Direct-to-Device Satellite Connectivity Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

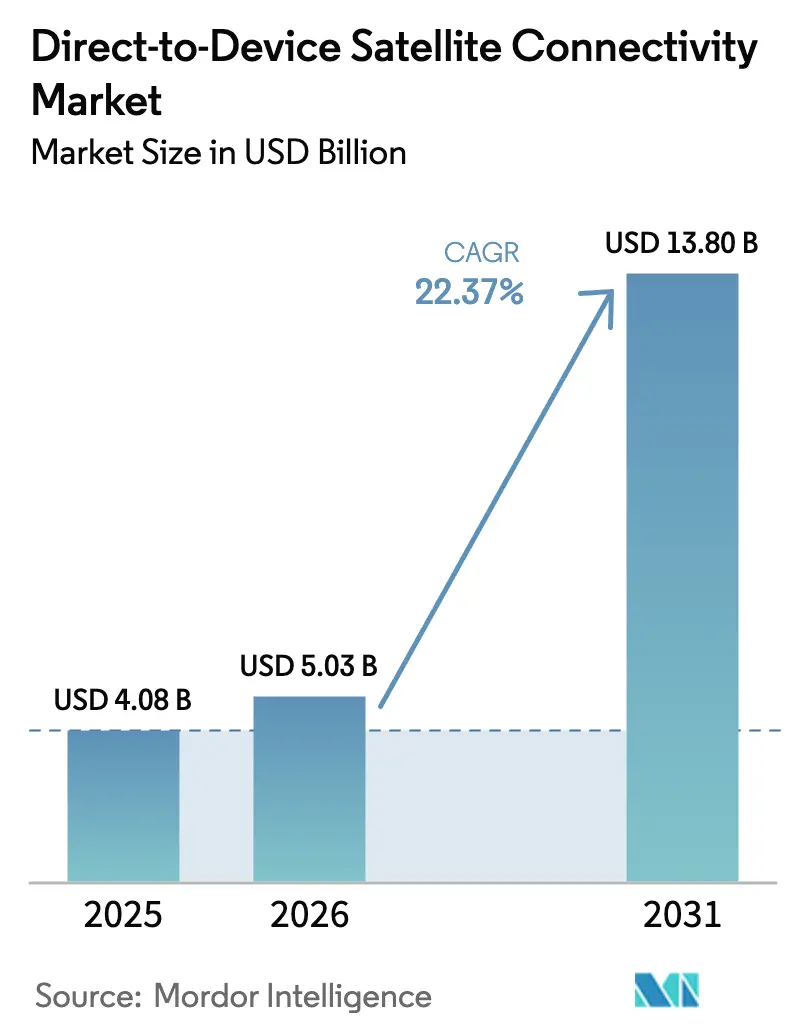

| Market Size (2026) | USD 5.03 Billion |

| Market Size (2031) | USD 13.80 Billion |

| Growth Rate (2026 - 2031) | 22.37% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Direct-to-Device Satellite Connectivity Market Analysis by Mordor Intelligence

The Direct-to-Device Satellite Connectivity Market size was valued at USD 4.08 billion in 2025 and is estimated to grow from USD 5.03 billion in 2026 to reach USD 13.80 billion by 2031, at a CAGR of 22.37% during the forecast period (2026-2031). Rapid adoption of 3GPP-compliant non-terrestrial network (NTN) chipsets by smartphone and wearable makers, falling small-satellite launch costs, and explicit rural-coverage mandates in major economies have moved satellite links from a niche safety feature to a mainstream layer in consumer devices. Mobile network operators in North America, Asia-Pacific, and Europe now bundle satellite text and voice in premium plans, accelerating mass-market awareness and compressing payback periods for low-Earth-orbit (LEO) constellations. Consumer willingness to pay for ubiquitous coverage is helped by monthly price points of USD 15-20, well below legacy satellite-phone tariffs, while enterprises view satellite IoT as an insurance policy against logistics disruptions. Competitive intensity is rising as vertically integrated LEO players leverage launch economies of scale and chipset vendors pursue horizontal partnerships that spread NTN integration costs across many handset brands.

Key Report Takeaways

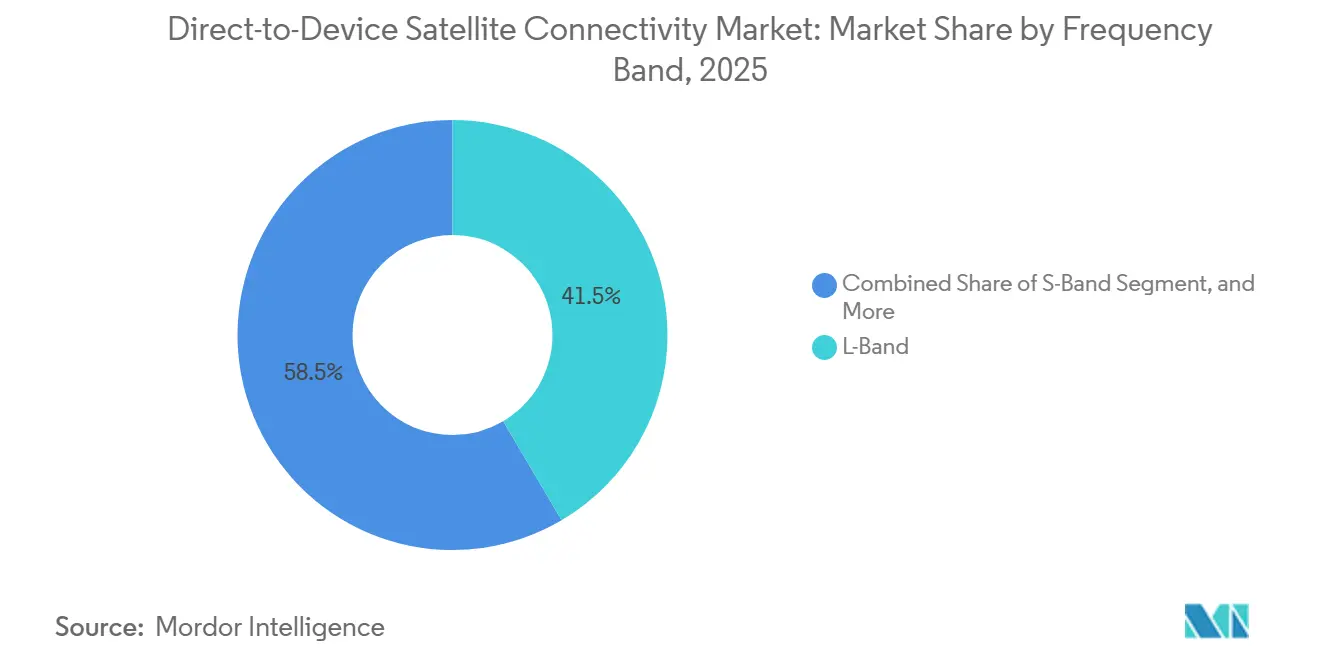

- By frequency band, L-band led with 41.53% of the direct-to-device satellite connectivity market share in 2025, while Ka-band is forecast to expand at a 25.61% CAGR through 2031.

- By device type, Smartphones accounted for 47.23% of 2025 revenue, whereas Wearables are advancing at a 25.82% CAGR to 2031.

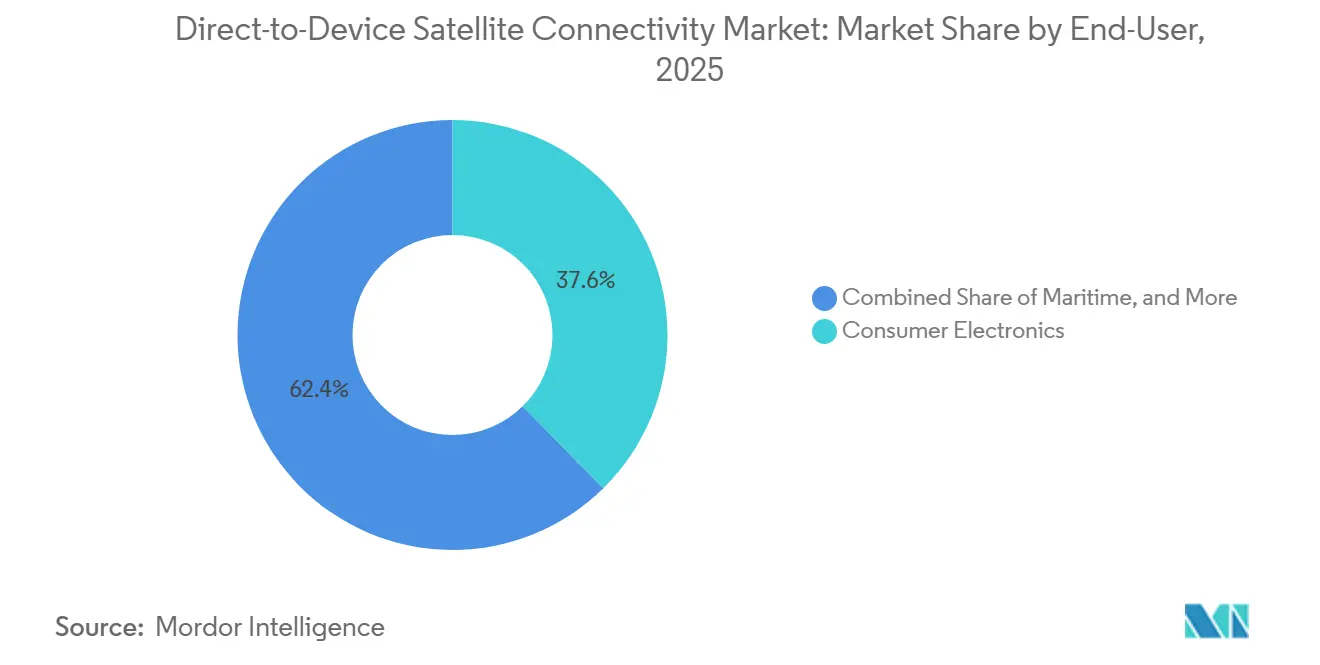

- By end-user industry, Consumer electronics captured 37.62% of 2025 spending, yet Government and Defense applications are projected to grow at a 27.11% CAGR during the same period.

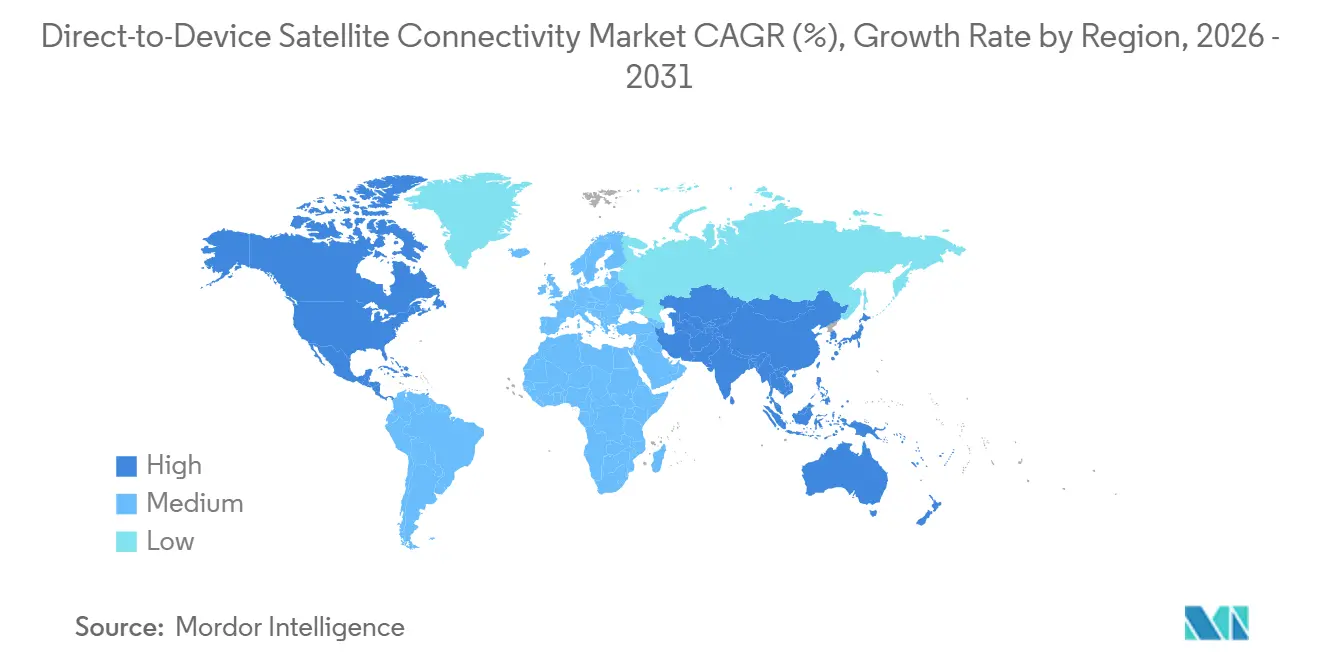

- By geography, North America dominated with a 39.22% revenue share in 2025, while Asia-Pacific is poised for the fastest growth at a 26.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Direct-to-Device Satellite Connectivity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of NTN-Compatible Smartphones | +6.2% | Global, with early concentration in North America, Europe, and Asia-Pacific premium segments | Short term (≤ 2 years) |

| Falling Launch Costs Due to Rideshare and Reusable Rockets | +4.8% | Global, particularly benefiting North America and Asia-Pacific constellation operators | Medium term (2-4 years) |

| 3GPP Release-17 NTN Standardization Uptake | +4.5% | Global, with faster adoption in regions with mature LTE and 5G infrastructure | Medium term (2-4 years) |

| National Rural-Coverage Mandates (US, India, AU, BR) | +3.9% | North America, Asia-Pacific, South America | Long term (≥ 4 years) |

| Demand from Unmanned Systems (UAVs and UGVs) | +2.7% | North America, Europe, Middle East (defense applications); Asia-Pacific (commercial agriculture) | Medium term (2-4 years) |

| Emerging Pay-As-You-Go IoT Micro-Data Plans | +2.1% | Global, with initial traction in North America and Europe logistics and agriculture sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of NTN-Compatible Smartphones

More than 150 million handsets shipped in 2025 with Release-17 NTN radios, making satellite connectivity a default feature in flagship and upper-midrange tiers. Apple, Samsung, Huawei, and multiple Android OEMs leveraged horizontal chipset platforms to avoid proprietary ground infrastructure, while the Federal Communications Commission’s Supplemental Coverage from Space rules removed regulatory ambiguity in the United States.[1]Federal Communications Commission, “Supplemental Coverage from Space Framework,” fcc.gov This scale effect spreads integration cost across a broader base, reduces retail price premiums, and primes users to expect seamless fallback when leaving terrestrial coverage.

Falling Launch Costs Due to Rideshare and Reusable Rockets

SpaceX regularly posts launch prices below USD 1 million for 200 kg payloads on Falcon 9 rideshare missions, a 60% reduction compared to typical expendable rockets in 2020.[2]Space Exploration Technologies Corp., “Falcon 9 Rideshare Pricing,” spacex.com Lower launch capex lets emerging operators such as Sateliot and Lynk Global orbit small batches, test in situ, then iterate, compressing constellation build-out timelines. Blue Origin’s New Glenn vehicle, expected to be online in 2026, will expand launch capacity, reinforcing a virtuous cycle of faster deployment and cheaper incremental capacity.

3GPP Release-17 NTN Standardization Uptake

Finalized waveforms, Doppler compensation, and timing-advance rules allow smartphones to roam between terrestrial and satellite cells without user intervention. Release-18, frozen in late 2024, added Ka-band procedures and power-saving uplink features, which AST SpaceMobile adopted in its BlueBird craft to support broadband speeds on unmodified phones. Standardization eases chipset development, grounds operator interoperability, and encourages regulators to align domestic rules with global procedures.

National Rural-Coverage Mandates

The United States RDOF allocates USD 20.4 billion over ten years for unserved areas, explicitly accepting LEO bids that meet latency and speed thresholds. India’s Digital India targets village-level connectivity by 2026 and favors administrative spectrum assignment for satellites, removing auction barriers. Australia and Brazil follow similar trajectories, ensuring a multi-year subsidy pipeline that underwrites revenue certainty for operators.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spectrum coexistence with terrestrial MNOs | -3.8% | Global, with acute friction in Europe and Asia-Pacific dense urban markets | Short term (≤ 2 years) |

| User-terminal power-budget constraints inside handsets | -2.9% | Global, affecting all battery-operated devices | Medium term (2-4 years) |

| Regulatory uncertainty on cross-border service rights | -2.3% | Europe, Asia-Pacific, Middle East and Africa | Medium term (2-4 years) |

| Limited revenue-generating use-cases beyond SOS/messaging | -2.1% | Global, particularly impacting consumer segment monetization | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Spectrum Coexistence with Terrestrial MNOs

Mobile operators argue that satellite downlinks spill into International Mobile Telecommunications bands, degrading urban uplinks. While U.S. rules cap unwanted emissions at -20 dBW/MHz, Europe has yet to harmonize thresholds, forcing country-by-country approvals that slow rollouts. Smaller satellite players lacking advanced beam-forming face costly redesigns, and lobbying by terrestrial incumbents seeks even stricter limits, injecting short-term deployment risk.

Limited Revenue-Generating Use-Cases Beyond SOS/Messaging

Emergency SOS is often bundled free, and entry-level text plans around USD 15-20 garner limited average revenue per user.[3]T-Mobile US Inc., “Direct-to-Cell Pricing Details,” t-mobile.com Broadband-class offerings from AST SpaceMobile promise higher pricing but remain in the pilot stage, while IoT customers demand sub-USD 5 plans, squeezing margins. Until a compelling mid-tier consumer app, such as ubiquitous video messaging, cloud gaming, or connected-car infotainment, achieves scale, investor appetite for additional constellation phases could soften.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Frequency Band: L-Band Incumbency Anchors Volume, Ka-Band Unlocks Throughput

L-band captured 41.53% of 2025 revenue within the direct-to-device satellite connectivity market, benefiting from decades-old Iridium and Globalstar assets that interoperate with existing chipsets and penetrate foliage and light structures. These characteristics underpin public-safety mandates and enterprise remote-worker kits, sustaining a sizable installed base. However, data-hungry use cases are drawing attention to Ku- and Ka-bands, where wider channels enable video conferencing and cloud access on handheld devices. 3GPP Release-18 standardized Ka-band NTN signaling, clearing a regulatory hurdle that had discouraged handset vendors from integrating antennas optimised for 27-40 GHz links.[4]3GPP, “Release 17 and 18 Specifications,” 3gpp.org

Ka-band shipments are forecast to grow at a 25.61% CAGR, and several operators are leasing existing geostationary capacity to seed service before the launch of dedicated LEO craft. This hybrid model accelerates go-to-market while preserving capital. Over the forecast, Ka-band’s share of the direct-to-device satellite connectivity market size is projected to close the gap with L-band as BlueBird, OneWeb-Eutelsat, and Viasat demonstrate multi-Mbps links on unmodified phones. Competitive advantage will hinge on beam-forming sophistication that keeps power budgets within handset limits and on coordinated spectrum rights that avoid urban interference, factors likely to consolidate supply around a handful of technically advanced players.

By Device Type: Wearables Carve a Safety-First Niche amid Smartphone Dominance

Smartphones accounted for 47.23% of 2025 device-type revenue in the direct-to-device satellite connectivity market, driven by Apple, Samsung, and Huawei embedding emergency texting in flagship models. The value proposition centers on seamless failover rather than standalone satellite pricing, thereby accelerating penetration in premium segments. Yet wearables are growing at a 25.82% CAGR as brands such as Garmin and Apple launch satellite-enabled smartwatches that operate independently of paired phones. For solo hikers, offshore workers, and first responders, the convenience of a wrist-mounted beacon with multi-day battery life outweighs the limited bandwidth.

By 2031, wearables are expected to represent a far larger share of the direct-to-device satellite connectivity market, fueled by falling module costs and the integration of health telemetry that must work beyond cellular footprints. Vehicle-mounted terminals, tablets, and rugged laptops lag because existing LTE and Wi-Fi solutions already satisfy most stationary broadband needs. Nevertheless, connected-vehicle platforms could emerge as the next inflection, once regulatory clearance for roof-mounted phased arrays on consumer cars mirrors the 2024 approval for commercial trucks. The competitive race, therefore, pivots on delivering satellite capability in form factors that maximize safety utility without compromising industrial design.

By End-User Industry: Defense Demand Accelerates, Consumer Volume Sustains Scale

Consumer electronics maintained the largest slice, 37.62% of 2025 revenue, proof that mass-market hardware underpins the direct-to-device satellite connectivity market share. Yet military and civil-government users are projected to log a 27.11% CAGR through 2031 as defense ministries seek resilient command links for unmanned aerial vehicles, remote sensors, and contested-spectrum operations. Commercial maritime and aviation segments adopt satellite messaging for distress compliance and cockpit data, reinforcing baseline demand even when consumer upgrades slow.

Government contracts typically span five to seven years, locking in predictable cash flows that de-risk constellation expansion. In agriculture, low-cost IoT tags transmit soil moisture and equipment health data, expanding the addressable node count without requiring high-bandwidth connections. Energy, utilities, and mining entities deploy satellite for pipeline monitoring and remote-site automation, monetizing uptime gains that dwarf subscription fees. As verticals diversify, operators can cross-subsidize rural smartphone traffic with higher-margin enterprise service-level agreements, sustaining growth while consumer pricing remains competitive.

Geography Analysis

North America retained 39.22% of 2025 revenue, anchored by FCC rule clarity and the USD 20.4 billion Rural Digital Opportunity Fund, which subsidizes satellite service in unserved areas. SpaceX and T-Mobile added over 3 million direct-to-cell subscribers by early 2026, validating consumer appetite and creating network effects that encourage handset vendors to ship NTN-ready devices. Canada leverages Telesat’s Lightspeed LEO network for Arctic and prairie communities, while Mexico eyes Starlink backhaul for federal connectivity programs. Venture capital density, reusable-rocket leadership, and dual-use military interest collectively sustain the region’s lead.

Asia-Pacific is forecast to post a 26.62% CAGR, propelled by China’s integration of Beidou messaging in Huawei and Xiaomi handsets, India’s administrative spectrum allocation that removes auction friction for OneWeb-Eutelsat and Jio-SES, and Japan’s KDDI-Starlink and Rakuten-AST SpaceMobile partnerships. Australia’s Regional Telecommunications Review endorsed satellite as the default option for its outback, and Telstra now bundles Starlink backhaul for remote towers. Dense urban markets such as South Korea use satellite mainly for maritime coverage and disaster resilience, but long-term demand from autonomous vehicles could expand indoor urban use cases.

Europe, South America, and Middle East, and Africa split the remainder. European rollouts await harmonized coexistence rules from CEPT, delaying broad commercial service despite Eutelsat OneWeb pilots with Vodafone and Orange. Brazil’s Anatel mandates coverage of the Amazon basin, positioning satellite as the only scalable solution for schools and clinics. In the Middle East and Africa, Yahsat and Thuraya serve government, energy, and NGO users; growth hinges on handset price declines and prepaid IoT plans that match local spending power.

Competitive Landscape

The direct-to-device satellite connectivity market remains moderately fragmented. SpaceX benefits from vertical integration across launch, satellite manufacturing, and the ground segment, enabling aggressive pricing that legacy satellite phone providers cannot match. AST SpaceMobile differentiates with 2,400 ft² phased-array satellites that promise 120 Mbps broadband to standard smartphones but require higher per-unit capex, introducing single-failure exposure AST.

Qualcomm and MediaTek pursue a horizontal strategy, embedding Iridium and Viasat links in reference chipsets that any handset maker can adopt, diffusing satellite capability across hundreds of models, and diluting individual carrier leverage.

Legacy operators Iridium, Globalstar, and Viasat leverage installed L-band and Ka-band assets while investing in LEO orbits to remain relevant. Specialist IoT networks, Skylo, Sateliot, Hiber, Kepler, target agriculture and logistics niches with sub-USD 5 plans, a segment large in node count but sensitive to terminal cost. Patent filings on beam-forming, regenerative payloads, and Doppler control hint at an intellectual-property moat for early movers. Regulation continues to shape rivalry; operators with seasoned spectrum-lobbying teams navigate cross-border approvals more quickly, creating first-mover advantages in complex jurisdictions.

Direct-to-Device Satellite Connectivity Industry Leaders

Space Exploration Technologies Corp.

AST SpaceMobile, Inc.

Lynk Global, Inc.

Iridium Communications Inc.

Globalstar, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: AST SpaceMobile scheduled 20 BlueBird launches via SpaceX rideshare, with AT&T advancing USD 400 million in capacity prepayments through 2028.

- February 2026: Apple prolonged free Emergency SOS via satellite to Dec 2027 and disclosed Globalstar plans for 50 additional satellites to cut latency.

- January 2026: SpaceX and T-Mobile upgraded direct-to-cell plans to include voice and limited data for USD 20 per month, surpassing 3 million subscribers.

Global Direct-to-Device Satellite Connectivity Market Report Scope

The Direct-to-Device Satellite Connectivity Market Report is Segmented by Frequency Band (L-Band, S-Band, Ku-Band, Ka-Band, and Others (UHF, X-Band)), Device Type (Smartphones, IoT Modules and Sensors, Wearables, Laptops and Tablets, and Connected Vehicles), End-User Industry (Consumer Electronics, Maritime, Aviation, Logistics and Transportation, Agriculture, Energy and Utilities, Government and Defense, and Other End-user Industry), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| L-Band |

| S-Band |

| Ku-Band |

| Ka-Band |

| Other Frequency Bands (UHF, X-Band) |

| Smartphones |

| IoT Modules and Sensors |

| Wearables |

| Laptops and Tablets |

| Connected Vehicles |

| Consumer Electronics |

| Maritime |

| Aviation |

| Logistics and Transportation |

| Agriculture |

| Energy and Utilities |

| Government and Defense |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Frequency Band | L-Band | ||

| S-Band | |||

| Ku-Band | |||

| Ka-Band | |||

| Other Frequency Bands (UHF, X-Band) | |||

| By Device Type | Smartphones | ||

| IoT Modules and Sensors | |||

| Wearables | |||

| Laptops and Tablets | |||

| Connected Vehicles | |||

| By End-User Industry | Consumer Electronics | ||

| Maritime | |||

| Aviation | |||

| Logistics and Transportation | |||

| Agriculture | |||

| Energy and Utilities | |||

| Government and Defense | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the direct-to-device satellite connectivity market in 2031?

The market is expected to reach USD 13.80 billion by 2031, reflecting an 22.37% CAGR from 2026 to 2031.

Which device category will grow the fastest through 2031?

Wearables are projected to grow at a 25.82% CAGR as safety-oriented smartwatches and trackers embed satellite beacons.

Why is Ka-band gaining traction despite L-band dominance?

Ka-band supports higher bandwidth, and Release-18 standardization enables smartphones to handle Doppler shifts, encouraging operators to launch video-capable services.

What role do rural-coverage mandates play in market growth?

Government subsidy programs in the United States, India, Australia, and Brazil earmark billions for unserved areas, directly underwriting satellite deployments.

Which region will add the most new users by 2031?

Asia-Pacific leads with a forecast 26.62% CAGR, propelled by China’s Beidou integration, India’s Digital India goals, and Japanese operator partnerships.

Page last updated on: