Dimethyl Carbonate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

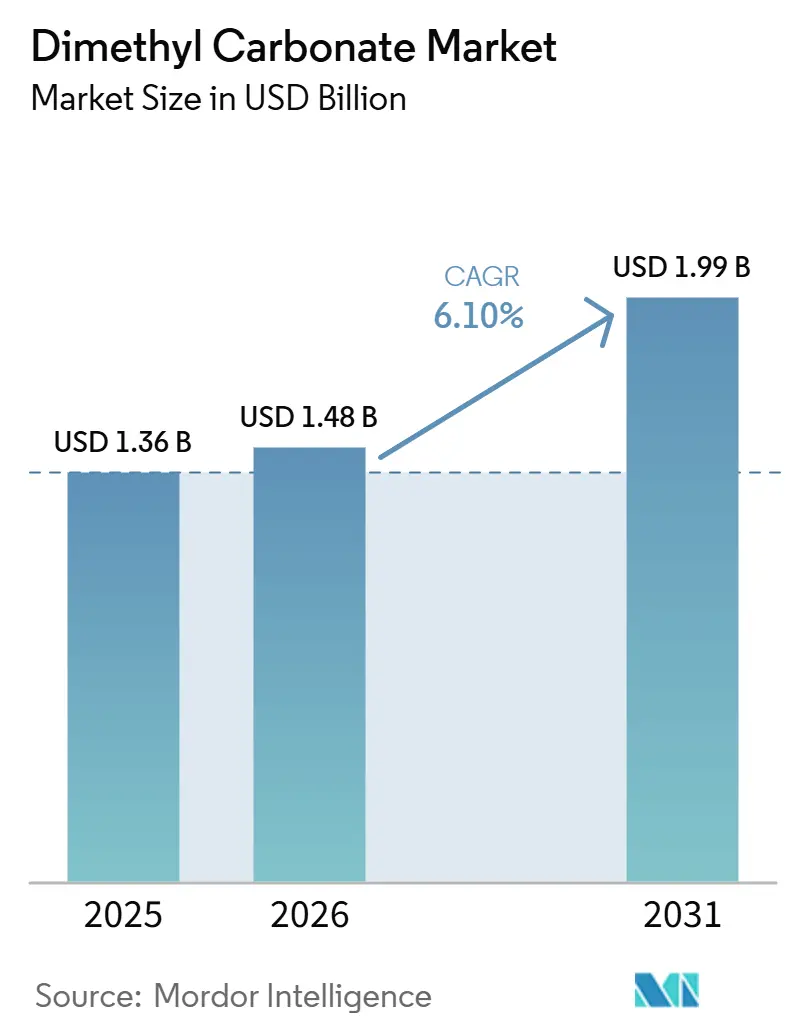

| Market Size (2026) | USD 1.48 Billion |

| Market Size (2031) | USD 1.99 Billion |

| Growth Rate (2026 - 2031) | 6.10% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dimethyl Carbonate Market Analysis by Mordor Intelligence

The Dimethyl Carbonate Market size is projected to expand from USD 1.36 billion in 2025 and USD 1.48 billion in 2026 to USD 1.99 billion by 2031, and is expected to register a CAGR of 6.10% between 2026 to 2031. The dimethyl carbonate market is driven by steady demand from polycarbonate production and faster growth in battery electrolyte applications, which is shifting the value mix toward higher-purity grades. The market is also experiencing a growing divide between commodity and premium supply, as industrial-grade material remains volume-heavy while battery and pharmaceutical grades require stricter quality standards and command better pricing. Asia-Pacific continues to define the market's direction through its large chemical base, scale in battery manufacturing, and concentration of downstream buyers in China, South Korea, and Japan. Competitive dynamics are moving toward feedstock integration, long-term supply arrangements, and process quality upgrades, particularly in premium battery applications. Margin conditions remain exposed to methanol and CO2 price fluctuations, placing suppliers with purification capacity and regional proximity to battery customers in a better position to defend profitability.

Key Report Takeaways

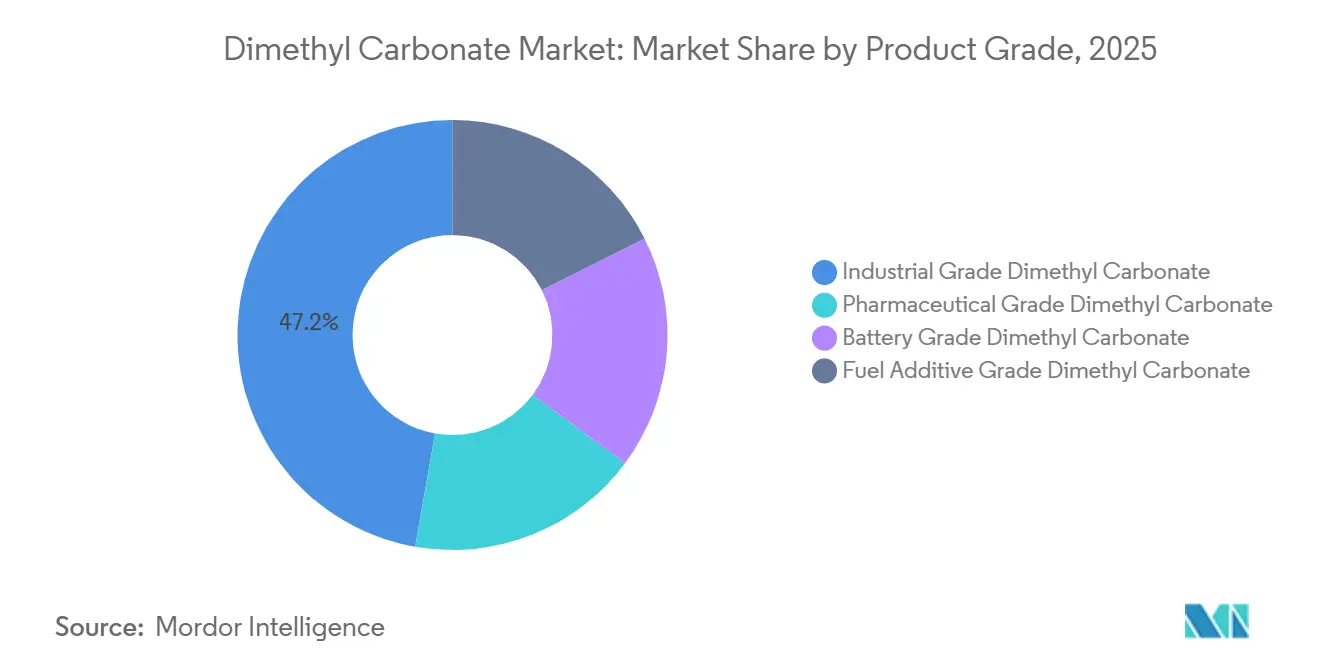

- By product grade, industrial grade led with 47.22% share in 2025, while battery grade is forecast to expand at 7.91% CAGR through 2031.

- By application, polycarbonate synthesis accounted for 35.41% of the market in 2025, while battery electrolyte is projected to grow at an 8.32% CAGR through 2031.

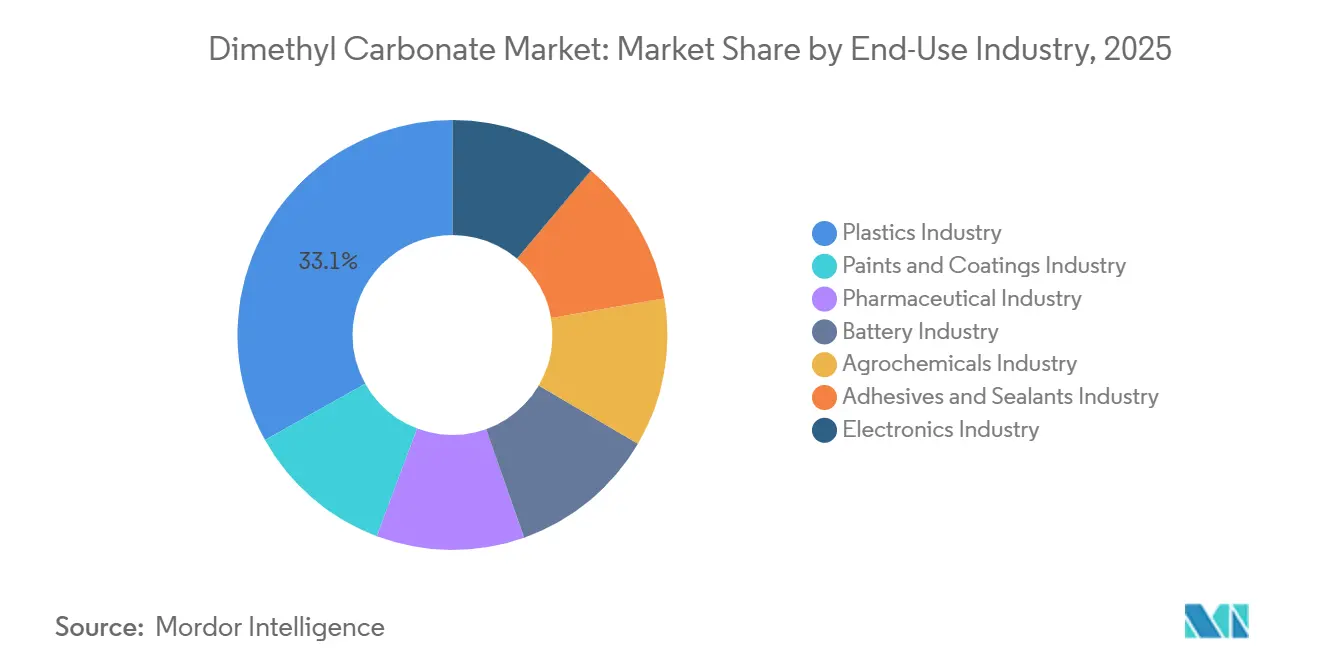

- By end-use industry, plastics accounted for a 33.12% share in 2025, while the battery industry is expected to grow at an 8.54% CAGR through 2031.

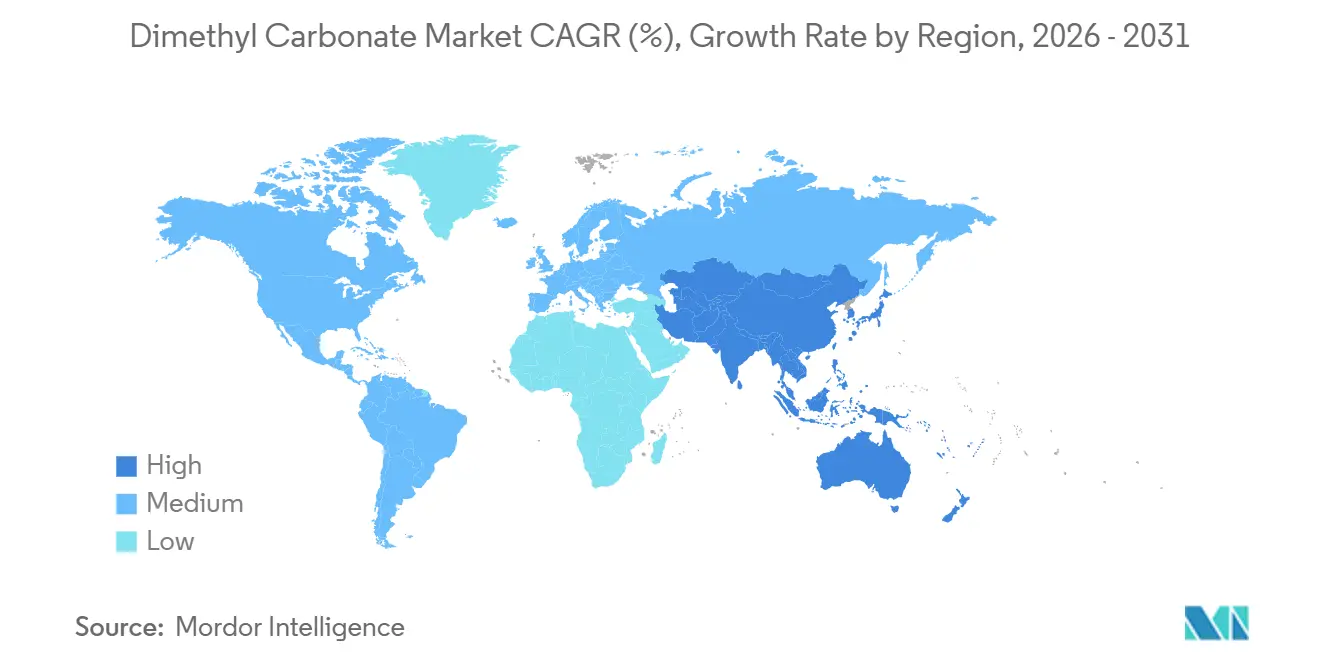

- By geography, Asia-Pacific held 59.37% share in 2025 and is also projected to record the fastest regional growth at 6.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dimethyl Carbonate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for high-purity dimethyl carbonate in lithium-ion battery electrolytes | +1.5% | Global, concentrated in China, South Korea, and Japan, with growing pull from North America | Medium term (2-4 years) |

| Expanding use in polycarbonate synthesis, replacing phosgene-based routes | +1.2% | APAC core, especially China and South Korea, with spillover to Europe and North America | Medium term (2-4 years) |

| Shift toward safer, low-toxicity solvents across industrial and laboratory applications | +0.8% | Global, with the strongest regulatory traction in Europe and North America | Long term (≥ 4 years) |

| Growth in pharmaceutical manufacturing and Green Active Pharmaceutical Ingredient (API) Synthesis | +0.5% | Global, with early adoption in Europe, North America, and India | Long term (≥ 4 years) |

| Expansion of the lithium-ion battery base from EV and energy storage demand | +1.8% | Global, with China leading and Europe and North America following | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for High-Purity Dimethyl Carbonate in Battery Electrolytes

Battery-grade dimethyl carbonate requires purity of 99.99% or above, which keeps its realized pricing well above industrial-grade material. In the dimethyl carbonate market, this premium is significant because revenue growth is being driven by product mix improvement, not only by higher volumes. Global battery demand for EV and storage applications reached 1 TWh in 2024, with EV batteries accounting for more than 950 GWh, up 25% from 2023. Battery demand is projected to exceed 3 TWh by 2030, supporting a firm long-term outlook for solvent procurement. In Europe, chemistry mix remains an important consideration because Lithium Iron Phosphate (LFP) batteries use less dimethyl carbonate per unit than NMC cells, meaning rising capacity does not translate into a proportional increase in solvent demand. The dimethyl carbonate market therefore favors suppliers that secure long-term battery contracts and can consistently meet purity requirements, logistics control, and contamination risk standards.

Expanding Use in Polycarbonate Synthesis Replacing Phosgene-Based Routes

Dimethyl carbonate supports a non-phosgene route to polycarbonate production, making it relevant where chemical handling standards are tightening. In the dimethyl carbonate market, this application keeps industrial-grade demand stable even as battery applications grow faster in value terms. A 2025 pilot study validated a continuous CO2-to-dimethyl carbonate (DMC)-to-diphenyl carbonate process over a 150-hour run, achieving an 85.9% overall DMC yield and polymer-grade polycarbonate quality comparable to conventional material. China, South Korea, and Japan remain the largest polycarbonate production base, maintaining a strong regional demand floor for this application. The same upstream process can support both industrial and high-purity output, giving producers flexibility to adjust purification focus as downstream conditions change. The dimethyl carbonate market benefits from this dual-track model as it allows suppliers to balance mature plastics demand with faster battery-related growth.

Shift Toward Safer, Low-Toxicity Solvents Across Industries

The shift toward safer solvents is expanding the addressable base for dimethyl carbonate in pharmaceuticals, analytical chemistry, and fine chemicals. In the dimethyl carbonate market, this trend is relevant because regulatory preference can support adoption even when volume gains start from a smaller base. A 2025 review in Green Chemistry noted that organic carbonates are becoming a fast-growing class of green reaction media across industrial organic synthesis. A separate 2025 study showed that dimethyl carbonate can replace acetonitrile in reversed-phase liquid chromatography for peptide purification without reducing product quality, offering a viable path for facilities seeking to lower solvent risk while maintaining process continuity in sensitive purification work. The dimethyl carbonate market also benefits from fuel additive demand, where restrictions on methyl tert-butyl ether (MTBE) in some jurisdictions sustain interest in alternative oxygenates, although this remains a smaller factor compared to batteries or polycarbonate.

Growth in pharmaceutical manufacturing and green Active Pharmaceutical Ingredient (API) synthesis

Pharmaceutical use of dimethyl carbonate centers on its role as a methylating agent and a carbonylating reagent in the formation of carbamates and carbonates. This segment of the dimethyl carbonate market is smaller by volume but remains relevant due to high-quality standards and firm pricing. Pharmaceutical-grade material must meet United States Pharmacopeia (USP) and EP-aligned purity requirements of 99.995% or higher, along with tight residual solvent and endotoxin controls, which raise entry barriers for new suppliers and limit the number of producers that can serve high-value, regulated applications. India and China are becoming increasingly relevant demand centers as generic and biosimilar manufacturing expands under stricter process requirements. The dimethyl carbonate market is therefore gaining an additional quality-driven growth segment that operates independently of the volume cycles associated with commodity industrial applications.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High dependence on methanol and CO2 feedstock prices | -1.2% | Global, with higher sensitivity in the Asia-Pacific, where feedstock import dependence is elevated | Medium term (2-4 years) |

| Handling and purification challenges for high-purity battery and pharmaceutical grades | -0.9% | Global, most acute in emerging markets without advanced purification and quality control infrastructure | Long term (≥ 4 years) |

| Competition from alternative carbonate and organic solvents | -0.8% | Europe and North America, where propylene carbonate and ethyl methyl carbonate hold comparable functional positions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Dependence on Methanol and CO2 Feedstock Prices

Methanol and CO2 are the primary feedstocks in the main synthesis routes used across the dimethyl carbonate market, making production economics closely tied to energy cycles and procurement conditions that suppliers cannot fully control. Methanol costs rose 35% to 40% in the first quarter of 2026, and dimethyl carbonate spot prices in Asia increased by 25% to 30% during the same period. This cost increase pushed some commodity buyers toward a more cautious procurement stance through the third quarter of 2026. The dimethyl carbonate market also faces CO2 sourcing risk, as green production routes rely on nearby industrial flue gas streams, and disruptions in adjacent sectors can interrupt planned output.

Handling and Purification Challenges for High-Purity Grades

High-purity production requires multistage distillation, advanced drying, and strict quality control to remove trace methanol, moisture, and acidic impurities. In the dimethyl carbonate market, these steps act as a capacity filter, as not every industrial-grade producer can upgrade to battery or pharmaceutical quality. The capital requirements are significant, concentrating premium output among larger and more integrated suppliers. Storage and transport add further complexity, as dimethyl carbonate has a relatively high vapor pressure and requires tighter containment practices than standard bulk commodity handling. These logistics demands raise export costs for emerging market suppliers seeking to enter battery supply chains. As a result, the dimethyl carbonate market faces a constraint that limits near-term expansion, and the same barrier supports stronger pricing for producers that meet certification and purity thresholds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Industrial Grade Holds Volume, While Battery Grade Lifts Value

Industrial grade held 47.22% of the dimethyl carbonate market in 2025, reflecting its established use in polycarbonate synthesis and coatings production. Its role in phosgene-free carbonylation keeps demand steady, as many downstream users require large, reliable base volumes. The market continues to depend on this grade for scale, particularly in Asia where plastics processing and engineering materials production remain well established. Battery grade is projected to grow at a 7.91% CAGR through 2031, making it the fastest-growing product grade in the study. This growth is driven by the expansion of electric vehicles and rising energy storage deployment, both of which are increasing demand for electrolyte solvents.

Pharmaceutical grade remains smaller in volume but commands the highest selling price, as purity must exceed 99.995% and compliance requirements are more stringent. This makes regulated supply a specialized niche with fewer credible producers and stronger margin protection. Fuel additive grade benefits from restrictions on methyl tert-butyl ether (MTBE) in several jurisdictions, which supports its place in the product portfolio, although it is not the primary demand driver. The dimethyl carbonate market is therefore divided across distinct value pools: industrial grade carries the bulk of volume, battery grade drives growth, and pharmaceutical grade supports premium pricing. This division is central to producer strategy, as the same upstream chemistry can supply multiple grades, while downstream purification determines final pricing power.

By Application: Polycarbonate Synthesis Keeps Scale While Battery Electrolyte Sets the Pace

Polycarbonate synthesis accounted for 35.41% of the dimethyl carbonate market in 2025, making it the largest application segment. This application remains important because engineering plastics demand is broad across automotive parts, electronics enclosures, and optical uses. The market continues to depend on this base-load application for capacity utilization, particularly in major Asian production clusters. Battery electrolyte is forecast to grow at an 8.33% CAGR through 2031, making it the fastest-growing application segment. This growth reflects rising cell output in China, South Korea, and the United States as automakers and storage developers continue placing new orders for battery-related equipment.

A 2025 pilot study showed that continuous CO2-to-dimethyl carbonate (DMC) to polycarbonate production can achieve 85.9% DMC yield with product quality comparable to that of conventional methods. Solvents and reagents are growing more slowly but are gaining support from the replacement of more hazardous chemicals in regulated settings. A 2025 Green Chemistry study established that dimethyl carbonate can serve as an acetonitrile substitute in peptide purification, strengthening the case for its use in controlled processing environments[1]De Luca C., et al., “Replace, Reduce, and Reuse Organic Solvents in Peptide Downstream Processing, The Benefits of Dimethyl Carbonate Over Acetonitrile,” Green Chemistry, pubs.rsc.org. Fuel additives remain a smaller application, but policy pressure on traditional oxygenates maintains a demand floor in some regions. The market also has potential in other electrolyte-related uses, including supercapacitors and dye-sensitized solar cells, although these remain at an earlier stage than mainstream lithium-ion demand.

By End-Use Industry: Plastics Leads Current Demand While Batteries Drive Future Expansion

Plastics accounted for 33.12% of the dimethyl carbonate market in 2025, retaining its position as the largest end-use segment. This reflects continued demand for polycarbonate and engineering resins across China, South Korea, and Japan. The market remains tied to this segment because plastics production provides a stable volume base and a consistent demand pattern. The battery industry is projected to grow at an 8.54% CAGR through 2031, making it the fastest-growing end-use segment. This pace reflects how quickly procurement is shifting toward electrolyte-grade solvents as EV manufacturers and energy storage developers scale output.

Paints and coatings remain a mature downstream area where dimethyl carbonate serves as a low-VOC co-solvent and coalescent. The pharmaceutical segment is also expanding as API manufacturers in India and China move away from legacy methylating agents toward greener process routes. The market has additional exposure to agrochemicals, where dimethyl carbonate supports the synthesis of pesticides and herbicides, and to electronics, where high-purity material is used in photolithography and liquid-crystal-related applications. Adhesives and sealants represent a smaller but growing niche where lower toxicity supports indoor air quality compliance. The dimethyl carbonate market, therefore, presents a layered end-use profile, combining established plastics demand, rising battery demand, and smaller regulated applications that improve the overall value mix.

Geography Analysis

Asia-Pacific held 59.37% of the dimethyl carbonate market share in 2025 and is expected to grow at a CAGR of 6.92% through 2031, making it both the largest and fastest-growing regional market. The region's position is driven by China, which combines large-scale chemical production, strong battery manufacturing, and significant downstream demand for plastics. China's dimethyl carbonate capacity exceeded 405.5 million tons per year in 2025, with the Pearl River Delta accounting for 52% of the country's battery-grade consumption. Eastern China accounted for 72% of downstream polycarbonate customers, supporting local demand and reducing logistics costs. China's new energy vehicle sales surpassed 10 million units in 2024, sustaining strong structural demand for electrolyte solvents. Japan and South Korea contribute through premium-quality supply, with UBE Corporation utilizing its gas-phase nitrite process to serve higher-end battery applications.

North America has been shifting away from reliance on imports toward domestic production. Previously, dimethyl carbonate (DMC) and ethyl methyl carbonate were fully imported into the United States, exposing battery supply chains to external sourcing risks. UBE Corporation has committed USD 700 million to a Louisiana facility targeting 100,000 tons per year of DMC, with operations scheduled for the first quarter of fiscal year 2027. The Japan Bank for International Cooperation (JBIC) confirmed financing support for this project through UBE's U.S. subsidiary, reinforcing the strategic importance of domestic battery solvent supply.

Europe remains a significant demand center for pharmaceuticals, coatings, and specialty chemicals, rather than for large volumes of battery electrolytes. The dimethyl carbonate market in Europe is shaped by Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) compliance, which increases registration and traceability requirements for suppliers serving the region[2]European Chemicals Agency, “Dimethyl Carbonate, Substance Information,” ECHA, echa.europa.eu. Lithium iron phosphate (LFP) batteries exceeded 10% of European electric vehicle (EV) battery demand in 2025, reducing dimethyl carbonate intensity per kilowatt-hour compared with nickel manganese cobalt (NMC)-heavy chemistries. South America and the Middle East and Africa remain early-stage markets, though Brazil, Argentina, and Saudi Arabia show potential through petrochemical and specialty chemical investment activity.

Competitive Landscape

The dimethyl carbonate market is moderately consolidated in high-purity supply and fragmented in industrial-grade output. The top five producers held 58% of high-purity-grade supply, while industrial-grade production remains fragmented, particularly in China. Pricing power, certification requirements, and customer retention are stronger in battery-related applications than in commodity-grade material. Shida Shinghwa, Shandong Haike Chemical, and Dongying Hi-tech Spring Chemical Industry compete on scale, feedstock integration, and proximity to downstream customers. Shida Shinghwa held more than 40% of the global high-end carbonate solvent supply.

Competitive pressure in the dimethyl carbonate market is shifting toward long-term contracts and logistics-linked supply arrangements. Haike Xinyuan's agreement to supply BYD with at least 100,000 tons per year of lithium battery solvents demonstrates how pipeline delivery and offtake security can convert geographic proximity into a competitive advantage. UBE Corporation competes through process quality and access to premium battery customers in Japan and the United States. Its Louisiana investment addresses the absence of domestic battery-grade production capacity in North America and reduces dependence on imports. The project's financing structure indicates that battery solvent production is being treated as critical industrial infrastructure rather than a standard commodity expansion.

Competition is also forming around cleaner synthesis technology and carbon efficiency. A 2025 Springer Nature study demonstrated continuous CO2-based production achieving high yield and polymer-grade output quality, supporting the commercial relevance of alternative process routes. Research published by the Royal Society of Chemistry examined electrochemical and green carbonate pathways, reinforcing the push toward lower-footprint production methods. These developments could serve as a differentiator by improving sustainability positioning while reducing exposure to standard commodity cost patterns. Producers that combine purification capability, customer access, and process innovation are likely to remain competitive as the market shifts toward battery and regulated high-purity applications.

Dimethyl Carbonate Industry Leaders

UBE Corporation

Shinghwa Advanced Material Group Co.,Ltd.

LOTTE Chemical Corporation

Dongying Hi-tech Spring Chemical Industry Co., Ltd.

Shandong Haike Chemical Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: UBE Corporation announced revisions to its Louisiana DMC/EMC (Ethyl Methyl Carbonate) plant plan: total capital investment increased from approximately USD 500 million to USD 700 million, attributable to higher material prices, rising US construction costs, and additional tariff measures; the operational start date was revised to Q1 FY2027. UBE plans to inject an additional USD 200 million into its US subsidiary in FY2026 to fund the revised budget.

- January 2026: Haike Xinyuan signed a three-year cooperation agreement with BYD Lithium Battery, committing to supply at least 100,000 tons per year of lithium battery solvents, including DMC, EC, EMC, and DEC, to BYD's Hubei project via dedicated pipeline transportation. The pipeline supply model eliminates spot-market exposure and positions Haike Xinyuan as a preferred integrated supplier to BYD.

Global Dimethyl Carbonate Market Report Scope

Dimethyl carbonate is a clear, flammable, and non-toxic liquid used as an organic solvent and methylating agent. It is VOC-exempt in the United States and Canada, and serves as a replacement for toxic chemicals such as phosgene and methyl halides in chemical synthesis.

The dimethyl carbonate market is segmented by product grade, application, end-use industry, and geography. By product grade, the market is segmented into industrial grade dimethyl carbonate, pharmaceutical grade dimethyl carbonate, battery grade dimethyl carbonate, and fuel additive grade dimethyl carbonate. By application, the market is segmented into polycarbonate synthesis, battery electrolyte, solvents, reagents, fuel additives, and electrolyte. By end-use industry, the market is segmented into plastics industry, paints and coatings industry, pharmaceutical industry, battery industry, agrochemicals industry, adhesives and sealants industry, and electronics industry. The report also covers market size and forecasts for dimethyl carbonate across 16 countries in major regions. The market sizes and forecasts are provided in terms of value (USD).

| Industrial Grade Dimethyl Carbonate |

| Pharmaceutical Grade Dimethyl Carbonate |

| Battery Grade Dimethyl Carbonate |

| Fuel Additive Grade Dimethyl Carbonate |

| Polycarbonate Synthesis |

| Battery Electrolyte |

| Solvents |

| Reagents |

| Fuel Additives |

| Electrolyte |

| Plastics Industry |

| Paints and Coatings Industry |

| Pharmaceutical Industry |

| Battery Industry |

| Agrochemicals Industry |

| Adhesives and Sealants Industry |

| Electronics Industry |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Grade | Industrial Grade Dimethyl Carbonate | |

| Pharmaceutical Grade Dimethyl Carbonate | ||

| Battery Grade Dimethyl Carbonate | ||

| Fuel Additive Grade Dimethyl Carbonate | ||

| By Application | Polycarbonate Synthesis | |

| Battery Electrolyte | ||

| Solvents | ||

| Reagents | ||

| Fuel Additives | ||

| Electrolyte | ||

| By End-Use Industry | Plastics Industry | |

| Paints and Coatings Industry | ||

| Pharmaceutical Industry | ||

| Battery Industry | ||

| Agrochemicals Industry | ||

| Adhesives and Sealants Industry | ||

| Electronics Industry | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Dimethyl Carbonate Market?

The Dimethyl Carbonate Market size is projected to expand from USD 1.36 billion in 2025 and USD 1.48 billion in 2026 to USD 1.99 billion by 2031, and is expected to register a CAGR of 6.10% between 2026 to 2031.

Which product grade is leading demand today?

Industrial-grade led the dimethyl carbonate market in 2025 with a 47.22% share, supported by demand for polycarbonate and coatings.

Which application is growing the fastest in dimethyl carbonate use?

Battery electrolyte is the fastest-growing application, with a projected 8.33% CAGR through 2031 as cell production expands.

Why is Asia-Pacific the most important regional base?

Asia-Pacific held 59.37% share in 2025 and combines China’s large production capacity, battery manufacturing scale, and dense downstream customer base.

Page last updated on: