Ebola Vaccine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.42 Billion |

| Market Size (2031) | USD 3.27 Billion |

| Growth Rate (2026 - 2031) | 6.17% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

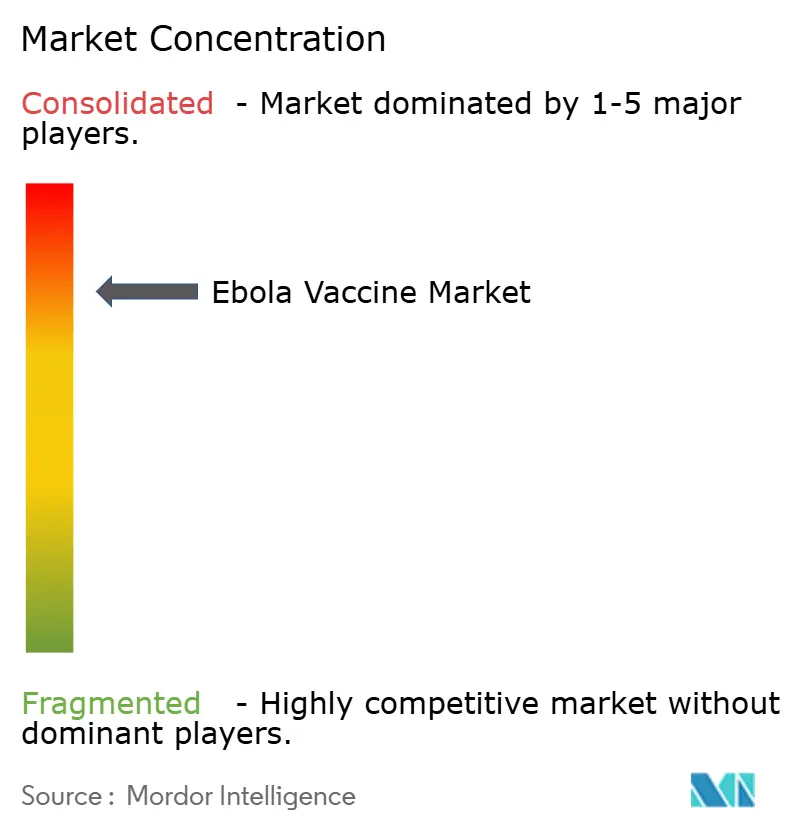

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ebola Vaccine Market Analysis by Mordor Intelligence

The Ebola Vaccine Market size is projected to be USD 2.30 billion in 2025, USD 2.42 billion in 2026, and reach USD 3.27 billion by 2031, growing at a CAGR of 6.17% from 2026 to 2031.

Institutional demand is driving significant changes in the Ebola vaccine market, as Gavi's 2024 preventive vaccination initiative decouples procurement from outbreak incidence[1]Gavi, “Ebola Vaccine Stockpile and Preventive Vaccination Funding,” gavi.org. Recombinant vector products still anchor revenues, yet inactivated and thin-film freeze-dried candidates signal a pivot toward thermostable solutions that bypass ultra-cold storage limits. Government health departments dominate purchasing decisions, and their stockpile-rotation policies create a recurring floor that shields the Ebola Vaccine market from the volatility of sporadic case counts. At the same time, Asia-Pacific governments are expanding sovereign reserves, intensifying geographic competition, and stimulating new platform investment.

Key Report Takeaways

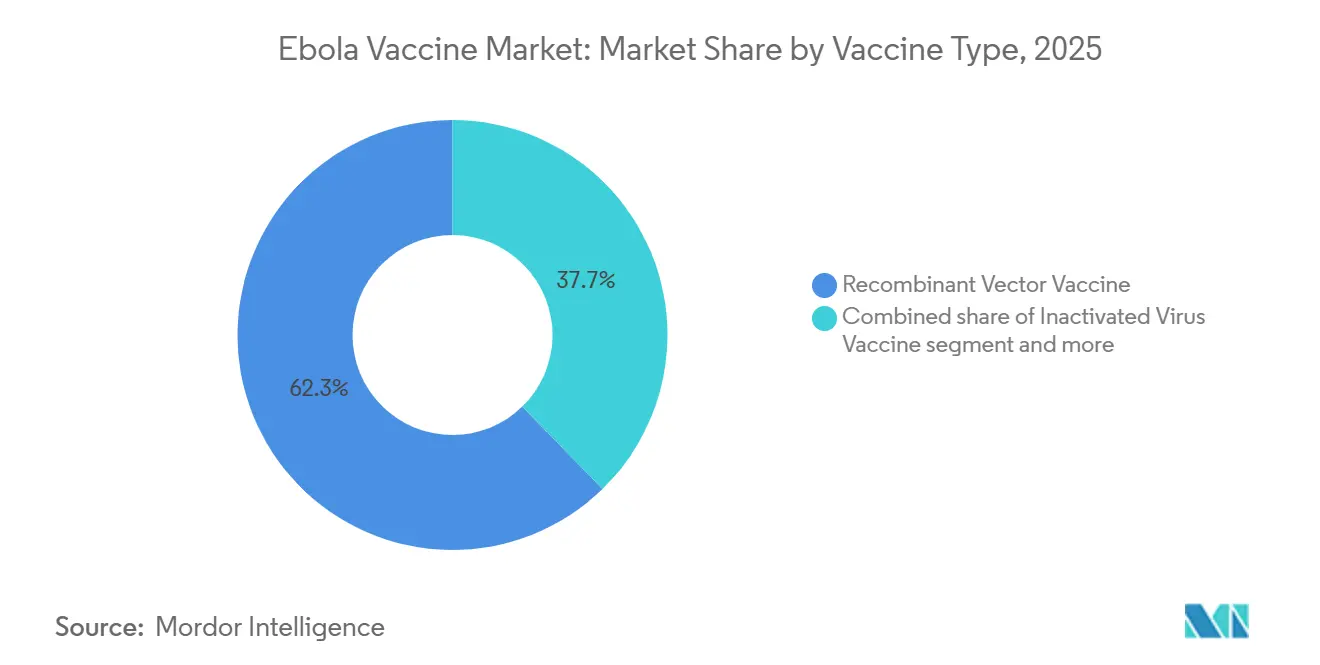

- By Vaccine Type, recombinant vector products captured 62.3% of the Ebola Vaccine market share in 2025, while inactivated candidates are forecast to grow at a 7.23% CAGR through 2031.

- By End User, government health departments held 54.23% of the Ebola Vaccine market size in 2025 and are advancing at an 8.85% CAGR to 2031.

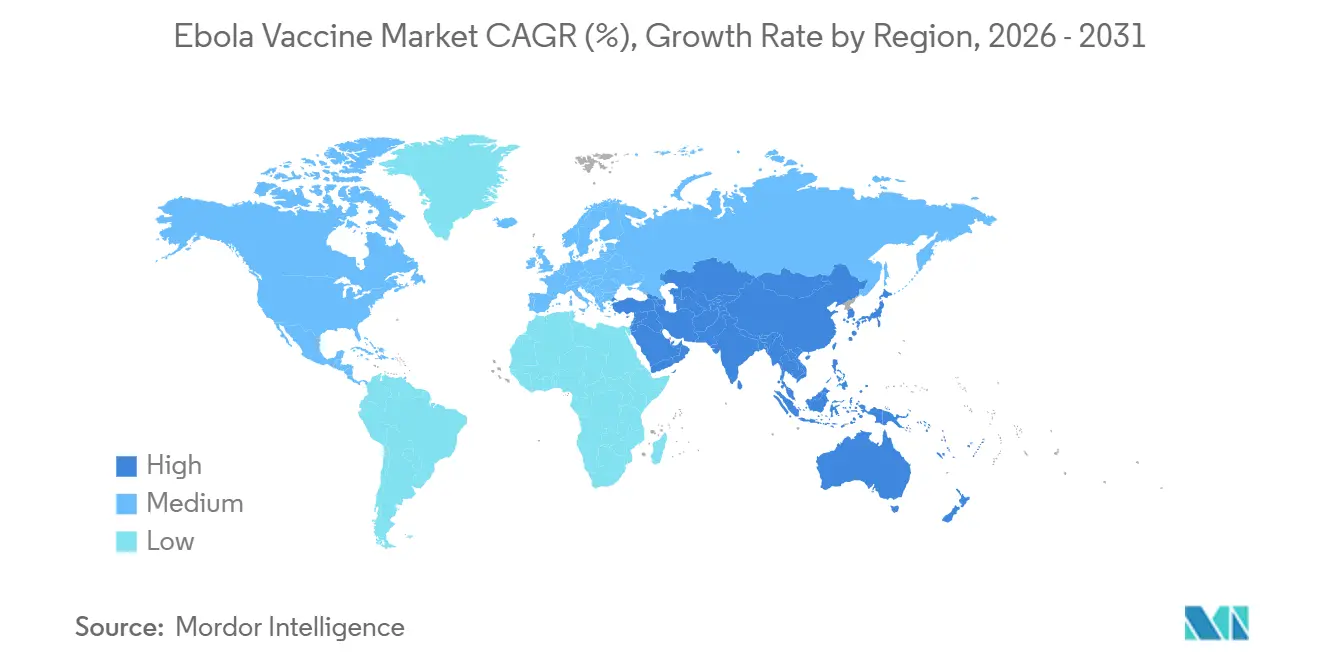

- By Geography, North America commanded 46% of 2025 revenue, but Asia-Pacific is set to expand at a 7.5% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ebola Vaccine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gavi-funded global stockpile ensures institutional demand and rapid deployment | +1.8% | Global, concentrated in Sub-Saharan Africa | Long term (≥4 years) |

| Recurring outbreaks and ring vaccination standard sustain outbreak-driven demand | +1.5% | Sub-Saharan Africa, spill-over West Africa | Medium term (2-4 years) |

| Regulatory approvals and WHO prequalification expand eligible populations | +1.2% | Global, priority Africa & emerging Asia-Pacific | Medium term (2-4 years) |

| Preventive vaccination for HCW/FLW expands use cases | +1.0% | Global, early adopters DRC, Guinea, Uganda | Long term (≥4 years) |

| Occupational vaccination recommendations create baseline demand | +0.4% | North America, Europe, select Asia-Pacific hubs | Long term (≥4 years) |

| Shelf-life expiry and stockpile rotation drive recurring procurement | +0.3% | Global, Gavi-managed | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Gavi-Funded Global Stockpile Ensures Institutional Demand and Rapid Deployment

Gavi’s 500,000-dose stockpile and its 2024 preventive-funding window moved the Ebola Vaccine market away from pure outbreak response. Between 2021-2023, 95% of Gavi shipments were preventive, confirming that endemic countries now place standing orders for healthcare-worker immunization. The September 2025 market-shaping roadmap locked in volume commitments through 2030, giving manufacturers forward-visibility and stabilizing the Ebola Vaccine market size. Allocation protocols reward pre-qualified suppliers with rapid fill-finish capacity, reinforcing incumbent advantages. Compliance with WHO prequalification and ICH Q7 GMP remains compulsory for stockpile participation.

Recurring Outbreaks and Ring Vaccination Standard Sustain Outbreak-Driven Demand

Uganda’s February 2025 Sudan ebolavirus episode and DRC’s September 2025 Kasai flare-up illustrate persistent zoonotic spill-over that triggers ring vaccination. Each deployment consumes 3,000-10,000 doses, supporting a baseline of roughly 50,000 outbreak-response doses per year. Inter-outbreak intervals in DRC have shortened to 1.8 years since 2018, underlining a structural demand driver for the Ebola Vaccine market. Absence of a licensed Sudan vaccine, however, limits effectiveness outside Zaire outbreaks.

Regulatory Approvals and WHO Prequalification Expand Eligible Populations

Merck’s ERVEBO label extension to children greater than or equal to 12 months in 2023 expanded the addressable population by 22% in high-risk regions. National registrations in multiple African states removed emergency-use delays, accelerating deployment. Johnson & Johnson’s Zabdeno/Mvabea provides a non-live-vector alternative but faces logistic hurdles from its 56-day dosing interval. Regional approval harmonization under the African Medicines Agency is expected to reduce duplicative reviews by 40%, opening mid-tier entry pathways.

Preventive Vaccination for HCW/FLW Supported by SAGE and Gavi Expands Use Cases

WHO-SAGE’s 2023 guidance and Gavi’s USD 30 million envelope launched in 2024 institutionalize occupational immunization. DRC’s August 2024 campaign vaccinated 12,000 healthcare workers, and Guinea’s initiative covered 8,500 staff, shifting demand from episodic to programmatic [2]World Health Organization, “SAGE Meeting Report,” who.int. Laboratory personnel at 23 BSL-4 sites add stable demand, as OSHA and EU Directive 2000/54/EC embed vaccination within workplace safety budgets.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Small, sporadic addressable population limits commercial scale | -0.8% | Global | Long term (≥4 years) |

| Ultra-cold chain requirements complicate last-mile logistics | -0.6% | Sub-Saharan Africa, remote Asia-Pacific | Medium term (2-4 years) |

| No licensed vaccines for Sudan ebolavirus; limited cross-protection | -0.5% | East Africa, spill-over DRC | Medium term (2-4 years) |

| Pricing and stockpile governance constraints dampen uptake | -0.3% | Global, Gavi & ICG | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Small, Sporadic Addressable Population Limits Commercial Scale

Cumulative confirmed Ebola cases remain below 35,000, capping peak annual volume at roughly 300,000 doses when stockpile rotation is included. Fixed costs for prequalification and cold-chain validation exceed USD 50 million, yet tiered Gavi pricing keeps peak revenue per supplier under USD 150 million, tempering private investment. The Sudan vaccine gap persists largely because expected returns do not offset Phase III trial costs estimated at USD 80-120 million [3]Coalition for Epidemic Preparedness Innovations, “Sudan Vaccine Cost-Benefit Analysis,” cepi.net.

Ultra-Cold Chain Requirements Complicate Last-Mile Logistics

ERVEBO must be stored at –60 °C to –80 °C, a condition absent in 68% of DRC health facilities, driving logistics costs to USD 12 per dose during the 2025 Kasai response. Dry-ice shortages delayed vaccination by 72 hours, underlining operational risk. Johnson & Johnson’s 2 °C–8 °C product reduces cold-chain strain, but its two-dose schedule narrows field usefulness. Ambient-temperature formulations, such as TFF’s thin-film freeze-dried candidate entering Phase I in 2026, may unlock remote demand if efficacy proves comparable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vaccine Type: Recombinant Vectors Lead, Inactivated Candidates Gain Momentum

Recombinant vectors controlled 62.3% of 2025 Ebola Vaccine market share on the back of ERVEBO’s single-dose convenience and 97.5% efficacy. Despite ultra-cold storage hurdles, predictable Gavi rotation keeps demand steady. The segment anchors over half of the 2026 Ebola Vaccine market size and maintains entrenched first-mover advantages.

Inactivated virus products are forecast to expand at a 7.23% CAGR, propelled by Chinese and Indonesian programs targeting thermostable formulations for domestic stockpiles. DNA and subunit approaches remain niche due to device costs and early-stage pipelines, yet they illustrate technology diversification that could reshape the Ebola Vaccine market if cold-chain barriers persist. Zabdeno/Mvabea’s two-dose adenovirus platform carves out niches among immunocompromised groups but sacrifices outbreak agility. Regulatory lead times and prequalification costs continue to shield incumbents, making thermostability the clearest path for newcomers to capture Ebola Vaccine market share.

By End User: Government Health Departments Dominate and Accelerate

Government agencies held 54.23% of 2025 revenue and are growing fastest at 8.85% CAGR as Gavi channels preventive funding directly to ministries of health. This cohort commands more than half of the 2026 Ebola Vaccine market size because stockpile rotation, outbreak response, and occupational programs converge under a single budget line.

Hospitals form the secondary tier, driven by CDC mandates for 127 U.S. Ebola Treatment Centers and equivalent European facilities, generating steady yet modest demand. Research institutes at BSL-4 labs create a predictable micro-segment, while NGOs and private corporations purchase on an as-needed basis. The structural dominance of governments ensures that public procurement policies will continue to steer the Ebola Vaccine market well beyond the forecast horizon.

Geography Analysis

North America’s 46% share in 2025 reflects robust preparedness funding rather than local incidence. The U.S. Strategic National Stockpile maintains roughly 50,000 doses, and CDC guidelines institutionalize annual replenishment. Canada upgraded its reserve to 10,000 doses in 2025 following lessons from Uganda’s outbreak, embedding ring-vaccination protocols into its response plan. Mexico’s role is confined to laboratory immunization. Regulatory rigor under FDA and OSHA ensures that only pre-qualified suppliers penetrate the Ebola Vaccine market here.

Asia-Pacific is the fastest-growing region, with a 7.5% CAGR. Japan invested USD 18 million in 2024 for 20,000 ERVEBO doses and freezer upgrades, while South Korea aims to secure 15,000 doses by 2027. China’s inactivated candidate could localize supply by 2026, consistent with Healthy China 2030 self-sufficiency mandates. India’s demand remains limited to laboratory staff, yet guidelines published in 2025 lay the groundwork for broader adoption. Australia’s National Medical Stockpile keeps 5,000 doses for BSL-4 facilities.

Europe accounted for a significant share of 2025 spending. Germany leads with 25,000 doses, followed by the United Kingdom at 18,000, all coordinated through ECDC’s Health Security Committee. EMA authorization of Zabdeno/Mvabea adds platform diversity but uptake outside stockpiles is minimal. Africa and the Middle East rely heavily on Gavi: the Africa CDC initiative aims to pre-position 100,000 doses by 2027 and establish fill-finish capability in Dakar. South American participation remains research-focused, led by Brazil’s Fiocruz with a 2,500-dose reserve.

Competitive Landscape

Merck’s ERVEBO holds the majority of global volume, delivering the highest Ebola Vaccine market share due to early WHO prequalification and single-dose efficacy. Johnson & Johnson captures a distant second place; its two-dose course limits surge use but secures European orders.

Emerging competition centers on thermostability: TFF Pharmaceuticals enters Phase I in 2026, and China’s Institute of Medical Biology advances an inactivated platform for domestic reserves. Oxford’s and IAVI’s Sudan-specific vectors compete for an unmet segment valued near USD 100 million annually but face investment hurdles due to small volumes.

Strategic alliances emphasize manufacturing decentralization. SK Bioscience’s 2023 deal with Merck localizes ERVEBO production in South Korea, reducing single-supplier risk in the Ebola Vaccine market. The Institut Pasteur de Dakar partners with Africa CDC to establish a regional fill-finish, shortening delivery lead times. Incumbents leverage patent positions until at least 2029, and WHO prequalification costs of more than USD 20 million act as a de facto moat. Nonetheless, the African Medicines Agency’s harmonized pathway may lower entry barriers for mid-tier firms such as Bio Farma and Bharat Biotech after 2026.

Ebola Vaccine Industry Leaders

Merck & Co.

Johnson & Johnson

TFF Pharmaceuticals

Bharat Biotech

GSK

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: MSD and CEPI launched a USD 30 million program to develop a lower-cost ERVEBO version.

- January 2026: University of Oxford began a USD 26.7 million filovirus-vaccine project covering Ebola, Sudan, and Marburg.

- February 2025: Uganda, the WHO, and partners initiated the first Sudan ebolavirus vaccine field trial.

Global Ebola Vaccine Market Report Scope

Ebola vaccines are medical countermeasures developed to prevent Ebola virus disease (EVD), primarily targeting the highly fatal Zaire ebolavirus species. As of 2026, there are two primary licensed and World Health Organization (WHO) prequalified vaccines: Ervebo, a single-dose, live-attenuated recombinant vaccine manufactured by Merck, and a two-dose prime-boost regimen consisting of Zabdeno and Mvabea developed by Johnson & Johnson.

The Ebola vaccine market is segmented by vaccine type, applications, end users, and geography. By vaccine type, it is segmented into developed recombinant vector vaccine, inactivated virus vaccine, DNA vaccine, subunit vaccine, and others. By end-users, the segmentation includes large hospitals, government health departments, research institutes, NGOs, and others. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Recombinant Vector Vaccine |

| Inactivated Virus Vaccine |

| DNA Vaccine |

| Subunit Vaccine |

| Others |

| Hospitals |

| Government Health Departments |

| Research Institutes |

| NGOs |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Vaccine Type | Recombinant Vector Vaccine | |

| Inactivated Virus Vaccine | ||

| DNA Vaccine | ||

| Subunit Vaccine | ||

| Others | ||

| By End User | Hospitals | |

| Government Health Departments | ||

| Research Institutes | ||

| NGOs | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the Ebola Vaccine market expected to grow through 2031?

The Ebola Vaccine market is projected to expand at a 6.17% CAGR between 2026-2031, rising from USD 2.42 billion to USD 3.27 billion.

Which platform currently dominates global procurement?

Recombinant vector vaccines, led by Merck’s ERVEBO, held majority of the market share in 2025

Why are government health departments the largest buyers?

They manage national stockpiles, coordinate ring-vaccination campaigns, and now fund preventive programs, giving them 54.23% of 2025 revenue and the fastest segment CAGR at 8.85%.

Which region is forecast to grow quickest?

Asia-Pacific is set to grow at a 7.5% CAGR as Japan, South Korea, and China all expand sovereign stockpiles and pursue local manufacturing.

Page last updated on: