DRAM For AI Accelerator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

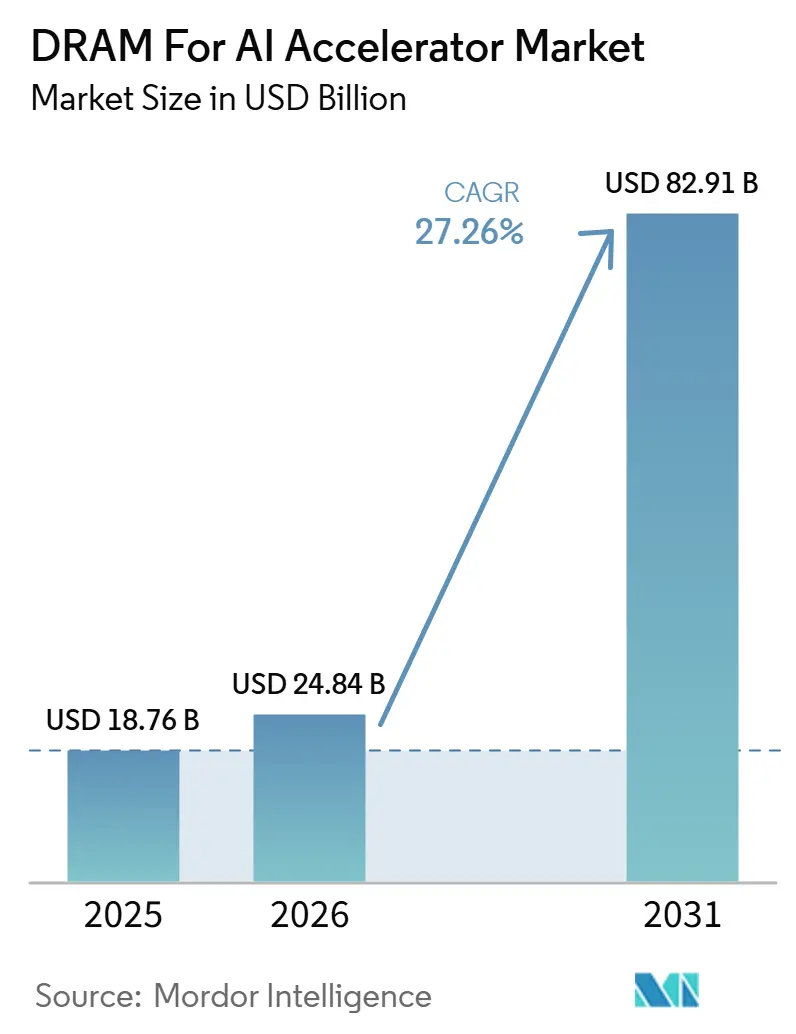

| Market Size (2026) | USD 24.84 Billion |

| Market Size (2031) | USD 82.91 Billion |

| Growth Rate (2026 - 2031) | 27.26% CAGR |

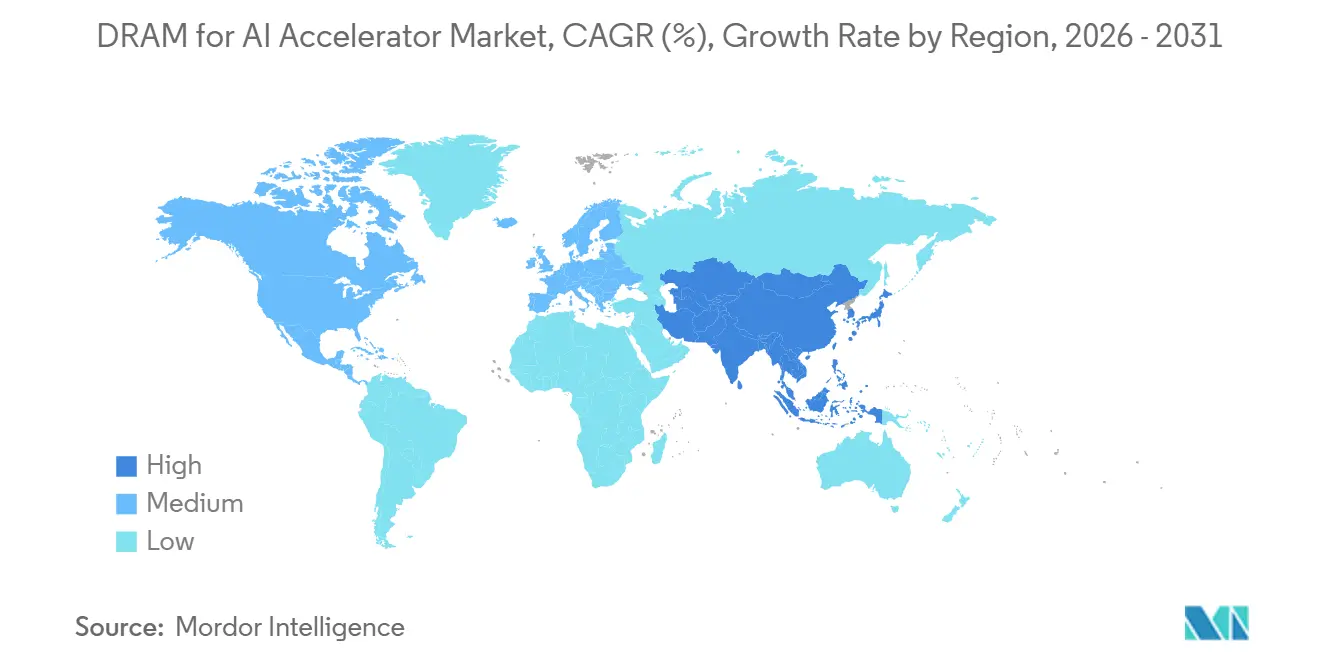

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

DRAM For AI Accelerator Market Analysis by Mordor Intelligence

The DRAM for AI accelerator market size was valued at USD 18.8 billion in 2025 and is forecast to reach USD 82.9 billion by 2031, at a CAGR of 27.3% from 2026 to 2031. The DRAM for AI accelerator market is growing faster than the broader memory market because AI training and inference systems now require bandwidth-optimized memory rather than general-purpose configurations. The center of demand has shifted toward HBM-rich compute platforms, making supply agreements, packaging access, and qualification status more important than spot pricing in this DRAM for AI accelerator market. Capacity expansion is also becoming more strategic, because memory output now depends on both wafer supply and advanced packaging readiness across the value chain. North America continues to anchor demand through hyperscaler spending, while Asia-Pacific is strengthening its role as both a production base and a fast-rising consumption center in the DRAM for AI accelerator market. The main opportunities are tied to higher-density memory stacks, custom accelerator programs, and closer long-term coordination between memory suppliers, cloud platforms, and AI system builders.

Key Report Takeaways

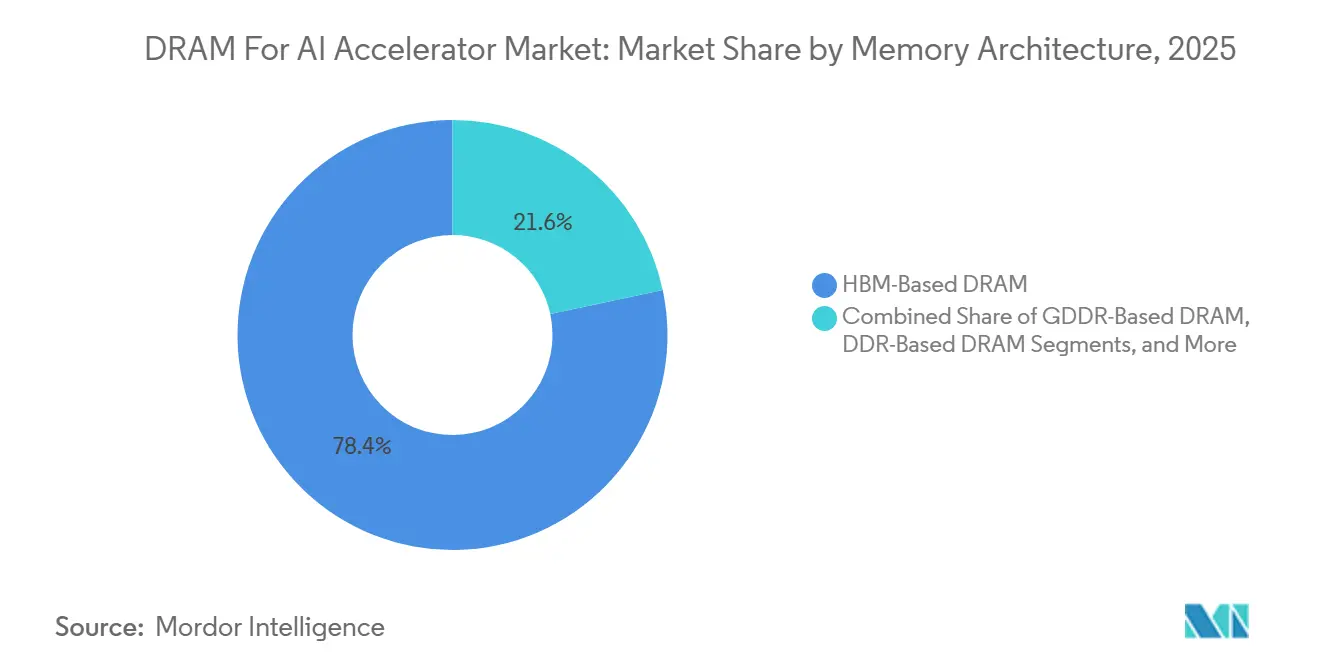

- By memory architecture, HBM-Based DRAM held a 78.4% share in 2025, and is also projected to record the fastest growth at 28.2% through 2031 in the DRAM for AI accelerator market.

- By AI accelerator type, GPU platforms held 74.4% share in 2025, while AI accelerator ASICs are forecast to expand at 28.2% through 2031 in the DRAM for AI accelerator market.

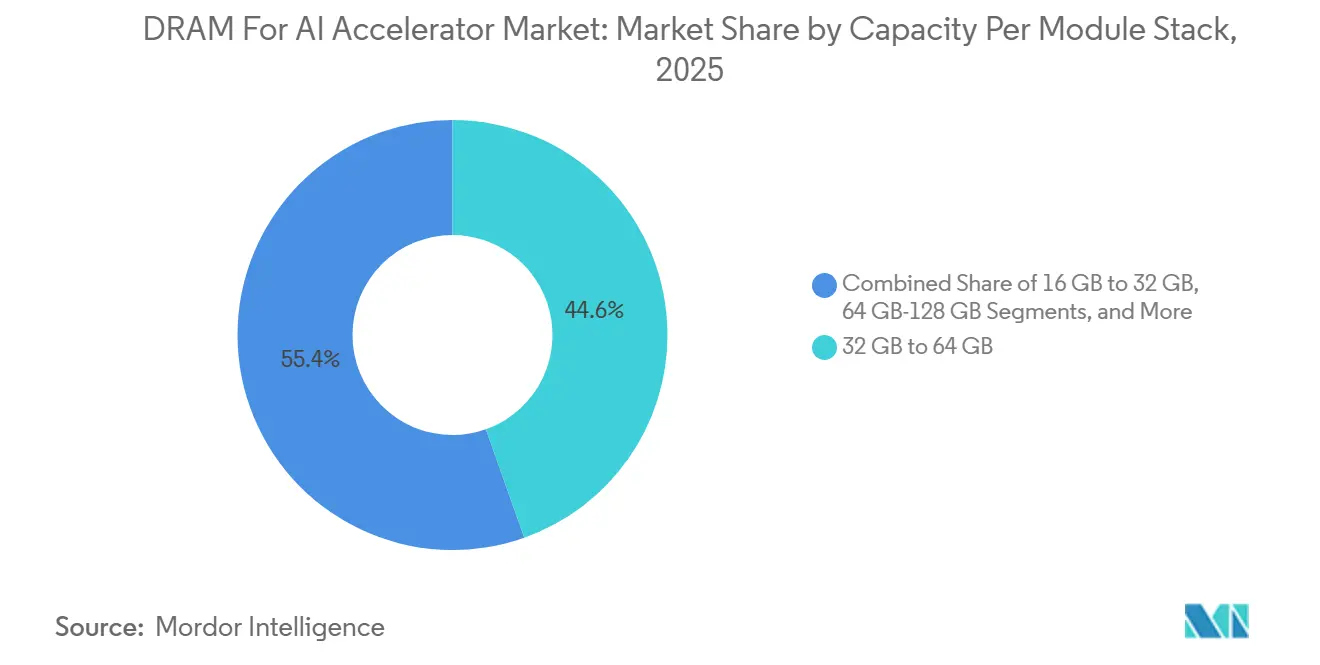

- By capacity per module or stack, the 32 GB-64 GB tier accounted for 44.6% share in 2025, while the Above 128 GB tier is projected to grow at 28.3% through 2031 in the DRAM for AI accelerator market.

- By application, training workloads accounted for 63.2% in 2025, while inference is forecast to expand by 27.9% through 2031 in the DRAM for AI accelerator market.

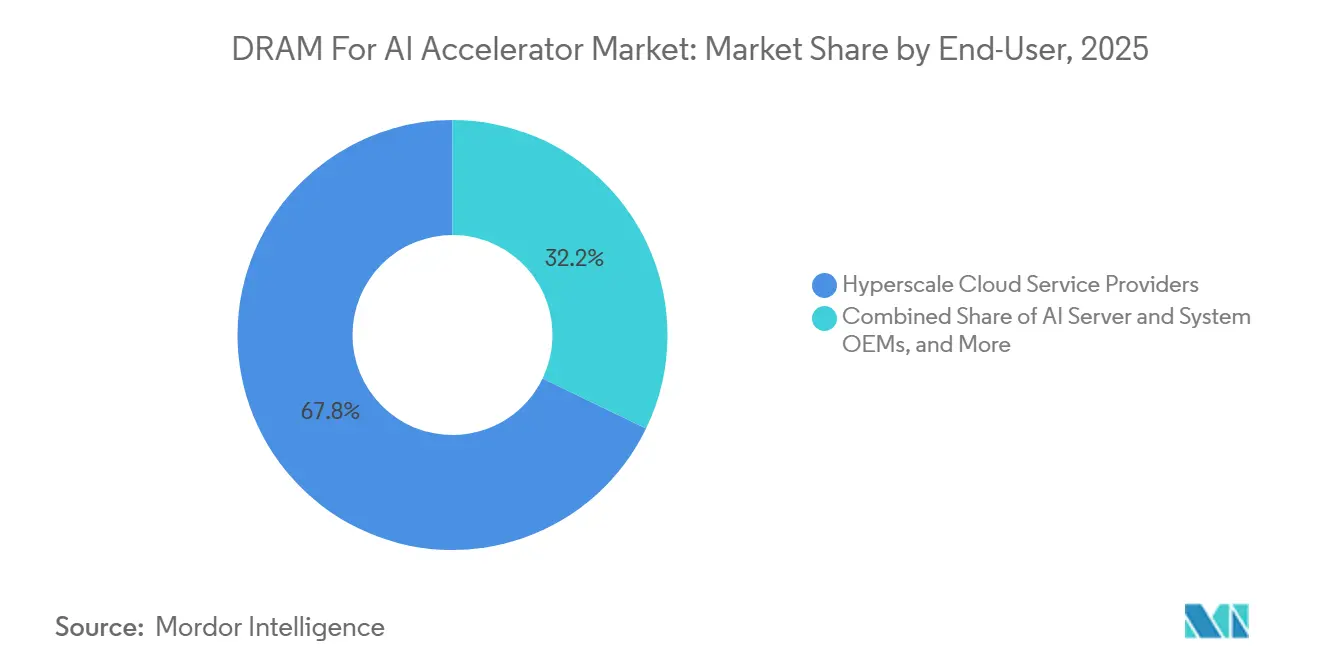

- By end user, hyperscale cloud service providers held 67.8% share in 2025, and the same segment is projected to grow at 27.7% through 2031 in the DRAM for AI accelerator market.

- By geography, North America accounted for 44.9% share in 2025, while Asia-Pacific is projected to grow at 28.1% through 2031 in the DRAM for AI accelerator market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global DRAM For AI Accelerator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising HBM Attach Rates in AI GPU Platforms | +8.5% | Global | Short term (≤ 2 years) |

| Shift to Bandwidth-Optimized Memory Stacks | +6.5% | Global | Medium term (2-4 years) |

| Higher AI Server Cluster Memory Density Requirements | +5.0% | North America and Asia-Pacific | Medium term (2-4 years) |

| More Multi-GPU Servers and Memory Pooling Demand | +3.0% | Global | Short term (≤ 2 years) |

| HBM Yield Improvement and Supply Expansion | +2.0% | Asia-Pacific (South Korea, Japan) | Medium term (2-4 years) |

| Rising GDDR Use in Cost-Sensitive AI Inference GPUs | +1.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising HBM Attach Rates in AI GPU Platforms

The DRAM for AI accelerator market is being pushed higher as leading AI GPUs now treat HBM as a core requirement rather than an optional memory choice. NVIDIA’s B200 carries 192 GB of HBM3e at 8 TB/s bandwidth, and the Rubin generation scales to 288 GB of HBM4 per GPU.[1]NVIDIA Corporation, “NVIDIA Vera Rubin POD, Seven Chips, Five Rack-Scale Systems, One AI Supercomputer,” NVIDIA Technical Blog, developer.nvidia.com At rack scale, NVIDIA stated that 72 Rubin GPUs pool their HBM into a 13.5 TB coherent memory fabric, demonstrating how memory capacity and interconnect design are advancing together. That architecture keeps HBM demand high even if accelerator shipment growth becomes less linear, because more memory is being attached to each deployed device. Google’s June 2026 paper on TPU system evolution also confirmed a 10x increase in HBM capacity and bandwidth per training node across five generations. In the DRAM for AI accelerator market, that pattern supports sustained value growth because memory content per compute node continues to increase with each platform cycle.

Shift From General-Purpose DRAM to Bandwidth-Optimized Memory Stacks

The DRAM for AI accelerator market is also advancing because the memory discussion has shifted from raw capacity toward bandwidth efficiency and stack architecture. JEDEC released the JESD270-4 HBM4 standard in April 2025, defining a 2,048-bit interface, 32 independent channels, data rates up to 8 Gbps, and support for up to 64 GB per stack. That publication matters because it gives buyers and system designers a clear interoperability baseline for the next memory generation. The same standards path continued in December 2025, when JEDEC disclosed work on SPHBM4 to deliver HBM4-level throughput with reduced pin count. As a result, DRAM for AI accelerator market is benefiting from a more formal migration toward bandwidth-optimized stacks rather than repeated tuning of conventional DRAM formats. This change also supports longer product cycles for HBM platforms because customers can now plan around standards-based scaling rather than one-off implementation paths.

Rapid Growth in AI Server Cluster Memory Density Requirements

The DRAM for AI accelerator market is further supported by the rising memory footprint of AI server clusters at the node, rack, and system levels. NVIDIA’s Rubin platform connects each GPU with 3.6 TB/s of bidirectional NVLink bandwidth, and the NVL72 rack reaches 260 TB/s of scale-up bandwidth across the full system. That design means memory demand is no longer set solely by a single accelerator, because the full cluster is built to behave like a single large compute and memory domain. Google’s TPU 8i, introduced at Google Cloud Next 2026, pairs 288 GB of HBM with 384 MB of on-chip SRAM to keep more working data close to the processor. The result is that each new server generation increases the memory requirements for competitive AI performance. In the DRAM for AI accelerator market, this keeps demand tied to memory density per deployment, not only to the number of chips shipped.

Increase in Multi-GPU Server Configurations and Memory Pooling Demand

The DRAM for AI accelerator market is also being strengthened by the move toward multi-GPU systems that rely on pooled memory. NVIDIA introduced NVLink Fusion in 2026 to let semi-custom and custom compute devices participate in a rack-scale NVLink architecture. That step matters because it extends coherent memory fabrics beyond a single vendor’s standard GPU lineup. Once multiple devices are expected to operate within a single connected memory environment, each accelerator still needs strong local memory resources to support portability and balanced system performance. This reduces the practical room for low-memory configurations in high-value AI deployments. In the DRAM for AI accelerator market, the adoption of pooled memory designs therefore expands the addressable demand tied to every rack-scale build. It also links memory revenue more tightly to full-system design choices than to component-level substitution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| HBM Packaging Bottlenecks and Limited Advanced Substrate Capacity | -3.5% | Global | Short term (≤ 2 years) |

| High Qualification Barriers for New DRAM Suppliers | -2.5% | Global | Long term (≥ 4 years) |

| Memory Allocation Competition From General Server DDR Demand | -1.5% | North America and Europe | Medium term (2-4 years) |

| Export Controls and Geopolitical Constraints on Advanced Memory Supply | -2.5% | Asia-Pacific, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

HBM Packaging Bottlenecks and Limited Advanced Substrate Capacity

The DRAM for AI accelerator market continues to face a real cap from advanced packaging and substrate readiness, even as memory demand remains strong. Samsung’s commercial HBM4 program uses a 4nm base die and achieves up to 3.3 TB/s per stack, demonstrating the level of process integration now required for leading AI memory products. In July 2026, Samsung Electronics and SK Hynix committed KRW 240 trillion (USD 155 billion) in the Chungcheong region to new HBM fabrication plants and advanced packaging facilities, underscoring the extent of downstream capacity that still needs to be built. The scale of that investment shows that packaging remains a bottleneck large enough to shape supplier strategy and regional capital allocation. When packaging lines lag wafer output, memory dies alone do not translate into a finished accelerator supply. That is why the DRAM for AI accelerator market still faces near-term supply friction, even while spending on capacity is accelerating.

High Qualification Barriers for New DRAM Suppliers

The DRAM for AI accelerator market is also restrained by long customer validation cycles and the technical complexity needed for a qualified HBM supply. JEDEC’s HBM4 standard has established a common framework, but it does not eliminate the need for system-level testing across power, thermals, yield, and controller compatibility. Samsung’s February 2026 HBM4 shipment announcement made clear that mass production remains aligned with customer qualification schedules, underscoring that commercial timing is still tied to approval milestones rather than manufacturing output alone. New entrants, therefore, face a barrier that is part manufacturing challenge and part relationship challenge with accelerator designers. This slows supplier diversification even when demand is attractive and capital is available. As a result, the DRAM for AI accelerator market remains difficult to enter at the high end, which limits how quickly supply can expand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Memory Architecture: HBM Establishes a Durable Structural Lead in AI Memory

HBM-Based DRAM held 78.4% of the DRAM for AI accelerator market share in 2025, and is also projected to expand at a 28.2% CAGR through 2031. That lead reflects how AI accelerator memory is now being selected on bandwidth, density, and system efficiency rather than on conventional cost-per-bit logic alone. Google’s June 2026 TPU paper showed a 10x increase in HBM capacity and bandwidth per training node across five generations, which helps explain why HBM has moved from a premium option to a core platform requirement. JEDEC’s HBM4 standard also formalized the next step in this migration, with up to 64 GB per stack and a much wider interface structure for high-throughput computing. In the DRAM for AI accelerator industry, that combination makes HBM the reference architecture for frontier AI deployments.

GDDR-Based DRAM remains relevant in the DRAM for AI accelerator market, where cost-sensitive inference systems need a lower memory bill than HBM-heavy training hardware. Its role is strongest in workloads that can accept lower packaging complexity while still requiring meaningful bandwidth. DDR-Based DRAM continues to sit in the system memory layer of AI servers, where it supports orchestration, data movement, and host-side buffering rather than direct high-bandwidth accelerator execution. As rack-scale AI systems become more coherent, DDR still matters, but its strategic role is shifting from core accelerator memory toward support memory across the full server design. The result is that the DRAM for AI accelerator market is not moving entirely away from other memory types, but it is clearly assigning them narrower roles within an HBM-centered architecture stack.

By AI Accelerator Type: ASICs Challenge GPU Incumbency in Inference Tiers

GPU platforms accounted for 74.4% of the DRAM for AI accelerator market size in 2025, while AI accelerator ASICs are forecast to grow at 28.2% through 2031. GPUs keep the lead because they remain the default choice for hyperscaler training clusters and broad AI software compatibility. At the same time, custom ASIC programs are gaining traction because large cloud providers want better cost control and tighter alignment between memory, interconnect, and model-serving behavior. Google’s TPU 8i features 288 GB of HBM and 8,601 GB/s of bandwidth, demonstrating how quickly proprietary accelerator programs are closing the capability gap with mainstream GPU platforms.[2]“Google’s Training Supercomputers From TPU v2 to Ironwood, Architectural Stability, Scale, Resilience, Power Efficiency, and Sustainability Across Five Generations,” arXiv, arxiv.org In the DRAM for AI accelerator market, this means procurement growth is expanding beyond a single dominant accelerator category, even as GPUs still control the largest installed base.

FPGA-based accelerators hold a smaller position, but they retain value in low-latency communications, financial computing, and targeted deployment environments where reconfigurability remains important. CPUs with AI acceleration also maintain a place in enterprise inference setups that prioritize compatibility with established server infrastructure and broader software support. That keeps the DRAM for AI accelerator market tied to multiple compute paths rather than a single hardware template. Even so, the strongest growth pressure is still shifting toward products that can support large HBM footprints and high parallel memory throughput. The net effect is that GPUs continue to define present-day volume, while ASICs are shaping where future memory demand expands fastest in the DRAM for AI accelerator market.

By Capacity Per Module or Stack: Ultra-High Density Tiers Signal a Generational Step Change

The 32 GB-64 GB tier captured 44.6% share of the DRAM for AI accelerator market size in 2025, while the Above 128 GB tier is projected to expand at 28.3% through 2031. The current installed base still reflects large deployments of earlier HBM-rich GPU systems that made this middle range the practical standard for production clusters. That position is now being challenged by much denser memory designs tied to the next wave of accelerator launches. NVIDIA’s Rubin generation scales to 288 GB of HBM4 per GPU, and Google’s TPU 8i also launched with 288 GB of HBM, which raises the performance bar for new frontier systems. In the DRAM for AI accelerator market, this makes the Above 128 GB tier the clearest signal of where next-cycle system specifications are heading.

The 64 GB-128 GB tier remains an important bridge segment because it fits many enterprise inference clusters that need strong memory resources without the highest frontier cost profile. Smaller tiers still serve edge inference, workstation, and selected FPGA-oriented environments where memory budgets and application needs are more constrained. Samsung stated that its commercial HBM4 offers 24 GB to 36 GB per 12-layer stack and improves power efficiency by 40% compared with HBM3e, supporting the move toward higher capacity without constant package redesign. That matters because the scaling path in this DRAM for AI accelerator market is increasingly based on denser stacks rather than simply adding more components around the package. As a result, capacity migration is becoming more continuous, narrowing the gap between the mainstream enterprise tier and the highest frontier tier.

By Application: Inference Rapidly Narrows the Gap on Training-Driven Demand

Training workloads accounted for 63.2% of the DRAM for AI accelerator market share in 2025, while inference is projected to grow at 27.9% through 2031. Training remained larger because frontier model development still depends on dedicated clusters with very high memory density and bandwidth requirements. However, inference is growing rapidly as real-time serving, agentic AI, and long-context workloads increase the memory burden in production environments. Google positioned TPU 8t for large-scale pre-training and TPU 8i for inference and agentic workloads, which shows that memory-intensive inference is now important enough to justify purpose-built hardware variants. In the DRAM for AI accelerator industry, that shift is narrowing the historic separation between training memory needs and inference memory needs.

High-performance computing remains the third application track in the DRAM for AI accelerator market, especially for simulation, genomics, and climate workloads that require high memory throughput similar to that of AI training. Professional visualization also remains in demand, with greater relevance for workstation and rendering environments that typically rely on lower-intensity memory configurations than top-tier AI systems. These two segments do not lead the DRAM for AI accelerator market, but they broaden the installed base and soften the dependence on a single workload pattern. They also keep GDDR and other non-HBM memory paths relevant at the system level, even as HBM leads value creation. The application mix is therefore changing less through replacement and more through the rising memory intensity of both training and inference within the same broader compute landscape.

By End User: Hyperscalers Drive Volume, OEMs Distribute It Across Enterprise Clusters

Hyperscale cloud service providers held a 67.8% share in 2025 and are projected to grow at 27.7% through 2031 in the DRAM for AI accelerator market. Their lead reflects the concentration of spending among cloud platforms, which are building internal training and inference clusters at a pace that smaller buyers cannot match. This gives hyperscalers a direct role in setting qualification priorities, supply agreements, and the timing of high-density memory adoption across the value chain. It also means demand in the DRAM for AI accelerator market is increasingly shaped by a limited number of procurement programs with very large unit requirements. That concentration supports stronger revenue visibility for qualified suppliers, even when broader memory markets remain more cyclical.

AI server and system OEMs form the second-largest end-user layer because they package accelerator-heavy systems for enterprise buyers and turn cloud-scale design choices into deployable infrastructure. Their importance is especially evident in the mid- to upper-tier memory, where enterprise AI clusters need strong performance but still follow more standardized system configurations. Semiconductor companies represent another significant user group because they need advanced DRAM for custom ASIC validation, benchmarking, and early production. Research and academic institutions remain the smallest group, and their access often depends on cloud platforms or public supercomputing programs rather than direct procurement. The DRAM for AI accelerator market, therefore, combines extreme demand concentration at the top with a broader downstream distribution path across OEMs, chip developers, and research users.

Geography Analysis

North America represented 44.9% of the DRAM for AI accelerator market size in 2025. The region leads because the largest hyperscaler capital programs remain concentrated in the United States, where model development and AI infrastructure build-outs are still centered. That demand pattern keeps the DRAM for AI accelerator market closely tied to the purchasing behavior of Microsoft, Google, Amazon, and Meta, even when production takes place elsewhere. The United States also shapes the regulatory environment for advanced memory. The Bureau of Industry and Security added HBM to ECCN 3A090.c in its December 2024 rule and extended related export controls to shipments involving China and Macau, thereby reinforcing North America’s central role in the allied-country supply chain.

Europe remains a smaller regional block in the DRAM for AI accelerator market, and its demand is rising from a lower starting base. The region is supported by sovereign AI programs, local data center investments, and enterprise interest in inference infrastructure that meets data residency requirements. That gives Europe a steadier adoption profile, with greater emphasis on controlled deployment and compliance-readiness than on the largest frontier training clusters. The region does not yet match North America on spending scale, but it remains relevant because local deployment requirements continue to create demand for high-bandwidth AI systems.

Asia-Pacific is the fastest-growing regional segment in the DRAM for AI accelerator market, with a projected CAGR of 28.1% through 2031. The region plays a dual role as both the main production base for advanced DRAM and a rising demand center for AI compute infrastructure. In July 2026, Samsung Electronics and SK Hynix committed KRW 240 trillion, or USD 155 billion, in South Korea’s Chungcheong region for new HBM fabrication plants and advanced packaging facilities. Micron also broke ground on its Hiroshima expansion in July 2026 to strengthen HBM production capacity in Japan. The Rest of the World segment remains early-stage, but sovereign AI spending in parts of the Middle East is beginning to pull more of the DRAM for AI accelerator market into new deployment geographies.

Competitive Landscape

The DRAM for AI accelerator market remains highly concentrated, as SK Hynix, Samsung Electronics, and Micron Technology supply HBM products that sit at the center of current AI accelerator demand. That concentration matters because HBM accounted for 78.4% of market demand in 2025, which means leadership in this memory category strongly shapes the direction of the broader DRAM for AI accelerator market. The main competitive contest is therefore less about basic participation and more about who can scale qualified output, improve yields, and secure long-term slots in top AI hardware programs. Supplier positioning is also shaped by the ability to manage advanced packaging, base die development, and customer qualification simultaneously. This makes the competitive structure tighter and slower to change than in traditional DRAM cycles.

Samsung strengthened its position in February 2026 by shipping commercial HBM4 with a 4nm base die, bandwidth up to 3.3 TB/s per stack, and a 40% power-efficiency improvement over HBM3e.[3]Samsung Electronics, “Samsung Ships Industry-First Commercial HBM4 With Ultimate Performance for AI Computing,” Samsung Newsroom, news.samsung.com That move was strategically important because it showed Samsung’s push to differentiate through deeper in-house integration rather than relying solely on standard memory scaling. Micron reinforced its own position in July 2026 by announcing up to USD 3 billion to strengthen the U.S. semiconductor ecosystem, including a long-term supply arrangement linked to raw silicon wafers. These moves show that competition in the DRAM for AI accelerator market is increasingly being fought through capital depth, ecosystem control, and supply assurance rather than pricing alone.

South Korea remains central to this race because Samsung Electronics and SK Hynix announced combined investment plans of KRW 240 trillion, or USD 155 billion, in July 2026 for HBM fabrication and advanced packaging in the Chungcheong region. That level of spending indicates that top suppliers are treating packaging access and output scale as strategic weapons in the DRAM for AI accelerator market. Demand-side competition is also pushing suppliers forward, because Google’s TPU 8t and TPU 8i show that hyperscalers are expanding their own accelerator roadmaps alongside mainstream GPU platforms.[4]Google Cloud, “TPU 8t and TPU 8i Technical Deep Dive,” Google Cloud Blog, cloud.google.com As custom silicon programs expand, memory makers will need to support more platform variants without losing qualification speed or yield discipline. The competitive landscape in the DRAM for AI accelerator market therefore remains concentrated at the top, but it is becoming more demanding in execution across both supplier and customer ecosystems.

Global DRAM For AI Accelerator Market Report Scope

The DRAM for AI Accelerator Market Report is Segmented by Memory Architecture (HBM-Based DRAM, GDDR-Based DRAM, and DDR-Based DRAM), AI Accelerator Type (GPU, AI Accelerator ASIC, FPGA, and CPU with AI Acceleration), Capacity Per Module/Stack (Up to 16 GB, 16 GB to 32 GB, 32 GB to 64 GB, 64 GB to 128 GB, and Above 128 GB), Application (Training, Inference, High Performance Computing, and Professional Visualization), and Geography (North America, Europe, Asia-Pacific, and Rest of the World). The Market Forecasts are Provided in Terms of Value (USD).

| HBM Based DRAM |

| GDDR Based DRAM |

| DDR Based DRAM |

| GPU |

| AI Accelerator ASIC |

| FPGA |

| CPU with AI Acceleration |

| Up to 16 GB |

| 16 GB to 32 GB |

| 32 GB to 64 GB |

| 64 GB to 128 GB |

| Above 128 GB |

| Training |

| Inference |

| High Performance Computing |

| Professional Visualization |

| Hyperscale Cloud Service Providers |

| AI Server and System OEMs |

| Semiconductor Companies |

| Research and Academic Institutions |

| North America | |

| Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| Rest of Asia Pacific | |

| Rest of the World |

| By Memory Architecture | HBM Based DRAM | |

| GDDR Based DRAM | ||

| DDR Based DRAM | ||

| By AI Accelerator Type | GPU | |

| AI Accelerator ASIC | ||

| FPGA | ||

| CPU with AI Acceleration | ||

| By Capacity Per Module or Stack | Up to 16 GB | |

| 16 GB to 32 GB | ||

| 32 GB to 64 GB | ||

| 64 GB to 128 GB | ||

| Above 128 GB | ||

| By Application | Training | |

| Inference | ||

| High Performance Computing | ||

| Professional Visualization | ||

| By End User | Hyperscale Cloud Service Providers | |

| AI Server and System OEMs | ||

| Semiconductor Companies | ||

| Research and Academic Institutions | ||

| By Geography | North America | |

| Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| Rest of Asia Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

What is the projected value of DRAM for AI accelerators by 2031?

The DRAM for AI accelerator market is forecast to reach USD 82.91 billion by 2031, up from USD 18.76 billion in 2025, with a 27.26% CAGR from 2026 to 2031.

Why is HBM leading AI memory demand?

HBM led with 78.36% share in 2025 because leading AI GPUs and custom accelerators now rely on very high bandwidth, dense stacks, and tighter memory-to-compute integration.

Which application is expanding fastest in AI memory demand?

Inference is the fastest-growing application at 27.94% through 2031, as real-time serving and agentic AI workloads require more memory capacity and bandwidth.

Which end users drive the largest memory purchases?

Hyperscale cloud service providers led with 67.84% share in 2025, reflecting the scale of training and inference infrastructure spending among the largest cloud platforms.

Which region is growing fastest for AI accelerator DRAM?

Asia-Pacific is projected to grow at 28.10% through 2031, supported by its role as both the main production base and an expanding AI compute deployment region.

What is the biggest near-term supply challenge?

Advanced packaging and qualification remain the main constraints, because wafer output alone does not guarantee finished HBM availability for qualified AI accelerator programs.

Page last updated on: