Electronic Manufacturing Services For Communication Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

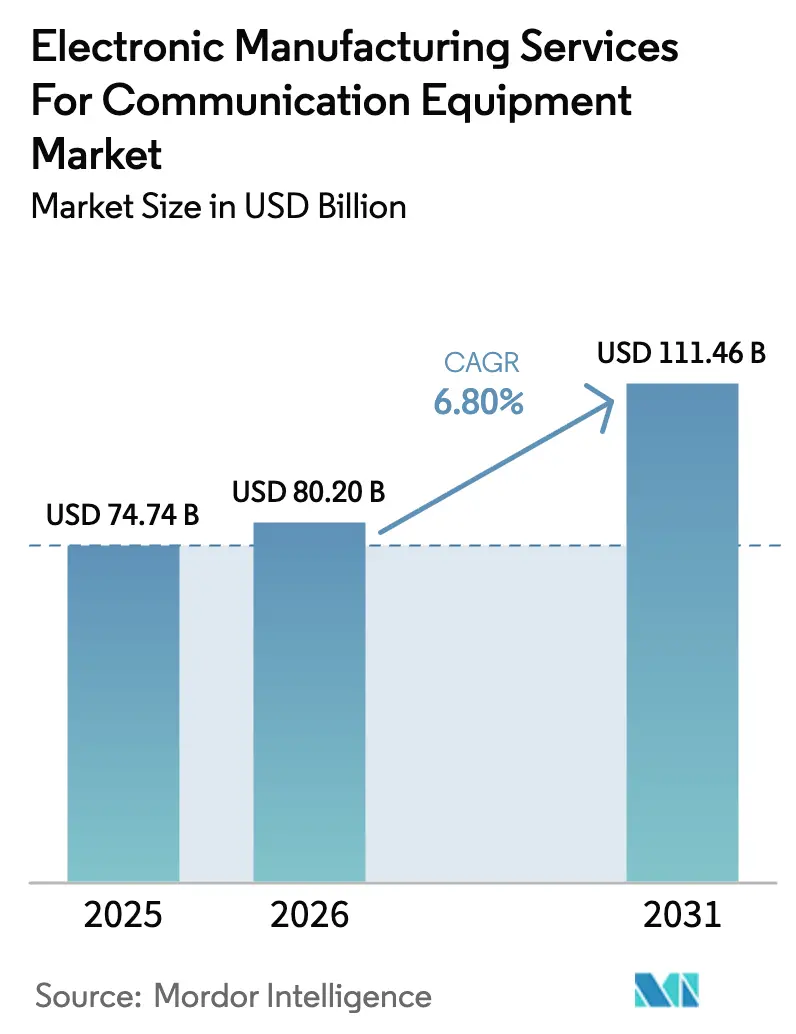

| Market Size (2026) | USD 80.20 Billion |

| Market Size (2031) | USD 111.46 Billion |

| Growth Rate (2026 - 2031) | 6.80% CAGR |

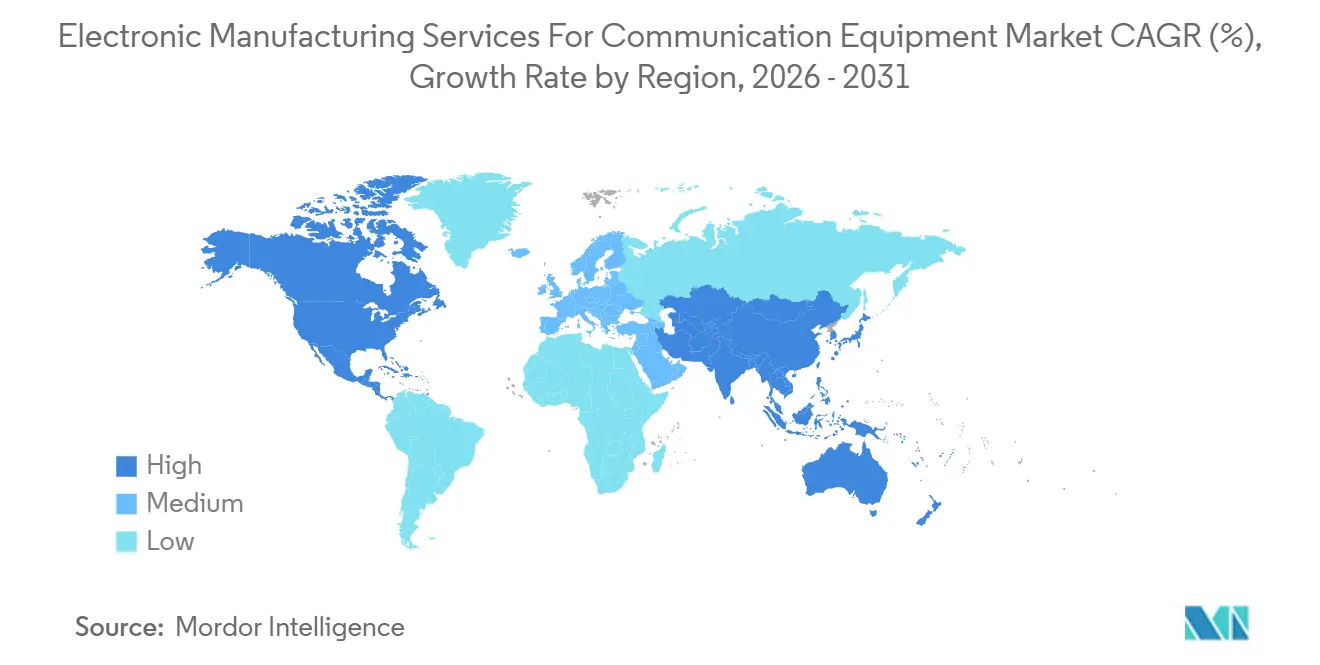

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

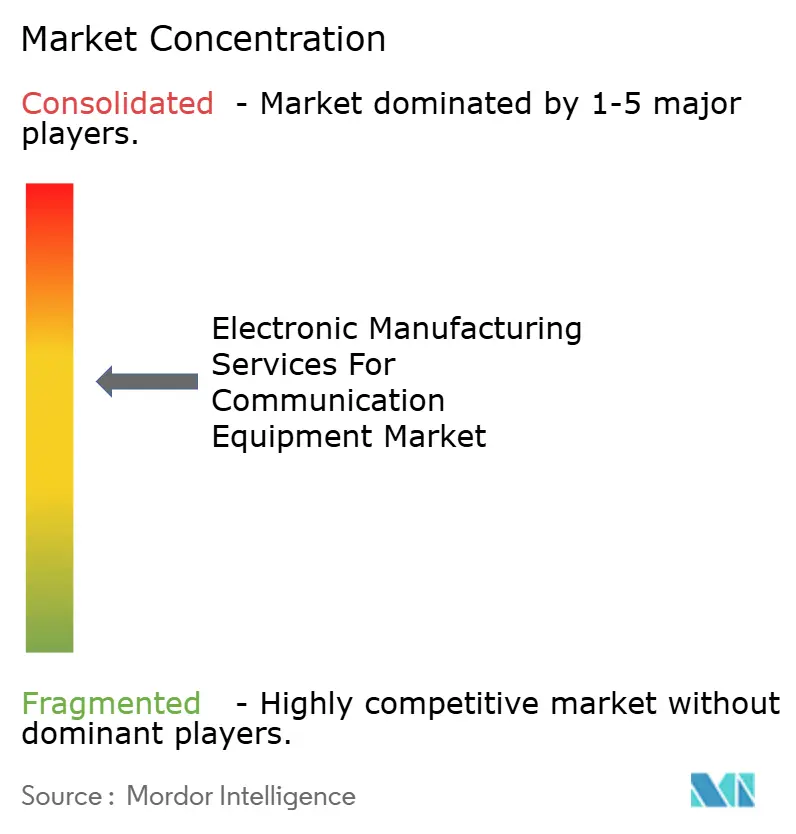

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electronic Manufacturing Services For Communication Equipment Market Analysis by Mordor Intelligence

The electronic manufacturing services for communication equipment market reached USD 80.2 billion in 2026 and is projected to attain USD 111.46 billion by 2031, advancing at a 6.8% CAGR over 2026-2031. The market’s current size underscores three structural forces that will shape the next five years, telecom OEMs are converting fixed plants into variable-cost supply chains, governments are offering production-linked incentives to anchor high-value assembly at home, and 5G radio frequency (RF) printed circuit boards now demand specialized surface-mount technology (SMT) lines that only a limited number of contract manufacturers can operate at scale[1]Source: Telefonaktiebolaget LM Ericsson, “Annual Report 2024,” Ericsson, ericsson.com. Accelerated 5G deployments, rising demand for fiber-optic backhaul in emerging markets, module miniaturization that favors system-in-package (SiP) architectures, and supply-chain nearshoring are expanding the electronic manufacturing services for communication equipment market opportunity across all regions. Competitive intensity remains high, yet regulatory compliance costs and stringent vendor qualification processes create switching barriers that stabilize long-term relationships with scale players.

Key Report Takeaways

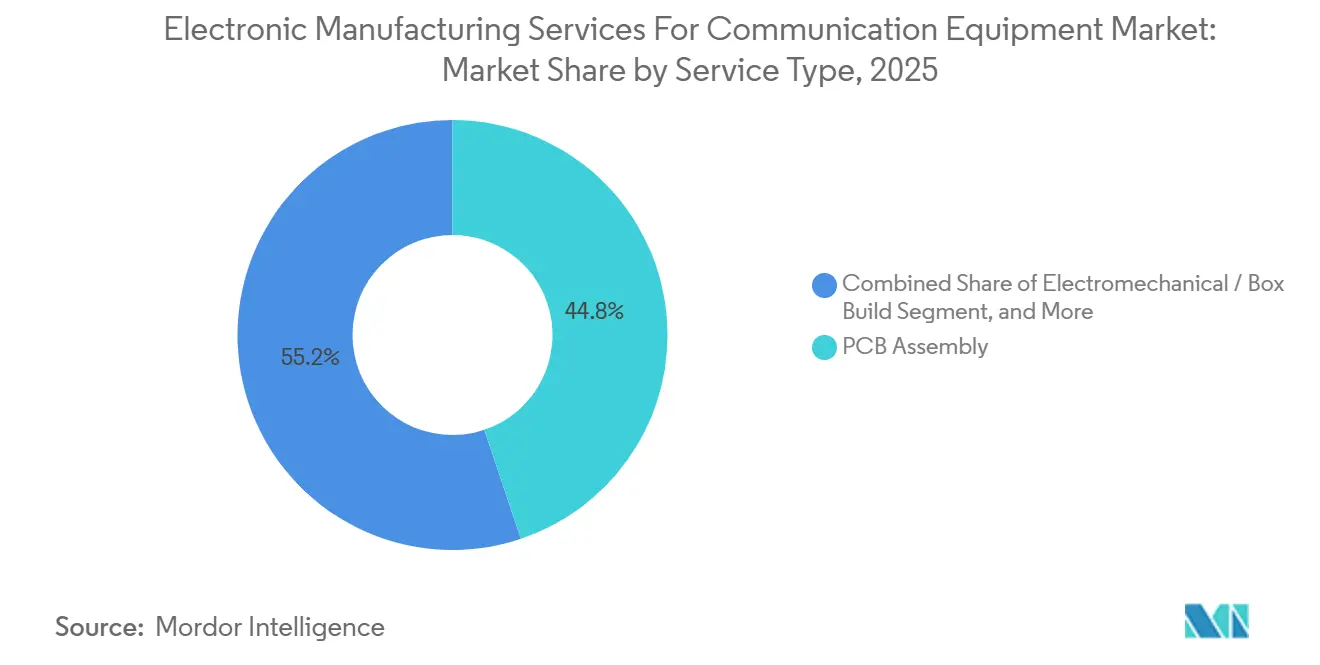

- By service type, printed circuit board (PCB) assembly held 44.84% of revenue in 2025, while electromechanical assembly and box build are projected to grow at a 6.94% CAGR through 2031.

- By business model, contract manufacturing accounted for 60.91% of 2025 revenue, whereas hybrid and turnkey agreements are forecast to grow at 7.06% through 2031.

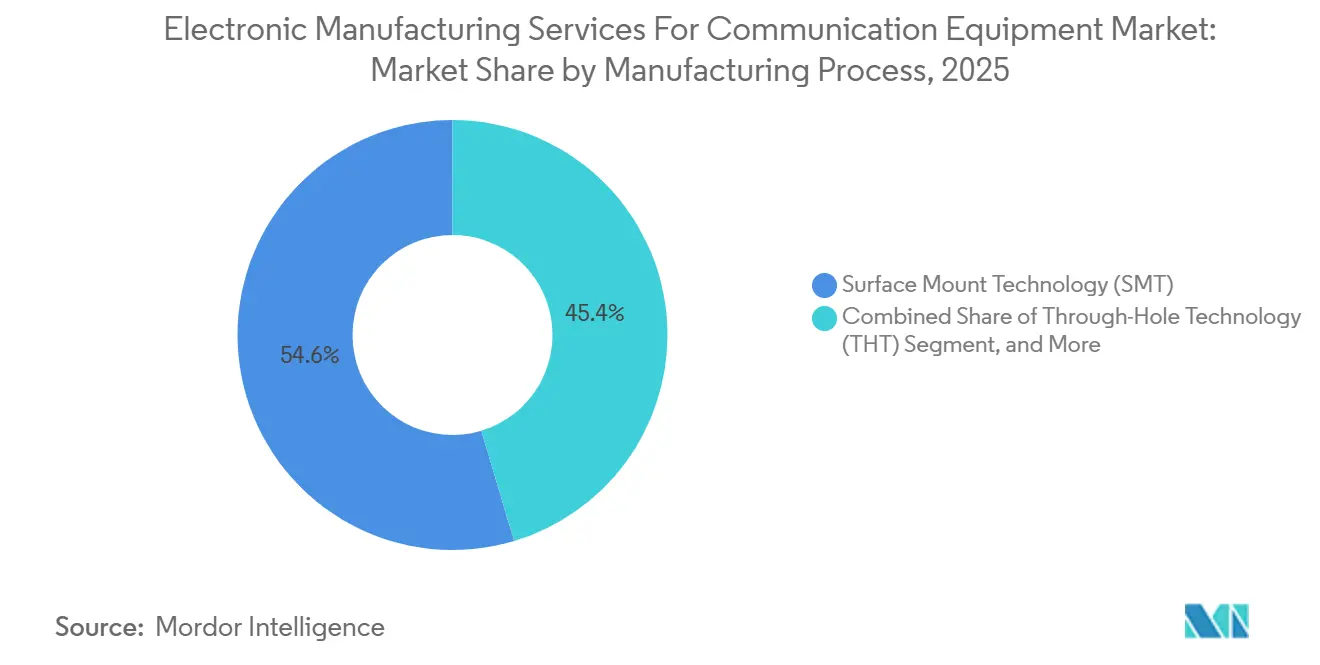

- By manufacturing process, surface-mount technology accounted for 54.63% of 2025 production volume, but advanced packaging and hybrid processes will expand at 7.27% through 2031.

- By geography, Asia Pacific commanded 63.77% of 2025 revenue yet will grow at 7.81%, outpacing North America and Europe as China, India, and Southeast Asia add both domestic 5G capacity and export-oriented lines.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electronic Manufacturing Services For Communication Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated 5G Roll-out Requiring Complex RF PCB Assemblies | +1.5% | Global, with early concentration in China, South Korea, North America | Medium term (2-4 years) |

| Telecom OEM Shift Toward Asset-Light Manufacturing Models | +1.2% | Global, particularly acute among mid-tier equipment vendors in Europe and North America | Short term (≤2 years) |

| Rising Demand for Fiber-Optic Backhaul Equipment in Emerging Markets | +0.9% | Asia Pacific core (India, Indonesia, Philippines), spillover to Middle East and Africa | Long term (≥4 years) |

| Miniaturization of Communication Modules Driving Advanced Packaging Adoption | +1.1% | Global, led by Asia Pacific advanced packaging hubs in Taiwan, Singapore, Malaysia | Medium term (2-4 years) |

| Government Incentives for Domestic Telecom Manufacturing | +1.0% | National, with early gains in India, Mexico, Vietnam, and Central Europe | Medium term (2-4 years) |

| Supply-Chain Near-shoring to Mitigate Geopolitical Risks | +0.8% | North America (Mexico), Europe (Poland, Czech Republic), Asia Pacific (India, Vietnam) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Accelerated 5G Roll-out Requiring Complex RF PCB Assemblies

The 4G-to-5G transition doubles or triples PCB layer counts, introduces low-loss laminates such as Rogers RO4000 and Taconic TLY-5, and demands drilling and plating tolerances that fewer than 20 contract manufacturers can achieve at telecom-grade yields[2]Source: Rogers Corporation, “RO4000 Series High Frequency Circuit Materials,” Rogerscorp.com. Each massive-MIMO antenna integrates up to 256 transceiver chains on multilayer RF PCBs, and corresponding SiP modules must meet insertion-loss targets below 0.5 dB while dissipating more than 50 W cm-2. Capital requirements for automated X-ray inspection, environmental stress screening, and traceability exceed USD 10 million per SMT line. Nokia’s qualification regime, anchored in IPC-A-610 Class 3 and ETSI EN 301 489-1, further narrows the supplier pool[3]Source: European Telecommunications Standards Institute, “ETSI EN 301 489-1 V2.2.3,” Etsi.org. The resulting demand surge lifts both revenue and margins for providers that own advanced RF assembly assets, thereby expanding the electronic manufacturing services for communication equipment market.

Telecom OEM Shift Toward Asset-Light Manufacturing Models

Hardware margins of 15-25% compare unfavorably with the 60% gross margin achievable in RAN software and network analytics. Consequently, vendors are divesting assembly plants and outsourcing entire product lines. Ericsson eliminated 8,500 manufacturing jobs in 2024 and handed RAN Compute production to Flex and Jabil, cutting fixed costs by roughly USD 400 million while trimming lead times by six weeks. Mid-tier firms such as Mavenir and Parallel Wireless now rely on turnkey partners that assume inventory risk and guarantee intellectual property safeguards stronger than standard original design manufacturing clauses. This pivot from ownership to partnership enlarges the electronic manufacturing services for communication equipment market, aligns cost structures with carrier CAPEX volatility, and accelerates the adoption of hybrid engagement models.

Rising Demand for Fiber-Optic Backhaul Equipment in Emerging Markets

National broadband initiatives in India, Indonesia, and Nigeria are triggering large procurements of optical line terminals and dense wavelength-division multiplexing (DWDM) transponders that require micron-level alignment and automated testing unavailable in many local factories. India alone has earmarked the installation of 500,000 5G base stations between 2024 and 2027 and extended its incentive program to telecom hardware, offering 4-6% rebates on incremental sales manufactured domestically. Contract manufacturers with optical alignment expertise are winning multi-year agreements, thereby widening geographic participation and boosting the electronic manufacturing services for communication equipment market.

Miniaturization Driving Advanced Packaging Adoption

Small-cell radios and customer premises equipment now demand footprints under 1 L, pushing OEMs to replace discrete layouts with SiP designs. Flip-chip interconnect cuts parasitic inductance by up to 60%, wafer-level packaging slices per-unit cost once volumes exceed one million, and heterogeneous integration combines CMOS, gallium nitride, and silicon photonics die in a common module. Jabil’s 2025 opening of a Pune advanced-packaging site illustrates the capital flow toward this frontier. As demand for high-performance, space-constrained modules rises, advanced packaging capacity becomes a distinctive competitive lever inside the electronic manufacturing services for communication equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Margin Pressure from Volatile Component Prices | -0.5% | Global, with acute impact in regions lacking long-term supply agreements | Short term (≤2 years) |

| Talent Shortages in Advanced SMT Operations | -0.3% | North America, Europe, and emerging manufacturing hubs in India and Vietnam | Medium term (2-4 years) |

| IP Security Concerns Limiting ODM Adoption | -0.2% | Global, particularly affecting Western telecom vendors evaluating Asian ODM partners | Medium term (2-4 years) |

| Volatile Demand Cycles Linked to Carrier CAPEX | -0.4% | Global, with cyclical intensity varying by regional 5G deployment phases | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Margin Pressure from Volatile Component Prices

Gross margins in telecom assembly hover between 6-12%, leaving thin cushions against semiconductor and laminate price spikes. During the 2021-2023 shortage, spot prices for many power-management ICs soared 200-400%, clipping operating margins by up to 300 basis points before cost-pass-through clauses took effect. Smaller providers lacking volume leverage often pay 15-25% higher average procurement costs than tier-one peers. Rogers and Taconic have instituted annual laminate price increases of 3-8%, further eroding profitability for manufacturers locked into fixed-price deals.

Volatile Demand Cycles Linked to Carrier CAPEX

Carrier spending can swing 20-40% year-over-year as operators navigate spectrum auctions and macroeconomic shifts. The 2023 lull reduced global base-station shipments by 18%, idling SMT lines and furloughing labor at multiple sites. Although surge-capacity staffing alleviates shortages during peaks, it imposes 8-12% cost penalties during troughs. Only the largest OEMs can afford minimum-volume reservation agreements, which leaves smaller vendors vulnerable to squeezing during both peaks and slumps. The resulting unpredictability dampens the electronic manufacturing services for communication equipment market CAGR by roughly 0.4 percentage points.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: PCB Assembly Dominates While Box Build Accelerates

The PCB assembly segment accounted for 44.84% of 2025 revenue within the electronic manufacturing services for communication equipment market share, confirming its role as the foundational value node. Electromechanical assembly and box build are set to grow 6.94% per year through 2031, reflecting OEM decisions to outsource final system integration, enclosure fabrication, cable harnessing, and functional testing. Transferring these labor- and capital-intensive steps allows vendors to unlock working-capital tied to inventory and reinvest in software.

Engineering services, though a smaller slice, earn 25-40% higher margins and often serve as the entry point for deeper engagements. Test implementation services are rising in parallel, propelled by over-the-air validation demands in 5G radios. Logistics services complete the bundle, granting contract manufacturers supply-chain visibility that cements strategic control. Collectively, these dynamics reinforce the scale advantage of providers that can deliver end-to-end solutions, thereby lifting the electronic manufacturing services for communication equipment market.

By Business Model: Contract Manufacturing Leads as Hybrid Deals Gain Ground

Contract manufacturing captured 60.91% of 2025 revenue and remains the core engagement style. OEMs such as Ericsson, Nokia, and Huawei prefer to keep design authority in-house while leveraging assembly partners for labor efficiency. Intellectual property concerns and certification requirements restrict broad adoption of original design manufacturing in telecom hardware. Hybrid and turnkey models are therefore becoming the preferred alternative for mid-tier software-centric vendors, advancing at 7.06% through 2031.

Those arrangements give suppliers latitude to optimize mechanical layouts and procurement while leaving critical RF algorithms and network software with the OEM. Inventory consignment, often embedded in turnkey agreements, lowers the customer’s working-capital burden by 30-50% and opens the door for revenue-share pricing schemes. This shift widens participation among smaller OEMs and keeps contract manufacturers central to the electronic manufacturing services for communication equipment market.

By Manufacturing Process: Advanced Packaging Emerges as the Growth Frontier

Surface-mount technology handled 54.63% of 2025 production volume, underscoring its role as the assembly workhorse for communication equipment. However, advanced packaging and hybrid processes hold the fastest outlook, expanding 7.27% annually as SiP modules, flip-chip die-attach, wafer-level redistribution, and heterogeneous integration become mandatory in millimeter-wave 5G radios and 400-Gb optical engines.

Through-hole technology persists for military-grade and outdoor equipment, but its share continues to slide. Only a handful of EMS providers currently run volume flip-chip or die-to-wafer bonding at telecom-grade yields, creating a capability gap that commands 15-30% pricing premiums. Winning this frontier is likely to determine long-run positioning within the electronic manufacturing services for communication equipment market size for many suppliers.

Geography Analysis

Asia Pacific owned 63.77% of 2025 revenue and is forecast to grow 7.81% through 2031, underpinning the largest slice of the electronic manufacturing services for communication equipment market. China remains the dominant hub, yet incremental capacity now flows toward India, Vietnam, and Malaysia as geopolitical concerns and incentive programs diversify supply chains. India’s output jumped from USD 3.2 billion in 2020 to USD 9.8 billion in 2024 under its Production Linked Incentive scheme. Vietnam approved USD 3.2 billion of new electronics projects in 2024, highlighting its ascent as a secondary pole for export-oriented telecom assembly. Japan and South Korea remain leaders in advanced packaging and test, although high labor costs limit volume share.

North America, driven principally by Mexico, is experiencing renewed investment. Flex alone operates 11 Mexican campuses totaling more than two million units of annual telecom equipment capacity. The United States focuses on secure defense and satellite communication systems, while Canada’s niche lies in optical networking gear leveraging its photonics research base.

Europe occupies a mid-tier role. Germany excels in high-reliability assemblies for automotive and defense, whereas Poland and Czech Republic are capturing price-sensitive volume from Western OEMs. European Union funding through the Chips Act is catalyzing semiconductor back-end and advanced packaging lines that will support regional telecom hardware. The United Kingdom retains niche military communication capacity but has lost broader share since Brexit. South America, Middle East, and Africa together remain below 10% share. Nonetheless, national broadband programs in Nigeria and Saudi Arabia are spurring localized assembly of optical gear, creating early footholds for regional EMS providers. These pockets of activity broaden the geographic footprint of the electronic manufacturing services for communication equipment market and hedge OEMs against single-region concentration risks.

Competitive Landscape

The top five contract manufacturers, Hon Hai Precision Industry, Flex, Jabil, Pegatron, and Wistron, command roughly 40% of global revenue, signaling a moderate level of concentration. Multi-sourcing policies force OEMs to split volume across three to five approved suppliers per product line, sustaining price pressure but also reducing supply-chain risk.

Scale players invest in vertical extensions such as logistics and after-sales repair to lift margin, while specialists build moats around RF assembly, optical alignment, or advanced packaging that can earn 15-30% premiums.

Digital twin simulations, AI-based optical inspection, and automated material handling are spreading rapidly; early adopters report defect-escape reductions of up to 60%. Government incentives are nurturing new challengers, Dixon Technologies and Optiemus Electronics in India and several Mexico-based firms now compete for North American contracts. The electronic manufacturing services for communication equipment market hence reflects both scale economies and capability niches, with ample room for entrants that master emerging process requirements.

Electronic Manufacturing Services For Communication Equipment Industry Leaders

Hon Hai Precision Industry (Foxconn)

Flex Ltd.

Jabil Inc.

Pegatron Corporation

Wistron Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Flex confirmed a USD 280 million expansion of its Guadalajara facility, adding 150,000 m² for 5G radio-unit and optical-transport lines to serve North American carriers.

- September 2025: Jabil opened an advanced packaging plant in Pune, India with an initial USD 120 million investment to provide flip-chip and SiP services for RF modules under India’s incentive program.

- August 2025: Sanmina secured a five-year contract to manufacture optical line terminals and DWDM transponders in the Czech Republic, projecting USD 85 million in annual revenue.

- July 2025: Fabrinet completed a USD 95 million capacity expansion in Thailand, bringing automated optical alignment and environmental screening for 400-Gb and 800-Gb transceivers.

Global Electronic Manufacturing Services For Communication Equipment Market Report Scope

The Electronic Manufacturing Services for Communication Equipment Market encompasses the provision of design, assembly, production, and testing services for communication equipment by third-party manufacturers.

The Electronic Manufacturing Services for Communication Equipment Market Report is Segmented by Service Type (Electronic Manufacturing Services including PCB Assembly, Electromechanical Assembly and Box Build, Prototyping, Other EMS including Cable Assembly and Testing; Engineering Services; Test and Development Implementation; Logistics Services; and Other Service Types), Business Model (Contract Manufacturing, Original Design Manufacturing, and Hybrid and Turnkey Models), Manufacturing Process (Surface Mount Technology, Through-Hole Technology, Advanced Packaging and Hybrid Processes), and Geography (North America including United States, Europe, Asia Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value in USD.

| Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | |

| Prototyping | |

| Other Electronic Manufacturing Services | |

| Engineering Services | |

| Test and Development Implementation | |

| Logistics Services | |

| Other Service Types |

| Contract Manufacturing (CM) |

| Original Design Manufacturing (ODM) |

| Hybrid / Turnkey / Other Business Models |

| Surface Mount Technology (SMT) |

| Through-Hole Technology (THT) |

| Advanced Packaging / Hybrid Processes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| South-East Asia | |

| Rest of Asia Pacific | |

| South America | |

| Middle East | |

| Africa |

| By Service Type | Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | ||

| Prototyping | ||

| Other Electronic Manufacturing Services | ||

| Engineering Services | ||

| Test and Development Implementation | ||

| Logistics Services | ||

| Other Service Types | ||

| By Business Model | Contract Manufacturing (CM) | |

| Original Design Manufacturing (ODM) | ||

| Hybrid / Turnkey / Other Business Models | ||

| By Manufacturing Process | Surface Mount Technology (SMT) | |

| Through-Hole Technology (THT) | ||

| Advanced Packaging / Hybrid Processes | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| South-East Asia | ||

| Rest of Asia Pacific | ||

| South America | ||

| Middle East | ||

| Africa | ||

Key Questions Answered in the Report

How large is the electronic manufacturing services for communication equipment market today?

The market was valued at USD 80.2 billion in 2026 and is projected to reach USD 111.46 billion by 2031.

What is the expected CAGR for electronic manufacturing services that target communication equipment?

The market is forecast to post a 6.8% CAGR over 2026-2031.

Which service type contributes the most revenue?

PCB assembly contributed 44.84% of 2025 revenue, reflecting its universal role across telecom hardware categories.

Why are hybrid and turnkey business models gaining popularity?

Mid-tier OEMs favor hybrid deals because they protect critical intellectual property while shifting inventory and procurement risk to the contract manufacturer, supporting a 7.06% CAGR through 2031.

Page last updated on: