Energy And Utilities Testing, Inspection, And Certification Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

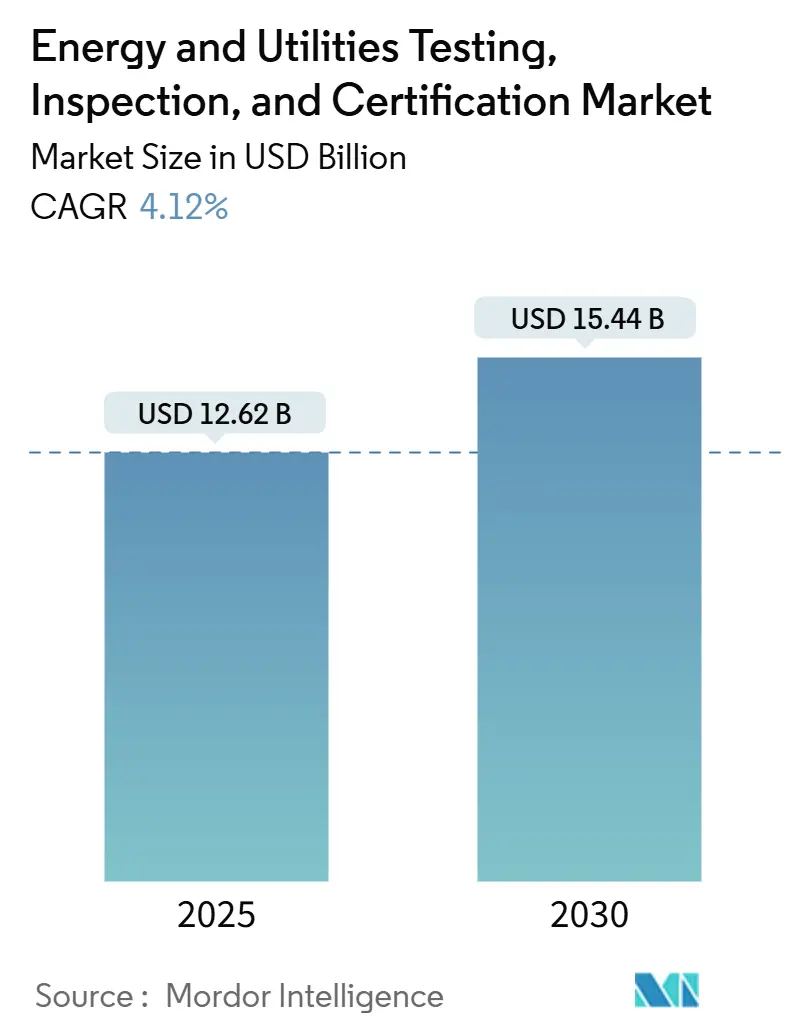

| Market Size (2025) | USD 12.62 Billion |

| Market Size (2030) | USD 15.44 Billion |

| Growth Rate (2025 - 2030) | 4.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

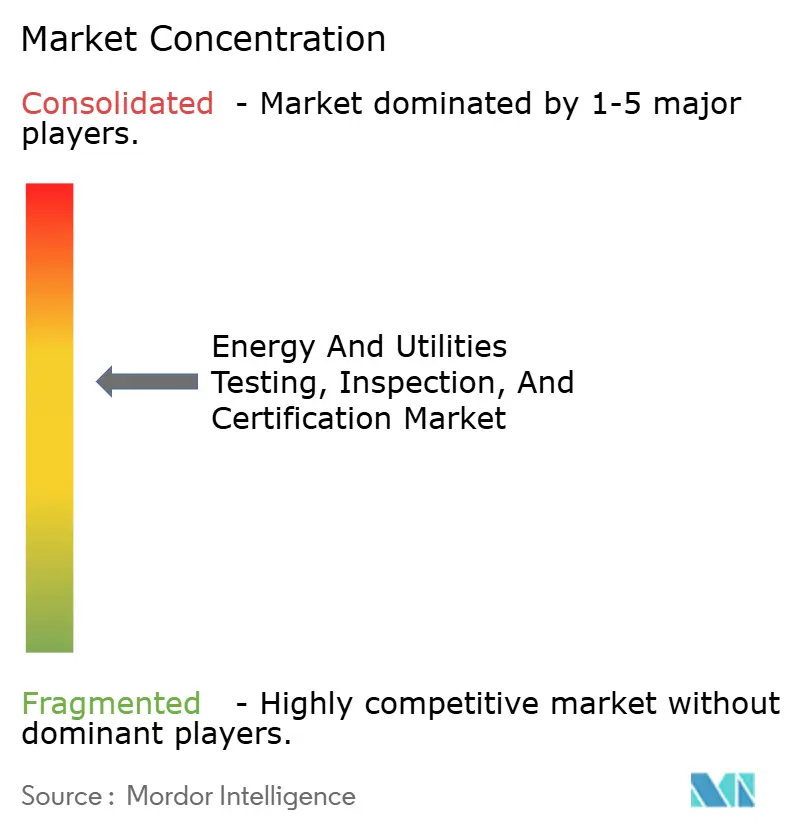

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Energy And Utilities Testing, Inspection, And Certification Market Analysis by Mordor Intelligence

The energy and utility testing inspection certification market size reached USD 12.62 billion in 2025 and is on track to climb to USD 15.44 billion by 2030, reflecting a 4.12% CAGR over the forecast horizon. Aging grid assets, record renewable additions, and tightening cybersecurity rules are expanding the addressable universe for third-party power testing, inspection certification services. Rising replacement costs for substation equipment, the shift to digital substations built on IEC 61850, and mandatory carbon-intensity verification under the European CSRD are steering utilities toward external specialists. At the same time, drone-enabled inspections and predictive analytics curb outage risks, while industry consolidation promises broader geographic reach and deeper technical portfolios. Asia-Pacific leads demand thanks to massive grid buildouts across China and India, whereas North America and Europe rely on these services to extend the life of post-war infrastructure.

Key Report Takeaways

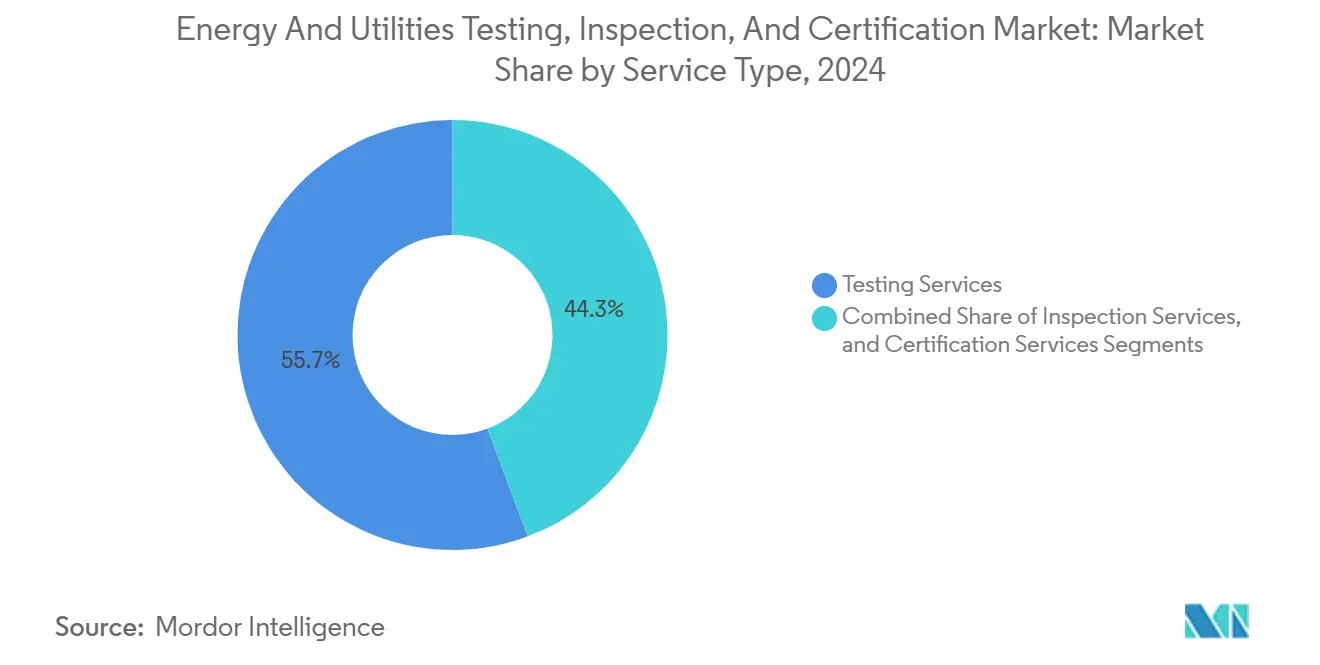

- By service type, Testing Services held 55.7% of the energy and utility testing inspection certification market share in 2024, and certification services are forecast to post the fastest 4.6% CAGR through 2030 within the energy and utility testing inspection certification market size.

- By sourcing type, the outsourced model accounted for 67.2% of the energy and utility testing inspection certification market size in 2024.

- By geography, Asia-Pacific dominated with 45.3% of the 2024 energy and utility testing inspection certification market share, while also advancing at a 4.8% CAGR to 2030.

Global Energy And Utilities Testing, Inspection, And Certification Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging grid infrastructure requires a life-extension assessment | +1.2% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Surge in renewable build-outs needing pre-commissioning TIC | +1.8% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| Stricter carbon-intensity disclosure and ESG-linked finance | +0.7% | Global, early in the EU and North America | Medium term (2-4 years) |

| Digital-substation roll-outs drive software-centric testing | +0.9% | Global, spillover from developed to emerging | Long term (≥ 4 years) |

| On-site drone/robotic inspections cut downtime | +0.6% | Global, early gains in North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Cyber-resilience certification for smart-meter/DER gateways | +0.8% | Global, guided by IEC 62443 | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging grid infrastructure requires a life-extension assessment

Many transmission and distribution assets installed between the 1960s and 1980s now exceed their nominal service life. NERC’s PRC-005 standard compels utilities to prove protection-system integrity through periodic testing, spurring demand for dissolved-gas analysis, infrared thermography, and partial-discharge diagnostics.[1]“PRC-005,” North American Electric Reliability Corporation, nerc.comIn Michigan, stricter asset-management rules issued after successive outages pushed DTE Energy to accelerate transformer health assessments, raising regional spending on life-extension programs. Because a replacement high-voltage transformer can cost USD 2 million, utilities often find that qualified testing can stretch usable life by another decade, generating an immediate return on investment.

Surge in renewable build-outs needing pre-commissioning TIC

Wind, solar, and storage plants must meet grid-code ride-through, reactive-power, and frequency-support tests before interconnection. VDE Renewables alone verified 2.8 GW of PV modules in 2024, applying salt-mist, PID, and LID protocols for coastal projects. The VDE-AR-N series, aligned with ENTSO-E network codes, standardizes these tests across voltage levels, which helps developers but still mandates on-site witness services. Battery-based storage introduces thermal-runaway, grid-forming, and cyber hardening checks, expanding revenue pools for certification bodies with integrated power-electronics laboratories.

Stricter carbon-intensity disclosure and ESG-linked finance mandates

The EU CSRD now obliges power companies to publish audited emissions data, which in turn elevates third-party verification work. SGS retained an AAA MSCI ESG rating for the fifth straight year, a credential that utilities often cite when selecting a verifier.[2]“SGS Distinguished for Sustainability Excellence,” SGS, sgs.com Green-loan covenants stipulate verified progress toward decarbonization, so certification demand spans ISO 50001 audits, Scope 1-2-3 footprint checks, and product-level carbon labeling. Higher margin, recurring engagements are emerging as TIC firms bundle ESG and grid-code services.

Digital-substation roll-outs drive software-centric testing

Utilities replacing copper wiring with Ethernet-based IEC 61850 processes must validate Sampled Values timing, GOOSE latency, and cyber resilience per IEC 62351. Bureau Veritas and SGS both run digital-substation labs to certify interoperability among protection relays, merging units, and network switches. Germany’s VDE FNN updated its resilience guidelines in 2024 to address cascading IT-OT failures, expanding TIC scope into penetration testing and firmware validation. Re-certification follows every firmware patch, ensuring a stable annuity stream.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented regional grid codes raise duplicative testing costs | -0.9% | Global, acute in Europe and the Asia-Pacific | Long term (≥ 4 years) |

| Shortage of power-sector TIC specialists inflates lead times | -1.1% | Global, severe in North America and Europe | Medium term (2-4 years) |

| Utility OPEX squeeze delays non-mandatory inspections | -0.8% | Global | Short term (≤ 2 years) |

| Immature standards for hydrogen-ready turbines curb certification | -0.3% | Global, early in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented regional grid codes raise duplicative testing costs

Despite progress on European network-code harmonization, national deviations persist. A wind-turbine controller that passes VDE-AR-N 4110 must still undergo separate validation for the UK Grid Code and France’s RTE specifications, adding USD 0.5-2 million to project budgets. In the Asia-Pacific region, misalignment between China’s GB, Japan’s JEAC, and nascent ASEAN rules forces manufacturers to recertify identical hardware multiple times, slowing cross-border equipment flow and prolonging payback periods for test investments.

Shortage of power-sector TIC specialists inflates lead times

The niche blend of high-voltage engineering, grid-code literacy, and cyber expertise narrows the talent pool. Lead-times for complex projects in North America have stretched beyond nine months, partly because the average age of field engineers now exceeds 50 years.[3]“Australian Energy Regulator Asset Management Review,” Australian Energy Regulator, aer.gov.au Intertek reacted by launching regional training hubs for EV-charging, battery, and smart-grid testing, yet demand still outpaces supply, constraining near-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Certification momentum accelerates against a testing-heavy base

Testing Services generated 55.7% of 2024 revenue, anchored by routine dielectric, mechanical, and functional checks across aging transformers and newly installed renewable assets. Utilities deploying utility-scale solar rely on grid-conformity tests—ride-through, reactive-power, harmonic compliance—before energization, cementing Testing Services as the backbone of the power testing inspection certification market. Advanced field diagnostic kits and drone-mounted thermal cameras trim outage-related losses, prompting utilities in Asia-Pacific, Europe, and North America to expand test scopes and contract durations. Revenue resiliency is reinforced by regulatory mandates such as NERC PRC-005 in the United States and VDE-AR-N 4105 in Germany, both requiring periodic protection-system validation. Long-term annuity streams emerge as asset owners schedule multi-year framework agreements that combine preventive diagnostics with warranty inspections.

Certification Services, although smaller, is set to clock a 4.6% CAGR through 2030. Heightened cyber-resilience obligations under IEC 62443 and expanding ESG disclosure rules elevate third-party attestations. The segment stands to gain further as hydrogen-ready turbines, grid-forming inverters, and vehicle-to-grid chargers reach commercialization, all needing conformance badges before utilities approve interconnection. Market leaders leverage their global accreditation portfolios to offer bundled conformity assessment paths, thereby reducing time-to-market for equipment manufacturers. These factors position Certification Services as the catalyst for incremental margin expansion within the energy and utility testing, inspection certification market over the next five years.

By Sourcing Type: Specialized know-how underpins outsourced dominance

The outsourced model captured 67.2% of 2024 spending. Grid digitalization and cyber-physical convergence demand laboratories equipped for both high-voltage withstand tests and protocol fuzzing capital burden utilities prefer to avoid. Third-party providers also manage multi-jurisdiction accreditation, saving OEMs from maintaining separate quality systems for each export destination. Outsourced partners thus absorb regulatory complexity, while utilities reallocate capital toward grid modernization projects. The impending Bureau Veritas–SGS tie-up underscores how scaled networks will deliver broader site coverage and faster mobilization.

In-house units remain active for routine oil analysis and relay calibration, especially inside vertically integrated utilities that historically built extensive test bays. Yet the skills needed for digital-substation packet-capture analysis or IEC 62619 lithium-battery safety tests sit largely outside traditional utility laboratories. As a result, outsourcing continues to gain share in software-centric and ESG-linked scopes, reinforcing its leadership in the power testing inspection certification market.

Geography Analysis

Asia-Pacific contributed 45.3% of 2024 revenue, the largest slice of the power testing inspection certification market, and will expand at a 4.8% CAGR to 2030. State Grid Corporation’s ultra-high-voltage roll-out and India’s Green Energy Corridor phase 2 pipeline both hinge on extensive pre-commissioning tests for 800 kV DC links, GIS switchgear, and STATCOM systems.[4]“Ultra-High-Voltage Projects,” State Grid Corporation of China, stategrid.com Regional bodies such as SIRIM and TISI are aligning certification pathways, but country-specific annexes still necessitate local witnessing, keeping demand strong for global and domestic TIC players. Renewable-heavy procurement across Vietnam, Indonesia, and the Philippines further drives site-acceptance testing for inverter-based resources under tropical conditions.

North America follows, buoyed by mandatory protection-system maintenance under NERC and a surge in clean-energy projects in ERCOT, CAISO, and PJM. Transmission-focused investment tax credits coupled with upgraded reliability standards mean every reconductoring or STATCOM install requires documented factory‐acceptance and site-acceptance tests. Yet the region’s specialist shortage and utility budget scrutiny elongate project queues, preventing revenue from rising in line with the infrastructure need.

Europe records steady mid-single-digit growth. Harmonized network codes streamline multi-country approvals, but nuances such as the UK’s post-Brexit divergence force duplicate certifications. German VDE standards act as a benchmark; their 2024 update formalized cyber-physical resilience checks for digital substations, broadening service scope. ESG disclosure under CSRD further intensifies demand for carbon-footprint audits, driving cross-selling between electrical and sustainability service lines.

Competitive Landscape

Global leaders SGS, Bureau Veritas, Intertek, and UL Solutions leverage broad accreditation catalogs and dense lab networks to serve utilities, OEMs, and engineering firms. Together, they hold a significant stake in 2024 revenue, giving the sector a moderate concentration profile. Proposed consolidation—in particular, the Bureau Veritas-SGS merger—would create a USD 30 billion giant with unmatched reach across more than 150 countries. Intertek is moving aggressively into battery and EV-charging fields, opening new centers in the United States, the United Kingdom, and China for high-power cycling and grid-interface validation.

Mid-tier players such as TÜV Rheinland, DEKRA, and DNV expand by acquiring niche cyber or power-electronics labs, while local champions in China and India win contracts by pairing low-cost field crews with government endorsements. Competitive advantage increasingly rests on the ability to deliver integrated electrical and cyber assessments. Market entrants focusing solely on legacy dielectrics struggle to win multi-disciplinary bids covering IEC 61850, IEC 62443, and ISO 14064. As standards evolve, players with automated reporting platforms and AI-driven condition-assessment tools are building switching costs that lock in long-term clients.

Energy And Utilities Testing, Inspection, And Certification Industry Leaders

SGS SA

Bureau Veritas SA

Intertek Group PLC

TÜV SÜD AG

TÜV Rheinland AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Bureau Veritas and SGS entered preliminary merger talks aimed at forming a USD 30 billion TIC entity with the scale to run integrated power, cyber, and ESG programs.

- December 2024: VDE Renewables unveiled enhanced PV module protocols targeting salt-mist corrosion and PID mitigation.

- November 2024: TÜV Rheinland broadened IEC 62443 certification services for digital substation gear.

- October 2024: VDE FNN updated VDE-AR-N 4105, easing small-scale generation approvals while preserving fault-ride-through safeguards.

Global Energy And Utilities Testing, Inspection, And Certification Market Report Scope

The energy and power industry's TIC (testing, inspection, and certification) market focuses on guaranteeing the safety, quality, and compliance of different products, systems, and processes. This market includes services that aim to confirm the performance, reliability, and adherence to regulatory standards of equipment, facilities, and operations related to energy generation, transmission, distribution, and consumption.

The TIC market in the energy and power industry is segmented by service type (testing, inspection, and certification), geography (China, United States, India, Japan, Brazil, Canada, South Korea, Germany, France, Saudi Arabia, Rest of the World), and application (power generation, storage, and distribution & sales). Further, in-house services are excluded from the scope of the study. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Testing Services |

| Inspection Services |

| Certification Services |

| In-house |

| Outsourced |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Testing Services | ||

| Inspection Services | |||

| Certification Services | |||

| By Sourcing Type | In-house | ||

| Outsourced | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the energy and utility testing, inspection certification market in 2025?

The energy and utility testing inspection certification market size stands at USD 12.62 billion in 2025.

What CAGR is projected for energy and utility testing, inspection certification market between 2025 and 2030?

Revenue is projected to advance at a 4.12% CAGR through 2030.

Which region leads demand for energy and utility testing, inspection certification market?

Asia-Pacific holds the largest 45.3% share and is growing the fastest at 4.8% CAGR.

Why are certification services growing faster than testing services?

Stricter ESG disclosure and IEC 62443 cyber rules require independent certifications, lifting segment growth to a 4.6% CAGR.

Who are the leading companies in this field?

SGS, Bureau Veritas, Intertek, and UL Solutions together account for roughly 60% of global revenue.

What role does digital-substation adoption play?

Migration to IEC 61850-based substations drives demand for software and cyber testing, creating recurring certification revenue.

Page last updated on: