Electronic Manufacturing Services For Healthcare And Medical Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

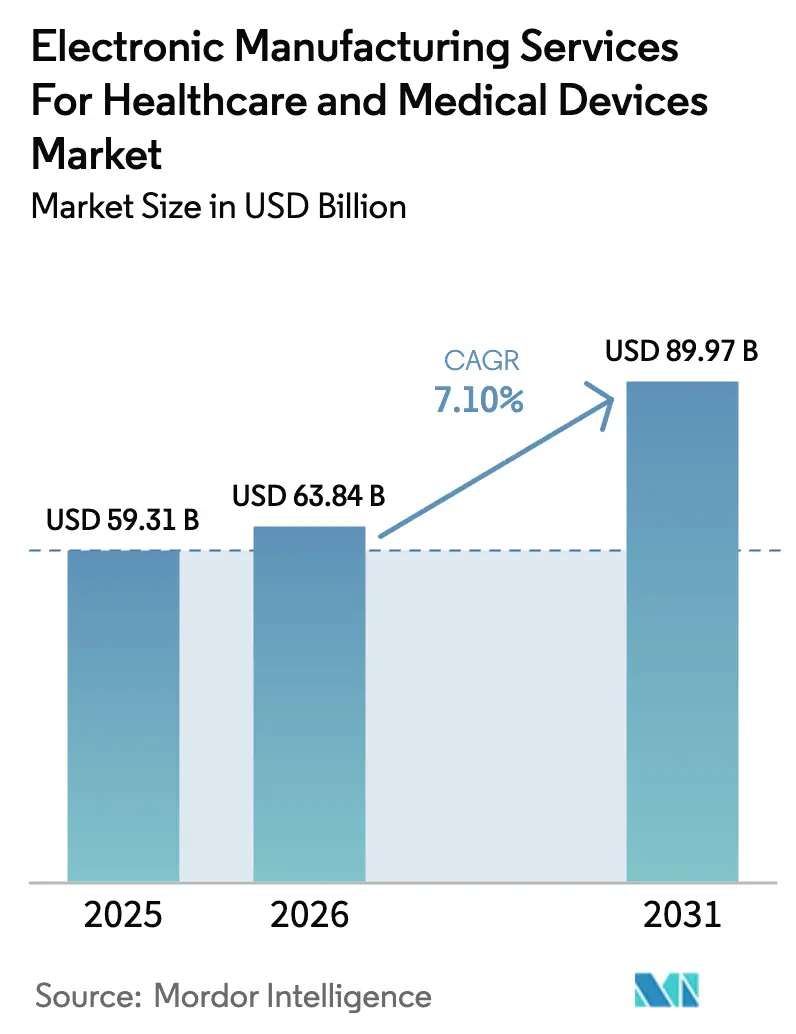

| Market Size (2026) | USD 63.84 Billion |

| Market Size (2031) | USD 89.97 Billion |

| Growth Rate (2026 - 2031) | 7.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

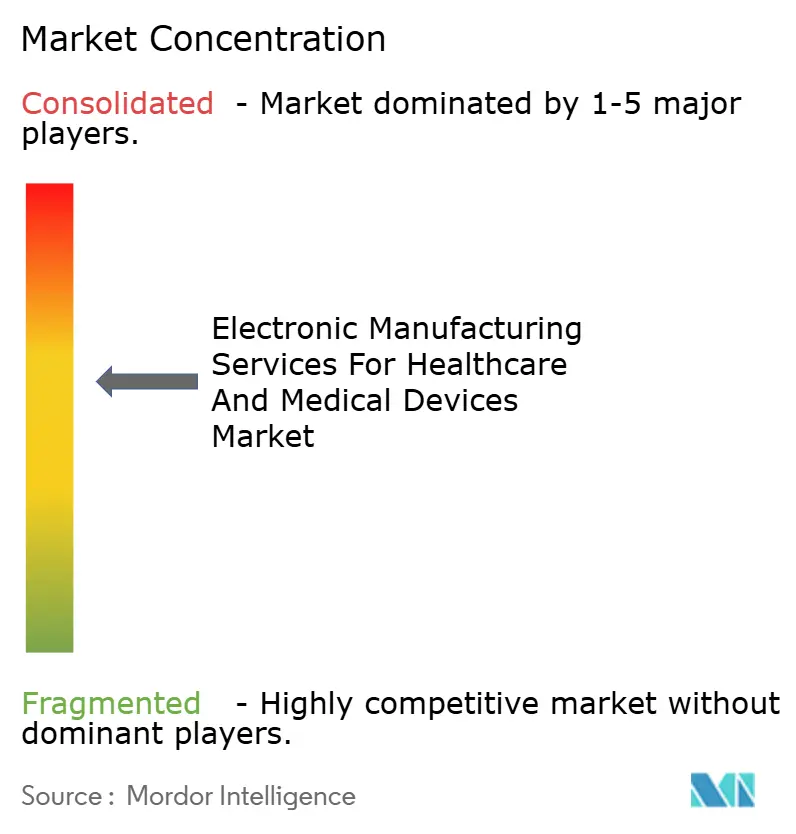

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electronic Manufacturing Services For Healthcare And Medical Devices Market Analysis by Mordor Intelligence

The electronic manufacturing services for healthcare and medical devices market held a market size of USD 63.84 billion in 2026 and is projected to reach USD 89.97 billion by 2031, registering a 7.10% CAGR. Original equipment manufacturers (OEMs) are reallocating assembly, prototyping, and regulatory-compliance workloads to specialized partners, spurring a steady rise in outsourcing penetration and underpinning revenue visibility for contract providers. Demand for connected-health platforms, implantables that rely on miniaturized electronics, and systems requiring ISO 13485-certified cleanroom production has intensified, pushing EMS providers to expand capacity, adopt AI-enabled surface-mount lines, and strengthen global component-sourcing networks. Nearshoring initiatives under the United States–Mexico–Canada Agreement (USMCA) and the European Union’s Health Emergency Preparedness and Response Authority (HERA) framework are reshaping geographic footprints, while ongoing semiconductor-supply volatility continues to elevate inventory days and operating-capital requirements.

Key Report Takeaways

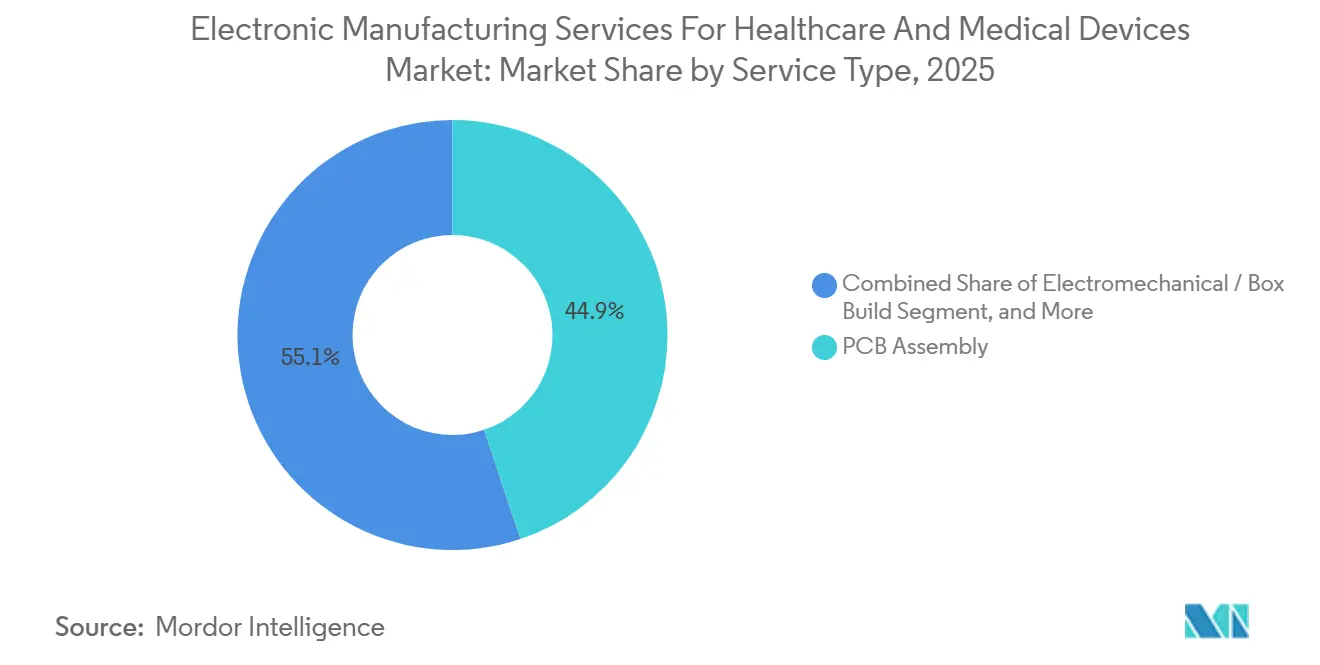

- By service type, PCB assembly led with 44.88% revenue share in 2025; electromechanical assembly and box build are advancing at a 7.63% CAGR through 2031.

- By business model, contract manufacturing controlled 61.71% of electronic manufacturing services for healthcare and medical devices market share in 2025, whereas hybrid and turnkey models are forecast to post a 7.41% CAGR from 2026 to 2031.

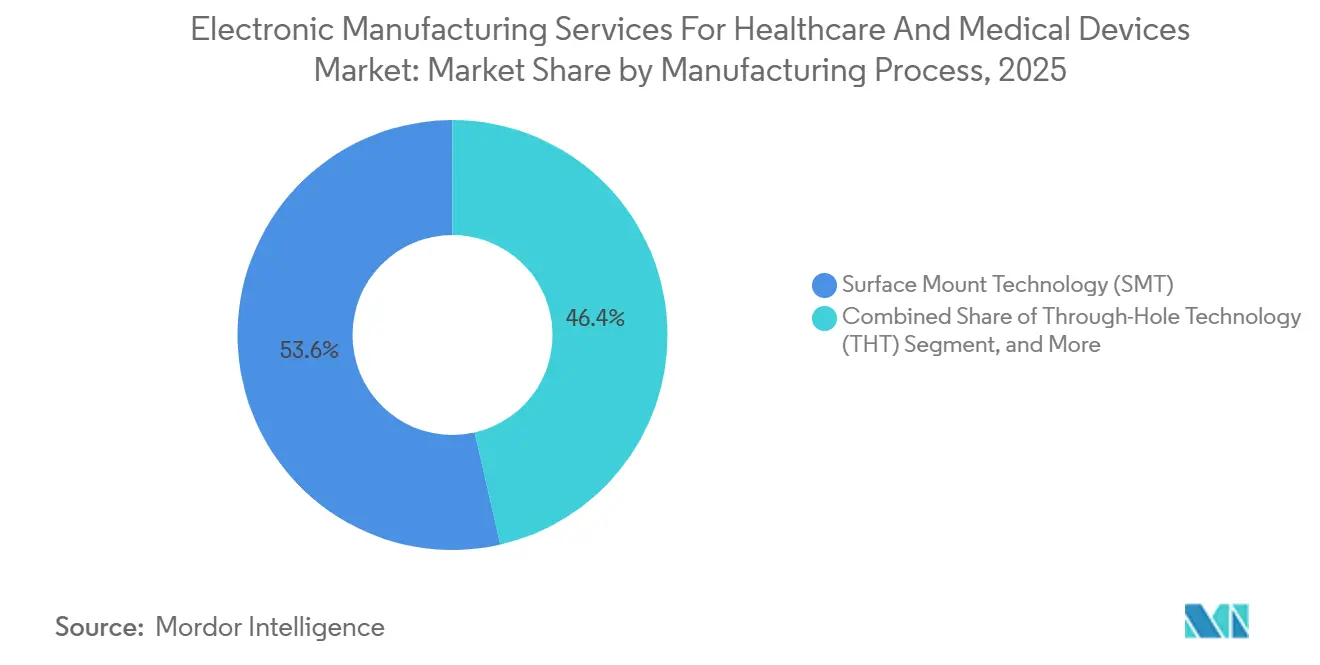

- By manufacturing process, surface-mount technology contributed 53.57% share of electronic manufacturing services for healthcare and medical devices market size in 2025; advanced packaging and hybrid processes are expanding at a 7.99% CAGR through 2031.

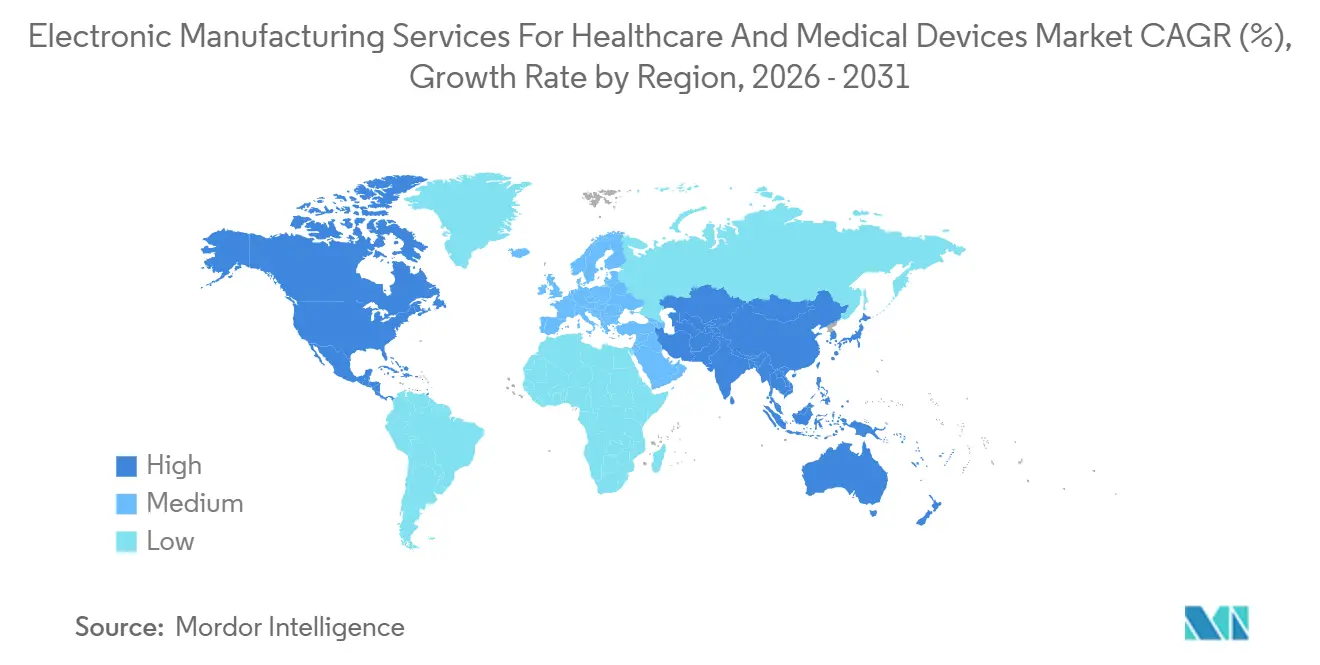

- By geography, Asia Pacific captured 62.94% revenue share in 2025 and is projected to grow at an 8.19% CAGR to 2031, pacing all other regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electronic Manufacturing Services For Healthcare And Medical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Outsourcing of Medical Device Manufacturing to EMS Providers | +1.8% | Global, with concentration in North America and Asia Pacific | Medium term (2-4 years) |

| Rising Complexity and Miniaturization of Medical Electronics | +1.5% | Global, led by North America and Europe for implantables; Asia Pacific for wearables | Long term (≥ 4 years) |

| Stringent Regulatory Requirements Driving Demand for ISO 13485-Certified Partners | +1.2% | Global, particularly North America and Europe under FDA QMSR and EU MDR | Short term (≤ 2 years) |

| Adoption of AI-Enabled SMT Lines to Reduce Defect Rates Below 50 ppm | +0.9% | North America, Europe, and leading Asia Pacific hubs (China, Japan, South Korea) | Medium term (2-4 years) |

| Nearshoring Incentives Linked to Health-Security Policies in USMCA and EU | +0.7% | North America (Mexico, United States) and Europe (Germany, Poland, Ireland) | Short term (≤ 2 years) |

| Growth of Smart Packaging Integration Creating Bundled EMS plus Pack Solutions | +0.6% | Global, with early adoption in Europe and North America for cold-chain biologics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Outsourcing of Medical Device Manufacturing to EMS Providers

OEM outsourcing penetration rose from 31% in 2020 to 38% in 2025 as companies diverted capital to clinical validation and digital-health software. Smaller firms without ISO 13485 infrastructure use contract manufacturing to satisfy FDA 21 CFR 820 compliance[1]Jabil. “Annual Report 2025.” jabil.com. Jabil reported 14% growth in healthcare-segment in 2025, with 60% of new contracts bundling design-for-manufacturing and supply-chain services. India’s production-linked incentive attracted USD 1.2 billion in EMS commitments between 2024 and 2025, bolstering South Asian capacity. India’s production-linked incentive scheme attracted USD 1.2 billion in EMS commitments between 2024 and 2025, diversifying global capacity toward South Asia. These shifts collectively raise the addressable base for the electronic manufacturing services for healthcare and medical devices market.

Rising Complexity and Miniaturization of Medical Electronics

Abbott’s FreeStyle Libre 3 sensor integrates radio and power management in a 21 mm package. Medtronic’s 2 g Micra AV2 pacemaker employs vertical die stacking. EMS providers deploy 01005-capable placers and X-ray inspection. Plexus noted that 40% of 2025 engagements included early-stage engineering to optimize thermal management. Medtronic’s 2 g Micra AV2 pacemaker employs vertical die stacking to eliminate wire bonds. EMS providers, therefore, invest in pick-and-place systems capable of 01005 handling and X-ray inspection for hidden joints. Plexus disclosed that 40% of 2025 contracts featured early-stage engineering to optimize thermal profiles and component footprint. The escalating technical bar is driving demand for turnkey engagements in electronic manufacturing services for the healthcare and medical devices market.

Stringent Regulatory Requirements Driving Demand for ISO 13485-Certified Partners

Effective February 2026, U.S. regulation aligns with ISO 13485:2016, tightening process-validation and risk-management expectations. The EU Medical Device Regulation similarly obliges contract assemblers to maintain technical files and surveillance records. EMS providers without certification face disqualification from bids, as evidenced by Benchmark Electronics’ customer audits reported in Q4 2025. Consequently, ISO-accredited capacity commands premium pricing and strengthens the value proposition of large providers within the electronic manufacturing services for healthcare and medical devices market.

Adoption of AI-Enabled SMT Lines to Reduce Defect Rates Below 50 ppm

Jabil implemented AI-driven optical inspection across 18 lines, cutting escape rates by 35%. Flex deployed generative-design tools, reducing first pass yield loss by 22%. Panasonic’s NPM-W2S placer provides ±25 µm accuracy for 0201 passives. Flex piloted generative-design software that reduced first-pass yield losses by 22%. Panasonic’s NPM-W2S placer handles 0201 passives at ±25 µm accuracy while logging real-time process data. These investments translate into shorter validation cycles and lower warranty exposure, further catalyzing spending in the electronic manufacturing services for the healthcare and medical devices market.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Semiconductor and Component Supply Chains | -1.1% | Global, with acute pressure in North America and Europe due to longer lead times | Short term (≤ 2 years) |

| High Capital Expenditure for Advanced Packaging and Hybrid Processes | -0.8% | Asia Pacific and North America, where EMS providers are expanding SiP and 3D-stacking capacity | Medium term (2-4 years) |

| Escalating Tariff Exposure on Medical Electronics Sub-Assemblies | -0.5% | United States and Europe, affecting imports from China and Southeast Asia | Short term (≤ 2 years) |

| Shortage of Flight-Approved PCBs Delaying Air-Ambulance Device Certification | -0.3% | North America and Europe, impacting portable defibrillators and ventilators | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in Semiconductor and Component Supply Chains

Analog front-ends and power-management ICs remained on allocation lists through 2025, driving 183 FDA-tracked medical-device shortages, 42% of which traced to component unavailability. Flex increased healthcare-segment inventory days from 45 in 2023 to 62 in 2025 to buffer supply risks. Smaller EMS firms lack the procurement leverage to secure allocations, pushing share toward larger providers and moderating growth in the electronic manufacturing services market for healthcare and medical devices.

High Capital Expenditure for Advanced Packaging and Hybrid Processes

A single SiP line can require USD 15 million–USD 50 million. Sanmina invested USD 35 million in Singapore during 2025, while Celestica spent USD 28 million upgrading Thai operations. Mid-tier providers struggle to justify such outlays, often subcontracting advanced steps, adding lead time, and eroding margins. The resulting barrier to entry slows supplier expansion and tempers the CAGR of the electronic manufacturing services market for healthcare and medical devices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Box Build Drives Turnkey Demand

PCB assembly commanded 44.88% of 2025 revenue within the electronic manufacturing services for healthcare and medical devices market share. Electromechanical assembly and box build remains the fastest-growing sub-segment, advancing at a 7.63% CAGR, because OEMs favor partners that integrate boards, enclosures, cabling, and final testing in cleanroom conditions. This turnkey preference compresses launch timelines for Bluetooth-enabled glucose monitors and connected infusion pumps, while also reducing coordination overhead. The electronic manufacturing services for healthcare and medical devices market size for prototype and DFM engagements rose as early-stage companies secured EMS help for regulatory submissions. Engineering and logistics services, although smaller, enable ISO-compliant cold-chain distribution and circular-economy recycling, steadily broadening total addressable revenue.

Growing regulatory complexity and supply-chain risk encourage OEMs to co-locate design, assembly, and testing under one certified roof. Providers that can pivot from surface-mount to system-in-package without external transfers capture incremental value and deepen switching costs. Consequently, electromechanical assembly revenue is likely to approach parity with PCB assembly before 2031, further diversifying the electronic manufacturing services for healthcare and medical devices market.

By Business Model: Hybrid Approaches Blend Control and Speed

Contract manufacturing dominated with 61.71% of 2025 revenue, reflecting OEM preference for IP control and build-to-print clarity. Hybrid and turnkey contracts, however, are expanding at a 7.41% CAGR as venture-backed firms and resource-constrained mid-tier OEMs seek component-sourcing expertise and DFM support. Under hybrid agreements, the OEM defines clinical requirements, while the EMS provider architects circuits, selects components, and validates processes, sharing liability but accelerating commercialization. This model allows EMS partners to recommend alternative parts that mitigate semiconductor shortages, thereby protecting schedules.

Turnkey contracts shift procurement risk to the EMS provider and convert fixed capital into a per-unit expense. Such predictability is attractive to investors evaluating device scale-up plans. Growth in turnkey engagements strengthens provider bargaining power, supporting margin stability across the electronic manufacturing services for healthcare and medical devices market size.

By Manufacturing Process: Advanced Packaging Unlocks Miniaturization

Surface-mount technology contributed 53.57% of 2025 revenue, continuing its reign in diagnostic analyzers and patient monitors. Advanced packaging and hybrid processes, though smaller, are growing fastest at 7.99% on the back of SiP adoption in wearable glucose monitors and subcutaneous drug-delivery systems. A SiP solution cuts board area by up to 60%, facilitating implantables such as Medtronic’s Micra. Hybrid lines that combine SMT, through-hole, and advanced packaging on one board address ventilators and anesthesia machines requiring robust power connectors and densely populated DSP sections.

Capital-intensive bonding and X-ray inspection tools restrict advanced-packaging capacity to large EMS providers. Their early entry grants pricing premiums and long-term contracts, locking in share and raising the technical floor for new entrants. Sustained equipment upgrades will keep advanced packaging the principal growth engine of the electronic manufacturing services for healthcare and medical devices market.

Geography Analysis

Asia Pacific commanded 62.94% revenue share in 2025 and is set for an 8.19% CAGR to 2031, supported by China’s 12% output growth and India’s USD 1.2 billion EMS pledges. Vietnam, Thailand, and Malaysia capture diversionary projects mitigating tariff risk. South Korea and Japan specialize in implantables, leveraging semiconductor-fabrication prowess.

North America benefits from USMCA rules-of-origin incentives. Mexico’s exports to the United States rose 18% in 2024, with Jabil, Flex, and Sanmina adding 2,500 jobs. Federal stockpile policies encourage localizing assembly of high-acuity devices. Canada supplies complementary design expertise.

Europe repatriates ventilator and dialysis-machine assembly under HERA grants[3]The Wall Street Journal. “Advanced Packaging in Medical Devices Drives Miniaturization.” wsj.com. Germany and Ireland expand ISO 13485 cleanrooms. Poland and Hungary appeal for cost-sensitive diagnostic work, while regulatory clarity supports capacity additions.South America and the Middle East and Africa remain nascent. Brazil and South Africa launch pilot lines for basic diagnostics. Limited local demand and regulatory complexity keep these regions a small contributor to electronic manufacturing services for healthcare and medical devices market size.

Competitive Landscape

The electronic manufacturing services for the healthcare and medical devices market show moderate concentration. Foxconn, Jabil, Flex, Sanmina, and Celestica accounted for a considerable share of global revenue in 2025, with the remainder split among regional specialists. Large providers emphasize horizontal integration, offering design-for-manufacturing, component procurement, assembly, testing, and logistics. Such breadth deepens customer lock-in and supports premium pricing. Jabil’s 2025 portfolio indicated that 60% of healthcare contracts included a full turnkey scope.

Technology adoption differentiates market leaders. Jabil patented an AI system that predicts solder-joint failure from reflow-profile deviations[4]European Commission. “HERA Framework.” ec.europa.eu. Flex deploys predictive-maintenance analytics that reduce unplanned downtime across Mexico plants. Foxconn leverages smartphone volume to secure favorable microcontroller allocations, shielding lead times for diagnostic devices. Regional specialists compete on depth rather than breadth. Fabrinet focuses on optical-precision assemblies for surgical lasers. Integer Holdings invests in hermetic sealing at Tijuana to serve implantable rhythm-management customers. Benchmark Electronics stresses regulatory documentation capability for surgical-robotics startups.

Capital intensity forces scale economies. System-in-package lines can run USD 15-50 million, restricting entry. Providers that fail to finance upgrades risk relegation to low-margin PCB work. The resulting two-tier structure shapes pricing power and drives consolidation within the electronic manufacturing services for healthcare and medical devices market.

Electronic Manufacturing Services For Healthcare And Medical Devices Industry Leaders

Foxconn Technology Group

Jabil Inc.

Flex Ltd.

Sanmina Corporation

Celestica Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: The U.S. Food and Drug Administration began full enforcement of the Quality Management System Regulation harmonized with ISO 13485:2016, obliging all Class II and III medical-device OEMs and their EMS partners to present conformity documentation during routine and for-cause inspections.

- April 2025: Jabil deployed AI-driven automated-optical-inspection across 18 surface-mount lines dedicated to medical devices, cutting escape rates by 35% and bringing defect levels below 50 ppm.

- January 2025: Jabil unveiled a USD 120 million expansion at Penang, Malaysia, adding 50,000 sq ft of ISO 13485 cleanrooms for implantable cardiac and neuromodulation devices; system-in-package lines start in Q3 2026.

- December 2024: Flex acquired a specialty medical-device manufacturer in Tijuana for USD 85 million, adding 200,000 sq ft and 800 staff focused on diagnostic-imaging box build.

Global Electronic Manufacturing Services For Healthcare And Medical Devices Market Report Scope

Electronic Manufacturing Services (EMS) for healthcare and medical devices involve specialized, outsourced services, including design, engineering, PCB assembly, testing, and supply chain management, tailored to produce compliant electronic components for medical OEMs.

The Electronic Manufacturing Services for Healthcare and Medical Devices Market Report is Segmented by Service Type (Electronic Manufacturing Services including PCB Assembly, Electromechanical Assembly/Box Build, Prototyping, and Other EMS; Engineering Services; Test and Development Implementation; Logistics Services; and Other Service Types), Business Model (Contract Manufacturing, Original Design Manufacturing, and Hybrid/Turnkey/Other), Manufacturing Process (Surface Mount Technology, Through-Hole Technology, and Advanced Packaging/Hybrid Processes), and Geography (North America including United States, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly / Box Build | |

| Prototyping | |

| Other Electronic Manufacturing Services | |

| Engineering Services | |

| Test and Development Implementation | |

| Logistics Services | |

| Other Service Types |

| Contract Manufacturing (CM) |

| Original Design Manufacturing (ODM) |

| Hybrid / Turnkey / Other Business Models |

| Surface Mount Technology (SMT) |

| Through-Hole Technology (THT) |

| Advanced Packaging / Hybrid Processes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Service type | Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly / Box Build | ||

| Prototyping | ||

| Other Electronic Manufacturing Services | ||

| Engineering Services | ||

| Test and Development Implementation | ||

| Logistics Services | ||

| Other Service Types | ||

| By Business Model | Contract Manufacturing (CM) | |

| Original Design Manufacturing (ODM) | ||

| Hybrid / Turnkey / Other Business Models | ||

| By Manufacturing Process | Surface Mount Technology (SMT) | |

| Through-Hole Technology (THT) | ||

| Advanced Packaging / Hybrid Processes | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

How large is the electronic manufacturing services for healthcare and medical devices market in 2026?

The market reached a size of USD 63.84 billion in 2026.

What is the forecast CAGR between 2026 and 2031?

A 7.10% CAGR is expected through 2031.

Which region leads market revenue?

Asia Pacific held 62.94% of revenue in 2025 and will grow fastest to 2031.

Which service type is expanding the quickest?

Electromechanical assembly and box build is advancing at a 7.63% CAGR.

Page last updated on: