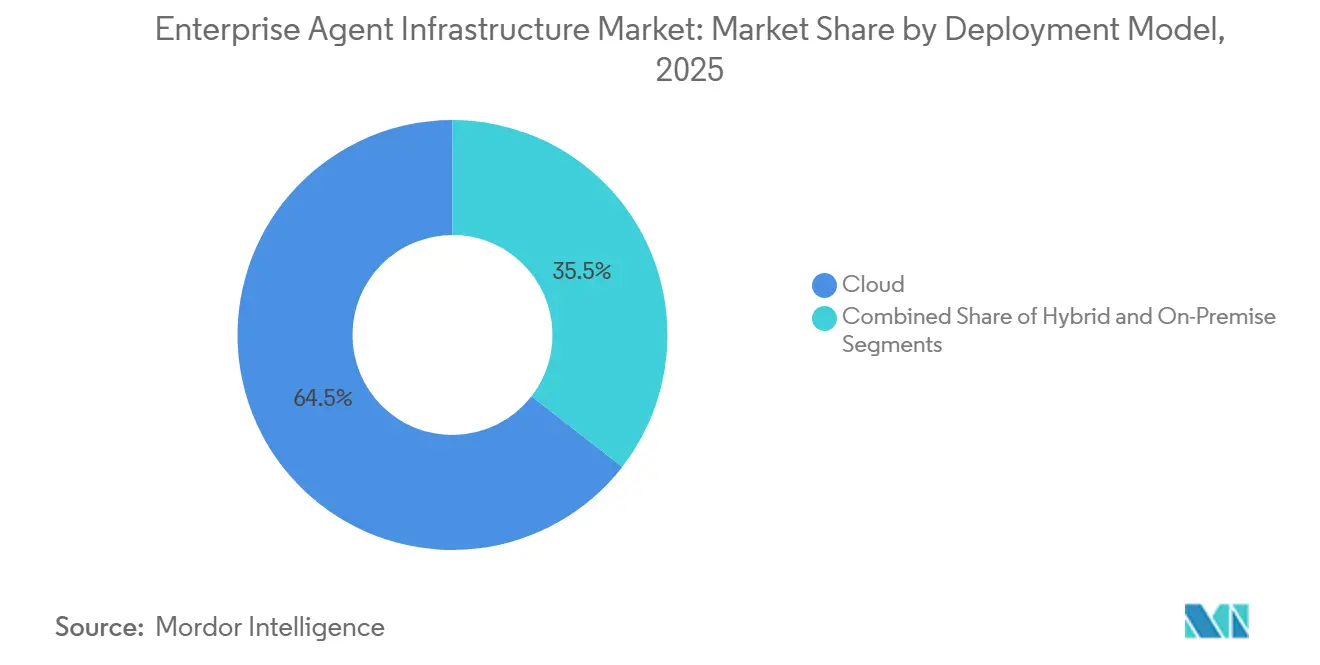

- By deployment model, cloud captured 64.49% of the Enterprise Agent Infrastructure market share in 2025, while hybrid deployments are forecast to advance at a 27.64% CAGR through 2031.

- By component, software led with a 44.39% share of the Enterprise Agent Infrastructure market size in 2025, whereas services are projected to expand at a 26.23% CAGR to 2031.

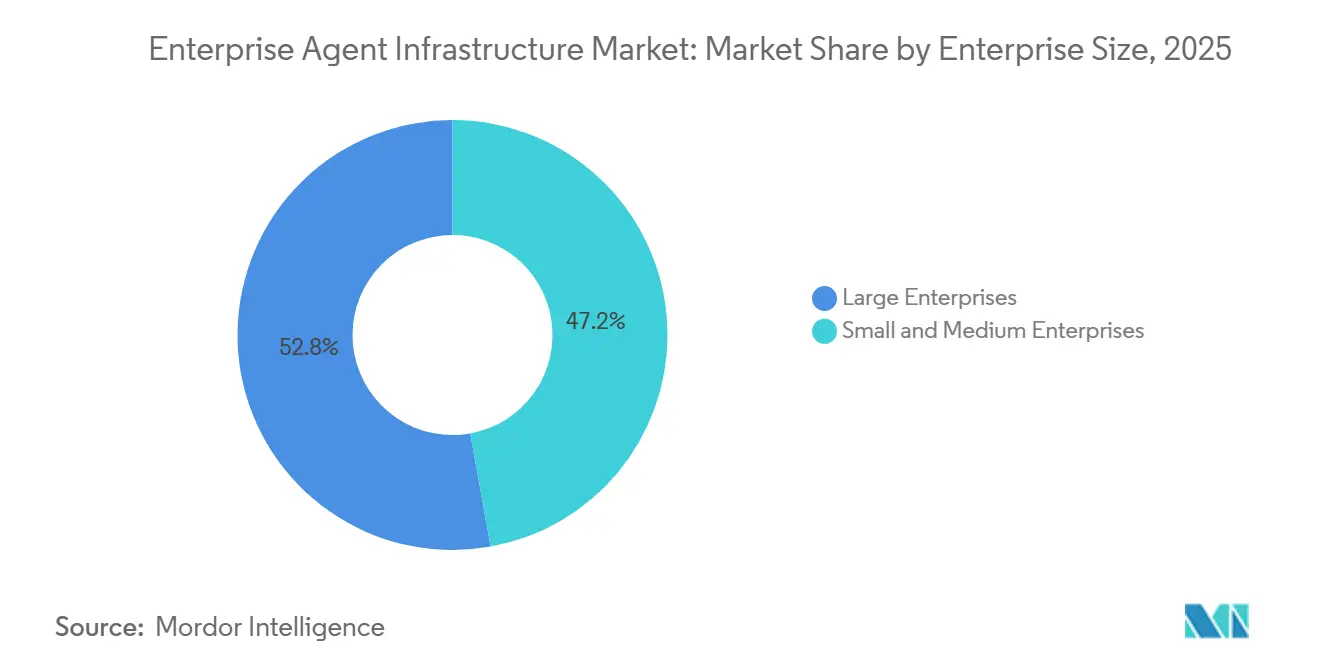

- By enterprise size, large organizations accounted for 52.84% of revenue share in 2025, yet small and medium enterprises are growing fastest at a 22.89% CAGR through 2031.

- By industry vertical, IT and telecom commanded 28.53% of 2025 revenue, while energy and utilities is the fastest-growing segment at a 25.89% CAGR to 2031.

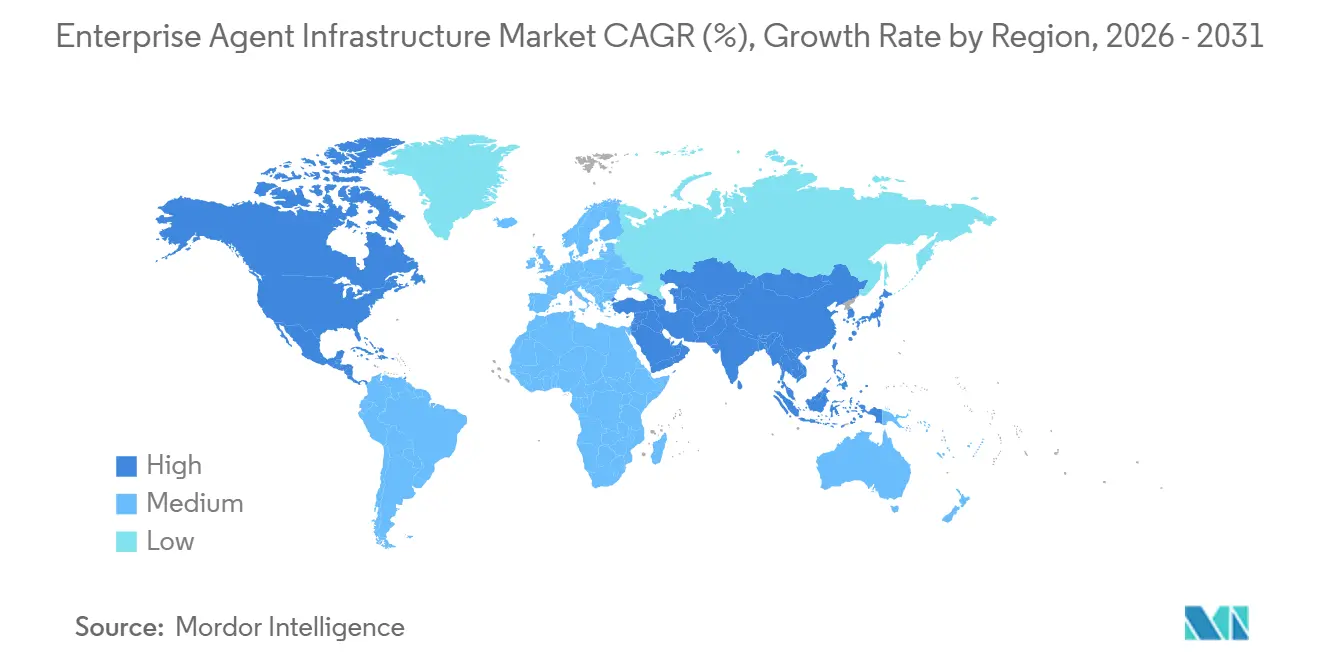

- By geography, North America led with 25.82% market share in 2025, and Asia-Pacific is expected to post the quickest regional expansion at a 24.26% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Enterprise Agent Infrastructure Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Cloud-Native AI Infrastructure | +12.5% | Global, concentration in North America and Europe | Medium term (2-4 years) |

| Surge in Conversational AI Deployments | +10.8% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Increased Investment in Autonomous IT Agents | +9.2% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Emergence of Vector Database Interoperability Standards | +7.5% | Global, early adoption in North America | Long term (≥ 4 years) |

| Rise of Compliance-Ready Agent Frameworks for Regulated Industries | +6.9% | Europe and North America, spillover to Asia-Pacific | Medium term (2-4 years) |

| On-Device AI Accelerators Enabling Edge Agents | +5.1% | Asia-Pacific manufacturing hubs, North America IoT deployments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Cloud-Native AI Infrastructure

Enterprises are lifting and shifting agent workloads into elastic cloud environments, reducing deployment cycles from quarters to weeks. Databricks surpassed USD 4 billion annualized revenue in 2025, with more than USD 1 billion coming from AI products that bundle orchestration, vector storage, and governance on a unified platform. Public cloud providers now offer GPU access, managed vector databases, and monitoring dashboards, creating switching costs that deepen vendor lock-in. Regulated sectors that cannot rely solely on public clouds are embracing hybrid stacks, reflecting a bifurcation of infrastructure strategies by industry. Microservice architectures enable incremental rollouts, allowing IT teams to validate return on investment before scaling and thereby accelerating adoption.

Surge in Conversational AI Deployments

Conversational agents have evolved from basic chatbots into context-aware assistants capable of executing transactions and orchestrating back-end systems. Anthropic’s Claude Code passed a USD 2.5 billion run rate in February 2026, with enterprise subscriptions quadrupling in less than two months. European firms are pursuing regional alternatives, such as Mistral’s Magistral models, to meet data-sovereignty mandates. The debut of Claude Cowork with plug-ins triggered a broad sell-off in legacy software stocks as investors recognized that autonomous conversational agents could cannibalize traditional SaaS revenue streams. Organizations now benchmark agent platforms on reasoning quality, context-window length, latency, and cost per million tokens.

Increased Investment in Autonomous IT Agents

Automated agents manage incident response, patch management, and capacity scaling, cutting mean-time-to-resolution while boosting uptime. A March 2026 Nikkei survey showed 80% of Japanese enterprises name agent introduction as a strategic priority, yet many struggle with performance visibility, driving demand for observability platforms. Fujitsu’s Kozuchi Enterprise AI Factory, launched in January 2026, bundles on-premise infrastructure with guardrails and quantization tools for finance and manufacturing customers. Accenture formed a 25,000-person Databricks practice to help clients scale multi-agent systems, underscoring the services opportunity. Enterprise deployments increasingly feature orchestrated agent swarms that coordinate task execution, driving up infrastructure sophistication.

Emergence of Vector Database Interoperability Standards

Vector databases have become the memory layer for retrieval-augmented generation and agentic reasoning, yet divergent APIs hinder portability. Pinecone’s serverless approach contrasts with Weaviate’s self-hosted flexibility, forcing enterprises to build abstraction layers. Elastic added Jina reranker models to its managed service in February 2026, lowering the burden of achieving high-precision semantic search. Industry groups have yet to agree on standards comparable to SQL, so frameworks such as LangChain serve as de facto portability layers.[1]Reintech Media, “Pinecone vs Weaviate vs Chroma: Vector Database Comparison 2026,” reintech.io Over the long term, interoperability is expected to unlock multi-vendor ecosystems and curb vendor lock-in.

Restraint Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Compute Costs and Energy Consumption | -8.3% | Global, acute where GPU supply is tight | Short term (≤ 2 years) |

| Data Privacy Regulations Limiting Orchestration | -6.7% | Europe and North America | Medium term (2-4 years) |

| Fragmentation of Agent Protocol Standards | -5.4% | Global, higher impact in multi-vendor environments | Long term (≥ 4 years) |

| Scarcity of Talent for Multi-Agent Alignment and Safety | -4.8% | Global, most acute in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Compute Costs and Energy Consumption

Continuous-running agents often incur higher inference expenses than one-time model training, tightening IT budgets. Japanese data centers will lift national electricity demand by up to 20% as enterprises run always-on agents. Model vendors are responding through aggressive price cuts, such as Mistral’s USD 2 per million tokens versus GPT-4o’s USD 5, making multi-model routing attractive. Organizations report 65% cost savings by combining Mistral for routine inference with premium models for complex tasks, yet GPU scarcity and rising energy prices still constrain scalability. Japan’s shortage of urban land and cooling capacity is pushing hyperscale facilities far from end users, creating latency trade-offs that could limit certain use cases.

Data Privacy Regulations Limiting Orchestration

The European Union AI Act and GDPR impose stringent audit, residency, and explainability requirements that fragment agent architectures across regions. Anthropic’s USD 20 million pledge to politicians favoring AI regulation indicates that vendors see clear rules as an on-ramp for enterprise sales but recognize the near-term compliance burden. Fujitsu markets Kozuchi as an on-premise solution for finance and manufacturing clients seeking to keep sensitive data inside their firewalls. Microsoft Japan faced an antitrust probe in February 2026 over potential cloud lock-in, highlighting regulatory scrutiny of hyperscale providers.[2]Fujitsu, “Fujitsu Launches Generative AI Service That Analyzes Source Code and Automatically Generates Design Documents,” fujitsu.com Multinational firms must run geographically isolated agent clusters, increasing operational overhead and diluting economies of scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Gains as Sovereignty Concerns Rise

Hybrid architectures accounted for a growing slice of the Enterprise Agent Infrastructure market in 2026 and are forecast to expand at a 27.64% CAGR through 2031. Cloud still represented 64.49% of the Enterprise Agent Infrastructure market share in 2025, reflecting the appeal of serverless inference services from Pinecone and unified stacks from Databricks. Regulated sectors such as defense and life sciences require on-premise control for sensitive data, yet they also need burst capacity for training and inference.

Hybrid models let enterprises keep confidential workloads in private data centers while offloading compute-intensive tasks to public-cloud GPUs, optimizing both cost and compliance. Cohere’s on-premises-first strategy with customers Oracle and Dell, and its USD 500 million raise, signal investor conviction that sovereignty-friendly deployments will remain pivotal. Fujitsu’s partnership with NVIDIA on CPU-GPU stacks underscores efforts to blend on-premise governance with cloud-burst elasticity.[3]Fujitsu, “Fujitsu Group Starts Manufacturing Sovereign AI Servers in Japan to Enhance Digital Sovereignty,” fujitsu.com

By Component: Services Surge as Integration Complexity Grows

Services are projected to expand at a 26.23% CAGR, reflecting the growing need for integration, fine-tuning, and observability solutions across industries. This growth is driven by enterprises seeking to enhance operational efficiency and streamline workflows through advanced service offerings. Software, on the other hand, accounted for 44.39% of the Enterprise Agent Infrastructure market size in 2025, providing essential tools such as orchestration frameworks, vector databases, and API access, which are critical for enabling seamless operations and data management.

Accenture’s 25,000-person Databricks business group highlights the trend of system integrators bundling software licenses with additional services like governance, training, and continuous optimization. This approach ensures that enterprises can maximize the value of their software investments while addressing complex deployment requirements. For instance, Databricks’ AppKit simplifies development by reducing boilerplate code; however, regulated deployments still necessitate professional services to ensure compliance and efficiency. Enterprises are increasingly opting for managed services that facilitate smooth upgrades, secure data pipelines, and optimize retrieval parameters. These services allow internal teams to concentrate on leveraging their domain expertise rather than managing the intricacies of platform infrastructure, ultimately driving better outcomes and innovation.

By Enterprise Size: SMEs Accelerate with No-Code Orchestration

Large enterprises accounted for 52.84% of 2025 revenue, leveraging specialized AI teams to deploy multi-agent systems. These enterprises focus on integrating advanced technologies to streamline operations, enhance productivity, and maintain a competitive edge. They invest heavily in research and development to ensure their systems remain at the forefront of innovation. Nonetheless, small and medium enterprises (SMEs) are forecast to grow at a 22.89% CAGR as no-code tools democratize development, enabling businesses with limited technical expertise to adopt and implement AI-driven solutions effectively.

Replit’s platform, used by employees at 85% of the Fortune 500, now integrates with Databricks, enabling non-technical staff to deploy agents via natural-language prompts. This integration simplifies deployment, making it accessible to a broader range of users. SMEs gravitate toward usage-based serverless pricing that removes capital-expenditure hurdles, enabling them to scale their operations without significant upfront investment. The Japan Information System Users Association found that only one-third of smaller firms had adopted agents, highlighting a skills gap that integrators aim to fill through training and support services. As managed platforms mature, SMEs are expected to adopt multi-model routing strategies that balance cost, latency, and accuracy, ensuring optimal performance while managing operational expenses effectively.

By Industry Vertical: Energy and Utilities Lead Growth Trajectory

IT and telecom accounted for 28.53% of 2025 revenue, driven by the growing adoption of network automation and customer service agents. These sectors are leveraging advanced technologies to streamline operations and enhance customer experiences. However, energy and utilities are projected to grow at the fastest rate, with a 25.89% CAGR through 2031. Grid operators are increasingly deploying agents for critical functions such as load balancing, predictive maintenance, and renewable energy integration. These agents enable the creation of real-time decision loops, which are far more efficient and effective compared to traditional legacy control systems.

Retailers, including Albertsons, are already using agentic price-optimization tools built on platforms such as Databricks. This trend indicates that commerce workflows are becoming a significant focus for automation. In the healthcare sector, implementations are prioritizing on-premises stacks to ensure compliance with HIPAA requirements and safeguard sensitive patient data. Meanwhile, manufacturers are collaborating with technology leaders such as Fujitsu and NVIDIA to develop physical AI solutions that control robotic assembly lines, enhancing precision and efficiency in production processes. Government demand for agent-based solutions is being addressed through FedRAMP-certified offerings like Claude for Government. These solutions expedite document analysis while maintaining stringent security standards, ensuring they meet the unique requirements of public sector operations.

Geography Analysis

North America commanded 25.82% of the Enterprise Agent Infrastructure market in 2025, benefiting from dense GPU availability, federal procurement incentives, and venture capital concentration. Enterprises leverage favorable cloud economics but face rising electricity costs, prompting hyperscalers to locate data centers in lower-cost regions within the continent. Regulatory scrutiny, such as state-level privacy statutes, forces organizations to implement granular data-residency controls that add complexity yet ultimately stimulate demand for compliance-ready agent frameworks.

Asia-Pacific is forecast to expand at a 24.26% CAGR through 2031, propelled by Japan, China, India, and South Korea. A March 2026 survey reported that 80% of Japanese firms with revenue above JPY 1 trillion (USD 6.7 billion approximately) had deployed generative AI, signaling top-down mandates for automation. Japan’s data-center capacity must double by 2030 and increase ninefold by 2040, exposing infrastructure bottlenecks that could moderate growth if power upgrades lag. India and Southeast Asian economies adopt multilingual models to serve diverse linguistic markets, supported by hyperscale investments from U.S. and Middle Eastern investors.

Europe’s outlook is shaped by the AI Act, which imposes audit-trail and transparency requirements. While compliance overhead slows early adoption, clear guardrails ultimately de-risk procurement for large enterprises. Vendors such as Mistral and Aleph Alpha position themselves as regionally compliant options, differentiating on data residency and explainability. The Middle East and Africa region leverages sovereign cloud partnerships, most notably the OpenAI-G42 alliance, to serve Arabic-language markets, while South America’s activity centers on Brazil and Argentina, where conversational agents automate Portuguese and Spanish customer support.

Competitive Landscape

Competition in the Enterprise Agent Infrastructure market is moderate, with vertical integration emerging as a key strategy. Foundation-model leaders Anthropic and OpenAI secured USD 30 billion and USD 8.3 billion, respectively, concentrating capital and advancing model capabilities. Second-tier players like Mistral and Cohere differentiate through on-premise flexibility and regional compliance, capitalizing on data-sovereignty mandates.[4]Mistral AI, “Announcing Magistral, The First Reasoning Model by Mistral AI, Excelling in Domain-Specific, Transparent, and Multilingual Reasoning,” mistral.ai Orchestration vendors such as Databricks bundle lakehouse storage, Agent Bricks, and governance to capture broader wallet share, a move reinforced by its USD 100 billion valuation and robust net revenue retention.

Vector-database providers Pinecone and Weaviate compete on latency, hybrid search accuracy, and deployment flexibility, while Elastic broadens managed model catalogues to enhance retrieval precision. IBM’s USD 11 billion acquisition of Confluent embeds real-time streaming into a unified data platform, underscoring incumbent efforts to close functionality gaps. Replit’s USD 400 million round and AppKit integration reveal how coding-assistant platforms lower entry barriers, potentially commoditizing orchestration and shifting value to governance and compliance tooling.

Enterprises are increasingly adopting multi-model routing strategies to optimize both cost and performance, thereby reducing the dependency on any single model provider and diminishing the lock-in advantages traditionally held by such providers. This shift has intensified competition among vendors, who now focus on differentiating themselves through factors such as context-window length, reasoning benchmarks, and energy efficiency. Despite these advancements, observability and safety tooling remain significant white-space opportunities in the market. The lack of mature products capable of effectively monitoring multi-agent alignment, cost, and latency at scale highlights a critical gap that vendors could address to meet enterprises' growing demands.

Enterprise Agent Infrastructure Industry Leaders

OpenAI OpCo, LLC

Anthropic PBC

Cohere Inc.

AI21 Labs Ltd.

Adept AI Labs, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Accenture and Databricks expanded their alliance, launching a business group with 25,000 certified professionals focused on scaling Agent Bricks, Lakebase, and Genie across multiple sectors.

- March 2026: Replit raised USD 400 million at a USD 9 billion valuation, unveiling Agent 4 with parallel task execution and sketch-to-design conversion for Fortune 500 users.

- February 2026: Anthropic finalized a USD 30 billion round at a USD 380 billion valuation and launched Claude Cowork, a workflow automation platform.

- February 2026: Databricks introduced AppKit, a TypeScript framework with default authentication and observability, integrated directly with Replit for one-click deployments.

Global Enterprise Agent Infrastructure Market Report Scope

The Enterprise Agent Infrastructure Market refers to the ecosystem of platforms, tools, and services that enable organizations to design, deploy, orchestrate, monitor, and scale autonomous and semi-autonomous software agents across enterprise environments. These agents, often powered by artificial intelligence, machine learning, and large language models, automate complex workflows, support decision-making, and enhance operational efficiency across business functions.

The Enterprise Agent Infrastructure Market Report is Segmented by Deployment Model (Cloud, On-Premise, and Hybrid), Component (Software, and Services), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (IT and Telecom, BFSI, Healthcare and Life Sciences, Retail and eCommerce, Manufacturing, Energy and Utilities, Government and Public Sector, and Other Industry Verticals), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-Premise |

| Hybrid |

| Software |

| Services |

| Large Enterprises |

| Small and Medium Enterprises |

| IT and Telecom |

| BFSI |

| Healthcare and Life Sciences |

| Retail and eCommerce |

| Manufacturing |

| Energy and Utilities |

| Government and Public Sector |

| Other Industry Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Deployment Model | Cloud | ||

| On-Premise | |||

| Hybrid | |||

| By Component | Software | ||

| Services | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Industry Vertical | IT and Telecom | ||

| BFSI | |||

| Healthcare and Life Sciences | |||

| Retail and eCommerce | |||

| Manufacturing | |||

| Energy and Utilities | |||

| Government and Public Sector | |||

| Other Industry Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value and forecast growth rate of the Enterprise Agent Infrastructure market?

It was USD 0.54 billion in 2026 and is projected to reach USD 4.39 billion by 2031, reflecting a 52.06% CAGR.

Which deployment model is expected to grow fastest?

Hybrid deployments are forecast to grow at a 27.64% CAGR between 2026 and 2031 as firms balance scalability with data sovereignty.

Why are services growing faster than software?

Integration, fine-tuning, and observability needs push services to a 26.23% CAGR, outpacing standalone software revenue.

Which region will see the highest growth?

Asia-Pacific is projected to expand at a 24.26% CAGR, led by Japan, China, India, and South Korea.

What are the main cost challenges for enterprises?

High GPU prices and rising energy consumption can inflate inference costs, prompting cost-optimization strategies such as multi-model routing.

How concentrated is the competitive landscape?

The market scores a 6 out of 10, indicating that while leading vendors are influential, opportunities remain for emerging specialists.

Page last updated on: