Electronics Manufacturing Services For Consumer Electronics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 126.97 Billion |

| Market Size (2031) | USD 165.30 Billion |

| Growth Rate (2026 - 2031) | 5.42% CAGR |

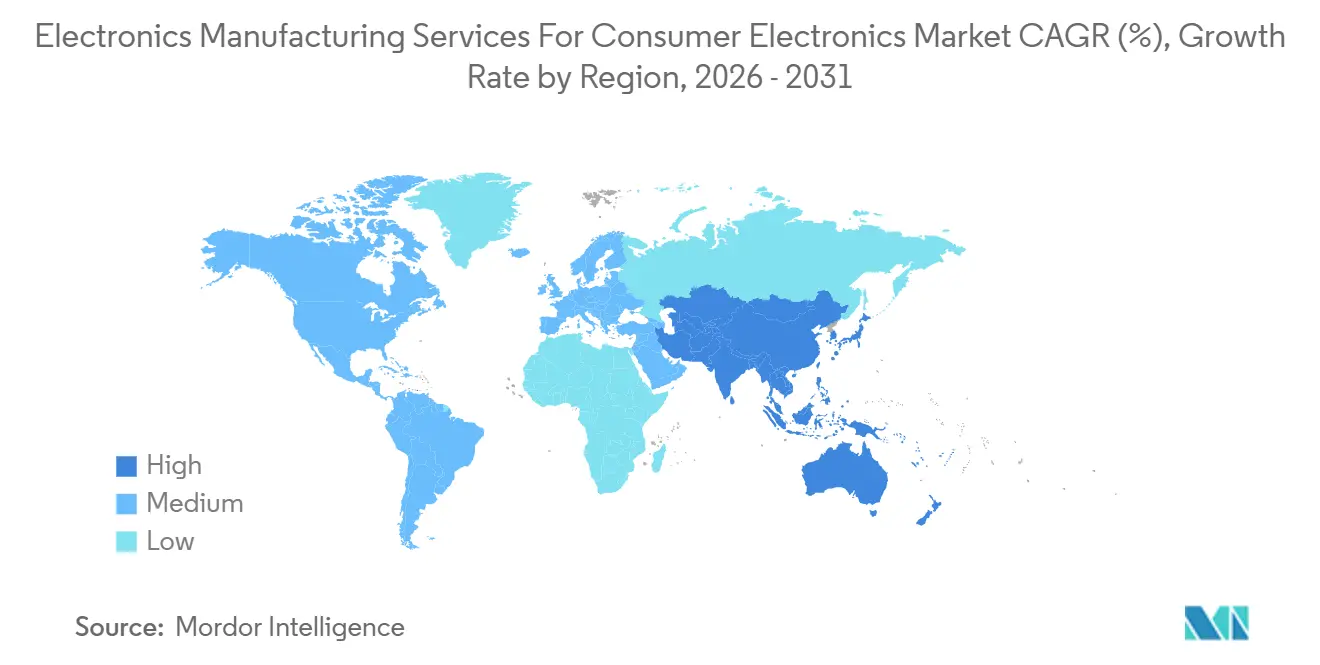

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

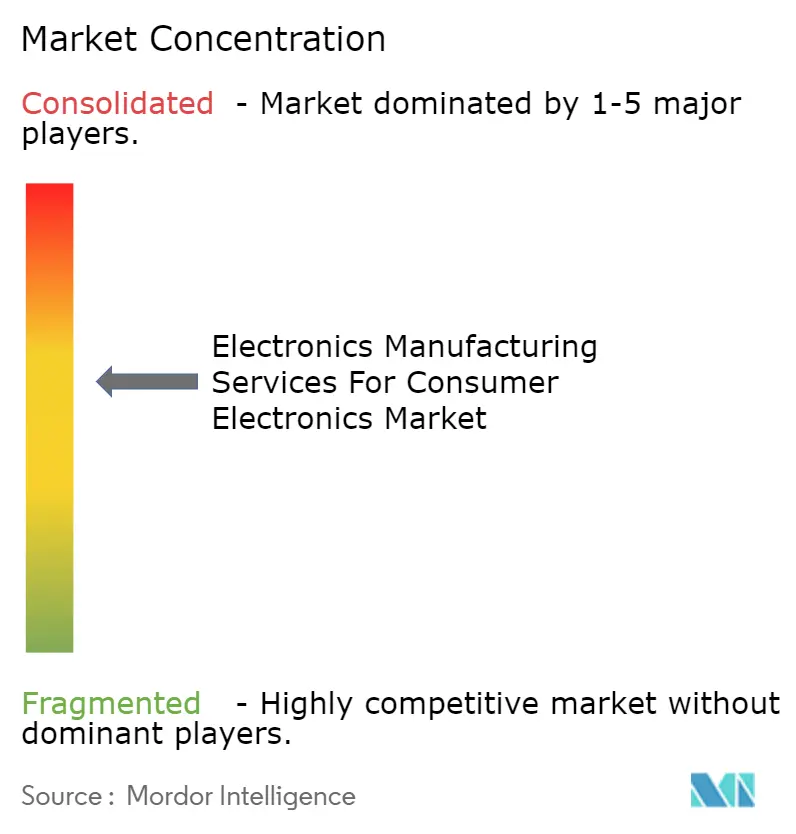

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electronics Manufacturing Services For Consumer Electronics Market Analysis by Mordor Intelligence

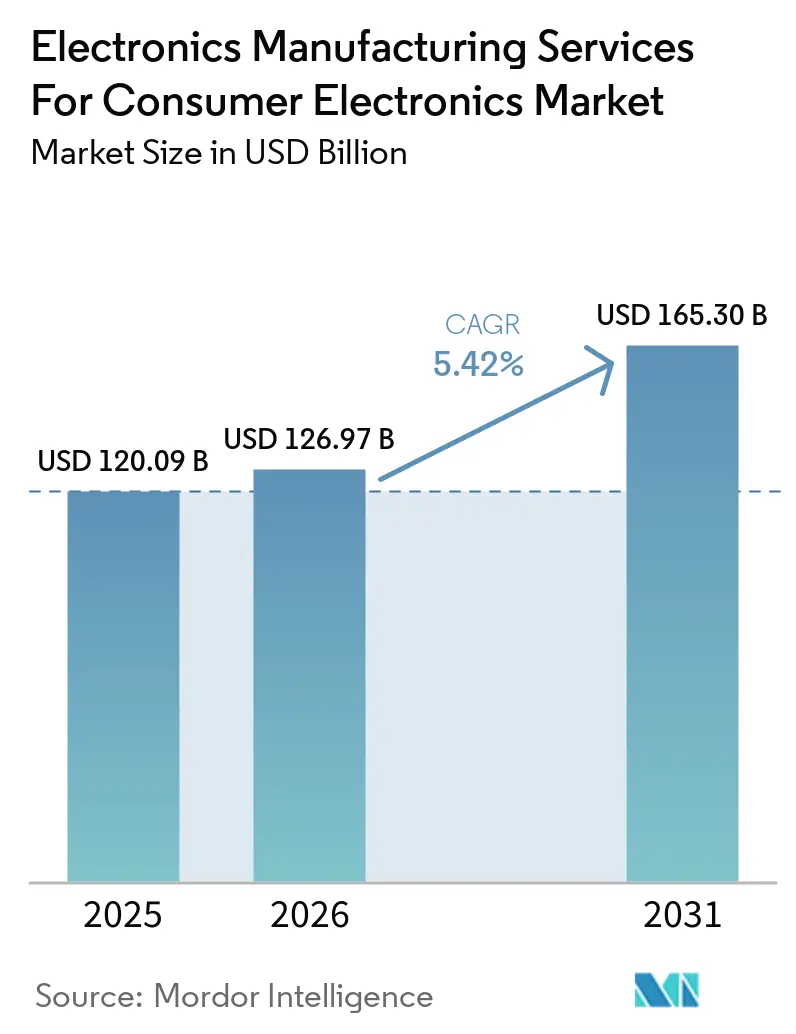

The Electronics Manufacturing Services For Consumer Electronics Market size is expected to grow from USD 120.09 billion in 2025 to USD 126.97 billion in 2026 and is forecast to reach USD 165.30 billion by 2031 at 5.42% CAGR over 2026-2031. Rapid outsourcing by original equipment manufacturers (OEMs), tighter smartphone refresh windows, and a shift toward turnkey assembly models are fueling this upswing. Brands now value agility over pure labor arbitrage, favoring partners that can prequalify new lines and absorb component price volatility. Asia Pacific’s ecosystem depth-from substrate fabrication to advanced packaging-keeps the region in a leadership position, while policy tools such as India’s Production-Linked Incentive (PLI) scheme add momentum. At the same time, U.S. export controls on extreme-ultraviolet lithography equipment have segmented access to leading-edge chips, intensifying competition among Taiwanese, Vietnamese, and Indian providers. Box-build demand, AI-ready advanced packaging, and sustainability mandates under the EU Right-to-Repair Directive round out the core growth levers.

Key Report Takeaways

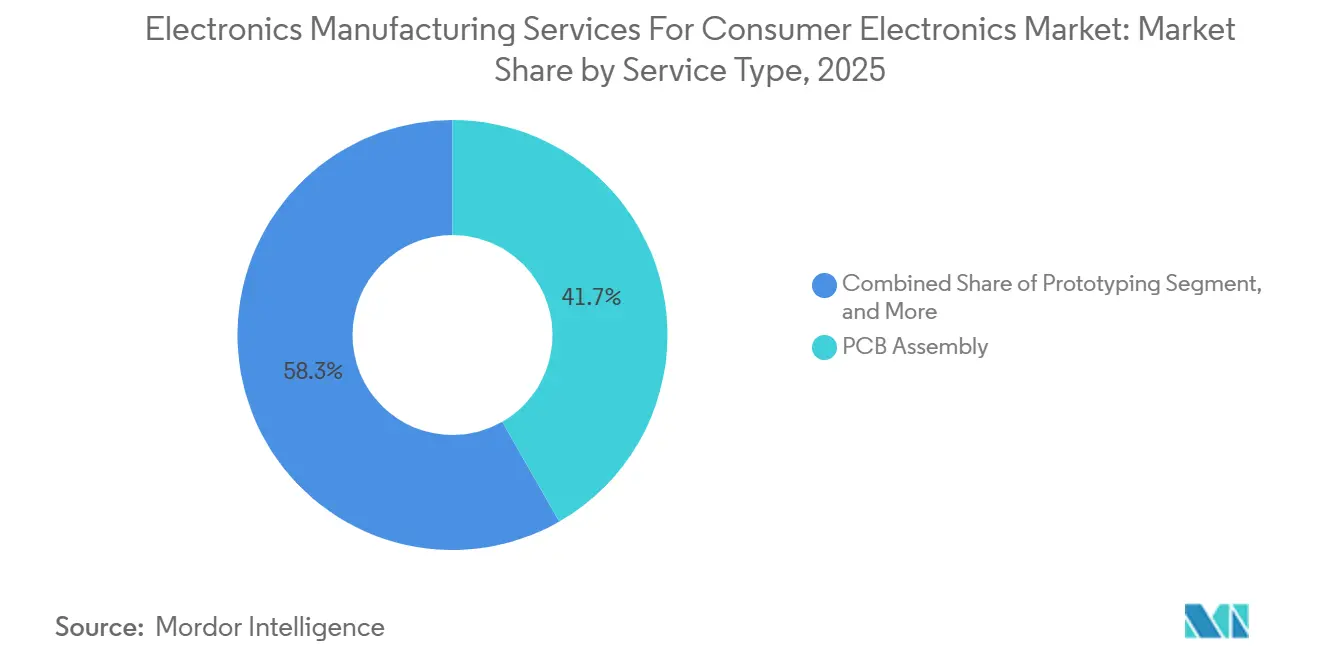

- By service type, PCB assembly led with 41.73% revenue share in 2025; electromechanical and box-build services are advancing at a 5.81% CAGR to 2031.

- By business model, contract manufacturing held 64.46% of the electronics manufacturing services for consumer electronics market share in 2025, while hybrid and turnkey models record the fastest projected CAGR at 6.03% through 2031.

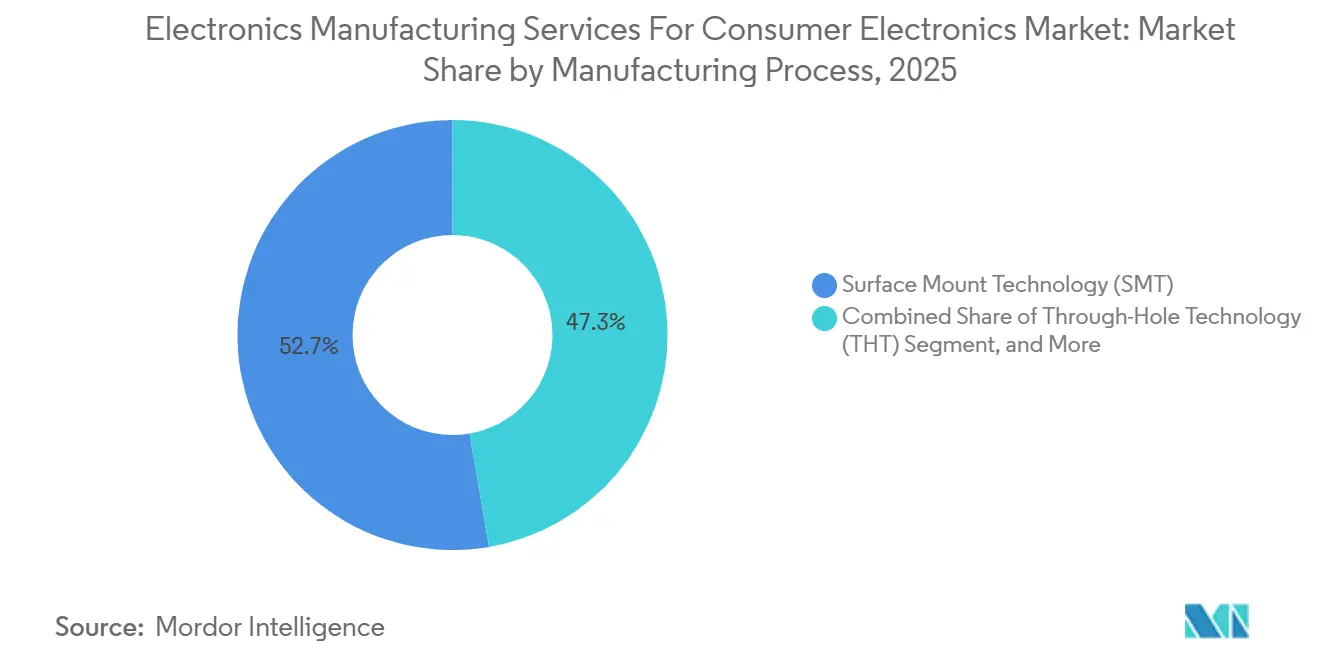

- By manufacturing process, surface-mount technology accounted for 52.71% of the electronics manufacturing services (EMS) for consumer electronics market size in 2025 and advanced packaging processes are expanding at 5.96% CAGR to 2031.

- By region, Asia Pacific captured 60.88% of 2025 revenue and is on track for a 6.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electronics Manufacturing Services For Consumer Electronics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of smart wearables requiring miniaturized high-density EMS | +0.9% | Global (Asia Pacific, North America) | Medium term (2–4 years) |

| Shortening product life cycles in smartphones driving outsourcing | +1.2% | Global (Asia Pacific, North America) | Short term (≤ 2 years) |

| OEM push for regionalized manufacturing, China-plus-one | +1.4% | Asia Pacific (India, Vietnam, Malaysia), North America (Mexico) | Medium term (2–4 years) |

| Adoption of advanced packaging substrates in consumer SoCs | +0.8% | Asia Pacific core, spill-over to North America | Long term (≥ 4 years) |

| Rising demand for eco-designed electronics under EU Right-to-Repair | +0.5% | Europe, global supply chains | Long term (≥ 4 years) |

| Integration of AI accelerators in edge devices boosting complex PCB demand | +0.7% | Global (North America, Asia Pacific) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Proliferation Of Smart Wearables Requiring Miniaturized High-Density EMS

Wearable shipments hit 523 million units in 2025, and the typical smartwatch now packs multilayer rigid-flex boards under 10 mm thick.[1]International Data Corporation. “Worldwide Quarterly Wearable Device Tracker Q4 2025.” 2025. idc.com EMS partners responded by installing laser direct imaging and micro-via drillers that achieve sub-50 µm line widths, enabling densities above 120 components per cm². Thermal management is vital because devices lack active cooling; suppliers co-design spreaders and select chipsets to keep skin-contact temperature below 41 °C, the IEC 62368-1 limit IEC.CH. Apple’s relocation of Watch assembly to a Luxshare cleanroom in Bac Giang underscores the trend toward regionalized wearable production.

Shortening Product Life Cycles In Smartphones Driving Outsourcing

Flagship devices launched in 2025 stayed on shelves for only 9.7 months, compared with 14.2 months in 2020. OEMs therefore offload assembly to EMS partners that spread equipment costs across several brands. Foxconn’s Zhengzhou site can retune 47 SMT lines within 72 hours, swapping stencils and reprogramming pick-and-place heads to pivot among three brands. Outsourcing converts fixed overhead to variable cost, a decisive advantage when obsolescence risk is high.

OEM Push For Regionalized Manufacturing, China-Plus-One

A McKinsey survey found that 68% of global brands established secondary lines outside China in early 2025. India’s PLI reimbursed up to 6% of incremental sales, driving smartphone output to 340 million units in 2025. Vietnam attracted USD 8.9 billion in electronics FDI, though congestion at Hai Phong port added 4.3 days to dwell time. Brands now hedge supply-chain risk by duplicating capacity across South and Southeast Asia.

Adoption Of Advanced Packaging Substrates In Consumer SoCs

Premium smartphones integrate CPU, GPU, and neural cores through fan-out wafer-level packaging and 2.5D interposers. Apple’s A18 leveraged TSMC InFO-PoP stacking for DRAM-on-logic, demanding die-attach accuracy below 5 µm. Intel’s Foveros Direct 3D, in volume since Q2 2025, signals a future cascade into mid-tier devices. EMS providers investing in ISO Class 6 cleanrooms and X-ray metrology are poised to capture this high-margin work.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Margin pressure from volatile commodity prices | -0.6% | Global (Asia Pacific, Europe) | Short term (≤ 2 years) |

| Geopolitical export controls on advanced semiconductor technology | -0.8% | Asia Pacific (China), global spill-over | Medium term (2–4 years) |

| Labor shortages and wage inflation in key EMS hubs | -0.5% | Asia Pacific (Vietnam, India, Malaysia) | Medium term (2–4 years) |

| Environmental compliance costs, RoHS3 and PFAS bans | -0.3% | Europe, global supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Margin Pressure From Volatile Commodity Prices

Copper swung between USD 8,200 and USD 10,400 per ton in 2025, while epoxy resin climbed 14% year on year.[2]London Metal Exchange. “Copper Prices 2025.” 2025. lme.com PCB laminate, up to 22% of bill-of-materials, drove EMS gross-margin compression; Flex saw a 120 basis-point dip in fiscal Q3 2025 despite pass-through clauses. Smaller firms lacking scale struggle most, occasionally exiting low-complexity builds.

Geopolitical Export Controls On Advanced Semiconductor Technology

U.S. rules effective October 2024 bar 14 nm-and-below logic tools from Chinese EMS firms. Mainland providers pivoted to mature-node chips, ceding flagship programs to Taiwanese and Southeast Asian rivals with access to 5-nm parts. Luxshare and BYD locked in TSMC allocations for 2026 devices, whereas Wingtech struggled to source comparable silicon. The result is a two-tier EMS landscape split along lines of technology access.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Box Build Gains as Brands Seek Turnkey Partners

PCB assembly accounted for 41.73% of 2025 revenue, anchoring the electronics manufacturing services for consumer electronics market. However, electromechanical and box-build contracts are forecast to expand at 5.81%, surpassing overall growth as brands consolidate suppliers. This shift reflects demand for turnkey enclosures, thermal solutions, and final testing within a single purchase order, trimming coordination costs and boosting launch velocity.

Box-build fees often bundle cable routing, firmware flashing, and packaging, allowing EMS partners to capture a larger share of project value. Prototyping remained niche yet crucial for design-for-manufacturing validation, with Sanmina delivering sub-10-day cycles.[3]Sanmina Corporation. “Annual Report 2025.” 2025. sanmina.com Testing services gained profile as AI-centric boards require neural-network accuracy checks, prompting Benchmark to boost automated-test capacity by 18% in 2025. The EMS for consumer electronics market size for box-build is therefore positioned to widen its slice through 2031.

By Business Model: Hybrid Models Rise as Brands Lack Design Resources

Contract manufacturing held 64.46% of 2025 revenue, yet hybrid and turnkey arrangements are projected to scale at 6.03%, the swiftest pace among models. Start-ups in wearables and IoT prefer partners that deliver industrial design, antenna tuning, and power management, compensating for their limited engineering bench. Chinese ODM specialists offer standardized reference designs priced 15-20% below those of Taiwanese peers, enticing cost-conscious brands.

Hybrid agreements see EMS firms supply subsystems, such as Pegatron’s vapor-chamber cooling, that cut throttling by 18%, while OEMs retain user-experience control. As a result, the electronics manufacturing services for consumer electronics market adapt to co-creation models, letting providers embed themselves earlier in product cycles and secure thicker margins. The electronics manufacturing services for consumer electronics industry thus evolve from build-to-print toward shared IP ecosystems.

By Manufacturing Process: Advanced Packaging Responds to AI Integration

Surface-mount technology accounted for 52.71% of 2025 process revenue, underscoring its ubiquity. Yet advanced packaging and hybrid flows will climb at 5.96% through 2031 as AI accelerators and high-bandwidth memory push bandwidth beyond 1 TB/s. EMS leaders combine SMT with wafer-level chip-scale and 2.5D interposers for system-in-package modules, boosting device performance while shrinking footprints.

Amkor’s 12 mm × 14 mm module that integrated an application processor, PMIC, and RF chip reduced the mainboard area by 23%, demonstrating hybrid gains. Cleanroom investments, ISO Class 6 certification, and X-ray inspection lift capital intensity but unlock assembly fees 40-60% above standard SMT rates. Consequently, the electronics manufacturing services for consumer electronics market size linked to advanced packaging is on a strong trajectory, while through-hole technology persists only for high-stress connectors and batteries

Geography Analysis

Asia Pacific generated 60.88% of global revenue for the EMS for consumer electronics market in 2025 and is projected to expand at a 6.55% CAGR through 2031, maintaining the region’s leadership position. The electronics manufacturing services for consumer electronics market share advantage stems from dense component ecosystems in Guangdong, Jiangsu, and Penang, coupled with India’s PLI incentives that reimburse up to 6% of incremental sales for five years. Vietnam attracted USD 8.9 billion in electronics foreign direct investment in 2025, yet port congestion at Hai Phong extended container dwell time by 4.3 days, eroding logistics savings that initially drew OEMs from China. Malaysia’s Kulim corridor strengthened test and packaging depth, while Thailand concentrated on mid-tier smartphone assembly, ensuring that the electronics manufacturing services for consumer electronics market continue to pivot around a multi-country Asia Pacific supply base.

India’s electronic manufacturing services for the consumer electronics market size accelerated as smartphone output hit 340 million units in 2025, with exports comprising 58% of shipments.[4]Ministry of Electronics and Information Technology. “PLI Annual Report 2025.” 2025. meity.gov.in Foxconn, Pegatron, and Wistron installed box-build lines in Tamil Nadu, Uttar Pradesh, and Karnataka, exploiting bonded-warehouse rules that reduce customs clearance to 12 hours. Vietnam’s Bac Ninh province hosts Samsung’s six-plant complex, anchoring a cluster of tier-2 printed circuit board and lens suppliers that shortens lead times by 27% relative to components shipped from Shenzhen. Mexico’s Guadalajara and Chihuahua facilities serve as regional hubs for laptop and networking gear, leveraging USMCA rules that waive tariffs on assemblies with 75% North American value content. Collectively these locations form the backbone of the China-plus-one strategy, giving OEMs alternate routes when export controls or pandemic restrictions disrupt Chinese supply lines.

North America and Europe together commanded under 25% of 2025 revenue but focus on high-mix, low-volume builds that demand tight intellectual-property security and proximity to design teams. U.S. facilities in California and Texas specialize in advanced packaging pilots and ruggedized tablets for defense uses, while Romanian and Polish factories assemble battery-management systems for European electric-vehicle programs. Brazil protects its consumer-electronics base through tariff barriers and localized content rules, driving EMS firms such as Flex to certify Brazilian subsidiaries for ISO 14001 to win public-sector orders. The Middle East and Africa remain niche, with the United Arab Emirates serving primarily as a logistics re-export hub that feeds European and African channels. As policy and labor variables evolve, parallel capacity across three continents is now essential to preserve supply continuity in the electronics manufacturing services for consumer electronics market.

Competitive Landscape

The top five providers- Foxconn, Pegatron, Flex, Wistron, and Jabil- collectively held a considerable share of 2025 revenue, underscoring a moderately concentrated electronics manufacturing services for consumer electronics market. Taiwanese leaders defended share by automating legacy lines; Foxconn deployed 1,200 collaborative robots that lowered smartphone labor minutes 31% at its Zhengzhou campus, enhancing cost resilience. Pegatron invested USD 800 million to open a Tamil Nadu laptop plant that trimmed the assembly cycle time by 22% through in-line functional test cells, signaling a strategic push into premium PC segments.

Chinese challengers such as Luxshare and BYD Electronic gained ground by offering integrated design and manufacturing packages priced up to 20% below Taiwanese equivalents, particularly in wearables and audio devices. Luxshare’s 51% acquisition of a Vietnamese EMS firm delivered 180,000 m² of floor space and embedded access to Samsung’s supply chain, enabling rapid ramp of smartphone box-build orders. BYD opened a 120,000 m² ISO Class 7 facility in Shenzhen focused on rigid-flex wearables, achieving defect rates below 50 ppm via automated optical inspection.

Emerging disruptors from India, including Dixon Technologies and Bhagwati Products, leverage PLI cash subsidies to undercut foreign contract assemblers in entry-level smartphones and hearables. Technology differentiation is also accelerating: Jabil installed computer-vision quality gates in Penang that cut false rejects 47% while Benchmark added 240-vector-per-second automated test equipment in Suzhou to validate neural-processing boards. Coupled with blockchain traceability pilots aimed at EU sustainability audits, these moves show that digital capability, not location alone, is shaping future competitive advantage in the electronics manufacturing services for consumer electronics market.

Electronics Manufacturing Services For Consumer Electronics Industry Leaders

Foxconn Technology Group

Pegatron Corporation

Flex Ltd.

Jabil Inc.

Wistron Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Foxconn confirmed a USD 2.3 billion campus in Karnataka, India, with 50 million-unit annual capacity for smartphones, tablets, and wearables.

- November 2025: Luxshare completed a USD 340 million acquisition of a Vietnamese EMS company, adding three factories and 12,000 staff.

- October 2025: Pegatron inaugurated an USD 800 million Tamil Nadu facility for laptops and tablets, starting with 4 million units yearly and scalable to 8 million.

- September 2025: Flex and an automotive-electronics partner invested USD 150 million in a Guadalajara ADAS assembly joint venture.

- August 2025: Jabil won a USD 1.2 billion five-year turnkey contract for an IoT device family produced in Malaysia and Mexico.

Global Electronics Manufacturing Services For Consumer Electronics Market Report Scope

The Electronics Manufacturing Services for Consumer Electronics Market Report is Segmented by Service Type (Electronic Manufacturing Services including PCB Assembly, Electromechanical Assembly/Box Build, Prototyping, and Other Services; Engineering Services; Test and Development Implementation; Logistics Services; and Other Service Types), Business Model (Contract Manufacturing, Original Design Manufacturing, and Hybrid/Turnkey/Other Models), Manufacturing Process (Surface Mount Technology, Through-Hole Technology, and Advanced Packaging/Hybrid Processes), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | |

| Prototyping | |

| Other Electronic Manufacturing Services | |

| Engineering Services | |

| Test and Development Implementation | |

| Logistics Services | |

| Other Service Types |

| Contract Manufacturing (CM) |

| Original Design Manufacturing (ODM) |

| Hybrid / Turnkey / Other Business Models |

| Surface Mount Technology (SMT) |

| Through-Hole Technology (THT) |

| Advanced Packaging / Hybrid Processes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| South-east Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Service type | Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | ||

| Prototyping | ||

| Other Electronic Manufacturing Services | ||

| Engineering Services | ||

| Test and Development Implementation | ||

| Logistics Services | ||

| Other Service Types | ||

| By Business Model | Contract Manufacturing (CM) | |

| Original Design Manufacturing (ODM) | ||

| Hybrid / Turnkey / Other Business Models | ||

| By Manufacturing Process | Surface Mount Technology (SMT) | |

| Through-Hole Technology (THT) | ||

| Advanced Packaging / Hybrid Processes | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| South-east Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What share does Asia Pacific hold in electronic manufacturing services for consumer electronics?

Asia Pacific captured 60.88% of 2025 revenue and is projected to grow at a 6.55% CAGR through 2031.

Which service segment is expanding fastest?

Electromechanical and box-build services post the highest growth, advancing at 5.81% from 2026 to 2031.

How are OEMs mitigating export-control risks?

Brands duplicate capacity across India, Vietnam, and Mexico so they can reroute production if China faces new restrictions.

Why are hybrid business models gaining traction?

Emerging wearable and IoT brands lack in-house engineering and rely on EMS partners for design plus manufacturing, driving a 6.03% CAGR in hybrid and turnkey contracts.

What technology investments differentiate leading EMS firms?

Advanced packaging cleanrooms, collaborative-robot assembly, computer-vision defect detection, and blockchain traceability systems help providers win premium contracts.

Page last updated on: