Electric Tea Maker Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.56 Billion |

| Market Size (2031) | USD 2.12 Billion |

| Growth Rate (2026 - 2031) | 6.32% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Electric Tea Maker Market Analysis by Mordor Intelligence

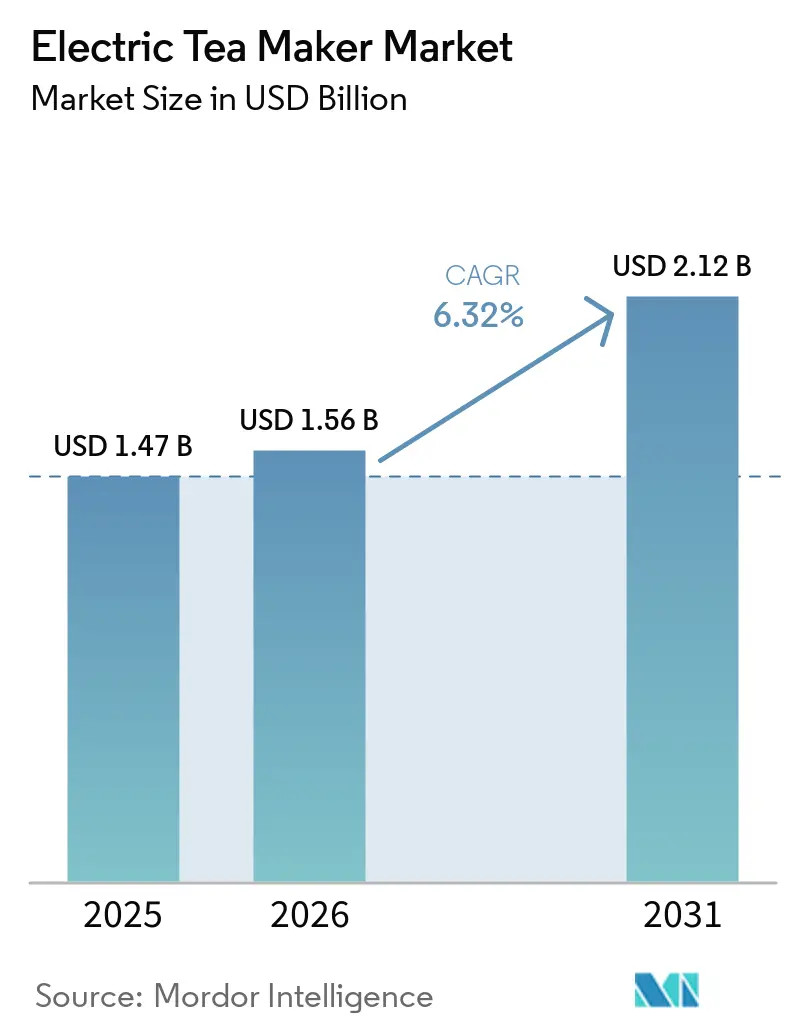

The global electric tea maker market size stood at USD 1.56 billion in 2026, up from USD 1.47 billion in 2025, and is projected to reach USD 2.12 billion by 2031 at an 6.32% CAGR. Consistent household upgrades to programmable and variable-temperature models, steady hospitality purchasing, and the normalization of smart connectivity in mid-range price tiers support near-term resilience. The market growth is supported by increasing adoption of variable-temperature kettle technologies and smart kettles (Wi-Fi/app-controlled) models that allow precise brewing and remote operation. Market integrity benefits from tighter border enforcement against unsafe or counterfeit appliances, as evidenced by the United Kingdom Office for Product Safety and Standards’ recurring border rejections citing failures to meet core electrical and plug safety requirements. Consumer confidence in compliant offerings is also shaped by North American adoption of UL 60335-1 7th Edition as the baseline appliance safety framework for household devices. On the sustainability front, the European Union’s Right to Repair initiative raises expectations for serviceability and product longevity messaging, which premium brands already use to differentiate build quality and post-purchase support[1]europarl europa.eu https://www.europarl.europa.eu/news/en/press-room/20240419IPR20590/right-to-repair-making-repair-easier-and-more-appealing-to-consumers. Material innovation is another driver, with rising demand for borosilicate glass kettle designs and BPA-free plastic kettle options that address health and safety concerns. Portable formats, such as a travel tea maker, are also emerging, especially among urban and mobile consumers.

Key Report Takeaways

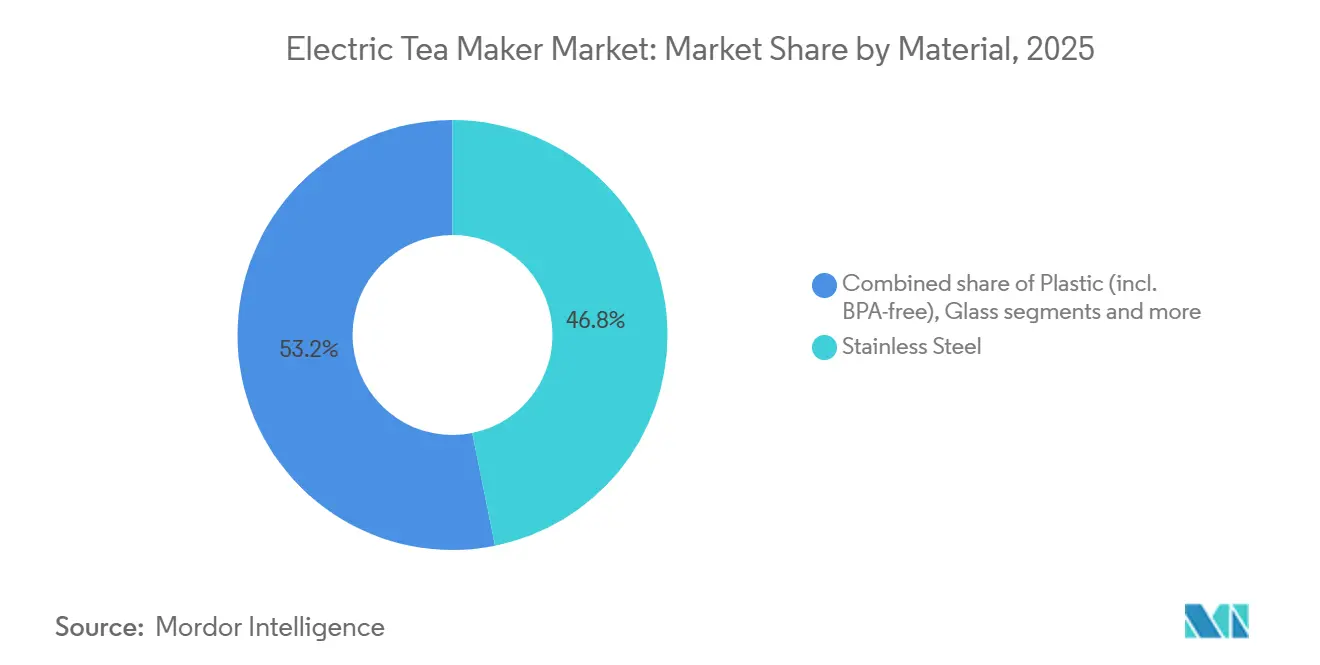

- By material, stainless steel led with 46.83% of the global electric tea maker market share in 2025; plastic is forecast to expand at a 6.64% CAGR to 2031.

- By capacity, the 1.0–1.5-liter bracket commanded 51.72% of the global electric tea maker market share in 2025; >1.5 liters is projected to grow at a 6.57% CAGR through 2031.

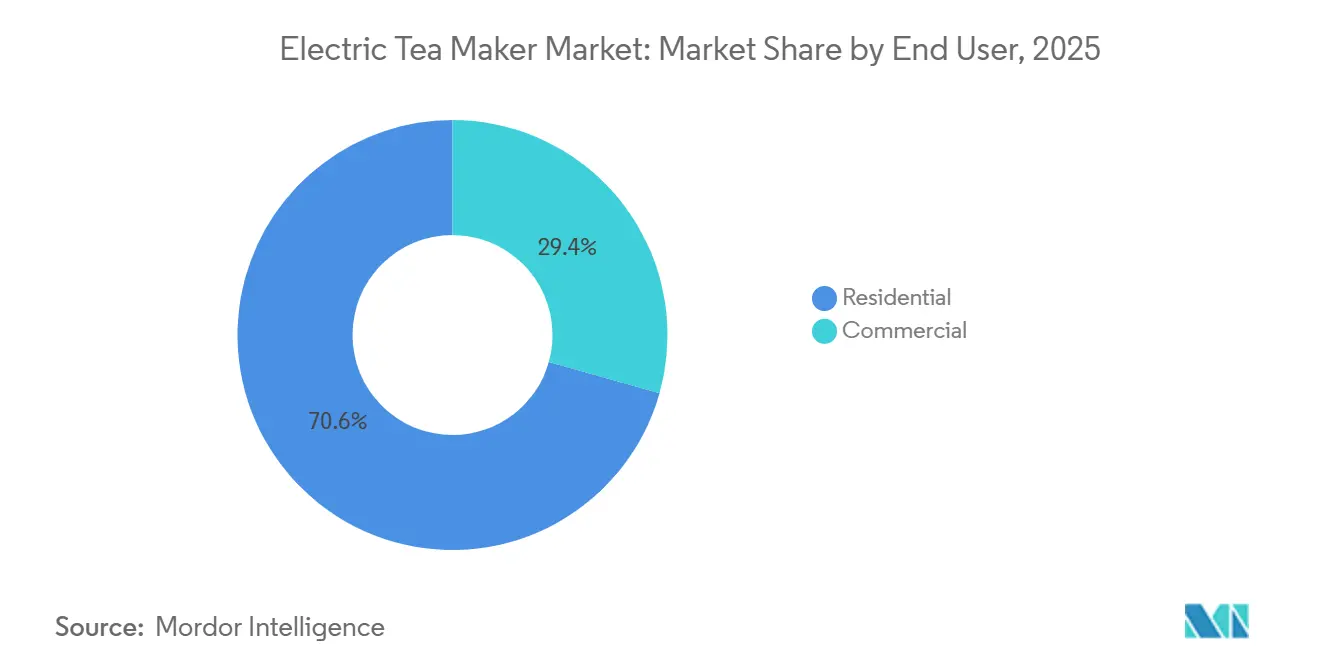

- By end user, residential accounted for 70.64% of the global electric tea maker market share in 2025; commercial is on track for a 6.84% CAGR to 2031.

- By distribution channel, B2C retail dominated with a 75.62% of the global electric tea maker market share in 2025; online sales within B2C are set to advance at a 7.46% CAGR through 2031.

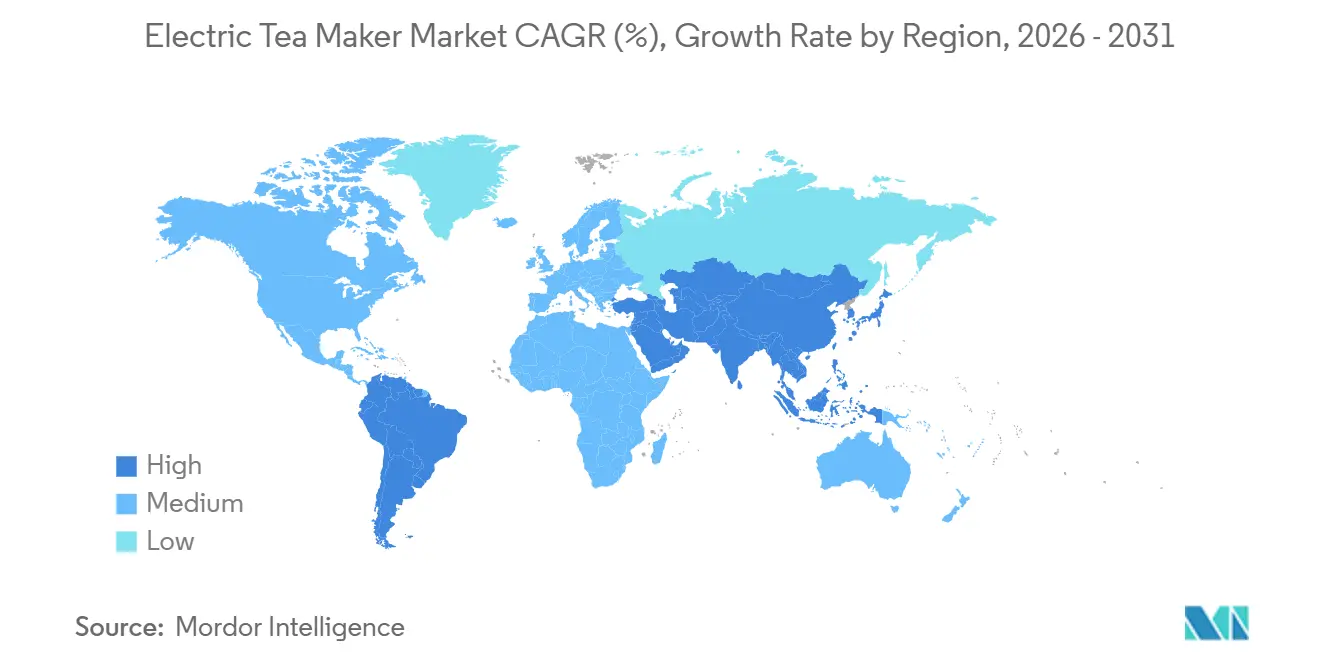

- By geography, Asia-Pacific held 41.94% of the global electric tea maker market share in 2025 and is projected to grow at a 6.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electric Tea Maker Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenience-driven hot beverage preparation at home and work | +1.2% | Global, strongest in North America and Europe, with high cordless adoption | Medium term (2-4 years) |

| Rising tea consumption and premium tea culture in key markets | +1.8% | Asia-Pacific core, spillover to the Middle East and North America | Long term (≥ 4 years) |

| Expansion of e-commerce and D2C for small appliances | +0.9% | Global, led by China and India, penetration, followed by the United States/EU marketplaces | Short term (≤ 2 years) |

| Adoption of smart/variable-temperature kettles for specialty teas | +1.5% | North America, Europe, and Asia-Pacific urban hubs | Medium term (2-4 years) |

| Health and wellness infusions enabled by tea makers | +0.7% | Global, early gains in metro areas with functional-tea demand | Short term (≤ 2 years) |

| Sustainability and repairability features influencing purchase decisions | +0.5% | EU, North America, and select Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Convenience-Driven Hot Beverage Preparation at Home and Work

Rapid-boil performance, cordless 360-degree bases, and one-handed pouring ergonomics position modern kettles as frictionless tools for morning routines and shared office pantries. Feature sets like programmable start times and short-duration keep-warm modes reduce queuing during peak times and enable consistent temperatures for consecutive brews without reboiling. In workplaces and coworking hubs, the capital-light nature of deploying multiple rapid-boil appliances has appealed to facility managers seeking hygienic hot-water access without plumbing retrofits, which supports steady procurement outside peak household seasons. At the design level, modern products meet stricter automatic shutoff, boil-dry protection, and handle strength test requirements defined by IEC 60335-2-15:2024, which indirectly improves the user experience by reducing nuisance faults and aligning thermal controls more closely with intended use. Modern consumers are also shifting toward cordless electric kettles for ease of use, while niche formats such as gooseneck electric kettles are gaining traction among specialty tea and pour-over enthusiasts. Additionally, multifunctionality is expanding, with products incorporating multifunction tea infuser systems and health pot capabilities to support herbal and wellness beverages.

Rising Tea Consumption and Premium Tea Culture in Key Markets

A broader shift toward quality-differentiated leaves and specialty formats requires reliable thermal precision at home and in retail service, which aligns with variable-temperature kettles that can deliver distinct temperature bands for green, oolong, white, and black teas. Global tea market dynamics in 2024 highlight continued interest in higher-quality, value-added segments alongside sustainability attributes, with voluntary sustainability standards accounting for a sizable share of world tea output. This trend amplifies consumer expectations for brewing consistency to realize flavor benefits in these premium tiers. As specialty-focused retailers expand in urban centers, their brew protocols influence home routines, reinforcing consumer intent to reproduce café-level extraction precision with electric kettles that offer multi-step presets. These patterns sync with connected appliances that store user profiles or program sequences by tea type, helping casual drinkers achieve repeatable results with minimal trial-and-error. Safety standards function as underpinning guardrails for this premium shift, since temperature control and insulation design must perform reliably at fine-grained settings over extended usage cycles defined in IEC 60335-2-15. Collectively, these developments strengthen long-term demand for variable-temperature equipment across the electric tea maker market.

Expansion of E-Commerce and D2C for Small Appliances

Online discovery and purchasing compress the path to purchase by packaging price transparency, reviews, and product videos that focus attention on durable build quality, boil-time performance, and after-sales support. Direct-to-consumer storefronts allow premium brands to own customer relationships and control merchandising narratives about safety, materials, and care. At the same time, marketplaces broaden access to lower-cost models that meet entry-level needs. That said, the openness of cross-border marketplace logistics attracts counterfeiters that exploit fragmented oversight; the United States Customs and Border Protection notes that the vast majority of intellectual property seizures originate from a narrow set of jurisdictions and travel through mail and express channels typical of marketplace parcel flows, which keeps vigilance high for small electric appliances. Repeated safety alerts and border rejections by the United Kingdom authorities highlight how illegal plugs, unsafe fuses, and poor earthing persist in listings that mimic compliant brands, underscoring the importance of authorized-seller programs and traceable model numbers on online product pages[2]gov.uk https://www.gov.uk/product-safety-alerts-reports-recalls/product-safety-report-foldable-travel-electric-kettle-2604-0082. As brands consolidate their e-commerce operations, alignment with evolving standards and documentation practices becomes part of the online merchandising stack, signaling compliance to reduce buyer hesitation. The net effect continues to support unit growth through digital channels while reserving premium margins for company-owned storefronts that foreground material safety and warranty coverage.

Adoption of Smart/Variable-Temperature Kettles for Specialty Teas

Precision control spanning the typical 70°C to 100°C window is a functional differentiator for brewing green, oolong, white, and black teas at their respective extraction optima, a capability that on/off kettles cannot match with the same repeatability. Connected models add app interfaces and firmware logic to manage presets and guide users through time, temperature, and rest sequencing for delicate leaves or herbal blends. The seventh edition of IEC 60335-2-15 codifies additional requirements that intersect with connectivity, including provisions for remote operation to ensure safety algorithms govern heating behavior across both local and remote inputs. In North America, integration with the UL 60335-1 framework reinforces common testing and documentation workflows, shortening timelines for multi-market product families that share safety architectures[3]shopulstandards.com https://www.shopulstandards.com/ProductDetail.aspx?productId=UL60335-1_7_S_20251211. The rise of specialty brewing has further accelerated demand for variable-temperature kettles and gooseneck electric kettles, which offer precision pouring and temperature control. Meanwhile, hybrid appliances such as multifunction tea infuser units and health pot systems allow users to prepare tea, herbal infusions, and functional beverages in a single device.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material price volatility (stainless steel, plastics, electronics) | -0.8% | Global, more acute in high-cost markets | Short term (≤ 2 years) |

| Proliferation of low-quality/counterfeit imports is eroding brand trust | -0.6% | Concentrated in e-commerce-heavy channels | Medium term (2-4 years) |

| Compliance burden for multi-market safety and environmental standards | -0.4% | EU, North America, the Middle East, and Japan | Long term (≥ 4 years) |

| Infrastructure constraints (voltage variability, limescale/water quality) | -0.3% | South Asia, Africa, parts of South America, and Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw Material Price Volatility (Stainless Steel, Plastics, Electronics)

Stainless steel price movements and alloy input swings affect unit economics, pressuring margins for both entry-level and premium models. Market updates from steel producers and distributors show that 304-series pricing has faced stepwise increases into 2026 in parts of Asia, with certain Taiwan mills posting consecutive monthly hikes through early April 2026, citing currency shifts, energy costs, and upstream nickel dynamics[4]xrtgsteel.com https://xrtgsteel.com/rising-global-costs-drive-april-2026-stainless-steel-prices-to-new-highs/. Chinese stainless pricing commentary in early 2026 similarly points to inventory adjustments and supply-demand balances that can influence appliance-grade coil purchase costs, reinforcing the need for hedging in OEM contracts. For planners, volatility complicates forward pricing and SKUs that depend on specific grades for corrosion performance. When sudden surcharges flow through logistics or raw materials, brands face choices between passing costs to retail prices or adjusting material specs, each with a different brand-perception tradeoff. In this context, supply agreements, material alternates for non-wetted components, and staggered procurement windows help buffer costs without diluting perceived quality in the electric tea maker market.

Proliferation of Low-Quality/Counterfeit Imports Eroding Brand Trust

Border authorities continue to intercept unsafe or counterfeit kettles that present electrical hazards in the United Kingdom. OPSS reports documenting shipments rejected for non-compliant plugs, inadequate earthing, and dangerous fuse constructions that pose fire or shock risks. In the United States, customs data emphasize that the majority of intellectual property seizures occur in small-parcel channels typical of cross-border e-commerce, signaling persistent brand-protection exposure for legitimate manufacturers. Manufacturers respond with authorized-seller programs, model verification resources, and consumer education, as seen in prominent brands’ counterfeit-identification pages that guide shoppers to flag suspicious listings and avoid fraud. Reputational harm from look-alike products that fail early or perform unsafely can spill over to genuine brands when consumers misattribute defects, increasing warranty costs and driving additional investment in enforcement and education. As platforms refine seller checks, documentary compliance, and transparent traceability remain essential signals that differentiate legitimate offers in the electric tea maker market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Plastic Gains on Cost, Steel Retains Safety Reputation

The segment profile shows stainless steel accounting for 46.83% of 2025 revenue, while plastic is projected to grow the fastest over the forecast period of 6.64%. Health-conscious consumers, however, keep gravitating to all-steel or glass-wetted interiors, a trend that intensified after university research in 2025 highlighted microscopic particle releases from plastic assemblies under heat, sharpening the premium for borosilicate glass and 304/316-grade stainless designs. As global standards harden, handle strength testing and impact criteria for glass, along with requirements for safe automatic shutoff and boil-dry protections, are shaping design baselines across this segment, aiding premium positioning where durability and safety documentation matter most. Glass retains a premium niche, favored by buyers who prioritize visual clarity and inert contact, particularly in the upper bands of the electric tea maker market.

Price-performance dynamics steer brand playbooks in this segment. The interior-wetted surface narrative has become central to positioning, with clear disclosures about grades of stainless steel and glass construction used to differentiate models. On the cost side, component choices remain sensitive to alloy and resin movements, reinforcing the need for procurement hedging and for clear segmentation between budget, mid-range, and premium lines as raw-material prices shift. With these conditions in place, stainless steel is likely to maintain a high share in developed markets. At the same time, plastic’s affordability supports faster percentage growth from a larger installed base in emerging markets across the electric tea maker market.

By Capacity: Mid-Size Dominates, Large Formats Gain on Commercial Uptake

The 1.0–1.5-liter bracket accounted for 51.72% of 2025 sales, reflecting its fit for two- to four-person households and compact kitchens. Product platforms in this mid-size range tend to balance boil speed, footprint, and energy use per cycle, which helps sustain broad appeal across regions. Large-format units above 1.5 liters are set to outpace the category on CAGR, tied to hospitality chains, tea-focused retailers, and larger households that benefit from fewer cycles and higher throughput per boil. Smaller travel-oriented sizes below 1.0 liter meet portability needs but remain limited by refill frequency and perceived tradeoffs in performance. These practical considerations support stable leadership for mid-size appliances in household channels while offering headroom for large formats in commercial and multi-user settings in the electric tea maker market.

Design and safety frameworks support diversity of capacity. Glass-bodied kettles that emphasize visibility tend to concentrate in mid-size models to balance weight, impact risk, and handling safety, aligned with new impact and handle tests in the IEC 60335-2-15 standard. Stainless steel dominates larger-capacity applications where commercial handling or heavy household use favors dent resistance and long service life. For buyers who prefer to standardize across sizes and voltage requirements, multi-market safety documentation tied to UL 60335-1 in North America and to the IEC framework in Europe and the Middle East hastens approvals and aligns user instructions across product families. These underpinnings help scorecards for total cost of ownership, throughput per cycle, and safety margin remain central to capacity choices across the electric tea maker market.

By End User: Residential Anchors Volume, Commercial Pursues Margin

Residential customers accounted for 70.64% of 2025 revenue, buoyed by steady replacement cycles and the spread of precision presets that remove guesswork from brewing. Commercial demand is set to grow faster, at a CAGR of 6.84%, as cafés, tea bars, hotels, and office pantries codify brew protocols by tea type. This approach depends on reliable, repeatable temperature control. Connected features simplify training and support fleet management across locations, while safety provisions for remote operation in IEC 60335-2-15 provide an extra layer of risk control for operators. In practice, this move toward protocolized brewing elevates the perceived value of premium models that already have durability, clear documentation, and test evidence. With these priorities front and center, procurement teams can justify higher per-unit prices by linking to quality and consistency gains in the electric tea maker market.

Household users continue to prioritize ergonomics, fast boiling, and easy cleaning, but concern about microscopic plastic particles from heated components has heightened sensitivity to interior materials and disclosures, a consumer lens shaped by 2025 university research. In commercial settings, safety and reliability drive brand selection, supported by visible compliance labels and authorized service availability. Enforcement communications from market surveillance authorities and customs services further nudge buyers toward documented, traceable products, bolstering the case for established brands that can evidence compliant builds and proactive product stewardship. These forces sustain residential scale while empowering commercial channels to deliver faster growth and higher margin potential across the electric tea maker market.

By Distribution Channel: Online Surges, Offline Defends Service Touchpoints

B2C retail accounted for 75.62% of 2025 sales, with online sub-channels set to outpace overall retail growth of 7.46% as consumers lean on ratings, Q&A threads, and detailed product photos to assess performance claims and gauge quality. Direct-to-consumer outlets help premium brands control merchandising, certification display, and warranty communication, while marketplaces provide unmatched reach for budget SKUs. The flip side of that reach is exposure to counterfeit or non-compliant listings, a risk that customs and market-surveillance communications continue to spotlight across small appliances. To counter these risks, established manufacturers maintain authorized-seller rosters, model verification pages, and consumer guidance hubs that point shoppers to approved channels with after-sales support and legitimate warranties. Offline stores defend relevance through hands-on evaluation and bundled services, which help close premium purchases that depend on tactile checks and in-person explanations of safety and materials. This balanced channel architecture sustains broad access while improving trust signals in the electric tea maker market.

For brands seeking omnichannel consistency, publishing safety documentation, model-identification guidance, and service options in online listings mirrors the in-store experience and reduces consumer hesitation. Clarity on test standards, including references to IEC 60335-2-15 and UL 60335-1 where applicable, supports informed decisions by both households and commercial buyers. These practices contribute to higher conversion and fewer returns, strengthening the business case for continued digital expansion across the electric tea maker market.

Geography Analysis

Asia-Pacific led with 41.94% of 2025 revenue and is projected to post the highest regional growth through 2031, supported by large tea-drinking populations, expanding specialty formats, and the mainstreaming of variable-temperature features in mid-range price bands. Market entry and replacement cycles in the region benefit from global safety reference points, as the IEC 60335-2-15 framework defines durability and temperature-control checks that scale with rising unit volumes. Premium household segments and commercial tea service operators in urban hubs rely on equipment that meets these standards, anchoring consistent flavor delivery and service confidence. In parallel, global brand compliance and documentation practices ease cross-border listings in Asia-Pacific marketplaces, strengthening consumer assurance in markets where online discovery is common. With these supports, the electric tea maker market in Asia-Pacific sustains both value-led and feature-led trajectories.

North America is expected to grow at 5.6% over the forecast period, primarily through replacement purchases and premiumization in variable-temperature and connected models. Adoption tracks the North American baseline established by UL 60335-1 7th Edition, which harmonizes safety expectations with the underlying IEC framework and accelerates regulatory alignment for product families. In the United States, continued customs vigilance against counterfeit and unsafe small electronics reinforces the role of authorized distribution and documented compliance in maintaining consumer confidence. Canada’s compliance verification signals an active oversight posture that responsible importers can meet with robust testing and technical files, a practice that should sustain trust in premium brands across the category. Together, these elements underpin steady momentum for the electric tea maker market in North America.

Europe is projected to expand moderately anchored by replacement buying and sustainability narratives that emphasize longevity, repairability, and material transparency. The EU’s Right to Repair initiative, adopted in 2024, adds weight to consumer interest in service options and parts availability, which established brands can more readily support through existing service networks and documentation. Safety remains central: the latest IEC kettle standard shapes design and testing expectations, especially for glass impact resistance and handle integrity, helping buyers compare products on auditable criteria. These structural forces support durable growth across regional segments of the electric tea maker market.

Competitive Landscape

The electric tea maker market remains fragmented, with global brands competing alongside strong regional players and private-label offerings. Established manufacturers leverage multi-brand portfolios and compliance infrastructure to defend retail positions while expanding into premium and professional adjacencies. Groupe SEB’s portfolio and channel breadth illustrate this approach; the company reported first-half of 2024 Consumer business growth and highlighted momentum in select small-appliance categories, while maintaining investment in pro and premium segments. The company also executed targeted M&A to strengthen premium cookware and professional equipment capabilities, acquiring La Brigade de Buyer in January 2025 to complement its household brands with professional credibility. These moves help incumbents defend share against value-led entrants while expanding their relevance to commercial buyers that prize reliability, safety, and serviceability in the electric tea maker market.

Brand protection and channel integrity remain priority themes. Manufacturers invest in consumer education and verification tools to fight counterfeits and unsafe look alike models on marketplaces; a tactic reflected in company-owned anti-counterfeit portals that teach buyers to spot illicit listings and steer them to authorized channels. Standards alignment also serves as a competitive moat: the introduction of handle-strength and glass impact testing in IEC 60335-2-15 raises the quality floor. It can disqualify suppliers that cannot demonstrate compliance, thereby reinforcing the advantage of brands with accredited test data and robust technical files. In North America, alignment with UL 60335-1, 7th Edition, further clarifies expectations for product safety evidence, enabling quicker approvals for connected models and variable-temperature kettles that share safety architectures across regions. This interplay between compliance and brand equity shapes go-to-market strategies and margin realization in the electric tea maker market.

Adjacent-category innovation by large appliance makers enhances consumer comfort with app-controlled devices, thereby indirectly boosting awareness and adoption of connected kettles. At EuroCucina 2026, leading brands showcased AI-enabled appliances that embed learning logic and unified control environments, reinforcing consumer familiarity with digital interfaces and cross-device ecosystems. While these showcases are not kettle-specific, they prime the market for smart features and explainability in small appliances, which premium kettle lines can translate into simple, reliable presets rather than complex dashboards. With compliance, channel integrity, and user trust defining the playing field, established companies with integrated portfolios, service networks, and documented adherence to standards are positioned to capture incremental value in the electric tea maker market.

Electric Tea Maker Industry Leaders

-

Groupe SEB

-

Philips

-

Breville Group

-

Hamilton Beach Brands

-

De'Longhi

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: LG Electronics unveiled an integrated built-in kitchen suite with connected features at EuroCucina 2026, underscoring the mainstreaming of smart control in home appliances that can influence small-appliance adoption trajectories.

- April 2026: Samsung introduced new Bespoke AI appliances with adaptive performance features, reinforcing consumer familiarity with connected control experiences across the kitchen ecosystem.

- April 2026: United Kingdom OPSS flagged a foldable travel electric kettle for serious fire risk owing to a suspected counterfeit fuse link and a non-compliant mains plug that failed dimensional requirements.

- December 2025: UL published UL 60335 1, 7th Edition, an adoption aligned with the IEC 60335 1 framework with U.S. national differences, setting a North American safety baseline for household appliances.

Global Electric Tea Maker Market Report Scope

| Stainless Steel |

| Plastic (incl. BPA-free) |

| Glass (borosilicate) |

| Ceramic/Other |

| <1.0 Liter |

| 1.0–1.5 Liters |

| >1.5 Liters |

| Residential |

| Commercial |

| B2C/Retail Channels | Multi-brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B/Direct Sales/Project |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia‑Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia‑Pacific | |

| Middle East And Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Material | Stainless Steel | |

| Plastic (incl. BPA-free) | ||

| Glass (borosilicate) | ||

| Ceramic/Other | ||

| By Capacity | <1.0 Liter | |

| 1.0–1.5 Liters | ||

| >1.5 Liters | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail Channels | Multi-brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Direct Sales/Project | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia‑Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia‑Pacific | ||

| Middle East And Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the current size and outlook for the electric tea maker market?

The electric tea maker market size is USD 1.47 billion in 2025, rising to USD 1.56 billion in 2026 and USD 2.12 billion by 2031, at a 6.32% CAGR over 2026–2031.

Which region leads demand for electric tea makers today?

Asia-Pacific leads with 41.94% of 2025 revenue and is projected to grow at 6.98% fastest through 2031, supported by large tea-drinking populations and broader adoption of variable-temperature features.

Which buyer segment is growing fastest in electric tea makers?

Commercial buyers are the fastest-growing end user with a 6.84% CAGR to 2031, as cafés, tea bars, hotels, and office pantries standardize brew protocols by tea type.

Which materials and capacities are most preferred?

Stainless steel leads by value, while plastic grows fastest on cost appeal; mid-size 1.0–1.5-liter models dominate sales, and >1.5-liter units grow faster, tied to commercial and multi-user needs.

What standards and regulations most influence kettle design and compliance?

IEC 60335-2-15:2024 establishes global safety and durability benchmarks, UL 60335-1, 7th Edition, anchors North American compliance, and the EU’s Right to Repair initiative supports longevity and serviceability expectations.

How are online channels shaping purchases of electric tea makers?

B2C retail dominates with online sub-channels growing faster; brands rely on authorized sellers and compliance documentation to build trust, given persistent counterfeit risks in small-parcel cross-border flows.

Page last updated on: