Disposable Ureteroscope Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 238.71 Million |

| Market Size (2031) | USD 301.89 Million |

| Growth Rate (2026 - 2031) | 4.81% CAGR |

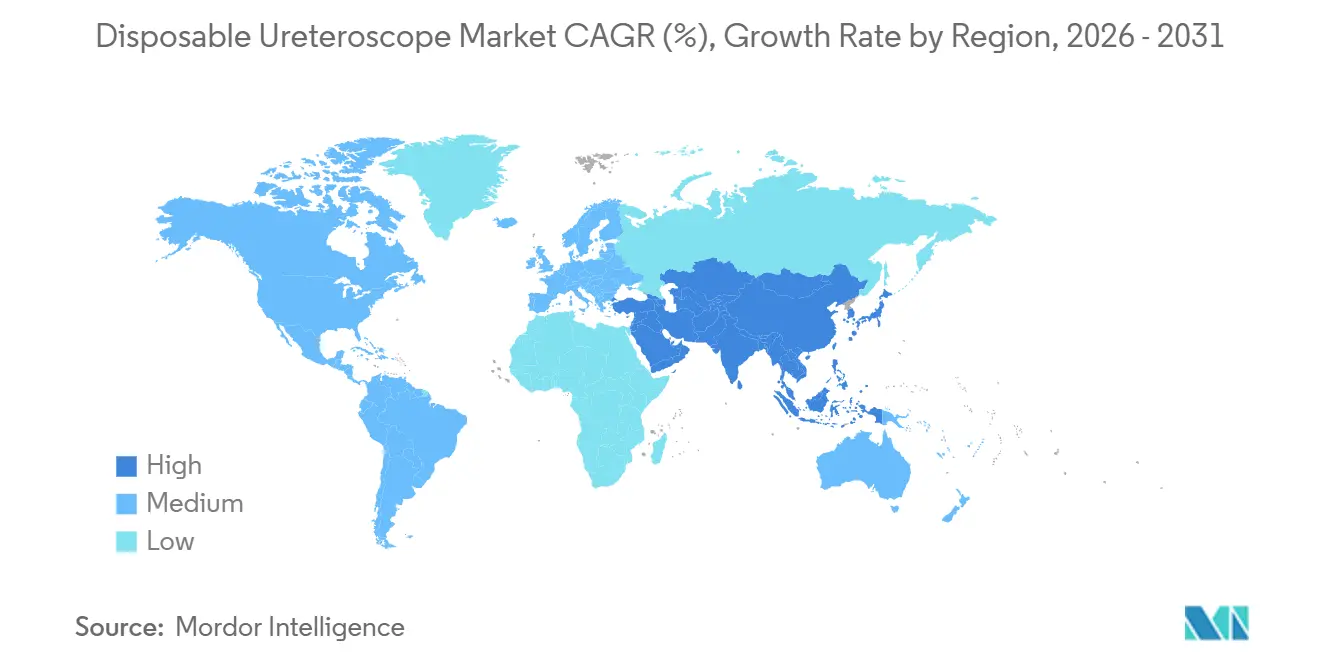

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Disposable Ureteroscope Market Analysis by Mordor Intelligence

The Disposable Ureteroscope Market size is estimated at USD 238.71 million in 2026, and is expected to reach USD 301.89 million by 2031, at a CAGR of 4.81% during the forecast period (2026-2031).

Infection-control imperatives, notably the FDA’s 2017–2021 review of 450 scope-related infection reports, are steering procurement toward single-use devices, while emerging sustainability mandates create countervailing pressure, especially in Europe. Unit prices have fallen as CMOS imaging sensors displaced CCD components, yet repair avoidance and reduced turnaround times, rather than price, remain the decisive adoption triggers in low-volume centers. The disposable ureteroscope market benefits as ambulatory surgical centers (ASCs) proliferate and reimbursement gaps close. In contrast, European hospitals negotiate hybrid configurations that reduce hazardous plastic volumes while still guarding against cross-contamination. Competition is tightening because Chinese firms now supply flexible scopes at sub-USD 1,000 price points, compressing margins for Western leaders even as innovation pivots to AI-assisted visualization.

Key Report Takeaways

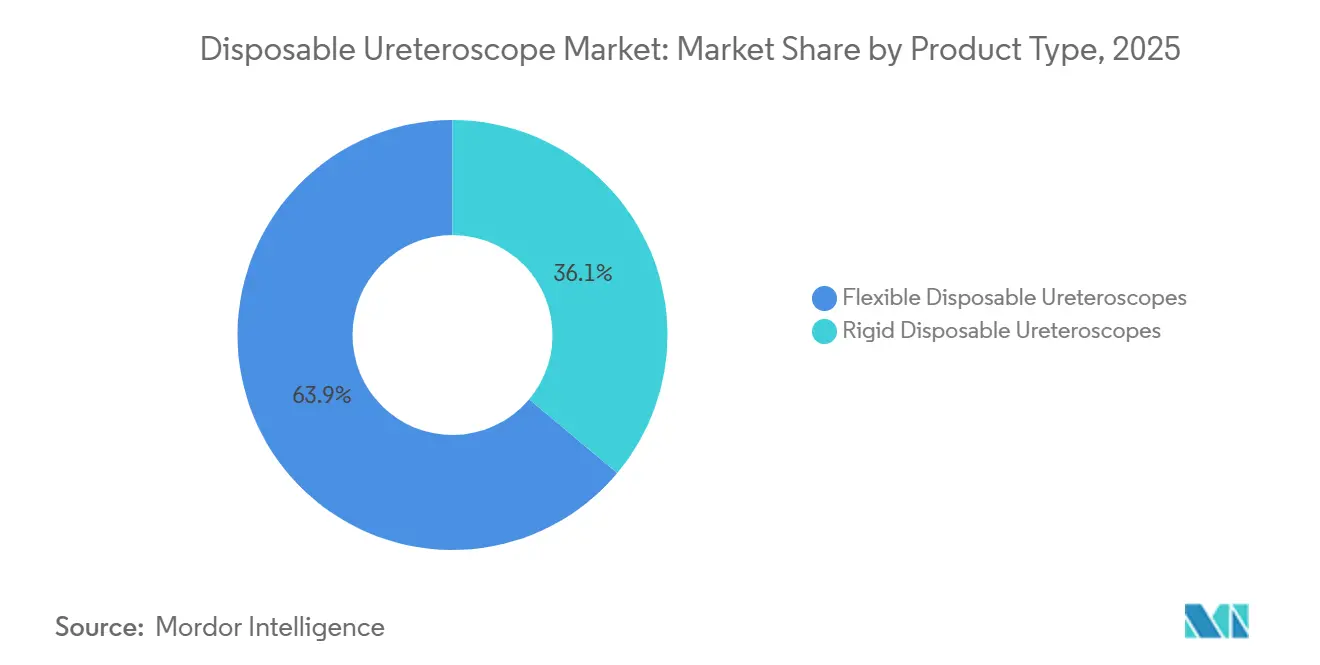

- By product type, flexible scopes led the disposable ureteroscope market with 63.91% market share in 2025 and are expanding at a 5.31% CAGR through 2031.

- By application, urolithiasis accounted for 72.68% of the disposable ureteroscope market in 2025, while kidney cancer procedures posted the fastest 5.83% CAGR through 2031.

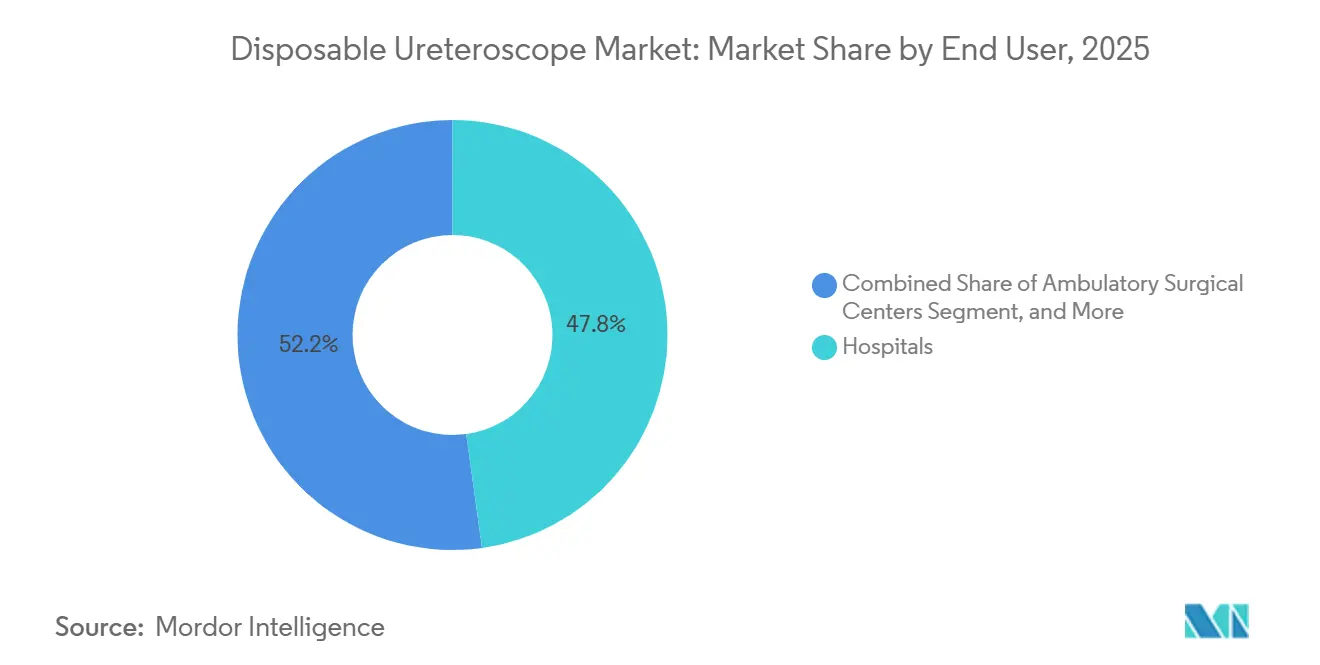

- By end user, hospitals accounted for 47.82% of revenue in 2025, whereas ASCs are growing at a robust 7.26% CAGR, driven by favorable CMS payment updates.

- By geography, North America retained 42.82% revenue leadership in 2025, yet Asia-Pacific is advancing at a 7.69% CAGR on the back of China’s and India’s large-scale capacity additions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Disposable Ureteroscope Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Urolithiasis & Urinary Tract Stones | +1.2% | Global, with acute concentration in North America, Middle East | Long term (≥ 4 years) |

| Growing Adoption of Minimally Invasive Endourology Procedures | +1.0% | North America, Europe, APAC core markets | Medium term (2-4 years) |

| Infection-Control & Regulatory Emphasis on Patient Safety | +0.9% | Global, led by North America & EU regulatory mandates | Short term (≤ 2 years) |

| Technological Advances in Digital Imaging & Maneuverability | +0.7% | North America, Europe, Japan, Australia | Medium term (2-4 years) |

| Cost Parity for Low-Volume Centers Via Repair-Avoidance | +0.5% | North America, Europe, select APAC facilities | Medium term (2-4 years) |

| ASC Boom in Emerging Markets Accelerating Disposable Uptake | +0.8% | APAC core (China, India), GCC, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Urolithiasis & Urinary Tract Stones

Kidney stone prevalence in the United States rose, and recurrence occurs in roughly half of patients within a decade.[1]George Kokor, “Cost-Effectiveness of Disposable Versus Reusable Ureteroscopes,” National Center for Biotechnology Information, ncbi.nlm.nih.gov This epidemiological surge translates into USD 5.3 billion in annual direct costs and productivity losses. The Middle East and North Africa have a 12%–13% prevalence, driven by hot climates and high-sodium diets. Climate models indicate that warming will expand the kidney-stone belt by up to 20% of the population base by 2030, thereby expanding the disposable ureteroscope market. Urologists increasingly favor flexible ureteroscopy for stones smaller than 2 cm, reinforcing demand for single-use optics that eliminate biofilm concerns.

Growing Adoption of Minimally Invasive Endourology Procedures

Flexible ureteroscopy accounts for roughly 70% of renal stone interventions in North America and Western Europe because it delivers 73%–93% stone-free rates with shorter hospital stays. Simulation-based curricula released by the American Urological Association in 2024 reduced the learning curve by 20%–25%, enabling more surgeons to achieve proficiency earlier. In India and China, private chains such as Apollo Hospitals reported a 35% rise in foreign patient stone-treatment cases in fiscal 2025, and these centers standardize on disposables to avoid the expense of sterile reprocessing. The cascading procedural shift keeps the disposable ureteroscope market on an upward trajectory.

Infection-Control & Regulatory Emphasis on Patient Safety

The FDA’s 2021 probe into infection events prompted updated 2024 guidance requiring manufacturers to validate cleaning protocols for channels under 4 mm. Single-use scopes eliminate 12–15 manual disinfection steps, saving USD 120–USD 957 per case. The U.K. National Health Service now requires every endoscopy unit to maintain a 20% disposable inventory, a policy likely to extend across the EU under 2026 ECDC guidelines. Such mandates directly amplify the disposable ureteroscope market.

Technological Advances in Digital Imaging & Maneuverability

CMOS sensor integration lowered per-unit prices by 30%–40% while raising image resolution to 1080p.[2]Institute of Electrical and Electronics Engineers, “CMOS Sensor Technology Advances,” ieee.org Olympus’s RenaFlex, cleared in April 2024, couples a 270-degree deflection with a 3.6 French working channel, matching reusable digital performance at half the capital cost. Boston Scientific’s LithoVue Elite, introduced in late 2025, adds AI-assisted stabilization that corrects surgeon tremor and shortens procedure time. These advances narrow the perceived gap between reusable and single-use ureteroscopes, spurring growth in the disposable ureteroscope market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Per-Unit Cost & Reimbursement Gaps | -0.6% | Global, acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Environmental Waste & Sustainability Pressure | -0.3% | Europe, North America (regulatory focus), spillover to APAC | Medium term (2-4 years) |

| Supply-Chain Risk for Medical-Grade Polymers & Chips | -0.4% | Global, concentrated in APAC manufacturing hubs | Short term (≤ 2 years) |

| Learning-Curve & Ergonomics Variability Among Surgeons | -0.2% | Global, more pronounced in low-volume centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Per-Unit Cost & Reimbursement Gaps

Single-use scopes priced at USD 700–USD 3,180 strain public systems where per-capita spend is under USD 500.[3]World Health Organization, “Global Health Expenditure Database,” who.int Brazil reimburses only USD 850, leaving hospitals to absorb shortfalls. Given India’s reimbursement of USD 600, clinicians turn to rigid disposables priced under USD 600. United States private insurers introduced prior authorization in 2025, delaying cases by several days. The cost hurdle curbs wider uptake and tempers the expansion of the disposable ureteroscope market in price-sensitive regions.

Environmental Waste & Sustainability Pressure

EU directives obligate manufacturers to finance take-back schemes by 2027, and each scope adds 150–200 g of complex waste. Germany now imposes carbon fees of EUR 50–100 per tonne on hospitals that exceed their baseline waste levels. France grants bonus points in tenders to vendors offering hybrid solutions. Such policies slow the disposable ureteroscope market in Europe until modular or recyclable designs mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Flexible Scopes Sustain Growth

Flexible models held a 63.91% share of the disposable ureteroscope market in 2025, with a forecast 5.31% CAGR, widening their advantage over rigid devices. Superior 270-degree deflection allows surgeons to access posterior calyces without repositioning and shortens operative time. CMOS-based flexible scopes account for more than half of the segment thanks to 30%–40% lower production costs and stronger low-light imaging relative to CCD sensors. Rigid scopes remain relevant for distal ureter stones and budget-constrained markets, though their 36.09% share will erode as CMOS costs approach rigid pricing levels.

Investment is pouring into AI-enabled flexible devices; Boston Scientific’s LithoVue Elite auto-optimizes contrast and white balance, cutting case length by nearly 10% in early trials. Rigid units are facing commoditization because Chinese suppliers such as Zhuhai PUSEN sell ISO-compliant products for under USD 400. Consequently, the disposable ureteroscope market tilts ever more heavily toward sophisticated flexible platforms.

By Application: Urolithiasis Dominates, Oncology Gains Momentum

Urolithiasis accounted for 72.68% of the disposable ureteroscope market share in 2025, as flexible scopes achieve up to 93% stone-free rates for sub-2 cm calculi. Prevalence continues to rise with obesity and dietary sodium intake, keeping stone extraction volumes high. Kidney cancer applications grow at a 5.83% CAGR because conservative ureteroscopic laser ablation now replaces radical surgery for low-grade upper tract urothelial carcinoma. New AUA guidelines mandate ureteroscopic biopsy before definitive treatment, adding an estimated 20,000 U.S. procedures annually.

Urethral stricture management accounts for 8%–10% of procedure volume and often uses rigid scopes, whereas “other” tasks, such as stent placement, make up the balance. While urolithiasis holds numerical primacy, oncology’s faster growth diversifies procedure mix, broadening the disposable ureteroscope industry’s use cases.

By End User: ASC Adoption Accelerates

Hospitals generated 47.82% of 2025 revenue, yet ASCs are expanding at a 7.26% CAGR after CMS boosted ASC reimbursement by 3.1% in 2024. ASCs turn over rooms 25–30 minutes faster with single-use scopes because no high-level disinfection is required, resulting in 40%–60% cost savings per case. United States ASC counts should top 6,500 by 2028, with urology-only facilities comprising an increasing share.

Specialty clinics and diagnostic centers, 15%–18% of end-user revenue, prefer rigid disposables for straightforward distal interventions. Hospitals will still manage large stones and oncology cases that require ancillary imaging and multidisciplinary support. Still, community facilities and ASCs will keep steering the disposable ureteroscope market toward single-use dominance in routine stone care.

Geography Analysis

The disposable ureteroscope market in North America accounted for 42.82% of the market share in 2025 and is expected to exhibit stable mid-single-digit growth. U.S. institutions perform nearly 400,000 ureteroscopies yearly, and disposable penetration already exceeds 25% in ASCs. Canadian provinces began pilot evaluations in 2025, though national uptake is gradual owing to global budget constraints. Mexico’s private hospitals cater to medical tourists and thus purchase premium flexible models, whereas public facilities rely on reusables.

Asia-Pacific is the fastest-expanding region, with a 7.69% CAGR. China’s domestic vendors supply CMOS-based flexible scopes at USD 800–USD 1,000, seizing roughly one-third of local revenues and boosting overall regional affordability. India’s hospitals added double-digit capacity from 2023 to 2025, but rigid disposables dominate because procedure reimbursement remains capped at USD 600. Japan, Australia, and South Korea exhibit mature, premium demand patterns, each exceeding 30% single-use penetration in high-volume centers after 2024 insurance changes.

Germany’s carbon fees and France’s tender preferences dampen growth, although the U.K. mandate for a 20% disposable inventory secures a baseline level of demand. Southern European countries adopt disposables mainly in private clinics that serve international patients, reflecting divergent reimbursement climates across the continent. South Africa’s most immense private groups pilot disposable scopes for immunocompromised patients, while the rest of Sub-Saharan Africa remains nascent due to limited urology infrastructure. South America adds 5%–7% of turnover, with Brazil’s 2024 reimbursement policy unlocking access for over 2,500 municipal hospitals, though low caps favor rigid models.

Competitive Landscape

The top five brands, Boston Scientific, Olympus, Ambu, Karl Storz, and Stryker, control significant revenue, leaving meaningful space for mid-tier and regional challengers. Olympus’s RenaFlex, cleared in 2024, couples a 9.5 French shaft with 1080p CMOS imaging and sells for USD 2,500–USD 3,000, a premium justified through bundled fiber and basket contracts that lower overall episode costs for integrated delivery networks. Boston Scientific’s refreshed LithoVue Elite adds AI stabilization, capturing about one-fourth of U.S. disposable sales by packaging scopes with ancillary consumables under value-based deals.

Ambu pioneered single-use endoscopy yet posted a 12% 2024 revenue decline as rivals matched its imaging quality at lower price points. Chinese entrants such as Zhuhai PUSEN and Mindray offer flexible units under USD 1,000, eroding Western margins in Asia-Pacific and entering Latin America via distributor alliances. European sustainability rules catalyze R&D into modular hybrids; Karl Storz and Richard Wolf released mid-priced offerings in 2024 that combine disposable optics with reusable handles, hedging against infection-control directives while addressing waste concerns.

White-space opportunities include pediatric scopes under 7 French, AI-based tissue classification, and biodegradable housings that comply with circular-economy mandates. Patent trends from 2024–2025 show an uptick in filings for recyclable polymer blends and detachable optical blocks, signaling that technology leadership will increasingly revolve around eco-design rather than pure imaging quality.

Disposable Ureteroscope Industry Leaders

Cook Medical

Fujifilm Holdings Corporation

Karl Storz SE & Co. KG

Olympus Corporation

Stryker Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: OPCOM Medical won its first FDA clearance for a flexible single-use ureteroscope, marking Taiwan’s entry into the U.S. market.

- May 2024: Cook Medical launched the Ascend Single-Use Flexible Ureteroscope across the United States and Canada, expanding its stone-management lineup.

- April 2024: Cook Medical began shipping the Ascend Single-Use Flexible Ureteroscope in both North American markets to deepen urology customer support.

- April 2024: Olympus secured FDA 510(k) clearance K233275 for RenaFlex, a 9.5 French disposable scope with 270-degree deflection that targets 15%–20% U.S. share by 2027 through bundled purchasing.

Global Disposable Ureteroscope Market Report Scope

The Disposable Ureteroscope Market Report is Segmented by Product Type (Flexible Disposable Ureteroscopes with CMOS, CCD, and Other Sensors; Rigid Disposable Ureteroscopes), Application (Urolithiasis, Kidney Cancer, Urethral Stricture, Others), End User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

| Flexible Disposable Ureteroscopes | CMOS Sensor Based |

| CCD Sensor Based | |

| Others | |

| Rigid Disposable Ureteroscopes |

| Urolithiasis |

| Kidney Cancer |

| Urethral Stricture |

| Others |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics / Diagnostic Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Flexible Disposable Ureteroscopes | CMOS Sensor Based |

| CCD Sensor Based | ||

| Others | ||

| Rigid Disposable Ureteroscopes | ||

| By Application | Urolithiasis | |

| Kidney Cancer | ||

| Urethral Stricture | ||

| Others | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics / Diagnostic Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the disposable ureteroscope market?

The disposable ureteroscope market size is USD 238.71 million in 2026 and is forecast to reach USD 301.89 million by 2031.

How fast is the market expected to grow?

The market is advancing at a 4.81% CAGR through 2031, with Asia-Pacific posting the highest regional CAGR of 7.69%.

Which product segment leads revenue?

Flexible scopes hold 63.91% share, driven by 270-degree deflection that improves access to complex renal anatomy.

Why are ASCs adopting single-use scopes quickly?

CMS raised ASC reimbursement by 3.1% in 2024 and disposables cut turnover time, delivering 40%–60% per-case savings.

How do sustainability rules affect scope adoption in Europe?

EU directives require recycling programs and impose carbon fees, encouraging hybrid designs that blend reusable handles with disposable optics.

Page last updated on: