Drifter Rock Drill Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

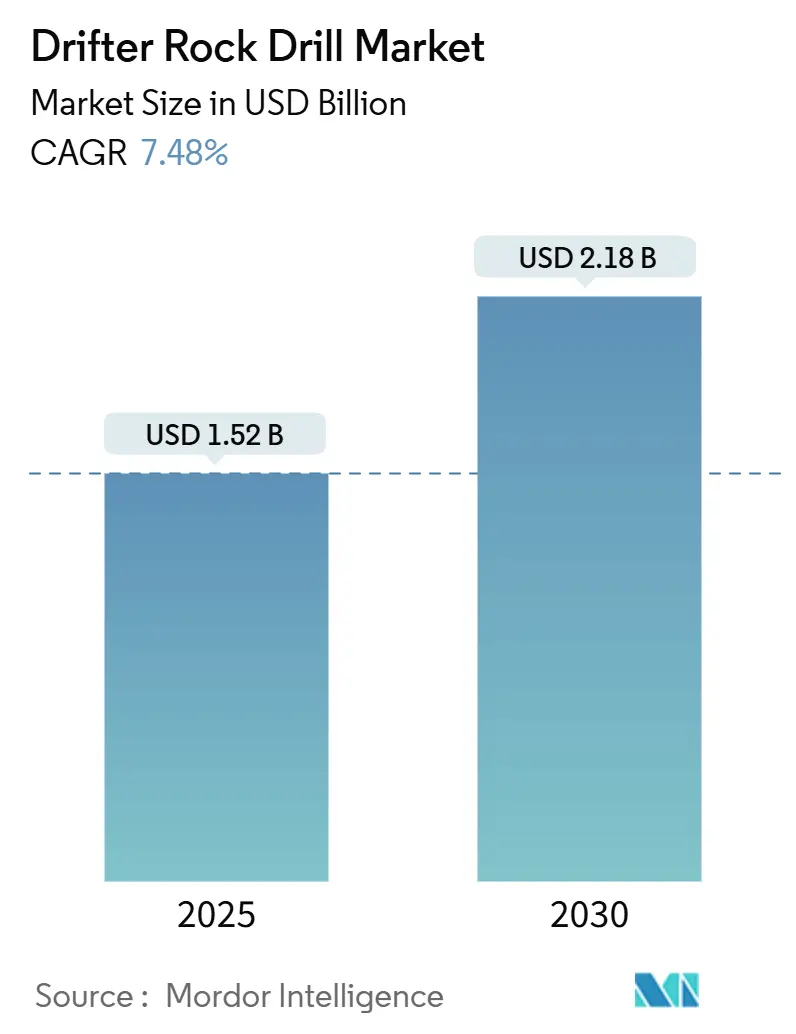

| Market Size (2025) | USD 1.52 Billion |

| Market Size (2030) | USD 2.18 Billion |

| Growth Rate (2025 - 2030) | 7.48% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Drifter Rock Drill Market Analysis by Mordor Intelligence

The Drifter Rock Drill Market size is estimated at USD 1.52 billion in 2025, and is expected to reach USD 2.18 billion by 2030, at a CAGR of 7.48% during the forecast period (2025-2030).

Growing tunnel construction, rising copper and nickel output, and the rapid integration of automation create sustained demand despite raw-material price swings. Hydraulic drifters continue to dominate greenfield and brownfield fleets, yet hybrid platforms increasingly win bids on jobs that blend urban emissions rules with remote-mine logistics. Heavy-duty rigs above 100 horsepower are penetrating iron-ore, copper, and battery-metal pits, while medium-duty machines stay essential for underground headings where profile constraints limit boom size. North America remains the single largest buyer, but Asia-Pacific outpaces all regions as China’s smart-mine mandate and India’s metro build-out accelerate unit turnover. Competition centers on vertical integration, digital services, and retrofit kits that extend asset life while helping operators satisfy tightening ESG covenants.

Key Report Takeaways

- By product type, hydraulic drifters led with 60.5% drifter rock drill market share in 2024, whereas hybrid systems are forecast to grow at a 10.8% CAGR through 2030.

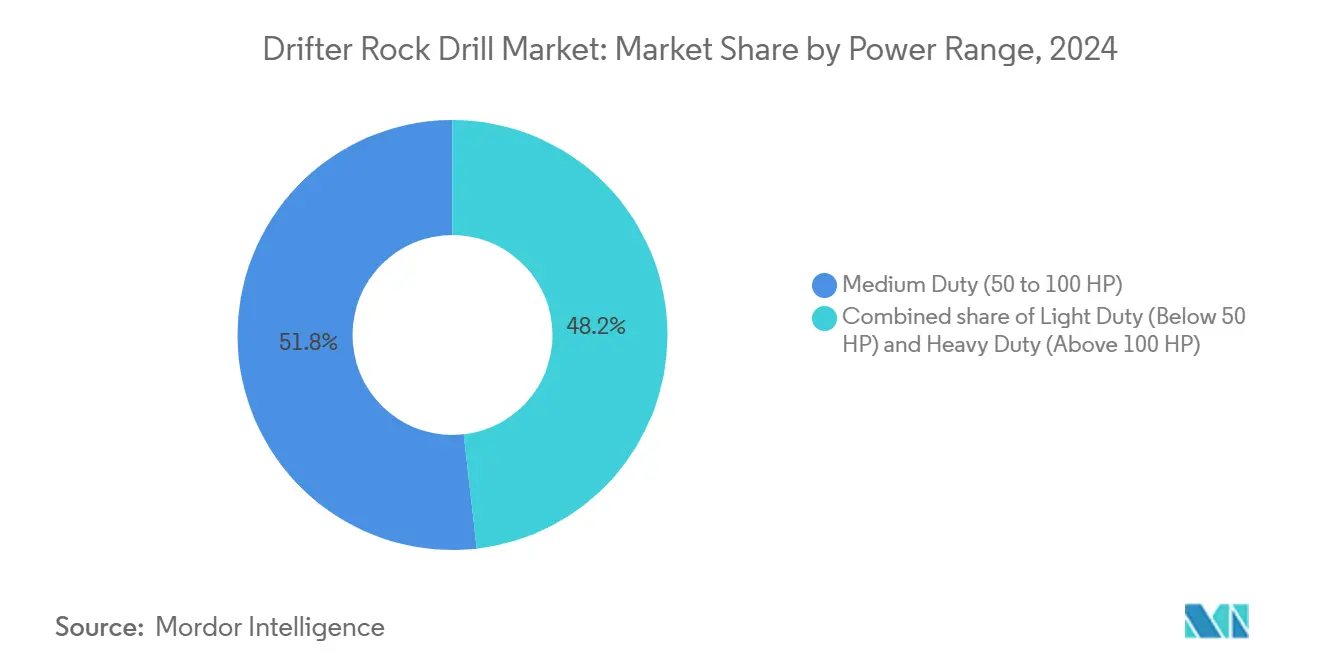

- By power range, medium-duty rigs captured 51.8% of 2024 revenue, but heavy-duty units above 100 HP are on track for a 9.4% CAGR to 2030 RIO.

- By application, underground mining accounted for 44.4% of application revenue in 2024; tunneling and construction activities are projected to expand at a 10.5% CAGR through 2030.

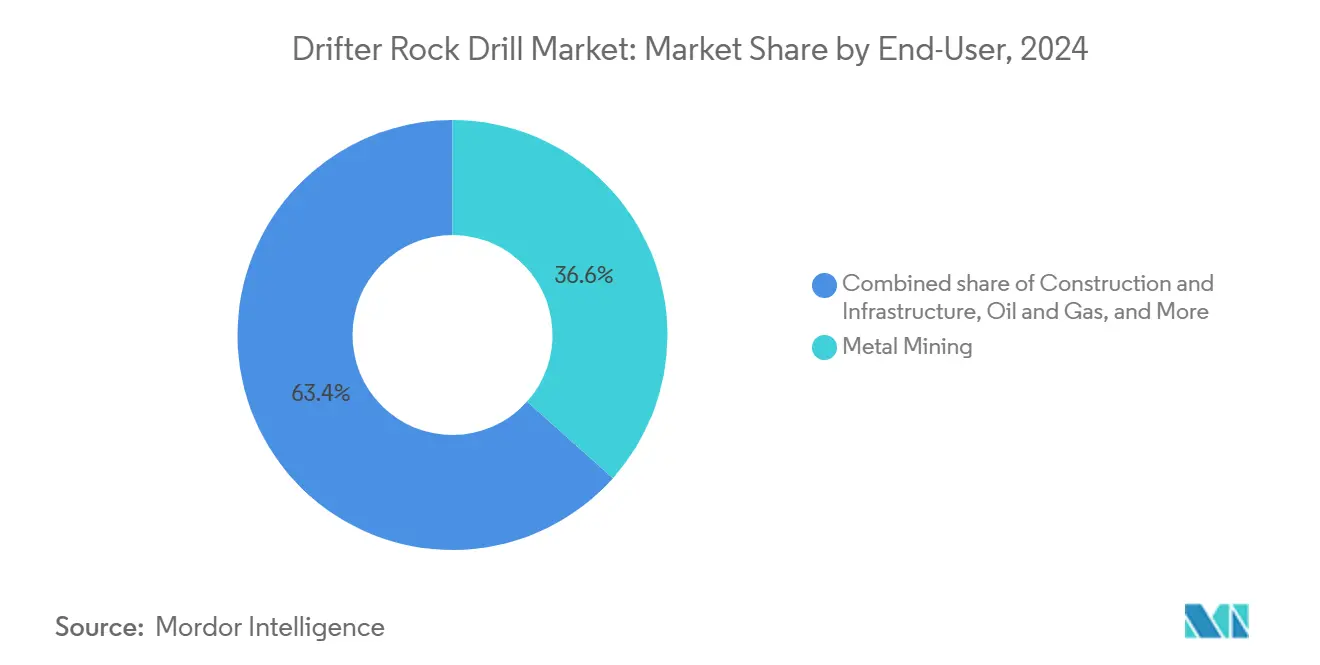

- By end-user, metal mining commanded 36.6% of end-user revenue in 2024, while construction and infrastructure is forecast to grow 8.9% annually to 2030.

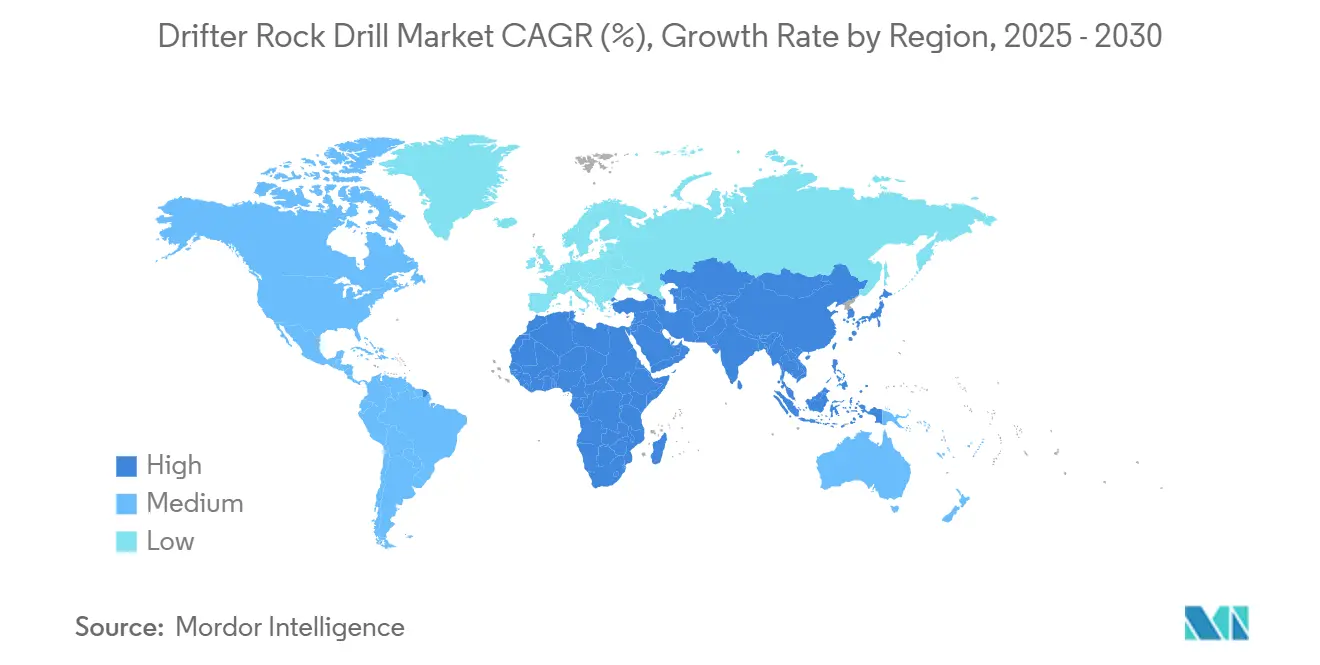

- By geography, North America held 33.3% of 2024 revenue, yet Asia-Pacific is poised for a 9.3% CAGR, the fastest among all regions.

Global Drifter Rock Drill Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Deep-water exploration and production equipment rebounds (post-2025 CAPEX wave) | 0.3% | Global, concentrated in North Sea, Gulf of Mexico, offshore Brazil, West Africa | Medium term (2–4 years) |

| Brown-field well and mine revitalization programs | 0.7% | North America (Appalachian coal, Permian Basin), Australia (mature gold fields), South Africa (deep-level gold) | Short term (≤2 years) |

| National Oil Company and mining entity drill-bit localization mandates | 0.6% | Middle East (Saudi Arabia, UAE), Latin America (Chile, Peru, Argentina), Indonesia | Medium term (2–4 years) |

| Hydrogen-ready gas field retrofits and geothermal drilling | 0.2% | Europe (North Sea hydrogen storage), Middle East (blue hydrogen projects), Iceland and New Zealand (geothermal) | Long term (≥4 years) |

| AI-optimized rig scheduling and autonomous drilling systems | 1.5% | Global, early gains in Australia, Canada, Scandinavia, expanding to Asia-Pacific and North America | Short term (≤2 years) |

| Government royalty-relief and fiscal incentives for ultra-deep mining and drilling | 0.3% | Canada (deep underground mines), Australia (block-cave projects), Chile (deep copper porphyries) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Tunneling And Metro Infrastructure Acceleration Drives Demand For Precision Drilling

Metro and road tunnels from Delhi to Vienna rely on satellite drifter fleets that pre-drill probe holes, grout curtains, and rock bolts before the main TBM face advances.[1]Railway Technology, “Europe–Asia Major Tunnel Projects,” railway-technology.com India’s North-South Corridor has mobilized 42 TBMs supported by more than 1,200 drifter rigs, while Europe’s Brenner Base Tunnel alone is expected to consume 8,000 drill bits each year. ISO 23469 and local geotechnical codes oblige contractors to adopt high-frequency percussion for tight hole spacing, locking in demand for premium drifters. Accelerating public-private financing funnels stable cash flow into equipment budgets, reducing buyer sensitivity to purchase price. Consequently, OEM backlogs for three-boom jumbos with 90-HP drifters extend into late 2026.

Underground Mine Automation And AI-Optimized Scheduling Lift Utilization Rates

Autonomous suites such as Sandvik AutoMine now synchronize multiple jumbos to drill 4-meter rings with sub-centimeter variance.[2]Mining Magazine, “Mine Automation Uptake,” miningmagazine.com Predictive maintenance analytics flag component failures 72 hours in advance, trimming unplanned downtime by nearly 30%. Mine planners upload digital drill logs each shift, updating block models weekly instead of quarterly and redirecting crews toward higher-grade zones. Australia’s work-health regulations that cap underground exposure accelerate remote-operation adoption, making autonomy not just efficient but legally advantageous. Smaller Latin American and African mines lease automation-ready rigs, spreading capital outlay over operating contracts and broadening the buyer base.

Heavy-Duty Equipment Adoption In Surface Mining Pursues Higher Penetration Rates

Producers of iron ore, copper, and lithium are moving from 75-HP crawlers to 120-HP and larger rigs to keep penetration at or above 35 meters per hour in formations exceeding 200 MPa. Chilean regulations tighten burden spacing, forcing tighter drill patterns that demand higher torque without rod breakage. Large compressors paired with adaptive percussion sensors lower cost per meter by cutting bit changes and re-drills, while autonomous truck fleets upstream drive symmetrical gains in haul cycles. As mines deepen, heavy rigs remain on benches longer before re-positioning, improving utilization and flattening the learning curve for new hires.

Hybrid Drilling Systems Balance Fuel Efficiency With Peak-Torque Demands

Hybrid drifters integrate a diesel genset and lithium-ion buffer that harvests regenerative energy on rod pull-back, trimming diesel use by up to 30%.[3]Sandvik Mining, “Hybrid Drifter Field Trial,” sandvik.com Carbon taxes like British Columbia’s add CAD 0.18 per liter to fuel, shortening payback periods to fewer than three operating years. European Stage V emissions rules bar non-DPF rigs from urban sites after January 2025, further lifting hybrid appeal. Remote operations in Papua New Guinea cut helicopter fuel sorties once hybrids entered service, freeing cash tied up in diesel inventories. Epiroc and Sandvik now sell factory-installed hybrid kits and field-retrofit packages, expanding revenue beyond new-build machines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated decommissioning of marginal fields and mature mine closures | -0.5% | North America (Appalachian coal, Sudbury nickel), Europe (lignite phase-outs), Australia (marginal gold operations) | Short term (≤2 years) |

| Tightening ESG-linked credit covenants and emissions compliance costs | -0.7% | Global, acute in Europe, North America, Australia where banks enforce Scope 3 emissions targets | Medium term (2–4 years) |

| Volatile tungsten-carbide pricing and supply-chain concentration | -0.6% | Global, acute in regions dependent on Chinese APT exports (Europe, North America, India) | Short term (≤2 years) |

| Skilled driller attrition in mature basins and workforce aging | -0.4% | North America (Canada, US), Europe (Nordic countries), Australia (fly-in-fly-out operations) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Tungsten-Carbide Price Volatility Squeezes Margins For Drill-Steel Fabricators

China’s 2024 quota cut sent ammonium paratungstate prices up 19%, compressing margins at small carbide-insert plants in India and Turkey. Western OEMs hedge by acquiring minority stakes in Chinese and African tungsten mines, but geopolitical risk persists. The European Critical Raw Materials Act now mandates 40% allied sourcing by 2030, incentivizing recycling plants in Sweden and Pennsylvania. Until secondary supply scales, spot prices remain volatile, complicating tender pricing for consumables and forcing many contractors to lock in six-month surcharge clauses.

Skilled Driller Attrition In Mature Basins Accelerates Automation Adoption

The average underground driller in Canada’s Sudbury Basin is 52 years old, and retirements threaten a 35% workforce decline by 2028. Similar gaps appear in Australia’s Kalgoorlie region despite six-figure salaries. Modern rigs embed touchscreen diagnostics that veterans find unfamiliar, while new entrants lack tactile drilling intuition. OEMs respond with one-button cycle starts and automated rod handling that shrinks onboarding from six weeks to ten days. Contractors shift headcount risk to equipment lessors, converting fixed labor into variable drill-meter charges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hybrid Momentum Builds On Hydraulic Base

Hydraulic models retained 60.5% 2024 revenue, securing the largest drifter rock drill market share thanks to tested reliability in stopes and open benches where percussion forces exceed 25 kN. Hybrid platforms, however, are expected to book a 10.8% CAGR to 2030, the fastest within the drifter rock drill market, as urban contractors and remote mines alike seek fuel cuts without sacrificing torque. Pneumatic units linger in legacy coal and small-quarry niches, but their modest 4.2% growth underperforms the wider drifter rock drill market. Electric rigs win in Scandinavia, where diesel ventilation costs remain high, yet most greenfields delay grid investment until throughput stabilizes above 0.5 million t/y.

Hybrid conversions attract owners of five-year-old hydraulic fleets that face stricter emissions rules. Retrofit kits install a 40 kWh battery and control software for USD 180,000, extending equipment life by seven years and positioning fleets for ISO 14001 tender prerequisites. Chinese challengers undercut Western hybrids by 30% on price but lag in aftermarket coverage outside Asia, limiting share gains to Indonesia and India. Technology patents cluster among Sandvik and Epiroc, whose combined filings since 2022 exceed 120, reinforcing a high entry barrier at the premium end.

By Power Range: Heavy-Duty Rigs Gain Speed As Benches Deepen

Medium-duty rigs between 50-100 HP captured 51.8% of the 2024 value and remain the workhorses for drift development, aggregate quarries, and mid-rise foundations. Heavy-duty machines above 100 HP, however, are projected to post a 9.4% CAGR, outpacing the drifter rock drill market average as copper and iron-ore pits deepen and hardness rises. That growth lifts the heavy-duty slice of the drifter rock drill market size each year, especially in Western Australia’s Pilbara, where 127-mm blast holes drilled to 15 meters demand 120-plus HP heads.[4]Rio Tinto, “Pilbara Drill Fleet Upgrade,” riotinto.com

Light-duty units below 50 HP retain niche relevance for geotechnical probes and Arctic conductor holes, yet handheld breakers are eroding their share. Powder-factor regulations further tighten burden spacing, requiring higher torque at faster rotation to avoid jammed rods. In underground settings, medium rigs stay efficient because boom positioning in constrained headings, rather than percussion power, governs cycle time. Noise-emission caps in the EU Machinery Directive 2006/42/EC add mufflers that sap up to 8% percussion energy on heavy hydraulics, pushing OEMs to redesign housing and damping.

By Application: Infrastructure Lifts Tunneling Demand Above Trend

Underground mining held 44.4% of 2024 revenue, the single largest application slice within the drifter rock drill market. Yet tunneling and construction are slated for a 10.5% CAGR through 2030, the fastest among applications, thanks to the USD 1.2 trillion Infrastructure Investment and Jobs Act in the United States and Saudi Arabia’s NEOM utility galleries. Surface mining occupied roughly 28% the 2024 value, buoyed by copper and lithium projects, while quarrying stayed steady at 12% as recycled-aggregate mandates cap virgin stone extraction.

Public-private partnership contracts increasingly link bond penalties to on-time tunnel delivery, prompting contractors to specify premium drifters that maximize meterage. The Brenner Base Tunnel’s commitment to a 12-meter daily advance exemplifies performance-driven procurement. Meanwhile, several North American underground nickel mines enter care-and-maintenance, softening demand but freeing rigs for redeployment to APAC infrastructure jobs. Demolition’s sub-3% share pivots toward electric drifters to meet nighttime noise limits in European downtowns.

By End-User: Construction And Infrastructure Races Ahead Of Metals

Metal mining controlled 36.6% of 2024 revenue, anchored by copper and lithium prices that spur deeper pits and expanded underground footprints. Construction and infrastructure, however, is projected to grow 8.9% annually, the fastest end-user trend inside the drifter rock drill market, as global road, rail, and utility build-outs consume thousands of heavy-duty drifters.[5]World Bank, “PPP Tunnel Financing,” worldbank.org Coal’s 18% share splits along regional lines: contracting in Europe and North America, expanding in India and Indonesia.

Energy-transition drivers amplify metal drilling needs, yet the scarcity of greenfield copper startups shifts capex to brownfield deepening that favors jumbo drifters. Infrastructure’s surge feeds OEM backlogs; Epiroc reported a 34% surface-drill order jump from Gulf states after NEOM’s first-phase civil packages were let. ISO 45001 safety clauses in World Bank tenders favor fleets with automatic rod handling and collision avoidance, giving certified suppliers an edge.

Geography Analysis

North America held 33.3% of global revenue in 2024, but a 6.1% CAGR trails the world average as mature basins rely on replacement rather than expansion. Brownfield pit deepening at mines like Bagdad and Macassa sustains orders for autonomous capable rigs, and the IIJA injects capital into mountain-pass highway widening, encouraging hybrid drifter leasing to meet state emissions caps. MSHA’s proximity-detection mandate, effective 2026, rewards OEMs that include collision sensors at the factory.

Europe accounted for roughly 26% of 2024 sales, driven by HS2 tunnel packages and Nordic battery-electric conversions. Germany’s Hambach pit-to-reservoir conversion and Sweden’s Kiruna mine electrification showcase dual infrastructure and mining demand streams. EU Stage V and the Critical Raw Materials Act favor battery-electric rigs and recycling joint ventures, while carbon taxes raise diesel costs enough to accelerate paybacks on hybrids.

Asia-Pacific, forecast at 9.3% CAGR, is the growth engine of the drifter rock drill market. China’s smart-mine rules, India’s metro surge, and Indonesia’s nickel buildout translate into hundreds of fresh rig orders every year. Australia’s lithium expansions sustain heavy-duty rig demand even as spot lithium prices fluctuate. GB 16423-2020 emissions caps push underground Chinese coal sites toward hybrid or full electric rigs, locking in technology upgrades through 2027.

South America’s 9% share rests on Chilean copper deepening and Argentine lithium brine wells that need heavy track-mounted rigs to drill through halite. Brazil’s Carajás iron-ore complex retenders blast-hole fleets, specifying 120-HP minimums to preserve a 50-meter-per-hour advance in itabirite. Middle East and Africa combine for about 6%, with Gulf giga-projects importing premium rigs and West African gold mines buying refurbished hydraulics as a hedge against capital scarcity.

Competitive Landscape

The drifter rock drill market shows moderate concentration. Sandvik Mining and Rock Solutions and Epiroc AB delivered 48% of unit shipments in 2024, leveraging in-house carbide sintering, hydraulic manufacturing, and global service branches. Mid-tier competitors, Furukawa, Boart Longyear, Caterpillar, and Komatsu, focus on rental models, regional financing, or attachment versatility to avoid direct price wars. Chinese builders Shandong Qidong and Everdigm captured 22% of Asia-Pacific volumes by pricing 30% below Western peers, though thin aftermarket networks constrain share gains outside low-cost regions.

Strategic moves lean on vertical integration and analytics ecosystems. Sandvik’s stake in Jiangxi Yashan secures 4,000 t/y of tungsten concentrate through 2029, buffering against quota volatility. Epiroc’s 6th Sense telematics now tracks 12,000 units, issuing predictive alerts that cut downtime by 28% and embed switching costs for customers reliant on its data lake. Hybrid retrofits at USD 180,000 per rig offer OEMs a fresh revenue stream while letting contractors comply with Stage V rules without full replacement.

Disruptors such as Mindrill Systems target sub-50 HP electric niches with USD 65,000 price points, undercutting incumbents for urban demolition jobs where zero emissions matter more than impact energy. However, ISO 45001 and 14001 certifications are prerequisites for World Bank-financed projects, a barrier that many low-cost Asian suppliers have yet to clear. Patent clustering among the top five firms raises the technology hurdle and sustains margins even as unit pricing comes under pressure in commodity cycles.

Drifter Rock Drill Industry Leaders

Sandvik Mining and Rock Solutions

Epiroc AB

Furukawa Rock Drill

Boart Longyear

Montabert

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Epiroc delivered the first fully autonomous SmartROC D65 to Luck Stone’s Virginia quarry, achieving sub-2 centimeter pattern variance and 90% utilization.

- August 2024: Sandvik launched the battery-electric DD422iE jumbo at Kiruna, drilling 191 meters in a month with zero diesel and 40% lower ventilation demand.

- July 2024: Caterpillar invested USD 150 million to expand its Gosselies, Belgium, plant for battery-electric loaders and jumbos.

- June 2024: Komatsu signed a five-year supply deal with Rio Tinto for 8 surface drills and 24 autonomous trucks integrating FrontRunner AHS.

- May 2024: Furukawa formed a JV assembly plant in Jubail to meet Saudi 40% local-content rules by 2027.

- April 2024: Boart Longyear won a USD 85 million drilling services contract at Newmont’s Cadia East block-cave expansion.

Global Drifter Rock Drill Market Report Scope

The Global Drifter Rock Drill Market report includes:

| Hydraulic Drifters |

| Pneumatic Drifters |

| Electric Drifters |

| Hybrid Systems |

| Light Duty (Below 50 HP) |

| Medium Duty (50 to 100 HP) |

| Heavy Duty (Above 100 HP) |

| Underground Mining |

| Surface Mining |

| Quarrying |

| Tunnelling and Construction |

| Demolition |

| Metal Mining |

| Coal Mining |

| Industrial Minerals |

| Construction and Infrastructure |

| Oil and Gas |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Product Type | Hydraulic Drifters | |

| Pneumatic Drifters | ||

| Electric Drifters | ||

| Hybrid Systems | ||

| By Power Range | Light Duty (Below 50 HP) | |

| Medium Duty (50 to 100 HP) | ||

| Heavy Duty (Above 100 HP) | ||

| By Application | Underground Mining | |

| Surface Mining | ||

| Quarrying | ||

| Tunnelling and Construction | ||

| Demolition | ||

| By End-User | Metal Mining | |

| Coal Mining | ||

| Industrial Minerals | ||

| Construction and Infrastructure | ||

| Oil and Gas | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the drifter rock drill market?

The drifter rock drill market size stood at USD 1.52 billion in 2025 and is forecast to reach USD 2.18 billion by 2030.

Which segment is expanding fastest within drifter rock drill equipment?

Hybrid systems are projected to register the quickest growth at a 10.8% CAGR as operators target lower emissions without compromising torque.

Which region will contribute most to future sales?

Asia-Pacific is poised for a 9.3% CAGR through 2030, lifted by China's smart-mine mandate and India's metro tunnel pipeline.

How concentrated is supplier power?

The market is moderately concentrated; the top two firms ship 48% of units, while several mid-tier vendors and low-cost Asian entrants share the remainder.

Why are heavy-duty rigs gaining popularity?

Deeper benches in iron-ore and copper pits and stricter burden-spacing rules require higher horsepower and torque to maintain target penetration rates.

How is tungsten price volatility affecting OEMs?

Spikes in tungsten-carbide costs squeeze small bit fabricators, prompting larger OEMs to secure mine stakes or invest in recycling to stabilize supply.

Page last updated on: