Energy and Utilities Enterprise Content Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.36 Billion |

| Market Size (2031) | USD 2.72 Billion |

| Growth Rate (2026 - 2031) | 14.87% CAGR |

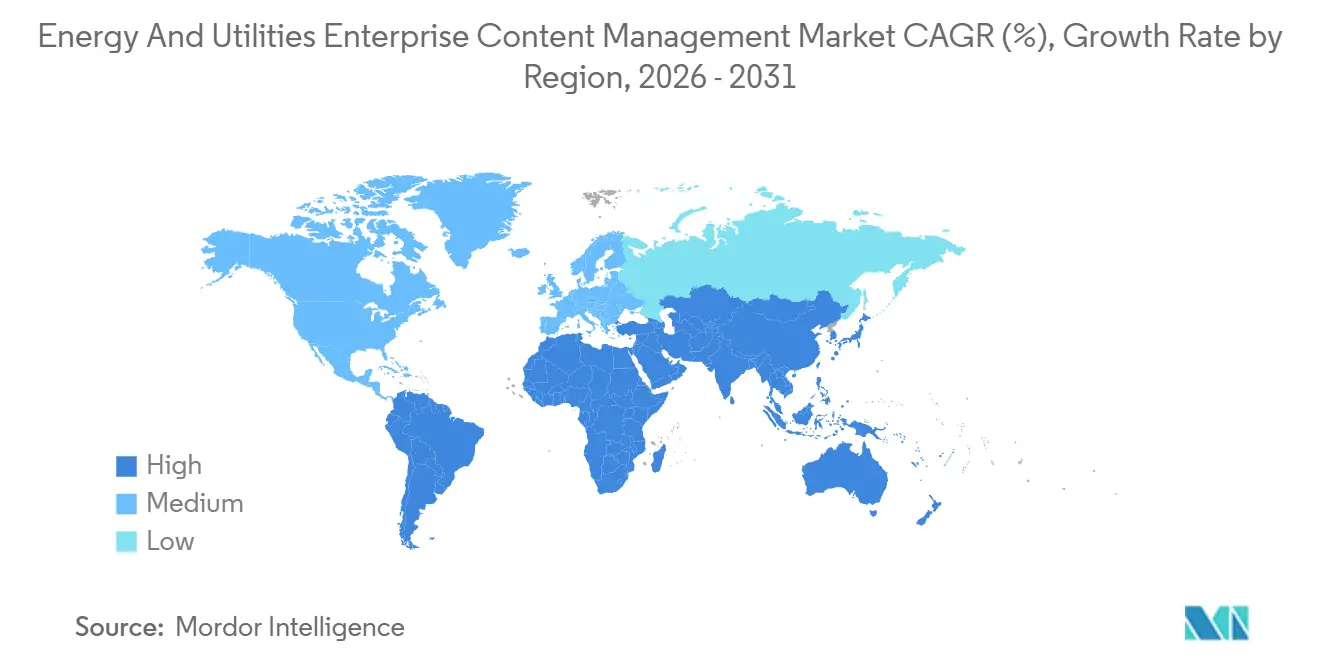

| Fastest Growing Market | Middle East and North Africa |

| Largest Market | North America |

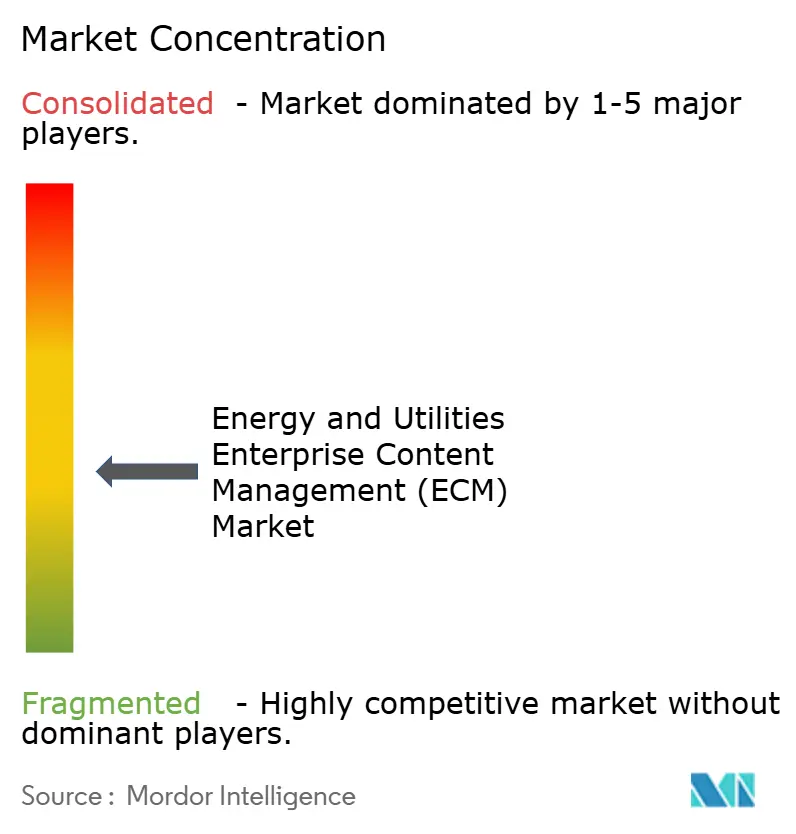

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Energy and Utilities Enterprise Content Management Market Analysis by Mordor Intelligence

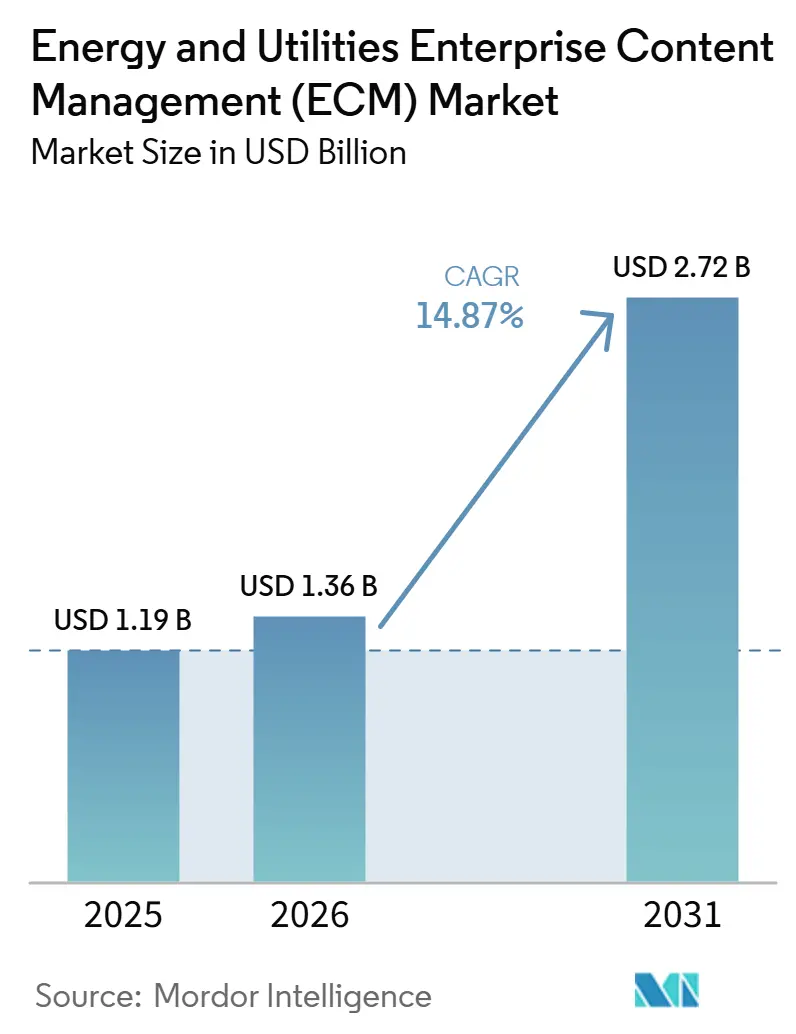

The energy and utilities enterprise content management market size is projected to be USD 1.19 billion in 2025, USD 1.36 billion in 2026, and reach USD 2.72 billion by 2031, growing at a CAGR of 14.87% from 2026 to 2031. The energy and utilities enterprise content management market is moving beyond document storage, as utilities, oil and gas operators, renewable developers, and related service providers now treat governed content as part of their operational infrastructure. Demand in the energy and utilities enterprise content management market is rising as grid modernization, renewable build-outs, and critical infrastructure oversight create larger volumes of engineering, safety, maintenance, and compliance records that must remain searchable and defensible. The energy and utilities enterprise content management market is also benefiting from the wider use of AI-ready retrieval tools, since field crews, project teams, and control room staff need faster access to approved manuals, procedures, and asset records under strict access controls. A clear opportunity in the energy and utilities enterprise content management market is taking shape around sovereign cloud, hybrid deployment, and OT-aware integration, where buyers want flexible architectures without weakening audit readiness or data control. Competitive activity in the energy and utilities enterprise content management market is therefore centered on deeper integration, workflow automation, and regulated cloud delivery, while migration complexity, metadata quality, and cybersecurity concerns continue to shape buying decisions.

Key Report Takeaways

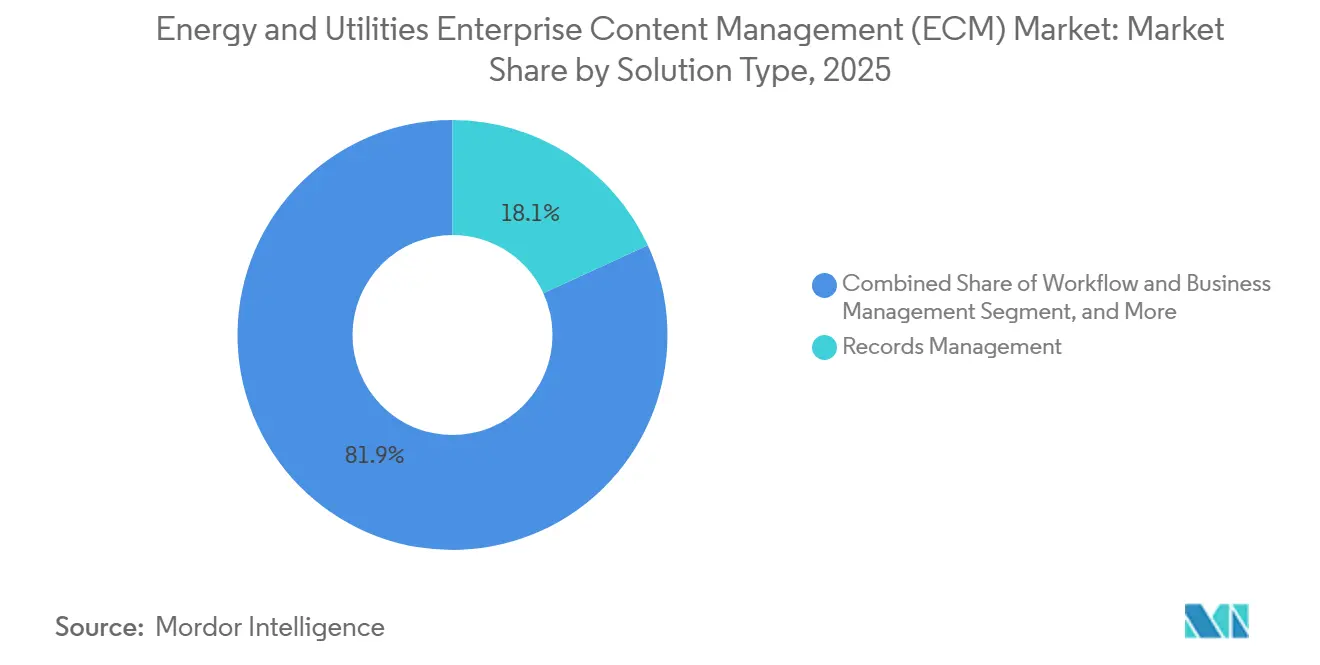

- By solution type, records management held 18.14% share in the energy and utilities enterprise content management market 2025, while workflow and business process management is forecast to expand at a 17.42% CAGR through 2031.

- By deployment mode, cloud accounted for 68.41% share in the energy and utilities enterprise content management market in 2025, while hybrid is projected to grow at a 17.83% CAGR through 2031.

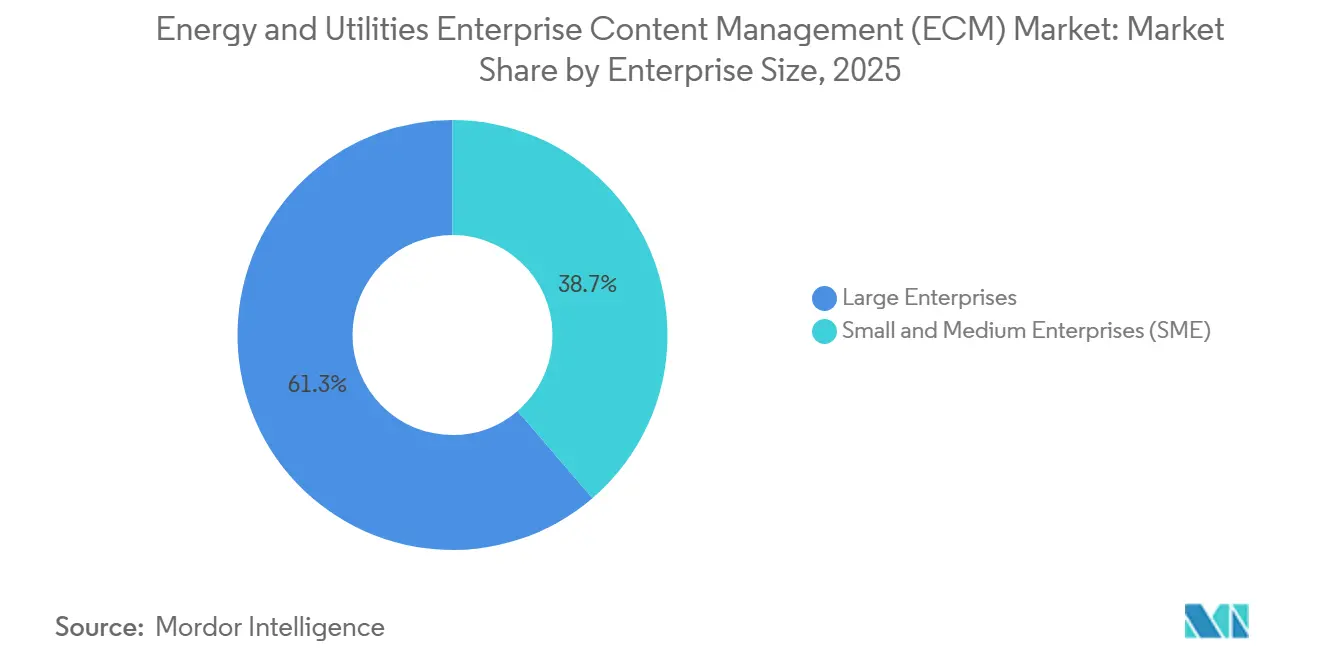

- By enterprise size, large enterprises held 61.28% share in 2025, while SMEs are projected to expand at a 17.64% CAGR through 2031.

- By end-user industry, electric utilities held 34.52% share in 2025, while renewable IPPs are projected to grow at an 18.91% CAGR through 2031.

- By geography, North America held 38.14% share in 2025, while the Middle East and Africa are projected to grow at an 18.24% CAGR through the energy and utilities enterprise content management market through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Energy and Utilities Enterprise Content Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Transformation of Utility Content Workflows | +3.2% | Global, strongest in North America and Western Europe | Short term (≤ 2 years) |

| Regulatory and Audit Readiness for Critical Infrastructure Records | +2.7% | North America and EU, spill-over to APAC core | Medium term (2-4 years) |

| AI Assisted Knowledge Retrieval for Field and Control Room Users | +2.1% | Global, led by North America, expanding to APAC | Short term (≤ 2 years) |

| Cloud Migration of Non-Core Content Repositories | +1.5% | Global, strongest in North America and Western Europe | Short term (≤ 2 years) |

| OT and IT Content Governance Convergence | +1.0% | North America and EU, spill-over to MEA | Medium term (2-4 years) |

| Lifecycle Digitization of Technical, Safety, and Maintenance Documentation | +0.7% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital Transformation of Utility Content Workflows

The energy and utilities enterprise content management market is gaining support from the steady removal of paper-based processes in control rooms, field service work, and project engineering. Utilities are digitizing maintenance logs, field visit records, and annotated drawings because these records still sit at the center of daily operations and compliance reviews. The pressure is stronger where experienced engineers are retiring, and companies need to preserve tacit knowledge before it is lost across plants, substations, and network programs. Buyers in the energy and utilities enterprise content management market are therefore looking past simple storage and focusing more on semantic search, structured tagging, and controlled reuse of approved content. This shift is widening the role of ECM from back-office record keeping to a broader knowledge and workflow layer across the enterprise.

Regulatory and Audit Readiness for Critical Infrastructure Records

Regulatory pressure remains one of the clearest growth supports for the energy and utilities enterprise content management market. FERC approved NERC Reliability Standard CIP-003-11 in March 2026, which broadens cybersecurity management controls to low-impact BES cyber systems and expands the population of assets that require structured records.[1]Federal Register, “Commission Approves CIP-003-11 Cyber Security Standard,” Federal Register, govinfo.gov NERC CIP-012-2, effective July 1, 2026, adds documentation and evidence requirements for communications between control centers. These changes mean compliance-driven procurement is no longer limited to large transmission operators because distribution utilities and smaller cooperatives also face heavier documentation burdens. Vendors that package audit evidence, retention control, and immutable workflow tracking into utility-ready formats are better placed than generic document management tools in regulated buying cycles.[2]North American Electric Reliability Corporation, “Standards, Compliance, and Enforcement Bulletin,” North American Electric Reliability Corporation, nerc.com

AI Assisted Knowledge Retrieval for Field and Control Room Users

The energy and utilities enterprise content management market is also advancing as utilities seek faster, safer access to approved procedures, manuals, permits, and incident records. This need is most visible in field operations and control rooms, where staff require the correct version of a document without sorting through folder-heavy repositories under time pressure. Research presented at AAAI in 2024 showed that agentic AI systems tuned to energy engineering content, with metadata filtering, hybrid retrieval, and reranking, improved document search accuracy and reduced hallucinations compared to more generic retrieval approaches.[3]AAAI Conference Proceedings, “Wikatoni: An Agentic AI System for Energy Engineering Workflows,” AAAI Conference Proceedings, doi.org That finding matters for the energy and utilities enterprise content management market because retrieval quality depends on governance of connectors, permissions, and metadata discipline, rather than on search alone. As a result, platforms that expose secure retrieval layers for operational users are becoming more relevant in evaluations tied to safety, uptime, and compliance.

Cloud Migration of Non-Core Content Repositories

The energy and utilities enterprise content management market is seeing continued movement toward cloud migration, though utilities are not applying one model to every repository. Many operators now separate highly sensitive operational records from administrative, archival, and project content, which supports a practical two-tier architecture across cloud, private infrastructure, and on-premises environments. OpenText announced in April 2026 that its partnership with S3NS would deliver sovereign cloud solutions, including Documentum Content Management with French data residency, for regulated operators that need tighter jurisdictional control.[4]OpenText, “OpenText and S3NS Partner to Deliver European Sovereign Cloud Solutions with Google Cloud,” OpenText Investor Relations, opentext.com This matters because the energy and utilities enterprise content management market increasingly depends on regional compliance fit rather than generic scalability or subscription pricing. Vendors that can support jurisdiction-specific cloud governance are gaining an edge where utilities operate across multiple regulatory environments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Repository Migration Complexity | -2.1% | Global, most acute in North America and Western Europe | Medium term (2-4 years) |

| Cybersecurity, Sovereignty, and Access Control Concerns | -1.7% | Global, especially EU and MEA | Long term (≥ 4 years) |

| Integration Friction Across OT, ERP, EAM, and ECM Platforms | -1.2% | Global, strongest in North America and APAC | Medium term (2-4 years) |

| Metadata Quality and Content Classification Gaps | -0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy Repository Migration Complexity

Legacy migration remains a significant barrier to the energy and utilities enterprise content management market, as many utilities hold decades of engineering, safety, inspection, and regulatory records in legacy repositories. Saudi Electricity Company’s SharePoint transformation involved nearly 40 TB of enterprise content across 12 business lines and more than 4,000 users, which shows the scale that even one large utility content program can reach. Volume is only one issue, because metadata lineage, document version history, and broken links to retired business systems often pose greater risks during migration. Utilities cannot accept degraded records that involve retention duties or compliance evidence, so migration planning becomes slower, more specialized, and more expensive. This keeps adoption selective in parts of the energy and utilities enterprise content management market where internal IT teams lack the budget or skills to perform large-scale repository cleanups.

Cybersecurity, Sovereignty, and Access Control Concerns

Cybersecurity and access control concerns continue to limit the pace of the energy and utilities enterprise content management market, especially where utilities need content access across both IT and OT environments. The basic challenge is that control system protection requires strict separation, while operational teams still need timely access to engineering records, procedures, and supporting documentation. ISO/IEC 27019:2024 reinforces the importance of energy-specific information security controls, raising the bar for content platforms seeking to serve regulated operators. The European Commission’s 2026 digital energy and AI roadmap also reflects a stronger policy focus on data governance in energy systems. Until vendors prove that permission-aware retrieval can respect network boundaries without cutting off operational knowledge access, adoption will continue to move first toward lower-risk administrative and project repositories before it reaches more sensitive operational records.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Records Management Stays Central While Workflow Demand Builds

Records management led the Energy and Utilities Enterprise Content Management market with 18.14% market share in 2025, while workflow and business process management is projected to grow at a 17.42% CAGR through 2031. This mix shows that the energy and utilities enterprise content management market still rests on compliance-heavy use cases, even as automation becomes more important. Records management remains the anchor because utilities, grid operators, and energy companies need retention control, defensible disposition, and traceable audit records for critical infrastructure documentation. That requirement is difficult to meet with generic file-sharing systems, especially when records must remain searchable and reviewable over long asset life cycles.

The faster rise of workflow and business process management shows that the energy and utilities enterprise content management market is shifting from passive storage toward governed process execution. Utilities increasingly want content to route approvals, support engineering change control, package compliance evidence, and document project milestones in real time. Document management and case management remain important because capital projects, contracts, permit files, and service issues all generate structured and unstructured records that need controlled access. Digital asset management and web content management serve narrower needs such as public disclosures, visualization assets, and customer-facing content, but they still complement broader governance programs. Procurement patterns now favor solutions that more tightly connect records, workflow, and document control, reducing the separation between compliance modules and operational content layers.

By Deployment Mode: Cloud Leads While Hybrid Expands on Sovereignty Needs

Cloud accounted for 68.41% of the Energy and Utilities Enterprise Content Management market size in 2025, while hybrid is forecast to expand at a 17.83% CAGR through 2031. The leading cloud position reflects strong uptake of software-as-a-service ECM for collaboration, project documentation, and historical repositories across the energy and utilities enterprise content management market. Cloud is attractive to organizations that want faster deployments, simpler upgrades, and easier access across distributed teams. It also benefits from vendor roadmaps that place AI functions, automation layers, and analytics capabilities more heavily in cloud-delivered environments.

Hybrid is growing faster because the energy and utilities enterprise content management market is not abandoning control in favor of one universal architecture. Utilities are keeping sovereignty-sensitive or OT-adjacent records in private environments while shifting administrative and archival content to commercial cloud platforms. OpenText’s April 2026 S3NS partnership reflects this demand by offering Documentum Content Management with strict French data residency for regulated operators. On-premises deployments still matter for some large transmission operators, nuclear generation settings, and markets with strict localization rules, but their relative share is easing as buyers seek more flexible deployment mixes. The result is a deployment pattern in which cloud remains the volume leader, while hybrid addresses the more complex and faster-growing needs of regulated utilities.

By Enterprise Size: Large Enterprises Hold the Base While SMEs Accelerate

Large enterprises held 61.28% of the Energy and Utilities Enterprise Content Management market size in 2025, while SMEs are projected to grow at a 17.64% CAGR through 2031. Large utilities, national grid operators, and major oil and gas companies continue to dominate spending because they manage very large document populations across sites, functions, and regulatory jurisdictions. These buyers also face more stringent compliance obligations and often require tailored support for asset management, engineering changes, and multi-entity reporting. That scale gives large enterprises a durable volume advantage in the energy and utilities enterprise content management market.

SMEs are expanding faster because smaller renewable developers, ESCOs, and distributed generation operators now face more formal governance expectations from financiers, regulators, and counterparties. These organizations previously relied more on general cloud storage, but permit files, project financing records, quality documents, and contract controls now require stronger versioning and audit support. M-Files launched M-Files for Contracts and M-Files for Quality in April 2026, demonstrating how vendors are packaging content governance into easier-to-adopt applications to achieve targeted business outcomes. This is compressing adoption timelines in the energy and utilities enterprise content management market because SME buyers can start with narrower, preconfigured use cases instead of full platform customization. As a result, the revenue base remains concentrated in large enterprises, but smaller energy companies with clearer governance needs increasingly shape incremental growth.

By End-User Industry: Electric Utilities Lead While Renewable IPPs Set the Pace

Electric utilities captured 34.52% of the Energy and Utilities Enterprise Content Management market share in 2025, while renewable IPPs are projected to grow at an 18.91% CAGR through 2031. Electric utilities lead because they generate large volumes of asset, outage, reliability, compliance, and workforce records across transmission and distribution networks. Longstanding NERC-CIP exposure has also pushed this group toward formalized record structures and repeatable evidence management. That has made utilities the most established buyer group within the energy and utilities enterprise content management market.

Renewable IPPs are growing faster because each solar, wind, storage, and distributed generation project creates permit, interconnection, PPA, engineering, and operations documentation that must stay current and auditable. Opdenergy selected Sitetracker in April 2026 to unify project, financial, and legal documentation across its global renewable portfolio, which highlights the push toward a single system of record in this segment. Oil and gas companies remain important users of ECM for engineering document control, HSE records, and regulatory submissions across dispersed operations. OpenText stated in August 2024 that Serica Energy deployed OpenText Content Cloud and Extended ECM for Engineering to strengthen governed engineering document management for long-life capital projects. Water utilities, ESCOs, and industrial prosumers remain smaller segments, but they are adding steady demand as environmental reporting, contract administration, and distributed energy governance become more documentation-intensive.

Geography Analysis

North America held a 38.14% share in 2025, making it the largest regional market for energy and utilities enterprise content management. The region’s lead reflects a long history of compliance with NERC-CIP, which has normalized structured record governance across many electric utilities in the United States and Canada. FERC’s March 2026 approval of CIP-003-11 and the current enforcement environment regarding CIP evidence have maintained high documentation discipline across critical infrastructure operators. NERC CIP-012-2 also strengthens the case for auditable records of communication security in utility operations. Buyers in this region are increasingly focused on consolidating siloed repositories, automating reporting workflows, and supporting AI-ready retrieval without weakening control.

Europe remains a strategically active part of the energy and utilities enterprise content management market, while the Asia-Pacific is developing through uneven but rising utility digitalization programs. The European Commission’s 2026 Strategic Roadmap for Digital Energy and AI supports stronger data governance foundations for smart energy services and enterprise AI. In Germany, EnBW adopted the Shareflex ECM platform in late 2024, with initial projects live in 2025 and a phased rollout of contract, document, and quality management modules across business units. TEAG completed its SAP S/4HANA Utilities cloud transformation in July 2026, which provides an integrated foundation for future content and data use across utility operations. Asia-Pacific is expanding more gradually, with adoption shaped by national utility modernization pace, grid expansion priorities, and renewable integration programs that increase engineering and compliance documentation volumes.

The Middle East and Africa are projected to grow at an 18.24% CAGR through 2031, making it the fastest-growing regional segment in the energy and utilities enterprise content management market. Growth there is tied to state-led energy diversification, large renewable project pipelines, and wider digital utility investment across GCC and African markets. The region is attracting attention because new infrastructure programs create large volumes of project, permit, engineering, and regulatory records that need stronger control from the outset. South America remains at an earlier stage, but utilities there are beginning to replace manual compliance and document-handling processes with more structured content environments as modernization programs advance.

Competitive Landscape

The energy and utilities enterprise content management market remains moderately fragmented, with global software vendors and mid-market specialists competing across different buyer profiles. OpenText Corporation, IBM Corporation, SAP SE, and Microsoft Corporation remain well placed in large utility accounts because buyers value integration with ERP, EAM, and broader enterprise systems. Their position is reinforced by the fact that utilities often prefer content platforms that can sit close to asset, finance, procurement, and service workflows. This gives established vendors an advantage in large and regulated deployments where switching costs can rise quickly. At the same time, the energy and utilities enterprise content management market still leaves room for specialists who focus on configurability, faster implementation, or narrower compliance use cases.

A major competitive theme in 2026 is cloud and ecosystem positioning. OpenText’s April 2026 partnership with S3NS shows how vendors are using sovereign cloud delivery to strengthen their relevance with regulated operators that need tighter jurisdictional control. Laserfiche launched its intelligent content management platform on AWS Marketplace in June 2026, reducing procurement friction for regulated buyers who already spend through AWS. M-Files also expanded its outcome-specific portfolio in April 2026 with applications for contracts and quality, which shows how vendors are targeting easier adoption paths for regulated documentation workloads.

Another point of competition in the energy and utilities enterprise content management market is the ability to support OT-aware governance instead of only office-centric content handling. Utilities are bringing engineered documents, maintenance history, and operational records closer together, which raises demand for permission-aware retrieval and stronger context across OT and IT boundaries. Academic work presented at AAAI 2024 showed that energy-tuned agentic AI architectures can improve retrieval quality compared to more generic search models, signaling a real threat to vendors that still depend on older discovery layers. Vendors that can connect governed retrieval, workflow automation, and utility-specific integration will be better placed in higher-value transmission, generation, and large project environments. The competitive field is therefore active, but no single supplier appears to control the energy and utilities enterprise content management market in a way that removes space for specialist growth or differentiated platform strategies.

Energy and Utilities Enterprise Content Management Industry Leaders

OpenText Corporation

Microsoft Corporation

International Business Machines Corporation

Oracle Corporation

Hyland Software, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: NERC's CIP-012-2 Reliability Standard (Cyber Security: Communications between Control Centers) took effect on July 1, 2026, imposing new documentation and evidence requirements on electric utilities managing inter-control-center communications. Utilities must now maintain auditable records of communication security configurations and incident detection procedures, directly expanding structured ECM procurement obligations in the transmission sector.

- July 2026: Thüringer Energie AG (TEAG) in Germany successfully completed its SAP S/4HANA Utilities cloud transformation, integrating SAP Service Cloud Version 2 and SAP Market Communication for Utilities, establishing the integrated content and data foundation required for future AI deployment across the utility's operations.

- June 2026: Laserfiche launched its intelligent content management platform on AWS Marketplace on June 2, 2026, enabling AWS customers in regulated industries, including energy and utilities, to procure Laserfiche's workflow automation capabilities through existing AWS cloud commitments, reducing procurement friction significantly.

- May 2026: Natuvion and IBM announced a strategic collaboration on May 21, 2026, to accelerate SAP transformation for energy utilities in Germany, jointly creating capacity to support up to 40 local and regional utility operators in migrating more than 10 million metering points to the SAP S/4HANA Utilities cloud platform.

Global Energy and Utilities Enterprise Content Management Market Report Scope

The energy and utilities enterprise content management market refers to the specialized ecosystem of software solutions and services designed to capture, manage, store, preserve, and deliver critical documents and operational data specific to the energy sector. This includes technologies such as document and records management, workflow and business process management, case management, and digital asset management, tailored to handle highly complex assets, such as engineering drawings, regulatory compliance files, safety inspections, and maintenance logs. Deployed on-premises, in the cloud, or in hybrid models, these solutions cater to organizations of all sizes across sub-sectors, including electric utilities, oil and gas, water utilities, and renewable independent power producers (IPPs). Driven by stringent regulatory compliance, asset lifecycle management, operational safety, and digital transformation in geographically dispersed environments, ECM solutions enable energy companies to streamline operations, mitigate risks, reduce downtime, and improve decision-making by transitioning from paper-based processes to digitized, intelligent content workflows.

The Energy And Utilities Enterprise Content Management Market Report is Segmented by Solution Type (Document Management, Records Management, Workflow and Business Process Management, Case Management, Digital Asset Management, Web Content Management, and Other Solutions), Deployment Mode (On-Premises, Cloud, and Hybrid), Enterprise Size (Small and Medium Enterprises (SME), and Large Enterprises), End-User Industry (Electric Utilities, Oil and Gas Companies, Water Utilities, Renewable Independent Power Producers (IPPs), Energy Service Companies (ESCOs), Industrial Prosumers, and Other End User Industry), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Document Management |

| Records Management |

| Workflow and Business Process Management |

| Case Management |

| Digital Asset Management |

| Web Content Management |

| Other Solutions |

| On-Premises |

| Cloud |

| Hybrid |

| Small and Medium Enterprises (SME) |

| Large Enterprises |

| Electric Utilities |

| Oil and Gas Companies |

| Water Utilities |

| Renewable Independent Power Producers (IPPs) |

| Energy Service Companies (ESCOs) |

| Industrial Prosumers |

| Other End User Industry |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Solution Type | Document Management | |

| Records Management | ||

| Workflow and Business Process Management | ||

| Case Management | ||

| Digital Asset Management | ||

| Web Content Management | ||

| Other Solutions | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| Hybrid | ||

| By Enterprise Size | Small and Medium Enterprises (SME) | |

| Large Enterprises | ||

| By End-User Industry | Electric Utilities | |

| Oil and Gas Companies | ||

| Water Utilities | ||

| Renewable Independent Power Producers (IPPs) | ||

| Energy Service Companies (ESCOs) | ||

| Industrial Prosumers | ||

| Other End User Industry | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2031 value for energy and utilities enterprise content management?

The sector is forecast to reach USD 2.72 billion by 2031, rising from USD 1.36 billion in 2026 at a CAGR of 14.87% over 2026 to 2031.

Which deployment model leads today?

Cloud leads with a 68.41% share in 2025, while hybrid is the faster-growing model with a 17.83% CAGR through 2031.

Which end-user group generates the most demand?

Electric utilities held the largest share at 34.52% in 2025 because they manage dense volumes of grid, asset, outage, and compliance records.

Which customer group is expanding the fastest?

Renewable IPPs are projected to grow at an 18.91% CAGR through 2031 as project pipelines create heavy volumes of permit, PPA, engineering, and Operation and Maintenance (O&M) documents.

Why is records management still the largest solution type?

Records management led with 18.14% share in 2025 because utilities and energy operators still need defensible retention, disposition, and audit support for critical infrastructure records.

Which region is growing the fastest?

The Middle East and Africa is expected to post the fastest CAGR at 18.24% through 2031, supported by utility digitalization and renewable infrastructure expansion.

Page last updated on: