Electronics Manufacturing Services For Lighting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.71 Billion |

| Market Size (2031) | USD 15.54 Billion |

| Growth Rate (2026 - 2031) | 4.10% CAGR |

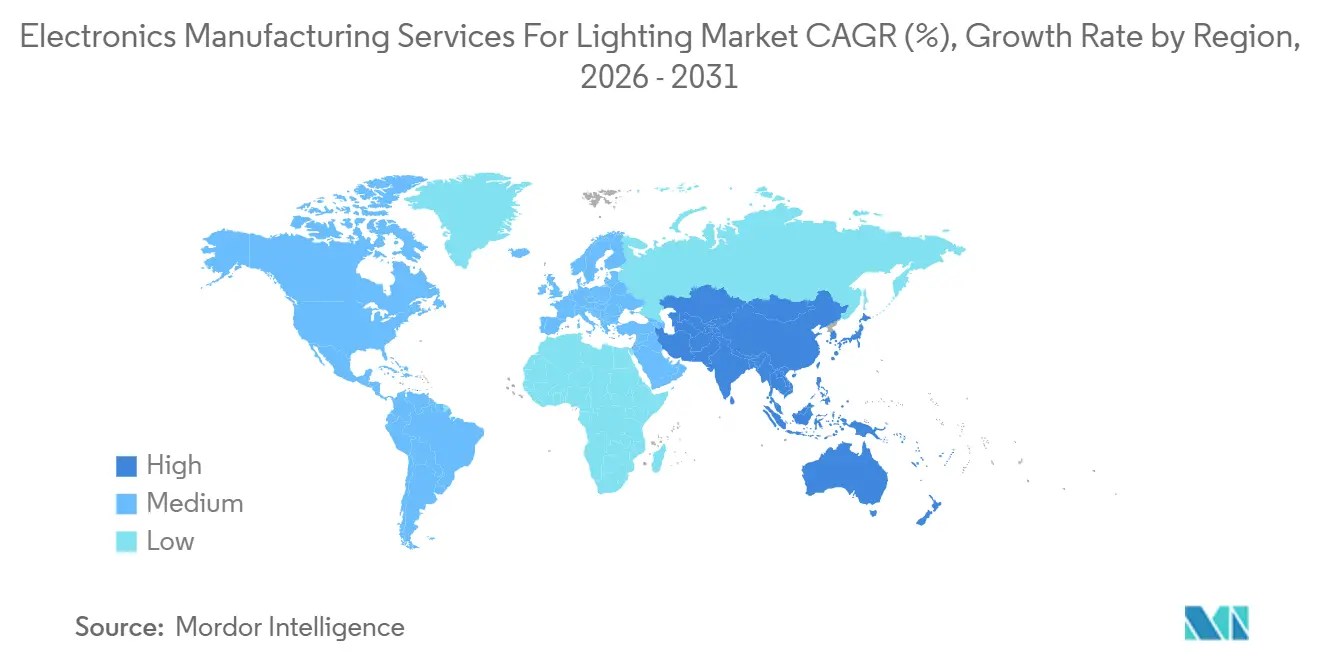

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

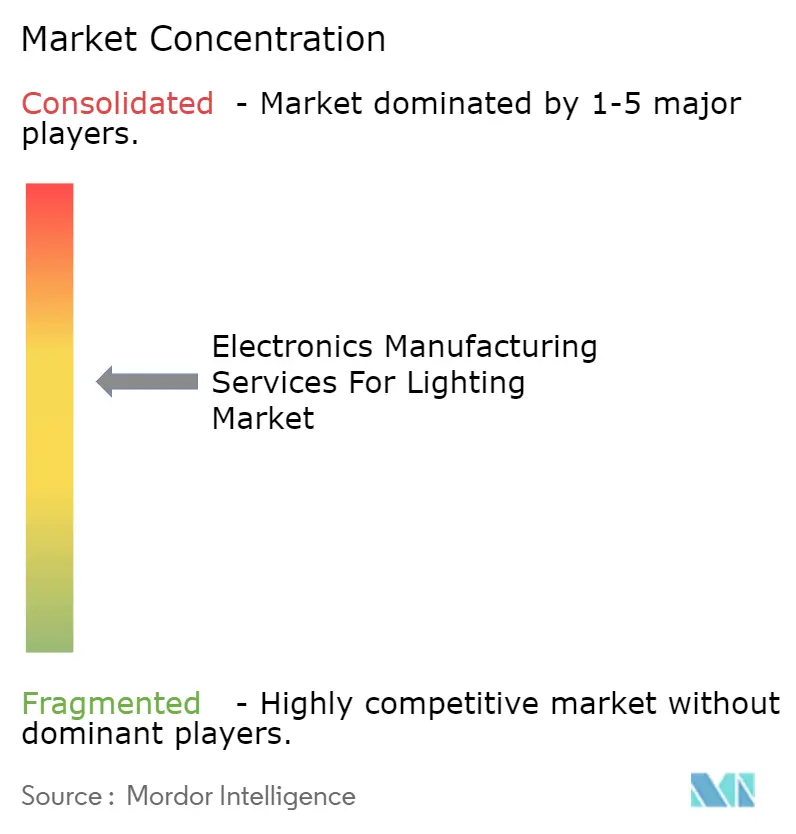

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electronics Manufacturing Services For Lighting Market Analysis by Mordor Intelligence

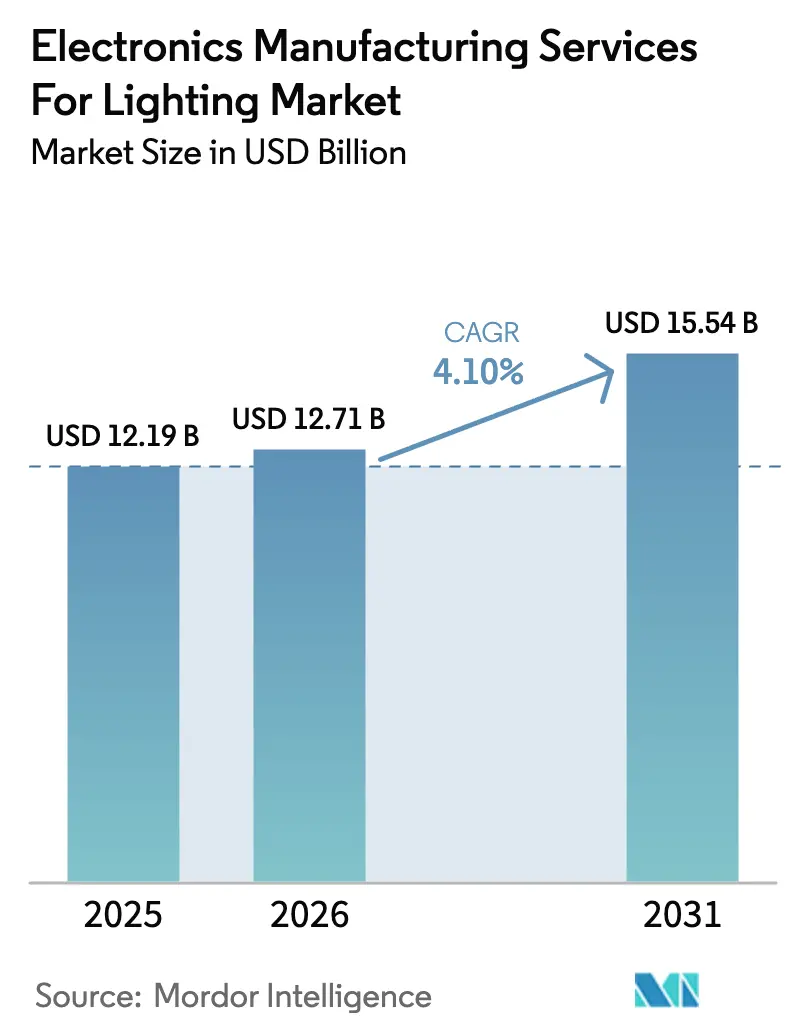

The electronics manufacturing services for lighting market size is projected to be USD 12.19 billion in 2025, USD 12.71 billion in 2026, and reach USD 15.54 billion by 2031, growing at a CAGR of 4.10% from 2026 to 2031. Market growth remains steady even as luminaire brands divest in-house assembly to free up capital for smart-lighting software, compliance testing, and sensor integration. Heightened outsourcing followed the November 2025 release of the DesignLights Consortium SSL V6.0 and LUNA V2.0 specifications, which tightened efficacy thresholds and mandated interoperability for embedded sensors, further accelerating demand for advanced surface-mount and box-build capabilities. Asia Pacific continues to anchor the supply base, helped by contract manufacturers in China and India that absorb near-shoring overflow from North American and European brands facing tariff uncertainty. Rising bill-of-materials complexity, component shortages, and raw-material price swings squeeze margins, yet regulatory tailwinds and the shift toward connected luminaires underpin service-revenue growth. Competitive intensity remains moderate as the top five vendors capture a considerable share of revenue, while regional specialists gain share through prototyping, co-location, and speed-to-market advantages.

Key Report Takeaways

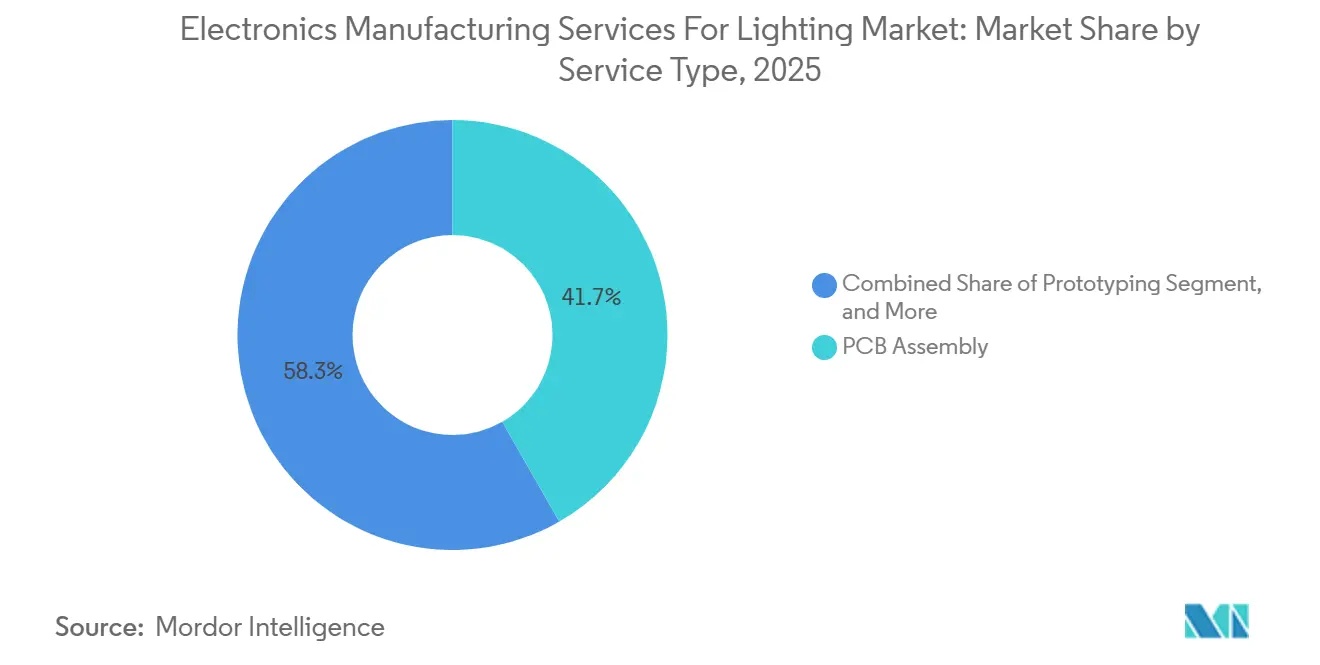

- By service type, printed-circuit-board (PCB) assembly led with 41.73% of electronics manufacturing services for lighting market share in 2025. Electromechanical assembly and box build is forecast to expand at a 5.81% CAGR through 2031, the fastest among service types.

- By business model, contract manufacturing held 64.46% of 2025 revenue, while hybrid and turnkey models are projected to grow at 6.03% through 2031.

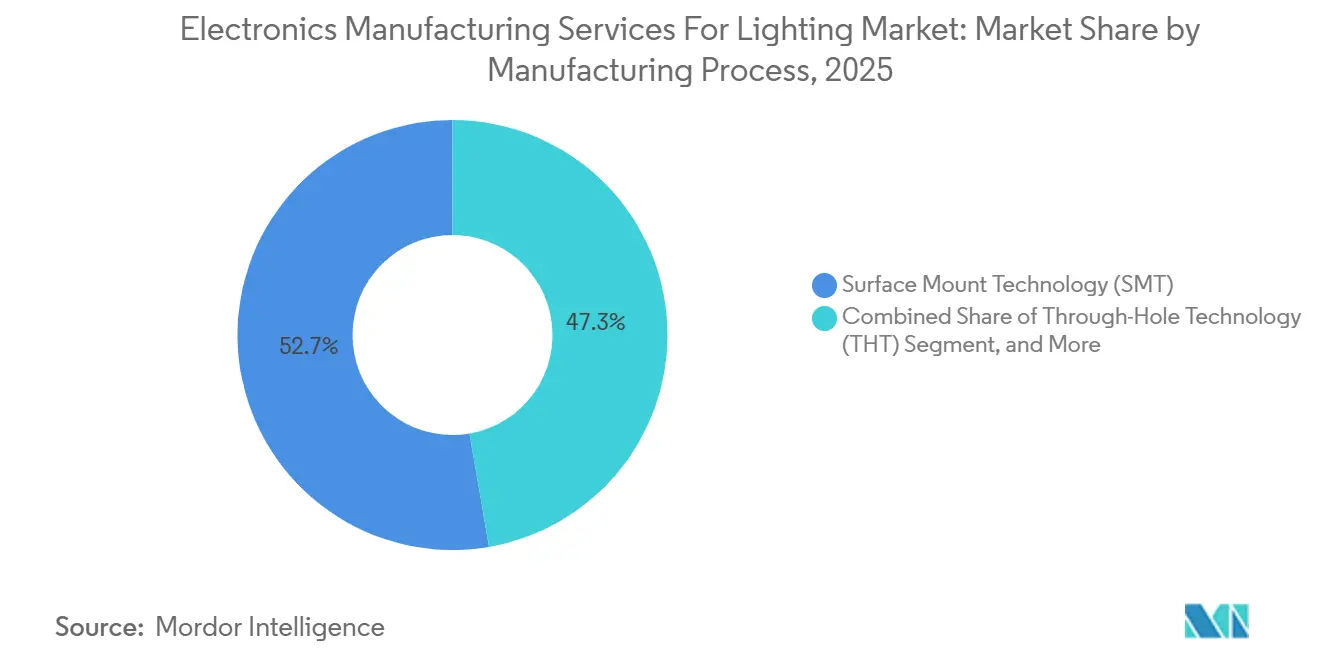

- By manufacturing process, surface-mount technology accounted for 52.71% of 2025 revenue, but advanced packaging and hybrid processes are advancing at a 5.96% CAGR.

- By geography, Asia Pacific commanded 60.88% of 2025 revenue and is expected to rise at a 6.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electronics Manufacturing Services For Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid LED penetration across commercial and industrial lighting | +1.2% | Global, with acceleration in Asia Pacific and North America | Medium term (2-4 years) |

| Outsourcing surge to reduce CAPEX and time-to-market | +1.0% | Global, especially North America and Europe | Short term (≤ 2 years) |

| Smart-lighting integration demands advanced electronics | +0.9% | Global, led by North America and Europe | Medium term (2-4 years) |

| Regulatory push for high-efficacy luminaire electronics | +0.7% | North America and Europe, early moves in Asia Pacific | Long term (≥ 4 years) |

| Thermal-optimised metal-core PCBs in high-lumen luminaires | +0.5% | Global, concentrated in industrial and outdoor segments | Medium term (2-4 years) |

| Near-shoring EMS capacity in Mexico and Central Eastern Europe to dodge tariffs | +0.6% | North America (Mexico), Europe (Poland, Czech Republic, Hungary) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid LED Penetration Across Commercial and Industrial Lighting

Solid-state technology now dominates retrofit decisions as total-cost-of-ownership calculations favor LEDs over legacy sources. The DesignLights Consortium noted an 18% year-over-year rise in qualified-product submissions for LED fixtures during 2025, most with tunable spectrum engines and integrated sensors.[1]DesignLights Consortium, “SSL V6.0 and LUNA V2.0 Technical Requirements,” DESIGNLIGHTS.ORG Brands lacking 0201-package pick-and-place precision and sub-100-ppm optical-inspection capabilities increasingly outsource PCB population and driver integration. Providers that invested in nitrogen-reflow ovens and X-ray inspection captured above-market growth by mastering high-thermal-conductivity metal-core boards. Demand for turnkey box-build services also rises because combining electronics, heat sinks, optics, and ingress-protection housings in one package can trim launch schedules by four to six weeks.

Outsourcing Surge to Reduce CAPEX and Time-to-Market

Luminaire makers continue shedding legacy assembly lines to redeploy capital toward cloud-based lighting controls and analytics. An IPC survey published in June 2025 found that 62% of electronics manufacturers saw stronger turnkey demand, reflecting a broader desire to swap fixed assets for variable costs. SSL V6.0 tightens lumen-maintenance and flicker metrics, requiring thermal chambers and photometric labs that cost USD 2 million-USD 5 million apiece, assets that contract manufacturers amortize across customers. Outsourcing also secures design-for-manufacturability reviews that can compress prototype cycles by eight weeks, a critical edge in seasonal specification cycles across commercial real estate.

Smart-Lighting Integration Demands Advanced Electronics

Connected luminaires now embed Zigbee, Thread, or Matter radios alongside LED drivers and sensors, quintupling component counts and tripling PCB layers. The Connectivity Standards Alliance issued Matter 1.2 in October 2024, obligating interoperability across major ecosystems.[2]Connectivity Standards Alliance, “Matter 1.2 Specification Release,” CSA-IOT.ORG Contract manufacturers consequently co-design antenna layouts, validate EMC compliance under CISPR 15, and flash firmware over the air at end-of-line. Box-build providers offering RF tuning and mesh-network commissioning are growing 170 basis points faster than the market composite. The trend is most pronounced in North America and Europe, where building codes require networked lighting for demand-response programs.

Regulatory Push for High-Efficacy Luminaire Electronics

North American and European regulators lengthen minimum efficacy baselines and tighten standby-power limits, pushing brands toward higher-performance LED drivers. Participation in IEC 62031 working groups gives contract manufacturers early visibility, enabling them to prequalify processes before new rules take effect. Firms that can deliver photometric and thermal test reports alongside assembled boards position themselves as compliance partners rather than mere suppliers.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent IC and LED driver shortages | -0.8% | Global, acute in Asia Pacific and North America | Short term (≤ 2 years) |

| Squeezed margins from raw-material price volatility | -0.6% | Global, especially affecting Asia Pacific makers | Medium term (2-4 years) |

| Elevated reject rates from stringent thermal-reliability tests | -0.3% | Global, centered in high-lumen and outdoor segments | Medium term (2-4 years) |

| Intellectual-property leakage concerns in ODM engagements | -0.2% | Global, heightened in Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent IC and LED Driver Shortages

Lead times for power-management ICs and constant-current drivers remained 16-24 weeks throughout 2025, twice pre-2020 norms. Niche lighting controllers compete with automotive demand for the same analog foundry space, compelling contract manufacturers to carry 12-16 weeks of safety stock. Tied-up working capital and schedule disruptions add layers of cost that ripple across production plans in China, India, Mexico, and the United States.

Squeezed Margins From Raw-Material Price Volatility

Copper traded between USD 8,200 and USD 10,800 per metric ton during 2025 on the London Metal Exchange, a 31% swing that eroded fixed-price contracts.[3]London Metal Exchange, “Copper Price Data 2025,” LME.COM Aluminum heat-sink costs followed a similar path amid energy-price spikes. Only the largest providers can negotiate quarterly index-linked adjustments; smaller shops absorb hits that cut gross margins by 150-200 basis points relative to pre-2024 levels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Box Build Accelerates on Smart-Lighting Complexity

PCB assembly commanded 41.73% of 2025 revenue, anchoring the EMS for lighting market. The electronics manufacturing services for lighting market size for electromechanical assembly and box build is projected to grow by a 5.81% CAGR between 2026 and 2031, outpacing the overall 4.10% trajectory. Heightened integration of radios, sensors, and optics elevates box build from optional to essential as brands seek turnkey partners that merge electronics with heat sinks and IP-rated enclosures.

Growth rests on rising demand for engineering services covering design-for-manufacturability, EMC analysis, and firmware validation. Prototyping programs benefit from co-located surface-mount lines that shorten iteration loops, while logistics services support configure-to-order shipments for retrofit projects. Providers that deliver end-to-end assembly, software flashing, and functional test in one plant can cut launch cycles by four weeks, a key differentiator as SSL V6.0 deadlines loom.

By Business Model: Hybrid and Turnkey Models Gain Momentum

Contract manufacturing retained a 64.46% share in 2025, yet the electronics manufacturing services for lighting market size for hybrid and turnkey engagements is set to advance at 6.03% through 2031. Brands with shrinking internal engineering staffs now specify performance targets and aesthetics, then delegate circuit design, sourcing, and compliance documentation to their manufacturing partners.

SSL V6.0’s stringent flicker and lumen-maintenance metrics make turnkey offerings attractive because they bundle thermal-chamber testing and photometric reports into one price. Original-design manufacturing remains smaller, appealing mostly to regional luminaires without R&D budgets. Still, hybrid deals that balance brand IP ownership with contract-manufacturer design input secure faster approvals and mitigate inventory risk, attracting capital-constrained mid-market players.

By Manufacturing Process: Advanced Packaging and Hybrid Lines Rise

Surface-mount technology accounted for 52.71% of 2025 revenue, but advanced packaging and hybrid processes are growing at a 5.96% CAGR, expanding their electronics manufacturing services for lighting market share alongside growing flip-chip LED adoption. Fan-out wafer-level and embedded-die approaches shrink driver footprints by up to 40% while improving thermal paths- advantages crucial for ultra-slim downlights.

Hybrid lines that combine surface-mount placement, selective soldering, and advanced packaging allow each subassembly- wireless modules, power converters, sensor boards- to follow an optimized process. The approach proves valuable for high-lumen industrial fixtures, where embedded copper coins dissipate 50-100 watts of heat and require X-ray inspection for voids. Contract manufacturers offering such mixed-technology lines win programs that smaller, single-process shops cannot qualify.

Geography Analysis

Asia Pacific’s dominance stems from dense supplier ecosystems, sustained labor-cost advantages, and government incentives such as India’s production-linked scheme, which attracted USD 3 billion in electronics investment during 2024. The electronics manufacturing services for lighting market size for the region is expected to grow at 6.55% through 2031, boosted by Chinese mega-sites and Southeast Asian overflow hubs. China’s USD 2.8 trillion electronics output in 2025 provided shared infrastructure, while Japan and South Korea supplied high-thermal-conductivity ceramics and GaN substrates.

North America shows a split growth pattern. The United States and Canada have limited surface-mount capacity due to labor costs, but Mexico’s electronics workforce reached about 750,000 in 2025 as Asian vendors opened Guadalajara and Monterrey sites to avoid tariffs. Duty-free treatment under the United States-Mexico-Canada Agreement encourages final assembly south of the border while design stays north.

Europe posted measured growth anchored by Germany’s engineering-heavy ecosystem and Central Eastern European plants in Poland, the Czech Republic, and Hungary. These locations offer 40%-60% lower labor costs than Western Europe while keeping tariff-free access to European Union markets. Limited local demand caps South America, the Middle East, and Africa at below 10% of global revenue, though Gulf smart-city projects signal nascent opportunity.

Competitive Landscape

The electronics manufacturing services for lighting market remain moderately fragmented, with Hon Hai, Flex, Jabil, Benchmark Electronics, and Sanmina controlling roughly 35%-40% of global revenue. Scale yields 8%-12% unit-cost advantages through bulk component purchases and amortized capital equipment, yet mid-tier specialists such as Zollner Elektronik and LACROIX Electronics win projects requiring quick-turn prototyping and co-located volume production.

Technology investment patterns diverge. Asian mega-sites install fully automated lines that place up to 100,000 components per hour and hit sub-50-ppm defect rates, while Mexican and Central and Eastern European satellites prioritize configure-to-order flexibility over sheer throughput. Hon Hai’s 2024 capital expenditures totaled USD 4.2 billion, including nitrogen-reflow ovens and automated optical inspection for high-thermal metal-core boards.

Strategically, suppliers vie for turnkey engagements that bundle design, procurement, assembly, and compliance paperwork, creating longer contracts and higher margins. Near-shoring continues as Asian incumbents build in Mexico to serve North American customers within two-week lead times. Indian entrants leverage government incentives to undercut labor-intensive box-build services by 5%-8%, intensifying price pressure on established vendors

Electronics Manufacturing Services For Lighting Industry Leaders

Hon Hai Technology Group

Flex Ltd.

Jabil Inc.

Benchmark Electronics

Sanmina Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Cree LED launched fully assembled L2 PCBA solutions for indoor and outdoor lighting applications, offering turnkey LED modules with integrated drivers and thermal-management systems that reduce luminaire brands' assembly complexity.

- December 2025: Bridgelux and Lumitech executed a patent cross-licensing agreement covering tunable white and RGBW LED array technologies, enabling both companies to manufacture and supply contract manufacturers with color-mixing solutions for human-centric lighting applications.

- September 2025: Jabil announced a USD 75 million expansion of its Chihuahua, Mexico facility to add 200,000 square feet of industrial and lighting electronics assembly capacity, targeting North American customers seeking nearshore alternatives.

- August 2025: Flex completed a strategic partnership with a North American commercial-lighting brand to provide turnkey design, assembly, and logistics services for a new line of Matter-enabled connected luminaires.

- June 2025: Sanmina disclosed plans to invest USD 40 million in advanced packaging and system-in-package equipment across its Asian facilities to support customers transitioning to ultra-slim LED drivers and integrated power modules.

Global Electronics Manufacturing Services For Lighting Market Report Scope

The Electronic Manufacturing Services for Lighting Market Report is Segmented by Service Type (Electronic Manufacturing Services including PCB Assembly, Electromechanical Assembly and Box Build, Prototyping, and Other EMS Types, Engineering Services, Test and Development Implementation, Logistics Services, and Other Service Types), Business Model (Contract Manufacturing, Original Design Manufacturing, and Hybrid or Turnkey Models), Manufacturing Process (Surface-Mount Technology, Through-Hole Technology, and Advanced Packaging or Hybrid Processes), and Geography (North America including United States, Canada, and Mexico, South America, Europe including Germany, United Kingdom, and Rest of Europe, Asia Pacific including China, Japan, South Korea, India, South-east Asia, and Rest of Asia Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value in USD.

| Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly / Box Build | |

| Prototyping | |

| Other Electronic Manufacturing Services | |

| Engineering Services | |

| Test and Development Implementation | |

| Logistics Services | |

| Other Service Types |

| Contract Manufacturing (CM) |

| Original Design Manufacturing (ODM) |

| Hybrid / Turnkey / Other Business Models |

| Surface-Mount Technology (SMT) |

| Through-Hole Technology (THT) |

| Advanced Packaging / Hybrid Processes |

| North America | United States |

| Canada | |

| Mexico | |

| South America | |

| Europe | Germany |

| United Kingdom | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| South-east Asia | |

| Rest of Asia Pacific | |

| Middle East | |

| Africa |

| By Service Type | Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly / Box Build | ||

| Prototyping | ||

| Other Electronic Manufacturing Services | ||

| Engineering Services | ||

| Test and Development Implementation | ||

| Logistics Services | ||

| Other Service Types | ||

| By Business Model | Contract Manufacturing (CM) | |

| Original Design Manufacturing (ODM) | ||

| Hybrid / Turnkey / Other Business Models | ||

| By Manufacturing Process | Surface-Mount Technology (SMT) | |

| Through-Hole Technology (THT) | ||

| Advanced Packaging / Hybrid Processes | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| South-east Asia | ||

| Rest of Asia Pacific | ||

| Middle East | ||

| Africa | ||

Key Questions Answered in the Report

What was the electronic manufacturing services for lighting market value in 2026 and its projected 2031 figure?

The market stood at USD 12.71 billion in 2026 and is projected to reach USD 15.54 billion by 2031.

Which service type is forecast to grow the fastest through 2031?

Electromechanical assembly and box build is expected to expand at a 5.81% CAGR, topping all other service categories.

Why are hybrid and turnkey business models gaining traction?

Stricter SSL V6.0 rules and shrinking in-house engineering teams push brands toward partners that handle design, sourcing, assembly, and compliance in a single package

What geographic region holds the largest share of EMS revenue for lighting?

Asia Pacific accounted for 60.88% of global revenue in 2025 and is expected to remain the dominant region through 2031.

Which companies lead the competitive landscape?

Hon Hai, Flex, Jabil, Benchmark Electronics, and Sanmina collectively capture roughly 35%–40% of global revenue, while regional specialists fill niche requirements.

Page last updated on: