Education Enterprise Content Management (ECM) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.62 Billion |

| Market Size (2031) | USD 3.53 Billion |

| Growth Rate (2026 - 2031) | 16.86% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Education Enterprise Content Management (ECM) Market Analysis by Mordor Intelligence

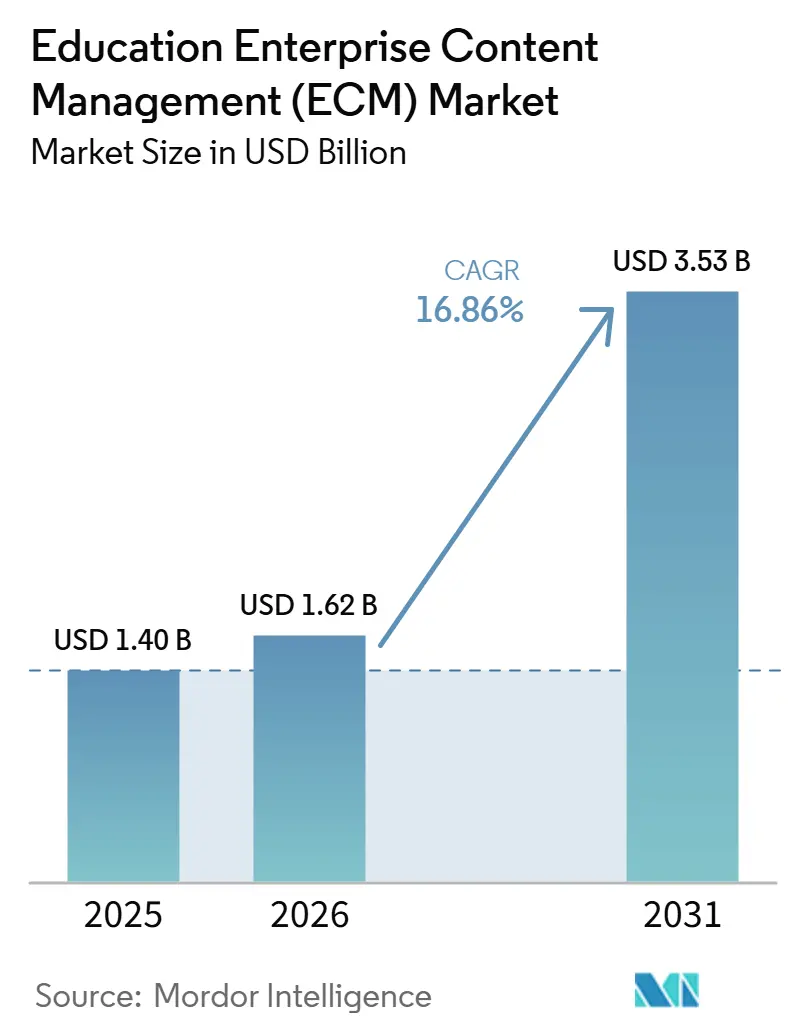

The education enterprise content management (ECM) market size is projected to be USD 1.40 billion in 2025, USD 1.62 billion in 2026, and reach USD 3.53 billion by 2031, growing at a CAGR of 16.86% from 2026 to 2031. Growth is being supported by institutions moving beyond basic file storage and adopting AI-powered search, tagging, and retrieval that make large academic repositories easier to use. The education enterprise content management (ECM) market is also benefiting from multi-campus cloud migration programs that bring scattered records, workflows, and archives into a single governed environment. Demand is rising because institutions want tighter integration among ECM platforms, learning management systems, student information systems, and enterprise resource planning software, enabling content to move through the student lifecycle with less manual work. Compliance duties around student records, accessibility, audit trails, and retention are pushing buyers toward platforms with stronger governance built into daily workflows. Opportunities remain strongest where digital credentials, professional learning content, and regional digitization programs are expanding, while vendors compete by combining AI features, Microsoft alignment, and education-specific policy controls.

Key Report Takeaways

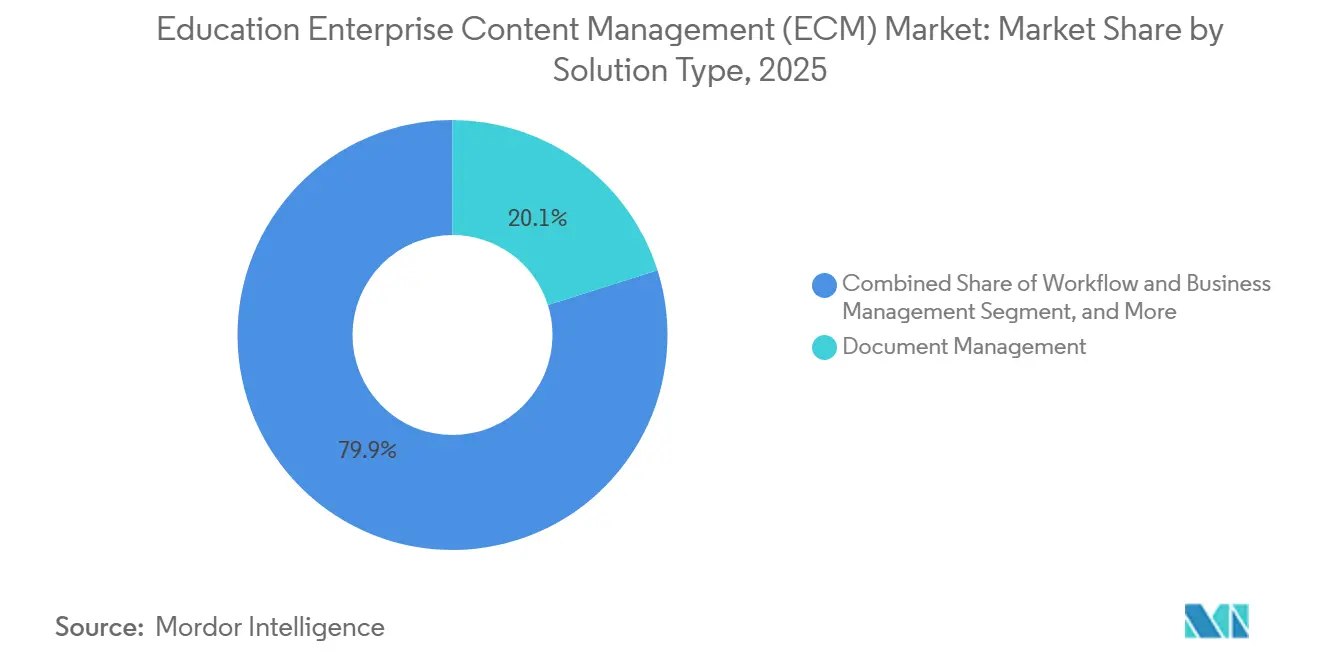

- By solution type, document management led with 20.14% revenue share in 2025, while workflow and business process management is projected to expand at a 19.42% CAGR through 2031.

- By deployment mode, cloud held 74.41% share of the education enterprise content management (ECM) market in 2025, while cloud is also projected to record the fastest growth at 18.83% through 2031.

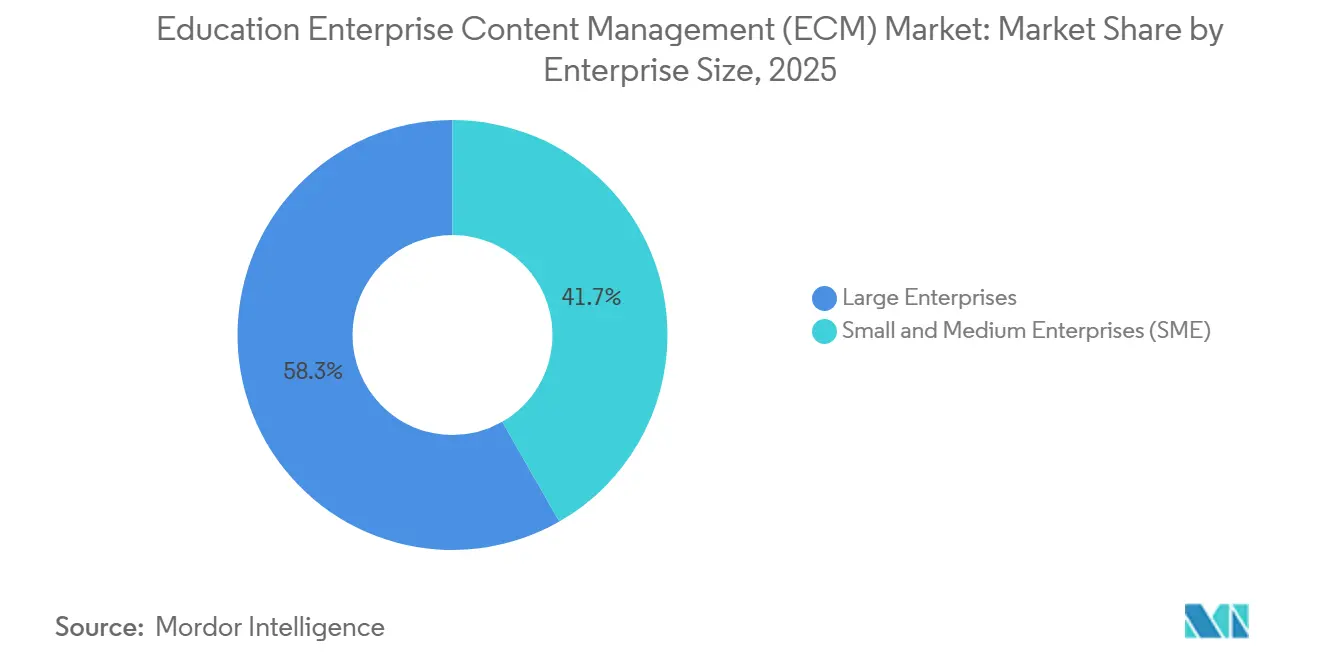

- By enterprise size, large enterprises accounted for 58.28% of the market share in 2025, while small and medium enterprises are projected to expand at a 18.64% CAGR through 2031.

- By institution type, higher education captured 42.16% share in 2025, while corporate and professional education is projected to grow at a 19.91% CAGR through 2031.

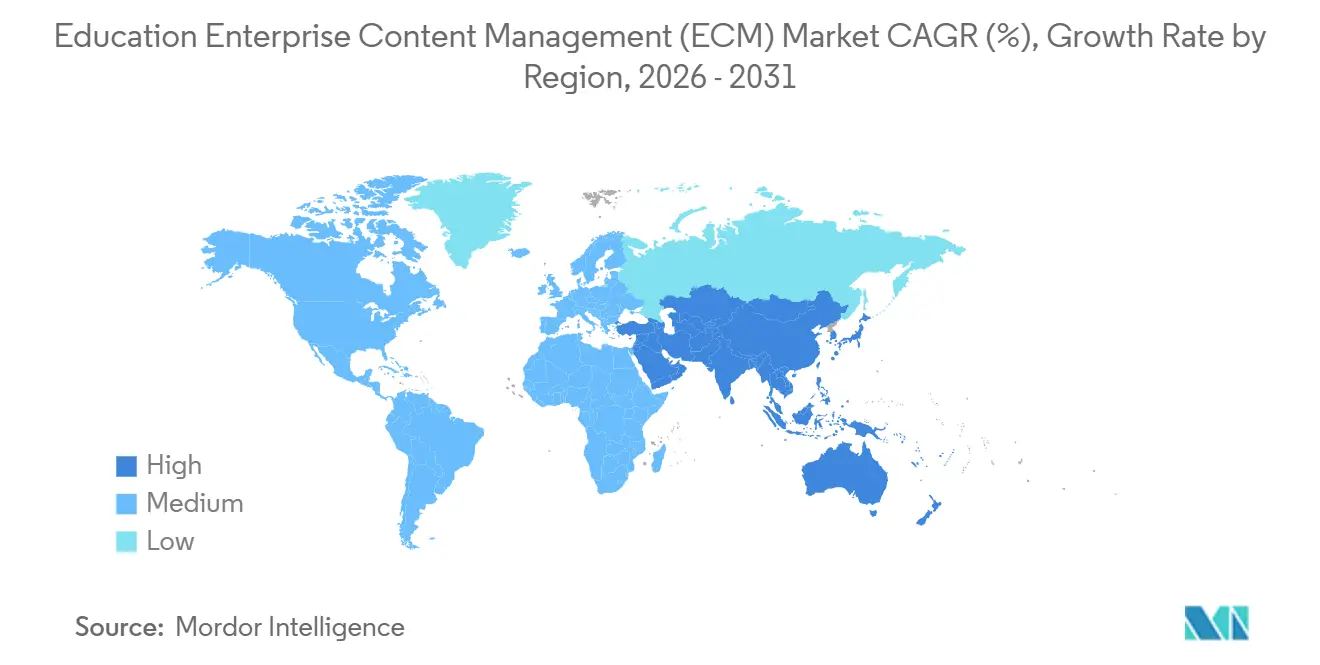

- By geography, North America held 41.14% of the education enterprise content management (ECM) market share in 2025, while the Asia-Pacific is projected to expand at a 19.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Education Enterprise Content Management (ECM) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Driven Content Search, Tagging, and Retrieval | +2.8% | Global | Short term (≤ 2 years) |

| Multi-Campus Cloud Migration for Unified Governance | +2.3% | North America and Europe | Short term (≤ 2 years) |

| Interoperability Across ECM, LMS, SIS, and ERP Platforms | +1.9% | Global | Medium term (2-4 years) |

| Record Retention, Auditability, and Accessibility Compliance | +1.6% | North America and Europe | Short term (≤ 2 years) |

| Growth In Digital Credentials and Assessment Repositories | +1.4% | Global | Medium term (2-4 years) |

| Research Data, Grant Documentation,and Knowledge Preservation | +1.0% | North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Driven Content Search, Tagging, and Retrieval in Learning Workflows

AI search and tagging are changing how the education enterprise content management (ECM) market serves faculty, administrators, and students. Semantic retrieval lets users query archived content in plain language instead of relying on rigid keyword rules. IBM launched the Content Cortex Essentials Edition in June 2026, featuring AI agents that classify, organize, and update documents at very high ingestion volumes while preserving security and governance.[1]IBM, “A New Era of Agentic Content Automation Has Arrived with IBM Content Cortex Essentials Edition,” IBM Community, community.ibm.com In the education enterprise content management (ECM) market, that kind of automation matters most for research universities and large education systems that manage grant files, course materials, and archives in many formats. The result is that content repositories are becoming more usable as living institutional knowledge bases rather than passive storage systems.

Multi-Campus Cloud Migration for Unified Content Governance

Cloud migration is accelerating because the education enterprise content management (ECM) market now faces governance fragmentation across campuses, departments, and satellite sites. Institutions are using cloud programs to standardize policies, improve content access, and reduce dependence on separate local repositories. The University of Maryland Libraries completed a full data center cloud migration on AWS in 2025, moving 95 TB of storage and shutting down all on-campus data center operations in less than 6 months.[2]Amazon Web Services, “Reimagining University Libraries with AWS, University of Maryland's Six-Month Cloud Migration,” AWS Public Sector Blog, aws.amazon.com Hyland strengthened this direction in June 2026 by bringing its Content Innovation Cloud to Microsoft Azure with geography-specific data residency options and Microsoft Marketplace availability. In the education enterprise content management (ECM) market, cloud consolidation is therefore becoming a governance redesign program rather than just an infrastructure change.

Interoperability Pressure Between ECM, LMS, SIS, and ERP Platforms

Interoperability pressure is becoming one of the clearest demand drivers in the education enterprise content management (ECM) market. Institutions want content to move easily between academic, administrative, and finance systems without the need for repeated manual uploads or custom workarounds. EDUCAUSE found that 67% of institutions cited system integration as their top technology challenge in 2024, with LMS and ERP integration most often cited.[3]EDUCAUSE, “LMS Integration Strategies for Universities, Connecting Learning Platforms with Campus ERP,” EDUCAUSE, educause.edu The LTI 1.3 Advantage standard from 1EdTech is helping normalize deep linking, roster sync, and grade passback across education platforms. As the education enterprise content management (ECM) market matures, buyers are placing greater value on proven integrations, which improve admissions turnaround, service response, and operational consistency across the student lifecycle.[4]1EdTech Consortium, “Learning Tools Interoperability (LTI),” 1EdTech, 1edtech.org

Record Retention, Auditability, and Accessibility Compliance for Student Content

Compliance has become a steady growth engine for the education enterprise content management (ECM) market because institutions now treat student content governance as an operational requirement. Schools need stronger control over who can access records, how long they are kept, and how every action is logged. FERPA continues to anchor this need in the United States by requiring clear controls around student education records and privacy protections. In the education enterprise content management (ECM) market, platforms with built-in retention rules, audit trails, and consent management are therefore gaining an advantage over simple document storage tools. This also raises the value of accessibility support, as institutions increasingly want a single, unified system that can support records, evidence files, and student-facing documentation without policy gaps.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Stack Integration Complexity Across Campus Systems | -2.3% | Global | Medium term (2-4 years) |

| Budget Cycles and Public Procurement Delays | -1.8% | Global | Short term (≤ 2 years) |

| Data Residency, Privacy, and Student Consent Constraints | -1.2% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Faculty And Administrator Resistance to Content Standardization | -0.7% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy Stack Integration Complexity Across Campus Systems

Legacy systems remain a major brake on the education enterprise content management (ECM) market because many institutions still run older SIS, ERP, and records systems built in isolation. These systems often have limited interfaces, proprietary data structures, and deeply embedded departmental workflows. EDUCAUSE reported that system integration remained the top technology challenge for institutions, which shows why ECM rollouts still face technical friction even when demand is strong. In the education enterprise content management (ECM) market, migration is difficult because schools must redesign processes and integrate software. This extends deployment timelines and increases the risk that institutions adopt governance tools only partially.

Budget Cycles and Public Procurement Delays in Education Institutions

Budget timing also slows the education enterprise content management (ECM) market, as many public institutions make technology decisions through lengthy funding and approval cycles. Annual or multi-year appropriations do not always match the release pace of modern subscription platforms. EDUCAUSE found in 2025 that 42% of institutions expected IT budget decreases for the 2025-2026 academic year, with a median expected reduction of 8%. In the education enterprise content management (ECM) market, this pushes vendors to frame value in terms of compliance risk reduction, labor savings, and service improvement rather than feature novelty alone. The result is slower conversion from interest to contract, especially in public higher education and budget-sensitive school systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Document Management Anchors The Foundation

Document management accounted for 20.14% of the education enterprise content management (ECM) market in 2025, making it the largest solution category. Its lead reflects the need for a reliable layer that can capture, store, retrieve, and control admissions files, financial aid records, contracts, transcripts, and accreditation evidence before wider automation is added. In the education enterprise content management (ECM) market, this category stays central because institutions usually cannot standardize approvals, retention, or case workflows until core document control is in place. California Baptist University used Laserfiche to support a paperless registrar and accounting environment while integrating record access with Banner SIS, demonstrating how document management often serves as the starting point for broader institutional workflow improvement.

Workflow and business process management is projected to expand at a 19.42% CAGR through 2031, making it the fastest-growing solution type in the education enterprise content management (ECM) market. Schools are automating admissions routing, financial aid verification, student conduct handling, staff onboarding, and other processes where delays affect service quality and enrollment outcomes. Digital asset management is also gaining importance as institutions manage larger libraries of video lessons, simulations, and interactive content that require version control and rights oversight. Web content management is drawing renewed attention as the education enterprise content management (ECM) market moves toward unified governance across public websites, intranets, student portals, and learning platforms.

By Deployment Mode: Cloud Consolidation Reshaping Procurement

Cloud accounted for 74.41% of the education enterprise content management (ECM) market in 2025, making it the dominant deployment model. Institutions value cloud delivery because it supports common access across campuses, stronger disaster recovery, and less local infrastructure maintenance. In the education enterprise content management (ECM) market, cloud is also helping schools better manage governance across distributed operations and remote learning environments. Hyland and OpenText have both emphasized cloud environments that address residency and governance needs at the infrastructure and content-control level.

Cloud is also projected to expand at a 18.83% CAGR through 2031, keeping it the fastest-growing deployment model in the education enterprise content management (ECM) market. On-premises systems remain in use where national rules or internal policies limit off-site storage of student data. Hybrid setups are gaining ground among research-heavy institutions that want to keep some sensitive workloads in local environments while moving administrative content into managed cloud services. EDUCAUSE noted that cloud-based services are expected to manage a larger share of higher education IT environments over the next few years, which supports continued cloud-led procurement in the education enterprise content management (ECM) market.

By Enterprise Size: Large Institutions Lead, SMEs Accelerating

Large enterprises held a 58.28% share in 2025, giving them the leading position in the education enterprise content management (ECM) market. Multi-campus universities, large school districts, and enterprise-scale learning organizations face higher record volumes, more complex policy needs, and broader integration requirements than smaller institutions. That scale makes them more likely to deploy full ECM suites that include document management, retention controls, workflow automation, and digital asset governance. Hyland said in March 2026 that 65% of higher education CIOs cited outdated SIS environments as their top digital transformation barrier, which helps explain why large organizations are using the education enterprise content management (ECM) market to strengthen process continuity around legacy core systems.

Small and medium enterprises are projected to expand at an 18.64% CAGR through 2031, making them the fastest-growing size segment in the education enterprise content management (ECM) market. Community colleges, independent schools, training providers, and smaller online learning organizations are shifting from ad hoc document handling to formal content governance as SaaS platforms lower implementation barriers. Softdocs supported that trend in April 2026 by adding compliant electronic signatures for ad hoc PDFs and removing per-envelope signature fees, which reduced cost friction for smaller institutions. The education enterprise content management (ECM) market is also drawing first-time SME buyers that need auditable repositories for digital credentials, compliance files, and learner evidence records.

By Institution Type: Higher Education Commands The Largest Share

Higher education accounted for 42.16% of the education enterprise content management (ECM) market in 2025, making it the largest institution segment. Universities manage a broad mix of research files, grant records, student records, accreditation evidence, admissions content, and library material that all require different access and retention rules. In the education enterprise content management (ECM) market, this complexity is heightened by the number of stakeholders involved, as faculty, administrators, students, researchers, and external reviewers each need different levels of access. OpenText demonstrated this kind of large-scale use case through its work with the UAE Higher Colleges of Technology, where Documentum enabled a broader zero-bureaucracy transformation across campuses.

Corporate and professional education is projected to grow at a 19.91% CAGR through 2031, making it the fastest-growing segment of the education enterprise content management (ECM) market. Enterprise learning teams need structured content repositories because skills content changes quickly, compliance training expands regularly, and organizations want better version control over learning assets. K-12 demand is also advancing as districts build more formal digital document and curriculum governance, especially where AI-supported instruction is being introduced at scale. Discovery Education said in March 2026 that its Connected Ecosystem was already trusted by 45% of U.S. K-12 schools, signaling that the education enterprise content management (ECM) market is moving toward more unified governance of instructional content and school workflows.

Geography Analysis

North America held 41.14% of the education enterprise content management (ECM) market share in 2025, making it the largest regional market. The region benefits from a dense base of institutions, a mature enterprise software ecosystem, and strong privacy and accessibility expectations that make governed content systems more necessary than simple storage tools. Microsoft expanded this environment further in June 2026 by introducing new AI-powered teaching capabilities in Microsoft 365 Education and linking them to Canvas, Brightspace, Moodle, and Schoology via LTI integrations. In the education enterprise content management (ECM) market, North America also remains a key testing ground for workflow improvements, as institutions seek faster approvals, cleaner audit trails, and better coordination across academic and administrative systems.

Asia-Pacific is projected to expand at a 19.24% CAGR through 2031, which makes it the fastest-growing region in the education enterprise content management (ECM) market. India’s National Education Policy 2020 digital infrastructure push is shaping procurement cycles across universities and colleges in 2025 and 2026. Many institutions across the region are moving from paper-heavy records environments to governed cloud repositories that can support student services and digital learning growth. Europe remains an important region in the education enterprise content management (ECM) market because privacy rules, records retention requirements, and research documentation standards continue to favor auditable content systems. The NIH updated the format requirements for Data Management and Sharing Plan submissions, effective May 25, 2026, reinforcing more formal research documentation practices for universities active in global research networks.

South America, the Middle East, and Africa remain smaller in scale, but each is carving out a distinct path in the education enterprise content management (ECM) market. Brazil and Argentina are leading South American adoption as universities continue to digitize administrative records and reduce dependence on paper-heavy processes. The UAE Higher Colleges of Technology used OpenText Documentum to support a zero-bureaucracy transformation across campuses, which shows how national modernization agendas are shaping the education enterprise content management (ECM) market in the Middle East. African adoption remains at an earlier stage and leans toward a cloud-first approach, which lets institutions gain governance capabilities without a major on-premises buildout.

Competitive Landscape

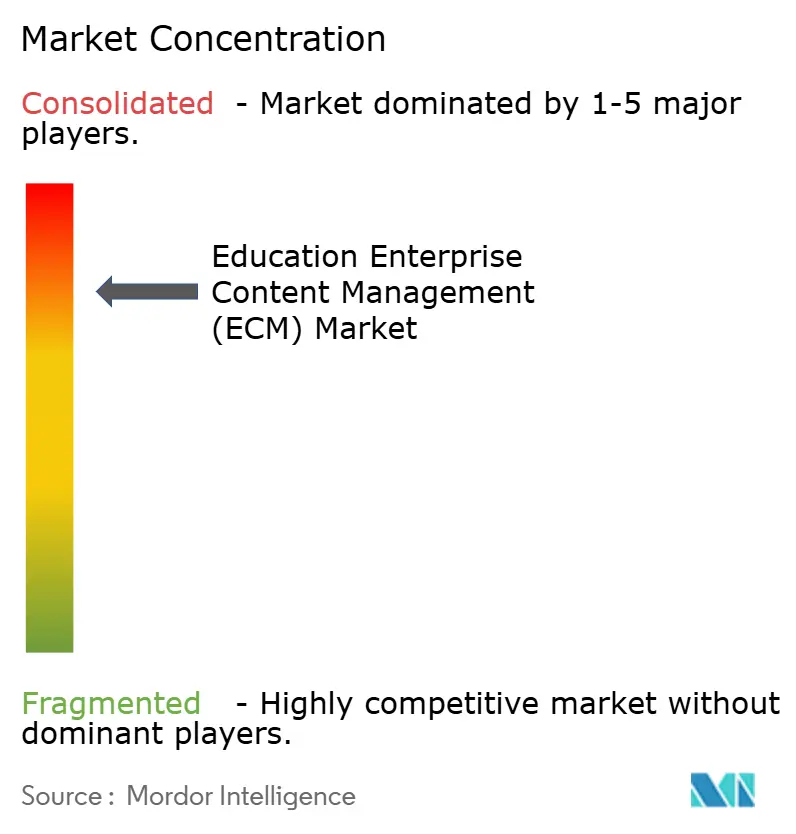

The education enterprise content management (ECM) market remains consolidated, with OpenText, Hyland, IBM, and Microsoft competing alongside education-focused specialists such as Laserfiche, DocuWare, and Anthology. In the education enterprise content management (ECM) market, vendors are distinguishing themselves through AI-enabled governance, close alignment with Microsoft, and deeper education compliance support. Hyland strengthened that position in June 2026 when it partnered with Microsoft to bring the Content Innovation Cloud to Azure with geography-specific data residency options and Microsoft Marketplace availability. OpenText reinforced the same direction in 2026 by extending governed content workflows and Microsoft 365 support in its Content Cloud roadmap. IBM also moved the category forward in June 2026 by packaging AI document classification and organization into Content Cortex Essentials Edition.

Laserfiche remains a credible option for K-12 districts and regional universities because its platform pairs document control with education workflow use cases, and California Baptist University used it to support a paperless registrar and accounting environment. Softdocs is pushing the education enterprise content management (ECM) market further into the SME segment by removing per-envelope signature fees and simplifying compliant document workflows. Microsoft is not a pure-play ECM vendor in this niche, but its Microsoft 365 Education integrations are shaping the collaboration layer around which many content platforms now need to work. That shift favors vendors that blend into everyday institutional systems rather than requiring schools to manage content in separate tools.

Newer competitors are focusing on narrow pain points such as admissions document extraction, archive intelligence, and content unification across learning systems. Kortext earned Microsoft Solutions Partner status with the certified software for Education AI designation in April 2026, demonstrating how vendors are combining content, data, and AI within a single governance framework. Ruanyun Edai Technology expanded Cogni AI in June 2026 to cover institutional records, learning materials, and legacy archives, adding another document intelligence option to the education enterprise content management (ECM) market. The result is a field where large vendors defend installed relationships while specialists pursue faster growth through focused education and use cases.

Education Enterprise Content Management (ECM) Industry Leaders

Microsoft Corporation

Adobe Inc.

OpenText Corporation

IBM Corporation

Hyland Software, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: IBM launched Content Cortex Essentials Edition on June 29, 2026, the successor to IBM FileNet Content Manager, introducing pre-packaged AI agents capable of classifying, organizing, and updating documents at ingestion rates of hundreds of millions of sections per day. The platform extended agentic content automation while maintaining enterprise-grade security, governance, and scalability with compatibility APIs for legacy FileNet applications.

- June 2026: Hyland announced a strategic partnership with Microsoft on June 1, 2026 to bring the Hyland Content Innovation Cloud to Microsoft Azure, enabling governed enterprise content management within the Azure ecosystem. The partnership added geography-specific data residency options, deep Microsoft 365 integrations, and Microsoft Marketplace availability for regulated sectors including education and government.

- April 2026: Kortext fusion earned the Microsoft Solutions Partner with certified software for Education AI designation on April 28, 2026, among the first purpose-built higher education applications to achieve this recognition. Built on Microsoft Fabric and Azure AI Foundry, the platform unifies institutional content, data, and AI within a single governance foundation, integrating directly with institutional learning systems and workflows.

- April 2026: Softdocs released its Spring 2026 Etrieve platform update on April 27, 2026, introducing fully compliant electronic signatures for ad hoc PDFs and enhanced search functionality with saved search management. The release eliminated per-envelope signature fees, reducing compliance costs for smaller K-12 and higher education institutions operating under budget constraints.

Global Education Enterprise Content Management (ECM) Market Report Scope

The education enterprise content management (ECM) market comprises software solutions and services that systematically capture, manage, store, preserve, and deliver unstructured and structured content within educational institutions and related organizations. This includes technologies such as document and records management, workflow and business process automation, case management, digital asset management, and web content management. Deployed on-premises, in the cloud, or in hybrid models, these solutions cater to organizations of varying sizes across institution types, including K-12 schools, higher education universities, corporate and professional training centers, and government or non-profit educational bodies. Driven by the rapid digitalization of learning environments, the need for secure student records management, stringent regulatory compliance (such as FERPA or GDPR), and the shift to hybrid administrative operations, ECM solutions enable educational institutions to eliminate paper-based processes, streamline admissions and faculty workflows, enhance collaboration, and improve overall operational efficiency.

The Education Enterprise Content Management (ECM) Market Report is Segmented by Solution Type (Document Management, Records Management, Workflow and Business Process Management, Case Management, Digital Asset Management, Web Content Management, and Other Solutions), Deployment Mode (On-Premises, Cloud, and Hybrid), Enterprise Size (Small and Medium Enterprises (SME), and Large Enterprises), Institution Type (K-12, Higher Education, Corporate And Professional Education, and Government and Non-Profit), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Document Management |

| Records Management |

| Workflow and Business Process Management |

| Case Management |

| Digital Asset Management |

| Web Content Management |

| Other Solutions |

| On-Premises |

| Cloud |

| Hybrid |

| Small and Medium Enterprises (SME) |

| Large Enterprises |

| K-12 |

| Higher Education |

| Corporate And Professional Education |

| Government and Non-Profit |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Solution Type | Document Management | |

| Records Management | ||

| Workflow and Business Process Management | ||

| Case Management | ||

| Digital Asset Management | ||

| Web Content Management | ||

| Other Solutions | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| Hybrid | ||

| By Enterprise Size | Small and Medium Enterprises (SME) | |

| Large Enterprises | ||

| By Institution Type | K-12 | |

| Higher Education | ||

| Corporate And Professional Education | ||

| Government and Non-Profit | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast size of the education enterprise content management (ECM) market?

The education enterprise content management (ECM) market stands at USD 1.62 billion in 2026 and is projected to reach USD 3.53 billion by 2031, growing at a 16.86% CAGR.

Which deployment model leads education ECM adoption?

Cloud leads the category with a 74.41% share in 2025 and is also the fastest-growing deployment model with an 18.83% CAGR through 2031.

Which institution group generates the largest demand for education ECM platforms?

Higher education holds the largest institution share at 42.16% in 2025 because universities manage complex records across admissions, accreditation, research, and student services.

Which region is growing the fastest in education ECM?

Asia-Pacific is the fastest-growing region, with a projected 19.24% CAGR through 2031, supported by digitization programs and expanding education infrastructure.

Why are schools and universities shifting to cloud-based content management?

Institutions want unified governance across campuses, stronger disaster recovery, lower infrastructure burden, and better access to records and workflows across distributed operations.

How is AI changing vendor competition in this space?

AI is moving ECM from basic storage toward semantic search, automated classification, and content intelligence, which is pushing vendors to compete on usability, governance depth, and integration quality.

Page last updated on: