Edge AI GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.01 Billion |

| Market Size (2031) | USD 20.09 Billion |

| Growth Rate (2026 - 2031) | 37.99% CAGR |

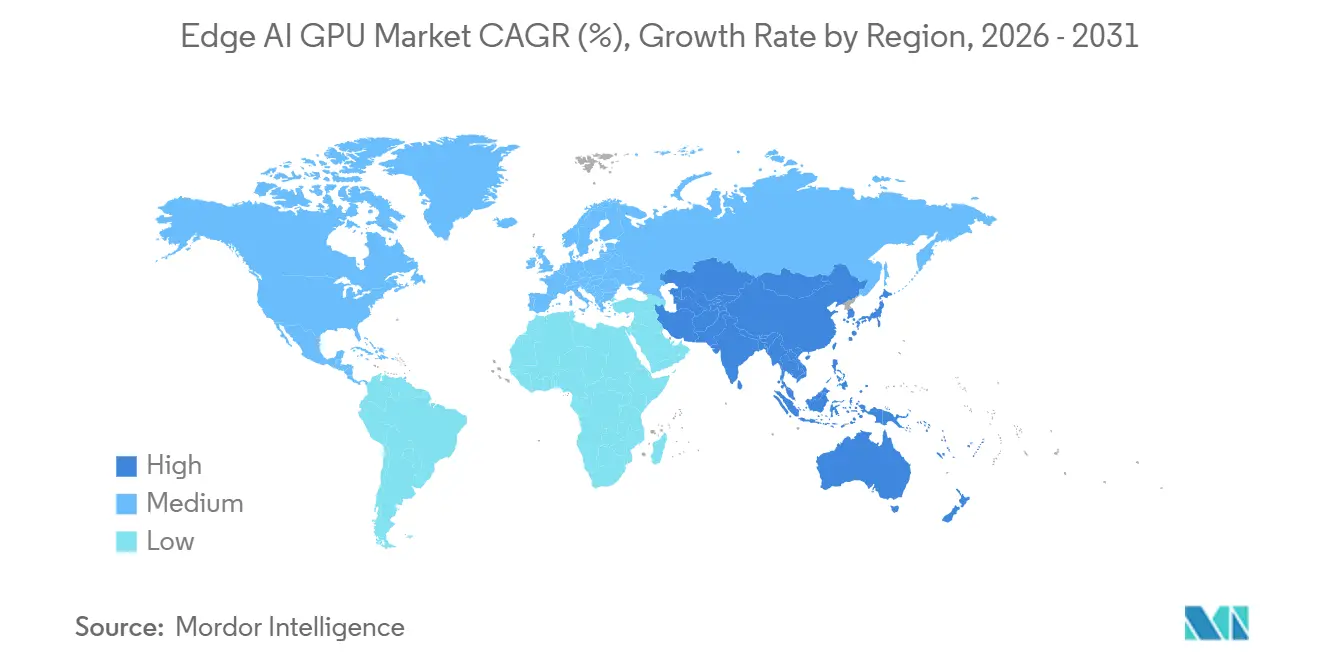

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Edge AI GPU Market Analysis by Mordor Intelligence

The edge AI GPU market size expanded from USD 2.97 billion in 2025 to USD 4.01 billion in 2031, registering a 37.99% CAGR from 2026 to 2031. Asia-Pacific accounted for 66.71% of global revenue in 2025, with integrated GPUs accounting for 61.59% of that share that year. Sovereign-AI mandates in the European Union and India, together with a significant share of global penetration of standalone 5G, accelerated on-premises inference, pushing enterprises toward lower-latency, GPU-powered edge nodes. Design wins for NVIDIA’s Jetson Orin among autonomous-robot OEMs, Intel’s Arc A-series trials at HPE and Dell, and venture backing for Hailo and Kneron illustrate a shift from single-vendor dominance toward heterogeneous silicon roadmaps. Supply-chain pressure at advanced-packaging foundries, coupled with 85 °C ambient thermal ceilings in industrial enclosures, threatens near-term product availability but also propels investment in chiplet layouts and sparse-matrix firmware.

Key Report Takeaways

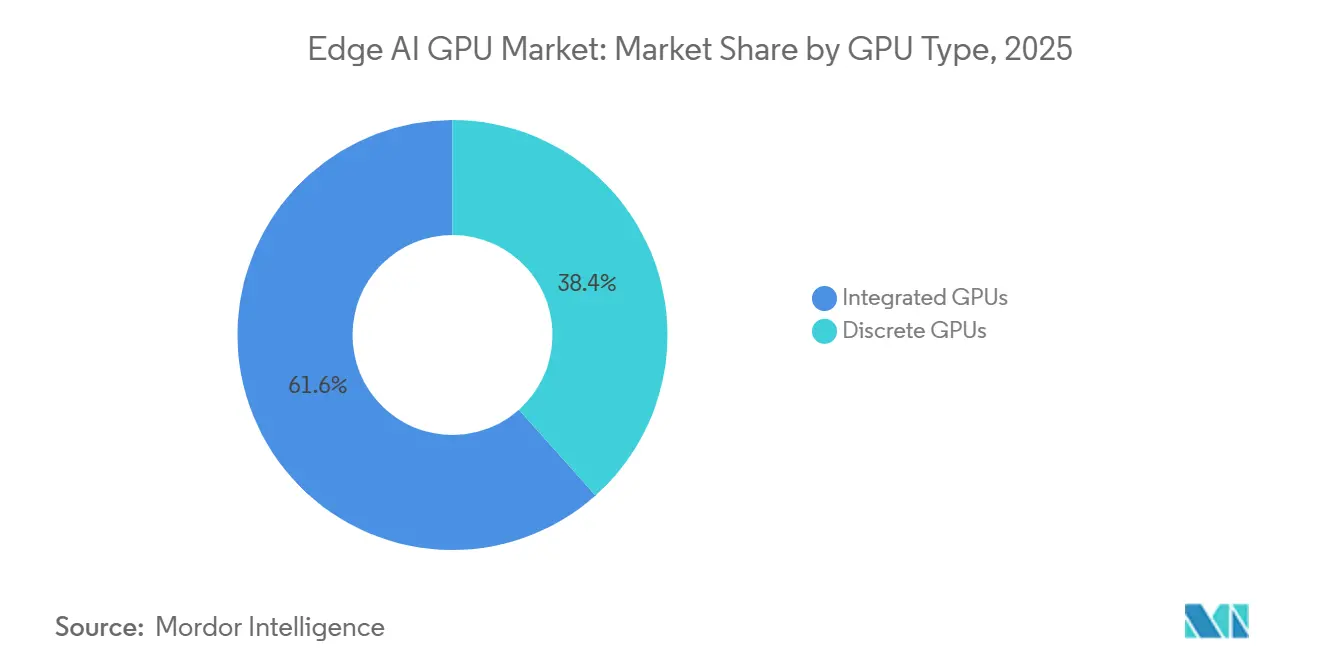

- By GPU type, integrated solutions led the edge AI GPU market with 61.59% market share in 2025.

- By deployment type, embedded devices accounted for 60.11% share of the edge AI GPU market size in 2025 and are projected to expand at a 38.91% CAGR between 2026 and 2031.

- By application, robotics and automation are advancing at a 38.67% CAGR through 2031.

- By region, Asia-Pacific accounted for 66.71% of revenue in 2025 and is forecast to grow at a 38.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Edge AI GPU Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Proliferation of IoT devices requiring low-latency AI processing | +8.2% | Global, especially Asia-Pacific manufacturing hubs and North American smart cities | Medium term (2-4 years) |

| Rapid deployment of 5G, enhancing edge bandwidth | +7.5% | Asia-Pacific core, spillover to Europe and the Middle East | Short term (≤ 2 years) |

| Rising demand for real-time video analytics in smart cities | +6.8% | Asia-Pacific, Europe, North America | Medium term (2-4 years) |

| Growing adoption of autonomous mobile robots in manufacturing | +5.9% | Asia-Pacific, North America, Europe | Medium term (2-4 years) |

| Regulatory push for data privacy favors on-device processing | +4.7% | Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| Emergence of cold-chain edge nodes in pharmaceutical logistics | +3.1% | North America and Europe corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of IoT Devices Requiring Low-Latency AI Processing

The global installed base of IoT endpoints needing on-device inference surpassed 15 billion units in 2025, forcing enterprises to abandon cloud-centric workflows. Round-trip latency of 80-120 milliseconds is incompatible with closed-loop robotics, surgical equipment, and industrial process control. Deploying GPU inference at the sensor collapses latency to under 5 milliseconds and cuts cycle times for collaborative robots by 40% in ABB field trials.[1]ABB Group, “Collaborative Robots Field Trial Results,” abb.com Vendors now build 5 nm SoCs with dynamic voltage scaling to keep power under 15 watts, aligning with fanless industrial designs. The trend materially expands addressable edge AI GPU market demand across automotive lines, medical devices, and smart utilities.

Rapid Deployment of 5G Enhancing Edge Bandwidth

Standalone 5G deployments expanded significantly by mid‑2025, enabling network slices that deliver sub‑10‑millisecond paths for edge inference. South Korean operators completed nationwide rollouts in 2024, supporting more than 2,000 GPU nodes at Seoul’s Guro Digital Complex for real‑time quality inspection.[2]GSMA, “Standalone 5G Economics,” gsma.com The European Union earmarked EUR 900 million (USD 1.01 billion) in 2025 to seed similar deployments, compelling carriers to co-locate GPU servers at base-station shelters. While the USD 150,000 CAPEX per standalone cell remains high in emerging economies, the value proposition for latency-sensitive analytics is now proven, widening the adoption of edge AI GPUs in telecom ecosystems.

Rising Demand for Real-Time Video Analytics in Smart Cities

More than 1.2 billion surveillance cameras were operating worldwide by end-2025, yet less than 8% of footage underwent automated review. Edge AI GPUs perform detection locally, sending only alerts to control centers, reducing backhaul volume. China mandated GPU-accelerated analytics in all new municipal installs from 2024, while the United Kingdom committed GBP 120 million (USD 152 million) in 2025 for London transit retrofits.[3]Ministry of Public Security China, “Smart-City Surveillance Mandate,” mps.gov.cn Transformer-based vision models that require triple the compute of CNNs now push municipalities toward higher-end discrete GPUs, expanding the edge AI GPU market base within public safety and transportation networks.

Growing Adoption of Autonomous Mobile Robots in Manufacturing

Manufacturers installed over 180,000 autonomous mobile robots in 2025, all of which rely on GPU-accelerated SLAM for navigating dynamic floors. Tesla’s Austin factory rolled out 400 Jetson Orin robots for intra-plant logistics in 2025, reducing floor space needs by 18%.[4]Tesla Inc., “Gigafactory Austin Robotics Deployment,” tesla.comBoston Dynamics’ Stretch robots secured 1,000-plus orders from DHL and FedEx, avoiding USD 15,000 in annual cloud egress fees per robot by using local GPUs. ISO 3691-4 safety rules formalized in 2024 further favor on-device inference, locking GPUs into every new mobile-robot SKU and widening the edge AI GPU market footprint in industrial automation.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High power consumption and thermal constraints of GPUs | -4.3% | Global, acute in outdoor and industrial deployments | Short term (≤ 2 years) |

| Supply-chain shortages of advanced packaging capacity | -3.8% | Global bottlenecks in Taiwan and South Korea | Medium term (2-4 years) |

| Skills gap in deploying containerized GPU stacks at edge sites | -2.9% | North America, Europe, emerging Asia-Pacific, and South America | Medium term (2-4 years) |

| Regulatory export controls limiting GPU availability | -2.6% | China, Russia, select Middle Eastern markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Power Consumption and Thermal Constraints of GPUs

Discrete GPUs drawing 75 watts generate 256 BTU per hour, overwhelming sealed IP65 enclosures. Vendors down-clock silicon, cutting throughput by up to 20% versus lab ratings, which narrows the advantage over sub-5-watt neural processors. Intel launched a 50-watt Arc A380E variant in 2025, but it faces NVIDIA’s 30-watt Orin NX in cost-sensitive segments.[5]Intel Corporation, “Arc A380E Thermal Design Brief,” intel.com European industrial sites pay EUR 95 (USD 107) in annual power for each 75-watt node, a charge that multiplies across 500-plus installations. Battery-powered field sensors, therefore, bypass GPUs for hybrid architectures, capping near-term edge AI GPU market penetration in ultra-low-power edge niches.

Supply-Chain Shortages of Advanced Packaging Capacity

Chiplet-based GPUs rely on TSMC’s CoWoS and InFO lines, which ran at 95% utilization through 2025. Planned expansions will lift output by end-2026, so vendors prioritize higher-margin data-center SKUs. AMD’s Instinct MI300 series faced eight-week lead-time slips that cascaded into embedded Ryzen AI variants. HBM3 supply remains concentrated at SK Hynix and Samsung, both of which funnel stock toward NVIDIA’s flagship data-center chips, leaving edge OEMs with six-month backlogs. Any Pacific supply disruption threatens the entire edge AI GPU market, prompting USD 1.6 billion U.S. funding for domestic packaging research and development.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By GPU Type: Integrated Solutions Dominate Cost-Sensitive Edge

Integrated GPUs held 61.59% share of the edge AI GPU market size in 2025, reflecting design wins in point-of-sale terminals, industrial HMI screens, and automotive infotainment. Snapdragon 8 Gen 3 and Dimensity 9300 SoCs fall within the 5-15 watt envelope, ideal for fanless chassis. Discrete GPUs, although smaller in volume, are expanding at a 38.48% CAGR to support 4K video analytics streams that require 12 TFLOPS at 30 FPS. Apple’s 40-core M3 Max blurred category lines by packing 65 TFLOPS into an integrated form factor, rivaling entry discrete cards. European Ecodesign labeling, effective from 2024, privileges integrated silicon in public procurements, further anchoring this segment within the broader edge AI GPU market.

Discrete devices still dominate where raw parallelism trumps power limits. An RTX A2000 at 70 watts offers 26 TFLOPS, doubling real-time detections per camera in municipal traffic analytics. As transformer-based vision models swell past 100 million parameters, discrete SKUs with dedicated tensor cores accelerate uptake in factories and smart cities. Heterogeneous roadmaps now see SoCs stacking extra GPU tiles, converging the performance vectors of integrated and discrete solutions.

By Deployment Type: Embedded Devices Lead, Gateways Accelerate

Embedded devices retained 60.11% of the edge AI GPU market share in 2025, serving mobile robots, cameras, and industrial controllers that prize sub-5 millisecond inference. Each autonomous forklift requires immediate collision avoidance, making on-board GPUs mandatory. Edge servers and gateways are scaling at 38.91% CAGR as factories move 200-plus camera feeds to centralized 2U rugged servers like HPE’s Edgeline EL8000, spreading GPU CapEx over many streams. Kubernetes stacks such as Fleet Command orchestrate containerized models across hundreds of sites, shrinking DevOps toil.

Yet connectivity gaps preserve embedded strength. Agricultural drones over remote fields cannot count on fiber backhaul, so on-device GPUs prevail. The draft IETF security guidance recommends hardware attestation, which is easier on integrated edge boards than in multi-tenant racks. The two deployment archetypes thus coexist, each reinforcing the trajectory of the edge AI GPU market.

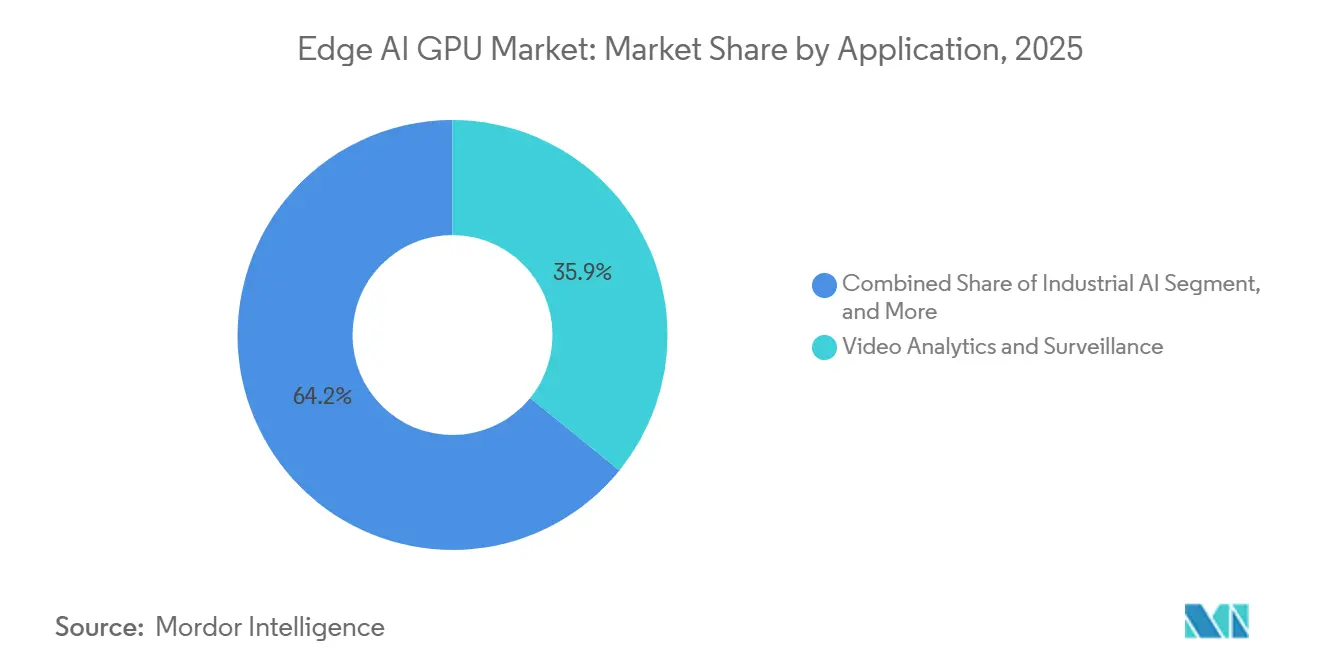

By Application: Video Analytics Leads, Robotics Surges

Video analytics accounted for 35.85% of revenue in 2025, driven by 1.2 billion global cameras. GPUs execute CNN and transformer pipelines locally, trimming WAN bandwidth by 90% for city operations. Robotics and automation is the fastest-rising slice, clocking a 38.67% CAGR, as factories deploy vision-guided pick-and-place systems that reached cost parity with labor after 8% annual wage inflation in developed economies. Industrial AI uses edge GPUs to watch vibration signatures, preventing 30-40% of unplanned downtime in 2025 Siemens pilots.

Healthcare, while smaller today, is scaling on the back of 200 FDA-cleared AI devices in 2025. Edge GPU servers inside hospitals pre-screen CT scans within minutes, cutting trauma diagnosis delays by 40%. Model complexity differs: video analytics often stays near 50 million parameters, while robotics models now exceed 100 million, steering them toward higher-end discrete silicon.

Geography Analysis

Asia-Pacific held 66.71% of the edge AI GPU market share in 2025 and is projected to grow at 38.83% CAGR to 2031. China ordered 800,000 GPU-ready nodes for smart-city programs under the New Infrastructure campaign. Japan budgeted JPY 50 billion (USD 340 million) in subsidies for small and medium manufacturers upgrading to edge AI. South Korea shipped 45,000 collaborative robots with GPU inference in 2025. India’s mission aims to deploy 10,000 GPU nodes by 2027 across the agriculture and health sectors.

North America ranks second. The U.S. Department of Energy funded USD 450 million in grid-edge analytics pilots in 2025, installing GPU nodes at substations. Canadian auto plants used GPUs for welding vision-guidance and defect trimming. Europe’s GDPR data-minimization principle directs enterprises toward local GPUs, and Germany’s automakers cut downtime by 25% through predictive maintenance.

South America’s share is smaller but rising as Brazilian farms and Chilean mines adopt GPU-based remote sensing. The Middle East and Africa are seeing early smart-city deployments in Dubai, including 5,000 GPU nodes for traffic analytics. Export-control rules limit shipments to Russia and select markets, modestly tempering wider geographic uptake of the edge AI GPU market.

Competitive Landscape

NVIDIA, Intel, and AMD held a significant share of combined market share in 2025, indicating moderate market concentration. Jetson modules remain the robotics reference, but Intel’s Arc A-series undercuts NVIDIA's list prices by up to 30%, and AMD’s Ryzen AI benefits from the Silo AI acquisition, which compresses models for edge inference. Hailo’s 2.5-watt accelerators replaced Jetson Nano in over 10,000 smart cameras in 2025, illustrating power-led substitution. Qualcomm leverages handset volumes to preload GPUs into General Motors' automotive infotainment systems, creating a latent installed base without incremental silicon cost.

Startup momentum is strongest below 5 watts. Kneron and SiMa.ai captured USD 150 million in 2025 funding for sub-watt processors. Patent filings show NVIDIA focusing on sparsity engines and quantization to cut power, defending turf against these alternatives. Intel’s 2024 Granulate buy elevates software optimization, squeezing 20-30% extra throughput from existing cards, prolonging replacement cycles, and influencing total addressable edge AI GPU market revenue.

Edge AI GPU Industry Leaders

NVIDIA Corporation

Intel Corporation

Advanced Micro Devices Inc.

Huawei Technologies Co. Ltd.

Qualcomm Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: NVIDIA invested USD 500 million to launch Jetson Thor, a 2,000-core SoC for humanoid robots, securing design wins with Figure AI and Agility Robotics.

- February 2026: Intel rolled out the Arc A310E 50-watt GPU for edge servers, shipping 15,000 units in the debut month through Dell and HPE partners.

- January 2026: Qualcomm and General Motors formed a USD 300 million joint venture to embed Snapdragon Ride GPUs into Ultium EV platforms for real-time battery and sensor fusion.

- December 2025: AMD bought Silo AI for USD 665 million, adding model-compression IP to its edge GPU stack.

Global Edge AI GPU Market Report Scope

The Edge AI GPU Market Report is Segmented by GPU Type (Integrated GPUs and Discrete GPUs), Deployment Type (Edge Servers/Gateways and Embedded Edge Devices), Application (Video Analytics and Surveillance, Industrial AI, Robotics and Automation, and Healthcare AI), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Integrated GPUs |

| Discrete GPUs |

| Edge Servers / Gateways |

| Embedded Edge Devices |

| Video Analytics and Surveillance |

| Industrial AI |

| Robotics and Automation |

| Healthcare AI |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East | |

| Africa |

| By GPU Type | Integrated GPUs | |

| Discrete GPUs | ||

| By Deployment Type | Edge Servers / Gateways | |

| Embedded Edge Devices | ||

| By Application | Video Analytics and Surveillance | |

| Industrial AI | ||

| Robotics and Automation | ||

| Healthcare AI | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East | ||

| Africa | ||

Key Questions Answered in the Report

What CAGR is forecast for the edge AI GPU market between 2026 and 2031?

The market is projected to grow at a 37.99% CAGR over the 2026-2031 period.

Which region leads shipments of edge inference GPUs today?

Asia-Pacific commanded 66.71% of global revenue in 2025 and remains the fastest-expanding geography.

Why are integrated GPUs still dominant at the edge?

Integrated designs fit 5-15-watt fanless envelopes typical of embedded kiosks and robots, giving them a 61.59% share in 2025.

What is the biggest restraint on edge AI GPU adoption?

High power draw and thermal limits that force performance throttling in sealed industrial enclosures.

Which application segment is growing fastest through 2031?

Robotics and automation are advancing at 38.67% CAGR as manufacturers embrace autonomous mobile platforms.

Page last updated on: