Egypt Construction Consulting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

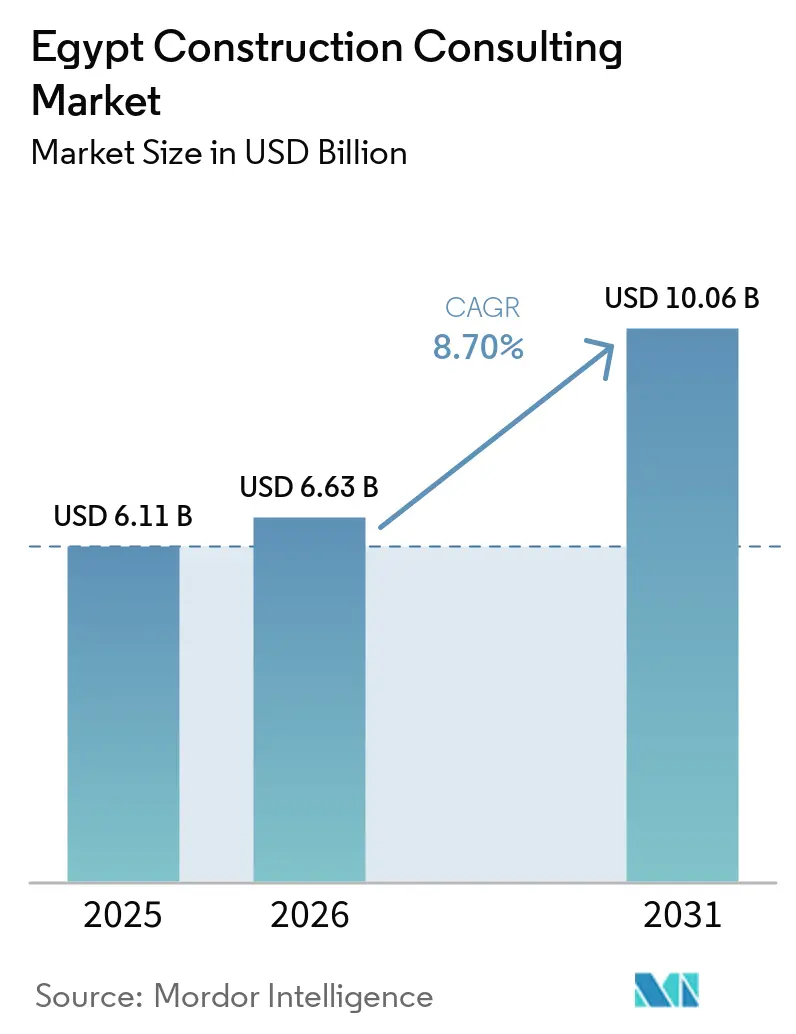

| Base Year Market Size (2025) | USD 6.11 Billion |

| Market Size (2026) | USD 6.63 Billion |

| Market Size (2031) | USD 10.06 Billion |

| Growth Rate (2026 - 2031) | 8.70% CAGR |

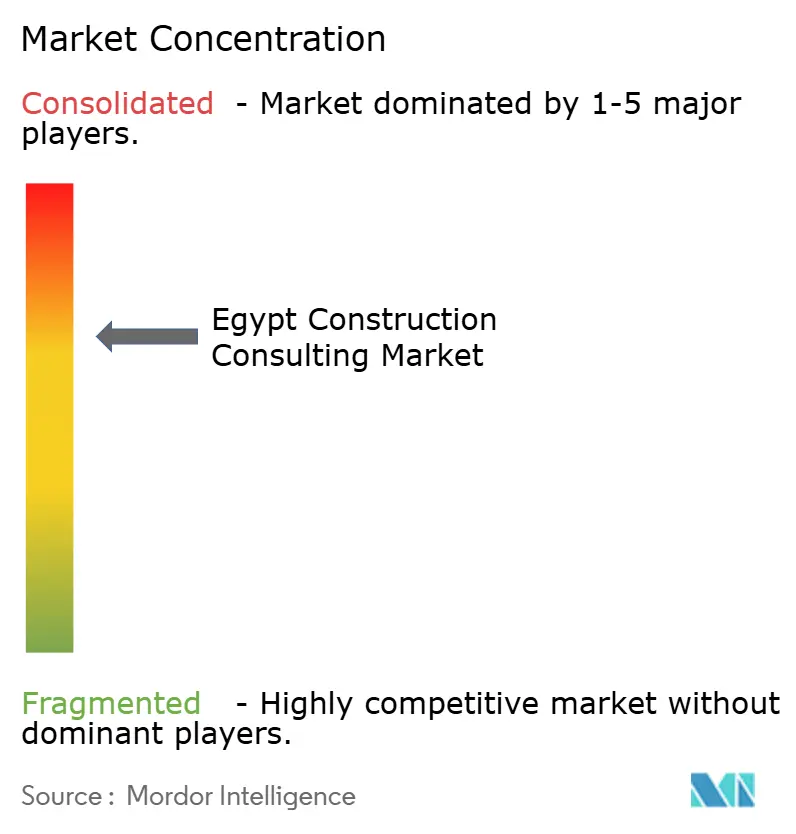

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Construction Consulting Market Analysis by Mordor Intelligence

The Egypt Construction Consulting Market size was valued at USD 6.11 billion in 2025 and is estimated to grow from USD 6.63 billion in 2026 to reach USD 10.06 billion by 2031, at a CAGR of 8.70% during the forecast period (2026-2031).

Mega-projects valued at USD 450 billion anchor a deep opportunity pool that rewards firms able to blend project-management, financial, and engineering skills. Updated Public-Private Partnership (PPP) rules cut approval times and formalize private-finance mandates, pushing transaction-advisory work into the mainstream. The Golden License fast-track, enacted under Executive Regulation 1203/2024, makes rigorous front-end due diligence compulsory and shifts value toward feasibility and master-planning specialists. Sovereign wealth fund inflows, led by ADQ’s USD 35 billion Ras El Hekma deal, import international governance standards and expand demand for firms versed in the Equator Principles and IFC Performance Standards.

Key Report Takeaways

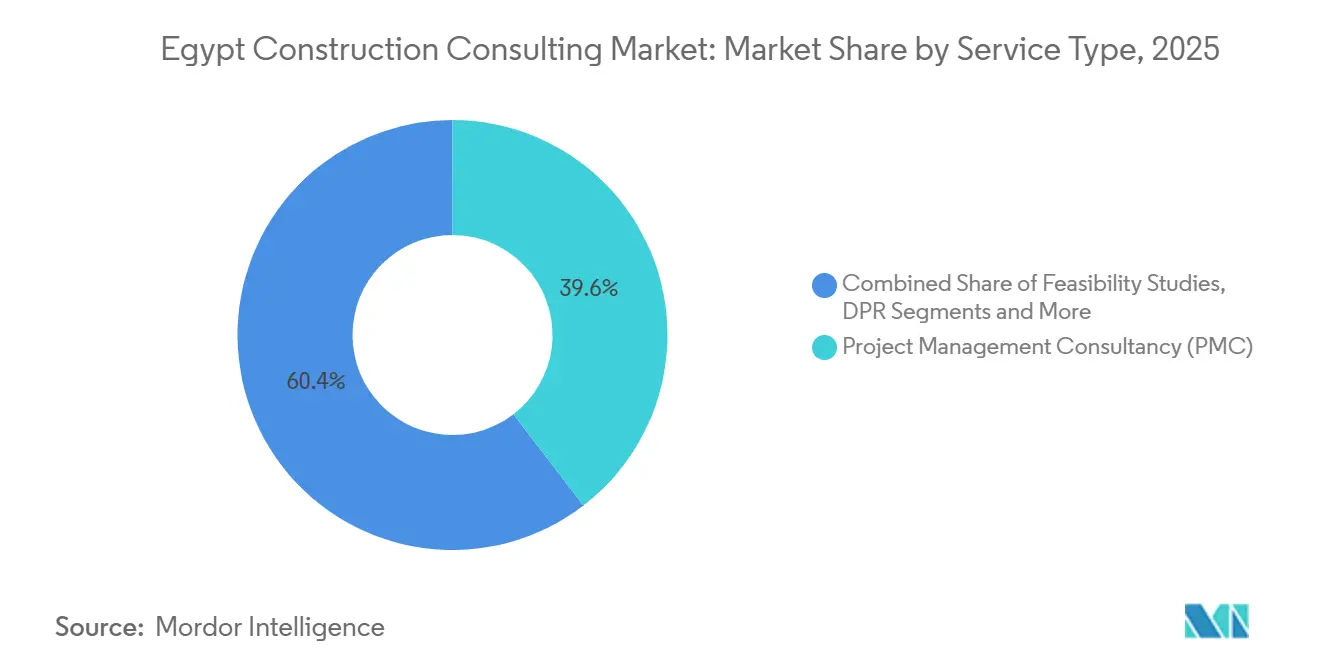

- By service type, Project Management Consultancy led the Egypt construction consulting market with 39.58% market share in 2025, while Master Planning and Other Services are projected to grow at a 9.3% CAGR through 2031.

- By sector, infrastructure and civil works accounted for 37.8% of the Egypt construction consulting market size in 2025; residential consulting is forecast to expand at a 9.25% CAGR between 2026 and 2031.

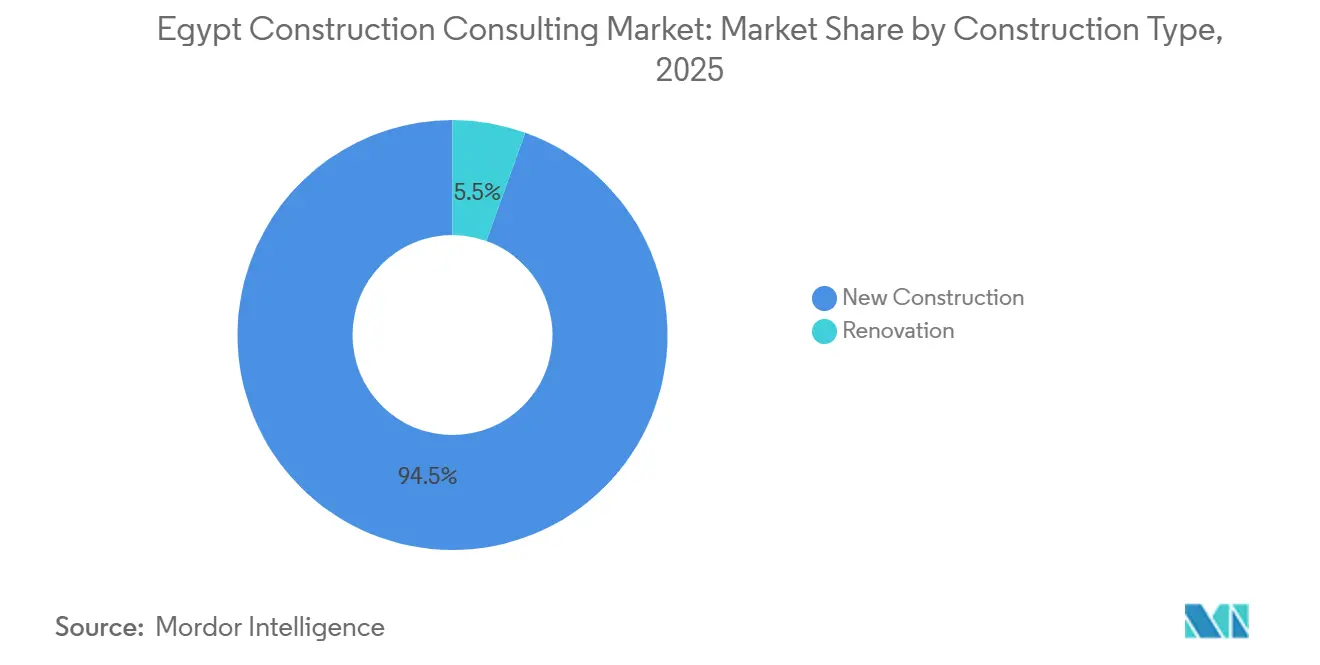

- By construction type, new construction accounted for 94.5% of the Egypt construction consulting market in 2025, while renovation consulting is advancing at a 10.5% CAGR through 2031.

- By investment source, public clients held 70% of the Egypt construction consulting market share in 2025 and private projects are expected to grow at a 10.1% CAGR to 2031.

- By geography, Greater Cairo captured 45.6% of the Egypt construction consulting market size in 2025 and is poised to register a 9.5% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Egypt Construction Consulting Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| USD 450 billion mega-project pipeline sustains multi-disciplinary consulting demand | 2.8% | National, with concentration in Greater Cairo, Ras El Hekma, New Administrative Capital, Suez Canal Economic Zone | Long term (≥ 4 years) |

| Amended PPP Law and Central PPP Unit accelerate private-finance advisory mandates | 2.1% | National, with early gains in Greater Cairo, Alexandria, and Giza | Medium term (2-4 years) |

| Golden License fast-track (Executive Regulation 1203/2024) heightens front-end due diligence needs | 1.6% | National, with priority zones: New Administrative Capital, Ras El Hekma, Suez Canal Economic Zone, Golden Triangle | Medium term (2-4 years) |

| Gulf SWF inflows spur international-standard project advisory opportunities | 1.5% | Greater Cairo, Ras El Hekma, Red Sea coastal developments | Short term (≤ 2 years) |

| Non-cash Payments Law 18/2019 reshapes contract-administration consultancy | 0.8% | National, with emphasis on public-sector projects and large private developments | Medium term (2-4 years) |

| Draft 2025 seismic-code upgrade triggers retro-engineering assessment services | 0.7% | National, with concentration in Greater Cairo, Alexandria, and high-density urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

USD 450 Billion Mega-Project Pipeline

The government is steering more than USD 450 billion into power grids, new cities, and transport corridors. The Cairo Monorail Line 1, opened in March 2026, illustrates the importance of multidisciplinary oversight, from rolling stock selection to station-area planning. Agricultural reclamation under the New Delta program spans 1 million acres and demands hydrology, agronomy, and civil works advice within a single mandate. The scale of Ras El Hekma requires hospitality master planning, coastal zone modeling, and multi-source financing expertise in a single bundle. Such breadth elevates consultancies that keep geotechnical, environmental, and financial-model teams in-house. Firms unable to integrate disciplines risk exclusion from tender shortlists.

Amended PPP Law and Central PPP Unit Reforms

PPP Law 67/2010, amended in 2021, introduced unsolicited bids and standardized templates. The Central PPP Unit now coordinates risk allocation and value-for-money tests, shrinking legal uncertainty for investors[1]Central PPP Unit, “Revised PPP Manual,” pppunit.gov.eg . Transaction advisors who pair engineering know-how with chartered-finance skills are winning desalination, waste-to-energy, and toll-road concessions. Private-source consulting revenues are therefore forecast to grow at a 10.1% CAGR to 2031, outpacing the overall Egypt construction consulting market. Developers also lean on advisors to navigate performance-based payment clauses that tie returns to availability metrics. The reform era shifts the value of consulting from traditional owner-engineer roles toward hybrid technical-and-financial mandates.

Golden License Fast-Track

Executive Regulation 1203/2024 bundles multi-agency approvals into a single-window process under the General Authority for Investment and Free Zones. Applicants must present holistic feasibility studies covering technical, financial, environmental, and social factors[2]General Authority for Investment and Free Zones, “Golden License Guidelines,” gafi.gov.eg . This requirement forces developers to involve consultancies earlier and allocate larger budgets to front-end work. Feasibility mandates are most intense in the New Administrative Capital, Suez Canal Economic Zone, and the Golden Triangle mining area. Multi-disciplinary firms with environmental scientists, quantity surveyors, and regulatory specialists gain a clear edge. Single-discipline boutiques face rising compliance hurdles and longer bid-lead times.

Gulf Sovereign Wealth Fund Inflows

ADQ’s USD 35 billion Ras El Hekma and Qatari Diar’s USD 29.7 billion Alam Al-Roum resorts apply International Finance Corporation environmental and social standards. Projects must also meet LEED or SITES certification, driving demand for consultants skilled in global sustainability frameworks. Lenders require detailed stakeholder-engagement records and construction environmental management plans. Egyptian developers pursuing institutional capital adopt similar governance, so international-standard advisory becomes a qualifying hurdle even for local projects exceeding USD 100 million. Smaller domestic practices without cross-border credentials struggle to win prime roles.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EGP volatility and imported-input inflation erode feasibility contingencies | -1.2% | National, with acute pressure on projects with hard-currency obligations | Short term (≤ 2 years) |

| Engineer out-migration tightens skilled-staff availability and labor cost | -0.9% | National, with concentration in Greater Cairo, Alexandria | Medium term (2-4 years) |

| Heritage-site approvals delay brownfield timelines in the Nile Delta | -0.5% | Nile Delta, Greater Cairo, Alexandria, Upper Egypt heritage zones | Medium term (2-4 years) |

| Lack of English text for 2021 PPP-Law amendments raises legal-advisory uncertainty | -0.3% | National, with an impact on international consultancies and foreign investors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EGP Volatility and Imported-Input Inflation

The Egyptian pound moved from EGP 30.85 per USD in January 2024 to EGP 52.34 in March 2026, then settled near EGP 29.76 by April 2026 after a Central Bank intervention[3]Central Bank of Egypt, “Monthly Statistical Bulletin April 2026,” cbe.org.eg . Contingency buffers of 10-15% in feasibility studies proved inadequate as software licenses, specialist equipment, and foreign experts are all dollar-denominated. Domestic firms' local-currency billing saw margins narrow sharply. International consultancies invoicing in USD gained relative pricing power. Many projects required scope rescoping mid-cycle, straining client-consultant relations and extending delivery schedules.

Engineer Out-Migration and Wage Inflation

Gulf labor markets pay senior Egyptian engineers two to three times domestic rates. Remittances hit USD 36.5 billion in FY 2024/25, underscoring the scale of talent flight. Consultancies now raise salaries by 15-20% annually to keep project managers, seismic specialists, and quantity surveyors. Smaller practices struggle to absorb wage spikes on fixed-price contracts. The Mehany 2030 training program focuses on entry-level technicians, leaving a skills gap at the mid-career level, which is crucial for complex infrastructure. Staffing shortages lengthen proposal timelines and curb the capacity of the Egypt construction consulting market to service overlapping mega-projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Master Planning Gains Momentum

Project Management Consultancy held 39.58% share of the Egypt construction consulting market in 2025. High-profile examples include Hill International’s oversight of the USD 4.4 billion Cairo Metro Line 3 extension. Master Planning and Other Services is on track for a 9.3% CAGR to 2031 as developers front-load design to avoid downstream change orders. The Egypt construction consulting market size for master-planning work is therefore expanding faster than the traditional PMC pool. Golden License rules require detailed feasibility files and embed master planners early in the value chain.

The Spine in Greater Cairo, budgeted at USD 28.2 billion, demonstrates this shift. Consultants harmonized zoning, utilities, and transit links before tower blueprints began. Digital twins such as Dar Al-Handasah’s PARA OS shorten design cycles and support predictive maintenance once assets go live. Clients now expect BIM-based quantity take-offs and 4D scheduling as standard. Firms that invest in these tools win repeat mandates, while laggards risk sub-contractor status.

By Sector: Residential Consulting Accelerates

Infrastructure and civil works accounted for 37.8% of 2025 spending in the Egypt construction consulting market. Residential consulting, however, is projected to post the fastest 9.25% CAGR through 2031 on the back of 310,000 housing units targeted for FY 2025/26. The Egypt construction consulting market size tied to housing continues to widen as the government pursues the “Housing for All Egyptians” program. The consulting scope spans architectural design, structural engineering, and mechanical, electrical, and plumbing coordination.

Demand also rises from the private middle-income and luxury brackets. Programs like “Diarna” and “Zilal” add tens of thousands of units across multiple cities. Value engineering and modular construction save cost without sacrificing quality, key to meeting price-sensitive social-housing goals. Parallel growth in data centers following the 2025 Data Sovereignty Decree requires consultants able to plan Tier III cooling, UPS redundancy, and high-density rack layouts.

By Construction Type: Renovation Consulting Picks Up

New builds accounted for 94.5% of 2025 activity, yet renovation mandates will grow at a 10.5% CAGR through 2031. Code ECP-201 updates are expected to align with Eurocode 8 seismic rules, forcing retrofits of hospitals, schools, and public offices erected before 2012. The Egypt construction consulting market share for renovation work will therefore grow from a small base. Heritage sites need structural reinforcement and facade renewal without damaging the cultural fabric, which increases the complexity of the consultation.

Smart-building retrofits add further momentum. The first wave of New Administrative Capital towers now requires energy-efficiency upgrades and digital building management systems. Dar Al-Handasah’s Cairo living lab proved that sensor-based maintenance can cut energy use 28% and speed repairs 40%. Consultants that pair structural expertise with IoT analytics win the lion’s share of these projects.

By Investment Source: Private Capital Gains Ground

Public clients drove 70% of 2025 outlays, anchored by the Ministry of Housing’s housing drive and power-grid upgrades. Private projects are expected to record a 10.1% CAGR to 2031 as PPP amendments and single-window licenses slash red tape. The Egypt construction consulting industry, therefore, tilts toward developers who mix foreign equity with domestic land contributions.

Mega-deals with sovereign wealth funds blur public-private lines. Ras El Hekma and Alam Al-Roum combine state land, Gulf equity, and multilateral debt. Consultancies help craft governance that satisfies all stakeholders and negotiate performance-based concessions. Public programs still secure baseline workloads, providing cyclical stability for firms anchored in government housing and sanitation schemes.

Geography Analysis

Greater Cairo accounted for 45.6% of Egypt's construction consulting market revenues in 2025 and is forecast to post a 9.5% CAGR through 2031. The New Administrative Capital continues to award master-planning and supervision contracts as ministries relocate. The East Nile Monorail, opened in March 2026, sustains multi-year advisory fees. Talaat Moustafa Group’s USD 28.2 billion Spine project, the first Special Investment Zone, generates work across zoning, utilities, and sustainability audits. A 2.5 million square-meter office stock and rising tenant-fit-out demand lock in pipeline visibility.

Alexandria and Giza together captured about 30% of the 2025 spend. Alexandria’s USD 750 million metro Phase 1 relies on independent engineering oversight to meet lender covenants. Giza Zoo’s redevelopment shows how tourism and heritage assets open niche design roles. Financial services decentralization sparks head-office projects in New Cairo, including interior architecture and LEED consulting.

The rest of the country, including Upper Egypt, Sinai, and the Red Sea, took 24% of 2025 fees, yet shows upside. The New Delta agricultural venture needs hydrologic modeling and irrigation design over 1 million acres. Ras El Hekma and Alam Al-Roum adopt global ESG standards, enabling consultants with multilingual teams and prior resort experience to win prime positions. Safaga Port expansion and the Four Seasons Luxor illustrate how logistics and hospitality schemes sustain demand beyond Cairo.

Competitive Landscape

The top five international firms, Dar Al-Handasah, AECOM, Hill International, WSP Middle East, and AtkinsRéalis control roughly 25-30% of the Egypt construction consulting market. They differentiate through digital twins, BIM level-3 execution, and global ESG credentials. Domestic leaders such as Shaker Consultancy Group and ECG Engineering balance the equation with lower overheads and deep familiarity with the procedures of the Egyptian Engineers Syndicate.

Technology adoption is the main battleground. More than 50% of consultants deploy 3D modeling; 86% employ 4D scheduling, and 78% use 5D cost estimation, yet contractor uptake lags, creating coordination gaps that consultees fill by offering BIM execution plans. Turner & Townsend’s August 2025 purchase of ValueMetric Consultants underscores foreign appetite for cost-management talent priced in local currency. ISO 9001 and ISO 14001 certifications now gatekeep access to government rosters, and international financiers demand compliance with the Equator Principles.

White-space niches emerge in data centers after the 2025 Data Sovereignty Decree and in seismic retrofits ahead of ECP-201 upgrades. Firms that build teams in these verticals secure above-market growth. Competitive intensity remains moderate, as skill shortages limit rapid new-entrant scaling. That imbalance lets incumbents pass wage inflation into fees, partially insulating margins despite EGP swings.

Egypt Construction Consulting Industry Leaders

Dar Al-Handasah (Shair & Partners)

AECOM Egypt

Hill International Egypt

WSP Middle East – Egypt

AtkinsRéalis (Atkins Egypt)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Hill International provided project-management services for the East Nile Monorail Line 1 opening in Cairo, part of the USD 2.9 billion Cairo Monorail system comprising two lines totaling 106 kilometers, marking Egypt's first monorail transit infrastructure and establishing a template for elevated-guideway consulting mandates in congested urban corridors.

- February 2026: Hassan Allam Holding acquired MetiPro, the engineering-procurement-construction (EPC) arm of Metito, for an undisclosed sum to expand water and wastewater treatment capabilities across Egypt, Middle East and North Africa (MENA), Africa, Commonwealth of Independent States (CIS), and Eastern Europe, positioning the combined entity to capture consulting and construction mandates for the Egyptian Ministry of Housing's EGP 77 billion (USD 1.55 billion) water-infrastructure program.

- August 2025: Turner & Townsend acquired Volumetric Consultants, a Cairo-based cost-management and quantity-surveying practice with approximately 20 staff, for an undisclosed sum, entering the Egypt market and appointing Ayman El-Ghazzawi as Country Manager to lead expansion into public infrastructure and private development advisory.

Egypt Construction Consulting Market Report Scope

| Project Management Consultancy (PMC) |

| Feasibility Studies |

| Detailed Project Reports (DPR) |

| Design and Engineering Services |

| Master Planning and Other Services |

| Residential | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Data Center | |

| Others - Institutional, Hospitality etc. | |

| Infrastructure/Civil | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Social Infrastructure | |

| Others |

| New Construction |

| Renovation |

| Public |

| Private |

| Greater Cairo |

| Alexandria |

| Giza |

| Rest of Egypt |

| By Service Type | Project Management Consultancy (PMC) | |

| Feasibility Studies | ||

| Detailed Project Reports (DPR) | ||

| Design and Engineering Services | ||

| Master Planning and Other Services | ||

| By Sector | Residential | |

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Data Center | ||

| Others - Institutional, Hospitality etc. | ||

| Infrastructure/Civil | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Social Infrastructure | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Investment Source | Public | |

| Private | ||

| By Geography | Greater Cairo | |

| Alexandria | ||

| Giza | ||

| Rest of Egypt | ||

Key Questions Answered in the Report

How large will the Egypt construction consulting market be by 2031?

The Egypt construction consulting market size is forecast to reach USD 10.06 billion by 2031, expanding at an 8.7% CAGR from 2026.

Which segment is growing fastest within the sector?

Master Planning and Other Services is projected to register the quickest 9.3% CAGR as Golden License rules shift value to early-stage advisory.

What is driving private-sector participation?

Amended PPP regulations allow unsolicited bids and standardized contracts, helping private projects grow at a 10.1% CAGR to 2031.

Why is renovation consulting gaining traction?

Expected seismic-code upgrades will make retrofit assessments mandatory, pushing renovation consulting to a 10.5% CAGR through 2031.

Which geography offers the strongest outlook?

Greater Cairo leads with 45.6% of 2025 revenue and is set for a 9.5% CAGR thanks to the New Administrative Capital and transport links.

Page last updated on: