Digital Workplace In Government and Public Sector Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

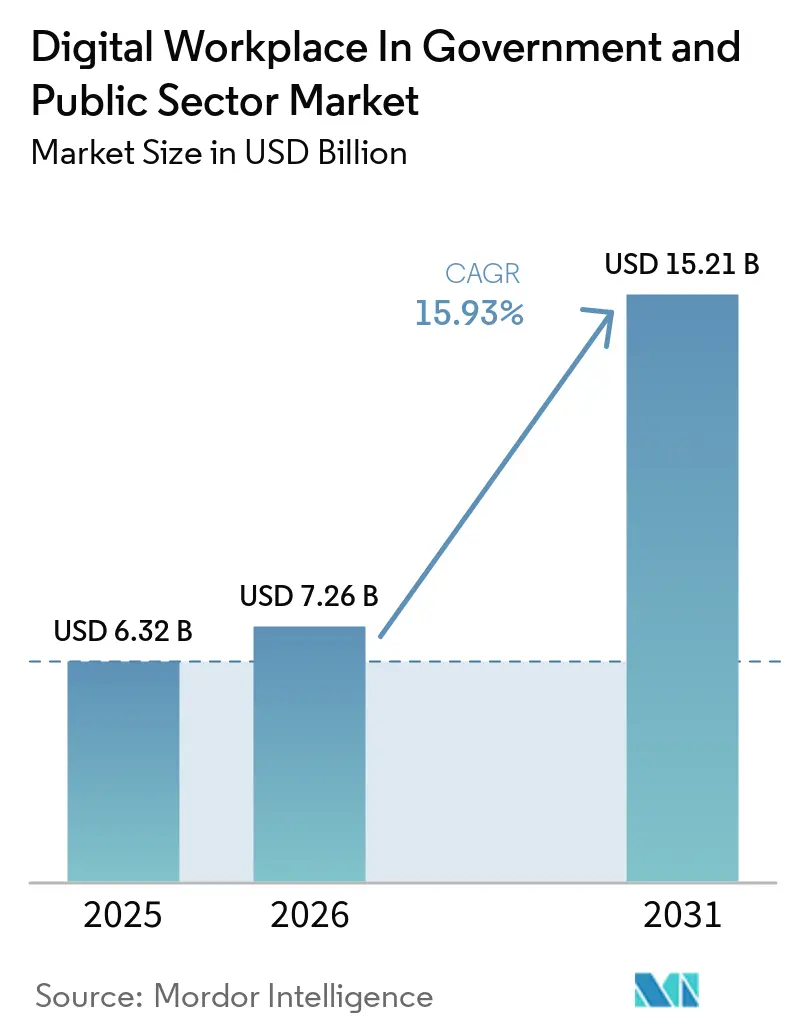

| Market Size (2026) | USD 7.26 Billion |

| Market Size (2031) | USD 15.21 Billion |

| Growth Rate (2026 - 2031) | 15.93% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

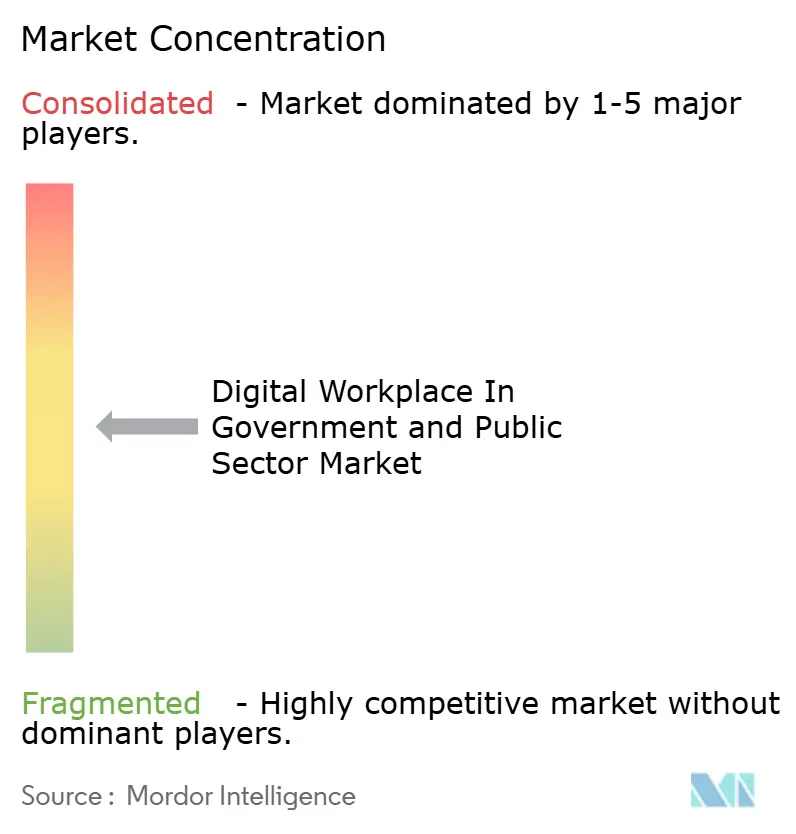

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Workplace In Government and Public Sector Market Analysis by Mordor Intelligence

The digital workplace in government and public sector market size is projected to be USD 6.32 billion in 2025, USD 7.26 billion in 2026, and reach USD 15.21 billion by 2031, growing at a CAGR of 15.93% from 2026 to 2031. The digital workplace in government and public sector market is being shaped by cloud-first procurement, stronger workforce compliance requirements, and the steady shift of generative AI from controlled pilots into day-to-day agency work. Zero trust security programs are also changing spending priorities because agencies now need managed endpoints, secure collaboration, and cloud-based work environments that can support continuous verification. At the same time, the digital workplace in government and public sector market continues to face slower rollout cycles where legacy estates and sovereign data rules make implementation more complex and raise total ownership costs. Competition is moving toward vendors that can combine compliant cloud delivery, workflow automation, and AI-enabled employee support in one environment rather than offering isolated tools. This leaves room for new contract wins in sub-federal and municipal government as SaaS pricing and cooperative purchasing make enterprise-grade workplace tools more accessible.

Key Report Takeaways

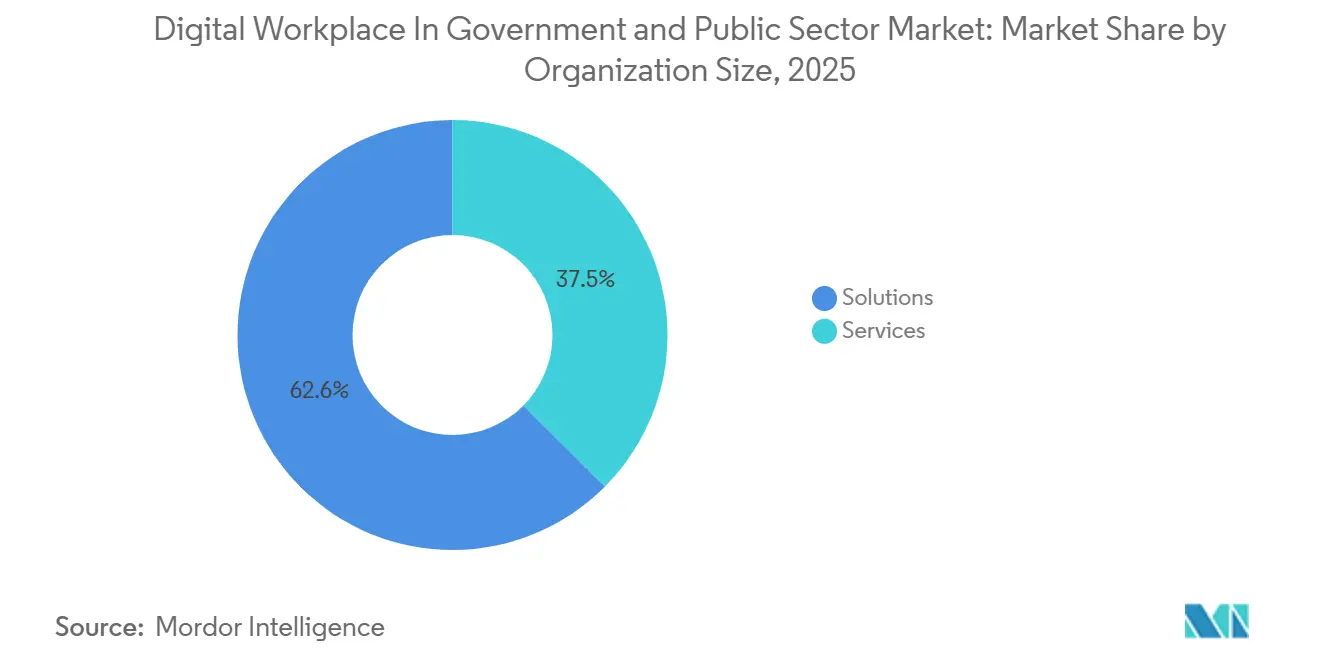

- By component, solutions held 62.55% of the digital workplace in government and public sector market in 2025, while the same segment is expected to grow at 16.23% CAGR through 2031.

- By deployment mode, cloud accounted for 46.22% of the digital workplace in government and public sector market size in 2025 and is projected to expand at a 16.67% CAGR through 2031.

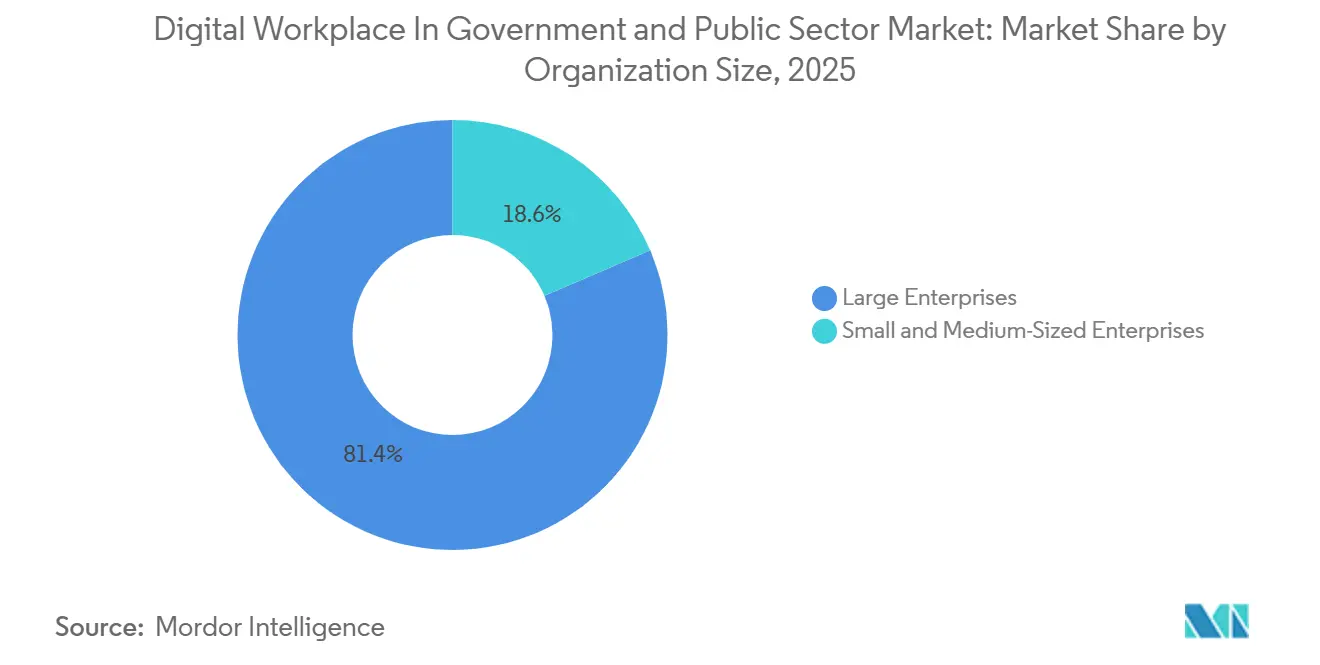

- By organization size, large enterprises held 81.44% share in 2025, while small and medium-sized enterprises are projected to grow at a 16.54% CAGR through 2031.

- By geography, North America held 38.45% share in 2025, while Asia-Pacific is projected to expand at a 16.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Digital Workplace In Government and Public Sector Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Government Cloud Modernization Programs | +4.0% | Global, led by North America and European Union | Short term (≤ 2 years) |

| Adoption of Generative AI for Citizen and Employee Knowledge Workflows | +2.9% | North America and Asia-Pacific, expanding globally | Short term (≤ 2 years) |

| Expansion of Secure Hybrid Work in Public Administration | +2.7% | North America, Europe, Asia-Pacific advanced economies | Short term (≤ 2 years) |

| Demand for Unified Digital Employee Experience Across Agencies | +2.1% | Global, North America and Europe leading | Medium term (2-4 years) |

| Rising Need for Zero Trust Collaboration Environments | +1.9% | North America and European Union, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Workforce Compliance and Auditability Requirements | +1.6% | North America, European Union, and national security-focused Asia-Pacific markets | Long term (≥ 4years) |

| Source: Mordor Intelligence | |||

Rising Government Cloud Modernization Programs

Government cloud modernization has moved from a broad policy goal to an operational requirement inside many public institutions. The GSA and ServiceNow OneGov agreement gave federal agencies discounts of up to 70% on ITSM Pro and Pro Plus bundles and projected workflow efficiency gains of 30%, which shows that centralized buying is being used to speed adoption of modern workplace platforms.[1]U.S. General Services Administration, “GSA and ServiceNow Strike Landmark OneGov Deal to Accelerate AI-Driven Government Modernization,” U.S. General Services Administration, gsa.gov Germany’s Deutsche Verwaltungscloud 2.0 program set out a federated cloud infrastructure for public administration from 2026 to 2029, which directly expands the addressable base for compliant workplace tools across multiple levels of government. The European Commission also awarded a EUR 180 million (USD 194 million) sovereign cloud contract in April 2026, which shows that large public bodies are now funding cloud environments as long-term institutional infrastructure rather than one-off IT projects. FedRAMP’s move toward consolidated rules and a continuous authorization model further supports this trend because agencies and vendors are being pushed toward cloud services that can present ongoing evidence of compliance instead of periodic documentation.

Adoption of Generative AI for Citizen and Employee Knowledge Workflows

Generative AI is becoming a core layer of the digital workplace in government and public sector market because agencies are using it in routine knowledge, search, and support workflows instead of limiting it to narrow pilots. The GAO reported in July 2025 that selected federal agencies had already moved generative AI use and management into active operating environments by 2024, which confirmed that deployment activity had advanced beyond experimentation.[2]U.S. Government Accountability Office, “Artificial Intelligence, Generative AI Use and Management at Federal Agencies,” U.S. Government Accountability Office, gao.gov Japan’s Digital Agency launched the government-wide GENNAI pilot in May 2026 for nearly 180,000 employees across ministries, using domestic large language models tuned to administrative language, which makes it one of the largest state-led workplace AI programs now in operation. ServiceNow strengthened the same direction in March 2026 when it launched EmployeeWorks with Moveworks integration, combining conversational AI and enterprise search in a single government-oriented front door for agency workers. In India, the Government of Andhra Pradesh announced work with IBM, BharatGen, and NxtGen in February 2026 to build a sovereign AI stack for citizen-focused and multilingual AI services, which reinforces how public sector AI is being tied to domestic control and language relevance.

Expansion of Secure Hybrid Work in Public Administration

Secure hybrid work remains a strong demand driver because return-to-office directives did not end remote or distributed work inside government, they forced agencies to redesign it under tighter control. The joint OMB and OPM memorandum issued in January 2025 formalized return-to-office implementation plans, which made agencies focus on work environments that can operate consistently across office, field, and home settings without weakening oversight.[3]U.S. Office of Personnel Management and Office of Management and Budget, “Joint OMB-OPM Memorandum, Agency Return to Office Implementation Plans,” U.S. Office of Personnel Management, opm.gov Microsoft’s release of Windows 365 Frontline for GCC and GCC High in 2026 showed that cloud PC environments now meet strict U.S. government hosting and compliance expectations, including support through government data centers. FedRAMP reported 525 certified services in 2026, which means agencies already have a large but curated pool of authorized cloud services to support secure workplace architectures. Citrix also launched its public sector platform in March 2026 to support FedRAMP High, air-gapped, and sovereign cloud deployments, showing that hybrid work demand now extends across both connected and isolated public environments.

Demand for Unified Digital Employee Experience Across Agencies

The digital workplace in government and public sector market is also being lifted by the need to reduce fragmentation across HR, IT service management, collaboration, and internal knowledge systems. The GSA and ServiceNow OneGov deal in September 2025 showed how agencies are using governmentwide contracting to reduce duplication and standardize access to AI-enabled workflow tools across departments. ServiceNow then launched EmployeeWorks in March 2026 as a single AI front door for public agencies, and it cited a 98% virtual agent deflection rate for IT tasks in the City of Raleigh, which highlights the efficiency gains agencies now expect from unified employee support platforms. Microsoft’s government cloud PC expansion supports the same shift because a unified workspace is easier to govern when endpoint access, applications, and security controls are delivered through one managed environment. Agencies that put this common layer in place earlier will have a more practical base for later AI agent rollout, while agencies that delay are more likely to carry duplicated tools, uneven controls, and inconsistent user experiences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Systems and Procurement Friction | -2.2% | Global, most acute in North America, European Union, and mature Asia-Pacific markets | Long term (≥ 4 years) |

| Heightened Data Sovereignty and Residency Constraints | -1.6% | European Union, Asia-Pacific core, spill-over to Middle East and Africa, and South America | Medium term (2-4 years) |

| Multi-Vendor Interoperability Complexity | -1.2% | Global | Medium term (2-4 years) |

| Public Sector Budget Rigidity and Multi-Year Approval Cycles | -0.9% | Emerging markets, with early friction in sub-national governments globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy Systems and Procurement Friction

Legacy infrastructure remains the most persistent barrier to faster adoption in the digital workplace in government and public sector market. The GAO reported that federal agencies spend more than USD 100 billion each year on IT and direct nearly 80% of that amount to operating and maintaining existing systems, which leaves a smaller pool for full modernization programs. The UK Cabinet Office reported in January 2025 that the number of highest-risk and most critical legacy systems rose 26% from 2023 to 2024, while only half of public services were digitized and digital expenditure remained 30% below benchmark levels. That pattern slows the replacement of old collaboration, endpoint, and workflow environments because agencies must fund continuity first and transformation second. Procurement reform may improve this over time, but current buying processes still stretch deployment timelines and make it harder for agencies to move quickly from fragmented tools to integrated workplace platforms.

Heightened Data Sovereignty and Residency Constraints

Data sovereignty rules are redirecting demand in the digital workplace in government and public sector market rather than stopping it, but they are making deployments more complex and slower to scale. The European Commission’s June 2026 proposal for the Cloud and AI Development Act introduced a common sovereignty assessment framework built on 48 criteria, which signals that public sector cloud decisions are becoming more formal, auditable, and jurisdiction-specific. In April 2026, the European Commission also awarded a EUR 180 million (USD 194 million) sovereign cloud contract to four providers for EU institutions, which shows that compliance with residency and control requirements now affects procurement at the largest public scale. Germany’s DVC 2.0 program, along with product launches such as Citrix Platform for Public Sector and Windows 365 Frontline for GCC and GCC High, shows that vendors must now support federated, single-tenant, air-gapped, or in-country configurations to remain relevant in sensitive government environments. These rules support spending on compliant platforms, but they also lengthen approval cycles, limit architecture choices, and raise delivery requirements for global suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Drive Platform Consolidation Across Agencies

Solutions accounted for 62.55% of the market in 2025 and are expected to grow at 16.23% CAGR through 2031, which shows that buyers are placing more value on integrated platform capability than on stand-alone service labor. Within the digital workplace in government and public sector market, agencies are directing visible demand toward unified communication and collaboration, employee experience platforms, intranet tools, and secure desktop access because these functions now sit close to daily mission delivery. The GSA and ServiceNow OneGov agreement reinforced that direction by offering deep discounts on AI-enabled workflow bundles and by emphasizing faster, more standardized modernization across agencies. Microsoft’s 2026 rollout of Windows 365 Frontline for GCC and GCC High also supports the solutions case because cloud PC and secure workspace tools are moving into the same buying frame as collaboration, endpoint control, and identity-centered access.

The services side is still important, but its role is changing from basic managed support toward implementation, migration, integration, and governance around platform environments. FedRAMP’s consolidated rules and transition toward continuous authorization signal a market structure that favors recurring SaaS and compliance-backed products, which reduces the relative weight of labor-heavy service models over time. Even so, the digital workplace in government and public sector industry still needs service providers to connect legacy estates, manage change, and support cross-agency rollout where internal skills remain limited. That means services will remain part of contract value, but the strongest position sits with vendors that can wrap services around a compliant product platform instead of selling services as a separate end point.

By Deployment Mode: Cloud Gains on Compliance Architecture and Budget Efficiency

Cloud held 46.22% of the market in 2025 and is the fastest-growing mode with a 16.67% CAGR through 2031, which shows that the digital workplace in government and public sector market size is shifting toward hosted environments that are easier to scale and govern. FedRAMP’s 525 certified services give agencies a pre-screened path to cloud adoption, which reduces review effort and supports faster procurement than a fully bespoke on-premises build. Microsoft’s GCC and GCC High cloud PC offer, together with ServiceNow’s government-ready workflow stack, shows that compliant cloud is now a practical operating model for collaboration, desktop access, and internal service delivery rather than a limited exception path. Cloud-native workplace tools also fit budget scrutiny more easily because they shift spending toward usage, upgrades, and measurable service levels instead of hardware refresh cycles.

Hybrid deployment is gaining importance as a bridge architecture for agencies that cannot move every workload into a common public cloud model at the same pace. Germany’s DVC 2.0 plan is built around a federated structure that spans government-operated infrastructure, certified commercial cloud, and sovereign European cloud services, which reflects how public administrations are mixing environments instead of forcing a single model. On-premises deployment still matters in classified, air-gapped, and public safety settings where external connectivity is restricted or prohibited. Citrix’s public sector launch in March 2026 captured this part of the market by supporting FedRAMP High, sovereign cloud, and isolated deployment requirements in one product framework.

By Organization Size: Large Agency Spend Anchors the Market as SME Growth Accelerates

Large enterprises held 81.44% of the market in 2025, which means the digital workplace in government and public sector market remains anchored by agencies with very large workforces, complex security obligations, and multi-year transformation budgets. These organizations often manage large endpoint estates, several classification levels, and multiple internal support functions, so they tend to favor broad workplace contracts that cover collaboration, service management, security, and employee support in a single structure. Japan’s GENNAI pilot across ministries and the continuing modernization of major government departments in Europe show how scale matters because only larger public bodies can roll out common workplace systems across such wide user populations. The UK Department for Work and Pensions’ 2025 support agreement with IBM also reflects how large agencies generate ongoing revenue even when part of the work still centers on maintaining and stabilizing existing platforms.

Small and medium-sized enterprises are the fastest-growing segment at a 16.54% CAGR through 2031, and that growth reflects easier access to enterprise-grade tools through shared buying routes and SaaS pricing. Kyndryl’s March 2026 award under the Texas Department of Information Resources cooperative contract is a clear example because it expands access to deliverables-based technology services for state and local government agencies without a full standalone procurement cycle. As this model becomes more common, smaller public entities can adopt secure endpoint management, workflow automation, and collaboration tools without building the same procurement depth as central governments. This is why the digital workplace in government and public sector market is opening faster at the municipal and regional level than in earlier technology cycles, even though large-agency contracts still dominate the revenue base.

Geography Analysis

North America held 38.45% of the digital workplace in government and public sector market share in 2025, which kept it as the largest regional base for spending and deployment. The region benefits from mature procurement and authorization frameworks, and the clearest examples are the GSA’s OneGov contracting model and FedRAMP’s large catalog of certified services. Return-to-office implementation plans issued by OMB and OPM in early 2025 also pushed agencies to invest in secure hybrid environments rather than simple office-only models. Microsoft’s government cloud PC expansion and FedRAMP 20x together show that vendors in North America are increasingly expected to pair usability with continuous compliance evidence.

Asia-Pacific is the fastest-growing region with a 16.67% CAGR through 2031, which shows that the digital workplace in government and public sector market size is rising quickly as government AI and sovereign cloud agendas mature. Japan’s GENNAI launch in May 2026 gave the region one of the clearest examples of large-scale government workplace AI deployment, with a target base of nearly 180,000 employees across ministries. In India, Andhra Pradesh’s February 2026 work with IBM, BharatGen, and NxtGen on a sovereign AI stack showed how regional demand is being linked to public service delivery, language localization, and domestic control of sensitive systems. This regional growth is also tied to a stronger preference for in-country data handling and government-specific compliance structures. Vendors with local infrastructure, domestic partnerships, and sovereign-ready product options are therefore better placed to capture new awards across Asia-Pacific.

Europe is being shaped by a combination of digital sovereignty rules and the need for interoperable public digital infrastructure. The European Commission’s Cloud and AI Development Act proposal in June 2026 introduced a 48-criterion sovereignty framework, which is pushing workplace procurement toward more auditable and jurisdiction-aware architectures. The Commission’s April 2026 sovereign cloud contract and Germany’s DVC 2.0 program show that this is no longer just a policy direction, it is now being translated into funded infrastructure and deployment design. The Middle East, South America, and Africa remain earlier-stage markets, but national digital government programs and external funding support are beginning to widen demand for collaboration, workflow, and employee support platforms.

Competitive Landscape

The digital workplace in government and public sector market is moderately consolidated, with large services integrators and platform-led vendors competing for the highest-value public contracts. Platform providers are strengthening their position through pre-certified environments, AI-enabled workflows, and government-specific routes to purchase, and this is visible in the combined weight of ServiceNow’s OneGov deal, Microsoft’s GCC and GCC High expansion, and the broader FedRAMP ecosystem. ServiceNow’s March 2026 launch of EmployeeWorks with Moveworks integration gave it a stronger front-door position in agency workflow and knowledge support, which is important because AI value is moving closer to the employee interface. Microsoft’s Windows 365 Frontline for GCC and GCC High added another competitive advantage by aligning secure desktop delivery with government-hosted cloud compliance requirements.

Services-led incumbents are responding by repositioning themselves around modernization programs, sovereign deployment, and regional public sector density. Kyndryl’s March 2026 Texas DIR award expanded its reach into state and local government through a cooperative contract, which is a practical route into smaller public entities that do not run large independent procurements. Its April 2026 SANDETEL contract in Andalusia and March 2026 assignment in Extremadura show the same approach in Europe, where public modernization work is increasingly tied to process automation, cloud adoption, and resilient infrastructure design. Capgemini’s June 2026 HM Revenue and Customs contract also fits this pattern because it centered on moving legacy infrastructure into a unified cloud-native platform with AI-powered customer experience capability. The practical result is that differentiation now depends less on labor scale alone and more on whether a vendor can combine compliant platform delivery, sovereign architecture, and measurable workflow outcomes.

White space remains strongest in sovereign-compliant AI deployment and in the smaller government segment where many entities still lack broad internal procurement and integration capacity. Citrix’s March 2026 public sector platform is a good example of how vendors are targeting that gap by supporting FedRAMP High, air-gapped, and data-localized deployment models in one offer. FedRAMP 20x and Europe’s CADA framework are likely to sharpen this divide because certification speed, machine-readable evidence, and jurisdictional control will matter more in near-term awards. Vendors that pair compliance automation, local hosting flexibility, and established government sales channels are therefore better positioned to keep winning as the digital workplace in government and public sector market moves further into AI-enabled operations.

Digital Workplace In Government and Public Sector Industry Leaders

Microsoft Corporation

Accenture plc

IBM Corporation

Tata Consultancy Services Limited

Capgemini SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Capgemini, in collaboration with NiCE and Route 101, signed a multi-year contract with HM Revenue and Customs to consolidate its legacy infrastructure into a unified, cloud-native platform with AI-powered customer experience capabilities, the contract is expected to deliver enhanced digital services to UK taxpayers at scale.

- May 2026: Japan's Digital Agency launched the large-scale GENNAI generative AI pilot targeting approximately 180,000 government employees across all ministries, approximately 100,000 employees gained access by May 29, 2026, with full ministry rollout progressing through FY2026.

- April 2026: The European Commission awarded a EUR 180 million (USD 204 million) sovereign cloud contract to four providers for EU institutions, the largest such procurement in EU history, establishing a benchmark for member-state government digital workplace deployments.

- April 2026: Kyndryl signed a contract with SANDETEL, the digital modernization entity of Andalusia's Regional Government in Spain, to provide consulting and managed services for process automation, cloud adoption, and National Security Scheme (ENS) compliance.

Global Digital Workplace In Government and Public Sector Market Report Scope

The Digital Workplace in Government and Public Sector Market comprises a comprehensive range of technologies, platforms, and services. These solutions enable public institutions, including federal and state governments, public agencies, educational institutions, and healthcare organizations, to establish integrated, secure, and collaborative digital environments for employees and stakeholders. The market includes enterprise collaboration tools, cloud-based productivity suites, unified communications, digital document management, workflow automation, cybersecurity frameworks, virtual desktop infrastructure, and employee engagement platforms.

The Digital Workplace in Government and Public Sector Market Report is Segmented by Component (Solutions [Unified Communication and Collaboration, Unified Endpoint Management, Enterprise Mobility and Management, Employee Experience Platforms and Intranet, Workflow Automation and Knowledge Management, and Virtual Desktop Infrastructure and Cloud PC] and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises and Small and Medium-Sized Enterprises), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions | Unified Communication and Collaboration |

| Unified Endpoint Management | |

| Enterprise Mobility and Management | |

| Employee Experience Platforms and Intranet | |

| Workflow Automation and Knowledge Management | |

| Virtual Desktop Infrastructure and Cloud PC | |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Nordics | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Component | Solutions | Unified Communication and Collaboration |

| Unified Endpoint Management | ||

| Enterprise Mobility and Management | ||

| Employee Experience Platforms and Intranet | ||

| Workflow Automation and Knowledge Management | ||

| Virtual Desktop Infrastructure and Cloud PC | ||

| Services | ||

| By Deployment Mode | Cloud | |

| On-Premises | ||

| Hybrid | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Nordics | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size and forecast for the digital workplace in government and public sector market?

The digital workplace in government and public sector market was sized at USD 6.32 billion in 2025, stands at USD 7.26 billion in 2026, and is forecast to reach USD 15.21 billion by 2031 at a 15.93% CAGR.

Which deployment mode is expanding the fastest in public sector digital workplace platforms?

Cloud is the fastest-growing deployment mode, with a 16.67% CAGR through 2031, and it held 46.22% share in 2025.

Why are government agencies increasing spending on workplace AI tools?

Agencies are using generative AI for knowledge workflows, enterprise search, summarization, and employee support, which is increasing the value of integrated workplace platforms.

Which region leads revenue and which region is growing the fastest?

North America led with 38.45% share in 2025, while Asia-Pacific is projected to record the fastest growth at a 16.67% CAGR through 2031.

What is the biggest barrier to wider rollout across government agencies?

Legacy systems and procurement friction remain the main obstacles because they extend timelines, tie up budgets in maintenance, and slow migration to integrated platforms.

Which vendors are best placed to compete for future contracts?

Vendors with FedRAMP-ready or sovereign-ready platforms, AI-enabled workflow tools, and strong public procurement access are best positioned, especially those combining product strength with implementation capability.

Page last updated on: