Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.22 Billion |

| Market Size (2031) | USD 13.91 Billion |

| Growth Rate (2026 - 2031) | 2.61% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market Analysis by Mordor Intelligence

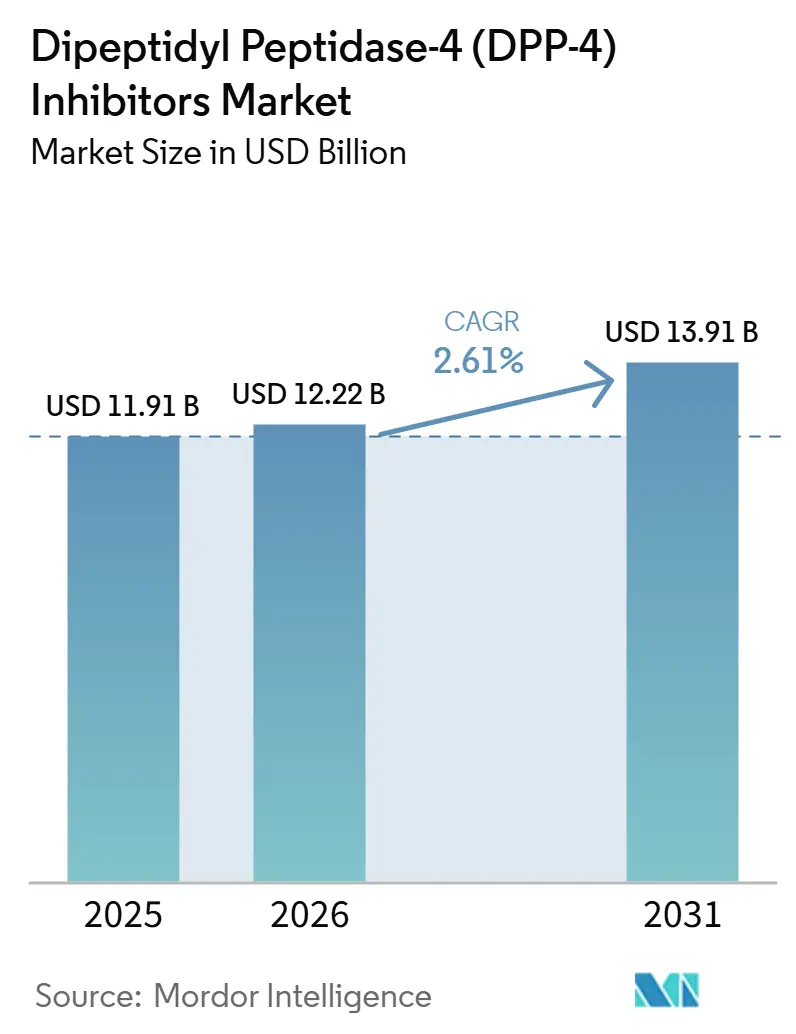

The Dipeptidyl Peptidase-4 Inhibitors Market size is projected to be USD 11.91 billion in 2025, USD 12.22 billion in 2026, and reach USD 13.91 billion by 2031, growing at a CAGR of 2.61% from 2026 to 2031.

The Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market continues to draw support from the rising global diabetes burden, with 589 million adults living with diabetes in 2024 and 251.7 million still undiagnosed, which keeps the long-term treatment pool broad across both developed and emerging care systems. The Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market also retains clinical relevance in older adults and patients with renal impairment, because these therapies remain well-suited to populations where low hypoglycemia risk and dosing flexibility matter in day-to-day prescribing. Oral dosing convenience, weight neutrality, and the growing use of combination therapy keep the Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market commercially relevant even as treatment algorithms continue to evolve. Growth remains moderate because the Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market is moving through a broader generic transition, with branded price pressure increasing as new generic entries expand access but compress unit revenue, especially in sitagliptin. Competitive strategy in the Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market is therefore shifting away from pure molecule differentiation and toward combination breadth, channel reach, reimbursement positioning, and disciplined pricing execution.

Key Report Takeaways

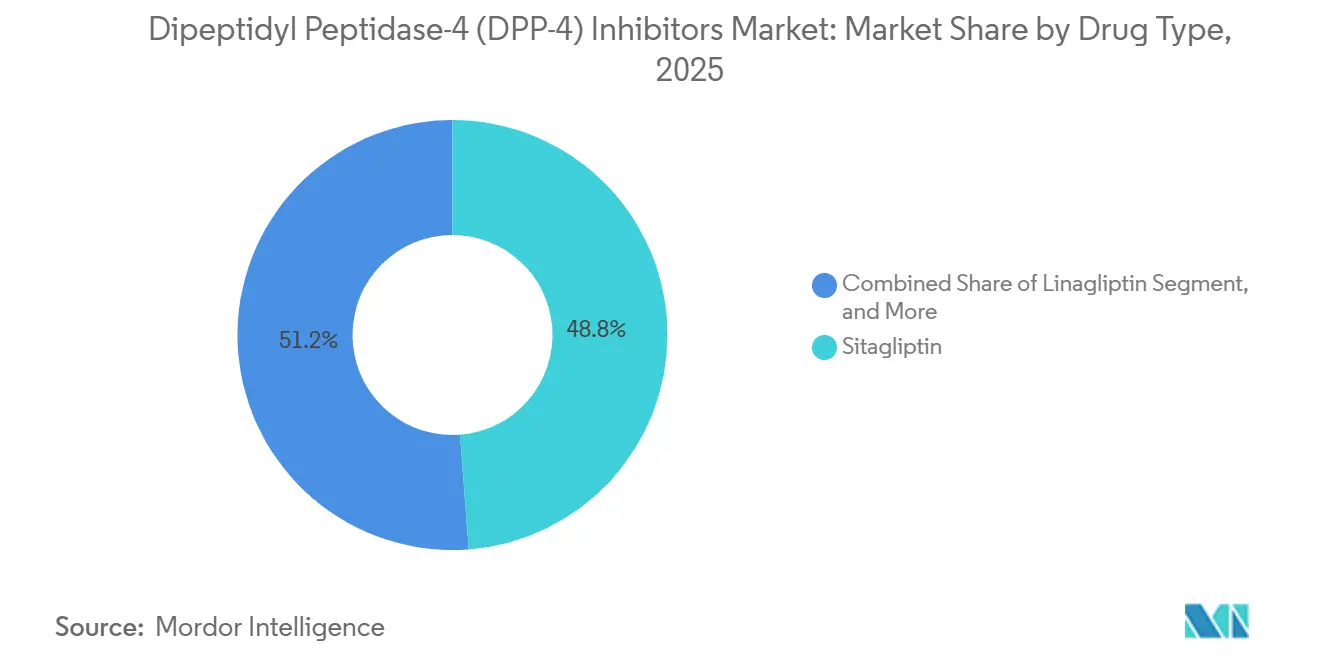

- By drug type, sitagliptin remained the dominant molecule with a market share of 48.83% in 2025 and is projected to expand at a 4.38% CAGR through 2031.

- By medication type, branded medication held 72.38% of the dipeptidyl peptidase-4 (DPP-4) inhibitors market share in 2025, while generic medication is forecast to expand at a 5.38% CAGR through 2031.

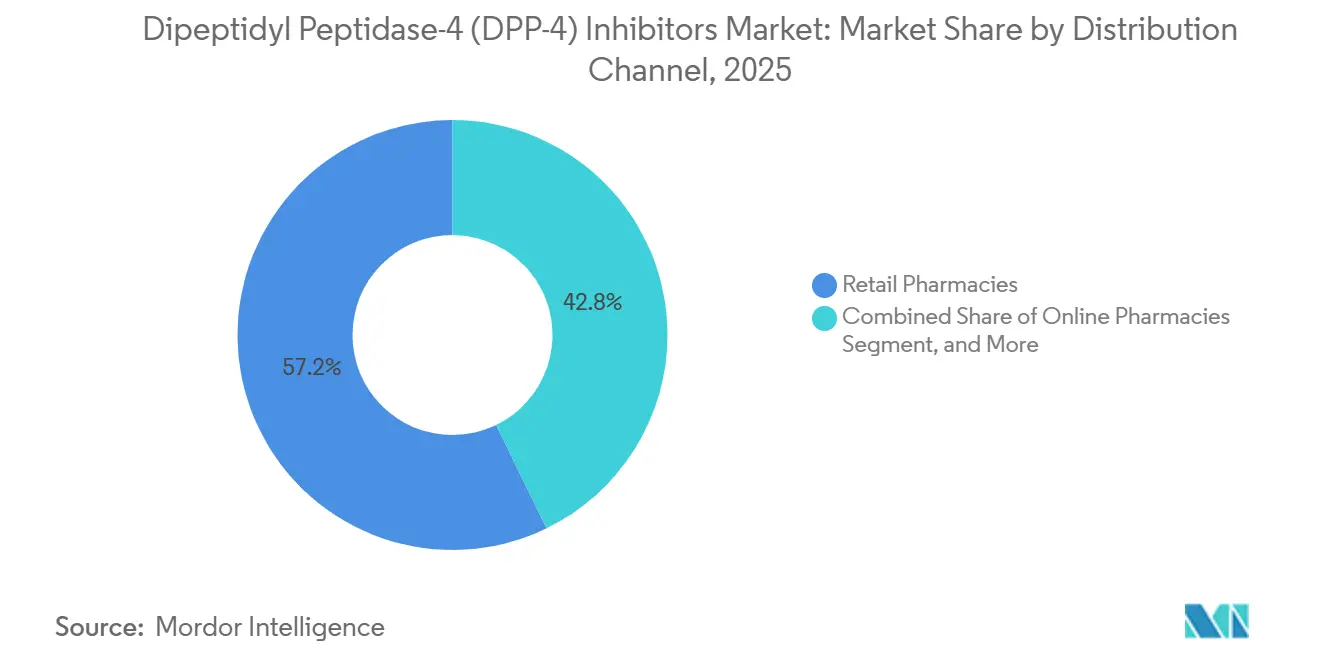

- By distribution channel, retail pharmacies accounted for 57.16% of the dipeptidyl peptidase-4 (DPP-4) inhibitors market size in 2025, while online pharmacies are projected to grow at a 6.02% CAGR through 2031.

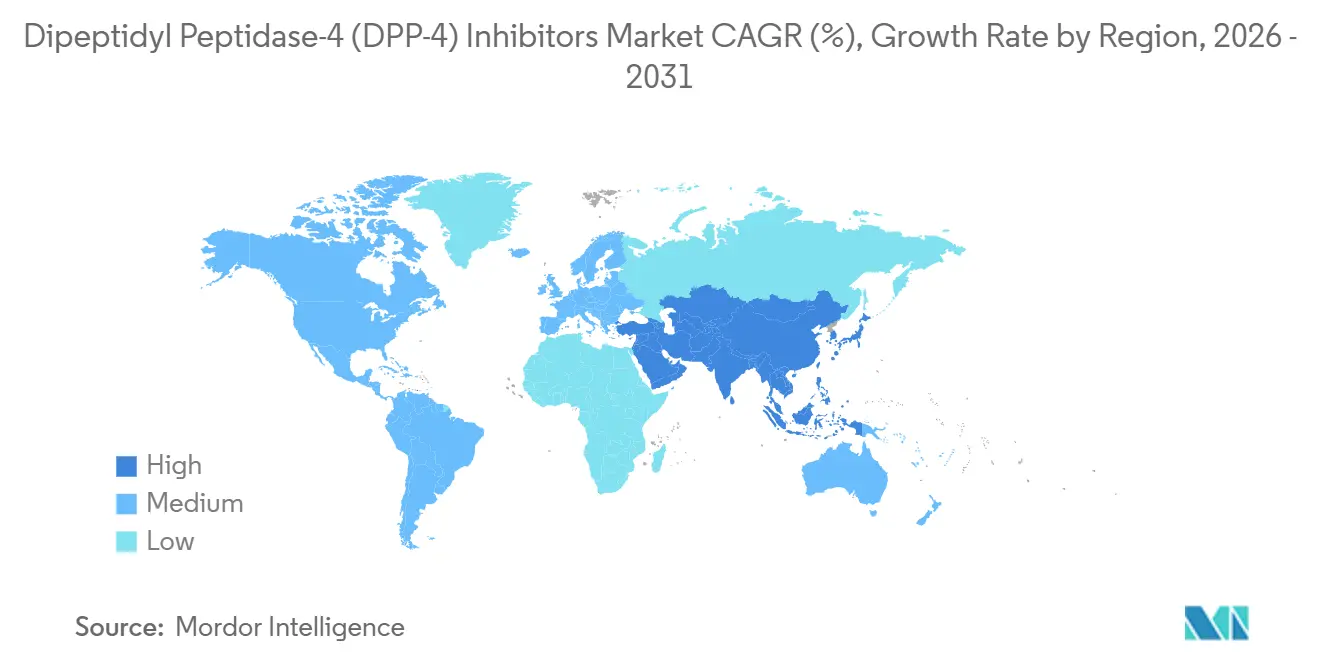

- By geography, North America held 39.63% of the dipeptidyl peptidase-4 (DPP-4) inhibitors market share in 2025, while Asia-Pacific is projected to record the fastest regional CAGR at 3.53% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Type 2 Diabetes Prevalence | +0.8% | Global, with peak intensity in APAC, MEA, and Latin America | Long term (≥ 4 years) |

| Preference for Low Hypoglycemia Oral Therapies | +0.25% | Global, concentrated in North America, Europe, and East Asia | Medium term (2-4 years) |

| Expansion of Fixed-Dose Combination Therapy Use | +0.35% | APAC core, including India and China, with spillover to MEA and Latin America | Medium term (2-4 years) |

| Patent-Lifecycle Defense and Brand Extension Activity | +0.15% | North America and EU | Short term (≤ 2 years) |

| Under-Served Elderly and Renal-Impaired Patient Pools | +0.40% | North America, Europe, and East Asia, including Japan and South Korea | Medium term (2-4 years) |

| Prescription Conversion from Injectable to Oral Maintenance Therapy | +0.30% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Type 2 Diabetes Prevalence

The dipeptidyl peptidase-4 (DPP-4) inhibitors market is supported by a diabetes burden that is still widening across most major care systems and income groups. The IDF Diabetes Atlas reported 589 million adults living with diabetes in 2024, and this total is projected to rise to 853 million by 2050, which keeps the addressable treatment base structurally large for oral glucose-lowering drugs. The same dataset showed that 251.7 million adults remained undiagnosed, which means future diagnosis and treatment expansion can continue to lift prescription volume in countries where screening access is improving. Urban diets, sedentary behavior, and longer life expectancy are pushing a larger share of this burden into densely populated parts of Asia, the Middle East, Africa, and Latin America, where oral therapy remains easier to scale than injectables. This broad patient flow gives the Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market a durable volume base, even when pricing pressure limits faster value growth.

Preference for Low Hypoglycemia Oral Therapies

The dipeptidyl peptidase-4 (DPP-4) inhibitors market benefits from steady physician demand for oral therapies that lower glucose without adding a high-severe hypoglycemia burden. A 2025 German claims analysis in older adults found that DPP-4 inhibitors lowered severe hypoglycemia risk by 49% in new users and by 69% in patients with severe renal insufficiency when compared with sulfonylureas.[1]K. Doni et al., “Real-World Harm Reduction of Metformin Plus DPP4 Inhibitors Versus Metformin Plus Sulfonylureas in Older Adults,” Drugs & Aging, springer.com This advantage matters in routine practice because many patients with type 2 diabetes are elderly, take several drugs, and are managed in primary care settings where treatment simplicity carries real weight. The dipeptidyl peptidase-4 (DPP-4) inhibitors market therefore, keeps a practical role in people who need oral treatment but cannot tolerate more aggressive regimens or greater hypoglycemia exposure. Low hypoglycemia risk also helps preserve adherence and refill continuity, which remains important in a therapy class used mainly for chronic maintenance.

Expansion of Fixed-Dose Combination Therapy Use

The dipeptidyl peptidase-4 (DPP-4) inhibitors market is increasingly supported by fixed-dose combinations that pair DPP-4 inhibitors with metformin and, in some cases, SGLT2 inhibitors. This matters because combination products allow mature molecules to stay relevant within broader oral treatment plans even when standalone use grows more slowly. The dipeptidyl peptidase-4 (DPP-4) inhibitors market also benefits when clinicians need to balance glycemic control, pill burden, tolerability, and renal considerations within a single regimen. ADA care standards continue to recognize DPP-4 inhibitors as weight-neutral options in the treatment pathway, which supports their fit as add-on agents in combination sequencing across varied patient profiles. As a result, fixed-dose combinations remain one of the clearest ways for the dipeptidyl peptidase-4 (DPP-4) inhibitors market to hold prescribing relevance while the broader diabetes treatment mix changes.

Patent-Lifecycle Defense and Brand Extension Activity

The dipeptidyl peptidase-4 (DPP-4) inhibitors market is also shaped by brand defense strategies that try to protect value after core molecules mature. Companies are leaning more heavily on line extensions, combination products, channel control, and selective patent defense to preserve branded positioning where prescriber loyalty is still meaningful. At the same time, new generic launches are forcing brand owners to reset expectations around price and reimbursement, especially in large prescription markets. Apotex launched generic sitagliptin tablets and sitagliptin with metformin tablets in the United States in June 2026, which shows how quickly branded pressure can intensify once entry barriers fall.[2]Apotex Corp., “Apotex Launches Sitagliptin Tablets and Sitagliptin and Metformin Hydrochloride Tablets, Eligible for 180-Day Shared Exclusivity,” Apotex Press Release, apotex.com This means the dipeptidyl peptidase-4 (DPP-4) inhibitors market is now less about preserving a single blockbuster and more about extending class value through portfolio design.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generic Erosion of Mature Brands | -0.10% | North America (primary), Europe, Japan | Short term (≤ 2 years) |

| Competition from SGLT2 Inhibitors and GLP-1 Receptor Agonists | -0.08% | Global, intensifying in North America and Europe | Long term (≥ 4 years) |

| Pricing Pressure from Payers and Formularies | -0.09% | North America & EU, spill-over to APAC reimbursement markets | Medium term (2–4 years) |

| Limited Differentiation Versus Newer Diabetes Classes | -0.07% | Global, most acute in North America and Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Generic Erosion of Mature Brands

The clearest value restraint on the dipeptidyl peptidase-4 (DPP-4) inhibitors market is the steady erosion of mature brand pricing once generic alternatives reach broad commercial availability. This shift expands patient access and prescription volume, but it also reduces revenue per prescription and caps headline value growth for the class. The June 2026 Apotex launch of generic sitagliptin and generic sitagliptin with metformin in the United States is a direct example of how fast branded pressure can build when large molecules enter the generic phase. Health Canada also authorized NRA-Sitagliptin Tablets, which support the broader pattern of national generic rollout across regulated markets.[3]Health Canada, “Product Monograph, NRA-Sitagliptin Tablets,” Health Canada Product Monograph, pdf.hres.ca As more formularies prioritize low-cost substitution, the Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market will likely see volume resilience but a tighter ceiling on branded value capture.

Competition from SGLT2 Inhibitors and GLP-1 Receptor Agonists

The dipeptidyl peptidase-4 (DPP-4) inhibitors market also faces growing competition from SGLT2 inhibitors and GLP-1 receptor agonists, which are gaining strong clinical attention in second-line and combination therapy. These competing classes have narrowed the space for standalone DPP-4 prescribing in patients where weight loss or broader cardiorenal outcomes carry more importance. A 2025 Delphi consensus on oral semaglutide showed that oral alternatives are increasingly part of treatment switching discussions, which means the oral convenience advantage of DPP-4 inhibitors is no longer unique. Even so, the Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market remains relevant where gastrointestinal tolerability, renal fit, and low hypoglycemia risk still shape prescribing behavior. The result is a class that is losing some standalone positioning but is still defending a narrower and clinically defined role.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Sitagliptin Anchors Volume While FDC Strategies Reshape Class Competition

Sitagliptin is the leading molecule in the dipeptidyl peptidase-4 (DPP-4) inhibitors market and is projected to grow at a 4.38% CAGR through 2031, which keeps it ahead of the overall class pace. This profile reflects an unusual mix of strong prescription relevance and weaker branded pricing power, because growth is increasingly volume-led rather than premium-led. The dipeptidyl peptidase-4 (DPP-4) inhibitors market continues to revolve around sitagliptin because the molecule remains familiar to physicians, adaptable in combinations, and easier to scale once generic access broadens. That makes sitagliptin important not only as a standalone oral therapy but also as a foundation for broader fixed-dose treatment strategies. The molecule, therefore, anchors class continuity at a time when several other parts of the treatment pathway are changing quickly.

The rest of the drug type landscape is more differentiated by local patent status, formulary access, and regional prescribing habits. Saxagliptin, linagliptin, alogliptin, and vildagliptin still hold specific positions in the dipeptidyl peptidase-4 (DPP-4) inhibitors market, but each one depends more heavily on country-level dynamics than on global growth momentum. Linagliptin remains especially relevant in patients where renal handling shapes treatment choice, while vildagliptin continues to benefit from established familiarity in selected European and Asian settings. The other drug types category is also becoming more visible in parts of Asia, where domestic molecule development is expanding the choice set and widening price-based competition. Across this segment, the dipeptidyl peptidase-4 (DPP-4) inhibitors industry is moving from pure molecule competition toward portfolio competition built on combinations, reimbursement fit, and sustained chronic-care access.

By Medication Type: Generics Gain Ground as Brand Premium Erodes Across Markets

Branded medication held 72.38% of the dipeptidyl peptidase-4 (DPP-4) inhibitors market size in 2025, while generic medication is projected to grow at a 5.38% CAGR through 2031. This split shows that brands still carried most revenue in 2025, even though the faster momentum is now clearly in lower-cost generic supply. The dipeptidyl peptidase-4 (DPP-4) inhibitors market is therefore shifting into a structure where value leadership and prescription growth no longer sit in the same tier. Brands remain more resilient in markets with later generic timing, stronger prescriber loyalty, or a slower pace of substitution. Generics, however, are set to absorb most incremental prescription volume because they match payer priorities and widen access in cost-sensitive care environments.

This divide is already visible in how companies are organizing their commercial approach. The dipeptidyl peptidase-4 (DPP-4) inhibitors market now rewards firms that can manage both branded positioning and fast generic execution across multiple channels. Apotex’s 2026 United States launch illustrates how generic manufacturers are moving directly into core class molecules once regulatory pathways are clear. Health Canada authorization of NRA-Sitagliptin Tablets shows that this migration is not limited to the United States and is spreading through other regulated markets as well. In practice, the Dipeptidyl Peptidase-4 (DPP-4) Inhibitors industry is becoming less about defending brand exclusivity and more about capturing long-duration refill volume at lower price points.

By Distribution Channel: Online Pharmacies Disrupt a Retail-Dominated Chronic-Care Channel

Retail pharmacies held 57.16% of the dipeptidyl peptidase-4 (DPP-4) inhibitors market size in 2025, while online pharmacies are expected to expand at a 6.02% CAGR through 2031. Retail kept the lead because chronic diabetes treatment still relies heavily on familiar neighborhood dispensing, insurer-linked networks, and repeat prescription habits. Hospital pharmacies also remain important in the dipeptidyl peptidase-4 (DPP-4) inhibitors market because many patients first receive therapy through institutional care pathways before shifting to long-term refill channels. Even so, online platforms are taking a larger share of the refill cycle as home delivery becomes easier to integrate into chronic disease management. This is especially relevant in a class where medication use is usually continuous, and adherence depends on reliable monthly access.

The online shift is not uniform, but it is becoming strategically important across major geographies. In the dipeptidyl peptidase-4 (DPP-4) inhibitors market, digital pharmacy models are improving access in dense urban regions as well as in smaller cities where physical pharmacy networks are thinner. They also reinforce generic uptake because price comparison is easier online, and patients can more readily switch toward lower-cost options once prescriptions are stable. Retail pharmacies will still remain central, but their economics are tightening as substitution pressure grows and payer controls become more active. This makes channel execution a larger part of competitive performance in the dipeptidyl peptidase-4 (DPP-4) inhibitors market than it was when branded dispensing dominated the class.

Geography Analysis

North America held 39.63% of the dipeptidyl peptidase-4 (DPP-4) inhibitors market share in 2025, which kept it as the leading regional contributor to class revenue. The region benefits from a large insured patient base, established chronic-care pathways, and long-standing physician familiarity with oral diabetes treatment sequencing. The dipeptidyl peptidase-4 (DPP-4) inhibitors market in North America is now entering a more price-sensitive phase because generic sitagliptin launches are widening access while also reducing branded pricing power. Apotex launched generic sitagliptin tablets and sitagliptin with metformin tablets in the United States in June 2026, which reinforces the speed of this transition. Even with that pressure, the region should remain commercially important because older patients and those with renal considerations continue to support steady prescribing.

Europe remains one of the most advanced regions in branded-to-generic migration within the dipeptidyl peptidase-4 (DPP-4) inhibitors market. The United Kingdom has already shown clear formulary movement toward generic sitagliptin, with the South Yorkshire Integrated Care Board designating generic sitagliptin as the first-line preferred gliptin for eligible patients and new starts in its 2025 position statement. Germany and the United Kingdom are likely to remain among the clearest examples of cost-led adoption, while France, Italy, and Spain still offer support from aging populations and reimbursement-backed oral care pathways. Central and Eastern Europe provide a smaller base today, but they still represent a meaningful expansion area for the Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market as access standards improve.

Asia-Pacific is projected to record the fastest regional growth at 3.53% CAGR through 2031, which makes it the most important expansion geography for the dipeptidyl peptidase-4 (DPP-4) inhibitors market over the forecast period. The regional story is broad rather than uniform, because Japan remains more brand-protected, China is becoming more crowded with domestic development, and India is seeing strong demand for combination-led oral treatment. Population scale, rising diagnoses, and improving reimbursement are lifting prescription opportunities across several countries at once. This gives the dipeptidyl peptidase-4 (DPP-4) inhibitors market a larger volume runway in Asia-Pacific than in the more mature Western regions, even if unit pricing remains lower. The Middle East and Africa, and South America are still earlier-stage contributors, but both regions can add incremental demand as diagnosis rates, reimbursement coverage, and pharmacy access continue to improve.

Competitive Landscape

The dipeptidyl peptidase-4 (DPP-4) inhibitors market remains moderately fragmented, with major branded positions still concentrated around a small group of long-established innovators and a widening generic tier that is changing the class economics. Merck, Boehringer Ingelheim and Eli Lilly, AstraZeneca, and Novartis continue to shape the branded side because they built the most recognized molecules, physician familiarity, and clinical histories in the class. That said, the Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market is no longer driven mainly by blockbuster exclusivity. It is now driven by who can hold a place in treatment combinations, protect formulary access, and sustain refill flow through both branded and generic channels. This keeps competition active even though the class is maturing.

Innovators are responding by shifting from single-molecule defense to broader portfolio management. One clear move in the Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market is the continued push toward fixed-dose combinations, because combinations help preserve relevance after standalone growth slows. Another move is continued brand protection in markets where legal and reimbursement conditions still support a longer branded window. Generic challengers are taking the opposite path and are pushing rapid entry into core molecules, with Apotex’s June 2026 sitagliptin launch in the United States serving as a visible example of how quickly generic competition can reset the pricing environment. This combination of portfolio defense and fast generic rollout is shaping the next phase of the dipeptidyl peptidase-4 (DPP-4) inhibitors market.

Regional players are also becoming more important than before. In the dipeptidyl peptidase-4 (DPP-4) inhibitors market, companies such as Sun Pharmaceutical Industries, Zydus Lifesciences, Glenmark, Dr. Reddy’s Laboratories, and several China-based manufacturers are building presence through generics, local combinations, and region-specific portfolios. Their growth matters because they are competing on affordability, market access, and adaptation to local prescribing habits rather than on global brand legacy alone. Overall, the dipeptidyl peptidase-4 (DPP-4) inhibitors market is moving toward a competitive model where payer policy, combination design, and chronic-care distribution matter as much as clinical identity.

Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Industry Leaders

AstraZeneca PLC

Boehringer Ingelheim International GmbH

Eli Lilly and Company

Merck & Co., Inc.

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Apotex Corp. launched generic sitagliptin tablets (25 mg, 50 mg, 100 mg) and generic sitagliptin-metformin hydrochloride tablets in the US, both AB-rated to Januvia and Janumet respectively, with 180-day shared exclusivity. This launch, following Sandoz's May 2026 entry, marked the full US genericization of the world's largest standalone DPP-4 inhibitor franchise, accelerating branded revenue compression for Merck's sitagliptin portfolio.

- April 2026: Japan's Intellectual Property High Court upheld three Boehringer Ingelheim patents covering linagliptin (Tradjenta), rejecting invalidation challenges from generics maker Nipro and clarifying that drug patents can remain valid without direct experimental data for every claimed therapeutic use. The ruling maintains Boehringer Ingelheim's linagliptin exclusivity window in Japan, one of the class's most valuable branded markets.

Global Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market Report Scope

The Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market comprises pharmaceutical products that inhibit the dipeptidyl peptidase-4 (DPP-4) enzyme to improve glycemic control in patients with type 2 diabetes mellitus. These drugs work by preventing the breakdown of incretin hormones, thereby increasing insulin secretion and reducing glucagon release in a glucose-dependent manner. The market includes both branded and generic DPP-4 inhibitor medications distributed through various healthcare channels for the management of type 2 diabetes.

The Dipeptidyl Peptidase-4 (DPP-4) Inhibitors Market is segmented by drug type, medication type, distribution channel, and geography. Based on drug type, the market is segmented into sitagliptin, saxagliptin, linagliptin, alogliptin, vildagliptin, and other drug types. By medication type, the market is categorized into branded medication and generic medication. Based on distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. Geographically, the market is analyzed across North America (United States, Canada, and Mexico), Europe (Germany, the United Kingdom, France, Italy, Spain, and the Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, and the Rest of Asia-Pacific), Middle East & Africa (GCC, South Africa, and the Rest of Middle East & Africa), and South America (Brazil, Argentina, and the Rest of South America). The report provides market size and forecasts in terms of value (USD) for all the above segments.

| Sitagliptin |

| Saxagliptin |

| Linagliptin |

| Alogliptin |

| Vildagliptin |

| Other Drug Types |

| Branded Medication |

| Generic Medication |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Type | Sitagliptin | |

| Saxagliptin | ||

| Linagliptin | ||

| Alogliptin | ||

| Vildagliptin | ||

| Other Drug Types | ||

| By Medication Type | Branded Medication | |

| Generic Medication | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of the dipeptidyl peptidase-4 (DPP-4) inhibitors market by 2031?

The dipeptidyl peptidase-4 (DPP-4) inhibitors market is forecast to reach USD 13.91 billion by 2031, rising from USD 11.91 billion in 2025 at a 2.61% CAGR from 2026 to 2031.

Why do DPP-4 inhibitors still matter in diabetes care despite newer drug classes?

They remain useful because they are oral, weight neutral, and well suited to older adults and patients with renal impairment, where low hypoglycemia risk and dosing flexibility continue to matter.

Which region is growing fastest for DPP-4 inhibitors?

Asia-Pacific is projected to record the fastest regional growth at 3.53% CAGR through 2031, supported by expanding diagnosis, reimbursement, and combination therapy use.

Which distribution channel leads DPP-4 inhibitor sales today?

Retail pharmacies led in 2025 with 57.16% share, but online pharmacies are expanding faster at a 6.02% CAGR as chronic refill behavior shifts toward home delivery.

Are generics changing the competitive structure of this space?

Yes. Branded medication held 72.38% share in 2025, but generic medication is forecast to grow faster at 5.38% CAGR, which is reshaping pricing and revenue mix across regions.

Page last updated on: