Electroporation Instruments Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

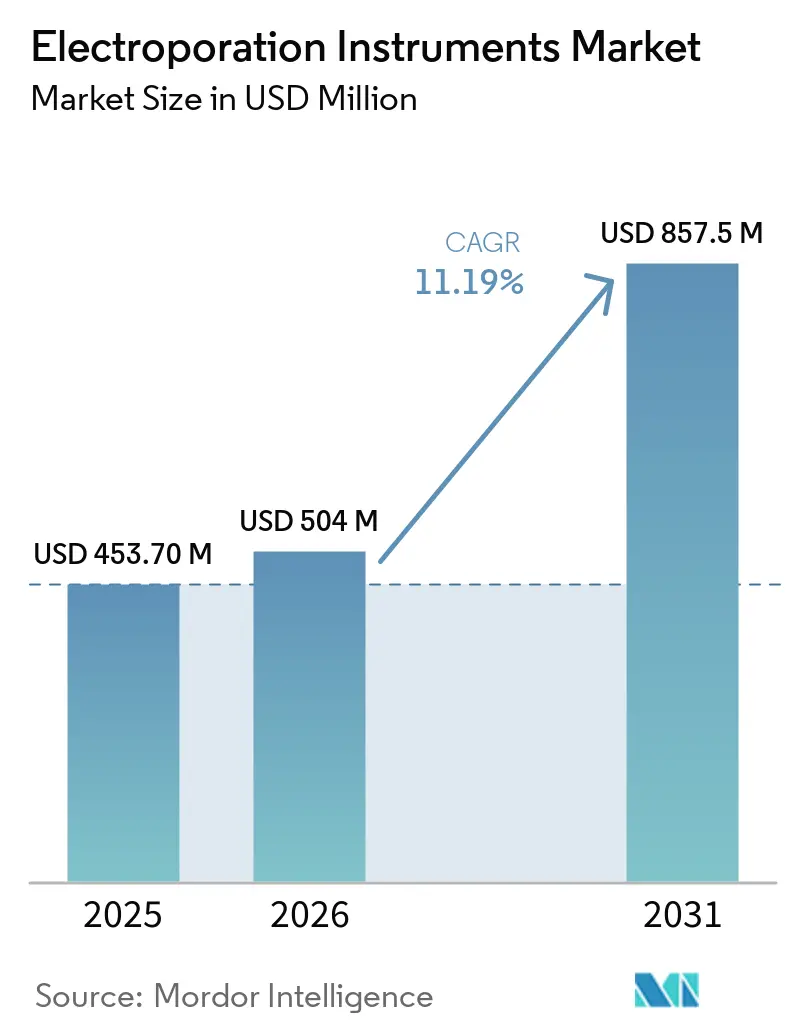

| Market Size (2026) | USD 504 Million |

| Market Size (2031) | USD 857.5 Million |

| Growth Rate (2026 - 2031) | 11.19% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electroporation Instruments Market Analysis by Mordor Intelligence

The Electroporation Instruments Market size is expected to grow from USD 453.70 million in 2025 to USD 504 million in 2026 and is forecast to reach USD 857.5 million by 2031 at 11.19% CAGR over 2026-2031.

The pivot from viral vectors toward non-viral transfection underpins this expansion as sponsors look to mitigate immunogenicity risks, shorten manufacturing timelines, and simplify regulatory filings. Heightened demand for good manufacturing practice (GMP) electroporation platforms in cell and gene therapy facilities, together with clinical validation of intradermal and intratumoral delivery, is keeping capital expenditure concentrated among biopharma companies and contract development and manufacturing organizations (CDMOs). Instrument makers are responding with closed-system, high-throughput designs that integrate real-time analytics and electronic-records compliance, thereby removing labor bottlenecks and improving batch reproducibility. North America supplies the largest customer base today, yet Asia-Pacific offers the fastest incremental growth as Japan, India, and China build greenfield CDMO capacity and accelerate approvals for allogeneic chimeric-antigen-receptor T-cell (CAR-T) therapies.

Key Report Takeaways

- By instruments, the total electroporation system accounted for 46.89% of the market share in 2025. However, the eukaryotic electroporation system is expected to grow at 12.53% CAGR by 2031.

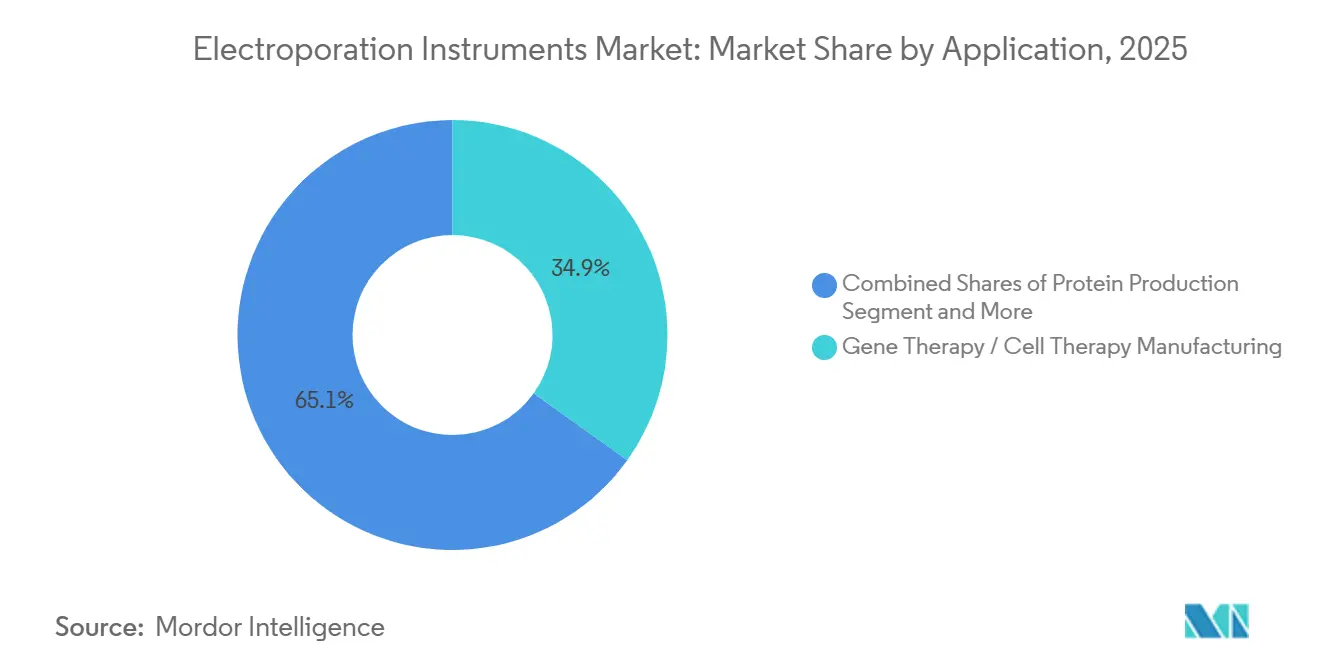

- By application, gene therapy and cell therapy manufacturing led the electroporation instruments market with 34.89% market share in 2025 and is projected at a 11.9% CAGR between 2026 and 2031.

- By end users, CDMOs recorded the fastest end-user expansion at a 12.6% CAGR through 2031, while biotechnology and pharmaceutical companies held 42.89% of 2025 revenue.

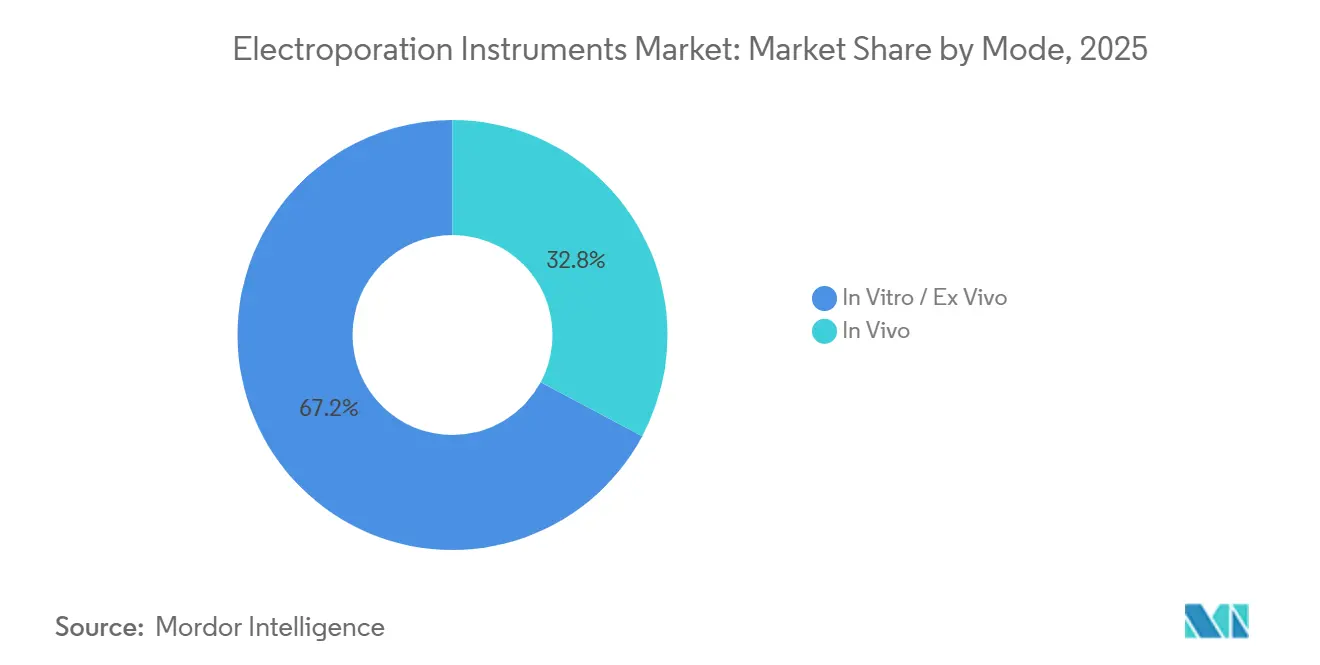

- By mode, In vitro and ex vivo systems accounted for 67.19% of 2025 revenue, whereas in vivo platforms are projected to advance at a 12.45% CAGR over 2026-2031.

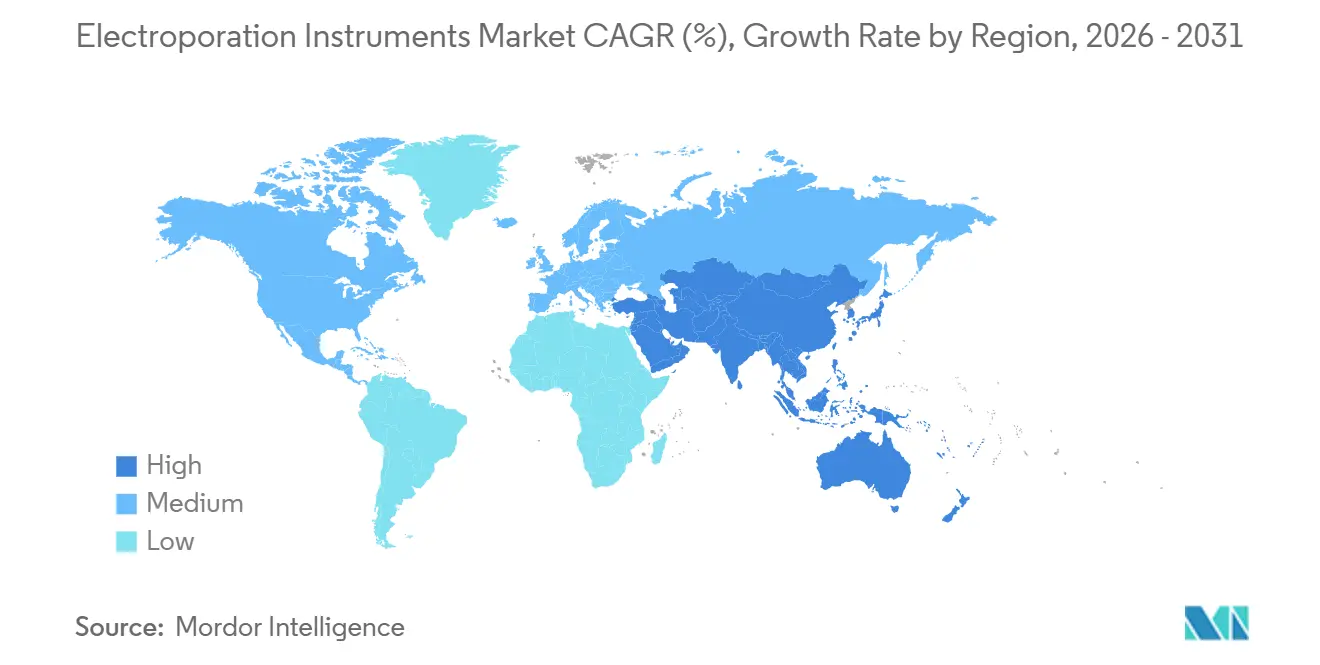

- By geography, North America captured 38.19% of global revenue in 2025, but Asia-Pacific is set to post the highest regional CAGR of 11.93% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electroporation Instruments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to non-viral delivery for CGT and gene editing | +2.1% | Global, with APAC CDMO acceleration | Medium term (2–4 years) |

| Expansion of electrochemotherapy (ECT) and IRE in clinical oncology | +1.8% | North America & EU core, spill-over to GCC | Medium term (2–4 years) |

| High-throughput and automated electroporation platforms in GMP | +2.5% | Global, led by North America & Japan | Short term (≤ 2 years) |

| In vivo DNA/RNA vaccine delivery and immunotherapy use-cases | +1.6% | North America, EU, APAC clinical-trial hubs | Long term (≥ 4 years) |

| FDA Master File-enabled acceleration for flow electroporation | +1.3% | United States | Short term (≤ 2 years) |

| Public biodefense funding catalyzing in vivo EP devices | +0.9% | United States, EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift to Non-Viral Delivery for CGT and Gene Editing

Transposon-mediated gene integration eliminates the immunogenicity and insertional-mutagenesis concerns associated with lentiviral or adeno-associated viral vectors, making electroporation central to the transition toward scalable allogeneic CAR-T platforms. Closed-system flow electroporators now process up to 200 billion cells per batch, a throughput unattainable with legacy cuvette designs. ISO 13485-certified devices accelerate notified-body reviews and facilitate cross-reference of Device Master Files in investigational new drug (IND) applications, compressing chemistry-manufacturing-controls (CMC) timelines by 4-6 months. The growing availability of Master Files at the FDA further tilts sponsor preference toward electroporation, as validation data can be leveraged across programs [1]U.S. Food and Drug Administration, “CMC Information for Human Gene Therapy INDs,” fda.gov. Collectively, these factors lift procurement budgets among vertically integrated biopharma firms and CDMOs alike.

Expansion of Electrochemotherapy and IRE in Clinical Oncology

Late-2024 FDA clearance for the NanoKnife system expanded irreversible electroporation beyond investigational use, offering prostate-cancer patients nerve-sparing treatment with 84% disease-free status at 12 months [2]AngioDynamics, “PRESERVE Multicenter Trial Outcomes,” ir.angiodynamics.com. Scandinavian ChemoTech secured an Indian import license in March 2026, unlocking a large price-sensitive oncology pool and highlighting the modality’s accessibility in resource-constrained settings. Ongoing randomized trials in Denmark may reduce bleomycin doses by 50%, lowering chemotherapy costs per cycle. Veterinary oncology provides a parallel revenue stream: more than 3,000 treatments have been completed globally, validating safety and efficacy in large animals and reducing translational risk to human indications. Regulatory pathways under the FDA’s 510(k) process and adaptive European frameworks shorten time-to-market for new indications.

High-Throughput and Automated Electroporation Platforms in GMP

Lights-out manufacturing addresses a critical labor bottleneck in autologous therapies. Automated systems integrated with robotic liquid handling cut operator time from 6–8 hours to under 90 minutes per patient lot. Japanese CDMOs have begun installing these platforms to scale output to more than 1,000 CAR-T lots annually, positioning Asia-Pacific as an emerging export hub. Real-time impedance monitoring now adjusts pulse parameters mid-process, improving batch-to-batch coefficient of variation from 18% to below 8%. Integration of 21 CFR Part 11 compliant audit trails satisfies electronic records requirements in both the United States and Europe. These performance gains justify premium pricing for next-generation electroporation instruments despite downward pressure on CDMO service margins.

In Vivo DNA/RNA Vaccine Delivery and Immunotherapy Use-Cases

The CELLECTRA 2000 device has administered roughly 19,000 doses across 6,000 clinical-trial subjects with no serious device-related adverse events, and a rolling BLA for INO-3107 could yield the first U.S. approval of an electroporation-delivered therapeutic vaccine by mid-2026. Phase 1b data from a Lassa fever study in Ghana showed robust CD8+ responses, confirming immunogenicity in low-infrastructure environments.

Competing delivery modalities still face tolerability hurdles: pain scores average 4.2 out of 10, necessitating topical anesthesia protocols that increase procedure complexity. Nevertheless, federal biodefense funding and the ability to bypass cold-chain logistics keep stakeholder interest alive. If Priority Review is granted, successful commercialization may unlock a follow-on pipeline of electroporation-enabled vaccines for endemic and emerging pathogens.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cell viability and cytotoxicity constraints at scale | -1.4% | Global | Medium term (2–4 years) |

| Strong competition from LNPs/viral vectors for in vivo delivery | -1.7% | North America & EU, emerging in APAC | Short term (≤ 2 years) |

| EU MDR compliance burden elongating time-to-market | -1.1% | Europe | Short term (≤ 2 years) |

| Patient pain/muscle contractions necessitating anesthesia in vivo | -0.6% | Global, acute in clinical-trial settings | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Cell Viability and Cytotoxicity Constraints at Scale

Electroporation triggers caspase-mediated apoptosis in modified cells when voltage gradients exceed 1,200 V/cm or pulse durations surpass 10 ms. Every percentage point of viability lost translates into dose yield reductions, a critical issue for allogeneic CAR-T batches exceeding 200 billion cells. Mechanical transfection alternatives post 92% viability but lack industrial throughput capacity. Process tweaks—lower buffer ionic strength, chilled cuvettes, extended recovery—can recover 5-8 percentage points yet necessitate full GMP revalidation, adding half a year to technology-transfer schedules. Capital-intensive retrofits with impedance sensors remain limited to roughly one-third of the installed base, prolonging exposure to yield variability risk.

Strong Competition from LNPs and Viral Vectors for In Vivo Delivery

A 2024 study reported 2.3-fold higher CD8+ T-cell responses with LNP-encapsulated DNA compared with electroporation-delivered plasmids in murine models. The mRNA-LNP manufacturing ecosystem can fill more than 3 billion doses annually, dwarfing global electroporation capacity. Viral vectors still feature in about 70% of FDA-approved gene therapies, offering a clearer regulatory precedent and established supply chains. Device capital costs of USD 80,000–250,000 plus single-use chambers challenge cost-of-goods calculations for large-volume vaccine programs. Consequently, electroporation’s commercial sweet spot remains in local tumor ablation and intradermal therapeutic vaccines rather than mass prophylaxis.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Gene Therapy Manufacturing Anchors Growth

The electroporation instruments market for gene and cell therapy manufacturing accounted for 34.89% of 2025 revenue and is projected to expand at a 11.9% CAGR between 2026 and 2031. Transition from autologous to allogeneic workflows demands reproducible, high-throughput transfection conditions, uniquely met by flow-electroporation systems that handle 200-billion-cell batches without open handling steps. Automated electroporation integrated in single-use, closed cartridges lowers labor input and reduces contamination risk, helping CDMOs meet tighter release timelines written into milestone-based clinical supply contracts. Electrochemotherapy for cutaneous lesions and irreversible electroporation for solid tumors represent mature niches that contribute long-tail consumable sales, with India’s 2026 regulatory clearance for IQwave exemplifying cost-conscious emerging-market traction.

Secondary applications, such as transient protein production, benefit from stable titers above 3 g/L using transposon-enabled electroporation, enabling bioreactor runs beyond 60 generations. In vivo DNA and RNA vaccine delivery remains small in revenue terms yet strategically significant; a potential INO-3107 approval would de-risk broader oncology and infectious-disease pipelines. Biomedical research continues to provide steady, albeit lower-margin, instrument demand; however, commodity cuvettes from Asian suppliers are compressing prices by roughly 12% relative to 2023 levels, prompting established brands to migrate laboratories toward GMP-ready upgrades.

By End User: CDMOs Drive Outsourcing Wave

Biotechnology and pharmaceutical companies retained the largest 42.89% revenue share in 2025, reflecting in-house GMP builds aimed at safeguarding proprietary cell-engineering protocols. Yet CDMOs are set to post the fastest 12.6% CAGR through 2031 as sponsors pivot to asset-light development strategies that defer capital expenditure until late-phase trials. Japanese, Indian, and Chinese service providers have announced multi-billion-cell capacity expansions that combine automated electroporation with viral-vector production under single-contract umbrellas, reducing technology-transfer friction for global clients.

Hospitals and specialty clinics represent a smaller, high-growth channel, fueled by the adoption of electrochemotherapy and irreversible electroporation systems for nerve-sparing oncology procedures, reimbursed under new Current Procedural Terminology (CPT) codes. Academic and research institutes have lengthened upgrade cycles to 8-10 years, tempering short-term unit sales but furnishing a conversion pipeline for GMP-compliant replacements.

By Mode: In Vivo Platforms Gain Clinical Traction

In vitro and ex vivo platforms commanded 67.19% revenue in 2025 owing to their entrenched role in CAR-T manufacturing, yet in vivo systems will grow faster at a 12.45% CAGR to 2031 as regulatory milestones accrue. Priority Review for INO-3107 could catalyze hospital adoption of intradermal devices by mid-2026, demonstrating that electroporation can combine outpatient tolerability with therapeutic efficacy. On the oncology front, NanoKnife’s microsecond-pulse IRE preserves neurovascular bundles and yields favorable continence and sexual-function scores, expanding urology center installations from under 50 in 2023 to around 150 by early 2026.

Ex vivo innovation continues as robotics shrinks hands-on time to under 90 minutes, improving consistency and enabling simultaneous processing of multiple patient lots. Device Master Files at the FDA simplify validation for closed systems, giving ex vivo platforms a compliance edge even as in vivo indications broaden.

By Instrument: Eukaryotic Systems Capture GMP Migration

Eukaryotic electroporation platforms accounted for 46.89% of the electroporation instruments market share in 2025 and are projected to advance at a 12.53% CAGR through 2031, markedly faster than legacy “total” systems that combine bacterial and mammalian modes. This growth reflects sponsor demand for GMP-validated instruments engineered around mammalian-cell pulse windows of 200–500 V/cm and 1–5 ms, parameters that deliver more than 80% CAR-positive yields while curbing viral-vector use by roughly 40% and lowering cost of goods sold for autologous CAR-T workflows. Lonza’s 4D-Nucleofector LV Unit PRO and MaxCyte’s ExPERT GTx now process up to 200 billion suspension T cells per closed-system batch, a throughput ceiling that dwarfs cuvette-based total systems capped near 10 billion cells and burdened by open-handling contamination risk.

Total and microbial electroporation systems continue to serve academic protein-production and synthetic-biology workflows, yet margin compression is intensifying as low-cost Asian entrants undercut incumbents on price. Harvard Bioscience’s 2025 U.S. distribution deal with Fisher Scientific bundles the BTX ECM 830 and Gemini X2 alongside Thermo Fisher reagents, a cross-sell tactic aimed at defending installed-base share while nudging researchers toward GMP-ready upgrades.

Geography Analysis

North America accounted for 38.19% of global revenue in 2025, buoyed by National Institutes of Health grants for non-viral delivery platforms and by clear CBER guidance on Device Master Files. Distribution agreements that place electroporation instruments alongside established reagent catalogs have widened the sales reach into academic labs, enabling upgrades to GMP-compliant systems. Clarity around reimbursement for irreversible electroporation has underpinned a rapid increase in NanoKnife placements in U.S. urology suites.

Europe’s growth remains dampened by Medical Device Regulation (MDR) bottlenecks that double conformity-assessment timelines and push some suppliers to prioritize North American launches. Notified-body capacity constraints have extended approval cycles to 24-30 months, favoring incumbents with dedicated regulatory teams and encouraging consolidation among smaller vendors. Despite these hurdles, irreversible electroporation studies in Denmark and Germany continue to broaden the European evidence base, positioning ECT and IRE devices for accelerated uptake once certificates are secured.

Asia-Pacific is forecast to outpace all other regions at an 11.93% CAGR through 2031 as Japan, China, and India commission automated GMP suites that embed electroporation at mass scale. Teijin’s Iwakuni upgrade to more than 1,000 CAR-T lots per year illustrates Japan’s leadership in flow-based closed systems. India’s first domestically produced CAR-T approvals de-risk local capacity investments, with CDMOs targeting sub-USD 60,000 price points suited to the country’s payer mix. China’s Porton Advanced already runs 200-billion-cell batches, demonstrating readiness for late-phase global trials. South Korea and Brazil represent nascent opportunities contingent on clearer reimbursement pathways and local GMP infrastructure build-outs.

Competitive Landscape

Market concentration is moderate: Lonza, MaxCyte, Thermo Fisher Scientific, and Bio-Rad Laboratories hold the majority combined share. MaxCyte’s Strategic Platform License model has expanded to four new agreements since 2024, converting capital-equipment sales into milestone-linked recurring revenue that buffers quarterly swings. Lonza’s July 2025 4D-Nucleofector LV Unit PRO integrates lentiviral and electroporation workflows, cutting vector consumption by 40% and strengthening the company’s lock-in among CAR-T manufacturers. Thermo Fisher and Harvard Bioscience leverage large distributor footprints to reach research labs, hedging against CDMO consolidation that could compress equipment margins.

Smaller entrants focus on white-space niches. Scandinavian ChemoTech dominates veterinary electrochemotherapy and builds clinical oncology exposure via India and Southeast Asia. Inovio seeks first-in-class approval for an electroporation-delivered therapeutic vaccine, potentially unlocking royalty streams from future device-drug combinations. Asian manufacturers such as Nepa Gene and BEX compete on price within academic markets but lack ISO-13485 documentation and Device Master Files required for GMP penetration. Automation innovators like Cellares position integrated shuttles as turnkey options for IDMO operators, reducing per-lot labor from hours to minutes and appealing to sponsors scaling late-phase programs.

Electroporation Instruments Industry Leaders

Lonza Group Ltd

MaxCyte, Inc.

Thermo Fisher Scientific

Bio-Rad Laboratories

Harvard Bioscience

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: MaxCyte, Inc. introduced ExPERT DTx, a high-throughput transfection platform for research and drug discovery. This modular 96-well electroporation system enables efficient transfection of primary cells and cell lines with minimal cellular stress, providing critical insights into biological processes and supporting scale-up to larger transfection volumes.

- January 2026: Teijin Regenet expanded the Iwakuni Factory to produce >1,000 CAR-T lots annually with automated electroporation integrated into closed workflows.

Global Electroporation Instruments Market Report Scope

As per the scope of the report, electroporation instruments, commonly known as electroporators, are specialized laboratory devices designed to introduce foreign molecules—such as DNA, RNA, proteins, or drugs—into cells by temporarily increasing the permeability of their membranes. The core principle is to apply brief, high-voltage electrical pulses to a cell suspension, creating nanoscale, transient pores in the phospholipid bilayer.

The electroporation instruments market is segmented by instrument, application, end users, mode, and geography. By instrument, the market is segmented into the total electroporation system, the eukaryotic electroporation system, and the microbial electroporation system. Based on the application, the market is segmented into protein production, gene therapy/cell therapy manufacturing, electrochemotherapy, irreversible electroporation, in vivo DNA/RNA vaccine and gene delivery, and biomedical research. By end users, the market is segmented into biotechnology & pharmaceutical companies, academic & research institutes, CROs & CDMOs, and hospitals & specialty clinics. Based on mode, the market is segmented into In Vitro / Ex Vivo and In Vivo. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Total Electroporation System |

| Eukaryotic Electroporation System |

| Microbial Electroporation System |

| Protein Production |

| Gene Therapy / Cell Therapy Manufacturing |

| Electrochemotherapy (ECT) |

| Irreversible Electroporation (IRE) |

| In Vivo DNA/RNA Vaccine & Gene Delivery |

| Biomedical Research (Academic/Industrial) |

| Biotechnology & Pharmaceutical Companies |

| Academic & Research Institutes |

| CROs & CDMOs |

| Hospitals & Specialty Clinics |

| In Vitro / Ex Vivo |

| In Vivo |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Instrument | Total Electroporation System | |

| Eukaryotic Electroporation System | ||

| Microbial Electroporation System | ||

| By Application | Protein Production | |

| Gene Therapy / Cell Therapy Manufacturing | ||

| Electrochemotherapy (ECT) | ||

| Irreversible Electroporation (IRE) | ||

| In Vivo DNA/RNA Vaccine & Gene Delivery | ||

| Biomedical Research (Academic/Industrial) | ||

| By End User | Biotechnology & Pharmaceutical Companies | |

| Academic & Research Institutes | ||

| CROs & CDMOs | ||

| Hospitals & Specialty Clinics | ||

| By Mode | In Vitro / Ex Vivo | |

| In Vivo | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the electroporation instruments market expected to grow by 2031?

It is forecast to reach USD 857.5 million by 2031, expanding at an 11.19% CAGR from 2026-2031.

Which application currently generates the most revenue?

Gene therapy and cell therapy manufacturing led with a 34.89% share in 2025.

Which end-user segment is expanding the quickest?

CDMOs are projected to grow at a 12.6% CAGR through 2031 as sponsors outsource manufacturing

Why are in vivo electroporation devices gaining interest?

Pending FDA review of INO-3107 and favorable prostate-cancer data for NanoKnife validate clinical efficacy and support hospital adoption.

Page last updated on: