Egypt Global Capability Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

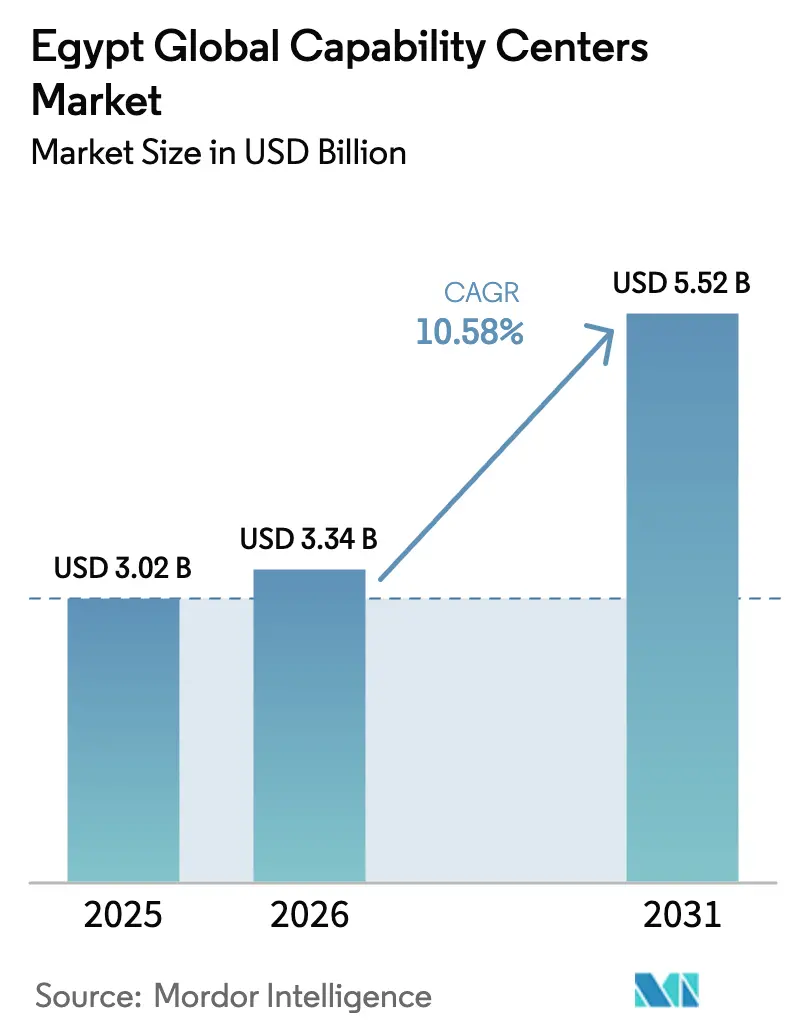

| Base Year Market Size (2025) | USD 3.02 Billion |

| Market Size (2026) | USD 3.34 Billion |

| Market Size (2031) | USD 5.52 Billion |

| Growth Rate (2026 - 2031) | 10.58% CAGR |

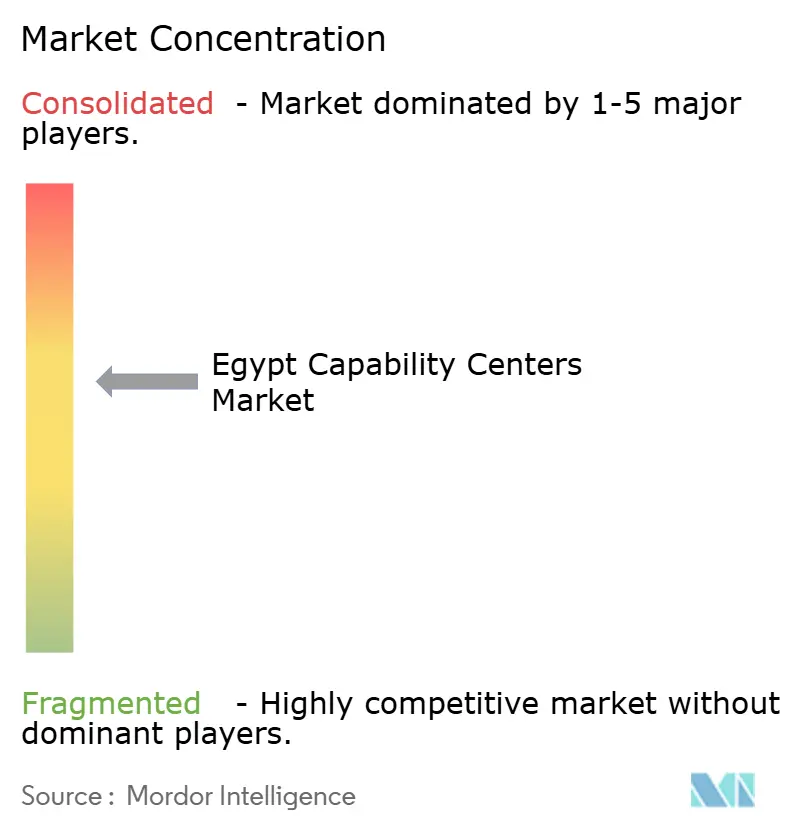

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Global Capability Centers Market Analysis by Mordor Intelligence

The Egypt Global Capability Centers Market size was valued at USD 3.02 billion in 2025 and estimated to grow from USD 3.34 billion in 2026 to reach USD 5.52 billion by 2031, at a CAGR of 10.58% during the forecast period (2026-2031). Favorable labor economics, an expanding STEM talent pool, and proximity to Europe and the Middle East support sustained inflows of nearshoring demand, while the Digital Egypt and National AI Strategy programs anchor long-term technology investment.[1]National Council for Artificial Intelligence, “Egypt National Artificial Intelligence Strategy: Second Edition (2025-2030),” ai.gov.eg Rising private infrastructure outlays in smart cities and data centers, together with streamlined “golden license” approvals, shorten launch timelines for new facilities. Multinational corporations are increasingly pairing cost savings with risk diversification following recent geopolitical supply chain shocks, making Egypt a preferred regional gateway for European and Gulf clients. Competition consequently shifts from price-led bidding toward specialized digital, analytics, and multilingual capabilities that elevate service quality and margin potential.

Key Report Takeaways

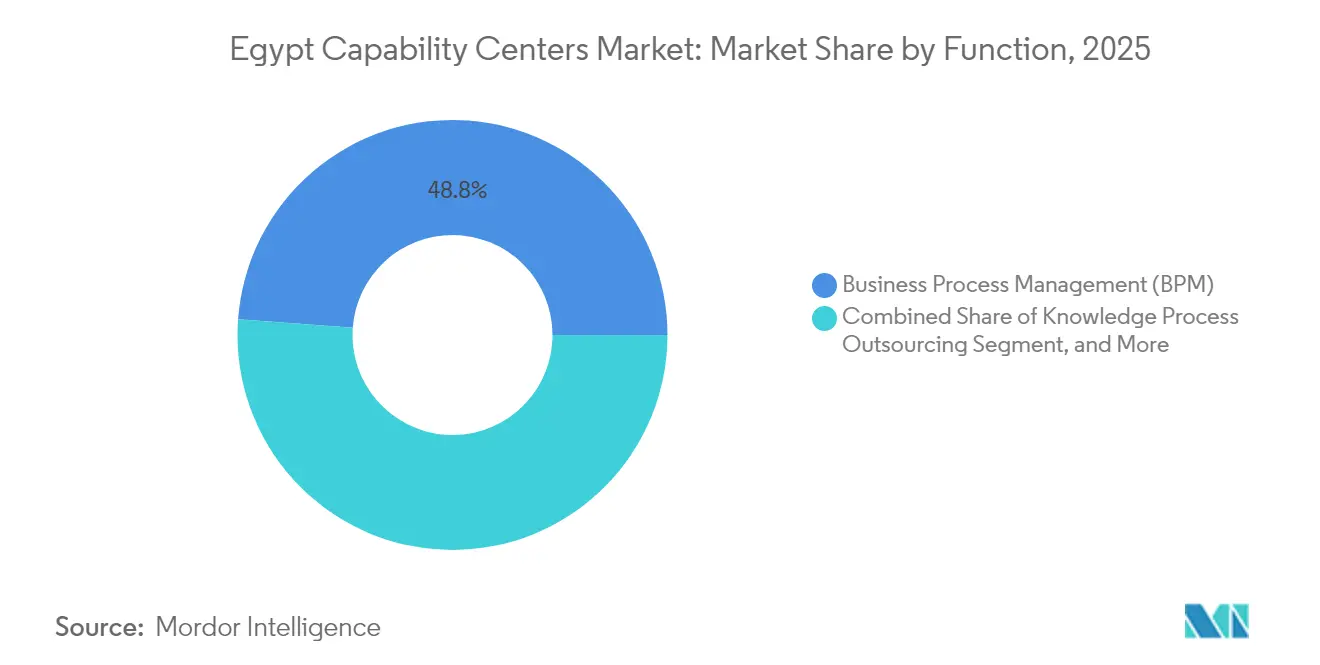

- By function, Business Process Management captured 48.83% of the Global Capability Centers market share in 2025, while Information Technology and Digital Services are set to record the fastest growth of 11.24% CAGR through 2031.

- By engagement model, captive centers held a 59.47% share of the Global Capability Centers market size in 2025; hybrid Build-Operate-Transfer structures are poised to expand at a 11.05% CAGR through 2031.

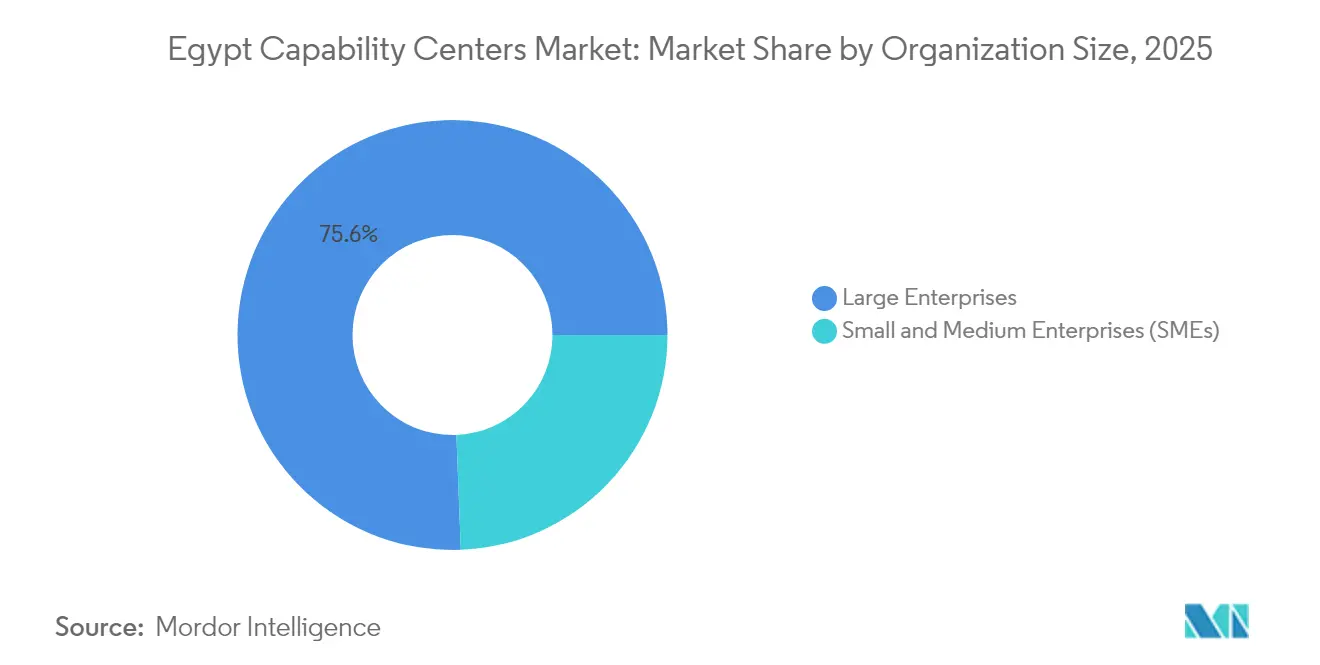

- By organization size, large enterprises controlled 75.62% of activity in 2025, whereas Small and Medium Enterprises will grow the quickest at 11.79% CAGR during the forecast period.

- By industry vertical, telecom and IT led with a 34.21% revenue share in 2025, and banking, financial services, and insurance are projected to advance at a 10.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Global Capability Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing STEM graduate pool | +2.1% | National, focused on Cairo, Alexandria, Giza | Medium term (2-4 years) |

| Competitive labor costs versus CEE and Asia Pacific | +1.8% | Global clients, core benefits for the EU and North America | Short term (≤ 2 years) |

| Fast-track government permitting for tech parks | +1.4% | National, early gains in the New Administrative Capital, Smart Villages | Short term (≤ 2 years) |

| Rapid digitization of Africa and Middle East enterprises | +1.9% | MENA and Africa, spill-over to global operations | Medium term (2-4 years) |

| Egypt-Saudi digital corridor | +1.2% | Regional MENA, extending to GCC markets | Long term (≥ 4 years) |

| EU nearshoring demand post-Ukraine conflict | +2.3% | European Union and associated markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing STEM Graduate Pool

Egypt produces approximately 50,000 IT-related graduates annually, creating a deep pool of talent for software development, data analytics, and multilingual service desks.[2]Keri Allan, “How Egypt is building a generation of IT pros to close the skills gap,” CIO, cio.com Enrollment under the Digital Egypt Builders Initiative surpassed 104,000 students in computer science and AI tracks in 2024, and new institutions such as the Egypt University of Informatics partner with Purdue University to raise curriculum standards. Government spending of USD 208 million on AI-ready campuses accelerates the adoption of robotics labs and cybersecurity sandboxes. Capability centers translate this pipeline into lower recruitment lead times and higher talent retention, improving delivery continuity for European and Gulf clients. The larger graduate base also lets providers rotate staff through blended BPM-digital roles, supporting higher-value offerings without losing volume contracts.

Competitive Labor Costs Versus CEE and Asia Pacific

Average fully loaded salary levels in Cairo remain below 20% of those in Central and Eastern Europe and approximately 35% of key Indian tier-one cities, even after accounting for wage inflation and currency liberalization. The Egyptian pound’s March 2024 float widened savings for foreign currency buyers, helping service providers quote multiyear deals in USD at predictable margins. Kearney’s 2023 Global Services Location Index ranked Egypt first in the Middle East and North Africa for cost attractiveness and people skills, reinforcing its position in vendor selection shortlists. Lower operating expenditure frees up capital for cloud migration, process automation, and cybersecurity upgrades, creating a virtuous cycle of quality improvement that secures clients for longer contract durations. As clients weigh nearshoring options, Egypt’s blended wage and skills proposition remains a decisive differentiator against Morocco, Poland, and the Philippines.

Rapid Digitization of Africa and Middle East Enterprises

Banks, retailers, and public agencies across Africa and the Middle East are stepping up their digital transformation investments to meet the growing demand for mobile-first services, creating opportunities for Egyptian centers to deliver support in Arabic, English, and French. Regional organizations use Egypt’s time zone overlap and cultural affinity to centralize helpdesks, cloud operations, and analytics. Cross-border data traffic over Egypt-hosted submarine cables grew at a double-digit clip in 2024, underscoring its role as an intercontinental switching node. Egyptian vendors earn recurring revenue by bundling application modernization with managed security and data residency compliance. Rising intra-African trade under the AfCFTA further lifts demand for logistics, treasury, and supply chain control tower services that leverage Egypt-based multilingual talent.

EU Nearshoring Demand Post-Ukraine Conflict

European multinationals are diversifying their delivery footprints away from Eastern Europe due to security, energy, and talent constraints prompted by the conflict in Ukraine. The June 2024 EU-Egypt Investment Conference unlocked EUR 40 billion in pledged private investment projects, many of which are earmarked for digital and business services. Dutch think tank Clingendael lists Egypt among the top three destinations for Dutch ICT nearshoring, citing four-hour flight times and salary arbitrage.[3]Monika Sie Dhian Ho, “Connecting Shores: Assessing Egypt’s ICT nearshoring potential,” Clingendael, clingendael.org European corporations value Egypt’s alignment with the General Data Protection Regulation under the Personal Data Protection Law, easing data transfer approvals. Near-term demand centers on finance operations, procurement, and compliance analytics, but pipeline forecasts indicate higher-value product engineering mandates once data residency and language needs are met through expanded language academies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency volatility and inflationary pressure | -1.7% | National, spillover to regional operations | Short term (≤ 2 years) |

| Persistent power supply disruptions | -1.3% | National, concentrated in industrial zones | Medium term (2-4 years) |

| Shortage of senior project managers | -0.9% | National, acute in Cairo and Alexandria | Medium term (2-4 years) |

| Rising competition from Morocco and Kenya | -1.1% | Regional Africa and MENA, global implications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Currency Volatility and Inflationary Pressure

Inflation eased from a 38% peak in 2023 to 26% by mid-2024 but remains above the Central Bank’s target band, complicating annual budget planning for international operators.[4]Central Bank of Egypt, “Monthly Inflation Bulletin July 2024,” cbe.org.eg Although foreign exchange reserves reached USD 46 billion by July 2024, following Gulf support and an enlarged IMF facility, periodic pound swings compel vendors to reprice contracts or absorb margin hits. Forward-hedging instruments exist, but they add complexity for small and medium providers. Multinationals partly offset risk by invoicing in hard currency and early paying local vendors to avoid price escalations; yet, sustained two-digit inflation still compresses domestic consumption, which underpins the local supplier ecosystem.

Persistent Power Supply Disruptions

Grid congestion and peak-summer load shedding continue to affect Cairo’s industrial zones, prompting operators to maintain diesel generators or lithium-ion battery farms, which in turn raises the operating cost per workstation. Government utility reforms and megaprojects such as the Benban solar park and green hydrogen ventures promise incremental capacity, but full resilience remains a medium-term deliverable. Capability centers, therefore, invest in Tier III-plus data center colocation and dual-feed fiber paths to meet global uptime service-level agreements. Energy efficiency initiatives such as chilled-water cooling and LED retrofits marginally decrease power draw but cannot yet compensate for extended outage windows during heatwaves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function / Capability: BPM Leadership Faces Digital Services Challenge

Business Process Management (BPM) generated the largest contribution to Egypt’s Global Capability Centers market size in 2025, capturing 48.83% of revenue. This was achieved by leveraging multilingual call center talent and near-Europe time zones to service customer care, finance, and HR processes. Providers enhance value by embedding robotic process automation into high-volume workflows, freeing agents to focus on complex interactions and creating cross-sell opportunities through analytics. The segment’s entrenched scale offers reliable cash flows that fund innovation labs and career progression ladders needed to retain mid-level supervisors. However, digital ambidexterity becomes critical as clients pivot from cost arbitrage toward end-to-end transformation, positioning Egyptian centers for blended deals that mix BPM with cloud and security.

Information Technology and Digital Services is projected to post the highest 11.24% CAGR through 2031, as the National AI Strategy targets a 30,000-strong AI workforce and 250-plus AI firms by the end of the decade. Early adopters focus on DevOps, application modernization, and low-code development that exploit proximity to European agile sprints. The rising share of digital work raises average billing rates, thereby lifting overall Global Capability Centers market growth in Egypt, even as seat volumes stabilize. Knowledge Process Outsourcing and Engineering services gain moderate traction as universities integrate design thinking modules and multinational industrial players establish R&D satellites in Alexandria. The combined momentum suggests a gradual shift from pure contact centers to higher-value intellectual property creation within Egypt.

By Engagement Model: Captive Dominance Challenged by Hybrid Innovation

Captive entities controlled 59.47% of Egypt’s Global Capability Centers market share in 2025, reflecting board-level emphasis on data security, compliance, and cultural alignment. Technology majors such as Microsoft, IBM, and Dell use Egypt to run multilingual helpdesks, finance shared services, and AI annotation labs, enabling tight integration with global product roadmaps. These captives benefit from ITIDA cash rebates, custom talent programs, and free-zone tax holidays that compress payback periods below three years.

The hybrid Build-Operate-Transfer model emerges as the fastest-growing option, with an 11.05% CAGR, offering phased risk transfer. Early months leverage a local vendor’s hiring and regulatory expertise, while staged equity flips full control to the client once critical mass is validated. The model resonates with high-growth European scale-ups that lack in-house offshore experience but are wary of vendor lock-in. Traditional BOT structures remain relevant for cost-sensitive corporations preferring third-party management in the long term. Together, these models diversify entry pathways, supporting a broader client mix and fueling the total expansion of the Global Capability Centers market in Egypt.

By Organization Size: Enterprise Dominance with SME Acceleration

Large enterprises generated 75.62% of 2025 revenue, securing favorable lease terms in Smart Villages and the New Administrative Capital, and locking in multi-year government incentive packages. Their global process maturity enables them to allocate entire value streams, from Level 1 service desks to Level 3 engineering, allowing for rapid staff ramp-ups of thousands. Cross-functional setups also elevate employee career trajectories, increasing retention and local knowledge transfer.

Small and medium-sized enterprises (SMEs) are expected to register a 11.79% forecast CAGR as cloud-native toolchains and remote-first processes lower entry thresholds. European SMEs turn to Egypt for bilingual support at a fraction of the Central European wage bill and appreciate the simplified one-day corporate registration process on GAFI’s digital portal. The Digital Egypt platform offers subsidized cybersecurity audits and micro-grants for automation pilots, slashing pilot costs. Tech-enabled SMEs often start with a forty-seat helpdesk but scale to 150-plus engineers within two years, adding incremental depth to the overall Global Capability Centers market in Egypt.

By Industry Vertical: Telecom Leadership Challenged by Financial Services Growth

Telecom and IT accounted for 34.21% of 2025 revenue, underpinned by Egypt’s role as a transcontinental cable choke point and by operator investments in regional network operation centers. Vodafone Intelligent Solutions, Orange Business, and Etisalat utilize ultra-low latency interconnection to monitor links across the Mediterranean, Red Sea, and Indian Ocean. The vertical also champions early 5G-enabled edge use cases that feed DevOps sandboxes for network slicing and IoT platforms.

The banking, financial services, and insurance sector is projected to expand at an 10.86% CAGR as digital payments, open banking, and regulatory technology workloads accelerate. HSBC’s Cairo hub now complements risk analytics with AI-based customer onboarding for the Middle East. The Central Bank’s fintech sandbox and data classification mandates are stimulating demand for compliance-grade hosting and Arabic-language natural language processing. The healthcare and life sciences sectors continue to grow steadily, driven by the need for vaccine cold-chain data monitoring. Meanwhile, industrial majors are incorporating digital twin modeling and maintenance analytics into Egypt-based centers, thereby expanding the footprint of the Global Capability Centers industry.

Geography Analysis

Greater Cairo contributed a significant share of the activity in 2025, driven by dual-feeder fiber routes, three international airports, and proximity to policymakers who facilitate license amendments. Class A office supply in Smart Villages and Cairo Festival City lowers fit-out timelines, while downtown revitalization attracts fintech start-ups seeking talent buzz. The region is expected to experience a prominent growth through 2031, as metro expansions reduce commute times and green building standards enhance employee wellness.

Alexandria holds a nominal share of the Egypt Global Capability Centers Market, thanks to Mediterranean port access and an engineering legacy tied to petrochemicals and logistics. Multinationals locate inventory optimization, procurement support, and French-speaking service lines here, leveraging Alexandria University’s francophone programs. Telecom Egypt’s new subsea cable landing stations enhance redundancy, helping the city target high-availability workloads.

The New Administrative Capital achieves a significant CAGR due to its purpose-built smart infrastructure, solar-powered campuses, and one-stop investor centers, which are capable of issuing a golden license within thirty days. Fiber, district cooling, and integrated security solutions reduce opex, while state-backed free-zone status cancels VAT on exported services. Beyond these hubs, Upper Egypt cities such as Assiut and Luxor court Arabic language content creation, supported by government wage subsidies. The Suez Canal Economic Zone offers bonded logistics analytics, although Red Sea security considerations necessitate risk mitigation. Coastal holiday towns of Hurghada and Sharm El-Sheikh experiment with hospitality helpdesks, whereas industrial corridors such as the 6th of October and 10th of Ramadan attract automotive and consumer goods data engineering teams. Collectively, regional diversity enhances Egypt’s value proposition, reinforcing the overall resilience of the Global Capability Centers market in Egypt.

Competitive Landscape

The provider universe remains moderately fragmented, with the top five players accounting for a prominent share of revenue. Captives dominate customer experience and enterprise IT, while global BPO leaders and Egyptian scale-ups compete on multilingual analytics and AI operations. Firms differentiate themselves through vertical depth, language academies, and compliance certifications such as PCI-DSS and ISO 27001, which reassure financial and healthcare clients.

Technology adoption is the new battleground. Deloitte will invest USD 30 million in an AI innovation hub, aiming to increase headcount from 350 to 5,000 by 2027, and plans to integrate process mining with generative AI accelerators. Capgemini’s Cairo center of excellence aims to double its staff to 1,200 by the end of 2025, with a focus on cloud modernization and synthetic data. Egyptian players, such as Raya CX and Xceed, leverage cultural affinity and competitive salaries to pitch agile squads to Gulf e-commerce and fintech start-ups.

White-space opportunities exist in renewable energy project management, ESG reporting, and Arabic speech recognition. Early movers partner with local universities to develop corpora and specialized curricula. Government support through the National AI Strategy and a forthcoming quantum computing lab promises fresh service lines that can command premium rates. Overall, competitive intensity encourages continuous upskilling, enabling the Global Capability Centers market in Egypt to sustain double-digit growth while mitigating price pressure.

Egypt Global Capability Centers Industry Leaders

Orange Business

Valeo Service Center

IBM Egypt

Amazon Development Center Egypt

Microsoft Egypt Development Center

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Egypt unveiled the National Artificial Intelligence Strategy 2025-2030, aiming to establish 250 AI companies and 30,000 professionals by 2030, with AI projected to contribute USD 42.7 billion to the GDP.

- December 2024: The OECD published a governance review praising 168 digital public services delivered under the Digital Egypt program, citing improvements in the ease of doing business.

- October 2024: Foundever announced an EUR 65 million contract center expansion, which will add 5,000 jobs over the next four years.

- September 2024: Acwa Power pledged USD 15 billion over six years for green hydrogen, with Phase 1 exceeding USD 4 billion and targeting 600,000 tonnes of annual green ammonia by 2028.

Egypt Global Capability Centers Market Report Scope

The scope of the global capability center study for the market segmentation by the Function/Capability for (i) Information Technology (IT) and Digital Services segment is limited to Software Development, Cloud and Infrastructure Management, Cybersecurity, Data Analytics and AI/ML; (ii) Engineering / ER&D segment is limited to Product Design and Testing, Embedded Systems, Digital Twin / Simulation; (iii) Business Process Management (BPM) segment is limited to Finance and Accounting, HR, Payroll and Talent Management, Procurement, Customer Service; and (iv)Knowledge Process Outsourcing (KPO) segment is limited to Market Research and Insights, Risk and Compliance, Legal and Regulatory Support, Strategy and Consulting Support. Similarly, for segmentation by the Engagement Model, scope for (i) Hybrid Build-Operate-Transfer (BOT) is limited to Joint Venture / Strategic Partnership and Virtual Captive Model. The rest of the segment scope is as specified for the listed segment.

| Information Technology (IT) and Digital Services |

| Engineering / ER&D |

| Business Process Management (BPM) |

| Knowledge Process Outsourcing (KPO) |

| Captive (Self-Build) / In-house |

| Build-Operate-Transfer (BOT) |

| Hybrid Build-Operate-Transfer (BOT) (Joint Venture / Strategic Partnership and Virtual Captive Model) |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT |

| Healthcare and Life Sciences |

| Manufacturing, Automotive and Industrial |

| Retail and Consumer Goods |

| Other Industry Verticals |

| By Function / Capability | Information Technology (IT) and Digital Services |

| Engineering / ER&D | |

| Business Process Management (BPM) | |

| Knowledge Process Outsourcing (KPO) | |

| By Engagement Model | Captive (Self-Build) / In-house |

| Build-Operate-Transfer (BOT) | |

| Hybrid Build-Operate-Transfer (BOT) (Joint Venture / Strategic Partnership and Virtual Captive Model) | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By Industry Vertical | Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT | |

| Healthcare and Life Sciences | |

| Manufacturing, Automotive and Industrial | |

| Retail and Consumer Goods | |

| Other Industry Verticals |

Key Questions Answered in the Report

What is the current value of Egypt’s Global Capability Centers market?

The Global Capability Centers market size in Egypt is expected to reach USD 3.34 billion by 2026.

How fast is Egypt’s capability center sector growing?

The market is forecast to expand at a 10.58% CAGR through 2031.

Which functional segment is growing the quickest?

Information Technology and Digital Services are projected to lead growth with an 11.24% CAGR to 2031.

Why do European firms prefer Egypt for nearshoring?

Egypt combines four-hour flight times, competitive salaries, GDPR-aligned data laws, and multilingual talent, reducing operational risk for European clients.

What government programs support the sector?

Digital Egypt and the National AI Strategy provide incentives, skills training, and streamlined golden licenses for technology investors.

Which industry vertical is expected to accelerate the most by 2031?

The banking, financial services, and insurance sector is projected to achieve an 10.86% CAGR, driven by fintech and compliance workloads.

Page last updated on: