Disposable Blood Pressure Cuffs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 412.02 Million |

| Market Size (2031) | USD 732.95 Million |

| Growth Rate (2026 - 2031) | 12.21% CAGR |

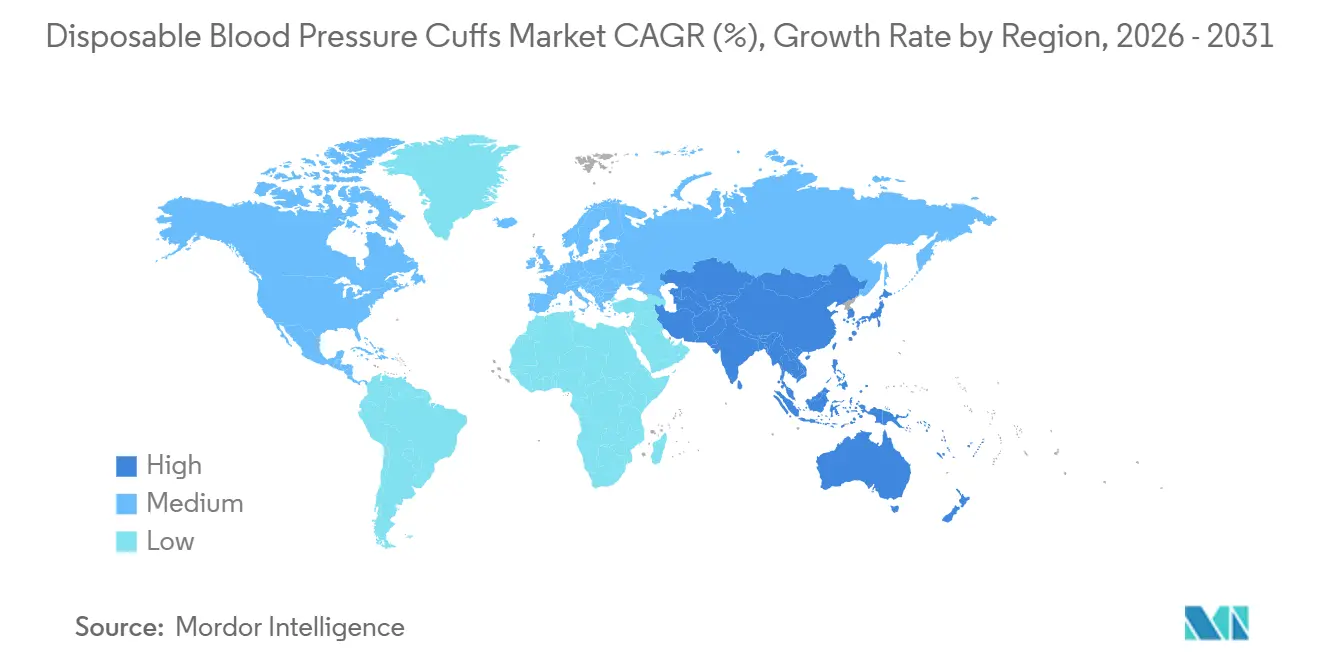

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

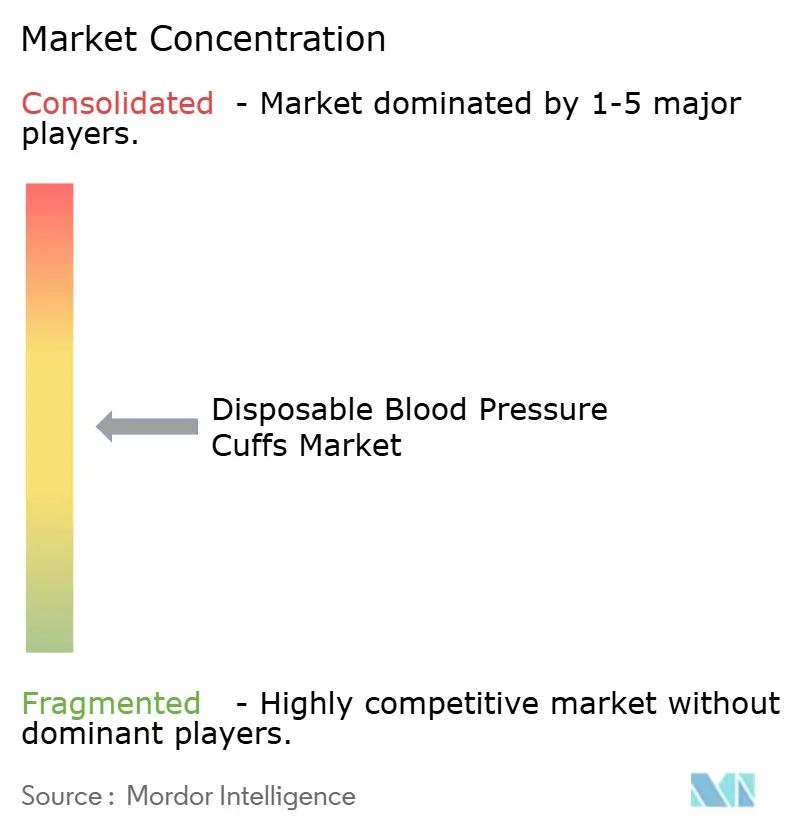

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Disposable Blood Pressure Cuffs Market Analysis by Mordor Intelligence

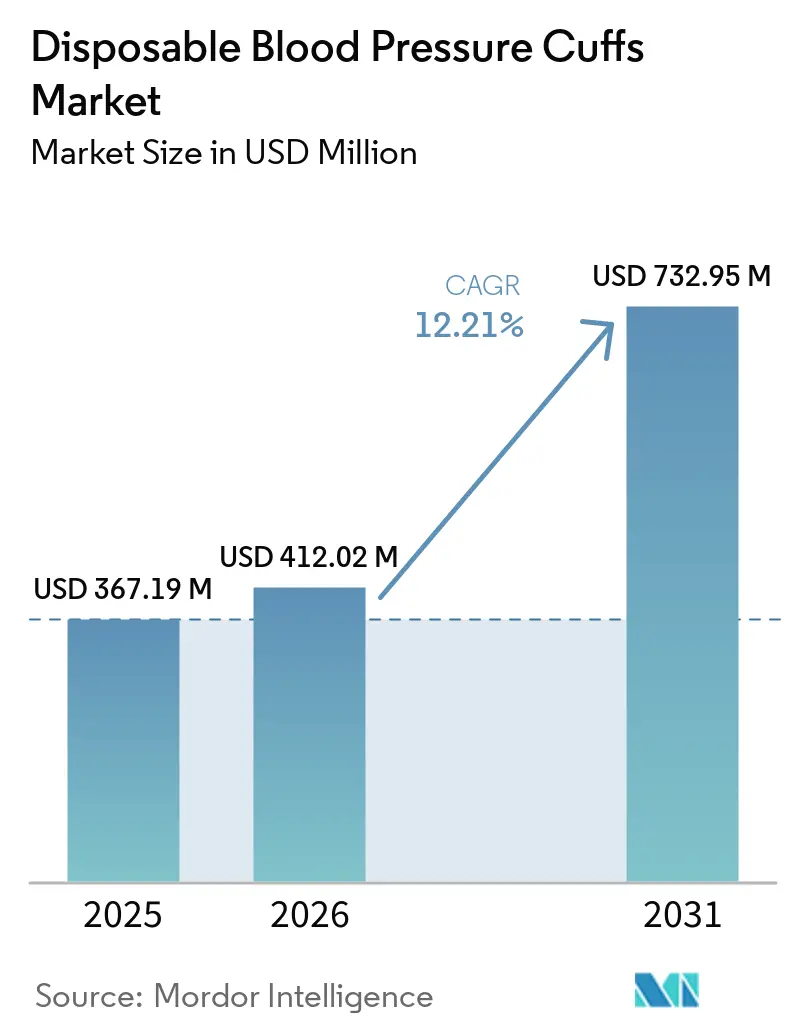

The Disposable Blood Pressure Cuffs Market size is projected to expand from USD 367.19 million in 2025 and USD 412.02 million in 2026 to USD 732.95 million by 2031, registering a CAGR of 12.21% between 2026 to 2031.

Hospital purchasing trends are shifting as infection prevention teams and procurement committees increasingly favor single-patient-use products over shared cuffs. An APIC issue brief revealed that 23% to 100% of non-invasive portable clinical items, including blood pressure cuffs, were contaminated in surveyed facilities, with up to 25% carrying multi-drug-resistant organisms. These findings have made contamination risks a critical factor in healthcare purchasing decisions. Additionally, the operational challenges of cleaning, staff training, audit record maintenance, and reprocessing compliance are reducing the appeal of reusable cuff programs, particularly in settings with strict accreditation standards.

Key Report Takeaways

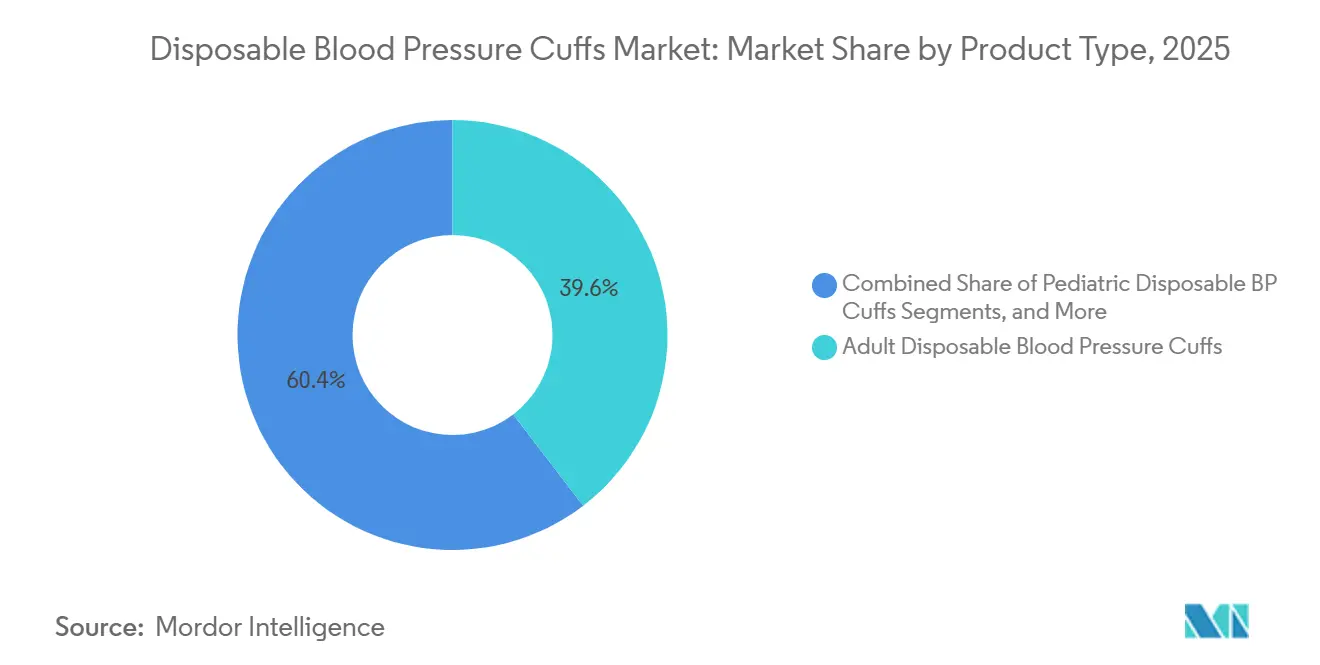

- By product type, adult disposable blood pressure cuffs held 39.63% share in 2025, while pediatric disposable blood pressure cuffs are projected to expand at a 14.38% CAGR through 2031.

- By material, vinyl disposable blood pressure cuffs accounted for 46.43% share in 2025, while thermoplastic polyurethane disposable blood pressure cuffs are forecast to grow at a 15.55% CAGR through 2031.

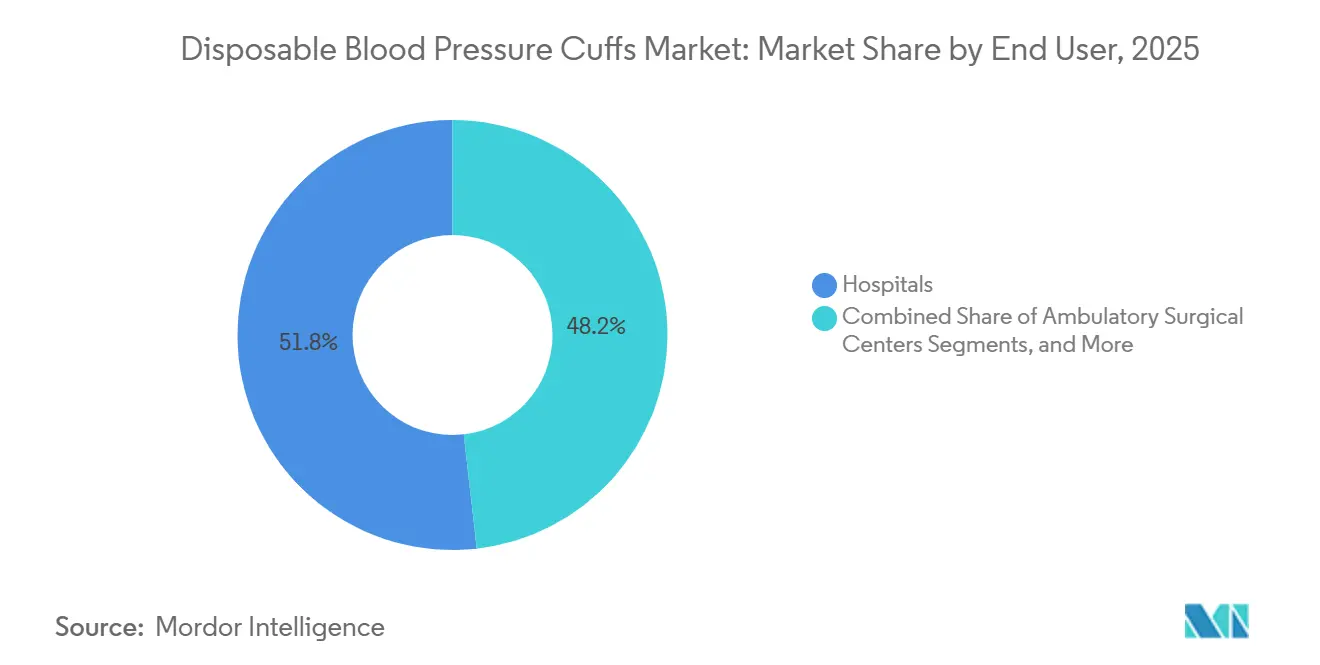

- By end user, hospitals contributed 51.78% of total market value in 2025, while ambulatory surgical centers are projected to advance at a 13.88% CAGR through 2031.

- By geography, North America held 38.86% share in 2025, while Asia-Pacific is projected to expand at an 14.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Disposable Blood Pressure Cuffs Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising infection-control protocols in procedures | +3.5% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Expansion of single-use clinical consumables | +2.8% | Global | Medium term (2-4 years) |

| Standardization of cuff sizing to reduce misdiagnosis | +1.5% | North America and Europe, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Shift toward patient-per-use accessories in icus | +2.2% | Global, strongest in North America and Asia-Pacific | Short term (≤ 2 years) |

| Growth in contract manufacturing for private label brands | +1.2% | Asia-Pacific core, with spillover to Middle East and Africa | Medium term (2-4 years) |

| Compatibility with multi-vendor monitor flexibility | +0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Infection-Control Protocols in Procedures

The disposable blood pressure cuffs market is experiencing growth due to stricter infection-control protocols. In April 2025, the CDC updated its guidelines, requiring reusable medical equipment, including blood pressure cuffs, to be cleaned and reprocessed before reuse. Staff involved in reprocessing must also undergo training and periodic assessments.[1]Centers for Disease Control and Prevention, “Core Infection Prevention and Control Practices for Safe Healthcare Delivery in All Settings,” CDC, cdc.gov Evidence shows contamination on portable non-critical devices is frequent enough to influence procurement decisions. When hospitals account for disinfectants, documentation, staff time, and quality checks, the cost difference between reusable and disposable cuffs becomes less clear. Additionally, a 2025 multisociety guidance paper increased pressure on healthcare systems to improve sterilization and disinfection practices, further driving demand for disposable cuffs.[2]National Academy of Medicine, “Addressing Major Sources of Carbon Emissions for Disposable Blood Pressure Cuffs,” NAM Perspectives, nam.edu

Shift Toward Patient-Per-Use Accessories in ICUs

ICUs and NICUs are significantly contributing to the growth of the disposable blood pressure cuffs market due to high patient vulnerability and intensive monitoring needs. A 2025 study revealed that 40.1% of critically ill neonates developed healthcare-associated infections, with 30.3% experiencing sepsis and higher mortality rates in those under 750 g. Neonatal care involves repeated cuff inflation and skin contact, increasing cross-contamination risks.[3]T. V. B. Araújo et al., “Epidemiology and Management of Infections in Critically Ill Neonates: Findings from a Cohort Study in a Brazilian Neonatal Intensive Care Unit,” Journal of Medical Microbiology, microbiologyresearch.org Standardized neonatal blood pressure charts, implemented in January 2024, have improved monitoring discipline, leading to higher cuff usage per patient. This trend highlights that demand in intensive care grows with monitoring frequency, not just patient admissions.

Standardization of Cuff Sizing to Reduce Misdiagnosis

The market is benefiting from a focus on cuff fit and size accuracy, as incorrect sizing can distort readings and lead to repeat measurements. Hospitals are prioritizing validated size ranges, especially in pediatric and neonatal care, where improper fit can quickly affect clinical outcomes. Standardized disposable ranges simplify cuff selection at the point of care, reducing reliance on shared reusable stock. Suppliers offering segmented options for neonatal, pediatric, adult, and large-arm cuffs are gaining traction. Regulatory scrutiny on neonatal cuff design increased in 2025, further supporting the market as hospitals seek products that minimize fit-related errors and streamline workflows.

Growth in Contract Manufacturing for Private Label Brands

Contract manufacturing is driving growth in the disposable blood pressure cuffs market by enabling private-label brands to offer high-quality products with diverse connector options. Asia-Pacific plays a key role, with localized medical-grade TPU production improving access to certified materials for local and export markets. ISO-certified factories now produce a wide range of cuffs with shorter lead times, reducing sourcing concentration and enhancing private-label credibility. Hospitals, surgical centers, and distributors benefit from cost control without compromising compatibility. Improved material availability near manufacturing bases strengthens procurement negotiations, reshaping supplier dynamics while maintaining demand.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Higher per-patient consumable cost versus reusable | -2.5% | Middle East and Africa, South America, and emerging Asia-Pacific markets | Long term (≥ 4 years) |

| Hospital reprocessing habits and installed base resistance | -1.8% | Global, with concentration in Middle East and Africa and South America | Medium term (2-4 years) |

| Connector fragmentation across monitor platforms | -1.2% | Global | Medium term (2-4 years) |

| Waste-handling and sustainability pressure | -0.9% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Per-Patient Consumable Cost Versus Reusable

In budget-conscious hospitals, outpatient clinics, and government-led tenders, financial teams often evaluate disposable blood pressure cuffs based on their per-patient consumable cost. This focus on unit price limits market penetration in facilities with reusable cuffs, trained staff, and established cleaning routines, despite hidden labor and compliance costs. In emerging markets, centralized purchasing separates infection-control decisions from budgets handling clinical and administrative consequences. Transitioning to disposable cuffs requires changes in ordering, storage, staff preferences, and materials management, slowing adoption in price-sensitive environments.

Waste-Handling and Sustainability Pressure

The disposable blood pressure cuffs market faces sustainability challenges as single-use products contribute significantly to hospital waste and carbon emissions. Manufacturing accounts for the largest share of lifecycle emissions, with incineration adding further environmental impact. Health systems, particularly in Europe and parts of North America, demand suppliers address material composition, disposal methods, and environmental trade-offs compared to reusable alternatives. Suppliers relying on conventional single-use plastics without eco-friendly solutions may face challenges in securing public tenders. Sustainability pressures are reshaping the market, favoring products aligned with environmentally-conscious practices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Adult Volumes Dominant, Pediatric Clinical Demand Accelerates

In 2025, adult disposable blood pressure cuffs accounted for 39.63% of the market, reflecting the routine nature of adult blood pressure monitoring in hospitals, clinics, and surgical centers. This segment dominates the market as adult patients represent the majority of daily monitoring in healthcare facilities. Rising obesity rates are driving demand for the 'others' category, which includes thigh and large-arm formats, where standard adult cuffs are unsuitable.

Pediatric disposable blood pressure cuffs are projected to grow at a 14.38% CAGR through 2031, making them the fastest-growing segment. Increased focus on blood pressure screening and monitoring for at-risk children is driving this growth. Neonatal cuffs, though a smaller niche, require higher sensitivity due to critical factors like fit and monitor performance, positioning suppliers with diverse size ranges favorably in premium hospital accounts.

By Material: Vinyl Leads by Installed Base, TPU Reshapes Premium Segment

Vinyl disposable blood pressure cuffs held 46.43% of the market in 2025, supported by cost-effectiveness, broad compatibility, and established use in hospitals. Healthcare systems prefer vinyl for its scalability and seamless integration with existing setups, which is critical in large procurement contracts. Nylon offers better durability than vinyl for specific applications but lacks the premium positioning of TPU.

Thermoplastic polyurethane (TPU) disposable blood pressure cuffs are expected to grow at a 15.55% CAGR through 2031, making them the fastest-growing material segment. TPU's biocompatibility and wear resistance make it ideal for high-acuity settings like neonatal and pediatric care. Covestro's localized TPU production enhances supply visibility for regional manufacturers, supporting higher selling prices and better margins for TPU-based cuffs.

By End User: Hospital Procurement Anchors the Market, ASCs Emerge as a Strategic Growth Vector

Hospitals contributed 51.78% of the market in 2025, making them the largest end-user segment. Hospitals drive the market due to high patient volumes, intensive monitoring, and strict infection control. Annual contracts through group purchasing organizations further solidify their importance by ensuring stable volumes and pricing.

Ambulatory surgical centers (ASCs) are projected to grow at a 13.88% CAGR through 2031, emerging as the fastest-growing end-user segment. The shift of procedures to outpatient settings with stringent infection prevention standards is fueling this growth. While clinics, home care, and emergency transport add demand, their growth remains uneven due to the continued use of reusable cuffs in cost-sensitive care pathways.

Geography Analysis

In 2025, North America accounted for 38.86% of the disposable blood pressure cuffs market share, maintaining its lead due to robust infection prevention systems and a higher willingness to invest in compliance-ready products. The U.S. market benefits from CDC guidelines and accreditation-linked purchasing standards, which drive healthcare facilities toward single-patient-use programs or improved reprocessing practices. Canada follows a similar trend, while Mexico shows growth potential as private hospitals modernize their clinical equipment. Baxter's expansion of U.S. manufacturing for Welch Allyn FlexiPort cuffs in 2025 enhanced supply resilience and strengthened local supply confidence.

Europe held a significant share of the disposable blood pressure cuffs market in 2025, shaped by the balance between infection control needs and environmental concerns. Strong clinical standards in Germany, the U.K., France, and the Nordics support the market, with procurement teams focusing on patient safety and device performance. The U.K. is exploring reusable alternatives to assess their impact on waste and emissions. Regions like Italy, Spain, Eastern Europe, and Turkey offer growth opportunities due to hospital modernization and expanding ambulatory care networks.

Asia-Pacific is projected to grow at a 14.67% CAGR through 2031, making it the fastest-growing region in the disposable blood pressure cuffs market. Growth in China and India is driven by hospital network expansion and demand for cost-effective, compliant consumables, while Japan and South Korea focus on premium care environments. The region benefits from increased manufacturing depth, supported by Covestro's localization of medical-grade TPU production in Taiwan. In the Middle East, Africa, and South America, private hospital expansions and rising infection-control expectations are gradually driving the adoption of single-patient-use cuffs. In the GCC, accreditation goals among private hospitals are boosting demand for disposable monitoring accessories that meet international standards.

Competitive Landscape

Baxter International, Cardinal Health, Medline Industries, Koninklijke Philips, and GE HealthCare Technologies dominate sales of disposable blood pressure cuffs in hospitals. The market is influenced by connector ecosystems, as monitor manufacturers often use proprietary formats for cuffs. This creates challenges for hospitals wishing to switch suppliers without altering their existing hardware. Manufacturers investing in multi-connector product lines can cater to a broader range of monitors, reducing the need for extensive stock-keeping units. In 2025, Baxter navigated FlexiPort allocation challenges and bolstered domestic manufacturing, highlighting the market's sensitivity to supply continuity.

While price remains a factor, the market increasingly emphasizes materials and environmental considerations. Baxter’s Hillrom FlexiPort EcoCuff exemplifies how established players are promoting single-patient-use products that prioritize environmental concerns, avoiding substances like BPA, DEHP, latex, and PVC. Concurrently, Chinese and Taiwanese OEM and ODM suppliers intensify price competition, offering broad connector compatibility and white-label programs backed by manufacturing certifications. This dynamic simplifies portfolio expansion for regional distributors and private-label entrants without requiring production assets. OMRON’s 2025 U.S. launch of monitors featuring its FDA De Novo-authorized IntelliSense AFib algorithm raises standards for cuff fit and cycling reliability, benefiting suppliers aligning with advanced monitoring systems.

Despite the dominance of established brands in acute care, opportunities for differentiation persist in the disposable blood pressure cuffs market. Suppliers focusing on monitor compatibility, reliable fulfillment, and environmental considerations over pricing are likely to gain. Cardinal Health’s 2025 introduction of the Kendall DL Multi System highlights the expansion of single-patient-use accessories into integrated monitoring workflows. This shift toward disposable monitoring systems is expected to sustain competition among major brands, private-label entities, and regional producers.

Disposable Blood Pressure Cuffs Industry Leaders

GE HealthCare Technologies Inc.

Cardinal Health, Inc.

Koninklijke Philips N.V.

SunTech Medical, Inc.

OMRON Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Medline Industries expanded its disposable blood pressure cuff portfolio by registering new single-patient-use formats in the FDA database, reinforcing its focus on hospital and ASC channels.

- June 2025: Unimed Medical Supplies, Inc. obtained FDA 510(k) clearance for its Disposable Neonatal NIBP Cuff, enhancing the availability of neonatal single-use cuffs for US NICUs.

- May 2025: Baxter International ended allocation for Welch Allyn FlexiPort Disposable Blood Pressure Cuffs after expanding manufacturing capacity to address supply constraints in North America.

- May 2025: OMRON Healthcare introduced disposable home blood pressure monitors with an IntelliSense AFib algorithm, offering advanced atrial fibrillation detection with high sensitivity and specificity.

Global Disposable Blood Pressure Cuffs Market Report Scope

As per the scope of the report, disposable blood pressure cuffs are single-patient-use bands that wrap around your arm. They are worn during a hospital stay to track blood pressure. When you leave, the cuff is thrown away to stop the spread of germs.

The disposable blood pressure cuffs market is segmented by product type, material, end-user, and geography. By product type, the market includes adult disposable blood pressure cuffs, pediatric disposable blood pressure cuffs, neonatal disposable blood pressure cuffs, and others. By material, the market is segmented into vinyl disposable blood pressure cuffs, nylon disposable blood pressure cuffs, thermoplastic polyurethane disposable blood pressure cuffs, and others. By end-user, the market is categorized into hospitals, ambulatory surgical centers, clinics, home care settings, and others. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Adult Disposable Blood Pressure Cuffs |

| Pediatric Disposable Blood Pressure Cuffs |

| Neonatal Disposable Blood Pressure Cuffs |

| Others |

| Vinyl Disposable Blood Pressure Cuffs |

| Nylon Disposable Blood Pressure Cuffs |

| Thermoplastic Polyurethane Disposable Blood Pressure Cuffs |

| Others |

| Hospitals |

| Ambulatory Surgical Centers |

| Clinics |

| Home Care Settings |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Adult Disposable Blood Pressure Cuffs | |

| Pediatric Disposable Blood Pressure Cuffs | ||

| Neonatal Disposable Blood Pressure Cuffs | ||

| Others | ||

| By Material | Vinyl Disposable Blood Pressure Cuffs | |

| Nylon Disposable Blood Pressure Cuffs | ||

| Thermoplastic Polyurethane Disposable Blood Pressure Cuffs | ||

| Others | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Clinics | ||

| Home Care Settings | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the disposable blood pressure cuffs space in 2026?

The disposable blood pressure cuffs market size stands at USD 412.02 million in 2026 and is projected to reach USD 732.95 million by 2031 at a CAGR of 12.21%.

Why are hospitals shifting toward single-patient-use blood pressure cuffs?

Infection prevention requirements, contamination concerns on shared devices, and the operational burden of reprocessing are making disposable cuffs more attractive for many hospitals.

Which product type leads demand and which is growing the fastest?

Adult cuffs led with 39.63% share in 2025, while pediatric cuffs are projected to record the fastest growth at a 14.38% CAGR through 2031.

Which material segment shows the strongest momentum?

Vinyl remained the largest material segment with 46.43% share in 2025, but TPU is forecast to grow the fastest at a 15.55% CAGR because of biocompatibility and performance advantages.

Which end-user group is creating the biggest revenue base?

Hospitals are the largest end-user group, contributing 51.78% of total market value in 2025 because they combine high patient throughput with stricter infection-control protocols.

Which region is growing the fastest through 2031?

Asia-Pacific is projected to expand at a 14.67% CAGR through 2031, driven by hospital expansion, stronger local manufacturing depth, and rising adoption of compliant disposable consumables.

Page last updated on: