Drill Collar Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.51 Billion |

| Market Size (2031) | USD 1.91 Billion |

| Growth Rate (2026 - 2031) | 4.81% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Drill Collar Market Analysis by Mordor Intelligence

The Drill Collar Market size is projected to be USD 1.44 billion in 2025, USD 1.51 billion in 2026, and reach USD 1.91 billion by 2031, growing at a CAGR of 4.81% from 2026 to 2031. Despite this measured, steady trajectory, the drill collar market is entering a transition phase. Demand is tilting toward heavier bottom-hole assemblies that can survive higher pressures and temperatures, even as land-rig activity moderates in North America. Weight-optimized designs are gaining favor because hybrid rigs use less fuel when the drill string is lighter, and that helps operators meet tightening emissions rules in Norway and under the United States Environmental Protection Agency’s methane program.[1]United States Environmental Protection Agency, “Final Rule: Oil and Natural Gas Sector Climate Review,” epa.gov Meanwhile, non-magnetic collars are moving from niche to mainstream as high-frequency LWD and rotary-steerable tools roll out across both shale and deepwater campaigns. Digital-twin fatigue monitoring is also starting to elongate service life, stretching replacement cycles and reshaping the revenue mix toward high-alloy variants.

Key Report Takeaways

- By type, standard steel held 65.1% of the drill collar market share in 2025, while non-magnetic drill collars are projected to grow at a 5.5% CAGR through 2031.

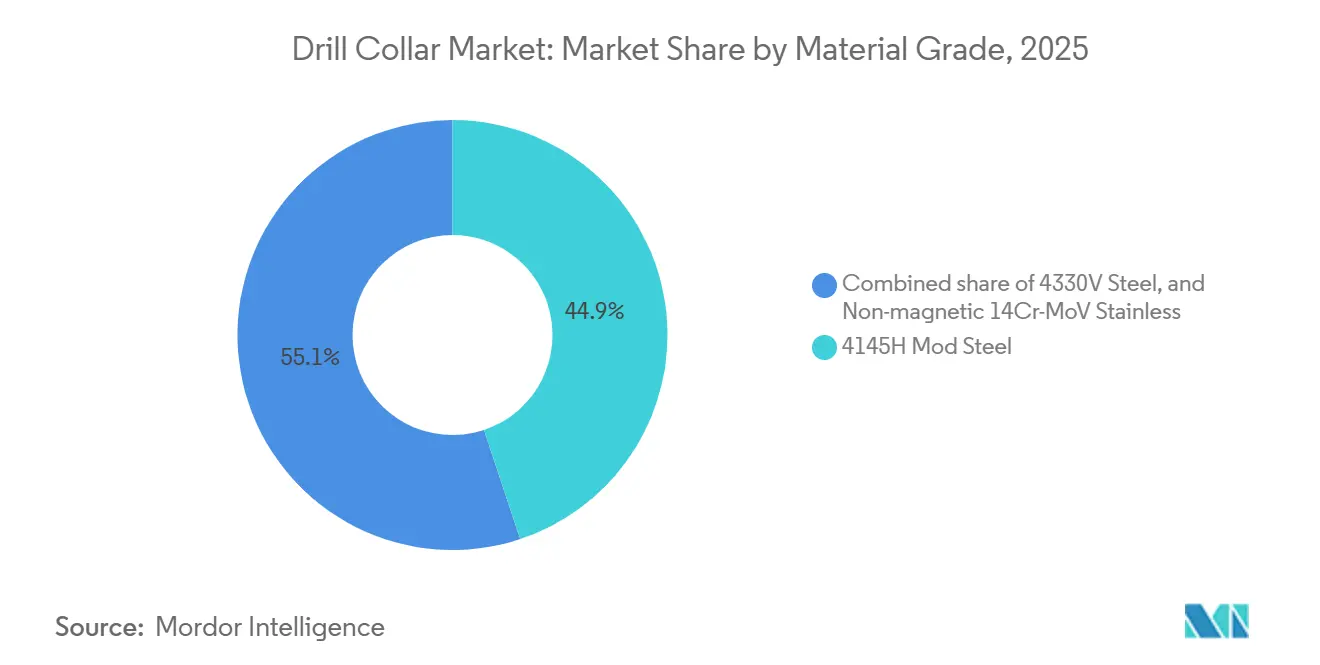

- By material grade, 4145H mod steel commanded 44.9% revenue in 2025, yet non-magnetic 14Cr-MoV stainless is expected to advance at a 5.8% CAGR through 2031.

- By deployment, onshore operations accounted for a 60.3% share of the drill collar market size in 2025, whereas offshore deployment is expected to expand at a 5.3% CAGR through 2031.

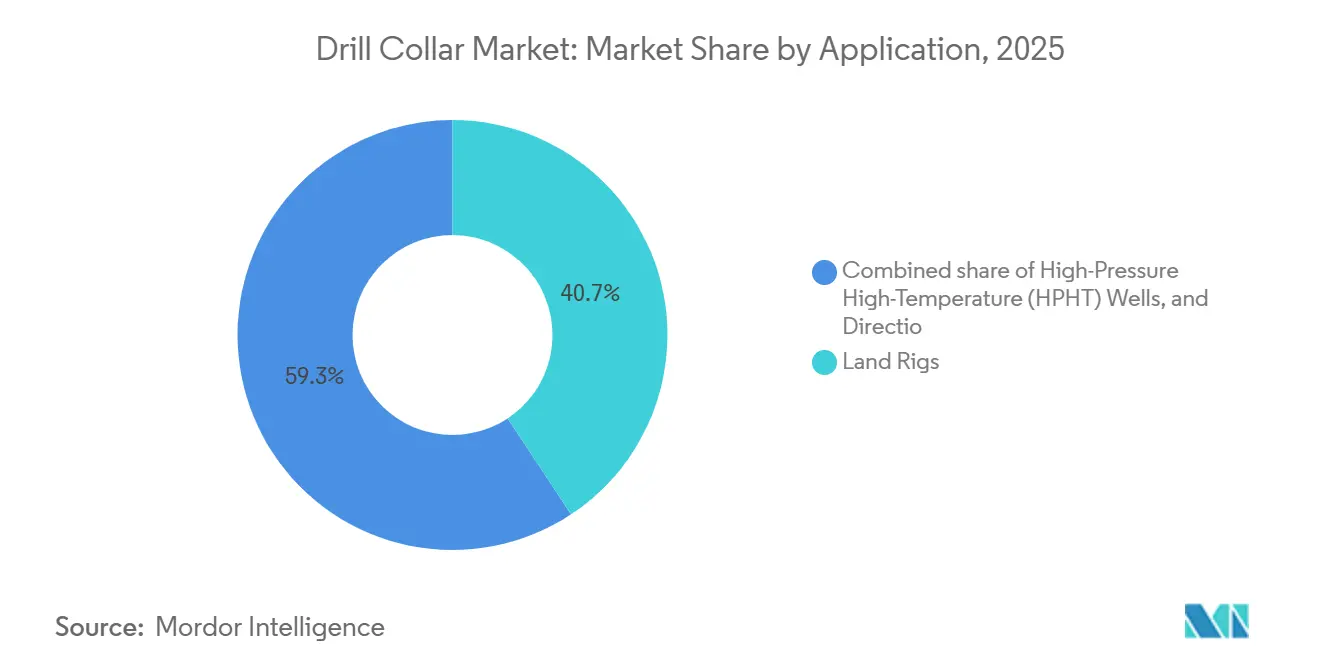

- By application, land rigs commanded 40.7% revenue in 2025, yet directional and horizontal drilling is advancing at a 6.0% CAGR into 2031.

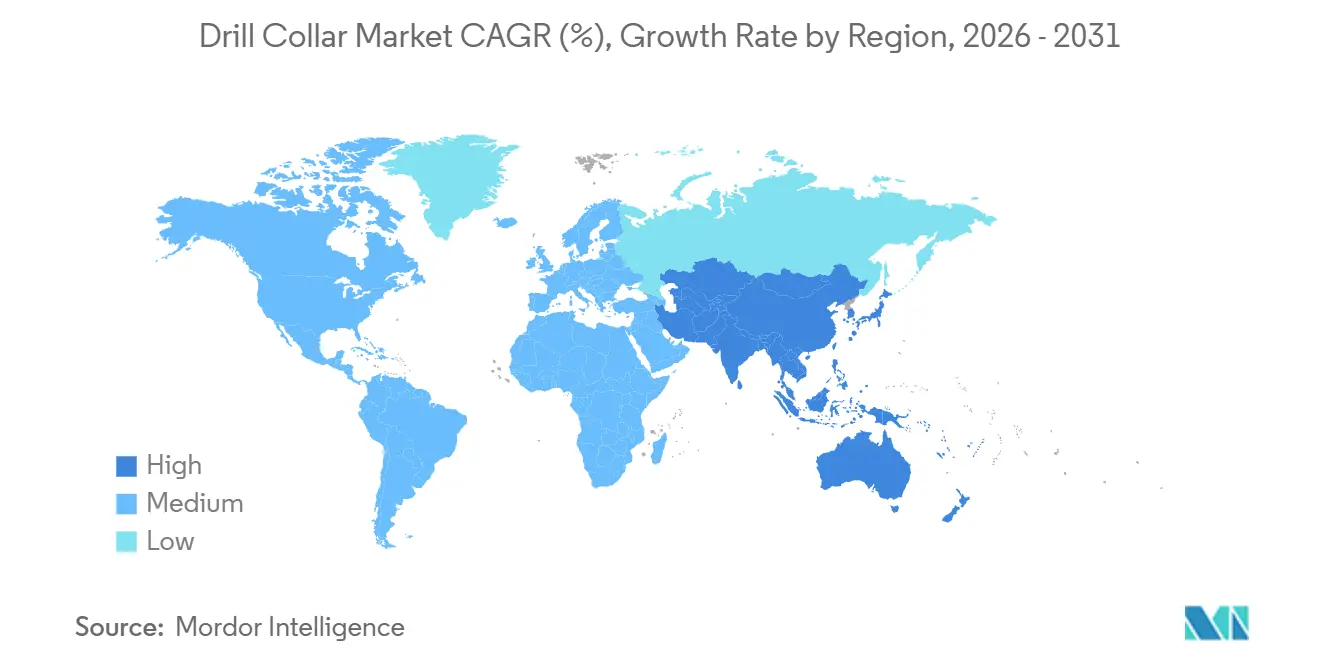

- By geography, North America led with 38.5% of the drill collar market share in 2025, while Asia-Pacific is forecast to record the fastest regional growth at a 6.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Drill Collar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovery in global rig counts post 2025 | +1.2% | Global, Middle East & Asia-Pacific | Medium term (2-4 years) |

| Growth of deep- & ultra-deepwater projects | +1.5% | Brazil, U.S. Gulf of Mexico, West Africa, Norway | Long term (≥ 4 years) |

| Rapid adoption of directional & horizontal drilling | +1.3% | North America shale, Middle East ERD, Asia-Pacific unconventionals | Medium term (2-4 years) |

| OEM-led collar weight optimization | +0.4% | Europe, North America | Short term (≤ 2 years) |

| Surging demand for non-magnetic collars | +0.8% | HPHT basins worldwide | Medium term (2-4 years) |

| Digital-twin fatigue-life prediction | +0.3% | North America and Europe first adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Recovery in Global Rig Counts Post 2025

International rig activity found a floor in early 2026 with 1,058 units working, including 229 offshore rigs, after several years of attrition.[2]Baker Hughes, “Rig Count Overview,” bakerhughes.com ADNOC Drilling reinforced the upward trend by ordering two premium jack-ups valued at USD 1.15 billion in January 2026.[3]ADNOC Drilling, “Investor Presentation 2026,” adnoc.ae India’s regulator outlined a USD 100 billion upstream target that includes 40 deepwater wildcats, each demanding dedicated drill-collar strings.[4]Offshore Technology, “India Deepwater Investment Outlook,” offshore-technology.com Reactivated eighth-generation drillships employ hybrid power that cuts fuel use by as much as 30%, yet the deeper wells they target require heavier collars to deliver weight-on-bit at 2,000 m water depth. As a result, demand is migrating from high-volume, low-spec replacements to lower-volume, high-spec upgrades.

Growth of Deep- & Ultra-Deepwater Drilling Projects

Petrobras approved SEAP I and SEAP II in early 2025, earmarking more than USD 12 billion for 32 wells in reservoirs beyond 2,000 m depth, with pressures above 15,000 psi that mandate 4330V or 14Cr-MoV collars. Beacon Offshore Energy’s Shenandoah field surpassed 100,000 bpd under 20,000 psi conditions, underscoring the shift toward extreme environments. Equinor allocated NOK 140 billion (USD 13.1 billion) for 2026 projects such as Johan Sverdrup Phase 2, where Arctic temperatures demand NORSOK-certified collars. Ultra-deepwater economics depend on avoiding stuck-pipe events that cost USD 1 million per day, so operators invest in collars forged for high yield strength and paired with real-time fatigue models. These technical thresholds are pushing the drill collar market toward premium metallurgy and digital support services.

Rapid Adoption of Directional & Horizontal Drilling

Directional and horizontal wells are expanding at 6.0% CAGR to 2031 as operators stretch laterals past 3,000 m to boost recovery. Halliburton’s HyperSteer MX rotary-steerable bit, launched in January 2026, enables build rates up to 15° per 30 m and relies on non-magnetic collars for azimuth accuracy within ±0.5°. The United States Permian Basin hosted 303 active rigs in April 2026, yet average lateral length rose from 2,400 m to 2,700 m, adding extra collar joints per well. Saudi Aramco’s renewals with Arabian Drilling emphasize extended-reach wells topping 2,500 m laterals, again reinforcing the need for non-magnetic alloys. Tightened permeability tolerances below 1.005 relative units are now routine, further differentiating premium suppliers.

OEM-Led Collar Weight Optimization to Cut Rig Emissions

Norway’s carbon tax reached NOK 2,000 per tonne (USD 184) in 2024, compelling operators to cut fuel burn wherever possible. Maersk’s hybrid jack-ups achieve 20–30% fuel savings, but string weight still dictates drawworks power. Manufacturers are trimming collar wall thickness by up to 10%, lowering hoist loads by roughly 15 t on a 3,000 m string. Shelf Drilling estimates that its hybrid unit shaves 1,800 t of CO₂ annually under this optimized design. The U.S. EPA methane standard finalized in 2024 adds regulatory momentum, rewarding rigs that consume less diesel through lighter strings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-oil price volatility dampens E&P CAPEX | -1.0% | Global, acute in North America shale & marginal offshore plays | Short term (≤ 2 years) |

| Availability of substitute down-hole weight solutions | -0.5% | North America land drilling, price-sensitive emerging markets | Medium term (2-4 years) |

| Supply crunch in low-permeability alloys | -0.3% | Europe and Asia specialty steel mills | Short term (≤ 2 years) |

| Stricter drilling-waste rules shorten collar cycles | -0.2% | Europe (OSPAR), North America (EPA), Asia-Pacific over time | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-Oil Price Volatility Dampens E&P CAPEX

The U.S. Energy Information Administration noted a 14% decline in upstream capital spending during 2024 and a 9% slide in cash flow among public producers, squeezing discretionary drilling budgets. Chevron disclosed a USD 18–19 billion 2026 capital plan but tied any upside to Brent benchmarks stabilizing above USD 70 per barrel. Operators can quickly defer completions or idle rigs without near-term production loss, causing sporadic demand swings for drill collars. Such pullbacks typically hit standard steel orders first, compressing plant utilization and eroding margins. In regions where breakeven prices hover near global benchmarks, procurement teams delay high-alloy purchases, slowing unit growth in the drill collar market.

Availability of Substitute Down-Hole Weight Solutions

Heavy-weight drill pipe offers a cheaper intermediate between normal pipe and collars, trimming rental expense by up to 20% in vertical and low-angle onshore wells. Hunting secured USD 231 million in Kuwait OCTG contracts that bundle HWDP with premium threads, challenging conventional collar suppliers. The product works best in shale laterals where only the build section needs non-magnetic collars, while the vertical interval carries HWDP. However, HWDP fatigue life drops sharply when dogleg severity tops 3° per 30 m, forcing operators back to true collars in complex wells. This substitution risk keeps pricing discipline tight in the standard-steel portion of the drill collar market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Non-Magnetic Variants Capture Directional Premium

Standard steel accounted for 65.1% of 2025 volume, reflecting its low cost and readiness for vertical wells. Non-magnetic collars, however, are expanding at 5.5% CAGR because high-frequency sensors cannot tolerate magnetic permeability above 1.01. The drill collar market size for non-magnetic variants is projected to expand from 2026 through 2031 as subsalt and long-reach laterals proliferate. Halliburton’s EarthStar 3DX now specifies this metallurgy on every HPHT BHA, validating the premium.

Manufacturers exploit the pricing headroom: Schoeller-Bleckmann’s 2024 EBIT margin reached 15.0% on stronger alloy demand. Standard steel continues to dominate U.S. shale where vertical sections exceed 1,500 m and operators recycle inventory aggressively. Yet as wired pipe migrates into land operations, sensor density rises and the non-magnetic share of the drill collar market rises alongside.

By Material Grade: Specialty Alloys Command HPHT Premium

4145H modified steel secured 44.9% of 2025 shipments thanks to its API acceptance and balanced cost. Non-magnetic 14Cr-MoV stainless is the fastest-growing grade at 5.8% CAGR, supported by pre-salt wells with high CO₂ and H₂S exposure. Drill collar market size growth in this grade is most noticeable in the U.S. Gulf of Mexico’s 20,000 psi projects.

4330V provides a higher-strength middle ground for Arctic and ultra-deepwater applications. Equinor employs it in Johan Sverdrup Phase 2 where seabed temperatures hover near 4 °C. Premium connections such as Tenaris Dopeless reduce galling risk, extending reuse cycles and shielding operators from volatile alloy prices.

By Deployment: Offshore Complexity Drives Specification Upgrades

Onshore held 60.3% volume in 2025, yet offshore is growing faster at 5.3% CAGR because every ultra-deepwater string can consume 30–40% more collar weight than a land well. ADNOC Drilling’s latest jack-ups integrate AI to adjust weight-on-bit in real time, demanding collars with surplus fatigue margins. In contrast, the United States Permian builds remain largely standard-steel, keeping unit costs low.

Offshore wells also impose stricter certification: NORSOK D-010 and ISO 10423 compliance are mandatory for North Sea programs, limiting supplier pools and buttressing prices. As hybrid power rigs move worldwide, weight optimization intersects with deepwater torque requirements, sustaining a premium tier within the drill collar market.

By Application: Directional Wells Demand Survey Precision

Land rigs captured 40.7% revenue in 2025, yet directional and horizontal drilling is on track for the quickest expansion at 6.0% CAGR. Every incremental 300 m of lateral length typically necessitates one extra non-magnetic collar, compounding demand. Drill collar market size gains therefore track closely with the lateral-length trend in shale and in extended-reach offshore projects.

HPHT wells, estimated at roughly one-quarter of offshore drilling in 2025, use specialty alloys throughout the BHA. Transocean’s Deepwater Aquila requires collars rated for 20,000 psi stack pressure. While these wells are few, each consumes a high-value package, lifting average selling prices across the drill collar market.

Geography Analysis

North America commanded 38.5% share in 2025 on the back of Gulf of Mexico deepwater and U.S. shale intensity, though regional rig counts slipped to 548 units by April 2026. Chevron still directs roughly USD 7 billion of its 2026 budget to Gulf projects, maintaining a floor for non-magnetic and HPHT-rated demand. Canada’s modest 54 working rigs grapple with takeaway constraints, tempering collar consumption but supporting niche suppliers skilled in cold-weather metallurgy.

Asia-Pacific is forecast to grow at 6.2% CAGR through 2031, the fastest pace among regions. India’s Directorate General of Hydrocarbons is steering USD 100 billion toward upstream work that includes 40 deepwater wildcats, each requiring dedicated drill-collar strings. ONGC’s USD 385.5 million contract for Krishna-Godavari drilling places early orders for HPHT-ready alloys. CNOOC’s Wenchang 16-2 adds regional pull, relying on domestic mills for shorter lead times.

Europe growth is anchored by Norway. Equinor’s NOK 140 billion 2026 plan keeps Johan Sverdrup on plateau and moves Breidablikk toward 140,000 bpd, both certified under Arctic drilling codes. Norway’s sharp CO₂ price encourages hybrid rigs that paradoxically need stiffer, heavier collars to manage deeper wells. In the Middle East and Africa, ADNOC Drilling’s USD 3.6 billion award slate confirms prolonged appetite for premium BHAs.

Competitive Landscape

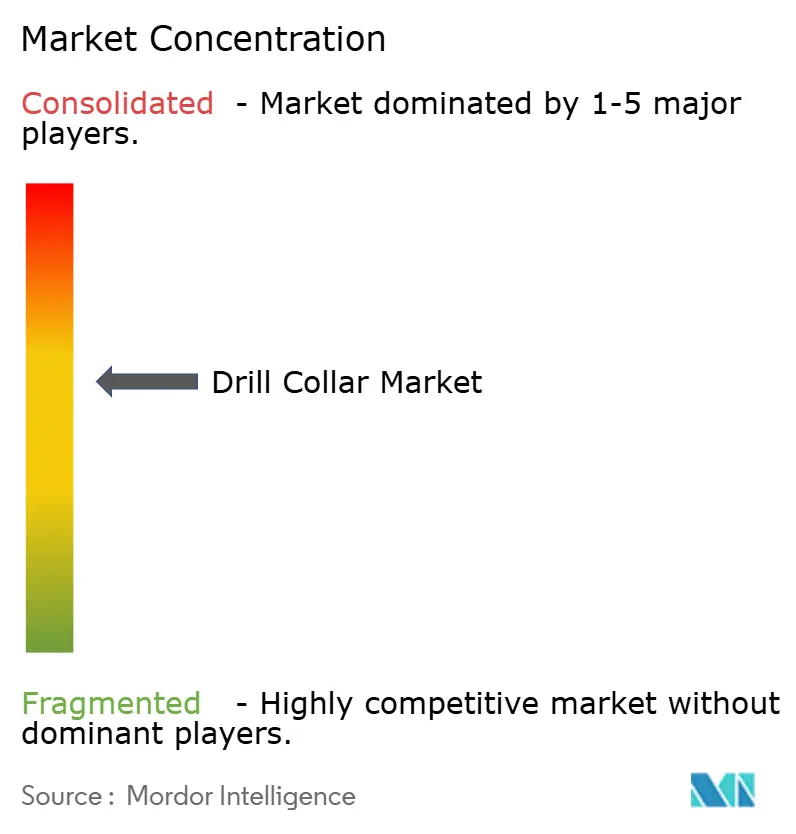

The drill collar market is moderately concentrated. The key vendors, including Schlumberger, National Oilwell Varco, Tenaris, Hunting, and Vallourec, hold a significant share of installed forging capacity and manage substantial raw-steel streams, thereby reducing mill-to-rig lead times. Schoeller-Bleckmann reported a 15.0% EBIT margin in Q3 2024, indicating strong pricing for non-magnetic collars. Tenaris allocated USD 16 million to double production in Midland, Texas, and reduce Permian delivery times from eight weeks to four weeks.

Digital differentiation is widening. Precision Drilling halved downtime with analytics in 2025 and is marketing similar fatigue models to operators. Schlumberger’s connector study with Mines validates a 30% life threshold, bringing service contracts that blend hardware and software into focus. Chinese mills such as Zhong Yuan Special Steel leverage domestic content rules to win APAC tenders within six-week windows, eroding the delivery advantage once held by European suppliers.

Regulatory gates remain high. API 7-1 mechanical tests, ISO 10424-1 threading, and sour-service certification under NACE MR0175 narrow the qualified supplier list. Vendors with integrated ultrasonic inspection and third-party witness capacity enjoy structural margins. Still, HWDP substitution and crude-price swings keep competition keen in the standard-steel tier of the drill collar market.

Drill Collar Industry Leaders

Schlumberger Limited

National Oilwell Varco (NOV)

Hunting PLC

Schoeller-Bleckmann Oilfield Equipment AG

Vallourec S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Halliburton introduced HyperSteer MX rotary-steerable bits, boosting build rates and reinforcing non-magnetic collar demand.

- December 2025: Petrobras endorsed a USD 109 billion 2026–2030 plan with 62% for pre-salt E&P, assuring sustained premium-alloy purchases.

- May 2025: ADNOC Drilling ordered two premium jack-ups worth USD 1.15 billion, each integrating AI for real-time drilling optimization and requiring heavier collars.

- May 2025: Halliburton released EarthStar 3DX, a 30,000 psi, 200 °C LWD platform that demands non-magnetic collars with permeability below 1.01

Global Drill Collar Market Report Scope

Located at the base of a drill string, a drill collar is a robust, thick-walled tube. Its primary function is to exert an axial load, termed Weight on Bit (WOB), facilitating the cutting through rock. As integral components of the bottom-hole assembly (BHA), drill collars impart stiffness to ensure a straight borehole and maintain tension, thereby averting drill pipe failures. The drill collar market encompasses the production, supply, and rental of these heavy, thick-walled steel pipes be it slick or spiral. These pipes, pivotal in bottom-hole assemblies (BHA), not only provide the essential weight-on-bit (WOB) but also play a crucial role in stabilizing drilling operations. Fueled by the relentless pursuit of oil and gas exploration and an escalating demand for energy, the market is witnessing robust growth, especially with the surge in horizontal and offshore drilling activities.

The Drill Collar market is segmented into type, material grade, deployment, application, and geography. By type, the market is divided into Standard Steel Drill Collar, and Non-Magnetic Drill Collar. By material grade, the market is segmented into 4145H Mod Steel, 4330V Steel, and Non-Magnetic 14Cr-MoV Stainless. By deployment, the market is divided among onshore and offshore. By application, the market is segmented into Land Rigs, HPHT Wells, Directional and Horizontal Drilling. The report also covers the market size and forecasts across major regions. The market sizing and forecasts for each segment are based on revenue (in USD).

| Standard Steel Drill Collar |

| Non-magnetic Drill Collar |

| 4145H Mod Steel |

| 4330V Steel |

| Non-magnetic 14Cr-MoV Stainless |

| Onshore |

| Offshore |

| Land Rigs |

| High-Pressure High-Temperature (HPHT) Wells |

| Directional and Horizontal Drilling |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Norway |

| United Kingdom | |

| Russia | |

| Netherlands | |

| Germany | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Iran | |

| Nigeria | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Standard Steel Drill Collar | |

| Non-magnetic Drill Collar | ||

| By Material Grade | 4145H Mod Steel | |

| 4330V Steel | ||

| Non-magnetic 14Cr-MoV Stainless | ||

| By Deployment | Onshore | |

| Offshore | ||

| By Application | Land Rigs | |

| High-Pressure High-Temperature (HPHT) Wells | ||

| Directional and Horizontal Drilling | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Norway | |

| United Kingdom | ||

| Russia | ||

| Netherlands | ||

| Germany | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Iran | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the drill collar market by 2031?

The drill collar market is forecast to reach USD 1.91 billion by 2031, supported by a 4.81% CAGR from 2026.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is anticipated to post the highest regional growth, advancing at a 6.2% CAGR on the back of Indian and Chinese deepwater programs.

Why are non-magnetic drill collars gaining traction?

High-frequency MWD/LWD tools and rotary-steerable systems require permeability below 1.01, making non-magnetic alloys indispensable in directional, HPHT, and ultra-deepwater wells.

How does digital-twin technology benefit drill collar operations?

Real-time fatigue modeling predicts remaining life, reducing unplanned downtime by more than 50% and extending collar service life by roughly 1520%.

What role do emissions regulations play in drill collar design?

Carbon pricing and methane rules push operators toward hybrid rigs with lighter strings, spurring OEM weight-optimization programs that trim collar wall thickness without compromising strength.

Which material grades dominate HPHT projects?

Premium 14Cr-MoV stainless and 4330V alloy steels lead HPHT deployments because they withstand pressures above 15,000 psi and temperatures around 150 °C while maintaining low magnetic permeability.

Page last updated on: