Dual-energy X-ray Absorptiometry (DEXA) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

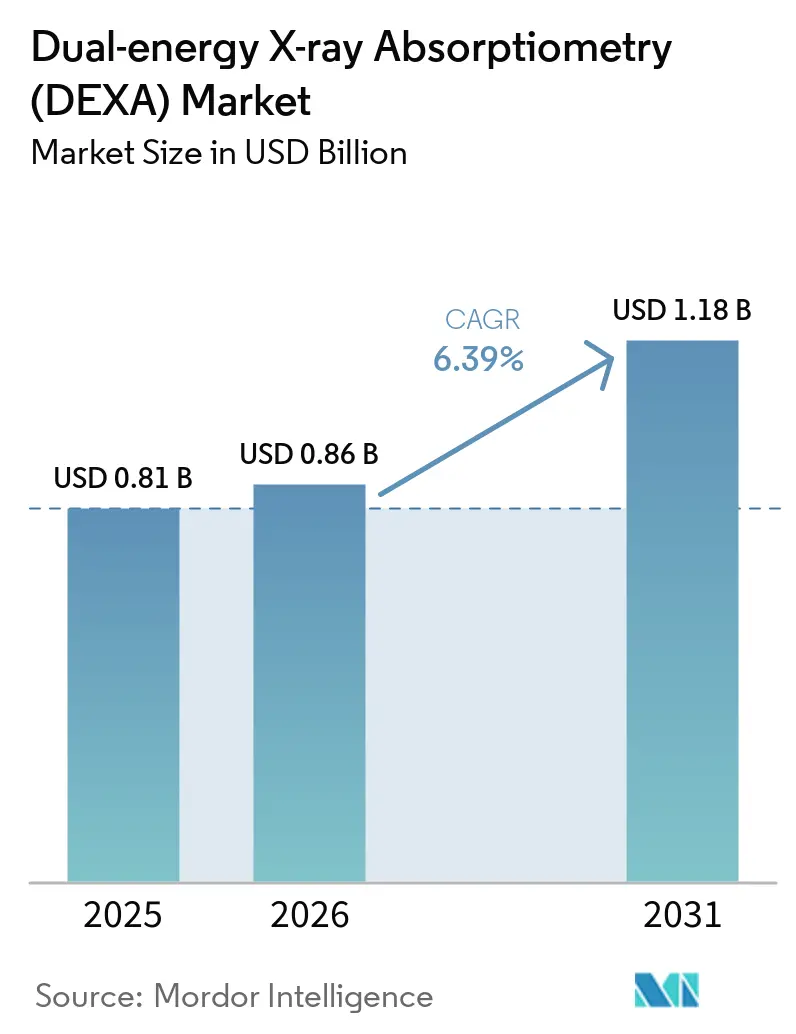

| Market Size (2026) | USD 0.86 Billion |

| Market Size (2031) | USD 1.18 Billion |

| Growth Rate (2026 - 2031) | 6.39% CAGR |

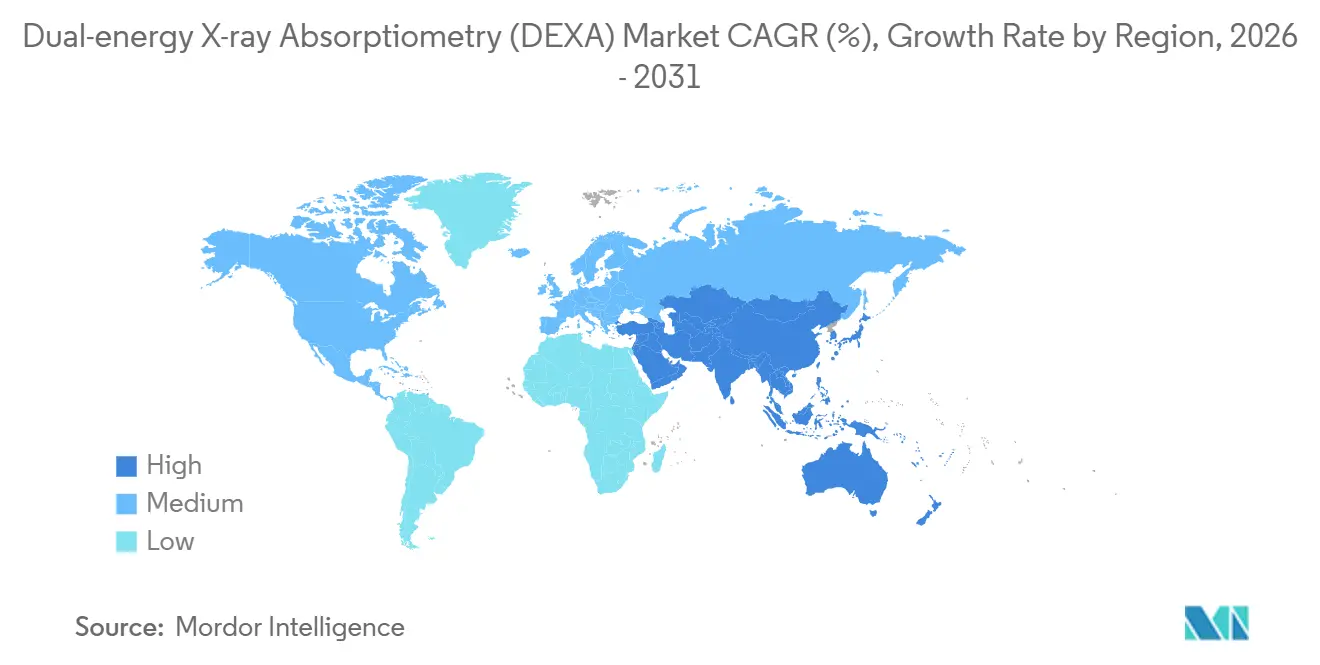

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

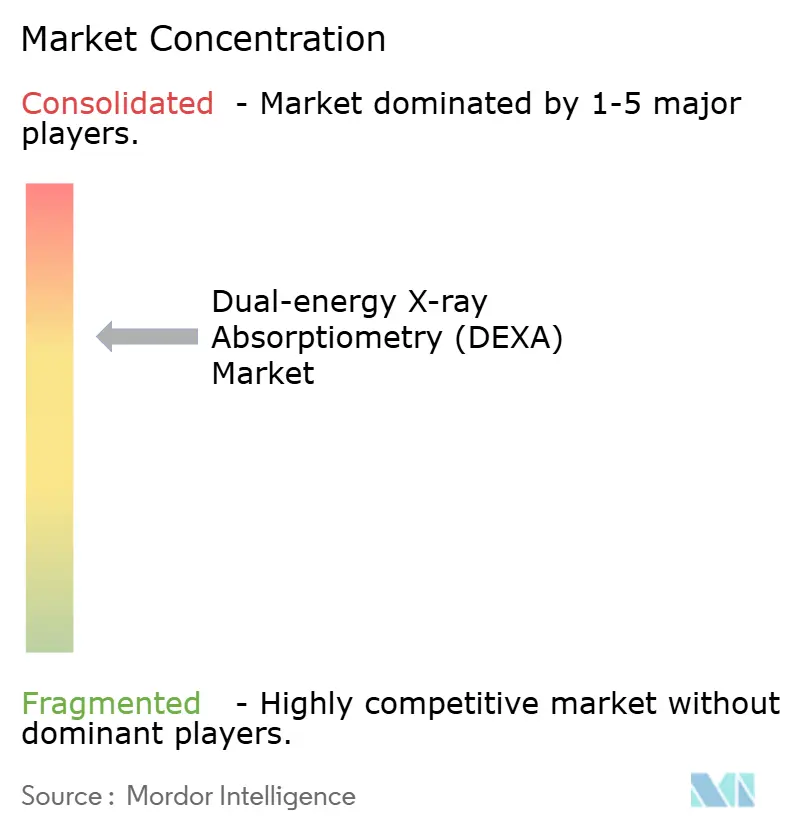

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dual-energy X-ray Absorptiometry (DEXA) Market Analysis by Mordor Intelligence

The Dual-energy X-ray Absorptiometry Market size is projected to expand from USD 0.81 billion in 2025 and USD 0.86 billion in 2026 to USD 1.18 billion by 2031, registering a CAGR of 6.39% between 2026 to 2031.

Expanding guideline-based screening, AI-enhanced imaging, and body-composition monitoring for GLP-1 therapy are widening the modality’s clinical footprint. Stable Medicare payment for central scans, combined with rising urban coverage in China, is sustaining capital investment even as office-based margins compress. Fan-beam platforms that couple rapid acquisition with automated fracture detection are displacing legacy pencil-beam units in high-throughput settings. Meanwhile, opportunistic CT programs are emerging as referral funnels rather than substitutes, reinforcing the need for confirmatory hip and spine measurements.

Key Report Takeaways

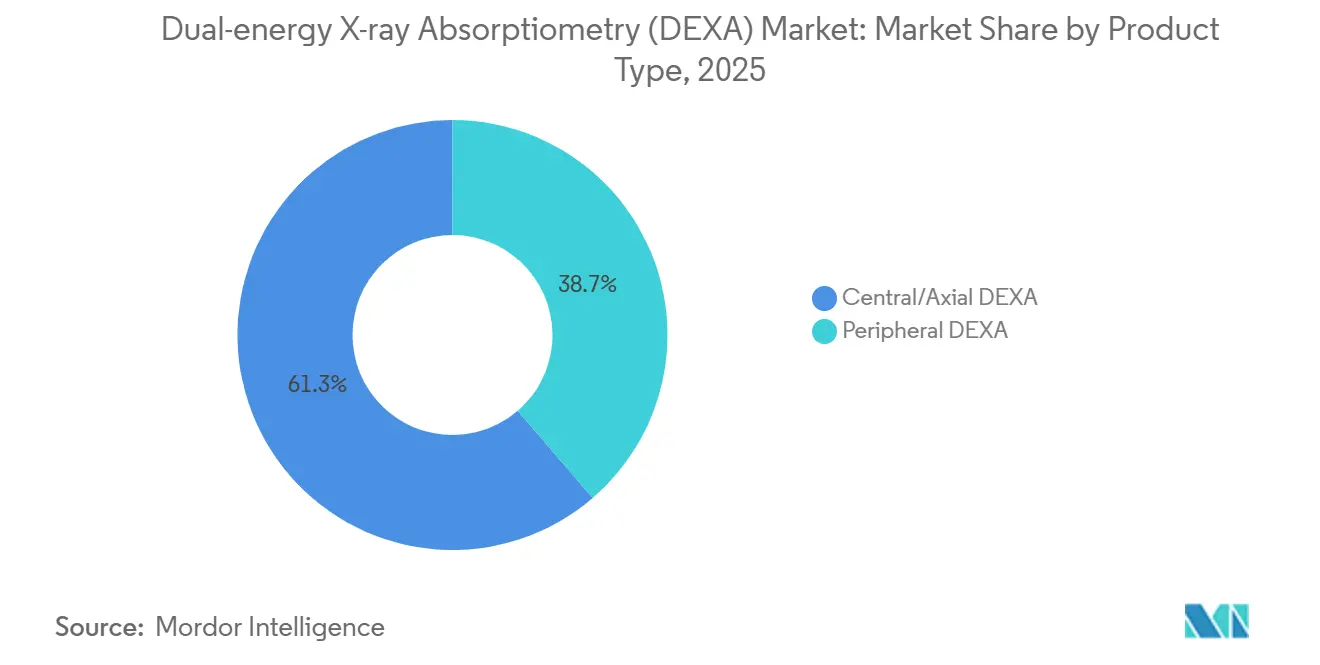

- By product type, central systems held 61.30% of the Dual-energy X-ray Absorptiometry market share in 2025, while the same segment is projected to advance at a 7.95% CAGR through 2031.

- By technology, fan-beam architectures commanded 65.98% revenue in 2025 and are expected to grow at an 8.16% CAGR to 2031.

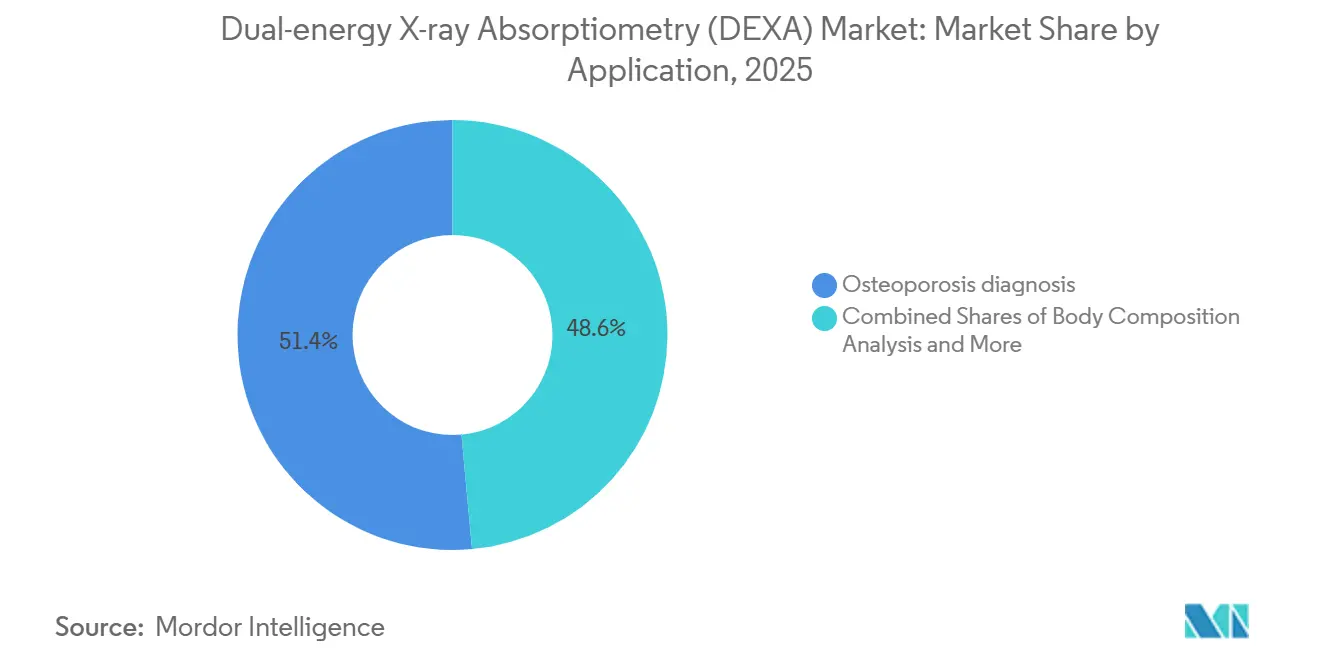

- By application, osteoporosis diagnosis accounted for 51.45% of the Dual-energy X-ray Absorptiometry market size in 2025 and is set to expand at an 8.45% CAGR.

- By end user, hospitals led with 45.13% revenue share in 2025, whereas specialty clinics are forecast to post the fastest growth at 8.56% to 2031.

- By geography, North America represented 42.17% of revenue in 2025, while Asia-Pacific is on track for an 8.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dual-energy X-ray Absorptiometry (DEXA) Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population and rising fragility-fracture burden | +1.8% | Global, with highest intensity in Japan, South Korea, Germany, Italy | Long term (≥ 4 years) |

| Guideline-backed screening and payer coverage expand testable populations | +1.5% | North America & EU, selective APAC markets (China tier-1/2 cities, Australia) | Medium term (2-4 years) |

| DEXA as clinical gold standard with add-on TBS and AI analytics | +1.3% | North America, Western Europe, urban APAC hubs | Medium term (2-4 years) |

| GLP-1 weight-loss programs spur DXA body-composition monitoring | +1.2% | North America, Western Europe, GCC | Short term (≤ 2 years) |

| Opportunistic CT case-finding channels referrals to confirmatory DEXA | +0.6% | North America, select EU markets with integrated radiology networks | Medium term (2-4 years) |

| Expansion of Fracture Liaison Services and systematic post-fracture care protocols | +0.5% | North America, UK, Australia, with emerging adoption in Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population and Rising Fragility-Fracture Burden

People aged 65+ climbed to 761 million in 2024 and will approach 994 million by 2030, with East Asia and Southern Europe aging the fastest [1]United Nations, “Ageing,” un.org. Japan already records 180,000 hip fractures a year, costing JPY 1.2 trillion (USD 8.1 billion) in direct care. South Korea saw a 14% fracture rise in fractures among women 70+ between 2020 and 2024. The WHO lists fragility fractures as the top cause of disability-adjusted life-years lost for women over 60 in high-income countries. This demographic wave ensures a persistent baseline for baseline and follow-up Dual-energy X-ray Absorptiometry market demand.

Guideline-Backed Screening and Payer Coverage Expand Testable Populations

The 2025 USPSTF update added 12 million U.S. women aged 50-64 with elevated FRAX scores to screening eligibility [2]USPSTF, “Osteoporosis Screening,” uspreventiveservicestaskforce.org. CMS kept national payment at USD 127.42 per central scan in 2025, protecting revenue stability. China’s National Health Commission bundled bone-density screening into its Essential Public Health Services for urban women 65+ in 2025, targeting 40 million beneficiaries by 2028. Australia similarly extended rebates to older men with prior fractures in 2024. These policies shift DEXA from optional to protocol-driven imaging, anchoring volume growth.

DEXA As Clinical Gold Standard With Add-On TBS And AI Analytics

Trabecular Bone Score secured FDA clearance in 2024 for integration with leading systems, boosting fracture-risk prediction by 18% in women with osteopenia [3]FDA, “Medical Devices,” fda.gov. Hologic’s Horizon embeds CNN-based vertebral-fracture detection that cuts radiologist read time 40% while maintaining 94% sensitivity. GE HealthCare’s Prodigy Fuga links directly to cloud-based FRAX, saving about 3 minutes per patient. The 2024 ACR Appropriateness Criteria grade DEXA + TBS as “usually appropriate” for glucocorticoid users, lifting procedure value.

GLP-1 Weight-Loss Programs Spur DXA Body-Composition Monitoring

Nine million U.S. prescriptions for semaglutide and tirzepatide were filled in 2024. Lancet data show 39% of weight lost on high-dose semaglutide is lean mass, heightening sarcopenia risk. The Endocrine Society’s 2025 guideline now calls for baseline and 6-month Dual-energy X-ray Absorptiometry scans in adults 60+ starting GLP-1 therapy. Private insurers such as Cigna began covering serial scans for BMI ≥ 35 members on GLP-1 drugs in 2025. Body-composition services are diversifying revenue beyond osteoporosis diagnosis.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement variability and declining in-office rates depress utilization | -1.1% | North America, select EU markets with mixed public-private payer systems | Short term (≤ 2 years) |

| Persistent post-fracture care gap and low screening adherence | -0.8% | Global, most acute in South America, MEA, rural APAC | Long term (≥ 4 years) |

| Substitution risk from opportunistic CT/QCT and QUS in select settings | -0.7% | North America, Western Europe, with an advanced radiology infrastructure | Medium term (2-4 years) |

| Cross-vendor standardization issues and capital/space constraints | -0.5% | Global, particularly acute in fragmented markets with multiple vendor presence | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reimbursement Variability and Declining In-Office Rates Depress Utilization

The 2025 Medicare schedule cut non-facility payment 3.2%, dragging aggregate office margins 11% below 2020 levels. Private payers diverge: Cigna pays 110% of Medicare in-network but only 85% out-of-network, skewing geographic access. Blue Cross NC tightened prior authorization in 2024, slicing local scan volume 7% in six months. Higher hospital facility fees shift the cost burden to patients on high-deductible plans, curbing elective tests. Rural centers with limited throughput struggle to recover capital on USD 80,000-150,000 units, slowing fleet renewal.

Persistent Post-Fracture Care Gap and Low Screening Adherence

Only 22% of women 65+ received osteoporosis therapy within a year of hip fracture in the 2024 IOF registry, and fewer than 30% obtained a DEXA scan to guide care. Fracture Liaison Services exist in just 38% of U.S. trauma hospitals. A 2025 Osteoporosis International cohort reported serial-scan adherence of 41% at two years, falling to 28% at four. Brazil’s public system reached only 15% of eligible older women in 2024. South Africa’s capacity covers 8% of the need, with nine-month waits in rural provinces. These gaps cap attainable volume even where hardware exists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Central Systems Dominate Clinical Workflows

Central platforms generated 61.30% of 2025 revenue and are poised for a 7.95% CAGR through 2031, underpinned by hip and spine metrics that remain the diagnostic gold standard. This segment undergirds the Dual-energy X-ray Absorptiometry market size because payers reimburse central scans at USD 127.42, roughly triple peripheral rates, and because AI-driven vertebral-fracture assessment and TBS analytics are available only on central hardware. Lifecycle services, software subscriptions, phantoms, and service contracts, contribute another quarter of revenue, raising total return on investment.

Peripheral devices occupy value niches in rural screening and occupational health. Units priced under USD 25,000 attract small clinics, but Medicare’s USD 37.26 payment under CPT 77081 constrains profitability. Clinical guidelines continue to advise confirmatory central imaging for treatment decisions, limiting peripheral uptake beyond triage programs. As reimbursement favors comprehensive assessment and body-composition analytics, central systems will retain the bulk of the Dual-energy X-ray Absorptiometry market share.

By Technology: Fan-Beam Architectures Deliver Speed And Precision

Fan-beam systems held 65.98% of 2025 revenue and are expected to outpace the overall Dual-energy X-ray Absorptiometry market at an 8.16% CAGR to 2031. Scan times under two minutes boost patient throughput and cut motion artifacts, critical for pediatric and bariatric cohorts. Narrow-angle fan beams now deliver radiation doses of just 0.4 μSv per whole-body exam, well below regulatory thresholds.

Pencil-beam technology persists where capital budgets are tight. Systems costing below USD 50,000 remain common in Latin America and Southeast Asia, yet their larger pixel size hampers vertebral morphometry and VFA analytics. The International Society for Clinical Densitometry cautions that pencil-beam and fan-beam data are not interchangeable, driving integrated networks toward fleet standardization on fan-beam platforms.

By Application: Osteoporosis Diagnosis Anchors Volume, VFA And Body Composition Accelerate

Osteoporosis diagnosis contributed 51.45% of 2025 revenue and is projected to post an 8.45% CAGR, sustaining the largest slice of the dual-energy X-ray absorptiometry market size. TBS algorithms and AI vertebral-fracture detection enhance risk stratification, justifying shorter rescan intervals and premium pricing.

Body-composition analysis is the fastest-growing niche as endocrinologists monitor lean-mass loss during GLP-1 therapy. Private insurers now reimburse follow-up scans at 6-month intervals, creating a repeat-service pathway outside Medicare’s 24-month osteoporosis window. VFA adoption is also climbing; AI modules identify fractures missed on plain radiographs, upgrading 22% of osteopenic women to treatment candidacy.

By End User: Specialty Clinics Outpace Hospitals As Workflows Integrate

Hospitals generated 45.13% of 2025 revenue, supported by outpatient imaging centers and fracture liaison programs. However, falling professional fees and rising facility charges are steering volume toward specialized outpatient sites.

Specialty clinics, orthopedics, endocrinology, and rheumatology, are projected to expand at 8.56%, the fastest pace in the Dual-energy X-ray Absorptiometry market. Same-visit scanning dovetails with glucocorticoid or GLP-1 prescribing, improving adherence. Diagnostic imaging centers sit between these poles, but face consolidation pressure as health-system acquisitions erode independent market share.

Geography Analysis

North America accounted for 42.17% of 2025 revenue. The 2025 USPSTF expansion and steady CMS rates maintain scan volume, yet office reimbursements dropped 3.2% year on year, pushing providers to hospital outpatient departments. Canada reimburses seniors province-wide, but utilization lags guideline targets, and Mexico’s coverage outside metros remains sparse.

Asia-Pacific is forecast to grow 8.44% through 2031, the fastest regional CAGR. China’s 2025 public-health mandate will install roughly 3,000 additional central units by 2028. Japan subsidizes prefectural screening to contain JPY 1.2 trillion annual fracture costs. India’s vast unmet need and low penetration represent upside once unit pricing falls below USD 40,000. Europe shows mixed maturity. The U.K. operates fracture liaison services in 62% of trusts, yet still scans only 28 women per 1,000 over 65 years old. Germany’s 2025 guideline update could add 2.5 million eligible women. France now reimburses TBS, an early adopter move. Budget limits restrain Italy and Spain, while GCC states mandate screening for older women, bolstering unit sales.

Competitive Landscape

Hologic and GE HealthCare together control a significant share of the installed bases in Western markets, giving them scale to fund AI modules and cloud analytics. Hologic’s Horizon uses a 1.2-million-image dataset to auto-score vertebral fractures, trimming read times 40%. GE’s Prodigy Fuga finishes whole-body scans in 60 seconds with real-time motion correction, appealing to bariatric and pediatric providers. Chinese OEMs, Guangzhou Yueshen, Mednova, OsteoSys, supply fan-beam systems at USD 40,000-70,000, rapidly penetrating tier-2/3 Chinese cities and MEA tenders. Fujifilm’s photon-counting patent promises 35% faster scans at sub-1% precision, signaling R&D momentum.

Standardization gaps remain; ISCD data show that least-significant-change differs up to 2.8% between major brands, nudging multi-site networks to single-vendor deals. Emerging CT analytics providers such as VirtuOst complement rather than cannibalize DEXA by flagging patients for confirmatory testing.

Dual-energy X-ray Absorptiometry (DEXA) Industry Leaders

Hologic, Inc.

GE HealthCare

Guangzhou Yueshen

OsteoSys Co., Ltd.

Mednovo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: BPL Medical Technologies officially completed the acquisition of South Korea-based Yozma BMTech Co., Ltd. This deal allows BPL to offer specialized bone mineral density (BMD) systems, marking its formal entry into the bone densitometry segment.

- March 2025: Hologic partnered with the IOF to deploy 50 AI-enabled Horizon systems in fracture liaison services across Europe and Asia-Pacific by 2027.

- February 2025: GE HealthCare secured FDA clearance for Prodigy Fuga, a 60-second whole-body composition scanner with cloud FRAX.

Global Dual-energy X-ray Absorptiometry (DEXA) Market Report Scope

As per the scope of the report, Dual-energy X-ray Absorptiometry, commonly known as a DEXA or DXA scan, is a highly accurate, non-invasive imaging test primarily used to measure bone mineral density (BMD). It is widely considered the gold standard for diagnosing osteoporosis and osteopenia, conditions characterized by weakened or thinning bones that increase the risk of fractures.

The Dual-energy X-ray Absorptiometry (DEXA) market is segmented by product type, technology, application, end user, and geography. Based on product type, the market is segmented into central/axial DEXA and peripheral DEXA. By technology, the market is segmented into fan-beam and pencil-beam. By application, the market is segmented into osteoporosis diagnosis, body composition analysis, and vertebral fracture assessment (VFA). By end users, the market is segmented into hospitals, diagnostic/imaging centers, and specialty clinics.

Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Central/Axial DEXA |

| Peripheral DEXA |

| Fan-beam |

| Pencil-beam |

| Osteoporosis diagnosis |

| Body composition analysis |

| Vertebral fracture assessment (VFA) |

| Hospitals |

| Diagnostic/Imaging Centers |

| Specialty Clinics (Orthopedics/Endocrinology/Rheumatology) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Central/Axial DEXA | |

| Peripheral DEXA | ||

| By Technology | Fan-beam | |

| Pencil-beam | ||

| By Application | Osteoporosis diagnosis | |

| Body composition analysis | ||

| Vertebral fracture assessment (VFA) | ||

| By End User | Hospitals | |

| Diagnostic/Imaging Centers | ||

| Specialty Clinics (Orthopedics/Endocrinology/Rheumatology) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Dual-energy X-ray Absorptiometry market in 2026?

Dual-energy X-ray Absorptiometry market in 2026 is expected to reach USD 0.86 billion in 2026.

What is the forecast CAGR for Dual-energy X-ray Absorptiometry through 2031?

The market is projected to grow at 6.39% over 2026-2031.

Which product type holds the largest share?

Central systems led with 61.30% of 2025 revenue.

Which region is expanding the fastest?

Asia-Pacific is expected to post an 8.44% CAGR to 2031.

Page last updated on: