Egypt Processed Poultry Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

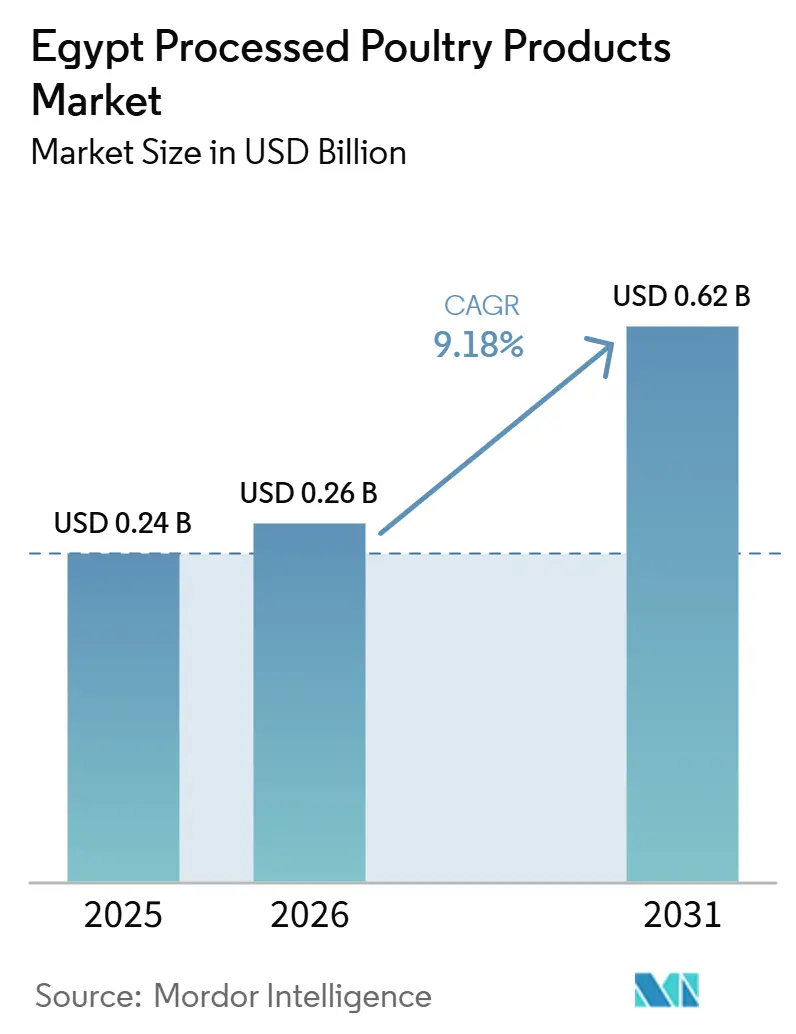

| Base Year Market Size (2025) | USD 0.24 Billion |

| Market Size (2026) | USD 0.26 Billion |

| Market Size (2031) | USD 0.62 Billion |

| Growth Rate (2026 - 2031) | 9.18% CAGR |

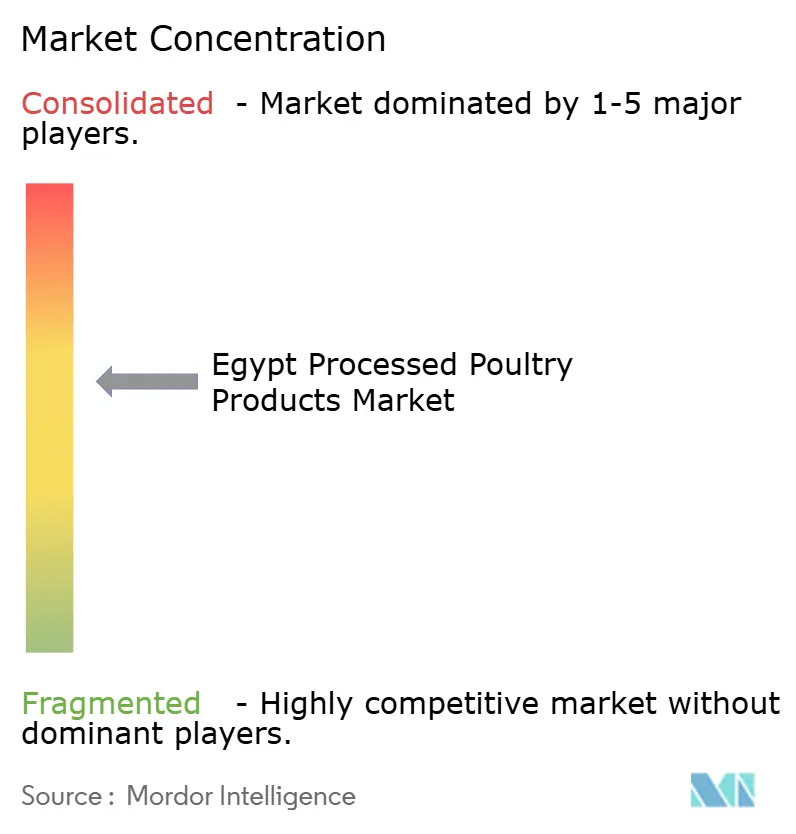

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Processed Poultry Products Market Analysis by Mordor Intelligence

The Egypt processed poultry products market size is projected to be USD 0.24 billion in 2025, USD 0.26 billion in 2026, and reach USD 0.62 billion by 2031, growing at a CAGR of 9.18% from 2026 to 2031. The Egypt processed poultry products market is benefiting from rising demand for convenient protein formats, especially in urban households where packaged and minimal-preparation food is gaining routine acceptance. The market is also supported by the formal foodservice base, which stands at USD 10.35 billion in 2026 and continues to pull certified, portion-standardized poultry products into quick service and institutional buying channels. Egypt’s food industry exports exceeded USD 6.80 billion in 2025, which shows the scale of local processing capability and supports confidence in domestic supply depth for the Egypt processed poultry products market. At the same time, imported feed dependence keeps processor economics tied to grain prices and currency conditions, since Egypt still relies on imports for 80.00% of corn needs and 95.00% of soybean needs. Even with that pressure, the Egypt processed poultry products market is moving toward more branded, chilled, frozen, and foodservice-oriented formats as retail standards, labeling requirements, and traceability practices strengthen the position of compliant processors.

Key Report Takeaways

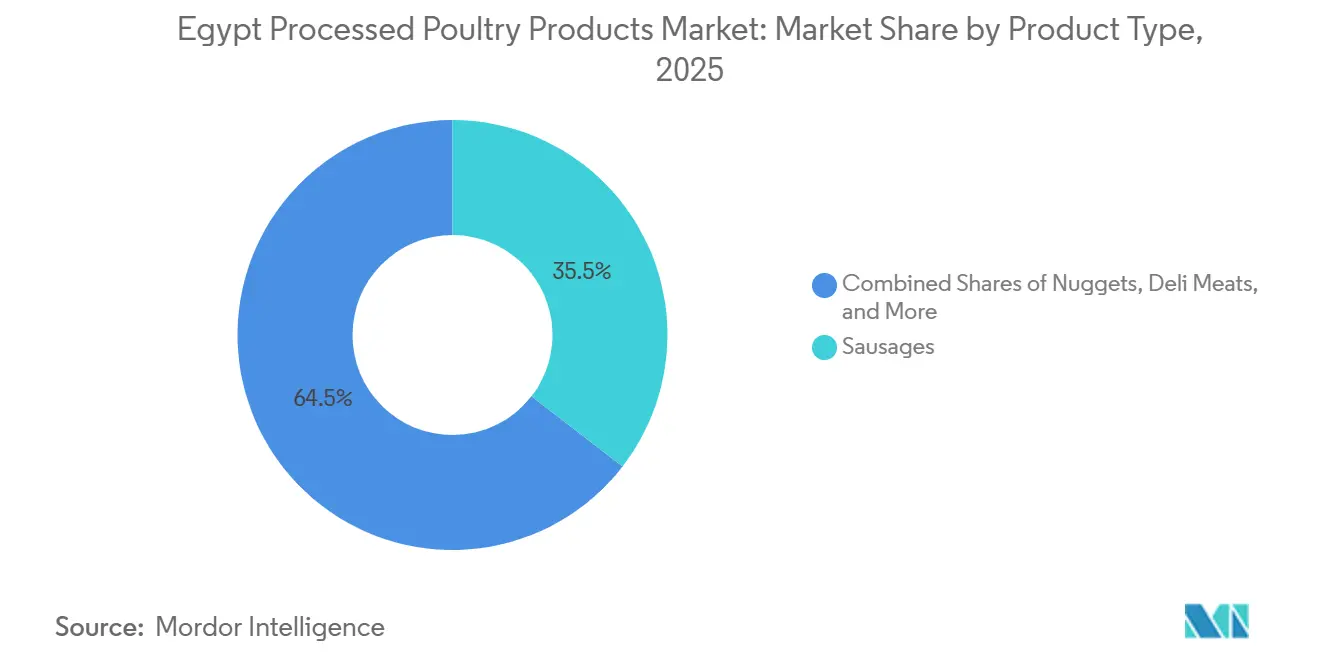

- By product type, sausages held 35.48% share in 2025, while tenders and marinated products are forecast to expand at a 10.78% CAGR through 2031.

- By form, fresh products accounted for 46.38% share in 2025, while frozen products are projected to grow at an 11.07% CAGR through 2031.

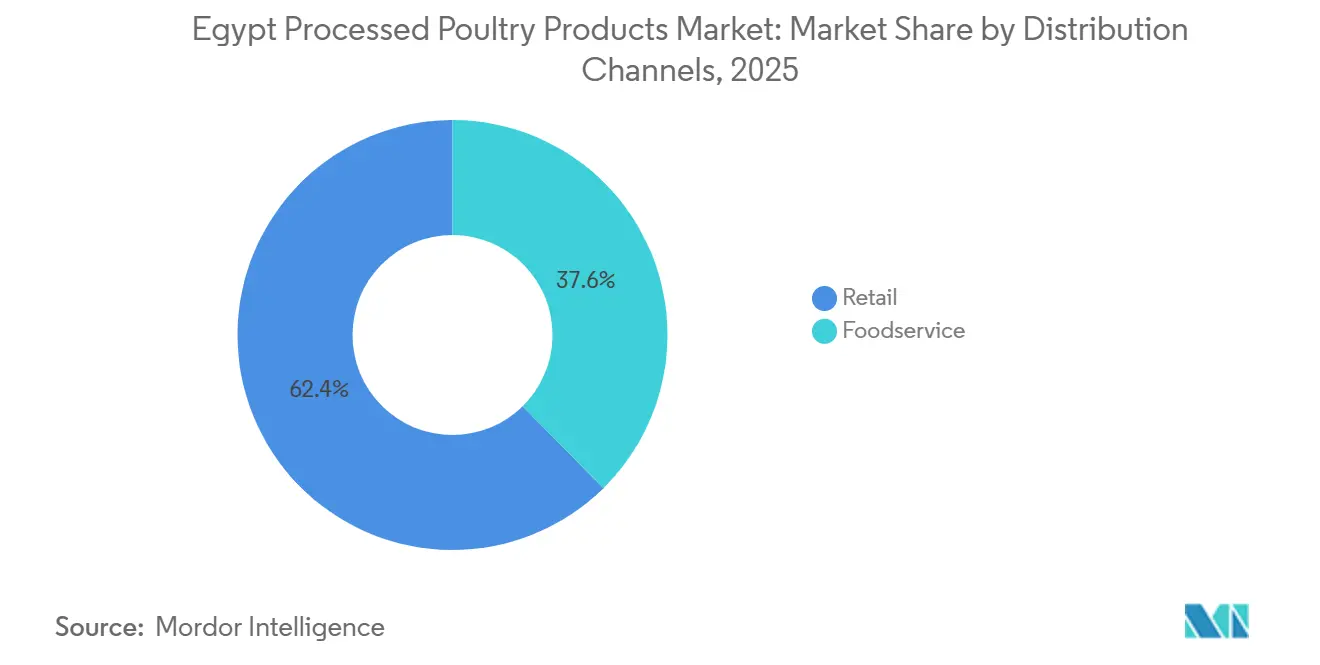

- By distribution channels, retail held 62.38% share in 2025, while foodservice is expected to advance at a 10.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Egypt Processed Poultry Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Convenient, Ready-To-Cook Protein | +2.7% | National, with highest concentration in Greater Cairo and Alexandria | Short term (≤ 2 years) |

| Expansion of Modern Retail and Foodservice Procurement | +1.9% | National, with early gains in Cairo, Alexandria, Red Sea corridor | Medium term (2–4 years) |

| Halal, Hygienic, Branded Protein Preference in Urban Egypt | +1.5% | Urban Egypt, spilling over to secondary cities | Medium term (2–4 years) |

| Import-Linked Price Pass-Through Supporting Local Processing | +1.0% | National | Short term (≤ 2 years) |

| Cold-Chain Expansion Enabling Value-Added Poultry Distribution | +1.3% | National, with early gains in Cairo–Upper Egypt corridor | Medium term (2–4 years) |

| High SKU Turnover from Pack Size and Recipe Innovation | +0.9% | National, urban-led | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Convenient, Ready-To-Cook Protein

The Egypt processed poultry products market is gaining from a consumer shift toward quick meal solutions that fit urban work schedules and shorter preparation windows. Egypt’s urbanization rate is above 43.00%, and that urban base is widening the addressable demand for packaged poultry items that can move from freezer or chiller to table in less than 15 minutes[1]Source: U.S. Department of Agriculture Foreign Agricultural Service, “Retail Foods Annual, Cairo, Egypt, EG2025-0010,” USDA GAIN Reports, apps.fas.usda.gov. Delivery-led grocery and meal ordering also supports this shift because platforms such as Talabat, Breadfast, and Rabbit make branded processed products easier to discover and reorder through digital shelves. This pattern strengthens demand for nuggets, strips, and marinated poultry, which fit both home meal preparation and fast casual consumption. It also gives suppliers a reason to widen pack sizes and recipe formats, because repeat buying improves when consumers treat these items as routine pantry or freezer staples. As a result, the Egypt processed poultry products market is moving closer to regular household use rather than occasional convenience-led purchasing.

Expansion of Modern Retail and Foodservice Procurement

The Egypt processed poultry products market is also being supported by the wider reach of modern grocery and formal procurement channels. In 2026, Egypt’s formal foodservice market stands at USD 10.35 billion, and that base is favoring pre-portioned and certified poultry formats that simplify kitchen operations and product consistency. Modern grocery growth has extended branded refrigerated and frozen shelf space beyond the largest cities, with Majid Al Futtaim continuing to add stores and low-cost Supeco locations in governorates that had more limited organized food retail coverage. This matters because processed poultry needs temperature-controlled merchandising, dependable restocking, and stronger consumer trust than informal fresh trade can offer. Formal buyers in quick service restaurants, hotels, hospitals, schools, and corporate catering are also more likely to insist on standardized cuts, battering, marination, and labeling. That procurement discipline is helping the Egypt processed poultry products market shift toward larger and more repeatable order volumes.

Halal, Hygienic, Branded Protein Preference in Urban Egypt

The Egypt processed poultry products market is seeing firmer demand for packaged products that present halal assurance, Arabic labeling, and visible product documentation. USDA’s 2025 FAIRS report states that packaged food sold in Egypt must meet labeling and documentation rules that include Arabic-language information and halal-related compliance requirements, which lifts the value of organized processing and formal distribution. In practice, this raises the relative appeal of branded processed poultry because shoppers can verify origin, handling, and product specifications more easily than in informal channels. The effect is strongest in Cairo and Alexandria, but it is also spreading into newer urban retail zones where organized grocery formats are expanding. Sausages benefit from this trend because they are easy to merchandise, familiar in household cooking, and easier to present in compliant packaged form. The same demand pattern supports the Egypt processed poultry products market by push.

Cold-Chain Expansion Enabling Value-Added Poultry Distribution

The Egypt processed poultry products market is gaining from the gradual extension of freezer and chiller infrastructure into secondary cities and new organized retail locations. Majid Al Futtaim’s continuing Egypt rollout, including new Supeco locations and Carrefour expansion in newer urban centers, is increasing the number of formal outlets that can handle branded processed poultry safely and consistently. This improves the practical reach of frozen nuggets, strips, and marinated products, which otherwise face narrower distribution windows than fresh products. It also reduces the sales penalty that processors face when launching differentiated SKUs outside Cairo and Alexandria. Better cold handling supports recipe innovation because products with batter, marinades, and shaped formats depend more heavily on stable storage conditions. Over time, the Egypt processed poultry products market should see more value shifting toward frozen and chilled ranges as infrastructure becomes less of a constraint.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feed and Live Bird Cost Volatility | −1.6% | National | Short term (≤ 2 years) |

| Food Safety Compliance and Labeling Burden | −0.7% | National | Medium term (2–4 years) |

| Consumer Price Sensitivity Versus Premium Processed Offerings | −1.3% | National, most pronounced in Lower and Upper Egypt | Short to medium term (1–3 years) |

| Informal Channel Competition and Weak Brand Loyalty in Value Segments | −1.0% | National, most pronounced in rural Egypt | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Feed and Live Bird Cost Volatility

The Egypt processed poultry products market remains exposed to feed cost swings because feed still accounts for 75.00% of poultry production costs, and Egypt depends on imports for 80.00% of corn and 95.00% of soybean requirements. This means processor margins can tighten quickly when grain markets or foreign currency conditions move against local buyers. Even after some easing, volatility remained visible because corn prices were down 29.20% in August 2024 from a year earlier, and feed prices fell from EGP 40,000 per ton to EGP 19,000-22,000 per ton by December 2025, which still shows how sharply costs can move within a short period[2]Source: U.S. Grains Council, “Egypt Market Profile,” U.S. Grains Council, grains.org. The problem for branded processors is that retail prices cannot always be raised at the same speed, especially in value-led categories. That pressure becomes more severe when live bird and informal fresh channels continue to offer lower visible prices to consumers. For the Egyptian processed poultry products market, this creates recurring pressure on pricing, investment timing, and promotional flexibility.

Consumer Price Sensitivity Versus Premium Processed Offerings

The Egypt processed poultry products market still faces a structural affordability challenge outside affluent urban catchments because processed products carry a visible premium over fresh or informal alternatives. This slows penetration in Lower Egypt, Upper Egypt, and price-sensitive urban districts where household food spending remains tightly managed. Informal outlets and live bird channels reinforce that pressure because they keep low-price comparisons in front of consumers every day. At the same time, compliance-related packaging, labeling, and cold-chain costs limit how far branded processors can reduce final shelf prices without damaging margins. The result is a market where premium formats can grow well in modern retail and foodservice, while mass adoption depends on more affordable pack sizes and sharper price architecture. That tension will continue to shape how the Egypt processed poultry products market balances premiumization with broader household reach.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sausages Lead, While Tenders and Marinated Products Add Faster Premium Growth

Sausages held 35.48% of Egypt's processed poultry products market share in 2025, which made them the largest product type in Egypt's processed poultry products market. Their position came from wide availability, easy use in Egyptian home cooking, and compatibility with both traditional grocery and quick service restaurant demand. They also travel well through fragmented retail because they are easier to stock and sell than more temperature-sensitive prepared items. Nuggets kept a stable role in the Egypt processed poultry products industry because they serve household buyers, school catering, and corporate meal programs with a familiar format. Tenders and marinated products are expected to grow at a 10.78% CAGR through 2031, and the Egypt processed poultry products market size for this segment is widening as restaurants and younger urban households look for more finished and flavor-led options.

That growth rate reflects more than simple convenience. Tenders and marinated products fit the needs of quick service operators that want portion consistency, lower preparation time, and predictable cooking results. They also match consumer interest in poultry items with stronger seasoning profiles and less preparation at home. Deli meats are building presence in premium grocery counters where chilled display quality and brand trust matter more than price alone. Meatballs remain smaller in value but continue to benefit from family meal use and the wider acceptance of frozen prepared foods. Across the product mix, the Egypt processed poultry products industry is steadily moving toward formats that can justify better pricing through convenience, flavoring, and tighter control of product quality.

By Form: Fresh Holds Current Scale, While Frozen Gains the Strongest Growth Momentum

Fresh processed poultry products accounted for 46.38% share in 2025, which kept them in the lead across form segments in the Egypt processed poultry products market. This position reflects a long-standing consumer preference for products that appear recently handled and are closely tied to routine household buying habits. Fresh products also fit the current store base because many smaller outlets still operate with limited cold storage depth. Chilled products serve an intermediate role by offering convenience with a shorter freshness cue than frozen alternatives. Frozen products are forecast to grow at an 11.07% CAGR through 2031, and the Egypt processed poultry products market size for frozen lines is rising as formal retail and controlled foodservice distribution broaden their reach.

Frozen growth matters because it opens the door to more differentiated product design. Nuggets, strips, panés, and marinated portions are easier to ship and store across longer distances when freezer conditions are stable. That allows suppliers to widen product range without taking the same spoilage or handling risk seen in fresh formats. Canned products remain the smallest form segment, serving narrower use cases where ambient shelf life matters more than texture or premium presentation. As the Egypt processed poultry products market expands beyond the largest urban centers, frozen and chilled products are likely to capture a bigger share of value because they support branded scale more effectively than fresh-only distribution.

By Distribution Channels: Retail Keeps the Lead, While Foodservice Advances Through Standardized Procurement

Retail retained a 62.38% share in 2025, which made it the dominant route to market in the Egypt poultry processed products market. Supermarkets and hypermarkets are especially important because they provide the cold-chain environment and shopper confidence that processed poultry needs. Even though traditional small grocers still account for more than 50.00% of packaged food sales by value nationally and more than 74.00% of food retail outlets, branded processed poultry remains more dependent on organized stores than many other packaged categories. Online grocery is becoming a relevant extension of retail because it gives brands a digital shelf and allows quick repeat purchasing of frozen and chilled stock-up items. This means the Egypt processed poultry products market still anchors volume in retail, while store quality and refrigeration capability determine which subcategories scale fastest.

Foodservice is projected to grow at a 10.66% CAGR through 2031, and the Egypt processed poultry products market size linked to this channel is improving as quick service chains and institutional buyers prefer standardized inputs. In 2026, Egypt’s formal foodservice market stands at USD 10.35 billion, which gives processors a large and structured demand base for portioned, marinated, and pre-battered poultry products. Hotels, hospitals, schools, and corporate catering buyers also prefer products that reduce kitchen labor and deliver uniform serving sizes. This creates a channel where compliance, reliability, and product specification matter more than in fragmented informal trade. The Egypt poultry processed products market is therefore seeing a clear division, with retail carrying the largest current volume and foodservice shaping a faster-growing value stream.

Geography Analysis

Greater Cairo and Alexandria account for the core demand base of the Egypt processed poultry products market because they combine the country’s largest urban populations with the deepest organized retail and cold distribution footprint. These two urban zones also sit close to major industrial locations such as 10th of Ramadan City and Obour City, which reduces transport complexity for chilled and frozen products. That operating advantage matters because processed poultry depends on consistent handling and timely replenishment more than informal fresh trade. The same geography also benefits from stronger consumer exposure to branded packaged food and more regular use of delivery platforms. For the Egypt processed poultry products market, this keeps Cairo and Alexandria at the center of both demand creation and product launch activity.

The Red Sea corridor and newer organized retail pockets form the next important layer of regional growth for the Egypt processed poultry products market. Tourism-linked foodservice in Hurghada, Sharm El Sheikh, and other coastal locations supports demand for standardized and compliant poultry products that fit hotel and resort procurement needs. Organized grocery expansion into places such as Fayoum and New Alamein is also extending the practical reach of chilled and frozen assortments. These areas do not yet match Cairo in scale, but they are becoming more relevant for branded processed poultry distribution.

Upper Egypt and rural governorates remain less penetrated in the Egypt processed poultry products market because live bird buying and informal butcher trade still hold a stronger position there. Price sensitivity is higher in these areas, which makes branded processed formats more vulnerable to comparison with lower-cost fresh alternatives. Cold storage and formal merchandising are also less dense, which narrows the feasible product mix for suppliers. Even so, the national processing base is strengthening, and Egypt’s food industry export performance points to a wider manufacturing platform that can support deeper domestic distribution over time[3]Source: Food Export Council Egypt, “Egyptian Food Industries Achieve a New Historic Milestone with Exports Exceeding USD 6.8 Billion in 2025,” FEC Egypt, feceg.com. As store quality, logistics, and household familiarity improve, the geography of the Egypt processed poultry products market is likely to broaden beyond its current urban core.

Competitive Landscape

The Egypt processed poultry products market is moderately concentrated, with domestic integrators, large import suppliers, and regional branded players each occupying a distinct position. Cairo Poultry Company leads through vertical integration, which gives it stronger control over feed, live production, processing, and route-to-market economics. The company reported FY2025 revenue of USD 316.00 million and net profit of USD 58.00 million, which showed the financial benefit of that integrated model in a volatile input environment. That performance strengthens Cairo Poultry Company’s ability to defend shelf presence and supply larger foodservice accounts. The Egypt processed poultry products market therefore remains difficult for smaller players that do not have similar control over sourcing, scale, and compliance.

Imported supply is also important in the Egypt processed poultry products market, especially for frozen and chilled formats where Brazil remains dominant. BRF S.A. and JBS S.A. account for 97.00%-98.00% of Egypt’s poultry imports by value, which shows how concentrated the import side of supply is even if domestic competition is broader. BRF reported record net revenue in 2025 and stated that it had accumulated 230 new export certifications since 2022, which supports its ability to keep serving halal-sensitive and scale-oriented regional markets. That external scale matters because importers can respond quickly when local category demand expands faster than domestic value-added capacity. The Egypt processed poultry products market thus combines local manufacturing strength with a meaningful import-backed supply layer.

Regional brand operators such as Americana Foods and Halwani Bros compete in the premium modern retail tier, where brand recognition and distribution depth still matter. Their role is strongest in categories where packaging, quality consistency, and cross-border brand familiarity influence consumer choice more directly than raw price. Competition is also shifting toward better product design, more reliable cold handling, and stronger traceability execution rather than simple volume expansion. Suppliers that can support quick service restaurant specifications, hold stable freezer availability, and manage labeling compliance are better placed to capture the faster-growing parts of demand. Overall, the Egypt processed poultry products market remains open enough for selective niche expansion, but it still favors companies with integrated supply, broad retail access, or strong import pipelines.

Egypt Processed Poultry Products Industry Leaders

Cairo Poultry Company

Halwani Bros Egypt

JBS S.A.

BRF S.A.

Golden Beef Food Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Egypt's poultry producers raised concerns over the increasing influx of low-priced frozen chicken imports, warning that the surge is placing significant pressure on domestic producers and threatening the sustainability of local poultry farming.

- May 2025: Mansourah Poultry Company (MPCO) announced the acquisition of a new poultry farm in Egypt's Nubaria region for EGP 31.4 million (approximately US$0.63 million) and plans to invest an additional EGP 100 million (approximately US$2 million) to expand the facility.

- January 2024: 3A Poultry, one of Egypt's leading poultry producers, announced plans to invest EGP 1 billion to expand its poultry production capacity. The investment is aimed at increasing domestic chicken production, strengthening food security, and supporting Egypt's efforts to reduce reliance on poultry imports while meeting the country's growing demand for poultry products.

Egypt Processed Poultry Products Market Report Scope

| Nuggets |

| Deli Meats |

| Sausages |

| Tenders/Marinated |

| Meatballs |

| Others |

| Fresh |

| Chilled |

| Frozen |

| Canned |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Channels | |

| Other Distribution Channels | |

| Foodservice |

| Product Type | Nuggets | |

| Deli Meats | ||

| Sausages | ||

| Tenders/Marinated | ||

| Meatballs | ||

| Others | ||

| Form | Fresh | |

| Chilled | ||

| Frozen | ||

| Canned | ||

| Distribution Channels | Retail | Supermarkets/Hypermarkets |

| Convenience Stores | ||

| Online Retail Channels | ||

| Other Distribution Channels | ||

| Foodservice | ||

Key Questions Answered in the Report

What is the 2026 value of Egypt processed poultry products?

The Egypt processed poultry products market stands at USD 0.26 billion in 2026 and is forecast to reach USD 0.62 billion by 2031.

How fast is processed poultry demand expected to grow in Egypt?

The category is projected to grow at a 9.18% CAGR from 2026 to 2031, supported by convenience demand, formal foodservice, and broader organized retail reach.

Which product category leads sales in Egypt?

Sausages led with 35.48% share in 2025 because they are widely available, easy to use, and fit both household and quick service demand.

Which format is growing fastest across Egypt?

Frozen products are projected to grow at an 11.07% CAGR through 2031 as retail refrigeration and controlled distribution improve.

Page last updated on: