Djibouti Container Shipping Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

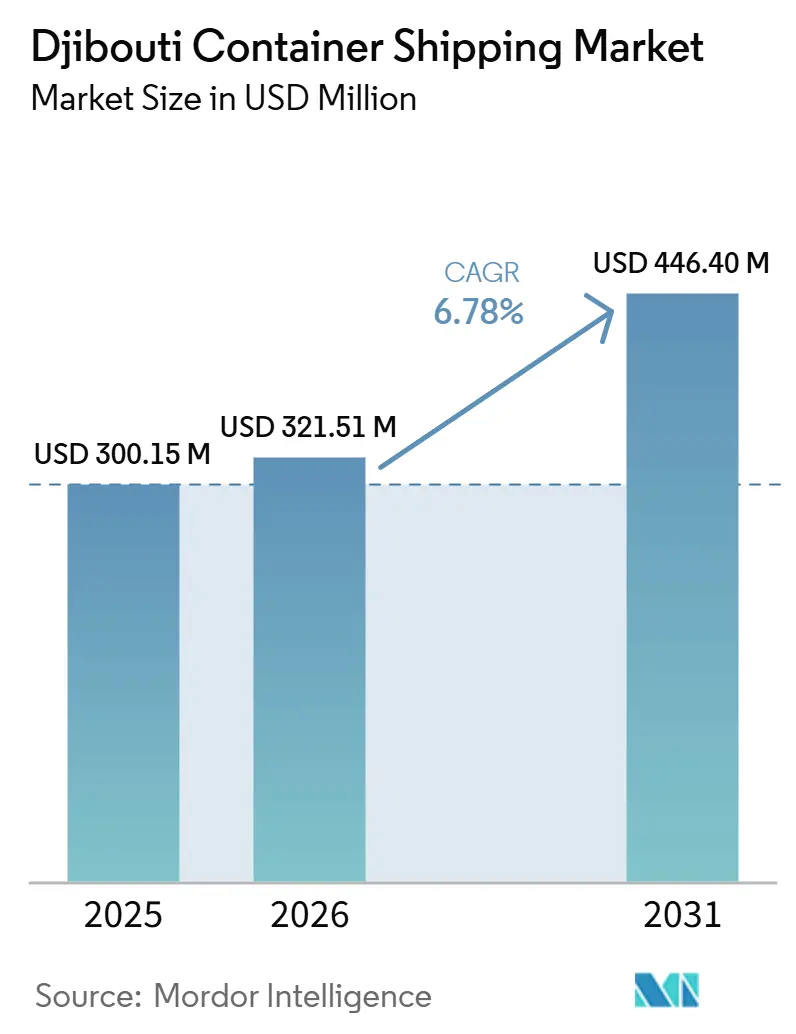

| Base Year Market Size (2025) | USD 300.15 Million |

| Market Size (2026) | USD 321.51 Million |

| Market Size (2031) | USD 446.40 Million |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Djibouti Container Shipping Market Analysis by Mordor Intelligence

The Djibouti container shipping market size is projected to grow from USD 300.15 million in 2025 to USD 321.51 million in 2026, and reach USD 446.40 million by 2031, growing at a CAGR of 6.78% from 2026 to 2031.

Djibouti’s position at the southern entrance to the Red Sea keeps the corridor important for container transfer, gateway trade, and regional vessel connectivity. SGTD’s recent investment cycle shows that Doraleh is being prepared for sustained traffic, not only temporary demand swings, with new yard equipment added in 2025 and handling capacity aligned with 2 million TEU by mid-2026. The digital operating layer is also improving, as Djibouti’s Port Community System connects ports, customs, free zones, and corridor tracking, and has been cited by DPFZA in World Bank benchmarking, which showed turnaround time moving from 24 hours to around 1 hour. Competition remains concentrated among a few global carriers on the mainline side and more dispersed across feeder and agency operators, which supports route coverage but keeps market power balanced. The growth path for this market still depends heavily on Ethiopia-bound cargo. At the same time, transshipment, cold-chain handling, acceptance of larger vessels, and improved digital clearance continue to expand operating opportunities.

Key Report Takeaways

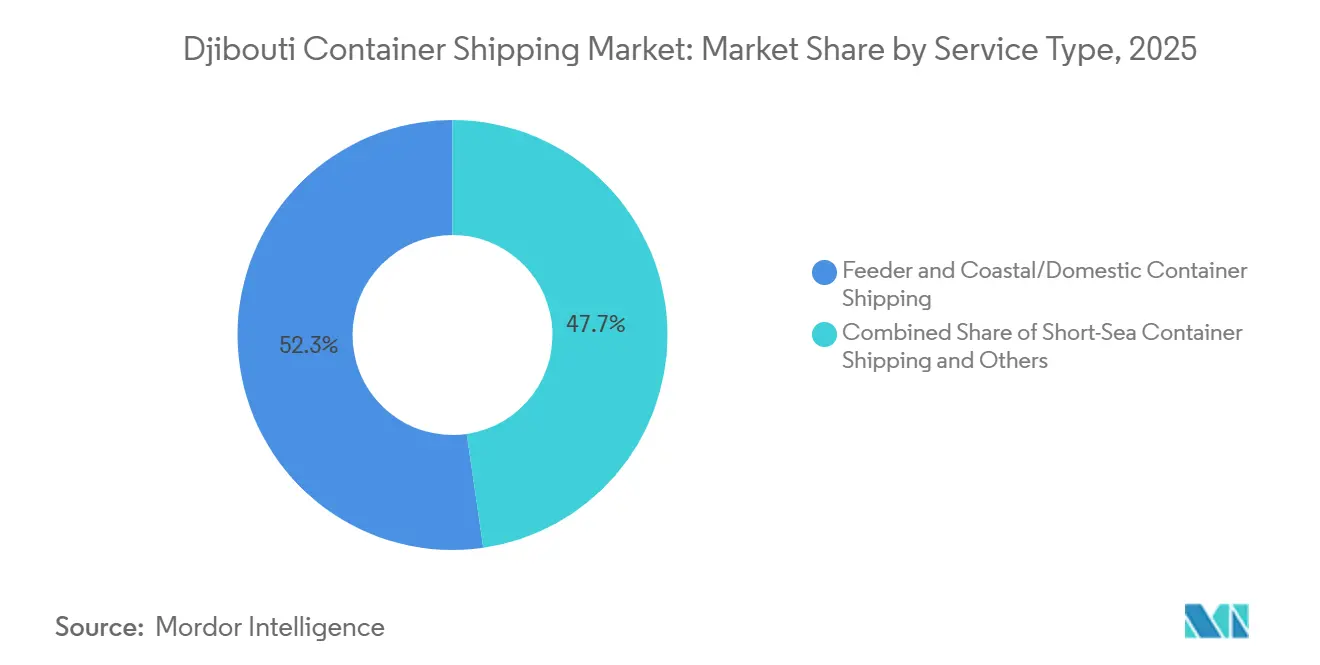

- By service type, feeder and coastal/domestic container shipping accounted for 52.28% of the Djibouti container shipping market share in 2025 and is forecast to expand at a 7.76% CAGR through 2031.

- By container type, dry containers accounted for 84.30% of the Djibouti container shipping market size in 2025, while reefer containers are projected to grow at 10.38% CAGR through 2031.

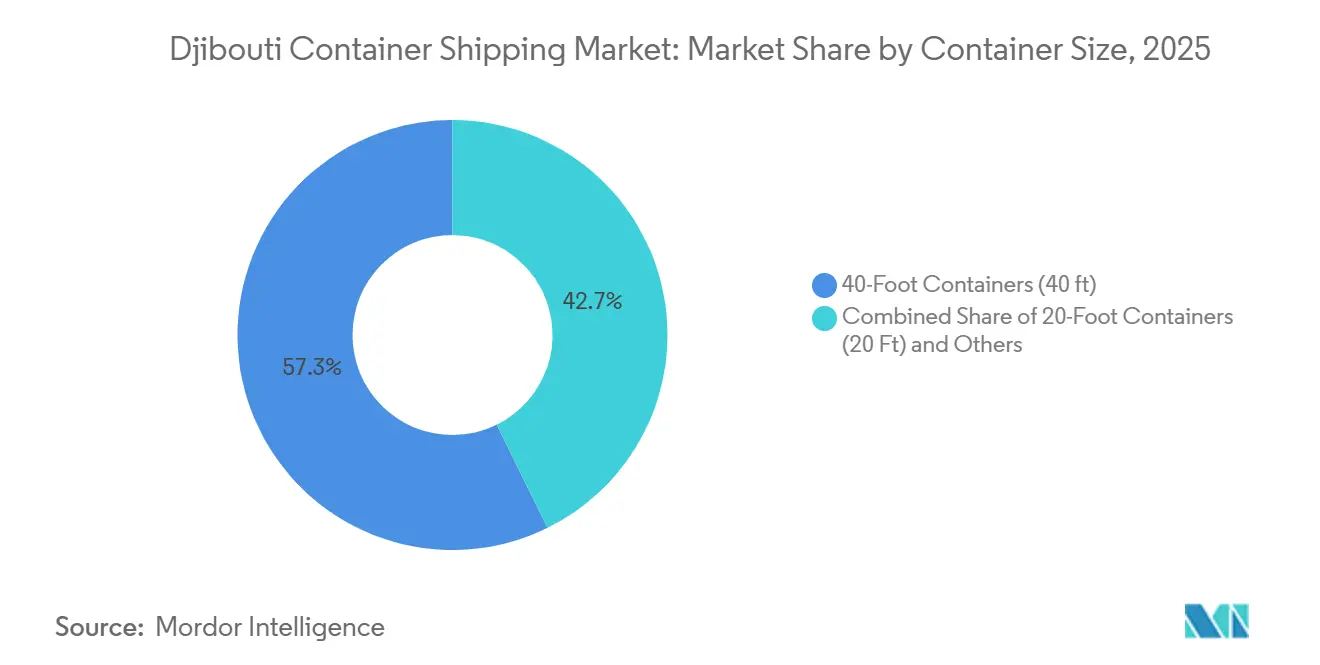

- By container size, 40-foot containers retained 57.29% of the Djibouti container shipping market share in 2025, while 20-foot containers are expected to grow at 8.04% CAGR through 2031.

- By load type, Full-container-load held 68% of the Djibouti container shipping market share in 2025, while Less-than-container-load is forecast to expand at 9.78% CAGR through 2031.

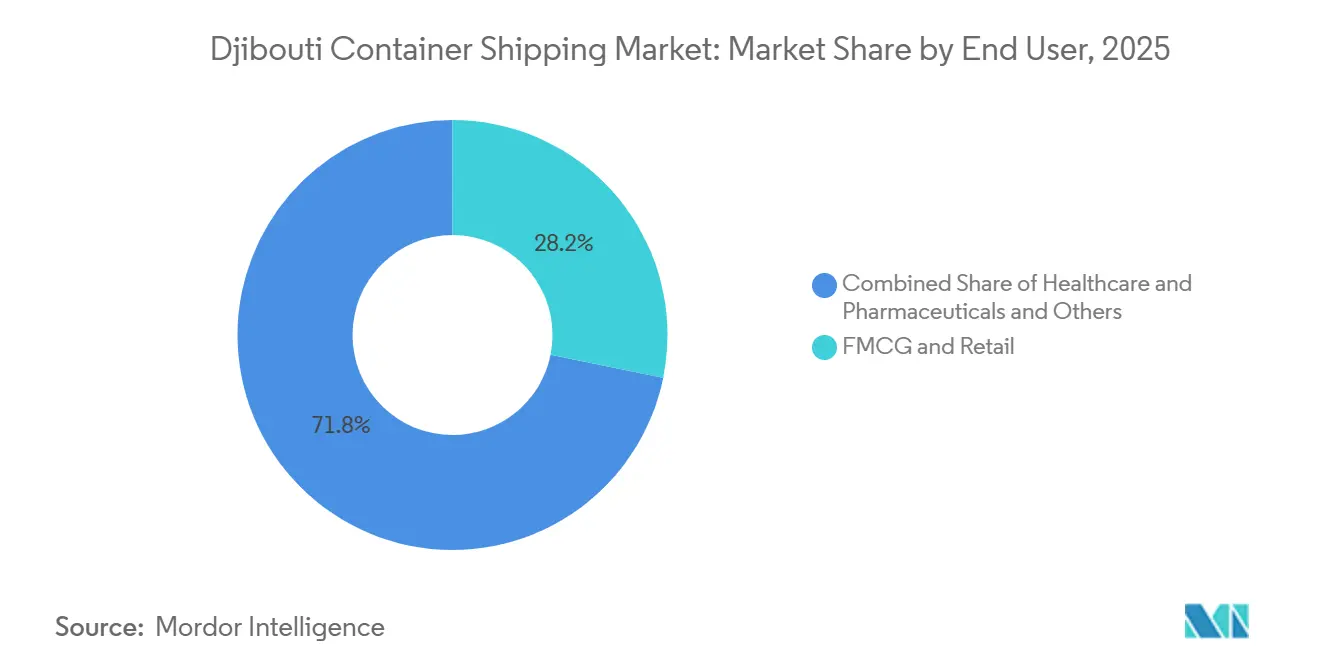

- By end-user industry, FMCG and retail accounted for 28.18% of the Djibouti container shipping market size in 2025, while healthcare and pharmaceuticals are projected to grow at a 9.10% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Djibouti Container Shipping Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Red Sea Rerouting Supports Container Volumes Through Djibouti | +1.8% | Global, East Africa core | Medium term (2-4 years) |

| Ethiopia Transit Cargo Dependence on Djibouti Corridors | +1.5% | National (Djibouti-Ethiopia corridor) | Long term (≥ 4 years) |

| Transshipment Hub Economics Favor Feeder and Mainline Connectivity | +0.9% | East Africa, Horn of Africa, Indian Ocean rim | Medium term (2-4 years) |

| Cold-Chain and Reefer Demand from Food and Pharmaceutical Imports | +0.6% | East Africa and the Middle East, spillover to the global reefer fleet | Medium term (2-4 years) |

| Terminal Productivity and Deepwater Capacity Improve Vessel Acceptance | +0.5% | Djibouti-specific (Doraleh Terminal) | Short term (≤ 2 years) |

| Digital Port Community Systems Reduce Clearance Friction | +0.3% | National (Djibouti) with regional benchmarking interest | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Red Sea Rerouting Supports Container Volumes Through Djibouti

The Djibouti container shipping market benefits from its position at the southern entrance to the Red Sea, where carriers need a reliable point for cargo transfer and onward distribution. SGTD’s roadmap shows that the terminal crossed 1,236,769 TEU in 2024, which confirmed a higher operating base before the next round of capacity additions[1]Source: SGTD, “Heart of the Regional Connectivity, Capacity Expansion Roadmap 2025-2026,” Transport Events Djibouti26 Presentation, transportevents.com. The same roadmap aligns the terminal with a 2 million TEU handling threshold by mid-2026, indicating that Doraleh has been preparing for larger, steadier flows. SGTD also added new ULCV handling capability in its official expansion material, supporting vessel sizes up to 23,000 TEU and strengthening the case for direct calls by larger ships. With location and equipment moving in the same direction, the Djibouti container shipping market remains well placed when carriers favor hub operations that can absorb shifting regional schedules.

Ethiopia Transit Cargo Dependence on Djibouti Corridors

The Djibouti container shipping market still draws most of its cargo demand from the Ethiopia corridor, which keeps hinterland trade at the center of volume growth. An official Ethiopian policy note stated that 95% of Djibouti port activity is tied to Ethiopian cargo, underscoring the tight link between the two systems. This linkage provides Djibouti with a reliable cargo hub as Ethiopian imports and exports remain active across the corridor. It also raises switching costs because transport routines, inland delivery systems, and shipper relationships have been built around this route over time. For the Djibouti container shipping market, this corridor dependence supports recurring demand in normal trade conditions, even as it leaves the market more exposed than a port system with a wider domestic base.

Cold-Chain and Reefer Demand from Food and Pharmaceutical Imports

The Djibouti container shipping market is seeing faster growth in temperature-controlled cargo than in standard cargo, especially for food and pharmaceutical flows that require tighter handling conditions. Ocean Network Express stated in 2025 that African trade is facing a reefer gap, indicating a shortage of suitable capacity relative to demand on routes to the region[2]Source: Ocean Network Express, “Solving the Reefer Gap, ONE’s Market Insights Reveal Key Drivers in African Trade,” ONE, one-line.com. The Global Cold Chain Alliance also highlighted strong momentum in East Africa cold-chain investment, which supports higher throughput for vaccines, biologics, frozen food, and other sensitive goods. This demand pattern encourages carriers and terminals to expand the number of reefer plugs, improve stack planning, and tighten service control for sensitive cargo. As a result, the Djibouti container shipping market is capturing more high-value shipments that depend on reliability and compliance rather than on the lowest freight rate.

Terminal Productivity and Deepwater Capacity Improve Vessel Acceptance

The Djibouti container shipping market benefits from terminal efficiency, as berth productivity and yard flow directly influence carrier scheduling and port choice. SGTD received 10 new RTG cranes in February 2025, bringing the fleet to 42 units and supporting operations at the 2 million TEU annual handling level. SGTD also began work on a 12-hectare sea yard in June 2025, which will add 500,000 TEU of annual capacity upon completion. DPFZA states that Djibouti’s Port Community System connects all operational ports, free zones, customs, and corridor tracking. At the same time, the World Bank benchmarking cited in the DPFZA release showed that turnaround time fell from 24 hours to around 1 hour. Together, physical expansion and digital coordination give the Djibouti container shipping market a stronger operating base for higher throughput and more demanding cargo flows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Security Disruption Risk in the Red Sea Corridor | -1.2% | Global, Red Sea corridor, and Gulf of Aden | Medium term (2-4 years) |

| Dependence on Ethiopia-Bound Cargo Creates Demand Concentration | -0.8% | National (Djibouti) | Long term (≥ 4 years) |

| Limited Domestic Consumption Base Caps Organic Growth | -0.4% | National (Djibouti) | Long term (≥ 4 years) |

| Port Congestion and Inland Bottlenecks Can Delay Turnaround | -0.3% | National, with hinterland concentration at the Djibouti City corridor | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Security Disruption Risk in the Red Sea Corridor

The Djibouti container shipping market remains exposed to the security climate in the Red Sea corridor because carrier routing decisions can change quickly when risk levels shift. Short-term volume support from rerouting does not remove the longer-term risk that unstable operating conditions can raise costs and weaken schedule reliability. Importers on this corridor are sensitive to changes in transit times, insurance costs, and cargo visibility, so uncertainty can delay booking decisions and reduce shipment efficiency. If direct Red Sea movements normalize on a sustained basis, some transshipment activity that benefited Djibouti during the disruption period could move back to other route patterns. This means the same event that supported traffic in one phase can restrain the Djibouti container shipping market when carriers place more weight on predictable routing and margin protection.

Dependence on Ethiopia-Bound Cargo Creates Demand Concentration

The Djibouti container shipping market has limited domestic demand, so its revenue base is more exposed to decisions made outside Djibouti than those of many other port markets. The 95% concentration of port activity in Ethiopian cargo highlights how little local cargo can offset external slowdowns. A change in Ethiopian trade policy, corridor preferences, or public-sector procurement timing can therefore produce an outsized effect on container volumes[3]Source: Investment and Finance Authority Ethiopia, “Inland Resilience Beyond the Red Sea Chokepoint,” IFA, ifa.gov.et . This concentration also reduces diversification across customer groups, since much of the corridor still relies on a single main inland economy. For the Djibouti container shipping market, this keeps growth prospects attractive but less balanced than in port systems with broader domestic or regional cargo bases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Feeder Dominance Reflects Transshipment Centrality

Feeder and coastal/domestic container shipping held 52.28% of the Djibouti container shipping market share in 2025 and is forecast to expand at 7.76% CAGR through 2031. In the Djibouti container shipping market, this lead reflects the port’s role as a transfer point where mainline cargo is redistributed to smaller ports across the Horn of Africa, the Red Sea, and nearby Indian Ocean routes. SGTD’s capacity roadmap and yard additions support this model because faster handling speeds discharge, sort, and load onward for regional services. The service format follows a hub-and-spoke system in which cargo does not stop in Djibouti as its final destination but continues onward via feeder links.

Deep-sea and ocean container shipping still anchors the long-haul leg connecting Djibouti to Asia and Europe via global carrier networks. MSC, Maersk, CMA CGM, and Hapag-Lloyd shape much of this service layer, while feeder operators compete on frequency, transit reliability, and corridor coverage. Short-sea services remain smaller, but they are gaining relevance as regional trade increasingly depends on more frequent, targeted links between nearby ports. In the Djibouti container shipping industry, the feeder segment is likely to remain the leading service format, as the port’s commercial role is centered on cargo transfer rather than large domestic consumption.

By Container Type: Dry Containers Lead While Reefer Reshapes the Mix

Dry containers accounted for 84.30% of the Djibouti container shipping market size in 2025, reflecting the heavy flow of consumer goods, industrial inputs, and agricultural cargo that do not require controlled-temperature handling. This cargo base remains broad because Ethiopia’s import profile still depends on standard containerized goods such as textiles, electronics, grain, and general merchandise. The operating rhythm at Doraleh also supports high dry-box throughput because standard containers move through the corridor at scale across both gateway and transfer cargo. In the Djibouti container shipping market, dry equipment will therefore remain the largest part of daily container movements.

Reefer containers are projected to grow at a 10.38% CAGR through 2031, the fastest rate in this segment. ONE’s 2025 commentary on the reefer gap in African trade and GCCA’s reporting on East Africa cold-chain momentum both support the view that temperature-sensitive cargo is expanding faster than the market average. Higher pharmaceutical and food imports require stable temperature control, better plug availability, and tighter handover procedures across the corridor. Within the Djibouti container shipping industry, reefer growth will shift the revenue mix and service expectations, even if dry containers remain the largest format by volume.

By Container Size: 40-Foot Units Sustain Volume Leadership

The 40-foot container segment retained 57.29% of the Djibouti container shipping market share in 2025, reflecting the preference of larger commercial importers for high-volume shipment formats that lower unit freight costs on longer routes. This format also suits the vessel classes and yard layouts used in the main Asia-to-Djibouti trade lane. Large wholesalers, manufacturing buyers, and public procurement flows can load more efficiently in 40-foot units when cargo volumes are predictable. In the Djibouti container shipping market, that keeps 40-foot containers are central to corridor economics and terminal planning.

The 20-foot container segment is forecast to grow at a 8.04% CAGR through 2031, making it the fastest-growing size category. Smaller importers, humanitarian cargo handlers, and consolidators prefer this format because it supports lighter financial commitments and more flexible shipment planning. Specialized sizes remain a smaller part of the mix, but they continue to serve project cargo and irregular freight tied to infrastructure and industrial imports. The Djibouti container shipping market, therefore, shows a stable lead for 40-foot units, while faster growth is coming from more flexible box formats that support a broader importer base.

By Load Type: FCL Anchors Revenues While LCL Captures Market Breadth

Full-container-load accounted for 68% of the Djibouti container shipping market share in 2025, reflecting the large-volume purchasing patterns of major wholesalers, government reserve buyers, and industrial importers. FCL also fits the long-haul trade structure because mainline consignments are often planned in full-box volumes before cargo reaches Djibouti. Rail and road transfers from the port to inland destinations are easier to organize at scale when importers move full containers in accordance with planned schedules. This keeps FCL as the main commercial base in the Djibouti container shipping market.

Less-than-container-load is projected to grow at a 9.78% CAGR through 2031, indicating a broader importer base entering the corridor. SME traders, humanitarian agencies, and e-commerce fulfillment activities all support smaller, more frequent consignments. DPFZA’s Port Community System and the World Bank benchmarking cited in the DPFZA release indicate that documentation and turnaround processes are becoming easier to manage, which improves the economics of smaller shipments. In the Djibouti container shipping market, LCL growth widens participation even though FCL remains the core revenue source.

By End-User Industry: FMCG Leads but Healthcare Redefines Growth Premium

FMCG and retail retained a 28.18% share in 2025, making it the largest end-user group in the market. Demand from Ethiopia’s urban consumer base supports recurring imports of packaged food, beverages, personal care products, and household goods. This cargo moves regularly and creates steady replenishment patterns, helping stabilize box demand across the corridor. In the Djibouti container shipping market, FMCG remains the main volume anchor because it combines repeat orders with broad cargo diversity.

Healthcare and pharmaceuticals are projected to grow at a 9.10% CAGR through 2031, the fastest pace among end-user segments. This group is being lifted by vaccine logistics, insulin and oncology distribution, temperature-sensitive generics, and related healthcare cargo that requires tighter control standards. The reefer gap identified by ONE and the East Africa cold-chain momentum highlighted by GCCA both support stronger growth for this end-user stream. The Djibouti container shipping market is therefore adding a higher-value freight stream even as manufacturing, electronics, chemicals, and other cargo groups continue to support the wider base.

Geography Analysis

Doraleh is the country’s only container facility of global significance, handling both gateway cargo for inland delivery and transshipment cargo for neighboring routes. SGTD’s official roadmap places capacity at 2 million TEU in 2026 and outlines a path toward 3.5 million TEU by 2030. This means the Djibouti container shipping market is shaped more by corridor demand and hub function than by local consumption.

The Ethiopia corridor remains the commercial core of the Djibouti container shipping market because inland cargo moves through a long-established route system built around port access. The high share of Ethiopian traffic creates a dependable base when trade is active, but it also limits geographic diversification. Regional transshipment widens the port’s reach by linking cargo flows across the Horn of Africa, the Red Sea, and nearby Indian Ocean routes. As handling capacity and digital coordination improve, Djibouti can serve a wider set of nearby markets without changing its basic gateway role[4]Source: Investment and Finance Authority Ethiopia, “Inland Resilience Beyond the Red Sea Chokepoint,” IFA, ifa.gov.et.

The competitive landscape around Djibouti is still changing, keeping the Djibouti container shipping market exposed to both opportunities and pressure from nearby ports. Deepwater access, larger vessel acceptance, and expanding yard space support Djibouti’s standing with mainline carriers. At the same time, the market’s long-term position will depend on how well it converts this infrastructure advantage into repeated carrier calls, cargo retention, and reliable inland movement. Geography, therefore, remains a strength for the Djibouti container shipping market, but it depends on corridor execution rather than on local scale alone.

Competitive Landscape

The Djibouti container shipping market is moderately concentrated. MSC, Maersk, CMA CGM, and Hapag-Lloyd are the main global names shaping long-haul volume flows, while regional operators compete on shorter connections and corridor reliability. MSC’s local information page for Djibouti and Ethiopia underlines the importance of integrated regional service coverage for carriers operating in this corridor. This setup keeps the Djibouti container shipping market competitive on service frequency and network reach rather than on purely local scale. It also means that no single feeder operator defines the full market even when a few mainline carriers influence the highest-value cargo streams.

A major strategic move in 2026 was Hapag-Lloyd’s agreement to acquire ZIM for around USD 4.2 billion, which would create a larger combined network with more than 400 vessels and over 18 million TEU of annual throughput if approvals proceed. Another important move was MSC’s TiL and BlackRock agreement to acquire CK Hutchison’s 80% stake in 43 international terminals, a transaction that could deepen vertical integration across port and shipping operations. These steps matter to the Djibouti container shipping market because carrier scale and terminal access affect where lines place capacity and how they manage transshipment networks. The mainline end of the market is therefore becoming more closely aligned with global portfolio decisions than with stand-alone country strategies.

Competitive differentiation is also moving into service design, reefer capability, and digital processing in the Djibouti container shipping market. CMA CGM reorganized its Indian Subcontinent and Middle East-East Africa services in March 2026, and earlier launched the KILIMA service, which shows that network planning around East Africa remains active. X-Press Feeders and COSCO Shipping Lines signed a partnership and leasing agreement in June 2025, indicating continued feeder coordination across major trade lanes. DPFZA’s Port Community System gives the Djibouti container shipping market a practical operational advantage by enabling faster documentation and improved corridor visibility, thereby improving the shipper experience and reducing clearance friction.

Djibouti Container Shipping Industry Leaders

A.P. Moller – Maersk A/S

Mediterranean Shipping Company (MSC)

CMA CGM Group

Hapag-Lloyd AG

Ocean Network Express (ONE)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: CMA CGM reorganized its Indian Subcontinent and Middle East-East Africa services, strengthening the KARIBU loop with new Seychelles coverage and direct calls at India’s Mundra and Cochin, and repositioning the SWAHILI EXPRESS as the primary Kenya and Tanzania service. The restructuring covers ports including Mombasa, Dar es Salaam, Djibouti, and Zanzibar.

- February 2026: Maersk signed an order agreement with New Times Shipbuilding for 8 vessels of 18,600 TEU each, with deliveries scheduled for 2029-2030. The order brought Maersk’s total orderbook to 33 vessels, with 4 deliveries still planned for the remainder of 2026.

- February 2026: Hapag-Lloyd AG signed a binding merger agreement to acquire 100% of ZIM Integrated Shipping Services Ltd. for USD 35.00 per share in cash, representing a total transaction value of USD 4.2 billion. The combined entity will operate 400+ vessels and transport over 18 million TEU annually, and regulatory and shareholder approvals are expected by late 2026.

- January 2026: ONE and COSCO Shipping Lines entered into the AL5 Slot Charter Agreement, further optimizing trade flow coordination between Premier Alliance and OCEAN Alliance cooperative frameworks on transoceanic services.

Djibouti Container Shipping Market Report Scope

| Deep-Sea/Ocean Container Shipping |

| Short-Sea Container Shipping |

| Feeder and Coastal/Domestic Container Shipping |

| Dry Containers (General Purpose) |

| Reefer Containers |

| 20-foot Containers (20 ft) |

| 40-foot Containers (40 ft) |

| Other Specialized Sizes |

| Full-Container-Load (FCL) |

| Less-Than-Container-Load (LCL) |

| FMCG and Retail |

| Manufacturing and Automotive |

| Healthcare and Pharmaceuticals |

| Electronics and Electrical Equipment |

| Industrial Chemicals and Raw Materials |

| Others |

| By Service Type | Deep-Sea/Ocean Container Shipping |

| Short-Sea Container Shipping | |

| Feeder and Coastal/Domestic Container Shipping | |

| By Container Type | Dry Containers (General Purpose) |

| Reefer Containers | |

| By Container Size | 20-foot Containers (20 ft) |

| 40-foot Containers (40 ft) | |

| Other Specialized Sizes | |

| By Load Type | Full-Container-Load (FCL) |

| Less-Than-Container-Load (LCL) | |

| By End-User Industry | FMCG and Retail |

| Manufacturing and Automotive | |

| Healthcare and Pharmaceuticals | |

| Electronics and Electrical Equipment | |

| Industrial Chemicals and Raw Materials | |

| Others |

Key Questions Answered in the Report

What is the projected value of Djibouti container shipping by 2031?

The Djibouti container shipping market is projected to reach USD 446.40 million by 2031, up from USD 321.51 million in 2026, at a 6.78% CAGR over 2026-2031.

Which service type leads container shipping activity in Djibouti?

Feeder and coastal or domestic container shipping led with a 52.28% share in 2025 and is also the fastest-growing service type, with a 7.76% CAGR through 2031.

Why is Djibouti important for regional container trade?

Djibouti serves as a Red Sea gateway and transshipment hub for Ethiopia and nearby regional ports, supported by Doraleh’s 2 million TEU capacity in 2026 and planned expansion toward 3.5 million TEU by 2030.

Which cargo categories are growing fastest through Djibouti?

Reefer cargo and healthcare-related shipments are growing fastest, with reefer containers at 10.38% CAGR and Healthcare and pharmaceuticals at 9.10% CAGR through 2031.

How dependent is Djibouti on Ethiopian cargo flows?

The corridor is highly concentrated, with Ethiopian cargo accounting for 95% of Djibouti port activity in 2026, which supports volume but increases exposure to corridor and policy shifts.

What are the main competitive strengths of Doraleh Container Terminal?

Its strengths include deepwater vessel acceptance, added RTG capacity, a sea-yard expansion plan, and a Port Community System that has reduced turnaround time from 24 hours to around 1 hour based on DPFZA and World Bank benchmarking.

Page last updated on: