Market Overview

| Study Period | 2019 - 2030 |

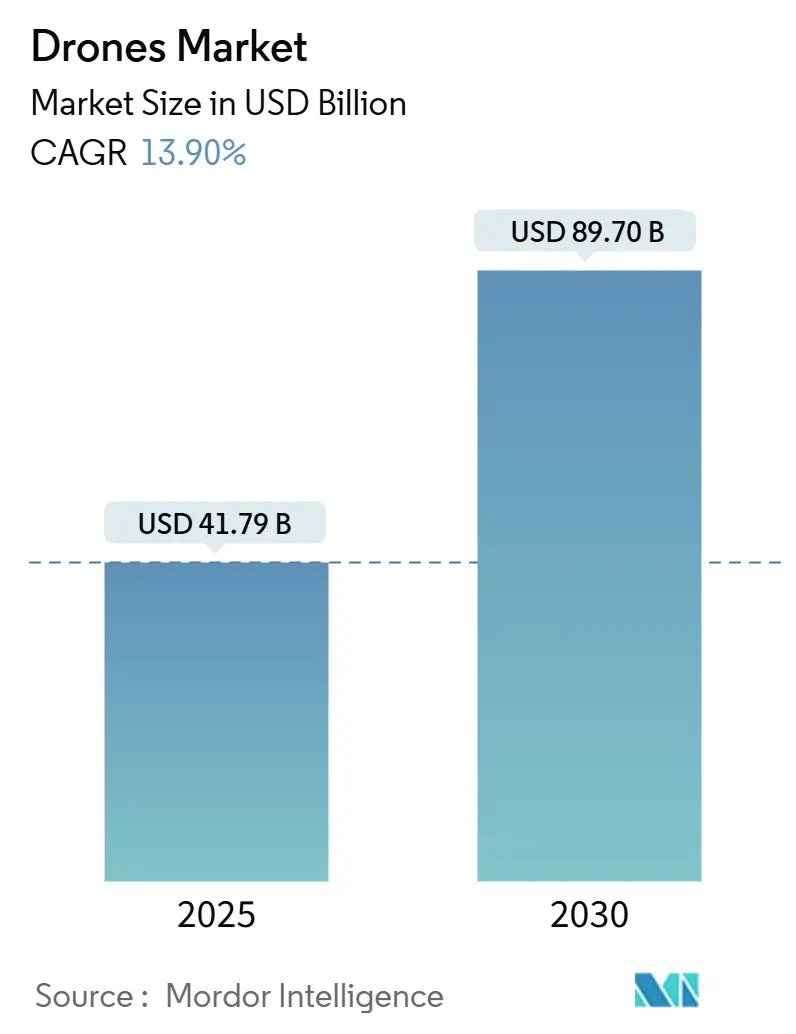

| Market Size (2025) | USD 41.79 Billion |

| Market Size (2030) | USD 89.70 Billion |

| Growth Rate (2025 - 2030) | 13.90% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Drones Market Analysis by Mordor Intelligence

The drones market reached USD 41.79 billion in 2025 and is on course to climb to USD 89.70 billion by 2030, reflecting a robust 13.9% CAGR. Adoption accelerates as on-board edge-AI runs complex perception algorithms on sub-10 W chipsets, making autonomous missions viable in construction, energy, and agriculture. Rapid 5G roll-outs with Multi-access Edge Computing (MEC) provide sub-10 ms latency that supports dependable Beyond Visual Line-of-Sight (BVLOS) control, while steep sensor‐price declines open sophisticated payloads to smaller operators. Regulatory momentum—most notably the FAA’s draft BVLOS rules and ICAO’s new Standards and Recommended Practices (SARPs)—signals greater airspace access. Yet supply chain strains, notably lithium-ion cell shortages and export curbs on rare-earth materials, continue to inflate bill-of-materials costs and could dampen discretionary demand. Overall, competition is shifting toward firms able to bundle hardware, AI software, and regulatory compliance into an end-to-end value proposition, accelerating consolidation across the drones market.

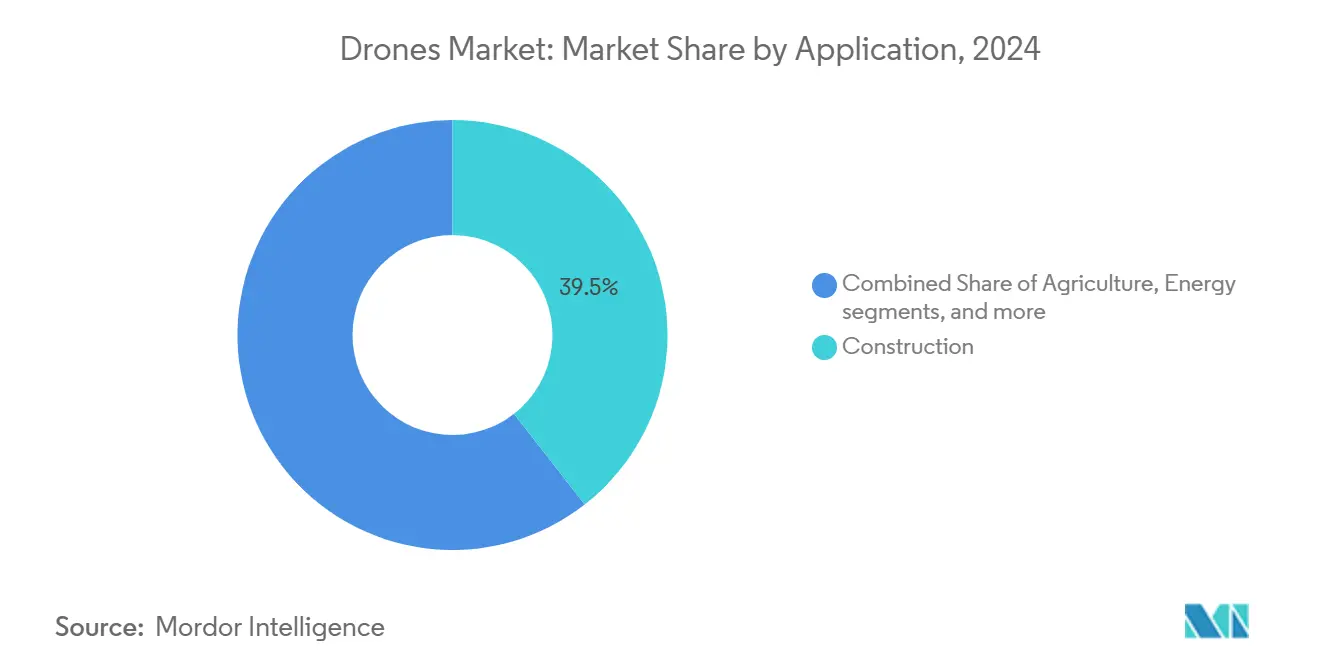

- By application, construction accounted for 39.45% of the drones market share in 2024, whereas the energy segment is forecast to advance at a 19.05% CAGR through 2030.

- By type, fixed-wing platforms led with 45.07% revenue share in 2024; hybrid/VTOL designs are set to expand at a 20.10% CAGR to 2030.

- By weight class, small drones (2–25 kg) captured 43.67% of the drones market size in 2024; large platforms (>150 kg) exhibit an 11.34% CAGR outlook.

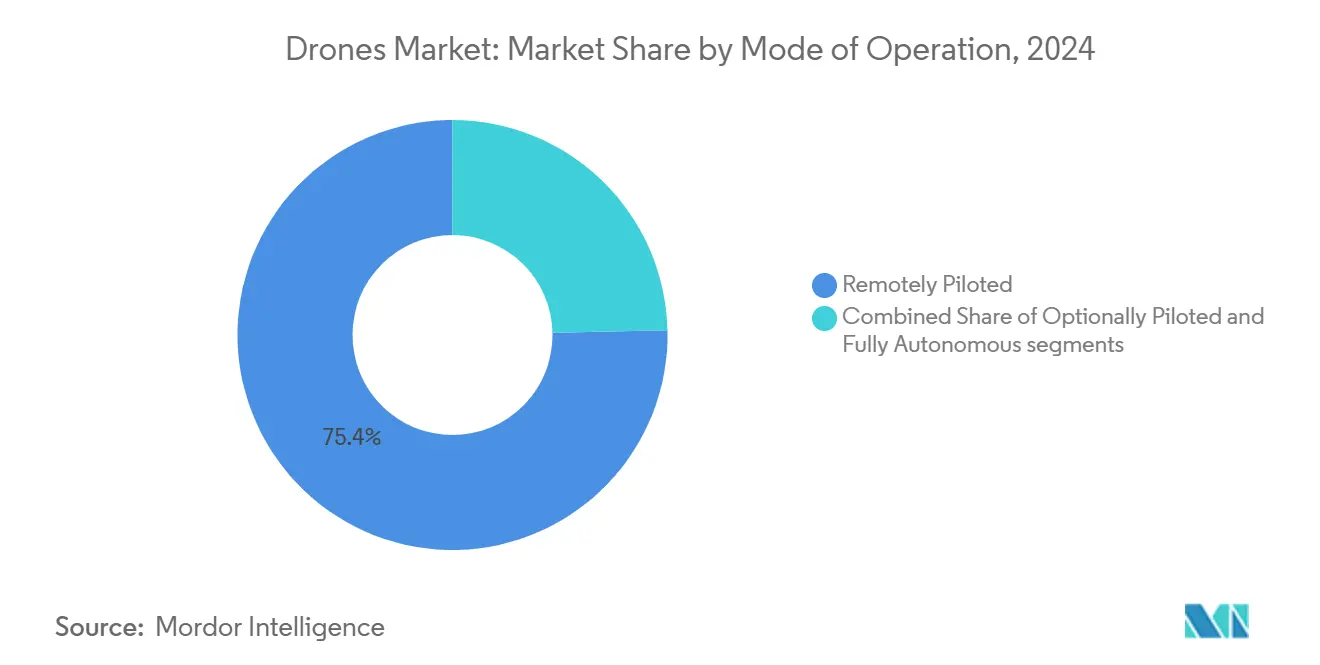

- By mode of operation, remotely piloted systems dominated the drone market, with a 75.35% share in 2024, while fully autonomous models are growing at a 14.97% CAGR.

- By end-user, commercial and consumer segments held 52.55% of the drones market in 2024; government deployments show the fastest 12.54% CAGR to 2030.

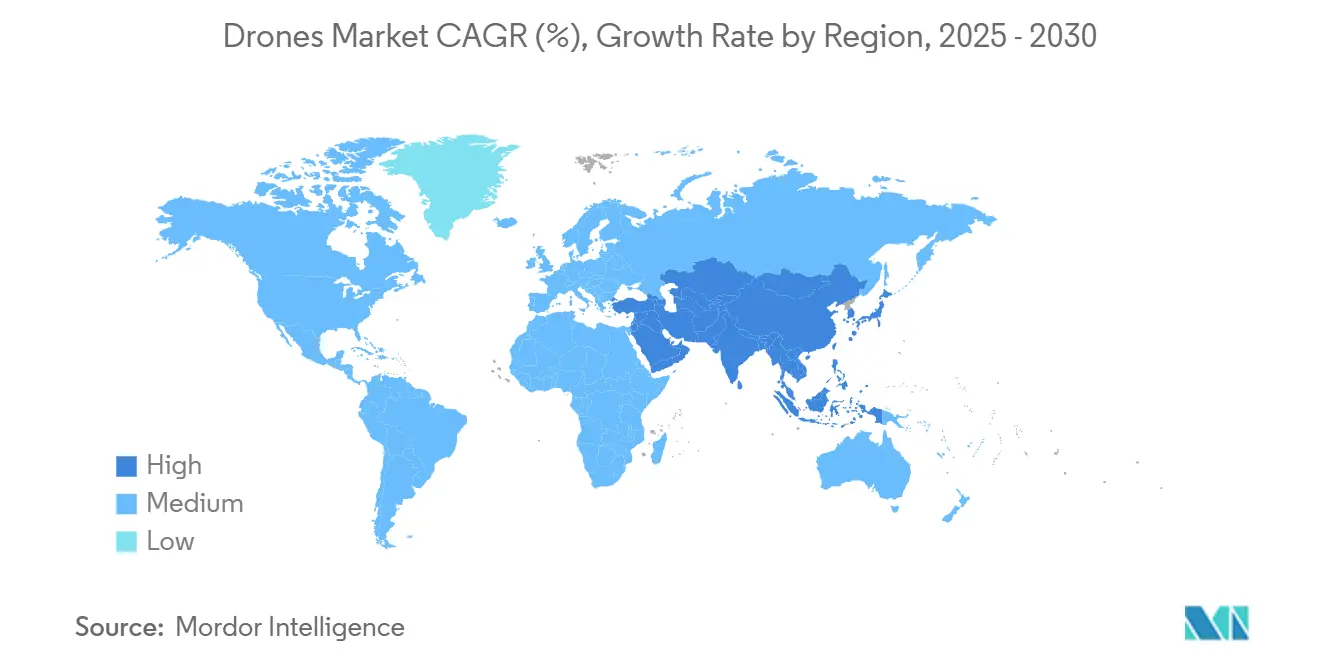

- By geography, North America retained 37.97% of global revenue in 2024; Asia-Pacific is the fastest-growing region, with a 15.27% CAGR.

Global Drones Market Trends and Insights

Drivers Impact Analysis

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| On-board edge-AI maturation: real-time processing unlocks autonomous operations | +3.2% | Global, early uptake in North America and Europe | Medium term (2-4 years) |

| 5G and MEC roll-outs: ultra-low latency enables BVLOS viability | +2.8% | North America and Asia-Pacific core | Medium term (2-4 years) |

| Sensor-cost freefall: Multispectral and LiDAR price declines expand ROI | +2.1% | Global | Short term (≤ 2 years) |

| U-space/UTM standardization: ICAO alignment accelerates cross-border operations | +1.9% | Europe and North America, spreading to Asia-Pacific | Long term (≥ 4 years) |

| On-demand logistics boom | +2.4% | Global, urban centers | Short term (≤ 2 years) |

| Decarbonisation economics | +1.8% | Europe and North America, emerging in Asia-Pacific | Long term (≥ 4 years) |

Source: Mordor Intelligence

On-board Edge-AI Maturation: Real-time Processing Unlocks Autonomous Operations

Edge inference engines now execute object detection, path planning, and contingency logic on lightweight 7-10 W processors, letting drones adapt in complex environments without back-haul latency. Utility operators report downtime cuts of up to 35% when AI-equipped craft flag anomalies and autonomously re-position for detailed imaging, driving strong ROI. Large language models are integrated into safety stacks to boost collision-avoidance decision quality.

5G and MEC Roll-outs: Ultra-low Latency Enables BVLOS Viability

Standalone 5G networks paired with carrier-edge nodes deliver sub-10 ms round-trip latency, removing the need for ground-based radio relays. Valmont’s 77-mile BVLOS inspection over T-Mobile’s 5G grid validated persistent command links and real-time video backhaul. The FCC’s Part 88 rules further cement a protected 5030-5091 MHz corridor for drone command channels.[1]Federal Communications Commission, “FCC Adopts Service Rules for the 5030-5091 MHz Band,” fcc.gov

Sensor-Cost Freefall: Multispectral and LiDAR Price Declines Expand ROI

Steep, ongoing price cuts for multispectral, thermal, and solid-state LiDAR modules open once-prohibitive drone use cases to smaller operators. Farms that previously relied on manual scouting now adopt real-time crop health mapping because sensors that cost thousands of dollars in 2018 sell for a fraction today. Lower hardware prices also accelerate infrastructure monitoring, where sensor fusion lets drones navigate cluttered corridors and flag defects without human guidance. Utilities report 78% better measurement accuracy when laser-induced breakdown spectroscopy pairs with thermal imaging, strengthening the business case for autonomous inspections. As manufacturers scale volumes and new entrants intensify competition, further cost compression is likely, expanding addressable opportunities in construction, energy, and environmental surveillance.

U-space/UTM Standardization: ICAO Alignment Accelerates Cross-border Operations

The ICAO Council’s SARPs for Remotely Piloted Aircraft Systems mirror legacy aviation rules, allowing operators to leverage a single certificate across regions.[2]International Civil Aviation Organization, “Standards and Recommended Practices for Remotely Piloted Aircraft Systems,” icao.int EASA’s Easy Access Rules for U-space establish digital air-traffic corridors where coordinated de-confliction supports higher-density missions.[3]European Union Aviation Safety Agency, “Easy Access Rules for U-space,” easa.europa.eu Together, they remove duplicated compliance burdens for multinational fleets.

Restraints Impact Analysis

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lithium-ion cell supply crunch inflating small-UAV BOM costs | -1.8% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Stringent India RPAS import bans limiting foreign OEM revenue | -0.9% | India, spill-over in South Asia | Medium term (2-4 years) |

| Privacy-by-design rules in EU slowing urban adoption | -0.7% | Europe, possible global uptake | Long term (≥ 4 years) |

| Spectrum-sharing conflicts with 5G mmWave bands | -0.6% | Global, dense urban zones | Medium term (2-4 years) |

Source: Mordor Intelligence

Lithium-ion Cell Supply Crunch Inflating Small-UAV BOM Costs

Battery cells comprise up to one-quarter of typical small-drone costs, and 30-40% price hikes since 2024 have forced OEMs either to absorb margin compression or lift selling prices. Geopolitical tensions and rising EV demand exacerbate the shortage, while China’s export curbs on key battery minerals threaten longer-term capacity.

Stringent India RPAS Import Bans Limiting Foreign OEM Revenue

India’s ban on finished-drone imports still caps a USD 1 billion addressable market and forces foreign brands to build locally or exit altogether. Global leaders such as DJI face a stark choice between joint ventures and lost sales, reshaping competitive dynamics in one of the world’s fastest-growing drone arenas. Despite the rules, grey-market inflows remain large; estimates suggest 90% of India’s 500,000 drones are unregistered Chinese models. The Production-Linked Incentive scheme directs INR 120 crore (USD 14.4 million) toward 27 domestic firms, but matching Chinese price-performance ratios is proving hard. While the policy nurtures local startups, limited technology transfer and higher component costs could slow overall market maturity compared with more open regimes.

Segment Analysis

By Application: Construction Dominance Faces Energy-Sector Disruption

Construction held 39.45% of the drones market in 2024 as aerial progress tracking, 3-D modeling, and site security became mainstream. High-resolution photogrammetry slashes survey time by over 70% compared with manual methods, while automated volume calculations speed payment cycles. The energy industry, though smaller, exhibits a 19.05% CAGR that could narrow the gap by 2030. Utilities now swap helicopters for AI-guided rotorcraft that spot insulator cracks or thermal hotspots in a single sortie, achieving around 60% annual cost savings. Agriculture follows closely, thanks to FAA-approved swarm spraying; firms such as Hylio report that over half of clients now deploy multi-drone swarms to cover large acreages.

Momentum is also building in public safety and entertainment. In trials, drone-as-first-responder (DFR) programs cut dispatch times from eight to 3.5 minutes, augmenting community policing efficiency. Cinematography continues to push payload innovation, encouraging wider sensor integration. These trends point to a progressively diversified drone market, each niche optimizing specific airframe, sensor, and autonomy requirements.

Note: Segment shares of all individual segments available upon report purchase

By Type: Fixed-Wing Leadership Challenged by Hybrid Innovation

Fixed-wing craft commanded 45.07% of 2024 revenue, prized for low energy consumption over long linear corridors such as pipelines. Yet, hybrid VTOL aircraft are scaling at 20.10% CAGR as urban air-mobility operators need vertical take-off to fit space-constrained rooftops. Rotary-wing units remain essential for hovering jobs like telecom-tower inspection or search-and-rescue. EHang’s EH216-S achieved the world’s first. Adoption of composite materials is another differentiator. Carbon-fiber-reinforced polymer airframes trim weight by up to 15% while preserving stiffness, directly extending range. Meanwhile, bio-based resins show promise for end-of-life recyclability, reflecting rising environmental scrutiny across the drone type certificate for a pilotless passenger eVTOL in 2024, underscoring hybrid viability.[4]EHang Holdings Limited, “EH216-S Obtains Type Certificate and Completes First Urban Flight,” ehang.com

Adoption of composite materials is another differentiator. Carbon-fiber-reinforced polymer airframes trim weight by up to 15% while preserving stiffness, directly extending range. Meanwhile, bio-based resins show promise for end-of-life recyclability, reflecting rising environmental scrutiny across the drone industry.

By Weight Class: Small Platforms Dominate, Large Cargo Drones Accelerate

Small airframes between 2 kg and 25 kg captured 43.67% of the drones market share in 2024, thanks to lighter regulatory burdens and flexible mission profiles. Large drones above 150 kg show an 11.34% CAGR as cargo and eVTOL passenger services inch toward certification. The FAA’s decision to let one operator supervise multiple heavy drones allows agriculture fleets to scale without proportional labor costs. Hylio has ramped up production to meet surging demand.

Battery-specific energy improvements and higher-torque motors enable heavier payloads within existing categories, blurring traditional weight boundaries. Modular payload bays further let operators up-gauge or down-gauge sensors without swapping airframes, reinforcing platform longevity.

By Mode of Operation: Remote Piloting Prevails While Autonomy Gains Ground

Human-in-the-loop control covered 75.35% of flights in 2024, mirroring regulatory norms still demanding a licensed remote pilot for most commercial sorties. Nevertheless, fully autonomous missions will grow at 14.97% CAGR as risk-based frameworks gain traction. The FAA’s draft BVLOS rule, if finalized, will let qualified systems self-separate from other traffic, accelerating adoption.[5]Federal Aviation Administration, “Unmanned Aircraft Systems (UAS) Beyond Visual Line of Sight Notice of Proposed Rulemaking,” faa.gov

Advanced autonomy hinges on AI-driven contingency management. Large language models now interpret flight telemetry and surrounding-aircraft intent, augmenting sense-and-avoid logic for crowded airspace. Optionally piloted platforms remain a transitional bridge, providing manual override for rare edge cases while automating routine legs.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Commercial Leads, Government Demand Rises

Commercial and consumer segments contributed 52.55% of 2024 revenue, spanning construction surveys, media capture, and precision farming. Government and civil agencies, however, will register a 12.54% CAGR to 2030 as public-safety bodies like the Chula Vista Police Department demonstrate measurable response-time reduction through DFR programs.

Defense procurement also expands, with global military drone budgets forecast to triple in the coming decade. Capabilities matured in conflict zones—such as AI-guided loitering munitions—tend to cascade into civilian inspection and security offerings, sustaining a virtuous innovation loop across the drones market.

Geography Analysis

North America produced 37.97% of global 2024 revenue, buoyed by FAA test-site programs and dedicated 5030-5091 MHz spectrum for command links. Wing and Walmart surpassed 150,000 parcel deliveries using fully integrated UTM services, demonstrating commercial readiness at scale. Policy, however, is tightening around data security, with the American Security Drone Act encouraging domestic production to replace Chinese airframes in federal fleets.

Asia-Pacific is the fastest-expanding region, with a 15.27% CAGR. China’s “low-altitude economy” strategy targets a CHY 3.5 trillion yuan (USD 487 billion) market by 2035 and supports local champions with testing corridors and purchase subsidies. India’s import embargo stifles foreign OEMs but fuels nascent manufacturing clusters under the PLI scheme. Japan and South Korea channel drones into infrastructure inspection and tsunami-response missions, reflecting high disaster-preparedness budgets.

Europe remains pivotal, anchored by EASA’s unified U-space blueprint that governs more than 1.6 million registered operators. Stringent privacy-by-design mandates prolong deployment cycles, yet sustainability-oriented projects—like drone-assisted offshore-wind maintenance—keep demand rising. The continent has also approved specific corridors for eVTOL trials, putting manufacturers on a clear path toward air-taxi certification by the late 2020s.

Competitive Landscape

The drones market displays moderate concentration. DJI maintains a commanding global presence, but escalating security reviews in North America and Europe drive public-sector buyers toward domestic suppliers. Merger and acquisitions activity is brisk: traditional aerospace firms acquire niche payload or autonomy specialists to assemble turnkey stacks. This vertical integration approach locks in high-margin software and compliance services alongside hardware sales, raising entry barriers for new pure-hardware entrants.

Two strategic archetypes dominate. Scale players like Wing pursue mass consumer logistics, banking on network effects and per-delivery cost optimization. Specialist vendors like Skydio chase defense and critical-infrastructure clients who prioritize anti-jam resilience and AI precision over unit price; Skydio’s USD 170 million Series E round underscores investor confidence in this premium tier. Meanwhile, Chinese contenders accelerate eVTOL production; EHang’s partnership with JAC Motors opens an automated assembly base aimed at thousands of units annually. Opportunity exists in underserved niches—high-altitude pseudo-satellite (HAPS) relays, arctic inspection, or blockchain-audited flight-log services. Players that combine domain-specific payloads, cloud analytics, and regulatory fluency can carve out a durable share before price competition compresses margins across the broader drone industry.

Drones Industry Leaders

-

SZ DJI Technology Co., Ltd.

-

Parrot Drones SAS

-

AeroVironment, Inc.

-

Skydio, Inc.

-

Yuneec International

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: EHang partnered with JAC Motors and Guoxian Holdings to establish a dedicated eVTOL factory in Hefei, China.

- January 2025: EHang’s EH216-S executed its first downtown-Shanghai flight, showcasing controlled urban air-taxi operations.

- May 2024: EASA published Easy Access Rules for U-space, formalizing automated drone-traffic management across the EU.

- April 2024: Zipline surpassed one million autonomous deliveries and forged new US retail and healthcare partnerships.

Global Drones Market Report Scope

Drones are pilotless platforms that can be remotely controlled by a human operator or navigated autonomously by a programmed onboard computer. Drones provide tremendous potential to transform urban and rural infrastructure and enhance agricultural productivity in developing countries.

The drones market is segmented by application, type, and geography. By application, the market is segmented into agriculture, construction, energy, entertainment, law enforcement, and other applications. The other applications segment of the market includes applications such as firefighting, aerial mapping, etc. By type, the market is segmented into fixed-wing drones and rotary-wing drones. Th market research report also covers the market sizes and market forecast for the drones market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| By Application | Construction | |||

| Agriculture | ||||

| Energy | ||||

| Entertainment | ||||

| Law-Enforcement | ||||

| Other Applications | ||||

| By Type | Fixed-Wing Drones | |||

| Rotary-Wing Drones | ||||

| Hybrid/VTOL Drones | ||||

| By Weight Class | Nano/Micro (Less than 2 kg) | |||

| Small (2 to 25 kg) | ||||

| Medium (25 to150 kg) | ||||

| Large (Greater than 150 kg) | ||||

| By Mode of Operation | Remotely Piloted | |||

| Optionally Piloted | ||||

| Fully Autonomous | ||||

| By End-User | Commercial and Consumer | |||

| Government and Civil | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | United Kingdom | |||

| Germany | ||||

| France | ||||

| Russia | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| India | ||||

| Japan | ||||

| South Korea | ||||

| Rest of Asia-Pacific | ||||

| South America | Brazil | |||

| Rest of South America | ||||

| Middle East and Africa | Middle East | United Arab Emirates | ||

| Saudi Arabia | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Rest of Africa | ||||

By Application

| Construction |

| Agriculture |

| Energy |

| Entertainment |

| Law-Enforcement |

| Other Applications |

By Type

| Fixed-Wing Drones |

| Rotary-Wing Drones |

| Hybrid/VTOL Drones |

By Weight Class

| Nano/Micro (Less than 2 kg) |

| Small (2 to 25 kg) |

| Medium (25 to150 kg) |

| Large (Greater than 150 kg) |

By Mode of Operation

| Remotely Piloted |

| Optionally Piloted |

| Fully Autonomous |

By End-User

| Commercial and Consumer |

| Government and Civil |

By Geography

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the drones market?

The drones market reached USD 41.79 billion in 2025.

How fast will the drones market grow through 2030?

It is projected to expand at a 13.9% CAGR, hitting USD 43.07 billion by 2030.

Which application segment grows the quickest?

Energy-sector deployments are forecasted to grow at 19.05% CAGR as utilities replace helicopters with autonomous inspection fleets.

Why are hybrid/VTOL drones gaining popularity?

Hybrid VTOL combines vertical take-off with fixed-wing cruise efficiency, a mix suited to urban air-mobility routes and logistics, fueling a 20.10% CAGR through 2030.

How do 5G networks influence BVLOS operations?

Sub-10 ms latency on 5G with edge-computing nodes supports reliable long-range command links, allowing regulators to craft safer BVLOS rules.

Which region will add the most incremental revenue by 2030?

Asia-Pacific, led by China’s low-altitude-economy initiatives, is expected to generate the largest absolute revenue gain thanks to a 15.27% CAGR.

Page last updated on: June 23, 2025