Electronics Manufacturing Services For Mobile Device Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

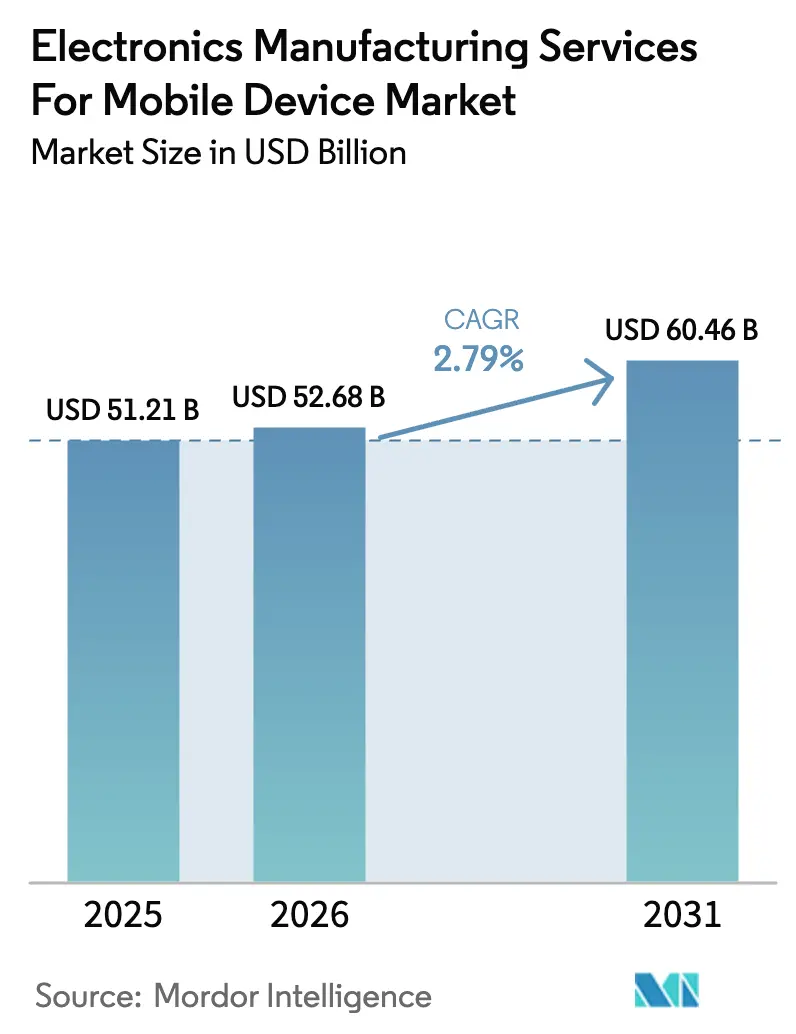

| Market Size (2026) | USD 52.68 Billion |

| Market Size (2031) | USD 60.46 Billion |

| Growth Rate (2026 - 2031) | 2.79% CAGR |

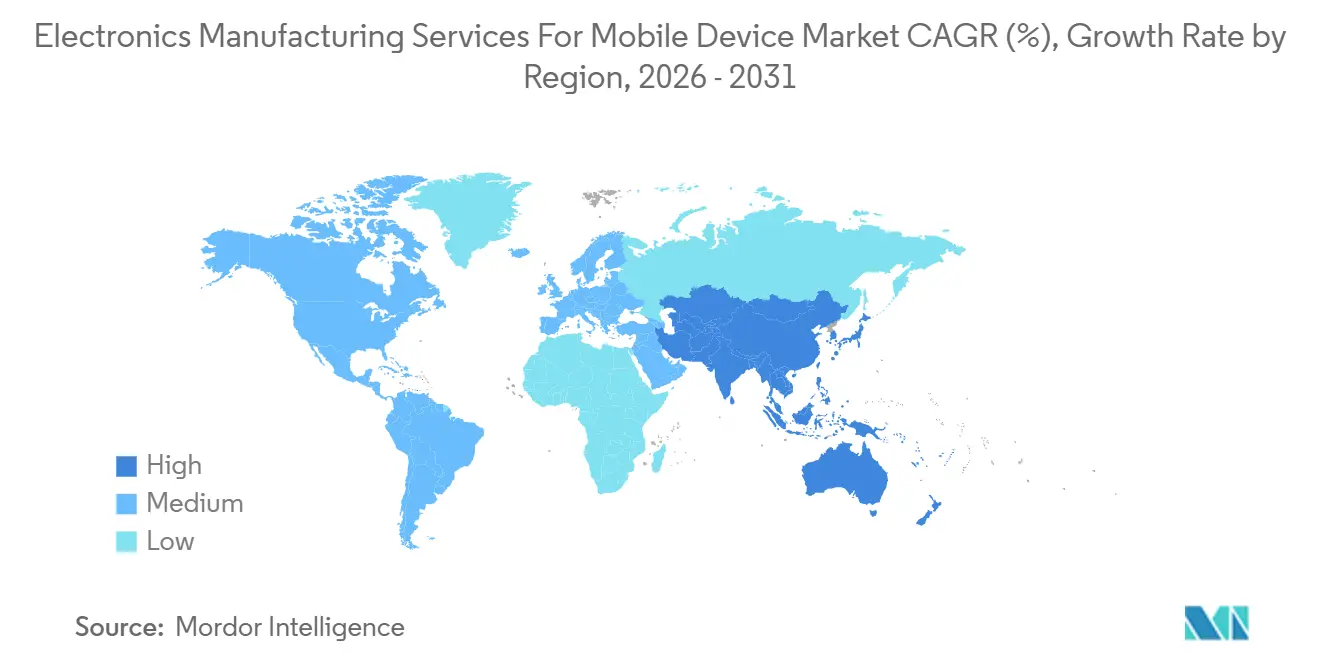

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

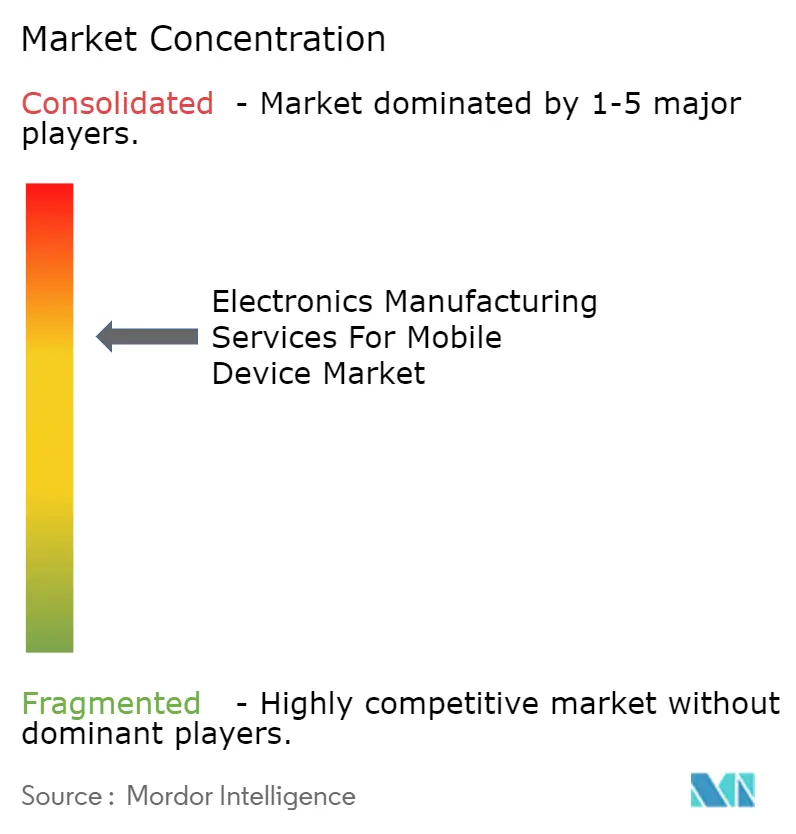

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electronics Manufacturing Services For Mobile Device Market Analysis by Mordor Intelligence

The Electronics Manufacturing Services For Mobile Device Market size is projected to expand from USD 51.21 billion in 2025 and USD 52.68 billion in 2026 to USD 60.46 billion by 2031, registering a CAGR of 2.79% between 2026 to 2031. The modest growth pace masks a structural pivot by original equipment manufacturers (OEMs) toward outsourcing high-value engineering, test development, and logistics while retaining brand stewardship. Sovereign-AI rules in the European Union and data-localization mandates in India are accelerating the need for on-device large language models, raising demand for advanced printed-circuit-board (PCB) assembly lines that only a handful of tier-one contract manufacturers operate at scale. Competitive intensity remains high as tier-one players diversify geographic footprints to mitigate labor-cost inflation in coastal China and to capture production-linked incentives in Vietnam, Mexico, and India. Meanwhile, green-audit requirements by Apple, Samsung, and Google are catalyzing capital outlays for renewable-energy sourcing and energy-recovery retrofits, raising both barriers to entry and price-premium opportunities for compliant providers.

Key Report Takeaways

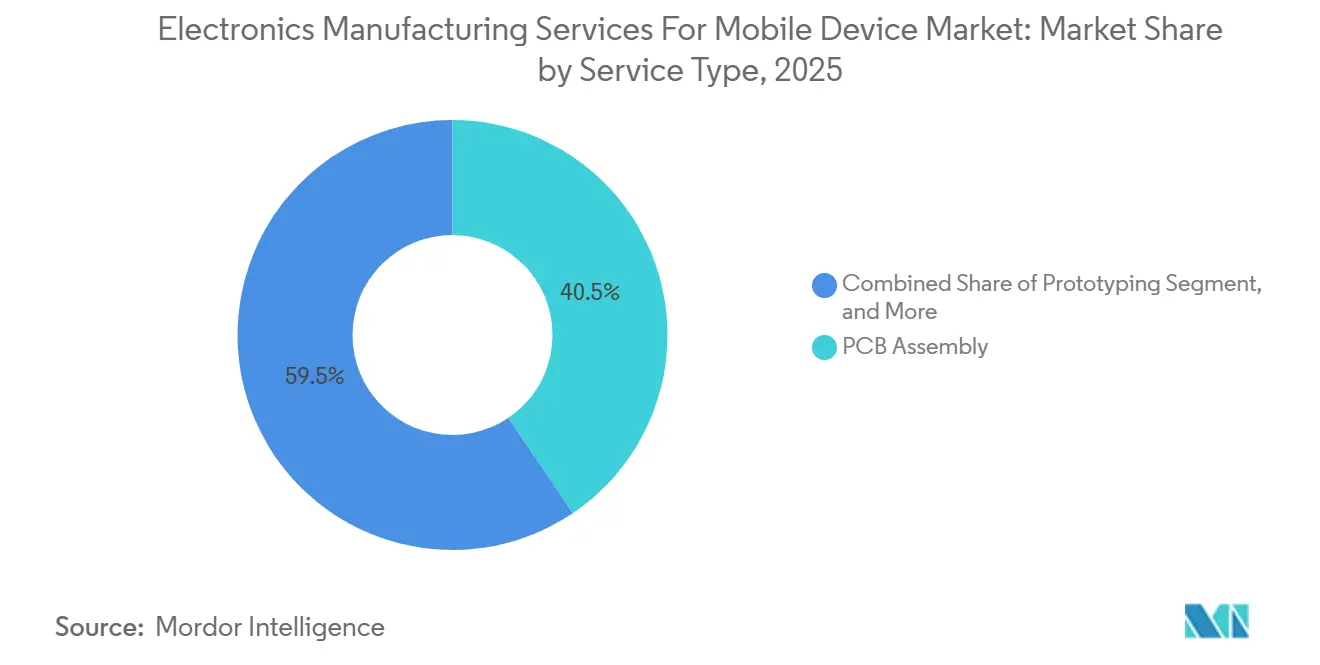

- By service type, PCB Assembly held 40.55% of the electronics manufacturing services for mobile device market share in 2025, while electromechanical assembly and box build is advancing at a 3.02% CAGR through 2031.

- By business model, contract manufacturing dominated with 63.84% revenue share in 2025, whereas hybrid and turnkey models exhibit the highest forecast CAGR at 2.97%.

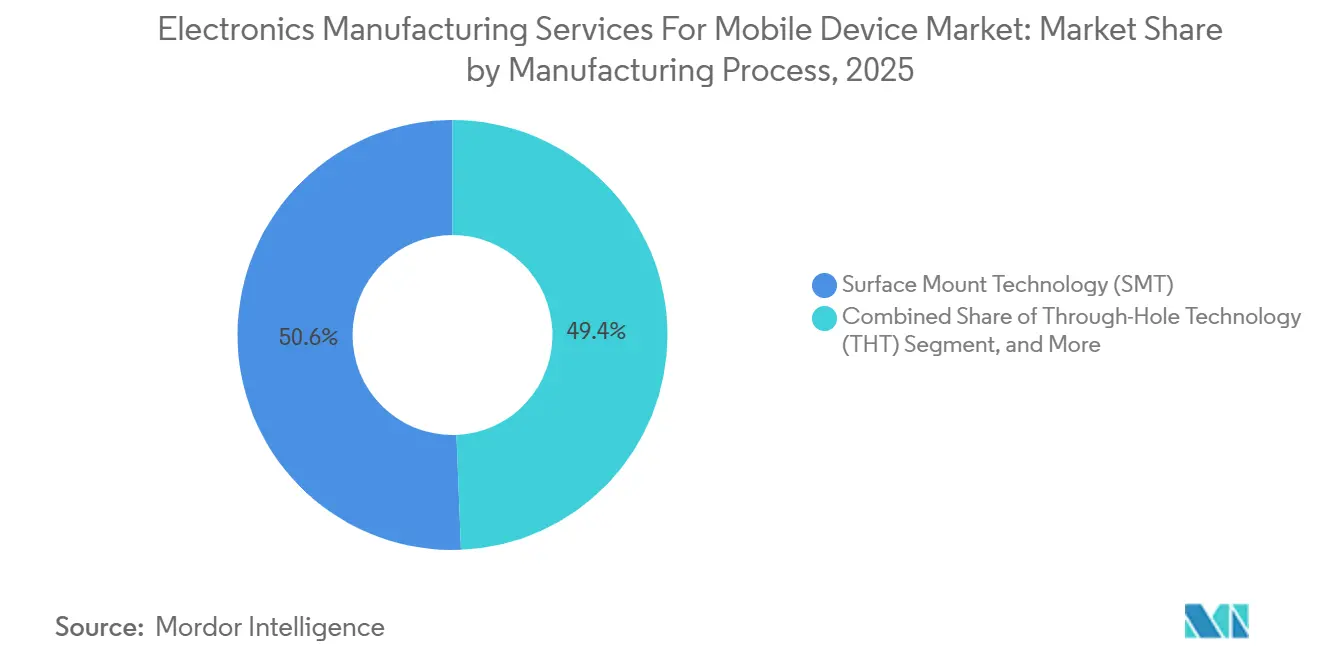

- By manufacturing process, surface mount technology commanded 50.63% of the electronics manufacturing services for mobile device market size in 2025, while advanced packaging and hybrid processes are projected to expand at a 3.42% CAGR to 2031.

- Asia Pacific captured 61.77% revenue share in 2025 and is poised to post the fastest regional CAGR of 3.88% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electronics Manufacturing Services For Mobile Device Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging 5G-Enabled Smartphone Design Outsourcing | +0.8% | Global, concentrated in Asia Pacific and North America | Medium term (2-4 years) |

| Generative-AI Edge Inference Demanding Advanced PCB Assembly | +0.9% | Global, led by North America and Asia Pacific | Long term (≥ 4 years) |

| Nearshoring Incentives in Mexico, Vietnam and India | +0.7% | Mexico, Vietnam, India | Medium term (2-4 years) |

| Ultra-Fine-Pitch SMT Capability Expansion Below 0.8 µm | +0.5% | Asia Pacific core, selective North America and Europe | Long term (≥ 4 years) |

| OEM Carbon-Neutrality Targets Driving “Green EMS” Audits | +0.3% | Global, strongest in Europe and North America | Medium term (2-4 years) |

| Big-Tech Co-investment in Automated Box-Build Lines | +0.4% | Asia Pacific and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging 5G-Enabled Smartphone Design Outsourcing

OEMs are moving radio-frequency front-end integration and antenna-tuning validation to contract manufacturers, trimming in-house engineering rosters by up to 30% and shortening mid-cycle refresh lead times. Apple’s expansion of iPhone assembly in India through Tata Electronics’ Hosur plant in late 2024 exemplified the strategy of pairing local-content compliance with tight design control. Foxconn reinforced the trend by investing USD 500 million in a dedicated 5G module line in Zhengzhou during 2025, equipped with pick-and-place systems that handle 03015M passives at sub-0.12-second cycles.[1]Foxconn Technology Group, “Investment Announcements 2025,” foxconn.com Regulatory agencies such as the U.S. Federal Communications Commission and India’s Telecommunications Engineering Center mandate specific-absorption-rate testing that few OEMs want to replicate in house, deepening reliance on accredited contract manufacturing facilities. Sub-6 GHz device programs targeting Southeast Asia and Latin America further amplify outsourcing because their simpler PCB stack-ups allow rapid reuse of reference designs.

Generative-AI Edge Inference Demanding Advanced PCB Assembly

Large language models exceeding 7 billion parameters now reside on smartphones, pushing neural processing unit (NPU) power draw to 8-12 W and requiring impedance-controlled power-delivery networks below 5 milliohms. MediaTek’s Dimensity 9400 chipset, publicized in late 2024, demands chip-on-wafer-on-substrate packaging with through-silicon vias, prompting Foxconn to allocate USD 300 million in 2025 to retrofit its Kunshan campus with fan-out wafer-level lines sourced from ASM Pacific Technology. Thermal simulation tools from Ansys and Siemens have become standard in design-for-manufacturability reviews because minor solder-mask variances can trigger thermal runaway in NPUs clocked at 3 GHz. Fewer than 15 providers worldwide currently sustain yield rates above 92% on heterogeneous-integration modules, concentrating bargaining power among technology leaders.

Nearshoring Incentives in Mexico, Vietnam and India

Governments placed over USD 12 billion in fiscal incentives during 2024-2025 to lure electronic manufacturing services capacity. Vietnam’s Circular 04/2024/TT-BCT exempts imported assembly equipment from value-added tax for five years, underpinning Foxconn’s USD 1 billion expansion in Bac Giang announced in March 2025.[2]Vietnam Ministry of Planning and Investment, “Circular 04/2024/TT-BCT,” mpi.gov.vn Mexico’s Plan Mexico program offers accelerated depreciation and streamlined permits within 100 km of the U.S. border, attracting Flex’s USD 250 million Guadalajara campus. India’s production-linked incentive scheme delivers cash rebates of 4-6% on incremental sales, encouraging Pegatron’s 15,000-person Tamil Nadu plant commissioned in 2025. These incentives cut lead times to North American and South Asian end-markets, yet nascent facilities operate at 60-70% of mature Chinese labor productivity in the first two years, tempering near-term gains in the electronics manufacturing services for mobile device market.

Ultra-Fine-Pitch SMT Capability Expansion Below 0.8 µm

Migration to 03015M and 02010M passives forces contract manufacturers to purchase nitrogen-atmosphere reflow ovens and laser-cut stencils with <0.5 µm surface roughness, costing USD 8-12 million per line. Fuji’s NXTR platform, released in 2024, offers ±15 µm placement accuracy at 42,000 parts per hour, yet by end-2025 only 30 facilities had installed the equipment. in the electronics manufacturing services for mobile device marke, rigid-flex PCBs for foldable designs require component placement strategies that accommodate bending radii of 3 mm without inducing solder-joint fatigue. Compliance with IPC-A-610 Class 3 workmanship, mandating zero bridging and a minimum 50% fillet height, has kept defect rates below 50 ppm only at providers that integrate automated optical inspection with real-time statistical process control.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Mobile-Component Shortage Cycles Post-2025 | -0.6% | Global, acute in Asia Pacific and Europe | Short term (≤ 2 years) |

| Intensifying IP-Leakage Litigation Against Tier-2 ODMs | -0.4% | Asia Pacific with spillover to North America and Europe | Medium term (2-4 years) |

| Rising Labor Costs in Coastal China Facilities | -0.5% | Asia Pacific, mainly coastal China | Medium term (2-4 years) |

| Tightening E-Waste Regulations on Device Refurb Lines | -0.3% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying IP-Leakage Litigation Against Tier-2 ODMs

Qualcomm’s December 2024 suit against Transsion Holdings sought damages exceeding USD 150 million for unlicensed modem designs, signaling heightened scrutiny of intellectual-property compliance.[3]Qualcomm Inc., “Legal Filings 2024,” qualcomm.com MediaTek audited 200 Shenzhen ODMs in 2024 and severed ties with 18 that reused unlicensed reference designs, underscoring the legal risk for thin-margin providers. Apple’s earlier dispute with Rivos heightened OEM vigilance, and quarterly audits of engineering repositories are now routine. The litigation climate favors tier-one providers with robust compliance regimes, but it also reduces supplier flexibility for brands aiming to diversify sourcing.

Rising Labor Costs in Coastal China Facilities

Average monthly wages for production technicians in Foxconn’s Zhengzhou campus climbed from CNY 5,800 (USD 820) in 2023 to CNY 6,400 (USD 905) in 2024, squeezing operating margins by 1.2 percentage points. Demographic shifts cut the coastal Chinese working-age population by 3.2 million between 2023 and 2025, tightening supply for IPC-certified labor. Pegatron responded in April 2025 with a USD 400 million automation push to deploy collaborative robots for screw-driving and functional testing, targeting a 30% reduction in labor hours by 2027. Inland relocation faces logistics gaps, with only 12% of smartphone assembly migrating inland by 2025, according to China’s Ministry of Industry and Information Technology. Shrinking labor-cost differentials versus Vietnam and India, in the electronics manufacturing services for mobile device market, are set to accelerate nearshoring from 2026 onward.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: PCB Assembly Anchors Revenue, Box Build Gains Momentum

PCB Assembly captured 40.54% of 2025, electronics manufacturing services for mobile device market revenue, underscoring its role in integrating multi-die system-in-package modules required for 5G smartphones constrained to mainboards under 45 cm². Electromechanical Assembly and Box Build is the fastest-growing category, with a 3.02% CAGR through 2031, as OEMs shift final integration closer to end markets to cut lead times and customs costs. Engineering Services gained visibility when sovereign-AI mandates required thermal-profile validation of neural processing units, compelling ODMs to embed simulation into early design stages. Test and Development Implementation rose steadily because accredited anechoic chambers remain scarce, while Logistics Services differentiated by enabling providers to trim safety stock from 18 weeks to 12 weeks.

Box-build momentum reflects OEM demand for turnkey partners that handle enclosure assembly, battery integration, and final inspection within a single site, curbing in-transit damage. Foxconn’s USD 500 million automated box-build line launched in Zhengzhou during 2025 illustrates the capital scale needed to compete. IPC-A-610 Class 3 adherence is pushing real-time statistical process control adoption, concentrating high-yield assembly among fewer than 15 global firms. Vendors meeting yield rates above 92% command modest price premiums despite intense price pressure on commoditized PCB assembly lines.

By Business Model: Contract Manufacturing Dominates, Hybrid Models Accelerate

Contract Manufacturing held 63.84% of 2025 revenue as brand owners favored asset-light strategies, reallocating capital toward software and marketing. Original Design Manufacturing (ODM) remained crucial for budget smartphones in emerging regions, providing turnkey reference designs to brands lacking engineering depth. Hybrid and Turnkey arrangements show the fastest expansion at a 2.97% CAGR, driven by mid-tier Chinese and Indian brands that seek single-umbrella partners to manage intellectual property and supply-chain risk. These hybrid frameworks slash development timelines by 8-12 weeks, pivotal for sub-USD 200 5G handsets.

Wingtech’s 2024 acquisition of Nexperia’s standard-product unit epitomizes vertical integration that allows ODMs to internalize bill-of-materials margin. Tier-one providers handle high-mix, low-volume flagship runs, while tier-two ODMs such as Huaqin and Longcheer focus on high-volume, low-mix economy devices. Ongoing IP-leakage concerns mean OEMs, in the lectronics manufacturing services for mobile device market, still reserve leading-edge antenna tuning and thermal algorithms for trusted partners even as they widen supplier rosters.

By Manufacturing Process: SMT Leads, Advanced Packaging Surges

Surface Mount Technology (SMT) processes accounted for 50.63% of 2025 production volume, thanks to throughput exceeding 1,200 parts per square inch and sub-0.12-second placement cycles for 03015M passives. Through-Hole Technology continues to decline as miniaturization pushes connector pitches below 0.5 mm. Advanced Packaging and Hybrid Processes, in the lectronics manufacturing services for mobile device market, will grow at a 3.42% CAGR through 2031 as fan-out wafer-level and chiplet-based designs become standard for on-device AI inference, reducing signal latency by up to 50% compared with wire-bonded packages.

Intel’s Foveros stacking uses 36 µm hybrid bonds, but fewer than a dozen EMS sites achieve yield above 85% on such heterogeneous modules. TSMC’s InFO packaging, long used in Apple’s A-series processors, is migrating to NPUs that dissipate 8-12 W, requiring thermal interface materials with a thermal conductivity exceeding 5 W/m-K. The stringent IPC-7095E thermal cycling requirement of 1,000 cycles from -40 °C to +125 °C adds 6-8 weeks to new-product introductions, reinforcing the competitive edge of EMS providers equipped with integrated test-house partnerships.

Geography Analysis

Asia Pacific accounted for 61.77% of 2025 revenue and is projected to grow at a 3.88% CAGR through 2031, buoyed by Vietnam’s USD 7.7 billion electronics FDI approvals in 2024, India’s USD 1.5 billion mobile-manufacturing pledges by mid-2025, and China’s dominance in ultra-fine-pitch SMT capacity. Foxconn’s USD 1 billion expansion in Bac Giang exemplifies the region’s magnetism for nearshoring investments. Thailand’s eight-year tax holidays for THB 1 billion (USD 28 million) projects enticed Samsung to enlarge its Chonburi campus for foldable-screen models. Malaysia’s Industrial Master Plan 2030 offers accelerated allowances and permit streamlining that favor EMS investors committed to local workforce development.

North America and Europe combined comprised roughly 28% of 2025 revenue. Mexico’s Plan Mexico incentives fueled Flex’s USD 250 million Guadalajara initiative, slicing Asia-to-U.S. lead times by 35% and trimming logistics costs by up to 22%. The European Chips Act earmarks EUR 43 billion (USD 47 billion) for advanced-packaging projects, attracting EMS providers that co-locate near substrate and die suppliers. Germany’s Bavaria and Baden-Württemberg clusters pivot toward prototyping and industry-4.0 automation as mass-volume smartphone assembly migrates to lower-cost regions.

South America and the Middle East and Africa together registered sub-10% revenue share in 2025 but gained traction through import-substitution policies. Brazil’s Informatics Law grants up to 80% tax relief on devices meeting local value-add thresholds, sustaining modest domestic EMS capacity. South Africa’s 2024 Electronics Manufacturing Incentive Program offers 30% capital grants for export-oriented facilities, aiming to leverage a regional smartphone market that surpassed 180 million units in 2024.

Competitive Landscape

The top five EMS and ODM players controlled about 45% of 2025 global capacity, yielding a moderately concentrated field where OEMs still deploy multi-sourcing to negotiate price concessions. Foxconn, Pegatron, and Wistron assembled more than 80% of iPhones in 2025 but face margin pressure as Apple seeks annual cost reductions of 3-5% while demanding compliance with renewable energy. Tier-two ODMs such as Wingtech, Huaqin, and Longcheer expand budget-handset share by bundling reference designs, component procurement, and regulatory certification, shortening customer time-to-market by up to 12 weeks. Luxshare Precision advanced in wearables after acquiring a majority stake in a Vietnamese facility for USD 180 million in 2025.

With fewer than a dozen plants globally capable of sub-0.8 µm pad-spacing assembly at 95% yield, ultra-fine-pitch SMT offers lucrative white space. Intel Foundry Services’ 2024 decision to offer advanced packaging externally could reshape traditional EMS dynamics by allowing OEMs to bypass contract manufacturers for heterogeneous integration. Jabil invested USD 150 million in 2025 to roll out digital-twin simulations across Asian sites, cutting solder-joint defects by 18% and demonstrating how process analytics differentiate incumbents.

Electronics Manufacturing Services For Mobile Device Industry Leaders

Hon Hai Precision Industry (Foxconn)

Pegatron Corporation

Wistron Corporation

Flex Ltd.

Jabil Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Foxconn announced a USD 700 million campus in Telangana, India, slated to open in Q4 2026 with automated optical inspection lines that meet IPC-A-610 Class 3 standards.

- December 2025: Pegatron and Tata Electronics formed a USD 500 million joint venture to add 10 million annual iPhone units in Tamil Nadu by 2027.

- November 2025: Luxshare Precision purchased a 60% stake in a Vietnamese wearable-device contractor for USD 180 million to diversify production outside China.

- October 2025: Flex committed USD 300 million to automate box-build operations at its Guadalajara campus, leveraging Plan Mexico incentives.

- September 2025: Jabil secured a five-year, USD 1 billion engineering and PCB-assembly contract for next-gen foldable smartphones, including thermal simulation and compliance testing.

Global Electronics Manufacturing Services For Mobile Device Market Report Scope

The Electronics Manufacturing Services for Mobile Device Market Report is Segmented by Service Type (Electronic Manufacturing Services including PCB Assembly, Electromechanical Assembly and Box Build, Prototyping, and Other Services; Engineering Services; Test and Development Implementation; Logistics Services; and Other Service Types), Business Model (Contract Manufacturing, Original Design Manufacturing, and Hybrid and Turnkey Models), Manufacturing Process (Surface Mount Technology, Through-Hole Technology, and Advanced Packaging and Hybrid Processes), and Geography (North America, Europe, Asia Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly / Box Build | |

| Prototyping | |

| Other Electronic Manufacturing Services | |

| Engineering Services | |

| Test and Development Implementation | |

| Logistics Services | |

| Other Service Types |

| Contract Manufacturing (CM) |

| Original Design Manufacturing (ODM) |

| Hybrid / Turnkey / Other Business Models |

| Surface Mount Technology (SMT) |

| Through-Hole Technology (THT) |

| Advanced Packaging / Hybrid Processes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| South-East Asia | |

| Rest of Asia Pacific | |

| South America | |

| Middle East and Africa |

| By Service Type | Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly / Box Build | ||

| Prototyping | ||

| Other Electronic Manufacturing Services | ||

| Engineering Services | ||

| Test and Development Implementation | ||

| Logistics Services | ||

| Other Service Types | ||

| By Business Model | Contract Manufacturing (CM) | |

| Original Design Manufacturing (ODM) | ||

| Hybrid / Turnkey / Other Business Models | ||

| By Manufacturing Process | Surface Mount Technology (SMT) | |

| Through-Hole Technology (THT) | ||

| Advanced Packaging / Hybrid Processes | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| South-East Asia | ||

| Rest of Asia Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

How large is the electronic manufacturing services for mobile devices market in 2026?

The market reached USD 52.68 billion in 2026 and is projected to expand to USD 60.46 billion by 2031 at a 2.79% CAGR.

Which service type currently contributes the most revenue?

PCB Assembly led with 40.55% revenue share in 2025, reflecting its central role in integrating multi-die system-in-package modules.

Which region is growing the fastest?

Asia Pacific is expected to record the quickest growth at a 3.88% CAGR through 2031, aided by incentive programs in Vietnam and India.

Why are hybrid and turnkey business models gaining traction?

They combine design ownership and supply-chain risk management under one partner, trimming development time by up to 12 weeks for mid-tier brands.

What is driving investments in advanced packaging?

On-device AI workloads require fan-out wafer-level and chiplet-based modules that cut signal latency by 40-50% relative to wire-bonded packages.

Page last updated on: