Electrical Steel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 30.37 Billion |

| Market Size (2031) | USD 40.16 Billion |

| Growth Rate (2026 - 2031) | 5.75% CAGR |

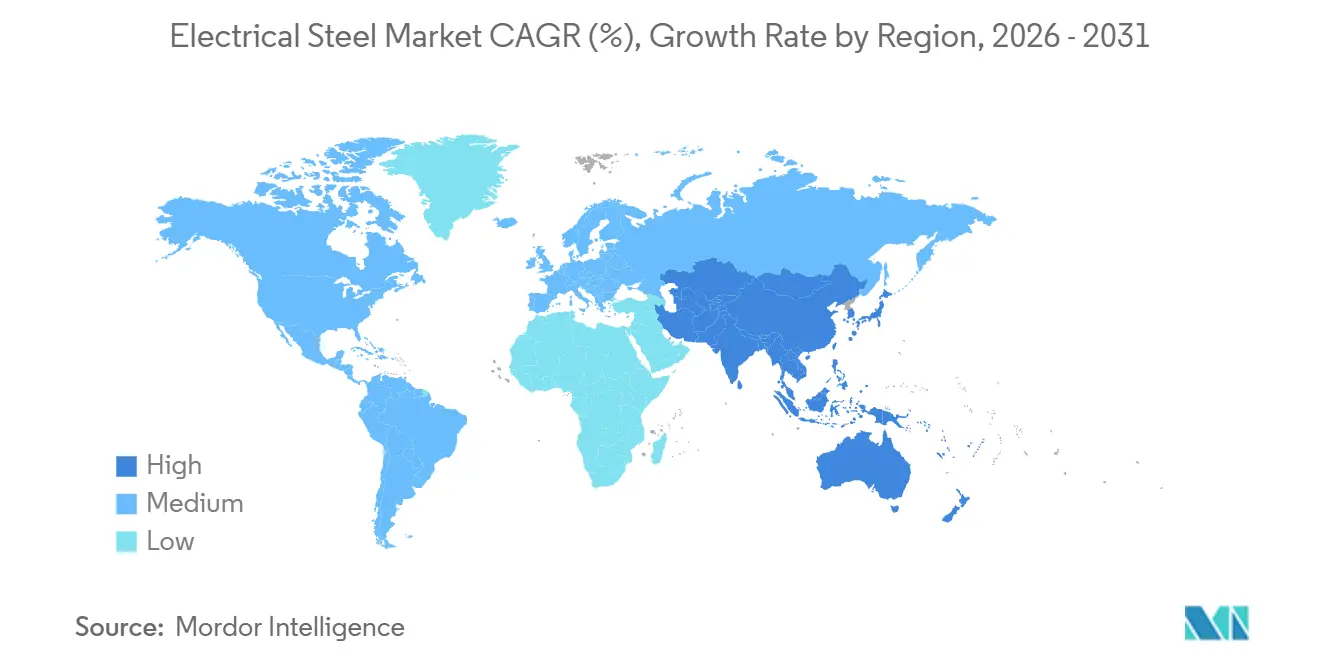

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electrical Steel Market Analysis by Mordor Intelligence

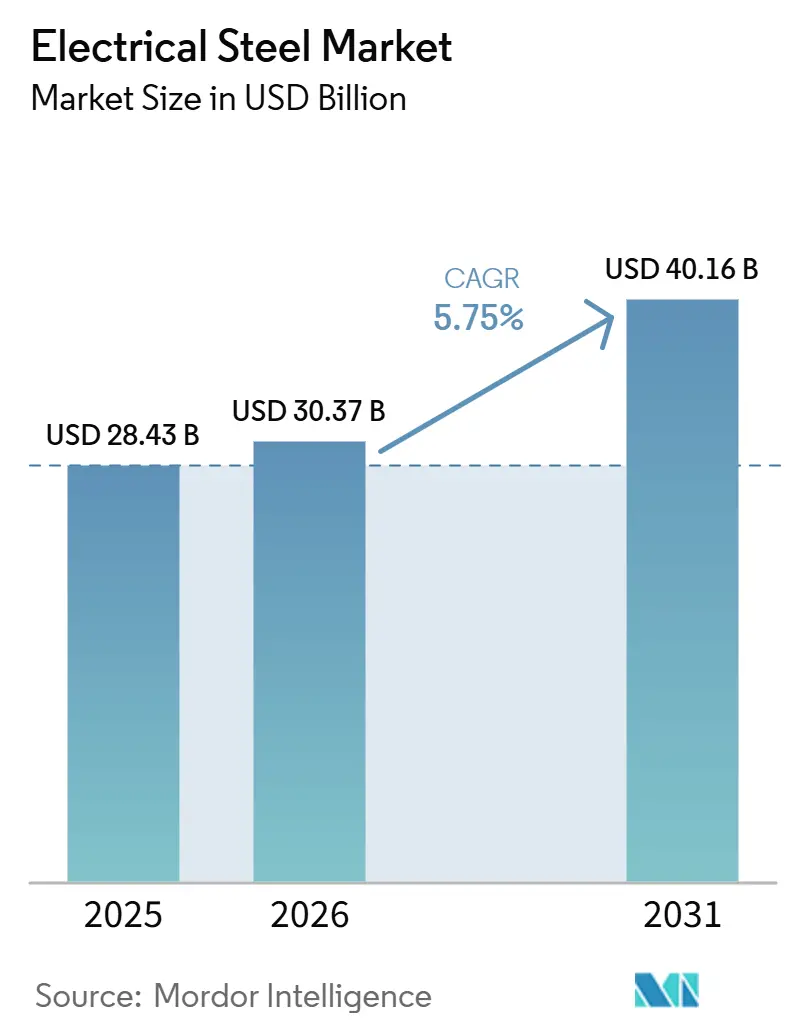

The Electrical Steel Market size is expected to grow from USD 28.43 billion in 2025 to USD 30.37 billion in 2026 and is forecast to reach USD 40.16 billion by 2031 at 5.75% CAGR over 2026-2031. The electrical steel market is supported by two demand cycles: grid reinforcement and vehicle and industrial electrification. Regulatory requirements are increasing demand for higher-grade materials, as motor-efficiency rules in the United States and Europe shift buyers toward lower-loss laminations instead of standard grades. A widening regional supply gap is shaping the electrical steel market, with Asian capacity expanding while parts of Europe face supply constraints and shutdowns due to import pressure. This gap is significant because electrical steel is used in transformers, motors, and power equipment, which are critical to energy security and industrial policy. New investments, such as ArcelorMittal’s Mardyck startup, indicate opportunities for targeted capacity additions where product positioning aligns with automotive and industrial electrification demand.

Key Report Takeaways

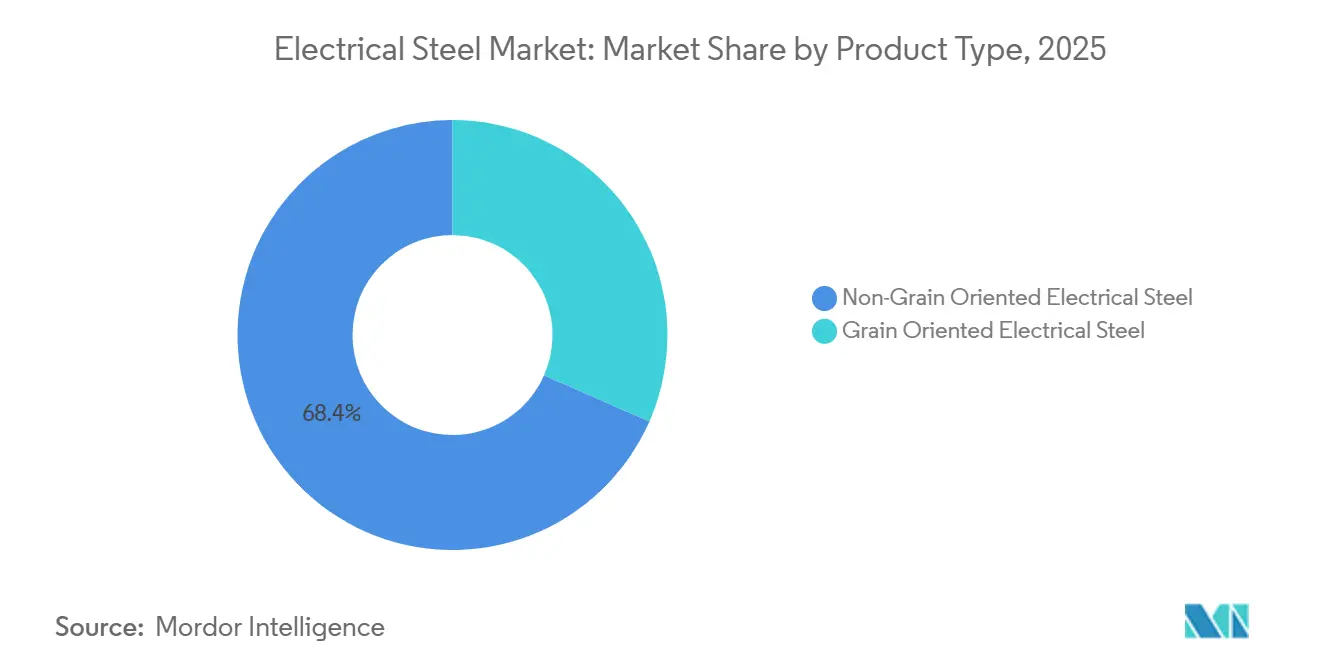

- By product type, non-grain-oriented electrical steel led with 68.42% share in 2025, while grain-oriented electrical steel is forecast to expand at a 6.24% CAGR through 2031.

- By application, motors accounted for 43.15% of revenue in 2025, while transformers are forecast to expand at a CAGR of 6.41% through 2031.

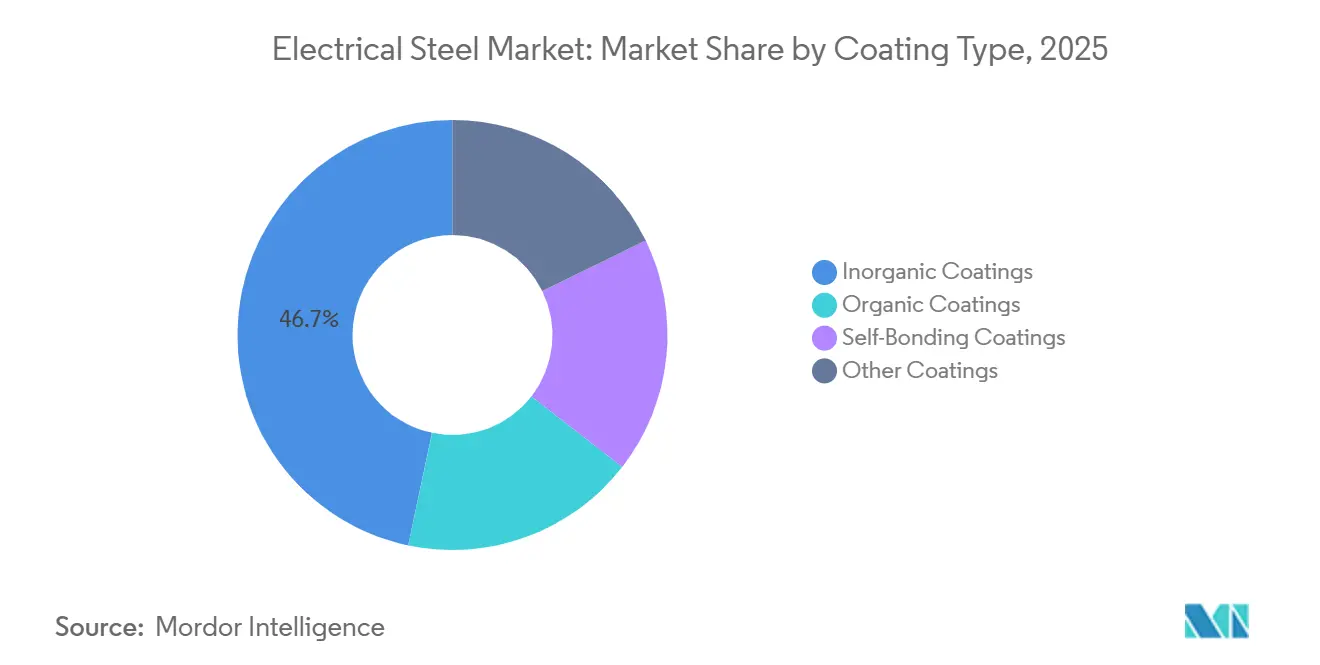

- By coating type, inorganic coatings held 46.71% of revenue in 2025, while self-bonding coatings are forecast to expand at a 6.84% CAGR through 2031.

- By geography, Asia-Pacific represented 54.82% of global revenue in 2025 and is projected to grow at the fastest CAGR of 6.37% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electrical Steel Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Electrification of Transportation and Industrial Systems | +1.5% | Global, concentrated in China, Europe, and North America | Short term (≤ 2 years) |

| Grid Modernization and Power Infrastructure Expansion | +1.8% | Global, strongest in India, the Middle East, and North America | Medium term (2-4 years) |

| Rising Demand for High-Efficiency Motors Driven by Regulatory Mandates | +1.0% | EU, North America, China, and Southeast Asia | Medium term (2-4 years) |

| Renewable Power Integration and Distributed Generation Growth | +0.8% | Global, concentrated in APAC, EU, and South America | Medium term (2-4 years) |

| Stringent Energy Efficiency Mandates for Transformers and Electrical Equipment | +0.5% | EU, China, and India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Electrification of Transportation and Industrial Systems

The electrical steel market is experiencing a demand shift, as EV traction motors require thinner silicon steel and tighter loss control than legacy motor platforms used at scale only a few years ago. Producer activity reflects this shift, with POSCO expected to report strong growth in non-oriented electrical steel exports in 2025, supported by supply agreements with global vehicle manufacturers. This trend extends beyond vehicles, as industrial motor upgrades are moving from optional spending to scheduled compliance activity under tighter efficiency regulations. As buyers shift to thinner gauges and lower iron-loss specifications, the electrical steel market is becoming less dependent on standard commodity grades and more dependent on process capability, coating performance, and metallurgical consistency. POSCO’s planned June 2026 consortium with Hyundai Motor and partner institutions indicates that the electrical steel market is approaching current manufacturing limits in developing high-silicon wide-sheet products for next-generation EV drives[1]POSCO Group Newsroom, “POSCO Partners with Hyundai Motor and 8 Organizations to Develop Next-Generation High-Efficiency Electrical Steel for EVs,” POSCO Group Newsroom, newsroom.posco.com. Leading producers are pursuing higher volumes while working to secure product classes that remain difficult for followers to scale.

Grid Modernization and Power Infrastructure Expansion

Grid spending is supporting the electrical steel market, as transformer demand rises with transmission additions, replacement cycles, and higher reliability targets across several major power systems. India remains undersupplied because government-approved grid investment through 2032 includes large additions in transmission line length and transformer capacity, while domestic CRGO output still trails annual consumption by a wide margin. This gap has led to long-term capacity commitments, including the JSW JFE joint venture formed to address persistent supply tightness in the country. The electrical steel market also benefits from overlapping replacement needs in Europe and North America, where older transformer fleets now operate alongside stricter efficiency expectations and resilience planning. As these regional demand waves occur simultaneously, producers with qualified Grain Oriented Electrical Steel (GOES) output remain well-positioned, even as broader steel cycles soften.

Rising Demand for High-Efficiency Motors Driven by Regulatory Mandates

Regulation, not just customer preference, is pushing the electrical steel market toward premium Non-Grain-Oriented Electrical Steel (NGOES), changing the pace at which high-grade material enters procurement lists. The European Ecodesign framework already requires IE4 performance for defined motor classes, increasing the need for lower-loss lamination steel in qualifying designs. The same trend applies in the United States, where Department of Energy (DOE) standards are shaping a motor upgrade cycle that supports premium core materials in both the installed base and new equipment. The International Energy Agency’s work on industrial energy use reinforces this shift, as motors account for a large share of industrial electricity demand worldwide. As a result, small efficiency gains at the unit level can translate into system-level benefits. The electrical steel market, therefore, gains a steadier demand base when standards embed higher efficiency classes into purchasing decisions. This also means the premium end of the electrical steel market is less exposed to short-term swings in discretionary capital spending than ordinary flat steel categories.

Renewable Power Integration and Distributed Generation Growth

Renewable power growth is supporting the electrical steel market, especially where new generation capacity increases demand for transformers, converters, and specialized magnetic components across the network. Wind generation plays an important role because variable-speed equipment depends on low-loss magnetic performance, favoring advanced grades within the GOES segment. Distributed generation is also changing the demand mix, as each added unit of renewable capacity often requires additional step-up and step-down equipment rather than a single centralized connection point. This shift increases electrical steel intensity across the system and broadens demand beyond the replacement cycle for conventional grid assets. The IEA’s 2025 work on industrial transition is expected to indicate that procurement decisions are increasingly considering lifecycle emissions and energy performance, which could benefit producers that combine technical quality with lower-carbon supply positioning. For the electrical steel market, this creates scope for value to shift toward suppliers that can meet both efficiency and sourcing expectations without increasing delivery risk.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Energy Consumption in Electrical Steel Manufacturing | -0.4% | Global, most acute in Europe and Japan | Long term (≥ 4 years) |

| Complex Manufacturing Processes and High Capital Intensity | -0.3% | Global, most constraining for emerging market entrants | Medium term (2-4 years) |

| Increasing Competition from Low-Cost Imports Displacing Domestic Producers | -0.2% | Europe and North America, with spillover to South America and the Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Energy Consumption in Electrical Steel Manufacturing

The electrical steel market faces a structural cost challenge because electrical steel requires significantly more energy to produce than conventional steel sheet. Non-grain-oriented electrical steel can require around 6,500 kWh per tonne, making power prices a key factor in operating economics across regions. This pressure is particularly evident in Europe, where higher electricity costs have reduced margins and contributed to plant shutdowns already facing import pressure[2]thyssenkrupp Electrical Steel, “Import Crisis for Grain-Oriented Electrical Steel, thyssenkrupp Electrical Steel Extends Production Cuts at Its Isbergues Site in France,” thyssenkrupp Electrical Steel, thyssenkrupp-steel.com. Producers cannot address this issue quickly because silicon alloying and annealing conditions directly affect magnetic performance. As a result, they cannot easily change energy inputs or process routes without affecting metallurgy. For the electrical steel market, capacity expansion remains more feasible in regions with lower power costs or stronger state support. The market may also continue to record uneven regional economics, even when end-use demand remains strong.

Complex Manufacturing Processes and High Capital Intensity

The electrical steel market also faces constraints due to the need for specialized rolling, annealing, and coating systems, which require significant upfront capital and lengthy qualification periods. Higher silicon content improves magnetic performance but increases brittleness, making precise rolling schedules and controlled furnace conditions more important than in conventional steelmaking. POSCO’s planned June 2026 development program highlights this challenge, as it targets 6.5% silicon-content wide-sheet production, a grade that remains difficult to commercialize at scale through standard processing routes. New entrants in India, Southeast Asia, and South America face more than a construction challenge; they must also complete a multi-year process to secure customer approval for tight magnetic tolerances. The electrical steel market remains relatively concentrated at the premium end because buyers of EV motors and transformers cannot switch to new mills without lengthy technical validation. This slows supply diversification and supports incumbent producers’ market positions, even as new demand attracts fresh investment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Non-Grain Oriented Steel Anchors Revenue; GOES Outpaces in Growth

Non-grain-oriented electrical steel is expected to account for 68.42% of the electrical steel market share in 2025, supported by its use in automotive, industrial, and appliance motors and laminations. This segment benefits from broad volume demand, as it serves multiple motor-driven systems rather than a single end-use chain. Premium product development is shifting toward thinner gauges, especially in EV drive systems, where low iron loss supports heat control and range performance. ArcelorMittal’s iCARe 420Save platform, which is expected to extend to a 0.2 mm gauge in 2026, aligns with this trend by targeting tighter lamination requirements in high-speed electrified drivetrains. The Chinese standard YB/T 6421-2025 indicates that higher-performance non-grain-oriented electrical steel (NGOES) for EV drive motors is moving into a more formal product class with defined coating and material expectations.

POSCO’s non-grain-oriented export momentum indicates continued offshore demand for premium grades through 2025, as global automakers broaden sourcing requirements for electrified platforms. Grain-oriented electrical steel (GOES), while smaller in revenue terms, is forecast to grow at 6.24% through 2031, making it the fastest-growing product segment. Its expansion is linked to transformer demand, transmission upgrades, and replacement activity, creating a value profile that differs from the higher-volume NGOES segment. This trend indicates a split in the evolution of the electrical steel industry, with NGOES expanding through volume penetration in mobility and industrial applications, while GOES grows through high-specification transformer applications. This structure supports two separate growth paths within the electrical steel market rather than a single broad-based cycle. It also positions producers with both product families to balance volume, pricing, and technical differentiation across changing end-use patterns.

By Application: Motors Command Share; Transformers Lead Growth

Motors are expected to account for 43.15% of revenue in 2025, making them the largest application segment in the electrical steel market. This position reflects the scale of installed motor populations across factories, commercial systems, transport equipment, and household appliances. The market gains stability from this diversified demand base because it is not tied to a single customer group or capital spending cycle. Regulation supports this position, as higher motor efficiency classes require better laminations and tighter magnetic performance, even when equipment designs appear similar externally. The cited self-bonding coating work also shows why application-level performance is becoming more important, as small efficiency gains and lower iron loss at the assembly level affect end products.

Transformers are projected to grow at a 6.41% CAGR, making them the fastest-growing application segment through 2031. Transmission build-outs, substation upgrades, renewable integration, and deferred replacement activities support this growth across multiple regions. India's demand gap between cold-rolled grain-oriented (CRGO) steel consumption and domestic output is important because it shows how grid programs can drive imports and new investment when local capacity remains insufficient. Generators, inductors, and other magnetic applications also play a supporting role, especially as power electronics, charging infrastructure, and energy storage systems expand. This makes the application base broader than a motors-versus-transformers view. Smaller applications can also strengthen demand for higher-quality magnetic performance when they are linked to fast-growing electrified systems that require higher-frequency magnetic performance.

By Coating Type: Inorganic Coatings Lead; Self-Bonding Drives Innovation

Inorganic coatings are expected to account for 46.71% of segment revenue in 2025, maintaining their lead across the electrical steel coating mix. Their role remains important because transformer lamination stacks depend on thermal stability, electrical insulation, and reliable dimensional behavior under operating stress. Organic coatings remain relevant where punchability and lower friction support stamping operations, particularly in motor and appliance applications. Other formulations, including semi-organic variants, address the needs of users seeking a balance between insulation quality and processability. This coating mix shows that the coating layer directly affects manufacturability, losses, and assembly performance. It also means suppliers compete on more than steel chemistry when end users compare magnetic and processing outcomes.

Self-bonding coatings are projected to expand at a 6.84% CAGR through 2031, making them the fastest-growing category in the electrical steel market. This growth is linked to the shift away from welding and riveting in motor lamination assembly, especially in electric vehicle (EV) applications, where efficiency, vibration, and thermal behavior affect performance. The journal evidence cited in the reports indicates an approximately 0.5% improvement in motor efficiency and a 10% reduction in iron loss compared with welding and gluing methods. ArcelorMittal included both conventional and rapid self-bonding varnish capabilities in its Mardyck investment, indicating that this technology is entering mainstream production. POSCO Mobility Solution also offers self-bonding motor cores with defined bond strength and fluid compatibility, indicating that the offering has matured into a commercial line for premium motor designs. In the electrical steel market, this creates a product competition layer in which coating performance can influence the value captured from comparable substrate grades.

Geography Analysis

Asia-Pacific is expected to hold 54.82% of the electrical steel market share in 2025 and is forecast to grow at a CAGR of 6.37% through 2031, giving the region significant scale and growth momentum. The electrical steel market in Asia-Pacific benefits from steelmaking capacity, transformer demand, EV manufacturing, appliance output, and industrial motor use. China remains central to this position, as the country supports regional production infrastructure and global export activity across the supply chain. India adds support through large grid investments and transformer additions, which drive demand for Grain-Oriented Electrical Steel (GOES) and highlight domestic capacity gaps. South Korea and Japan remain important in the electrical steel market, as they support technical capabilities in premium grades and high-performance supply chains linked to vehicles, industrial equipment, and transformer users.

North America and Europe together account for a smaller share than Asia-Pacific, but they remain important to the electrical steel market due to demand in grid equipment and advanced electrified systems. North America benefits from replacement needs and continued investment, which support demand for transformer-grade materials and qualified domestic or near-market supply. Europe faces supply pressure as imports gain share while local producers manage higher energy costs and weaker margin protection. The thyssenkrupp Electrical Steel shutdown at Isbergues through part of 2026 highlights the region’s exposure to import pressure and cost inflation. ArcelorMittal’s Mardyck startup presents a different signal in the electrical steel market, as it supports European demand for Non-Grain Oriented Electrical Steel (NGOES) tied to automotive and industrial electrification.

South America, the Middle East, and Africa remain smaller in absolute terms, yet each adds strategic demand to the electrical steel market. In South America, transformer procurement is linked to transmission densification and efforts to strengthen power delivery across large geographic areas. In the Middle East, infrastructure expansion and industrial diversification programs support the use of Grain-Oriented Electrical Steel (GOES) in transformers and NGOES in motor-driven systems. South Africa remains relevant in the electrical steel market, as power infrastructure rehabilitation supports transformer demand amid chronic capacity shortfalls. Trade policy could become more influential across these regions as high-growth markets review import patterns, domestic industry exposure, and cost pass-through into downstream equipment manufacturing.

Competitive Landscape

The global electrical steel market is moderately consolidated, with higher concentration in high-grade niches where a limited number of producers meet the specifications of transformers and EV motors. China Baowu Steel Group, POSCO, Nippon Steel, and ArcelorMittal form the leading group, with each competing through a different mix of volume, process capability, and product positioning. Competition in the electrical steel market depends on more than tonnage, as coating systems, gauge control, loss performance, and qualification history support pricing in premium categories. ArcelorMittal’s Mardyck investment reflects this trend, combining new production, self-bonding varnish capability, and a product platform focused on automotive electrification demand in Europe. This move indicates that the electrical steel market continues to support targeted capital allocation when downstream customers prioritize performance and local supply reliability.

POSCO’s planned June 2026 consortium with Hyundai Motor and partner institutions represents another strategic initiative, focusing on silicon-content wide-sheet production for high-efficiency EV drive motors. In the electrical steel market, such programs can create technical barriers that are harder to replicate than standard capacity additions. White-space opportunities remain in import-dependent grain-oriented electrical steel (GOES) markets and in coating technologies that improve motor performance without requiring customers to redesign the full material system. This also indicates a competitive route outside primary steelmaking, where specialty coaters and lamination processors can create value by improving bonding, stamping, and assembly outcomes on existing substrates. This is relevant because the electrical steel market can face disruption at the processing level, while integrated steel production remains capital-intensive and slow to change.

Europe illustrates strategic tension in the electrical steel market. The restructuring path of thyssenkrupp highlights cost pressure and import displacement when a region has limited room to defend specialty production. voestalpine is taking a different route by investing in more electrified steel production at Donawitz, signaling an expectation that lower-carbon positioning will have greater relevance in future procurement decisions. Therefore, the electrical steel market remains competitive across technology, location, and energy profile. This combination should keep premium grades strategically important, even as broader steel markets move through uneven regional cycles.

Electrical Steel Industry Leaders

NIPPON STEEL CORPORATION

JFE Steel Corporation

Cleveland-Cliffs Inc.

POSCO

China Baowu Steel Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: POSCO is set to launch a national R&D consortium with Hyundai Motor and eight partner organizations, supported by South Korea's Ministry of Trade, Industry and Energy (MOTIE) and managed by the Korea Evaluation Institute of Industrial Technology (KEIT). The consortium will develop 6.5% silicon-content wide electrical steel sheets for EV drive motors. The project aims to address the brittleness of high-silicon steel and validate performance in EV drivetrains, with a focus on motor efficiency and iron loss reduction.

- February 2026: ArcelorMittal is expected to commence operations at its EUR 500 million (USD 571.5 million) electrical steel production unit in Mardyck, near Dunkirk, France. The facility represents the group’s largest European investment in a decade outside decarbonization programs. The unit will serve industrial and automotive electrification markets and include self-bonding varnish coating capabilities and the next-generation iCARe 420Save product platform extending to a 0.2 mm gauge.

Global Electrical Steel Market Report Scope

Electrical steel is a specialized iron-silicon alloy designed for electromagnetic applications. Its silicon content, ranging from 1% to 6.5%, increases electrical resistivity and reduces energy loss (core loss). Manufacturers cut electrical steel into thin, insulated laminations to build the cores of transformers and electric motors.

The electrical steel market is segmented by product type, application, coating type, and geography. By product type, the market is segmented into grain oriented electrical steel and non-grain oriented electrical steel. By application, the market is segmented into transformers, motors, generators, inductors, and other applications. By coating type, the market is segmented into inorganic coatings, organic coatings, self-bonding coatings, and other coatings. The report also covers market size and forecasts for electrical steel across 16 countries in major regions. The market sizes and forecasts are provided in terms of value (USD).

| Grain Oriented Electrical Steel |

| Non-Grain Oriented Electrical Steel |

| Transformers |

| Motors |

| Generators |

| Inductors |

| Other Applications |

| Inorganic Coatings |

| Organic Coatings |

| Self-Bonding Coatings |

| Other Coatings |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Grain Oriented Electrical Steel | |

| Non-Grain Oriented Electrical Steel | ||

| By Application | Transformers | |

| Motors | ||

| Generators | ||

| Inductors | ||

| Other Applications | ||

| By Coating Type | Inorganic Coatings | |

| Organic Coatings | ||

| Self-Bonding Coatings | ||

| Other Coatings | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Electrical Steel Market?

The Electrical Steel Market size is expected to grow from USD 28.43 billion in 2025 to USD 30.37 billion in 2026 and is forecast to reach USD 40.16 billion by 2031 at 5.75% CAGR over 2026-2031.

Which product segment leads revenue in 2025?

Non-grain-oriented electrical steel led revenue with a 68.42% share in 2025 because it served a broad mix of automotive, industrial, and appliance motor applications.

Which application is growing the fastest?

Transformers are the fastest-growing application, with a 6.41% CAGR through 2031, supported by grid expansion, replacement demand, and renewable power integration.

Which region is strongest in this space?

Asia-Pacific was the leading region, with a 54.82% share in 2025 and the fastest regional CAGR of 6.37% through 2031, supported by deep manufacturing and expanding end-use demand.

Page last updated on: