Electric Vehicle Wireless Charging Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

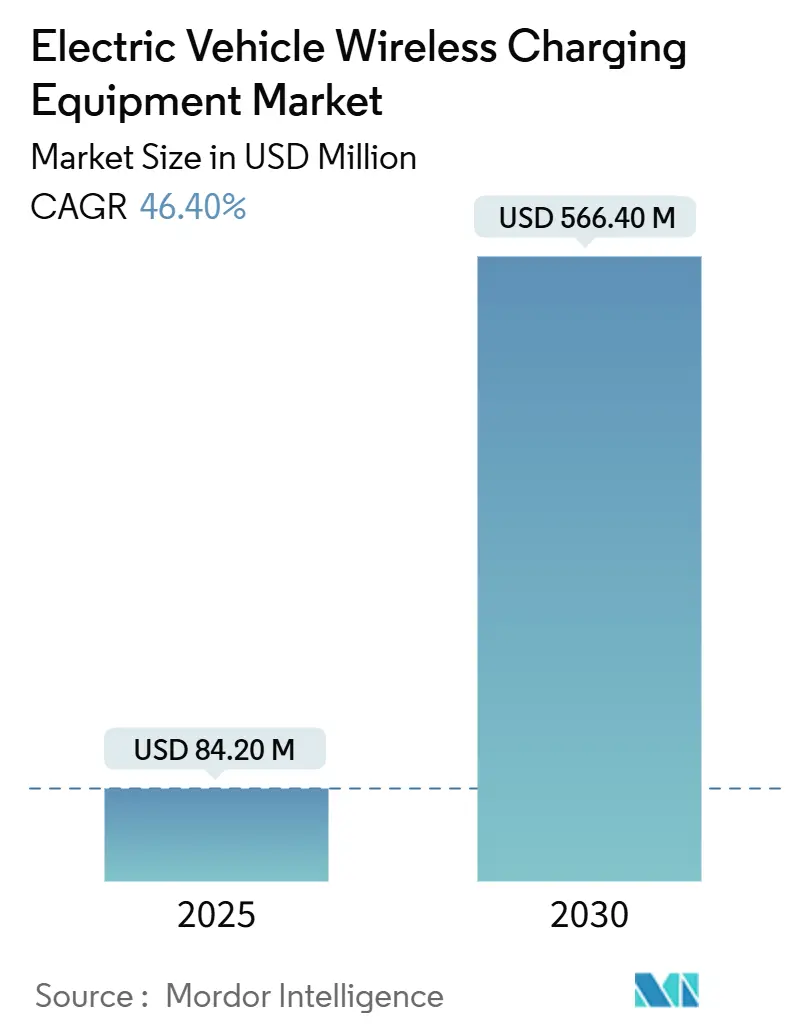

| Market Size (2025) | USD 84.20 Million |

| Market Size (2030) | USD 566.40 Million |

| Growth Rate (2025 - 2030) | 46.40% CAGR |

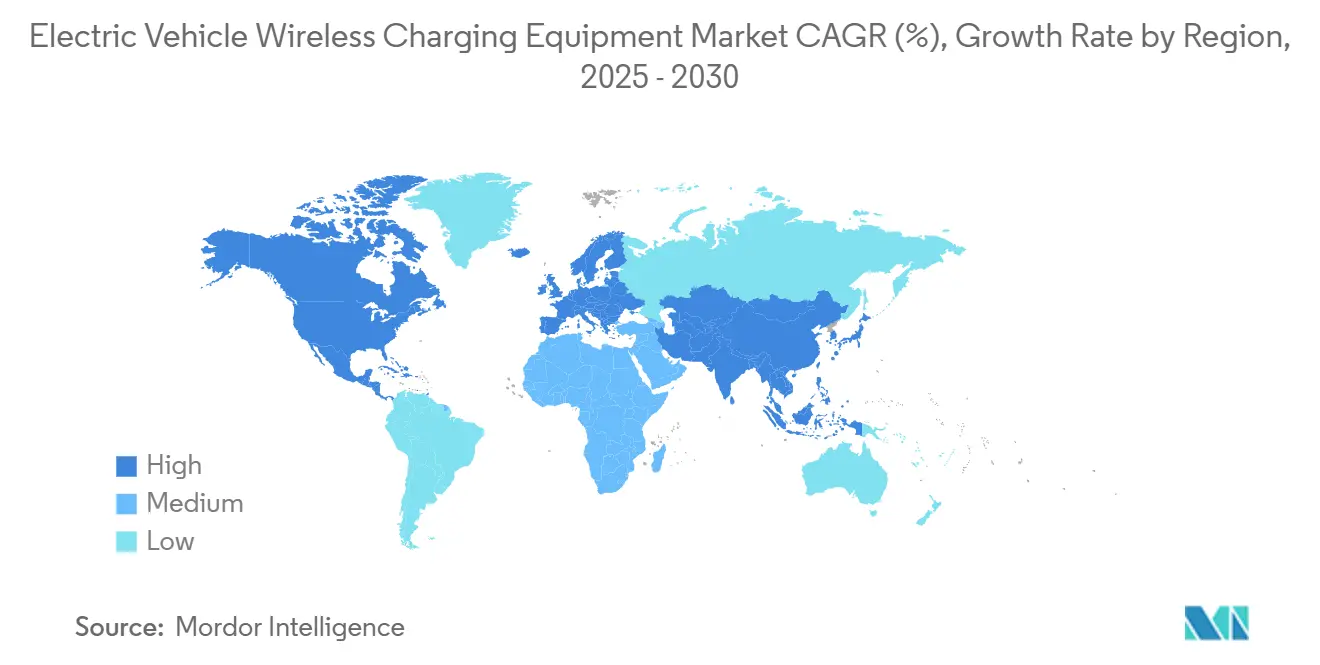

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Electric Vehicle Wireless Charging Equipment Market Analysis by Mordor Intelligence

The electric vehicle wireless charging equipment market size is valued at USD 84.20 million in 2025 and is projected to reach USD 566.40 million by 2030, growing at a 46.40% CAGR during the forecast period (2025-2030). Investment momentum reflects the shift from laboratory pilots to revenue-generating deployments, accelerated by Tesla’s purchase of Wiferion and the release of the SAE J2954 standard in August 2024. Automakers now view the technology as a differentiator because conventional plug-in infrastructure in major cities is approaching saturation. Europe currently commands the most significant regional demand, yet China’s rapid expansion of charging points positions the Asia-Pacific region as the fastest-growing arena. Across all areas, fleet operators emphasize that wireless charging reduces labor costs and enables high utilization rates, thereby reinforcing the adoption of technology despite higher capital expenditures.

Key Report Takeaways

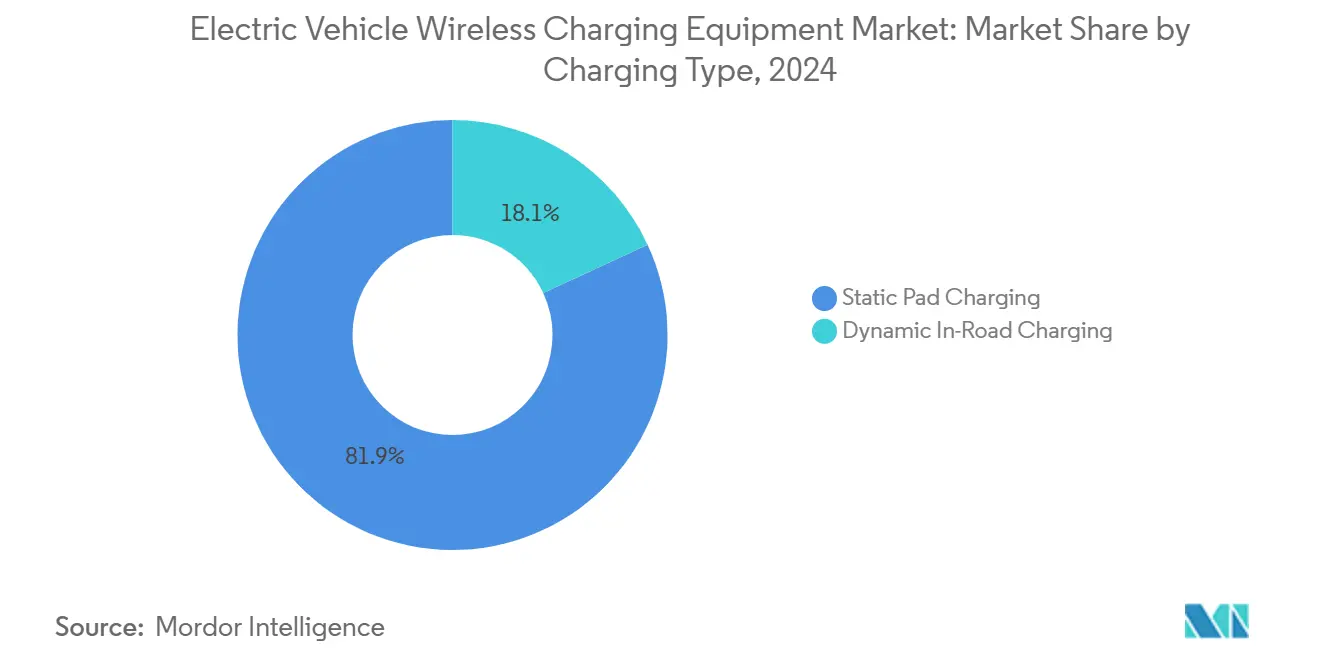

- By charging type, static pad systems led with 81.90% of the electric vehicle wireless charging equipment market share in 2024, while dynamic in-road solutions are forecast to climb at a 62% CAGR to 2030.

- By vehicle type, passenger cars held 65.20% of the electric vehicle wireless charging equipment market revenue share in 2024; buses and coaches are projected to expand at a 48% CAGR through 2030.

- By power output, units with up to 11 kW accounted for 57.80% of the electric vehicle wireless charging equipment market size in 2024. In contrast, installations above 150 kW are expected to grow at a 70% CAGR over the same period.

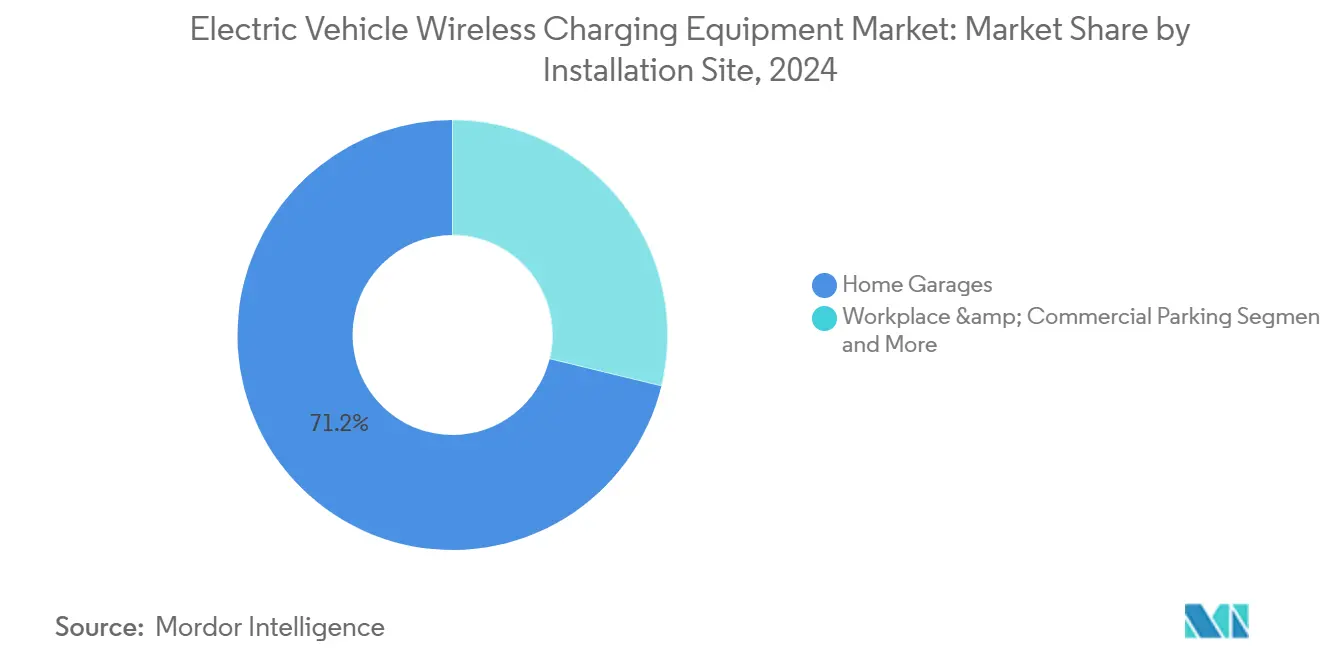

- By installation site, home garages represented 71.20% of the electric vehicle wireless charging equipment market size in 2024, while highway lane projects exhibit the highest outlook at a 57% CAGR through 2030.

- By technology platform, inductive resonant coupling led with 74.30% of the electric vehicle wireless charging equipment market share in 2024, while magnetic field alignment multi-coil systems are forecast to grow at a 66% CAGR through 2030.

- By power output, units with up to 11 kW accounted for 57.80% of the electric vehicle wireless charging equipment market size in 2024. above 150 kW are expected to grow at a 70% CAGR over the same period.

Global Electric Vehicle Wireless Charging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Point Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Acceleration In Global EV Sales | +12.5% | Global, with concentration in China, Europe, and North America | Medium term (2-4 years) |

| Extended Government ZEV Mandates & Incentives | +8.2% | North America & EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Early OEM Integration Into Premium Models | +7.8% | Global, led by German and Japanese automakers | Short term (≤ 2 years) |

| Fleet Electrification Demand For Autonomous Depot Charging | +6.9% | North America & EU, pilot projects in Asia-Pacific | Medium term (2-4 years) |

| Urban Anti-Cable Regulations & Curbside Inductive Pads | +4.1% | European cities, select North American municipalities | Long term (≥ 4 years) |

| Emerging SAE J2954-2 More Than 300 Kw Standard | +3.7% | Global, with early adoption in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Acceleration in Global EV Sales

The global momentum in electric vehicle sales creates unprecedented demand for differentiated charging solutions, with wireless technology emerging as a premium feature that commands higher margins for automakers. Tesla's strategic acquisition of Wiferion in August 2024 signals the technology's maturation beyond experimental phases, while WiTricity's establishment of a Japanese subsidiary in May 2024 demonstrates coordinated global expansion efforts.[1]"WiTricity Corporation, a U.S. company that manufactures EV wireless power transfer products, establishes a Japanese subsidiary in Tokyo", Japan External Trade Organization, www.jetro.go.jp The convergence of autonomous vehicle development with wireless charging is exemplified by Tesla filing four wireless charging patents in September 2024, targeting robotaxi applications where human intervention is impractical. This technological alignment suggests that wireless charging will transition from a luxury convenience to an operational necessity as mobility services scale.

Extended Government ZEV Mandates & Incentives

Zero-emission vehicle mandates increasingly recognize infrastructure limitations as barriers to adoption, prompting governments to incentivize wireless charging deployment through targeted subsidies and regulatory frameworks. Japan's consideration of subsidies for Tesla's charging stations within broader tariff negotiations illustrates how wireless technology becomes entangled with trade policy and industrial competitiveness. The establishment of the SAE J3400 standard as a Recommended Practice in September 2024 provides regulatory clarity, enabling government procurement programs to specify wireless charging requirements for public fleets.[2]"SAE Task Force Votes to Establish J3400 Standard as Recommended Practice, Joint Office of Energy and Transportation, driveelectric.gov European cities' exploration of anti-cable regulations for curbside parking creates a regulatory pull that complements a technology push, particularly as urban planners seek to eliminate visual pollution from charging infrastructure while maintaining accessibility.

Early OEM Integration into Premium Models

Automotive manufacturers leverage wireless charging as a differentiation strategy in premium segments, where technology premiums align with consumer willingness to pay for convenience features. BMW's collaboration with WiTricity on the 530e iPerformance represents the first commercially available wireless charging-enabled hybrid, establishing a template for luxury market penetration. Continental's announcement of an 11 kW wireless inductive charging system for production by the end of the decade, along with BMW and Mercedes-Benz's planned implementation, signals a coordinated industry movement toward standardization. The technology's integration with human-machine interface apps that guide precise vehicle positioning demonstrates how wireless charging enables broader automation strategies, positioning it as an enabler for autonomous parking and charging sequences.

Fleet Electrification Demand for Autonomous Depot Charging

Commercial fleet operators are increasingly viewing wireless charging as an operational imperative rather than a convenience feature, particularly for depot-based applications where labor costs for manual charging exceed the technology premiums. The Antelope Valley Transit Authority's deployment of three 250 kW inductive chargers from WAVE demonstrates how high-power wireless systems enable continuous fleet operations without the need for dedicated charging personnel. Electreon's Charging as a Service model eliminates upfront infrastructure investment while reducing battery capacity requirements by 50%, creating compelling total cost of ownership propositions for fleet operators. The technology's alignment with autonomous vehicle development creates synergistic value propositions, as demonstrated by Michigan's partnership with Electreon and Xos for wireless-charged delivery vehicles that operate without human intervention.

Restraints Impact Analysis*

| Restraint | (~) % Point Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High System & Installation Costs | -15.3% | Global, particularly acute in price-sensitive markets | Short term (≤ 2 years) |

| Interoperability & Standards Gaps | -8.7% | Global, with regional variations in adoption | Medium term (2-4 years) |

| Electro-Magnetic Safety Concerns In Dense Urban Zones | -6.2% | Urban areas globally are stricter in the EU and Japan | Medium term (2-4 years) |

| Grid Harmonics Constraints On Megawatt In-Road Lanes | -3.4% | Highway corridors with high-power dynamic charging | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High System & Installation Costs

Electric vehicle wireless charging systems command 2-3 times the cost of equivalent wired solutions, creating significant barriers to mass market adoption despite improving technology economics. WiTricity's 11 kW wireless charger carries a price point of USD 3,500, with installation costs ranging from USD 3,500 to USD 4,000, compared to traditional Level 2 chargers, which are typically priced below USD 1,000 when installed. Infrastructure deployment costs prove even more challenging, with dynamic charging lanes requiring an investment of approximately EUR 167 million, compared to EUR 105 million for equivalent fast-charging stations. However, both scenarios yield similar net present values over extended timeframes.[3]"A Corridor-Based Approach to Estimating the Costs of Electric Vehicle Charging Infrastructure on Highways", MDPI, www.mdpi.com The cost differential becomes particularly acute for public infrastructure deployment, where municipalities must justify premium pricing against limited utilization rates in early adoption phases.

Interoperability & Standards Gaps

Technical standardization challenges persist despite the establishment of SAE J2954, as competing technology platforms pursue proprietary advantages that fragment market development. The distinction between inductive resonant coupling and magnetic field alignment multi-coil systems creates compatibility concerns for infrastructure investors who are uncertain about future technology convergence. Patent landscape complexity, exemplified by Mojo Mobility's USD 192 million victory against Samsung for wireless charging patent infringement, creates legal uncertainties that discourage infrastructure investment. Regional variations in electromagnetic field exposure limits and safety standards further complicate global deployment strategies, as manufacturers must navigate different regulatory frameworks across key markets while maintaining cost-effective production scales.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Charging Type: Static Dominance Enables Dynamic Future

Static pad charging maintains commanding 81.90% of the electric vehicle wireless charging equipment market share in 2024, reflecting current commercial viability and consumer acceptance patterns, while dynamic in-road charging accelerates at 62% CAGR through 2030 as infrastructure investments target long-term mobility transformation. Static systems benefit from established installation protocols and proven reliability, as demonstrated by WiTricity's deployment across multiple automotive partnerships and Electreon's successful bus terminal implementations in Israel and Germany. Dynamic charging applications remain concentrated in pilot projects and specialized corridors. Yet, Michigan's 14th Street deployment and Sweden's Smartroad Gotland demonstrate commercial viability for heavy-duty applications where continuous charging enables smaller battery configurations.

The technology maturation timeline favors static solutions for immediate market development, while dynamic systems require coordinated infrastructure investment beyond individual vehicle purchase decisions. Oak Ridge National Laboratory's achievement of 270 kW wireless power transfer represents a breakthrough that bridges static and dynamic applications, as the same polyphase electromagnetic coupling technology enables both stationary and mobile charging scenarios. The growth trajectory of dynamic charging depends on public-private partnerships that align infrastructure investment with fleet electrification schedules, creating network effects that justify premium technology costs through operational efficiency gains.

By Vehicle Type: Commercial Fleets Drive Premium Adoption

Passenger cars command 65.20% of the electric vehicle wireless charging equipment market share in 2024, yet buses and coaches emerge as the fastest-growing segment at 48% CAGR through 2030, reflecting commercial operators' willingness to pay technology premiums for operational advantages that reduce total cost of ownership. Light commercial vehicles and medium & heavy trucks represent emerging applications where wireless charging enables autonomous depot operations without human intervention for charging procedures. Plug-in hybrid cars maintain steady demand as transitional technology, though their growth prospects diminish as battery electric vehicles achieve cost parity and charging infrastructure expands.

Fleet applications demonstrate superior economics compared to individual consumer adoption, as centralized depot charging enables standardized installation and maintenance procedures while maximizing utilization rates. The Port of Los Angeles's implementation of 500 kW wireless charging systems for heavy-duty trucks demonstrates how commercial applications can justify premium pricing through operational efficiency gains and compliance with emissions requirements. Buses and coaches particularly benefit from wireless technology's alignment with fixed route operations, where predictable charging schedules enable optimized battery sizing and reduced infrastructure complexity compared to opportunity charging with manual connections.

By Power Output: Megawatt Migration Accelerates

Up to 11 kW systems dominate current installations, accounting for 57.80% of the electric vehicle wireless charging equipment market share in 2024. This reflects residential and light commercial applications, where power requirements align with existing electrical infrastructure capabilities. In contrast, installations above 150 kW surge at a 70% CAGR, driven by commercial applications that demand rapid charging capabilities. The 11-50 kW segment serves as a bridge technology for workplace and retail applications, while 51-150 kW systems target fleet depot installations where moderate power levels balance charging speed with infrastructure costs. Applications exceeding 150 kW represent the technology frontier, where megawatt-class systems enable dynamic charging for heavy-duty vehicles and high-utilization commercial fleets.

Power output evolution reflects broader industry trends toward speedy charging, as demonstrated by ChargePoint's introduction of megawatt charging systems capable of delivering up to 3 megawatts for commercial applications. Wireless technology's power scaling challenges necessitate advanced thermal management and electromagnetic field control; however, breakthrough developments, such as Oak Ridge National Laboratory's 270 kW demonstration, demonstrate the technical feasibility of high-power applications. The power output distribution suggests market bifurcation between residential convenience applications and commercial efficiency solutions, with limited overlap in technology requirements and pricing strategies.

By Installation Site: Home Foundation Supports Highway Future

Home garages capture 71.20% of the electric vehicle wireless charging equipment market share in 2024, establishing wireless charging as a premium residential amenity that commands higher property values and appeals to affluent early adopters. Meanwhile, highway lanes represent the fastest-growing application, with a 57% CAGR through 2030, as public infrastructure investment targets the enablement of long-distance travel. Workplace and commercial parking installations serve as intermediate adoption vehicles, where employers provide wireless charging as employee benefits while testing technology reliability and user acceptance patterns. Public parking lots and retail locations offer revenue-generating opportunities for property owners, although utilization rates remain uncertain during early deployment phases.

Fleet and depot facilities demonstrate the most compelling economics for wireless charging adoption, as centralized installation enables standardized maintenance procedures while maximizing technology utilization through continuous operation schedules. Highway lane applications require coordinated public investment and standardized technology platforms; yet, successful pilot projects in Sweden and planned deployments in Michigan demonstrate the technical feasibility of dynamic charging infrastructure. The installation site distribution reflects technology adoption patterns that begin with controlled environments and expand toward public infrastructure as reliability and standardization mature.

By Technology Platform: Inductive Leadership Faces Multi-Coil Challenge

Inductive resonant coupling holds 74.30% of the electric vehicle wireless charging equipment market size in 2024, benefiting from established patent portfolios and proven commercial deployments. Magnetic field alignment multi-coil systems are expected to accelerate at a 66% CAGR through 2030, as next-generation technology platforms seek higher efficiency and power density advantages. Capacitive power transfer remains a niche application with specialized use cases, though its growth potential depends on breakthrough developments in energy transfer efficiency and safety protocols. The technology platform competition reflects fundamental physics trade-offs between power transfer efficiency, electromagnetic field containment, and system complexity.

WiTricity's acquisition of Qualcomm Halo's patent portfolio, encompassing over 1,500 wireless charging patents, demonstrates the strategic importance of intellectual property in technology platform competition. Magnetic field alignment systems offer theoretical advantages in terms of power density and misalignment tolerance; however, they require more complex control systems and higher manufacturing costs, which limit their current commercial viability. As demonstrated by Oak Ridge National Laboratory's breakthrough in polyphase electromagnetic coupling, the platform evolution suggests eventual convergence toward hybrid approaches that combine the reliability of inductive coupling with the performance advantages of multi-coil systems.

Geography Analysis

Europe controlled 38.20% of the electric vehicle wireless charging equipment market in 2024, anchored by climate regulations and early demonstration corridors such as Sweden’s e-motorway and Germany’s eCharge BASt. Norway added the world’s first inductive urban road in August 2024, showcasing Nordic leadership in blending renewable energy with wireless charging. Germany’s premium carmakers further boost regional usage by incorporating charging pads into luxury trims, reinforcing consumer familiarity.

Asia-Pacific accelerates at a 43% CAGR through 2030, propelled by China’s addition of 4.222 million charging points in 2024 alone. Beijing’s urban-renewal plans embed inductive bays within new apartment complexes, while provincial grants fund dynamic truck lanes on export corridors. Japan’s formation of the EV Wireless Power Transfer Council in April 2025 and WiTricity’s Tokyo branch underscore coordination among utilities, parts suppliers, and policymakers to seed national networks.

North America exhibits concentrated growth pockets. Michigan’s induction lane on 14th Street and California’s USD 20 million UCLA road project validate technical feasibility, but state-by-state rules on electromagnetic exposure mean patchwork permitting processes. The Joint Office’s support for SAE J3400 seeks to unify coupler specifications and integrate wireless billing data into federal funding criteria. Mexico and Canada remain emergent spaces; cross-border freight operators advocate for corridor interoperability to safeguard investment in trucks equipped with underbody receivers. Together, these regional narratives suggest the wireless EV charging market will evolve as a mosaic of national pilots scaling into continental networks. Cost declines and standard harmonization are expected to reduce adoption gaps by the decade’s end.

Mordor Intelligence provides coverage of the electric vehicle wireless charging equipment market across other key regional markets, including Asia and Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

Competition is moderate yet intensifying. WiTricity deploys a patent-heavy licensing model, having absorbed Qualcomm Halo’s 1,500-plus patents, and recently licensed Yura Corporation to penetrate Korean supply chains. Electreon promotes infrastructure-as-a-service, earning recurring revenue by operating inductive roads in Israel, Sweden, and the United States. Tesla occupies a vertically integrated niche, folding Wiferion’s hardware into its broader robotaxi roadmap and owning vehicle, software, and pad IP.

Tier-one suppliers such as Continental, Bosch, and MAHLE leverage existing OEM relationships to package inductive modules alongside conventional power-electronics suites. Siemens’ equity investment in WiTricity and ABB’s partnership announcements indicate a systemic shift: major electrical firms are preparing their portfolios to cover both wired and wireless formats, safeguarding their market share as fleet electrification accelerates.

Technological breakthroughs continue to reshape competitive dynamics. Oak Ridge’s 270 kW prototype recorded power densities up to ten times those of current commercial pads, pressuring private firms to accelerate their R&D timelines. Patent disputes exemplified by Mojo Mobility’s USD 192 million win highlight the strategic value of defensible IP. Consequently, many late entrants adopt cross-licensing to avoid litigation. Early-mover alliances forged in 2024–2025 are likely to harden into durable ecosystem clusters that set de facto standards for coil geometry, communication protocols, and safety certification.

Electric Vehicle Wireless Charging Equipment Industry Leaders

-

WiTricity Corporation

-

HEVO Inc.

-

Plugless Power Inc.

-

InductEV Inc.

-

Electreon Wireless Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The Indian government has introduced an innovative indigenous wireless charger, developed collaboratively by the Centre for Development of Advanced Computing (C-DAC) and the Visvesvaraya National Institute of Technology (VNIT) in Nagpur. Specifically designed for electric vehicles, this charger can charge up to 90% of a vehicle's battery in approximately three hours. This breakthrough highlights a significant technological achievement and supports the nation’s commitment to sustainable and efficient transportation solutions.

- November 2024: Electreon collaborated with UCLA on a USD 20 million wireless charging roadway project, representing California's first wireless charging road and demonstrating the technology's expansion into major U.S. metropolitan areas.

- November 2024: Michigan collaborated with Electreon and Xos Inc. to implement wireless charging technology for delivery vehicles in Detroit, showcasing commercial vehicle applications and state-level support for wireless charging infrastructure.

- June 2024: Oak Ridge National Laboratory achieved a world record of 270 kW in wireless power transfer for light-duty electric vehicles using polyphase electromagnetic coupling coils, demonstrating 96% efficiency and the ability to charge a Porsche Taycan to 50% state of charge within 10 minutes, thereby establishing new benchmarks for high-power wireless charging applications.

Global Electric Vehicle Wireless Charging Equipment Market Report Scope

The scope includes segmentation by Charging Type (Static Pad Charging, Dynamic In-Road Charging), Vehicle Type (Passenger Cars, Light commercial vehicles, Medium and Heavy Duty Trucks, and Buses and Coaches), Power Output (Up To 11 KW, 11-50 KW, 51-150 KW, and Above 150 KW), Installation Site (Home Garages, Workplace & Commercial Parking, Public Parking Lots & Retail, Fleet & Depot Facilities, and Highway Lane), Technology Platform (Inductive Resonant Coupling, Magnetic Field Alignment Multi-coil, and Capacitive Power Transfer), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The market forecasts are provided in terms of value (USD).

| Static Pad Charging |

| Dynamic In-Road Charging |

| Passenger Car |

| Light Commercial Vehicles |

| Medium & Heavy Trucks |

| Buses & Coaches |

| Up to 11 kW |

| 11-50 kW |

| 51-150 kW |

| Above 150 kW |

| Home Garages |

| Workplace & Commercial Parking |

| Public Parking Lots & Retail |

| Fleet & Depot Facilities |

| Highway Lanes |

| Inductive Resonant Coupling |

| Magnetic Field Alignment Multi-coil |

| Capacitive Power Transfer |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| By Charging Type | Static Pad Charging | |

| Dynamic In-Road Charging | ||

| By Vehicle Type | Passenger Car | |

| Light Commercial Vehicles | ||

| Medium & Heavy Trucks | ||

| Buses & Coaches | ||

| By Power Output | Up to 11 kW | |

| 11-50 kW | ||

| 51-150 kW | ||

| Above 150 kW | ||

| By Installation Site | Home Garages | |

| Workplace & Commercial Parking | ||

| Public Parking Lots & Retail | ||

| Fleet & Depot Facilities | ||

| Highway Lanes | ||

| By Technology Platform | Inductive Resonant Coupling | |

| Magnetic Field Alignment Multi-coil | ||

| Capacitive Power Transfer | ||

| Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current EV wireless charging equipment market size and projected growth?

The wireless EV charging market size is USD 84.20 million in 2025 and is forecast to rise to USD 566.40 million by 2030, representing a 46.40% CAGR.

Which charging type leads the market today?

Static pad systems lead with 81.90% market share, reflecting simpler installation and proven reliability.

Why do fleet operators favor wireless charging?

Eliminating manual plug-in labor and enabling round-the-clock operation reduces total operating costs and aligns with autonomous vehicle strategies.

What are the main obstacles to wider adoption?

High installation costs and interoperability concerns due to competing technology platforms and evolving standards remain primary restraints.

Page last updated on: