Electronic Manufacturing Services For Industrial Device Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 99.51 Billion |

| Market Size (2031) | USD 135.76 Billion |

| Growth Rate (2026 - 2031) | 6.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electronic Manufacturing Services For Industrial Device Market Analysis by Mordor Intelligence

The Electronic Manufacturing Services for Industrial Device market size stood at USD 99.51 billion in 2026 and is forecast to reach USD 135.76 billion by 2031, reflecting a 6.41% CAGR over 2026-2031. Outsourcing depth is widening as industrial OEMs reallocate capital from captive assembly lines to software-centric R&D, while edge-computing adoption reshapes controller and gateway designs. Near-shore investments in Mexico and Eastern Europe are fragmenting supply chains that were previously centered in coastal China, prompted by the United States CHIPS and Science Act and the European Union Critical Raw Materials Act[1]Source: U.S. Department of Commerce, “CHIPS Act Implementation Progress,” commerce.gov. Accelerated deployment of box-build micro-factories in brownfield plants, coupled with OEM demand for design-for-manufacturability expertise, is moving EMS revenue toward turnkey models. Persistent headwinds include skilled-labor inflation in North America and Europe and semiconductor lead-time volatility that inflates inventory carrying costs.

Key Report Takeaways

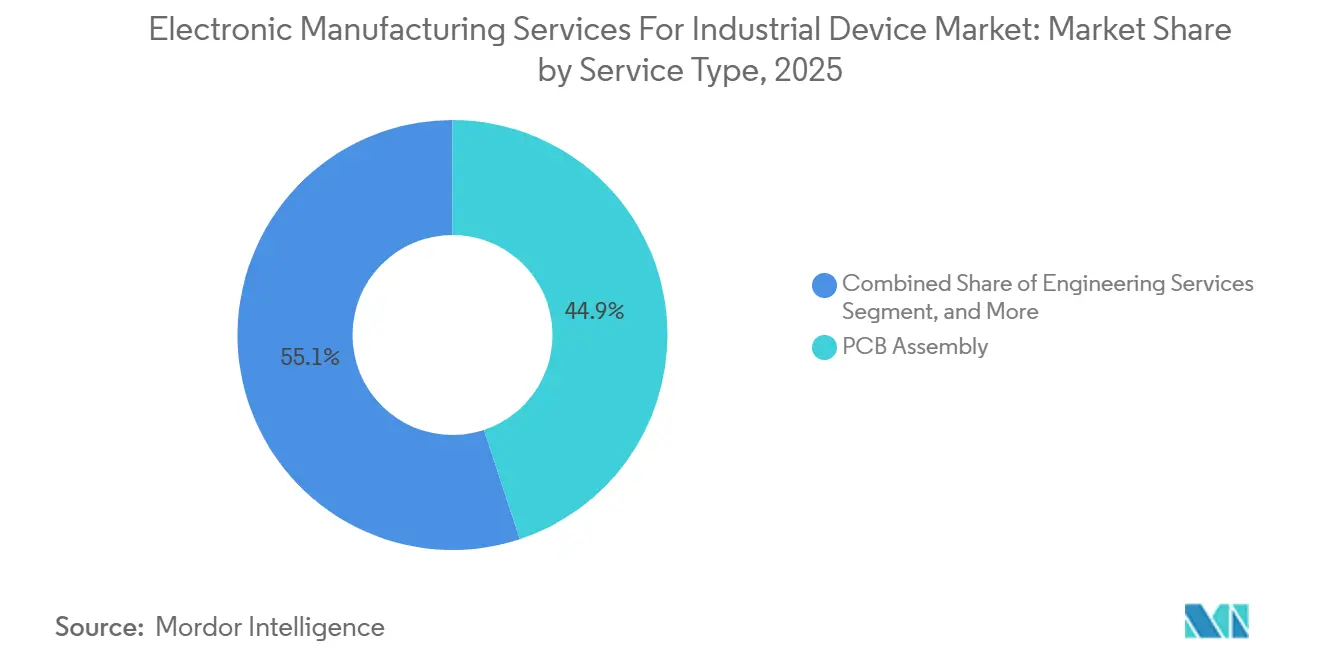

- By service type, printed circuit board assembly commanded 44.92% of Electronic Manufacturing Services for Industrial Device market share in 2025, while electromechanical box-build services are projected to expand at a 6.73% CAGR through 2031.

- By business model, contract manufacturing held 60.11% share of the Electronic Manufacturing Services for Industrial Device market size in 2025 and hybrid turnkey arrangements are forecast to grow at a 6.97% CAGR during 2026-2031.

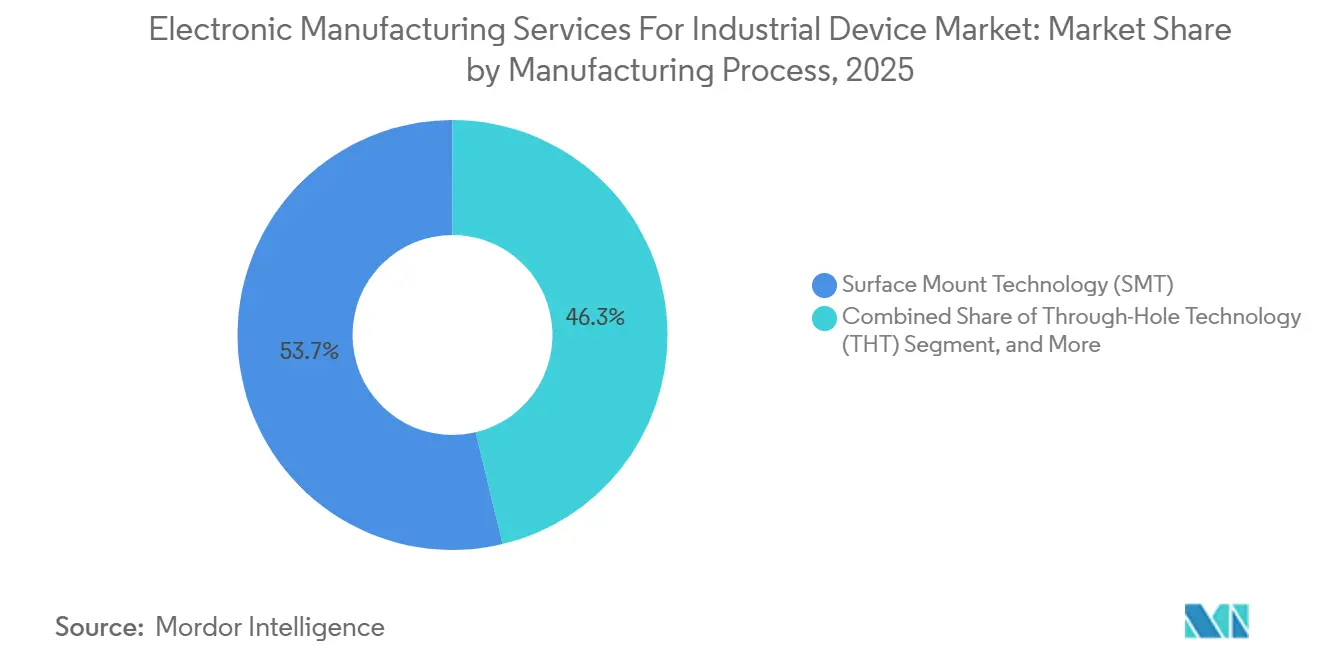

- By manufacturing process, surface-mount technology represented 53.73% of revenue in 2025, yet advanced packaging and hybrid processes are poised to advance at a 7.13% CAGR up to 2031.

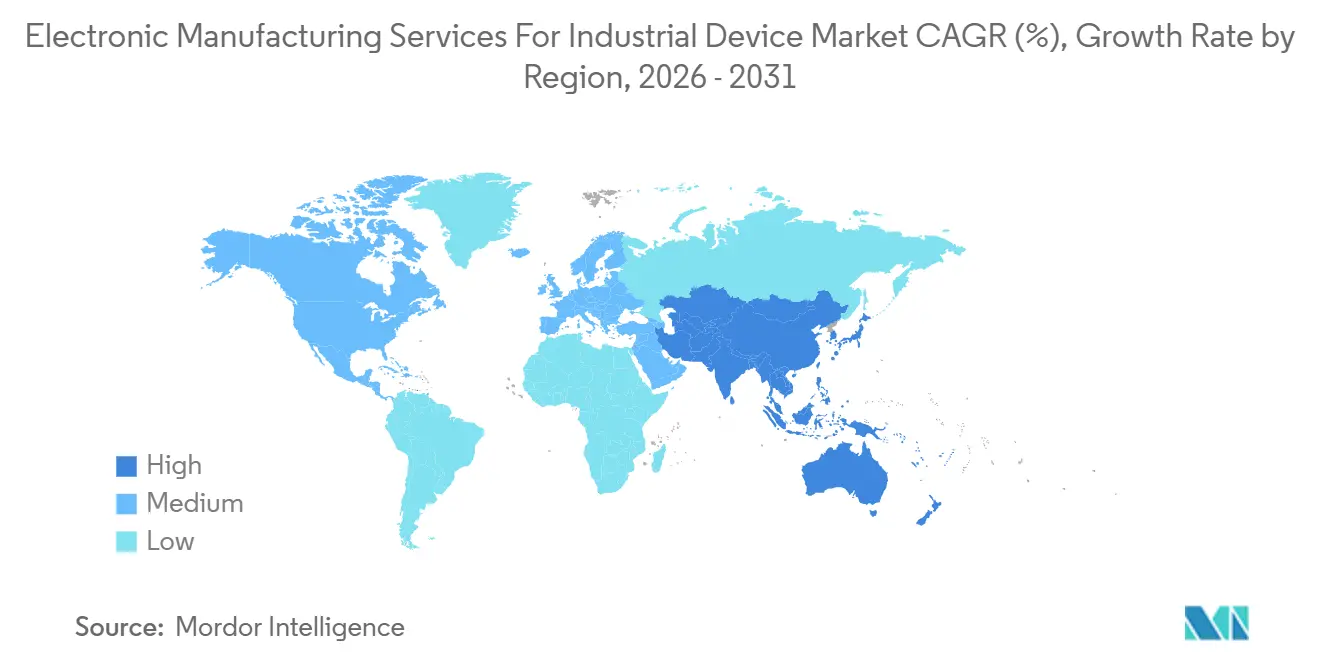

- By geography, Asia Pacific accounted for 55.83% of 2025 revenue and is anticipated to log the fastest regional CAGR at 7.57% through 2031, underpinned by investments in India and Vietnam.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electronic Manufacturing Services For Industrial Device Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM Cost-Reduction Imperatives Sustain Outsourcing Momentum | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Growth of Industrial Automation and IIoT Hardware | +1.5% | Global, led by APAC manufacturing hubs and North America industrial corridors | Long term (≥4 years) |

| Rising Demand for AI-Ready Edge Controllers and Gateways | +0.9% | North America, Europe, and APAC Tier-1 cities | Medium term (2-4 years) |

| Regulatory Push for Localized Supply Chains in North America and Europe | +0.8% | North America and Europe, with spillover to Mexico and Eastern Europe | Short term (≤2 years) |

| Near-Shore Capacity Expansion in Mexico and Eastern Europe | +0.7% | Mexico (Tijuana, Guadalajara), Poland, Czech Republic, Romania | Short term (≤2 years) |

| On-Site Box-Build Micro-Factories for Brownfield Plants | +0.5% | North America and Europe industrial belts, early adoption in Germany and U.S. Midwest | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

OEM Cost-Reduction Imperatives Sustain Outsourcing Momentum

OEMs in industrial automation, process control, and instrumentation have accelerated divestitures of in-house SMT lines to free capital for predictive-maintenance software and digital-twin development. Sanmina noted that 63% of its 2025 customer wins originated from OEMs shuttering internal lines, a 22-point rise over 2023[2]Source: Sanmina Corporation, “Form 10-K Annual Report 2025,” sanmina.com. Mid-tier OEMs between USD 500 million and USD 2 billion revenue experience the sharpest return-on-capital drag from captive fabrication, pushing them toward bundled EMS agreements that fix procurement, assembly, test, and logistics costs. European energy price inflation lifted the total cost of ownership for internal assembly by 18% between 2024 and 2025, reinforcing outsourcing decisions[3]Source: Financial Times, “Europe Energy Costs Manufacturing Impact,” ft.com. Although EMS partners now manage more of the physical build, OEMs maintain firmware and embedded-software control by deploying secure enclaves inside EMS facilities to protect intellectual property.

Growth of Industrial Automation and IIoT Hardware

Predictive-maintenance programs in automotive, aerospace, and heavy-equipment plants have accelerated demand for ruggedized gateways and controllers that meet extended-temperature and vibration benchmarks. Each gateway requires conformal-coated PCB assemblies and vibration-resistant solder joints, prompting EMS providers to upgrade reflow ovens, X-ray inspection, and selective-soldering lines. Flex reported that its industrial segment grew 19% year-over-year in Q3 2025, with IIoT hardware contributing 41% of that gain. The need to encapsulate power supplies, cooling modules, and I/O interfaces inside IP65 enclosures is lifting box-build revenue. Compliance with IEC 61131-3 programmable-controller standards has become standard, pressuring smaller EMS firms to invest in certification or exit the industrial vertical.

Rising Demand for AI-Ready Edge Controllers and Gateways

Industrial OEMs are embedding inference accelerators inside programmable logic controllers for real-time anomaly detection without cloud latency. Benchmark Electronics indicated that orders for edge controllers with neural-processing units advanced 34% in H1 2025, primarily from semiconductor-equipment and pharmaceutical customers. These designs require flip-chip bonding and through-silicon vias, specialized processes that only about 18% of EMS providers could supply as of early 2025. The capital burden is elevating entry barriers, while the EU AI Act imposes rigorous traceability of training data for safety-critical applications, adding documentation overhead for EMS partners handling firmware integration.

Regulatory Push for Localized Supply Chains

The CHIPS and Science Act earmarks USD 39 billion in direct subsidies and USD 75 billion in loan guarantees for U.S. semiconductor and electronics capacity, with 22% dedicated to industrial electronics as of December 2025. Complementary EU initiatives incentivize EMS providers to locate final assembly within 500 km of automotive and industrial design hubs. Celestica opened a 75,000 sq ft industrial-electronics plant in Brno, Czech Republic, to skirt tariffs and pare lead times for regional OEMs. Localization shifts are fragmenting once-consolidated Asian supply chains, raising logistics complexity and inventory days outstanding.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Margin Pressure from Rising Skilled-Labor Costs | -0.6% | North America, Europe, and Tier-1 APAC cities (Singapore, Tokyo) | Short term (≤2 years) |

| Volatile Semiconductor Lead Times Disrupt Production Schedules | -0.8% | Global, with acute impact in North America and Europe | Short term (≤2 years) |

| Industrial Firmware IP-Protection Concerns | -0.3% | Global, concentrated in high-value industrial verticals (aerospace, defense, medical) | Medium term (2-4 years) |

| Scope-3 Emissions Audits Increasing Compliance Costs | -0.4% | Europe and North America, with emerging requirements in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Margin Pressure From Rising Skilled-Labor Costs

Median hourly wages for electronics-assembly technicians in the United States climbed 11% to USD 28.40 in 2025, while European rates advanced 9% to EUR 24.60 (USD 27.80). Near-shore hubs such as Mexico and Poland experience intensified competition for talent as EMS providers battle automotive and aerospace industries for the same certified labor pool. Plexus disclosed that labor costs as a share of revenue rose 140 basis points in 2025, compressing operating margins to 5.8% from 7.2% a year earlier. Automation can relieve some pressure, yet collaborative-robot payback periods often exceed 36 months, deterring smaller firms.

Volatile Semiconductor Lead Times Disrupt Production Schedules

Industrial-grade microcontroller and power-management IC lead times oscillated between 18 and 34 weeks in 2025, with allocation conflicts arising from automotive and renewable-energy surges. EMS providers boosted safety stock, but inventory days outstanding at Jabil lengthened to 68 days from 54 days in 2024. A single missing component can stall box-build lines, and smaller EMS houses without direct foundry relationships often pay 20-30% distributor premiums for expedited shipments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Box-Build Momentum Reflects Brownfield IIoT Demand

PCB assembly retained a 44.92% revenue share of the Electronic Manufacturing Services for Industrial Device market in 2025. However, electromechanical box-build revenue is forecast to grow at 6.73% CAGR through 2031 as industrial clients retrofit legacy machinery with IIoT gateways, avoiding wholesale line replacements. The Electronic Manufacturing Services for Industrial Device market size tied to prototyping expanded when Venture Corporation logged a 27% rise in new-product-introduction projects during 2025, largely from industrial-robotics customers.

The pivot toward box-build work is most visible in plants older than 15 years; Zollner noted that 58% of 2025 box-build projects involved equipment that old. Logistics services that synchronize component arrival with production have become differentiators, and test-and-development requests are climbing as regulators demand pre-certification for electronics deployed in hazardous environments. Engineering services that cut field-failure rates below 0.5% are supporting ISO 9001:2015 compliance and commanding premium margins.

By Business Model: Hybrid Turnkey Models Capture Design-for-Manufacturability Value

Contract manufacturing still held 60.11% of 2025 revenue, yet hybrid turnkey models are projected to book a 6.97% CAGR to 2031, outpacing traditional approaches. The Electronic Manufacturing Services for Industrial Device market size attached to turnkey engagements is expanding because OEMs seek co-design input that trims prototyping cycles and shifts tooling risk to EMS partners. Fabrinet stated that turnkey contracts comprised 41% of its industrial revenue in Q2 2025, up from 28% two years prior.

OEMs accept risk-sharing structures where EMS suppliers co-invest in fixtures against multi-year volume commitments. ODM remains centered in Asia Pacific; Universal Scientific Industrial saw ODM revenue climb 16% in 2025, fueled by automation customers. Cybersecurity compliance under IEC 62443 further lifts turnkey demand, as EMS firms with certified secure-development lifecycles can expedite regulatory approvals.

By Manufacturing Process: Advanced Packaging Gains Traction for Edge-AI Modules

Surface-mount technology captured 53.73% of 2025 revenue, but advanced packaging and hybrid processes are set to rise at 7.13% CAGR, the fastest within the Electronic Manufacturing Services for Industrial Device market. Fine-pitch components below 0.4 mm are driving placement-equipment upgrades, while through-hole assembly persists for high-stress railway and grid-automation boards.

Adoption of wafer-level fan-out and system-in-package designs is accelerating among EMS providers that serve semiconductor-equipment and medical-device OEMs. Wistron qualified fan-out wafer-level packaging for edge-computing modules in September 2025 to target autonomous robots and collaborative arms. Hybrid processes combining SMT, through-hole, and wire-bonding suit power-electronics boards where high-current traces and digital controls co-exist. Achieving IPC-6012 Class 3 certification for high-reliability PCBs compels smaller EMS firms to upgrade traceability systems.

Geography Analysis

Asia Pacific generated 55.83% of Electronic Manufacturing Services for Industrial Device market revenue in 2025 and is forecast to post a 7.57% CAGR through 2031, the fastest regional growth. India’s production-linked incentive scheme drew USD 8.3 billion in EMS pledges by December 2025, with Foxconn, Wistron, and Pegatron scaling plants in Tamil Nadu and Karnataka. Vietnam and Thailand continue to capture relocation from Guangdong and Jiangsu, trimming China’s share by 4.2 points between 2023 and 2025. Japan and South Korea focus on high-precision industrial-robotics assemblies that command premium pricing.

North America represented roughly 22% of 2025 revenue, supported by CHIPS Act grants and OEM preferences for near-shore suppliers that shrink lead times. Mexico is the region’s growth engine, with SMT capacity in Tijuana, Guadalajara, and Monterrey expanding 18% year-over-year in 2025. The United States channels subsidies toward defense and critical-infrastructure electronics; Benchmark and Plexus expanded facilities in New Hampshire and Wisconsin to serve these verticals. Canada’s EMS base concentrates in Ontario and Quebec with aerospace and automation exposure.

Europe held about 18% of 2025 revenue, with Poland, Czech Republic, and Romania registering double-digit EMS growth as German and French OEMs hedge against Asia-Pacific supply risk. Celestica’s Brno plant illustrates this shift. Germany remains Europe’s largest market, yet labor-cost inflation and energy volatility limit margin upside. South America and the Middle East and Africa together contribute under 5% of revenue, with growth centered in Brazil and the United Arab Emirates. Compliance with RoHS and REACH rules adds 3-5% to ownership costs for EMS suppliers serving European customers.

Competitive Landscape

Competition is moderately concentrated: the top five players held around 38% of 2025 revenue in the Electronic Manufacturing Services for Industrial Device market. Foxconn, Jabil, and Flex are channeling capital into advanced packaging lines for AI-enabled edge modules, while Sanmina and Celestica differentiate via design-for-manufacturability consulting bundled with assembly. Tier-2 Southeast Asian providers underpriced incumbents by 12-15% in 2025, winning share on cost but lacking vertical integration.

Patent activity around AI-driven optical inspection climbed 34% in 2025, with Jabil and Benchmark filing heavily for machine-vision defect-detection systems. On-site micro-factories positioned within OEM premises are emerging as whitespace; small Indian and Vietnamese firms offer sub-500-unit minimums, appealing to niche automation innovators. Leaders now deploy digital twins of assembly lines, cutting new-product-introduction cycles by up to 30%, and tie analytics to first-pass yield metrics to sustain margin despite wage inflation.

Scope-3 emissions audits mandated by the International Sustainability Standards Board raise compliance expense, disproportionately burdening small regional EMS operators lacking ESG reporting infrastructure. Acquisition interest from well-capitalized players is rising, with recent deals such as Jabil’s Guadalajara plant purchase and Plexus’ Wisconsin specialty acquisition illustrating the trend.

Electronic Manufacturing Services For Industrial Device Industry Leaders

Foxconn Technology Group

Jabil Inc.

Flex Ltd.

Pegatron Corporation

Sanmina Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Foxconn committed USD 1.2 billion to a 250,000 sq ft industrial-electronics facility in Bengaluru, India, slated for Q3 2027 operation.

- December 2025: Jabil bought a 120,000 sq ft Guadalajara plant to boost near-shore capacity for North American automation customers.

- November 2025: Flex and Siemens partnered to co-develop AI-enabled edge controllers for automotive and discrete manufacturing, targeting Q2 2026 launch.

- October 2025: Celestica opened a EUR 45 million (USD 50.9 million)-investment plant in Brno, Czech Republic, equipped with SMT, through-hole, and box-build lines.

Global Electronic Manufacturing Services For Industrial Device Market Report Scope

The Electronic Manufacturing Services for Industrial Device Market refers to the provision of specialized manufacturing, engineering, testing, and logistics services for industrial devices. These services include PCB assembly, electromechanical assembly/box build, prototyping, and other related offerings.

The Electronic Manufacturing Services for Industrial Device Market Report is Segmented by Service Type (Electronic Manufacturing Services including PCB Assembly, Electromechanical Assembly/Box Build, Prototyping, Other Services; Engineering Services; Test and Development Implementation; Logistics Services; and Other Service Types), Business Model (Contract Manufacturing, Original Design Manufacturing, and Hybrid/Turnkey/Other Models), Manufacturing Process (Surface Mount Technology, Through-Hole Technology, and Advanced Packaging/Hybrid Processes), and Geography (North America, Europe, Asia Pacific, South America; and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly / Box Build | |

| Prototyping | |

| Other Electronic Manufacturing Services | |

| Engineering Services | |

| Test and Development Implementation | |

| Logistics Services | |

| Other Service Types |

| Contract Manufacturing (CM) |

| Original Design Manufacturing (ODM) |

| Hybrid / Turnkey / Other Business Models |

| Surface Mount Technology (SMT) |

| Through-Hole Technology (THT) |

| Advanced Packaging / Hybrid Processes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| South-East Asia | |

| Rest of Asia Pacific | |

| South America | |

| Middle East and Africa |

| By Service Type | Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly / Box Build | ||

| Prototyping | ||

| Other Electronic Manufacturing Services | ||

| Engineering Services | ||

| Test and Development Implementation | ||

| Logistics Services | ||

| Other Service Types | ||

| By Business Model | Contract Manufacturing (CM) | |

| Original Design Manufacturing (ODM) | ||

| Hybrid / Turnkey / Other Business Models | ||

| By Manufacturing Process | Surface Mount Technology (SMT) | |

| Through-Hole Technology (THT) | ||

| Advanced Packaging / Hybrid Processes | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| South-East Asia | ||

| Rest of Asia Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Electronic Manufacturing Services for Industrial Device market?

The market was valued at USD 99.51 billion in 2026 and is projected to reach USD 135.76 billion by 2031.

Which region is expanding the fastest?

Asia Pacific is expected to post a 7.57% CAGR through 2031, driven by India and Vietnam absorbing capacity from China.

Why are OEMs shifting to hybrid turnkey models?

Hybrid turnkey models bundle design-for-manufacturability and assembly, reducing OEM tooling outlays and accelerating product launches.

What manufacturing process is gaining share for edge-AI modules?

Advanced packaging and hybrid processes are projected to grow at a 7.13% CAGR, outpacing traditional SMT.

Page last updated on: