Egypt Dairy Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.71 Billion |

| Market Size (2026) | USD 4.84 Billion |

| Market Size (2031) | USD 5.54 Billion |

| Growth Rate (2026 - 2031) | 2.76% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Egypt Dairy Products Market Analysis by Mordor Intelligence

The Egypt dairy products market size is projected to grow from USD 4.7 billion in 2025, USD 4.8 billion in 2026, to USD 5.5 billion by 2031, growing at a CAGR of 2.8% from 2026 to 2031. The Egypt dairy products market is expanding on a stable demand base, as dairy remains a daily staple across income groups and the country’s population continues to rise toward 120 million by 2030. A gradual shift from loose and informal milk purchases to packaged and branded products is also shaping the Egypt dairy products market, especially in Greater Cairo, Alexandria, and other urban centers where food safety awareness and retail access are stronger. The formal channel is gaining ground, but growth remains measured because informal milk still accounts for 70% of raw milk at the farm gate, keeping a large share of dairy consumption outside branded formats. Competitive activity in the Egypt dairy products market centers on securing raw milk supply, expanding cold chain reach, and launching higher-value products in cheese, yogurt, and flavored dairy. The market outlook remains supported by modern trade expansion and a broader shelf-stable dairy base, although currency pressure, imported input costs, and the slow pace of formalizing the informal milk trade continue to limit faster headline growth.

Key Report Takeaways

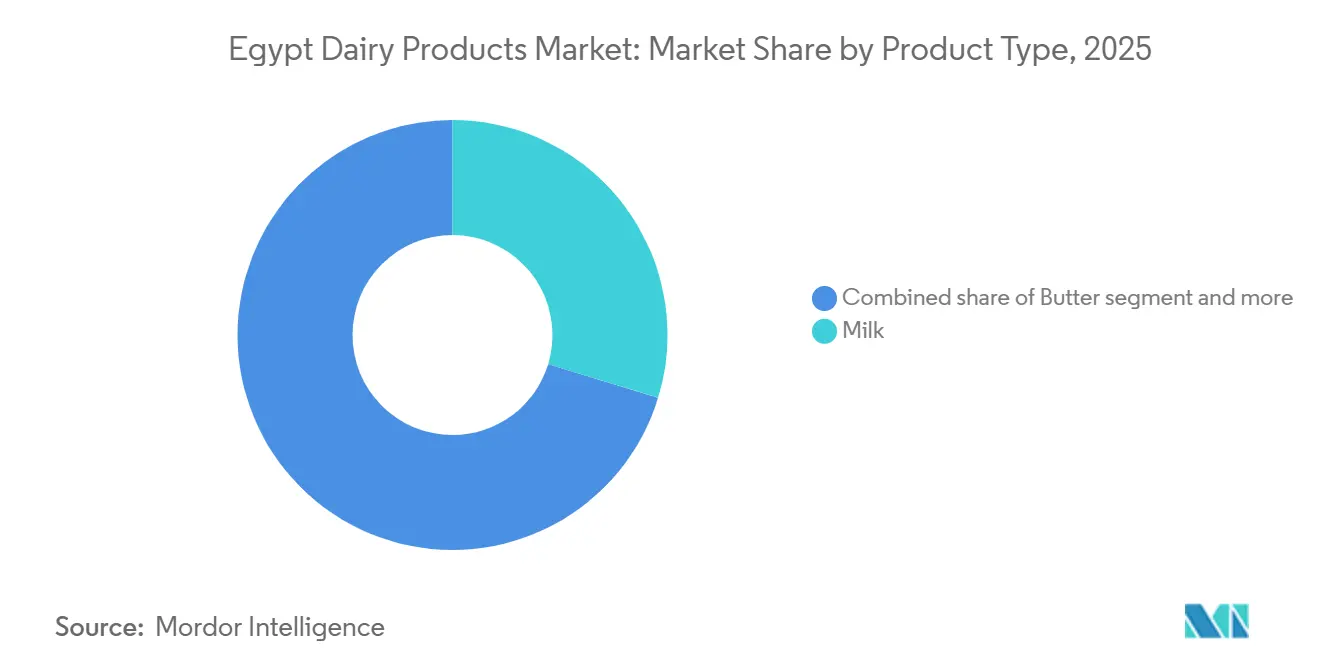

- By product type, milk accounted for the largest share of the Egypt dairy products market, at 29.7% in 2025, while butter is projected to grow at the fastest CAGR of 3.9% during 2026-2031.

- By distribution channel, off-trade accounted for the largest share of the Egypt dairy products market, at 84.6% in 2025, while on-trade is projected to grow at the fastest CAGR of 3.7% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Egypt Dairy Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising packaged dairy penetration | +0.6% | Greater Cairo, Alexandria, Delta urban centers | Short term (≤ 2 years) |

| Retail modernization and chain store expansion | +0.4% | Greater Cairo, Alexandria, North Coast, new satellite cities | Short term (≤ 2 years) |

| Premiumization of yogurt, cheese, and functional dairy | +0.5% | Greater Cairo, New Cairo, North Coast, Red Sea governorates | Medium term (2-4 years) |

| Local dairy localization and import substitution | +0.5% | National, early gains in Nubaria, Sadat City, Obour industrial zones | Medium term (2-4 years) |

| Expansion of refrigerated distribution and farm-to-retail integration | +0.3% | Giza, 6th of October City, Upper Egypt distribution corridors | Medium term (2-4 years) |

| Shelf-stable milk and powdered dairy demand in price-sensitive channels | +0.4% | Upper Egypt, rural Delta, peri-urban price-sensitive zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Packaged Dairy Penetration Across Urban Egypt

Rising urbanization continues to support the Egypt dairy products market, as a more mobile population steadily shifts from loose milk sold by informal vendors to packaged, chilled, and branded alternatives. Domestic raw milk output is expected to increase by 8% to 7 million tonnes in 2025. However, farms that meet international hygiene standards are expected to supply only 10% of that volume, indicating that processors will continue to depend on a mixed supply base to maintain consistency[1]Source: Food and Agriculture Organization, "Investing in climate-smart dairy value chains in Egypt", undp.org. The primary growth driver is the shift in consumption format rather than a sharp increase in raw milk availability, as branded supply generates more value per liter than unpackaged trade. Egypt’s Food Safety Authority, established under Law No. 1 of 2017, continues to enforce mandatory hygiene and labeling standards, supporting the adoption of formal packaged dairy products across retail channels. The Egyptian Organization for Standardization also plays an important role, as quality marks are becoming increasingly important for modern retail listings, helping branded processors strengthen shelf access against informal supply.

Retail Modernization and Chain Store Expansion

Retail modernization is improving access to branded dairy products and widening the formal sales base of the Egypt dairy products market. Carrefour is expected to surpass 100 stores in Egypt by 2026, highlighting the rapid expansion of organized grocery retail into cities and catchment areas that previously had limited modern retail coverage. Spinneys operates 35 branches across 11 governorates and targets 43 branches by the end of 2026, giving branded dairy suppliers more chilled shelf space and stronger product visibility in both established and expanding urban locations. Each new supermarket opening improves refrigerated handling, strengthens shelf-life management, and shifts more dairy spending into traceable branded channels. This shift is significant because, as organized retail becomes part of neighborhood shopping habits, informal dairy sellers lose repeat purchasing opportunities in categories where packaging, hygiene, and product range strongly influence consumer choice.

Premiumization of Yogurt, Cheese, and Functional Dairy

Premiumization is becoming more visible in the Egypt dairy products market as urban middle-income consumers spend more on higher-value yogurt, cheese, and functional dairy products. Danone Egypt is expected to introduce HiPRO yogurt in June 2026, offering 18 grams of protein per serving, no added sugar, no fat, and no artificial flavors. The launch is expected to mark the large-scale entry of functional protein dairy into mainstream retail. Juhayna is expected to launch Turkish Labneh variants in May 2026, featuring real ingredient pieces and a 100% natural formula free from vegetable oils. This launch indicates that premium ingredient positioning can attract buyers even in a cost-sensitive environment. The category remains underdeveloped, giving early entrants an opportunity to capture stronger value before mass-market competition expands. Obour Land’s processed cheese revenue is expected to increase by 26% in Q1 2026 after the commissioning of its new factory in December 2025, confirming that value-added cheese formats are growing faster than commodity dairy lines.

Government Push for Local Dairy Localization and Import Substitution

Local dairy production has become increasingly important in the Egypt dairy products market as the country seeks to reduce import exposure across key dairy categories. Egypt’s dairy import bill reached USD 807 million in 2024, up 13.1% from the previous year, with concentrated infant formula imports alone accounting for USD 225 million. The Ministry of Agriculture also drafted a formal dairy development roadmap targeting an increase in per capita dairy consumption from 61 kg to 70 kg by 2030 and a reduction in import dependency, giving processors clearer long-term policy direction. Beyti’s Nubaria expansion, supported by the Ministry of Industry and Transport in October 2024, added 100,000 tonnes per year across cheese, yogurt, and drinkable yogurt lines and signaled continued support for scaling up local manufacturing. This policy environment supports domestic processing investment and positions import substitution as a structural growth theme rather than a short-term response to currency pressure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Informal milk trade limits branded conversion | -0.5% | Delta, Upper Egypt, peri-urban zones nationally | Long term (≥ 4 years) |

| Currency depreciation raises imported input costs | -0.5% | National, concentrated in import-dependent processors | Short term (≤ 2 years) |

| Cold chain gaps outside major urban corridors | -0.3% | Upper Egypt, South Sinai, remote Delta | Medium term (2-4 years) |

| Feed cost volatility compresses producer margins | -0.4% | National, concentrated in large integrated farm operations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Informal Milk Trade Limits Branded Category Conversion

The informal milk trade remains one of the key constraints on the Egypt dairy products market, as a significant share of the country’s raw milk continues to move outside branded and regulated channels. The Ministry of Agriculture’s Animal Wealth Development Sector documented 826 milk collection centers, of which only half were officially licensed, indicating that supply chain formalization remains incomplete[2]Source: Egyptian Journal of Animal Production (EJAP), " ASSESSMENT OF DAIRY FARMS AND MILK COLLECTION CENTERS IN EL‑GHARBIA GOVERNORATE AS A MODEL OF THE EGYPTIAN DELTA", journals.ekb.eg. Informal milk is also expected to maintain a clear price advantage for many lower-income and rural households in 2025, slowing the pace at which branded dairy companies can convert demand. This challenge extends beyond distribution, as it also reflects long-standing consumer habits in Delta and Upper Egypt. As a result, the Egypt dairy products market is expected to formalize gradually rather than through a rapid shift in volume from informal supply to branded retail.

Currency Depreciation Increases Imported Input Costs

Currency depreciation remains a clear drag on the Egypt dairy products market, as many processors continue to rely on imported milk powder, cultures, specialty ingredients, and packaging. Egypt adopted a flexible exchange rate regime in March 2024, and the depreciation of the Egyptian pound increased the local currency cost of imported dairy inputs across the supply chain[3]Source: International Monetary Fund (IMF), "Arab Republic of Egypt – IMF Country Report No. 2024/001", www.imf.org. Juhayna reported EGP 522 million in foreign exchange-related expenses in H1 2025, highlighting the extent to which hard-currency sourcing can pressure margins, even when revenue increases. Higher input costs limit pricing flexibility, premium product expansion, and distribution investment, particularly in categories that depend more heavily on imported components. This pressure is strongest for processors focused on flavored milk, cream-based desserts, and specialty cheese, where passing costs on to consumers is more difficult in a price-sensitive environment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Milk Leads Everyday Consumption While Butter Expands Faster

Milk is expected to account for 29.7% of the Egypt dairy products market share in 2025, making it the largest product category in the Egypt dairy products market. Its leadership stems from its role as a daily staple across income groups and its broad presence in both urban and rural consumption patterns. UHT and powdered milk are expected to remain the practical backbone of demand in price-sensitive areas and geographies with limited refrigerated infrastructure, while fresh and flavored milk are likely to perform better in modern trade outlets. This balance keeps milk at the center of volume demand, as it addresses both affordability and convenience needs across the country. It also gives processors a stable base to introduce higher-value dairy formats without weakening their core mass-market portfolios.

Within the broader Egypt dairy products industry, butter is forecast to grow at a CAGR of 3.9% during 2026-2031, making it the fastest-growing product category by Egypt dairy products market size. The category is expected to benefit from the widening cost gap between imported and domestic butter following the weakening of the Egyptian pound, which has improved the relative value of local supply. Urban home baking culture is adding to retail demand, while hotels, cafés, and restaurants are supporting institutional purchases in tourism-linked areas. Cheese remains an important profit anchor within this mix, as Obour Land reported a 17% increase in white cheese revenue and a 26% increase in processed cheese revenue in Q1 2026, following the commissioning of its new factory in December 2025. Yogurt is also moving up the value ladder as drinkable formats gain traction and functional products, such as HiPRO, create a new premium layer in branded dairy.

By Distribution Channel: Off-Trade Holds the Revenue Base While On-Trade Records the Faster Growth Rate

Off-trade is expected to account for 84.6% of the Egypt dairy products market size in 2025, making it the largest distribution channel in the Egypt dairy products market. Convenience stores, supermarkets, and hypermarkets form the backbone of this channel in Greater Cairo, Alexandria, and the Delta, where organized retail coverage is strongest. Supermarkets and hypermarkets are especially important because they offer refrigerated product visibility, brand comparison, and reliable stock rotation, which are critical for packaged dairy products. Carrefour is expected to surpass 100 outlets in Egypt in 2026, while Spinneys is set to expand its branch network further by year-end, widening branded dairy shelf presence across formal retail. Online grocery still represents a smaller share of off-trade sales, but it is gaining relevance in Cairo among dual-income households for specialty cheese, flavored yogurt, and premium butter.

Within the Egypt dairy products industry, on-trade is forecast to grow at a CAGR of 3.7% during 2026-2031, making it the fastest-growing distribution channel in the Egypt dairy products market share base beyond retail. Hotels, resorts, cafés, and restaurants are driving this growth, rather than household demand alone. Coastal city development and stronger tourism activity are increasing institutional dairy purchases for buffets, foodservice preparation, and portion-controlled consumption formats. On-trade also functions as a product discovery channel, as consumers who first encounter premium yogurt, specialty cheese, or flavored butter in hospitality venues often seek the same products later in organized retail. Companies that develop foodservice-specific pack sizes, extended shelf-life options, and dedicated account relationships are better positioned to benefit from this growth than companies that sell only standard retail SKUs.

Geography Analysis

Greater Cairo and Alexandria are expected to represent the largest concentration of branded dairy demand in the Egyptian dairy products market in 2025. These urban centers combine higher supermarket density, stronger refrigerated logistics, and higher disposable income, supporting wider purchases of fresh milk, flavored milk, yogurt, cheese, and other packaged dairy lines. They also account for a large share of the country’s branded retail activity, as organized grocery is more developed there than in most other governorates. This urban corridor remains the primary launch base for premium dairy formats because retailers can support broader assortments, stronger cold chain execution, and more consistent merchandising. This combination keeps the Egypt dairy products market size most concentrated in the northern urban belt, even as new demand centers continue to develop.

The Red Sea and Mediterranean coastal belt is expected to be the fastest-expanding geography in the Egypt dairy products market during the 2026-2031 period, as hospitality growth is driving institutional demand faster than residential consumption growth. Locations such as Hurghada, Sharm El Sheikh, Marsa Matruh, and New Alamein are attracting more procurement from hotels, resorts, and cafés, especially for cheese, cream, flavored yogurt, and premium butter. Spinneys’ branch expansion into tourism-linked areas indicates that formal grocery retail is also strengthening alongside foodservice development in these locations. This trend gives dairy producers a dual route to growth, as the same geography can support both retail and hospitality demand as coastal destinations mature.

The wider national picture remains split between formal urban demand and informal rural supply, which continues to define the Egypt dairy products market. Delta governorates serve as both dairy farming centers and branded consumption zones, while Upper Egypt remains more dependent on lower-cost and shelf-stable formats due to lower income levels and thinner cold chain coverage. UHT milk, powdered milk, and processed cheese are better suited to this environment than chilled premium products because they can move more easily through uneven distribution conditions. Large manufacturing and logistics assets also support national distribution, with Beyti’s integrated Nubaria complex near Alexandria and DP World’s cold storage project in 6th of October City improving longer-distance supply capacity. Even so, last-mile temperature control outside the main urban corridors will take longer to strengthen, meaning formal branded dairy will continue expanding in phases rather than at a uniform national pace.

Competitive Landscape

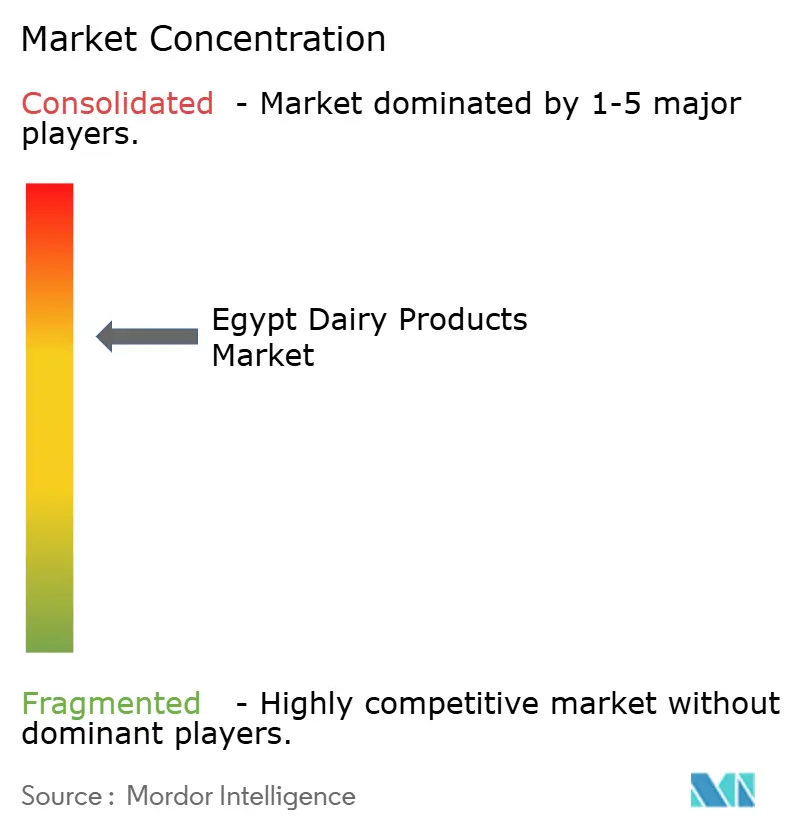

The Egypt dairy products market shows moderate concentration, with Juhayna Food Industries, Beyti, and Obour Land holding strong positions across milk, yogurt, and cheese. At the same time, a long tail of smaller regional players and import-oriented brands remains active. This structure creates a clear group of market leaders but does not result in the level of dominance seen in highly consolidated dairy markets. Companies continue to focus on three recurring priorities: capacity expansion, vertical supply control, and product premiumization. They are also using broader export activity to offset local currency volatility, adding resilience to leading business models. This pattern keeps the Egypt dairy products market competitive while favoring better-capitalized domestic processors with stronger route-to-market scale.

Juhayna remains one of the clearest examples of scale advantages in the Egypt dairy products market. Its Q1 2026 consolidated net profit is expected to rise 123.2% year over year to EGP 668.7 million, while sales are expected to reach EGP 8.6 billion, reflecting a stronger mix and improved branded execution. The company is also expected to report EGP 2.2 billion in capital investment and EGP 1.9 billion in export sales across the first nine months of 2025, indicating a simultaneous focus on production capacity and external revenue diversification. Beyti has followed a similar investment path through the expansion of its Nubaria complex, where additional production lines and integrated energy assets support scale, efficiency, and long-term manufacturing quality.

Obour Land illustrates how focused investment can strengthen a challenger position within the Egypt dairy products market. The company’s new processed cheese factory is expected to become operational in December 2025, and processed cheese revenue is projected to increase 26% in Q1 2026, showing how targeted capital spending can quickly improve category momentum. Danone’s planned launch of HiPRO in June 2026 indicates that international players still see room to build premium and functional demand in Egypt, especially in yogurt and wellness-adjacent formats. Arla Foods’ continued pursuit of Domty’s dairy business also shows that strategic interest in Egypt’s branded dairy base remains strong globally, even as the final ownership outcome remains pending. This mix of domestic scale leaders, active premium launches, and ongoing strategic interest supports a disciplined, moderately concentrated competitive landscape that remains open to category-specific gains.

Egypt Dairy Products Industry Leaders

-

Juhayna Food Industries

-

Arabian Food Industries Company

-

Obour Land for Food Industries S.A.E.

-

Danone SA

-

Beyti

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Danone Egypt introduced HiPRO yogurt in the Egyptian market. The product offered 18 grams of protein per serving in three flavors, with zero added sugar, zero fat, and zero artificial flavors. The launch marked the commercial entry of functional protein dairy into Egypt’s mainstream retail market and signaled confidence in the country’s growing premium consumer segment.

- May 2026: Juhayna Food Industries launched new Turkish Labneh variants, including Kalamata Olives & Thyme and Sundried Tomatoes & Basil. The products contained real ingredient pieces in 100% natural labneh and were free from vegetable oils. The launch positioned Juhayna at the artisanal premium end of the yogurt-labneh spectrum. It also coincided with a Q1 2026 consolidated net profit of EGP 668.7 million, up 123.2% year over year, reflecting strong underlying operational momentum.

- October 2025: Capital Agro Group launched a USD 25 million integrated frozen and chilled food logistics complex near key Delta ports. The company deployed USD 15 million in 2025 and planned to invest USD 10 million through 2027. The facility incorporated AI-based storage management and solar-renewable energy, supporting dairy cold chain throughput under a 25-year usufruct agreement.

- September 2025: DP World Egypt signed an agreement with Elsewedy Industrial Development to construct a USD 29 million (EGP 1.42 billion) cold storage facility in 6th of October City. The 16,194-square-meter facility included eight independently controlled chambers and 25,000 pallet positions for chilled and frozen products, including dairy. The project aimed to reduce food waste and extend cold chain reach toward Upper Egypt.

Egypt Dairy Products Market Report Scope

| Butter | ||

| Cheese | Natural Cheese | Cheddar |

| Cottage | ||

| Ricotta | ||

| Parmesan | ||

| Others | ||

| Processed Cheese | ||

| Cream | Fresh Cream | |

| Cooking Cream | ||

| Whippping Cream | ||

| Others | ||

| Dairy Desserts | Ice Cream | |

| Cheesecakes | ||

| Frozen Desserts | ||

| Others | ||

| Milk | Condensed Milk | |

| Flavored Milk | ||

| Fresh Milk | ||

| UHT Milk | ||

| Powdered Milk | ||

| Yogurt | Drinkable | |

| Spoonable | ||

| Sour Milk Drinks | ||

| On-trade | |

| Off-trade | Convenience Stores |

| Specialist Retailers | |

| Supermarkets and Hypermarkets | |

| Online Retail Stores | |

| Others |

| By Product Type | Butter | ||

| Cheese | Natural Cheese | Cheddar | |

| Cottage | |||

| Ricotta | |||

| Parmesan | |||

| Others | |||

| Processed Cheese | |||

| Cream | Fresh Cream | ||

| Cooking Cream | |||

| Whippping Cream | |||

| Others | |||

| Dairy Desserts | Ice Cream | ||

| Cheesecakes | |||

| Frozen Desserts | |||

| Others | |||

| Milk | Condensed Milk | ||

| Flavored Milk | |||

| Fresh Milk | |||

| UHT Milk | |||

| Powdered Milk | |||

| Yogurt | Drinkable | ||

| Spoonable | |||

| Sour Milk Drinks | |||

| By Distribution Channels | On-trade | ||

| Off-trade | Convenience Stores | ||

| Specialist Retailers | |||

| Supermarkets and Hypermarkets | |||

| Online Retail Stores | |||

| Others | |||

Key Questions Answered in the Report

What is the 2026 outlook for dairy products in Egypt?

The Egypt dairy products market is estimated at USD 4.8 billion in 2026 and is expected to reach USD 5.5 billion by 2031 at a 2.8% CAGR, supported by packaged dairy adoption and retail formalization.

Which product category is largest in Egypt dairy products?

Milk remained the largest category with 29.7% share in 2025 because it is a daily staple across income groups and works well in both chilled and shelf-stable formats.

Which product category is growing fastest through 2031?

Butter is projected to grow the fastest at a 3.9% CAGR during 2026-2031, supported by domestic substitution, urban baking demand, and foodservice use.

Why does off-trade dominate dairy sales in Egypt?

Off-trade held 84.6% of revenue in 2025 because supermarkets, hypermarkets, and convenience stores provide the strongest access to branded, refrigerated, and shelf-stable dairy products.

Page last updated on: