Egypt Dietary Supplements Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

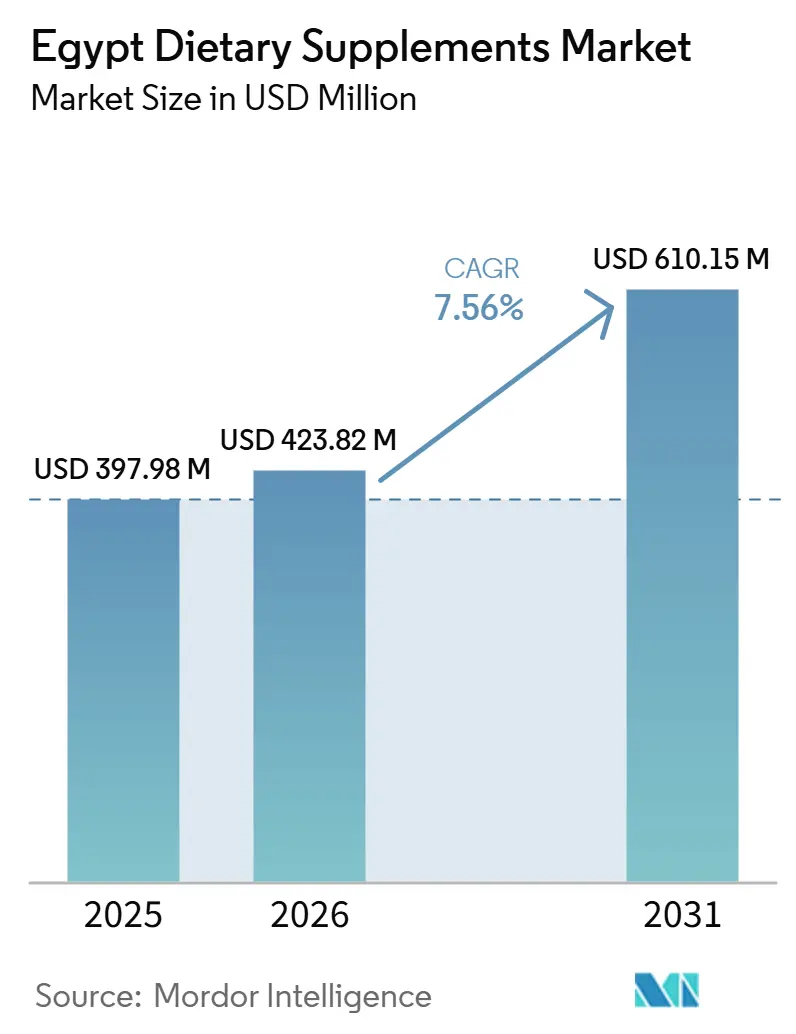

| Base Year Market Size (2025) | USD 397.98 Million |

| Market Size (2026) | USD 423.82 Million |

| Market Size (2031) | USD 610.15 Million |

| Growth Rate (2026 - 2031) | 7.56% CAGR |

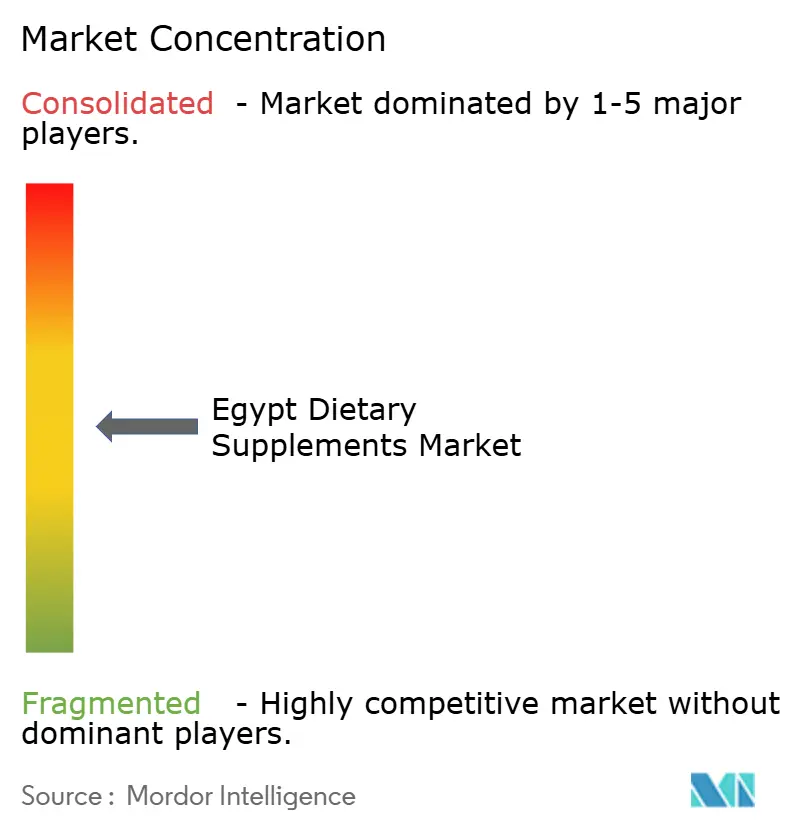

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Egypt Dietary Supplements Market Analysis by Mordor Intelligence

The Egypt dietary supplements market was valued at USD 397.98 million in 2025, is projected to reach USD 423.82 million in 2026, and is estimated to reach USD 610.15 million by 2031, growing at a CAGR of 7.56% during 2026–2031. The market is driven by a growing shift toward preventive healthcare and daily nutritional supplementation, increasing awareness of balanced nutrition in supporting overall wellness, and rising adoption of scientifically formulated products for long-term health maintenance. Continuous innovation in supplement formulations, including clean-label, plant-based, personalized, and multifunctional products, is expanding consumer appeal and encouraging repeat consumption. Advances in ingredient technologies, improved bioavailability, convenient dosage formats, and premium nutritional solutions are further enhancing product value.

Key Report Takeaways

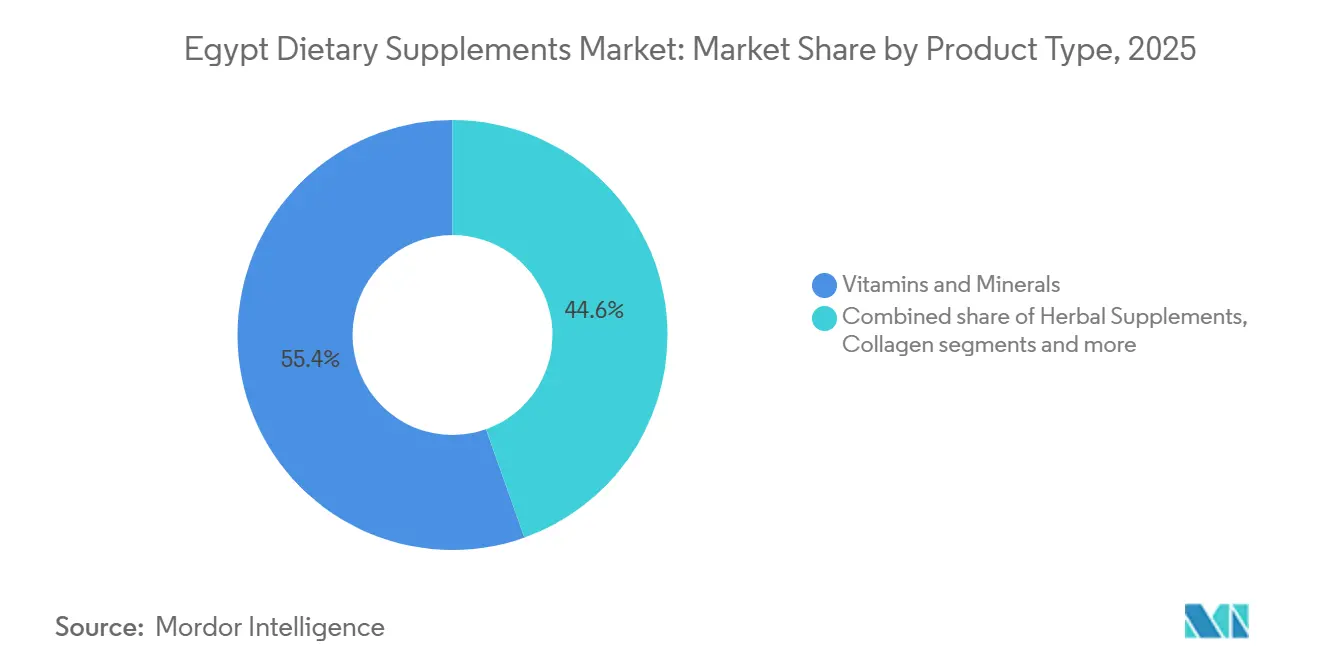

- By product type, vitamins and minerals held a 55.43% revenue share of the Egypt dietary supplements market in 2025; herbal supplements are forecast to expand at an 8.41% CAGR through 2031.

- By form, capsules accounted for a 35.45% revenue share in 2025; gummies are expected to advance at an 8.31% CAGR through 2031.

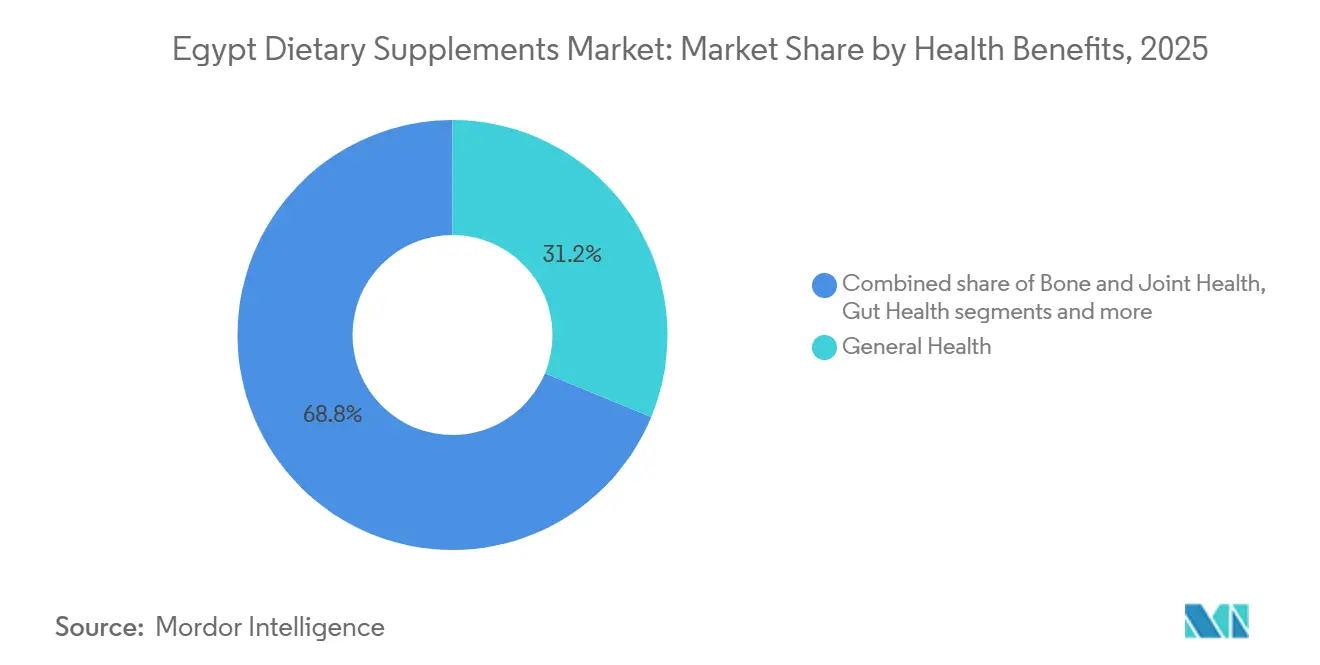

- By health benefits, general health captured a 31.23% share in 2025; bone and joint health is projected to grow at an 8.59% CAGR through 2031.

- By distribution channel, pharmacies and drug stores commanded a 48.34% share in 2025; online retail stores are expected to post the fastest growth at a 9.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Egypt Dietary Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer focus on preventive healthcare | +1.8% | National, led by Greater Cairo and Alexandria | Short term (≤ 2 years) |

| Rising incidence of lifestyle-related diseases | +1.5% | National; higher intensity in urban governorates | Medium term (2–4 years) |

| Expansion of sports, fitness, and active lifestyle trends | +1.0% | Greater Cairo, Alexandria; spill-over to secondary cities | Short term (≤ 2 years) |

| Growing adoption of personalized nutrition | +0.7% | Cairo and Alexandria; early adopters in professional segment | Medium term (2–4 years) |

| Preference for natural and plant-based supplements | +0.9% | National; stronger in peri-urban Delta and Upper Egypt | Medium term (2–4 years) |

| Growing innovation in supplement formulations | +0.8% | Cairo manufacturing hubs; nationwide retail | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing consumer focus on preventive healthcare

Growing consumer focus on preventive healthcare is driving demand, as consumers increasingly prioritize long-term wellness and nutritional maintenance over reactive healthcare. Greater awareness of balanced nutrition, immunity support, and healthy aging has encouraged the routine use of supplements as part of everyday health management. Consumers are becoming more proactive in addressing nutritional deficiencies and maintaining overall well-being through regular supplementation rather than waiting for health conditions to develop. This shift in health behavior is driving repeat purchases, expanding the user base across different age groups, and encouraging manufacturers to introduce scientifically formulated products tailored to preventive wellness. For instance, according to the State Information Service, annual spending on dietary supplements in Egypt exceeded EGP 50 billion in 2024, representing an approximately 30% increase compared with 2023, highlighting the country's growing adoption of preventive health and nutritional supplementation [1]Source: State Information Service, "ESDS: Egypt emerges as industrial hub for exporting "health" globally", sis.gov.eg.

Rising incidence of lifestyle-related diseases

The rising burden of chronic health conditions is encouraging consumers to adopt nutritional supplements as part of long-term health management. Growing concerns related to metabolic disorders, cardiovascular health, obesity, and diabetes have accelerated demand for products that support blood sugar management, heart health, weight management, and overall metabolic wellness. Consumers are increasingly incorporating vitamins, minerals, omega-3 fatty acids, and other functional nutrients into their daily routines to complement healthier lifestyles and maintain overall well-being. This trend has also encouraged manufacturers to expand scientifically formulated products targeting specific health concerns, strengthening demand for condition-focused nutritional supplements. For instance, according to the International Diabetes Federation (IDF), approximately 13.2 million adults in Egypt were living with diabetes in 2024, highlighting the growing need for nutritional support and preventive health solutions [2]Source: International Diabetes Federation (IDF), "Number of adults (20–79 years) with diabetes in Egypt (EG)", idf.org.

Expansion of sports, fitness, and active lifestyle trends

The expansion of sports, fitness, and active lifestyle trends is driving the Egypt dietary supplements market, as increasing participation in physical activity is encouraging consumers to incorporate nutritional supplements into their daily wellness routines. Growing awareness of the importance of exercise, muscle recovery, endurance, and overall physical performance has increased demand for protein supplements, amino acids, vitamins, minerals, electrolytes, and other sports nutrition products. This trend is also encouraging manufacturers to develop performance-oriented formulations with functional ingredients, convenient dosage formats, and targeted nutritional profiles. For instance, in May 2025, Egypt launched the "Sports Genome" phase of its National Genome Project, an initiative aimed at identifying genetic factors related to athletic performance, talent development, and sports excellence, reflecting the country's growing focus on sports, fitness, and health promotion.

Growing adoption of personalized nutrition

The growing adoption of personalized nutrition is driving the Egypt dietary supplements market, as consumers increasingly seek nutritional solutions tailored to their individual health goals, age, lifestyle, and specific physiological requirements. Rather than relying on standardized products, consumers are opting for customized combinations of vitamins, minerals, botanicals, probiotics, and other functional ingredients designed to address their unique nutritional needs. This shift is encouraging manufacturers to develop targeted formulations supported by scientific research, health assessments, and specialized nutrient combinations for different life stages and wellness objectives. Advances in nutritional science, digital health platforms, and individualized wellness recommendations are further supporting the adoption of personalized supplementation, while enabling companies to differentiate their product portfolios with nutrition solutions focused on specific consumer needs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory approval and product registration requirements | -1.5% | National; most acute for new entrants and international brands | Medium term (2–4 years) |

| Availability of counterfeit and unregistered dietary supplements | -1.0% | National; higher risk in informal urban markets and online channels | Short term (≤ 2 years) |

| High dependence on imported raw materials | -0.9% | National; particularly acute for API-intensive formulations | Medium term (2–4 years) |

| Intense competition from functional foods and fortified beverages | -0.7% | Urban governorates; modern trade-concentrated | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent regulatory approval and product registration requirements

Stringent regulatory approval and product registration requirements restrain the Egypt dietary supplements market by increasing the time and complexity involved in bringing new products to market. Manufacturers must comply with regulations covering ingredient approvals, product registration, labeling, quality standards, safety assessments, and manufacturing practices before commercialization. Frequent regulatory updates and extensive documentation requirements can prolong approval timelines, delaying product launches and limiting the introduction of new formulations. These compliance obligations also increase operational complexity for both domestic and international manufacturers, making it more difficult to expand product portfolios and respond quickly to changing consumer preferences.

Availability of counterfeit and unregistered dietary supplements

The availability of counterfeit and unregistered dietary supplements restrains the Egypt dietary supplements market by reducing consumer confidence in product quality, safety, and authenticity. Unauthorized products distributed through informal sales channels increase the risk of adulterated ingredients, inaccurate labeling, and substandard manufacturing practices, making consumers more cautious when purchasing dietary supplements. Counterfeit products also create unfair competition for legitimate manufacturers that invest in regulatory compliance and quality assurance, while damaging overall brand credibility within the market. Additionally, the circulation of unregistered supplements complicates regulatory enforcement and limits the ability of authorities to ensure consistent product standards, posing challenges to the sustainable growth of the organized dietary supplements industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vitamins and Minerals Anchor Demand While Herbals Accelerate

Vitamins and Minerals accounted for 55.43% of the Egypt dietary supplements market by product type in 2025. This category leads the market as it addresses a broad range of essential micronutrient requirements across different age groups and lifestyles. Consumers increasingly incorporate multivitamins and single-nutrient formulations into their daily wellness routines for long-term health maintenance rather than occasional use, resulting in consistent purchase frequency and repeat consumption. The availability of standardized formulations with well-established nutritional functions further strengthens consumer confidence compared to newer specialty supplements.

Herbal Supplements are projected to be the fastest-growing product type, registering a CAGR of 8.41% during 2026–2031. Growth is driven by increasing consumer preference for naturally derived ingredients perceived to offer holistic wellness support with fewer synthetic additives. The growing acceptance of traditional botanical remedies alongside modern nutritional practices is encouraging consumers to incorporate herbal formulations into their daily health routines. Manufacturers are expanding their portfolios with standardized plant extracts, adaptogenic herbs, and multifunctional botanical blends designed to support specific wellness goals, improving product differentiation and consumer appeal.

By Form: Capsules Dominate the Clinical Channel While Gummies Reshape Consumer Access

Capsules accounted for 35.45% of the market share by form in 2025. Their dominant position is supported by their ability to provide accurate dosing, protect sensitive ingredients from moisture, light, and oxidation, and accommodate a wide range of active compounds without compromising stability. Capsules are particularly suitable for formulations containing oils, probiotics, botanical extracts, and combination ingredients that require enhanced preservation and controlled release. Their smooth texture and ease of swallowing improve consumer compliance compared to larger dosage forms, while their minimal use of binders and fillers aligns with the growing preference for cleaner formulations. Additionally, capsule shells are available in both gelatin and plant-based alternatives, enabling manufacturers to address diverse dietary preferences and expand product offerings.

Gummies are projected to be the fastest-growing form, registering a CAGR of 8.31% during 2026–2031. Growth is driven by changing consumer preferences toward convenient and easy-to-consume supplement formats that fit into daily routines. Their taste, chewable texture, and portability support adherence to regular supplementation, particularly among consumers who have difficulty swallowing tablets or capsules. Ongoing innovation in low-sugar formulations, natural flavors, plant-based gelling agents, and multifunctional ingredient combinations is broadening their appeal across a wider consumer base. Manufacturers are also introducing gummies with improved stability, higher nutrient loading, and clean-label formulations, making them suitable for a broader range of nutritional applications.

By Health Benefits: General Health Leads but Bone and Joint Health Grows Fastest

General Health supplements held the largest health-benefits share at 31.23% in 2025. This position is driven by broad consumer demand for comprehensive nutritional support through daily supplementation, rather than targeting a single health condition. Consumers increasingly prefer products that provide balanced combinations of essential vitamins, minerals, antioxidants, and other nutrients to help maintain overall well-being, energy levels, and normal body functions. These formulations are suitable for routine use across multiple age groups and lifestyles, making them the first choice for individuals seeking long-term wellness support. Their versatility allows manufacturers to continuously introduce multinutrient formulations, once-daily products, and convenient combination supplements that simplify nutritional intake while meeting diverse wellness needs.

Bone and Joint Health is projected to be the fastest-growing health-benefits segment, registering a CAGR of 8.59% during 2026–2031. Growth is supported by increasing awareness of the importance of maintaining skeletal strength, joint flexibility, and mobility throughout adulthood. According to the United Nations Population Fund (UNFPA), approximately 63% of the population falls within the 15–64 age group, representing a large working-age population that increasingly seeks nutritional support to maintain physical performance, active lifestyles, and long-term musculoskeletal health. This is driving greater adoption of formulations containing calcium, vitamin D, magnesium, collagen, and other bone-supporting nutrients. In addition, growing participation in physical activities, increasing attention to healthy aging, and the availability of formulations with enhanced nutrient absorption and synergistic ingredient combinations are further accelerating demand for bone and joint health supplements.

By Distribution Channel: Pharmacies Lead with Institutional Reach While Online Retail Disrupts

Pharmacies and drug stores held 48.34% of the distribution share in 2025. Their dominant position is supported by high consumer trust in professionally supervised purchasing environments, where qualified pharmacists provide guidance on product selection, dosage, and potential nutrient interactions. These outlets offer a broad range of clinically recognized supplement brands and maintain strict storage and handling practices that help preserve product quality and efficacy. Consumers also prefer purchasing nutritional supplements alongside prescription and over-the-counter healthcare products, making pharmacies a convenient one-stop destination for health and wellness needs. Reliable product information, assurance of authenticity, and access to professional recommendations continue to reinforce consumer confidence, resulting in strong repeat purchases and sustained channel leadership.

Online retail stores are projected to be the fastest-growing distribution channel, registering a CAGR of 9.23% during 2026–2031. Growth is driven by the rapid expansion of digital commerce and increasing consumer preference for convenient purchasing. According to the International Trade Administration (ITA), internet penetration reached 81.9% in early 2025, with 96.3 million internet users, up from 72.2% in 2024, significantly expanding the potential online consumer base [3]Source: International Trade Administration, "Egypt Country Commercial Guide", trade.gov. The digital channel enables consumers to compare products, access detailed ingredient information, read customer reviews, subscribe to recurring purchases, and choose from a wider range of domestic and international brands than is typically available in physical stores.

Geography Analysis

Greater Cairo remains the largest regional market for dietary supplements, driven by its concentration of healthcare infrastructure, organized retail outlets, pharmacies, diagnostic centers, and wellness facilities. The region serves as the country's primary commercial hub, enabling faster introduction of new supplement formulations and wider availability of premium and specialized products. Consumers in this region have greater exposure to nutrition awareness campaigns, preventive healthcare practices, and digital health information, resulting in higher adoption of daily nutritional supplements. The strong presence of fitness centers, corporate professionals, students, and healthcare providers further supports sustained demand across a broad range of supplement categories, making Greater Cairo the primary growth engine of the market.

Lower Egypt accounts for a significant share of the market, supported by its extensive urban network, well-developed pharmacy infrastructure, and expanding organized retail sector. Governorates such as Alexandria and Sharqia serve as important commercial centers that facilitate the distribution of dietary supplements across neighboring areas. Increasing health awareness, growing participation in fitness activities, and wider access to healthcare services are encouraging consumers to incorporate nutritional supplements into their daily routines. The continued expansion of supermarket chains, pharmacies, and online retail platforms has improved product accessibility, while stronger logistics networks have ensured wider availability of both domestic and imported supplement products throughout the region.

Upper Egypt, along with the Canal, Sinai, and Frontier governorates, is emerging as an increasingly important market as healthcare infrastructure, pharmacy networks, and digital commerce continue to expand. Improvements in transportation, distribution capabilities, and e-commerce fulfillment are making dietary supplements more accessible in cities beyond the country's traditional commercial centers. Greater availability of healthcare services, increasing nutrition awareness, and broader internet connectivity are supporting gradual growth in supplement adoption among consumers. Although market penetration remains lower than in more urbanized regions, ongoing investments in retail expansion, healthcare accessibility, and digital purchasing channels are enabling manufacturers to strengthen their presence and capture long-term growth opportunities across these developing governorates.

Competitive Landscape

The Egypt dietary supplements market is moderately fragmented, with competition shared between established domestic manufacturers and multinational healthcare and nutrition companies. Domestic companies such as Amoun Pharmaceutical Company SAE and EVA Pharma benefit from strong regulatory familiarity, established relationships with pharmacy distributors, and efficient nationwide supply networks, enabling them to maintain broad product availability and respond quickly to evolving consumer requirements. International companies, including Bayer AG, Abbott Laboratories, and Amway Corporation, compete through globally recognized brands, extensive research capabilities, and diversified product portfolios spanning vitamins, minerals, sports nutrition, pediatric nutrition, and specialty wellness supplements.

Competition is increasingly centered on product innovation, formulation technology, and ingredient differentiation rather than price alone. Manufacturers are investing in advanced delivery systems, enhanced bioavailability technologies, sustained-release formulations, microencapsulation, and precision ingredient combinations to improve nutrient absorption and consumer convenience. Companies are also expanding their portfolios with premium products that address specific wellness needs, including immunity support, digestive health, healthy aging, cognitive wellness, and personalized nutrition. Greater emphasis on clean-label formulations, plant-based ingredients, sugar-reduced products, and clinically supported functional ingredients is enabling brands to differentiate themselves while meeting evolving consumer expectations for quality, safety, and efficacy.

The competitive landscape is further evolving through new product development and portfolio diversification across emerging supplement categories. Manufacturers are introducing formats such as probiotic gummies, collagen-infused beauty supplements, chewable nutraceuticals, multifunctional botanical blends, and personalized nutritional formulations to appeal to changing consumer lifestyles. Digital marketing, e-commerce expansion, pharmacist engagement, and consumer education initiatives have become important competitive strategies for increasing brand visibility and customer loyalty. As demand shifts toward convenient, science-backed, and premium nutritional solutions, companies that combine strong distribution capabilities with continuous product innovation and advanced formulation technologies are expected to strengthen their competitive positioning in the Egyptian dietary supplements market.

Egypt Dietary Supplements Industry Leaders

-

Bayer AG

-

Abbott Laboratories

-

Amoun Pharmaceutical Company SAE

-

EVA Pharma

-

Amway Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Pharco Pharmaceuticals announced plans to invest approximately EGP 1.5 billion in 2027, up from EGP 1.15 billion in 2025, as part of a strategy to expand production capacity, diversify product lines, and strengthen its presence across 50 global export markets.

- February 2026: Bayer Consumer Health launched Priorin Extra, a dietary supplement formulated to address hair loss, stimulate hair growth, and provide nutritional support.

Egypt Dietary Supplements Market Report Scope

A dietary supplement is a manufactured product intended to add nutritional value to the diet. The Egypt dietary supplements market is segmented by product type, form, health benefits, and distribution channel. Based on product type, the market is segmented into vitamins and minerals, herbal supplements, collagen, fatty acids, probiotics, enzymes, and other product types. Based on form, the market is segmented into tablets, capsules, powders, gummies, liquids, and other forms. Based on health benefits, the market is segmented into general health, bone and joint health, gut health, immune health, heart health, beauty supplements, and others. Based on distribution channel, the market is segmented into supermarkets/hypermarkets, pharmacies/drug stores and health stores, online retail stores, and other distribution channels. For each segment, the market sizing and forecast have been done based on the value (in USD million).

| Vitamins and Minerals |

| Herbal Supplements |

| Collagen |

| Fatty Acids |

| Probiotics |

| Enzymes |

| Other Product Types |

| Tablets |

| Capsules |

| Powders |

| Gummies |

| Liquids |

| Other Forms |

| General Health |

| Bone and Joint Health |

| Gut Health |

| Immune Health |

| Heart Health |

| Beauty Supplements |

| Others |

| Supermarkets/Hypermarkets |

| Pharmacies/Drug Stores and Health Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Vitamins and Minerals |

| Herbal Supplements | |

| Collagen | |

| Fatty Acids | |

| Probiotics | |

| Enzymes | |

| Other Product Types | |

| By Form | Tablets |

| Capsules | |

| Powders | |

| Gummies | |

| Liquids | |

| Other Forms | |

| By Health Benefits | General Health |

| Bone and Joint Health | |

| Gut Health | |

| Immune Health | |

| Heart Health | |

| Beauty Supplements | |

| Others | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Pharmacies/Drug Stores and Health Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the size of the Egypt dietary supplements space in 2026 and where is it heading by 2031?

The supplied draft values the Egypt dietary supplements market at USD 397.98 million in 2025 and projects it to reach USD 610.15 million by 2031 at a 7.56% CAGR over 2026-2031.

Which product category leads demand in Egypt?

Vitamins and Minerals led product demand with 55.43% share in 2025, supported by physician recommendation, routine pharmacy purchase, and common micronutrient needs.

Which format is growing fastest among supplement users in Egypt?

Gummies are the fastest-growing format with an 8.31% CAGR through 2031, helped by better ease of use for children, older adults, and first-time users.

Why is bone and joint support expanding so quickly in Egypt?

Bone and Joint Health is projected to grow at 8.59% through 2031 because Egypt has high osteoporosis prevalence, a rising older population, and clearer clinical guidance around vitamin D use.

Page last updated on: