EMEA Industrial Fats Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year Market Size (2025) | USD 58.81 Billion |

| Market Size (2026) | USD 61.29 Billion |

| Market Size (2031) | USD 79.08 Billion |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Europe |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

EMEA Industrial Fats Market Analysis by Mordor Intelligence

The EMEA Industrial Fats Market size was valued at USD 58.81 billion in 2025 and is estimated to grow from USD 61.29 billion in 2026 to reach USD 79.08 billion by 2031, at a CAGR of 5.23% during the forecast period (2026-2031). The market is driven by increasing demand for high-performance industrial fats that deliver superior functionality, consistent quality, and improved processing efficiency across modern manufacturing operations. Continuous advancements in refining, fractionation, blending, and interesterification technologies are enabling manufacturers to develop customized fat formulations with enhanced melting characteristics, oxidative stability, crystallization behavior, and thermal performance. The transition toward trans-fat-free formulations, sustainable raw materials, and certified sourcing practices is also accelerating innovation, encouraging manufacturers to invest in next-generation industrial fat solutions that comply with evolving regulatory and environmental standards.

Key Report Takeaways

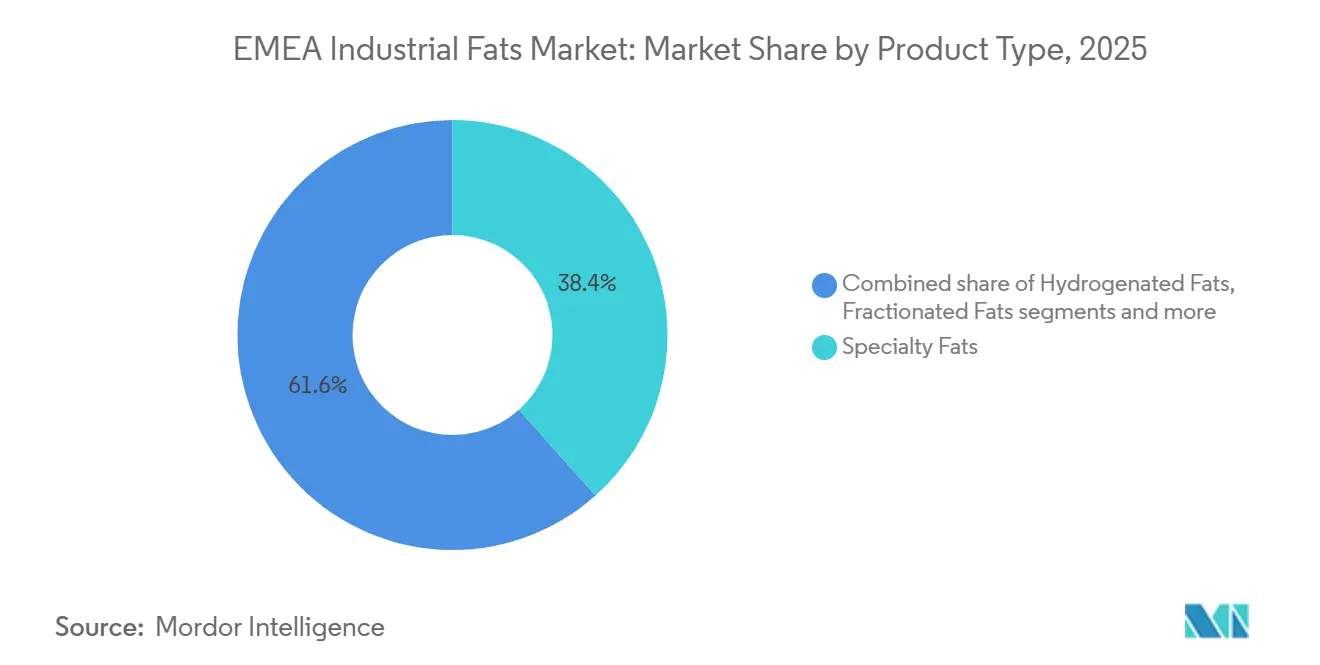

- By product type, specialty fats held a 38.41% revenue share of the EMEA industrial fats market in 2025; fractionated fats are forecast to expand at a 6.56% CAGR through 2031.

- By source, plant-based fats represented an 83.23% share in 2025; animal-based fats are projected to grow at a 6.91% CAGR through 2031.

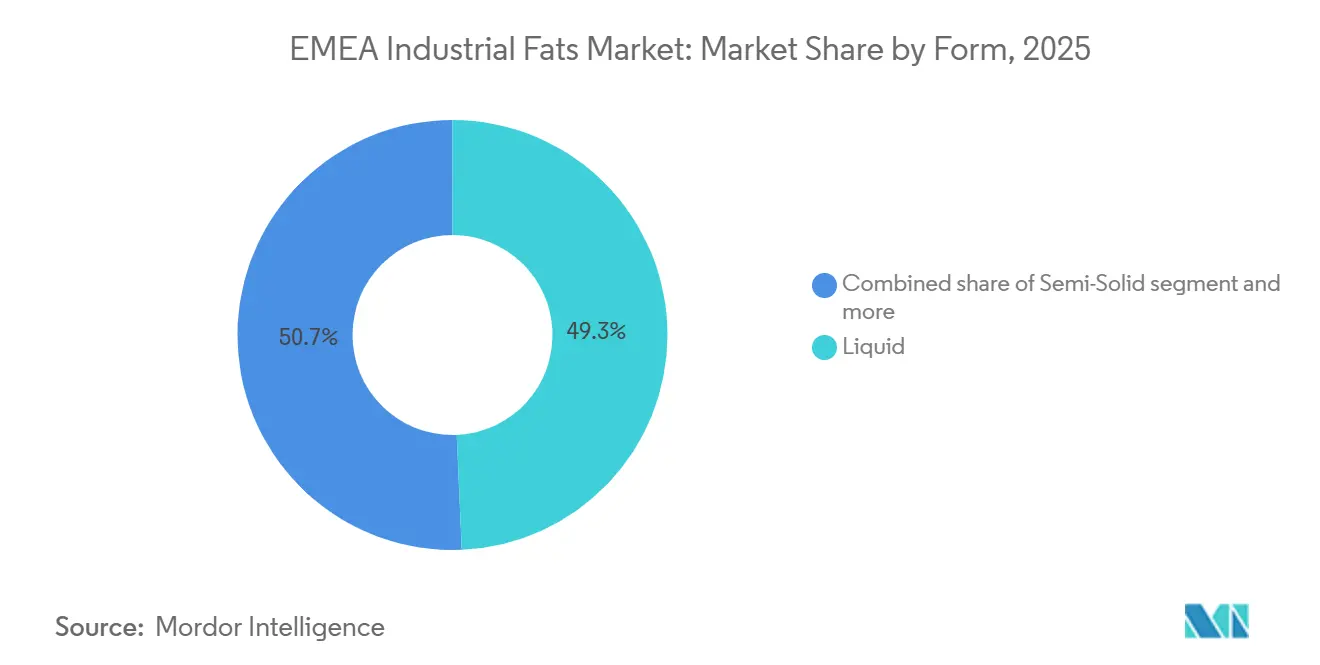

- By form, liquid fats accounted for a 49.32% revenue share in 2025 and are expected to remain the fastest-growing form, advancing at a 5.81% CAGR through 2031.

- By application, food processing captured a 31.23% share in 2025; biodiesel is anticipated to register the highest growth at a 6.54% CAGR through 2031.

- By geography, Europe commanded a 72.32% share of the EMEA industrial fats market in 2025; the Middle East and Africa are expected to post a 7.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

EMEA Industrial Fats Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in biodiesel and renewable fuel production | +1.5% | EU core (Germany, Netherlands, Belgium, France), MEA spill-over | Short term (≤ 2 years) |

| Increasing demand for sustainable and certified vegetable oils | +1.0% | Global, concentrated in EU (ISCC EU, RSPO) | Medium term (2–4 years) |

| Demand for processed and convenience foods | +0.9% | Western Europe, Gulf Cooperation Council | Medium term (2–4 years) |

| Growth in plant-based and vegan food manufacturing | +0.8% | Western Europe | Medium term (2–4 years) |

| Shift toward trans-fat-free and reformulated products | +0.6% | Europe-wide, post-Regulation (EU) 2019/649 | Short term (≤ 2 years) |

| Advancements in food processing technologies | +0.5% | EMEA processing hubs (Netherlands, Germany, Turkey) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in biodiesel and renewable fuel production

The expanding production of biodiesel and other renewable fuels is a major driver of the EMEA industrial fats market, as industrial fats serve as key feedstocks for biofuel manufacturing. Growing investments in renewable fuel production facilities and the increasing adoption of bio-based feedstocks are driving demand for vegetable- and animal-derived industrial fats with suitable conversion characteristics. Advancements in feedstock processing and fuel production technologies are improving conversion efficiency and expanding the use of industrial fats in renewable energy applications. For instance, according to the European Biodiesel Board, total EU-27 biodiesel and bioSAF production increased to 14.7 million metric tonnes in 2025, reflecting the continued expansion of renewable fuel manufacturing capacity across the region [1]Source: European Biodiesel Board, "EBB Statistical Report 2025-2026", ebb-eu.org. This growth in renewable fuel production is expected to strengthen long-term demand for industrial fats across the EMEA market.

Increasing demand for sustainable and certified vegetable oils

The growing preference for sustainably sourced and certified vegetable oils is driving the EMEA industrial fats market, as industrial manufacturers increasingly prioritize traceable raw materials that comply with environmental and sustainability requirements. Certified vegetable oils support responsible sourcing practices, enhance supply chain transparency, and help manufacturers meet evolving customer and regulatory expectations. This trend is encouraging producers to expand certified sourcing programs, strengthen traceability systems, and invest in sustainable refining and processing capabilities. For instance, FEDIOL, the EU vegetable oil and proteinmeal industry association, promotes responsible sourcing initiatives and supports the increased adoption of certified sustainable vegetable oils across the European vegetable oil value chain, reinforcing the transition toward sustainably produced industrial fats throughout the EMEA region.

Demand for processed and convenience foods

Rising demand for processed and convenience foods is a key driver of the EMEA industrial fats market. Industrial fats play an important role in improving texture, stability, mouthfeel, shelf life, and processing efficiency in large-scale food manufacturing. Food processors increasingly rely on specialized fat formulations to ensure consistent product quality, optimize production processes, and maintain functionality during storage and distribution. The expansion of convenience food manufacturing has increased the need for high-performance industrial fats that meet stringent quality and processing requirements. For instance, according to the Federal Statistical Office of Germany, the German convenience food processing industry generated approximately EUR 5.9 billion in revenue in 2025, reflecting the strong manufacturing base that supports demand for industrial fats across the region [2]Source: Federal Statistical Office of Germany, "Revenue in the convenience food manufacturing sector in Germany", destatis.de.

Growth in plant-based and vegan food manufacturing

The continued expansion of plant-based and vegan food manufacturing is a significant driver of the EMEA industrial fats market. Manufacturers increasingly rely on plant-derived fats to achieve the desired texture, structure, creaminess, melting behavior, and product stability in alternative formulations. Industrial fats improve processing efficiency, product consistency, and shelf life while delivering functional properties comparable to conventional ingredients. Advancements in lipid modification, fractionation, and blending technologies have enabled the development of customized plant-based fat systems with improved thermal stability, crystallization behavior, and oxidative resistance. Growing emphasis on clean-label formulations, sustainable ingredient sourcing, and product development is encouraging manufacturers to adopt plant-based industrial fats, supporting market growth across the EMEA region.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in vegetable oil raw material supply | -1.2% | Europe-wide (sunflower/rapeseed-heavy), MEA import-dependent markets | Short term (≤ 2 years) |

| Stringent regulations on fat composition and food safety | -0.8% | Europe-wide; GCC with phased convergence | Medium term (2–4 years) |

| Functional limitations of alternative fat ingredients | -0.5% | Europe-wide, particularly specialty fat applications | Long term (≥ 4 years) |

| Supply chain disruptions affecting specialty fat ingredients | -0.7% | Global supply affecting EMEA sourcing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in vegetable oil raw material supply

Fluctuations in the availability of vegetable oil feedstocks act as a significant restraint on the EMEA industrial fats market by creating uncertainty in raw material procurement and production planning. Industrial fats rely heavily on oils such as palm, sunflower, rapeseed, and soybean, making manufacturers vulnerable to supply disruptions caused by adverse weather conditions, crop diseases, geopolitical tensions, export restrictions, and logistics bottlenecks. Inconsistent raw material availability can affect production schedules, reduce operational efficiency, and increase the complexity of maintaining consistent product quality and long-term supply commitments. During periods of constrained supply, manufacturers may also face challenges in sourcing certified and traceable feedstocks, requiring alternative sourcing strategies or reformulation efforts that can further impact manufacturing efficiency and product consistency.

Stringent regulations on fat composition and food safety

Stringent regulations governing fat composition, product quality, and food safety represent a key restraint on the EMEA industrial fats market, as they increase compliance requirements for manufacturers. Regulatory frameworks covering trans-fat limits, contaminants such as 3-MCPD esters and glycidyl esters, labeling requirements, and quality standards require continuous monitoring, testing, and reformulation of industrial fat products. Manufacturers must invest in advanced refining technologies, quality assurance systems, and compliance processes to meet evolving standards while maintaining product functionality and consistency. These requirements increase production complexity, extend product development timelines, and raise operational costs, particularly for manufacturers supplying multiple markets with differing regulatory specifications across the EMEA region.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Specialty Fats Power Premium Applications, Fractionation Gains Dual-Use Traction

Specialty industrial fats held a 38.41% share of the EMEA industrial fats market in 2025, driven by their ability to deliver precise functional performance that conventional fats cannot consistently achieve. Manufacturers increasingly require fats with controlled melting behavior, oxidative stability, crystallization characteristics, viscosity, and thermal resistance to support standardized production processes and stringent product quality requirements. Continuous advancements in fractionation, interesterification, and lipid modification technologies have enabled the development of tailor-made fat systems with enhanced consistency, purity, and processing efficiency, allowing manufacturers to optimize production while minimizing formulation variability.

Fractionated fats are projected to register the fastest growth at a CAGR of 6.56% through 2031, driven by increasing demand for highly functional fat ingredients with consistent physical and chemical properties. Advances in dry and solvent fractionation technologies have enabled manufacturers to produce fats with precise melting profiles, improved crystallization behavior, enhanced oxidative stability, and superior processing performance without extensive chemical modification. These characteristics make fractionated fats increasingly attractive for manufacturers seeking greater formulation accuracy, product consistency, and production efficiency. Rising emphasis on clean-label formulations and reduced reliance on hydrogenation has further accelerated the adoption of naturally fractionated fats, as they offer targeted functionality while preserving the intrinsic properties of the original oil.

By Source: Plant-Based Dominates but Animal Fat Volumes Climb via Bioenergy

Plant-based sources accounted for 83.23% of the EMEA industrial fats market in 2025, owing to their broad availability, versatile functionality, and compatibility with modern industrial processing requirements. These feedstocks offer consistent quality, predictable fatty acid composition, and strong adaptability to refining, fractionation, blending, and interesterification processes, enabling manufacturers to produce fats with specific physical and performance characteristics. Their scalability and ability to support standardized production have made them the preferred raw material for large-volume industrial operations that require uniformity across manufacturing batches. Ongoing innovation in oil modification technologies has further improved the thermal stability, oxidative resistance, crystallization behavior, and storage performance of plant-derived fats, expanding their suitability for demanding industrial applications.

Animal-based fats are projected to register the fastest growth at a CAGR of 6.91% through 2031, driven by increasing efforts to maximize the value of by-products generated from livestock processing and strengthen circular economy practices across industrial value chains. Advances in rendering technologies, purification methods, and quality control systems have improved the consistency, safety, and industrial performance of animal-derived fats, making them more suitable for high-value manufacturing applications. Their high energy density, favorable lubrication characteristics, and unique fatty acid composition offer functional advantages that are difficult to replicate with some alternative feedstocks. Rising emphasis on resource efficiency and waste reduction is also encouraging greater utilization of animal-derived materials as industrial inputs rather than disposal streams.

By Form: Liquid Fats Lead Volume and Growth Simultaneously

Liquid fats accounted for 49.32% of the EMEA industrial fats market by form in 2025 and are projected to remain the fastest-growing form, registering a CAGR of 5.81% through 2031. Their dominant position is supported by superior handling efficiency, ease of storage and transportation, and seamless integration into continuous industrial manufacturing processes. Liquid fats enable precise dosing, rapid mixing, and uniform distribution during production, reducing processing complexity while improving operational efficiency. Their pumpability and compatibility with automated processing systems minimize material losses and downtime, making them well suited for large-scale industrial operations.

Semi-solid fats occupy a significant position in the EMEA industrial fats market due to their balanced functional characteristics, combining the stability of solid fats with the workability of liquid fats. Their plastic consistency enables good spreadability, controlled crystallization, and uniform structural properties, making them well suited for industrial processes requiring precise texture and consistency. Solid fats remain an essential form within the market owing to their structural integrity, high melting point, and oxidative stability. Their rigid crystalline structure provides enhanced durability during storage, transportation, and high-temperature industrial processing, reducing the risk of deformation or quality deterioration.

By Application: Food Processing Anchors Revenue; Biodiesel Reshapes the Growth Curve

Food processing accounted for 31.23% of the EMEA industrial fats market in 2025, driven by consistent demand for functional fats that enhance manufacturing efficiency, product consistency, and processing performance. Industrial fats are essential for improving texture, structural stability, moisture retention, and oxidative stability during large-scale production, enabling manufacturers to maintain uniform quality across high-volume processing operations. Advances in fractionation, blending, and enzymatic interesterification technologies have enabled the development of specialized fat systems with precise melting profiles and improved functional characteristics, supporting increasingly complex manufacturing requirements. According to the Government of the United Kingdom, the food and drink sector employed approximately 3.7 million people in 2025, making it one of the largest manufacturing ecosystems in the region. This scale reinforces the sustained demand for industrial fat ingredients across food production value chains[3]Source: Government of the United Kingdom, "Food Chain", gov.uk. Biodiesel is projected to register the fastest growth at a CAGR of 6.54% through 2031, driven by the increasing use of renewable lipid feedstocks in fuel production and a growing emphasis on low-carbon energy solutions. Industrial fats are gaining wider adoption as feedstocks due to their favorable conversion characteristics, high energy content, and compatibility with established biodiesel manufacturing processes. Advances in feedstock pretreatment, transesterification technologies, and refining processes are improving production efficiency, fuel quality, and feedstock utilization, making industrial fats more viable for large-scale biodiesel production. A growing focus on resource efficiency, circular economy practices, and the use of renewable raw materials is further supporting the expansion of industrial fat usage in biofuel manufacturing.

Geography Analysis

Europe accounted for 72.32% of the EMEA industrial fats market in 2025, supported by its well-developed industrial processing ecosystem, advanced refining capabilities, and established value chain for vegetable and animal fats. The region benefits from extensive infrastructure for refining, fractionation, hydrogenation, blending, and specialty fat production, enabling manufacturers to supply high-quality industrial fats with consistent functional characteristics. Strong regulatory frameworks governing food safety, renewable raw materials, product quality, and sustainability have encouraged continuous innovation in fat processing technologies. The presence of integrated supply chains and mature downstream manufacturing industries has further reinforced Europe's position in industrial fat production and consumption.

The Middle East and Africa is projected to register the fastest growth at a CAGR of 7.23% through 2031, supported by expanding industrialization, increasing investments in downstream processing industries, and growing production capacity for bio-based materials. Continuous development of refining infrastructure, oleochemical manufacturing, renewable fuel facilities, and industrial processing capabilities is creating strong demand for industrial fats across the region. Improvements in logistics networks, processing technologies, and regional supply chains are further enhancing manufacturing efficiency, while increasing emphasis on industrial diversification and domestic value addition continues to drive market expansion.

The overall EMEA industrial fats market is benefiting from ongoing technological advancements in lipid processing, increasing adoption of sustainable and renewable feedstocks, and growing demand for customized fat solutions with enhanced functional properties. Manufacturers are investing in advanced refining, fractionation, and fat modification technologies to improve product quality, operational efficiency, and regulatory compliance. Stronger sustainability initiatives, greater traceability across raw material supply chains, and continuous innovation in industrial fat formulations are supporting long-term market development, enabling the region to strengthen its position as a key global hub for industrial fat production and consumption.

Competitive Landscape

The EMEA industrial fats market is moderately consolidated, with major manufacturers competing through integrated raw material sourcing, advanced refining capabilities, broad product portfolios, and long-term supply agreements with industrial customers. Market participants focus on securing reliable supplies of vegetable and animal feedstocks through diversified sourcing networks and strategic procurement partnerships to ensure uninterrupted production and consistent product quality. Strong supply chain integration from raw material procurement and refining to processing and distribution—enables manufacturers to optimize operational efficiency, reduce lead times, and respond quickly to evolving industrial requirements. Companies including Cargill, Incorporated, Archer Daniels Midland Company, Bunge Limited, Wilmar International Limited, and AAK AB maintain competitive positions through extensive processing infrastructure and comprehensive industrial fats portfolios.

Competition is increasingly centered on technological innovation and the ability to deliver customized fat solutions with precise functional characteristics. Manufacturers continue to invest in advanced refining, fractionation, blending, and enzymatic interesterification technologies to improve melting profiles, oxidative stability, crystallization behavior, purity, and overall product performance. Digital process monitoring, automated production systems, quality assurance technologies, and advanced analytical capabilities are further enhancing manufacturing efficiency while ensuring consistent product specifications. These technological advancements enable suppliers to develop specialized industrial fats that meet increasingly stringent performance, sustainability, and regulatory requirements across multiple industrial applications.

Customer formulation support and technical collaboration represent another key competitive differentiator. Leading companies work closely with industrial customers to develop application-specific fat formulations that improve processing efficiency, product functionality, and manufacturing consistency. Dedicated innovation centers, technical service teams, pilot-scale testing facilities, and formulation expertise allow suppliers to optimize fat compositions for specific production requirements while accelerating product development cycles. In parallel, companies are strengthening sustainability initiatives through certified raw material sourcing, enhanced traceability systems, responsible procurement programs, and investments in low-carbon manufacturing processes, further reinforcing their long-term competitiveness within the EMEA industrial fats market.

EMEA Industrial Fats Industry Leaders

-

Cargill, Incorporated

-

Archer Daniels Midland Company

-

Bunge Limited

-

Wilmar International Limited

-

AAK AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: AAK, a specialty vegetable fat and oil producer, has announced the launch of ILLEXAO EN 10, a new cocoa butter equivalent for enrobed applications that enhances performance and formulation flexibility.

- September 2025: Nourish Ingredients has launched its specialty fats and precision fermentation technology into the European food manufacturing market, with the establishment of a global commercial hub in Leiden, the Netherlands.

EMEA Industrial Fats Market Report Scope

Industrial fats typically refer to artificially manufactured fats created on a large scale for food production, primarily trans fats and interesterified fats. The EMEA industrial fats market is segmented by product type, source, form, application, and geography. Based on product type, the market is segmented into specialty fats, hydrogenated fats, fractionated fats, blended fats, and others. Based on source, the market is segmented into plant-based and animal-based. Based on form, the market is segmented into liquid, semi-solid, and solid. Based on application, the market is segmented into food processing, biodiesel, oleochemicals, surfactants and detergents, lubricants and greases, cosmetics and personal care, animal feed, and pharmaceuticals. Based on geography, the market is segmented into Europe and Middle East and Africa. For each segment, the market sizing and forecast have been done based on the value (in USD million).

| Specialty Fats |

| Hydrogenated Fats |

| Fractionated Fats |

| Blended Fats |

| Others |

| Plant-Based |

| Animal-Based |

| Liquid |

| Semi-Solid |

| Solid |

| Food Processing |

| Biodiesel |

| Oleochemicals |

| Surfactants and Detergents |

| Lubricants and Greases |

| Cosmetics and Personal Care |

| Animal Feed |

| Pharmaceuticals |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Specialty Fats | |

| Hydrogenated Fats | ||

| Fractionated Fats | ||

| Blended Fats | ||

| Others | ||

| By Source | Plant-Based | |

| Animal-Based | ||

| By Form | Liquid | |

| Semi-Solid | ||

| Solid | ||

| By Application | Food Processing | |

| Biodiesel | ||

| Oleochemicals | ||

| Surfactants and Detergents | ||

| Lubricants and Greases | ||

| Cosmetics and Personal Care | ||

| Animal Feed | ||

| Pharmaceuticals | ||

| By Geography | Europe | United Kingdom |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving growth in EMEA industrial fats demand through 2031?

The main drivers are rising biodiesel and SAF feedstock demand under EU policy, ongoing food reformulation after trans fat limits, and expanding processed food manufacturing across Europe and MEA.

How large is the EMEA industrial fats space in 2026 and where is it headed?

The EMEA industrial fats market stood at USD 61.29 billion in 2026 and is forecast to reach USD 79.08 billion by 2031 at a 5.23% CAGR.

Which product category leads revenue in this space?

Specialty fats led in 2025 with 38.41% share because they are widely used in confectionery, bakery fillings, infant nutrition, and dairy-analogue products.

Which end use is growing the fastest across the region?

Biodiesel is the fastest-growing application with a projected 6.54% CAGR through 2031, supported by stronger renewable fuel demand across the EU.

Page last updated on: