Digital Servo Press Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.14 Billion |

| Market Size (2030) | USD 1.58 Billion |

| Growth Rate (2025 - 2030) | 6.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

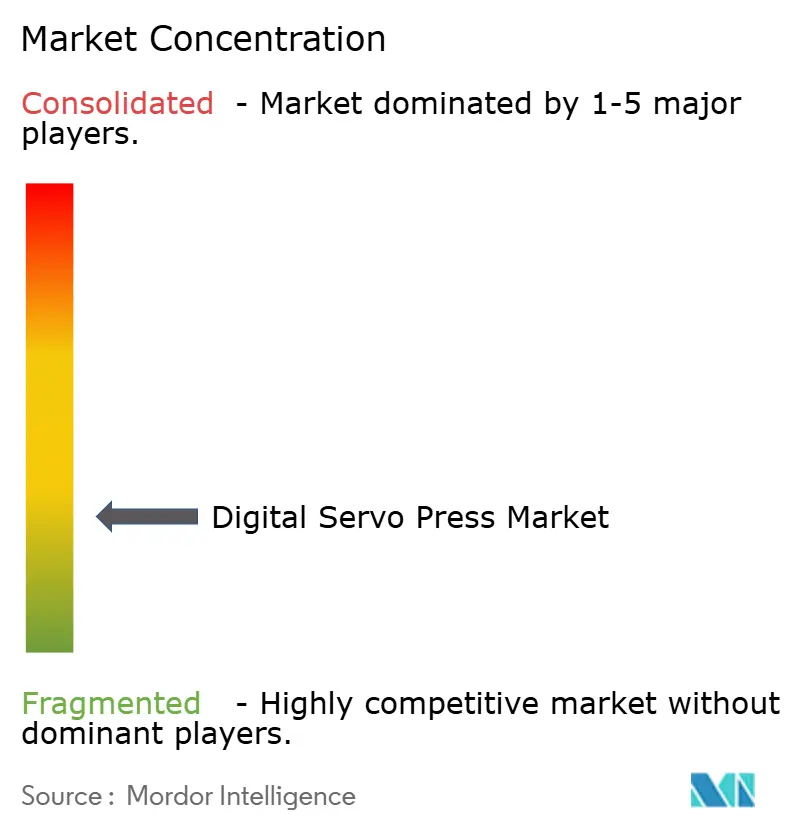

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Servo Press Market Analysis by Mordor Intelligence

The Digital Servo Press Market size is estimated at USD 1.14 billion in 2025, and is expected to reach USD 1.58 billion by 2030, at a CAGR of 6.74% during the forecast period (2025-2030). Rising demand for programmable force profiles, sub-millisecond response times, and full traceability in automotive battery modules, medical-device micro-joining, and electronics press-fitting is converting capital budgets away from hydraulic and pneumatic systems toward electric-servo alternatives. Quality-compliance mandates such as FDA 21 CFR Part 820 for medical devices and ISO 13485 for component-level traceability accelerate the shift because servo presses capture every force-displacement curve without secondary inspection steps. Manufacturers also seek energy savings, oil-free workspaces, and lower preventive-maintenance costs, which together reduce the total cost of ownership even when upfront prices are higher than legacy equipment. Asia-Pacific leads adoption thanks to China’s EV production ramp and ASEAN electronics greenfield projects, while North America and Europe retrofit servo technology into Industry 4.0 programs that favor closed-loop control and IIoT connectivity.

Key Report Takeaways

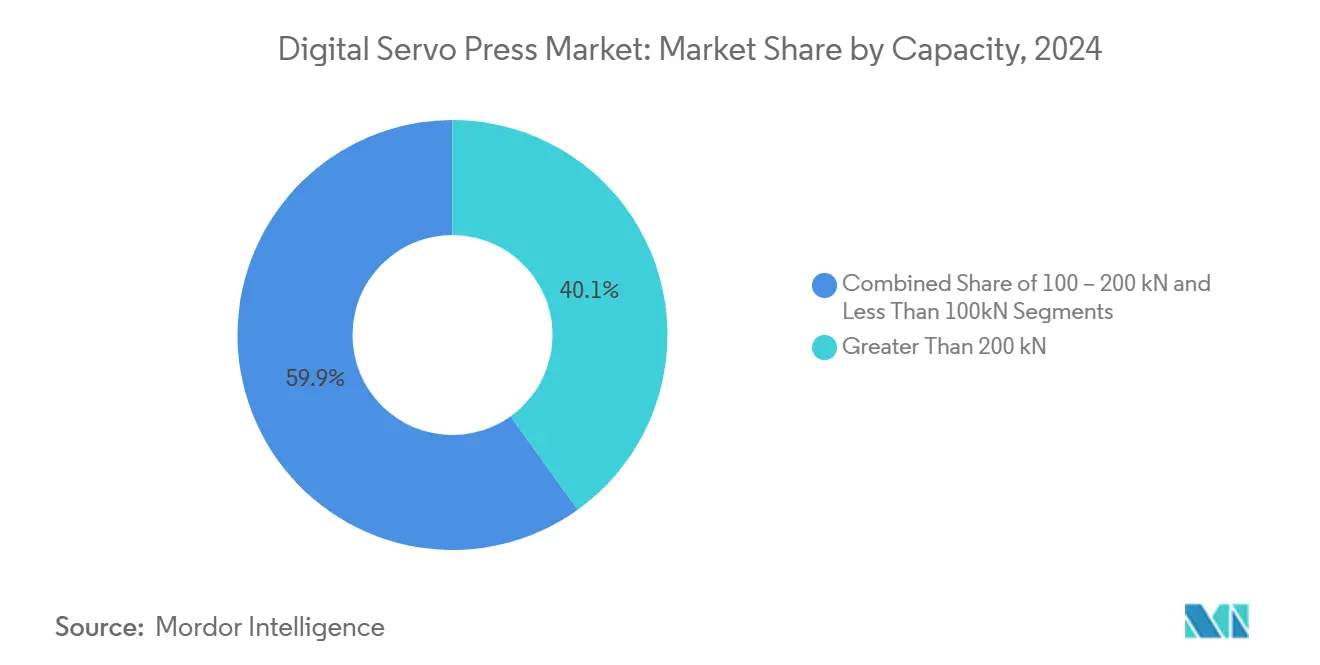

- By capacity, systems above 200 kN held 40.1% of the digital servo press market share in 2024, whereas sub-100 kN units are projected to expand at a 7.34% CAGR through 2030.

- By application, automotive and auto-components led with 44.3% revenue in 2024; medical devices are forecast to advance at a 7.67% CAGR to 2030.

- By frame type, straight-side and H-frame presses commanded 42.8% of revenue in 2024, while benchtop designs are set to grow at a 7.98% CAGR over the same horizon.

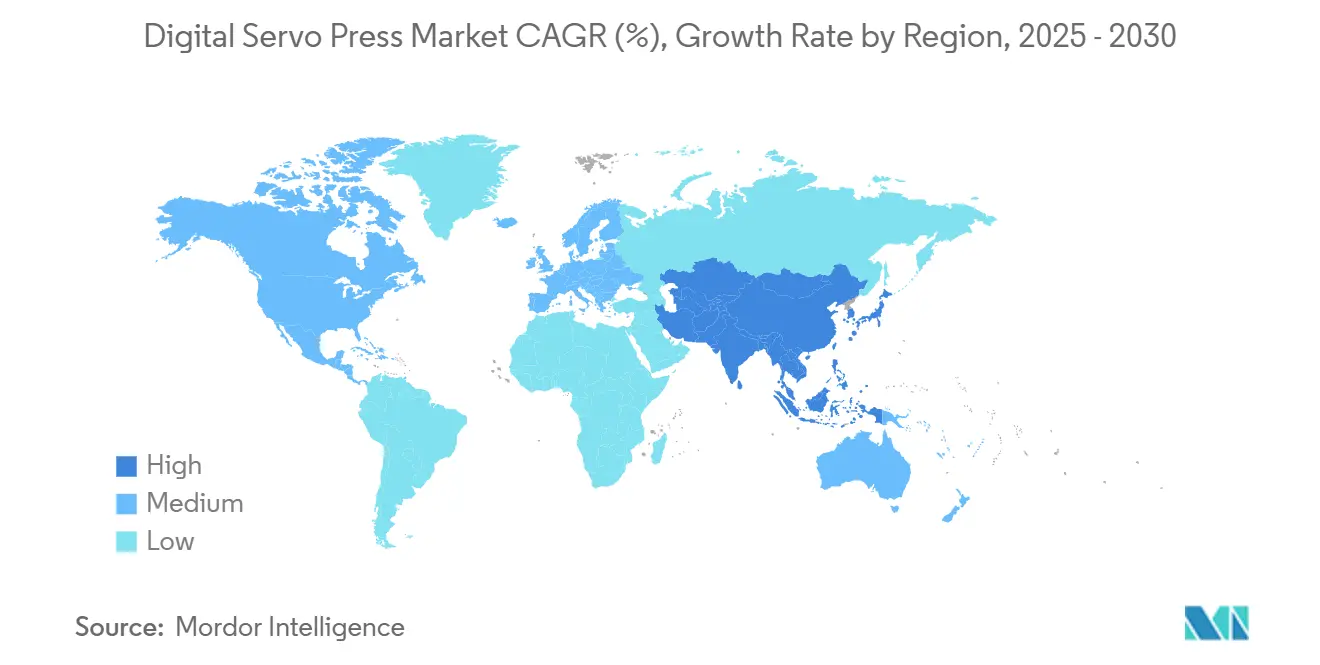

- By geography, Asia-Pacific accounted for 57.4% of installations in 2024 and is poised to post an 8.20% CAGR through 2030.

Global Digital Servo Press Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV, medical, and electronics assembly demanding high-precision, traceable press-fit and riveting | +2.1% | Global, concentrated in China, Japan, Germany, and ASEAN hubs | Medium term (2-4 years) |

| Industry 4.0/IIoT adoption—closed-loop control with full force–displacement data for quality compliance | +1.8% | North America, Europe, Japan; early adoption in China tier-1 suppliers | Short term (≤ 2 years) |

| Shift to lightweight materials and micro-joining requiring programmable, low-variance pressing profiles | +1.3% | Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| Energy efficiency, cleanliness, and lower maintenance versus hydraulic/pneumatic alternatives | +0.9% | Global, strongest ROI in high-volume plants | Medium term (2-4 years) |

| Flexible, software-defined setups enabling rapid changeovers and multi-product lines | +0.7% | North America, Europe, ASEAN | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EV, Medical, and Electronics Assembly Demanding High-Precision, Traceable Press-Fit and Riveting

Electric-vehicle battery packs require 200–400 joints to maintain tolerances of ±0.05 mm to prevent thermal runaway. Servo presses achieve this precision and document every cycle for potential future recalls. In 2024, China produced 9.5 million battery EVs, resulting in billions of pressing events that legacy hydraulic presses cannot certify economically at scale. In the U.S. and Europe, medical-device plants use integrated data acquisition sampling at 20 kHz to meet FDA design-control rules, eliminating the need for time-consuming post-press inspections. Electronics manufacturers in Thailand, Vietnam, and Malaysia require force precision within 1 N to avoid cracking brittle ceramic substrates during connector insertion. This demand across industries is expected to maintain high utilization rates and increase purchasing intentions among small, midsize, and tier-1 enterprises globally.

Industry 4.0/IIoT Adoption—Closed-Loop Control with Full Force–Displacement Data for Quality Compliance

Programmable force profiles—pre-load, insertion, hold, and retract—are executed in less than 2 seconds, replacing mechanical cam changeovers that previously took hours. Automotive lines use Ethernet/IP or OPC-UA links to store every pressing curve in centralized databases, enabling real-time dashboards for statistical process control. By 2024, AIDA Engineering will have installed over 2,200 servo presses globally, including 300 systems in North America, with safety stops that halt the ram within 0.5 mm when overload thresholds are reached. Japan’s Ministry of Economy, Trade, and Industry reported an increase in IIoT adoption from 11% in 2022 to 18% in 2024, supported by subsidies for smart-factory retrofits. This connectivity reduces scrap and rework, improves ROI, and drives the growth of the digital servo press market.

Shift to Lightweight Materials and Micro-Joining Requiring Programmable, Low-Variance Pressing Profiles

In 2024, European automakers used 150 kg of aluminum panels and 80 kg of composite battery enclosures per vehicle, ensuring a force variance of less than 5% to avoid surface defects. Servo presses measure material stiffness at first contact and adjust speed within milliseconds, protecting carbon fiber layups and ultra-high-strength steel brackets. Aerospace suppliers use servo riveting to prevent micro-cracks that could form under cyclic fatigue, maintaining structural integrity throughout the flight lifecycle. Electronics manufacturers press copper busbars into IGBT modules, requiring a force window of 2 N to protect silicon dies less than 5 mm thick. These complex material combinations demonstrate the benefits of programmable, electric-servo actuation.

Energy Efficiency, Cleanliness, and Lower Maintenance Versus Hydraulic/Pneumatic Alternatives

Electric motors consume power only during the stroke, reducing energy demand to one-quarter compared to hydraulic systems that run pumps continuously. Janome’s JP Series 5 operates in ISO Class 4 cleanrooms without oil mist, which is essential for semiconductor lines where a single particle can damage an entire wafer lot. Maintenance intervals extend to 5,000 hours between service checks, cutting annual upkeep costs by 60% in high-utilization plants. SEYI’s regenerative-braking design returns kinetic energy to the grid and reduces net power consumption by 12% in multi-shift operations. Carbon-credit schemes under EU and Chinese policies reduce payback periods to less than three years for retrofit projects, increasing the addressable market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher upfront cost vs. conventional presses creates ROI hurdles for SMEs | -1.2% | Global, acute in South America, the Middle East, and Africa | Short term (≤ 2 years) |

| Integration complexity with PLC/MES and the need for skilled programming/commissioning | -0.8% | ASEAN, India, Mexico, Eastern Europe | Medium term (2-4 years) |

| Limited suitability for ultra-high tonnage tasks compared to hydraulics | -0.5% | Global deep-drawing, hot-forging, heavy-stamping users | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Upfront Cost Versus Conventional Presses Creating ROI Hurdles for SMEs

A 200 kN straight-side servo press costs between USD 150,000 and 200,000, which is about twice the price of a comparable pneumatic unit. This higher cost extends the payback period to over four years for plants operating on a single-shift schedule. SMEs in Brazil, India, and Mexico often lack access to leasing options that allow investments to be spread over 7 to 10 years. As a result, they tend to prefer incremental upgrades to hydraulic systems. The total cost of ownership for servo technology becomes favorable only when energy savings, reduced scrap, and lower maintenance costs are calculated over a decade. However, many small firms lack the resources to conduct such analyses. European and Japanese OEMs now offer modular retrofits priced between USD 40,000 and 60,000. These retrofits, however, compromise the full programmability of purpose-built systems. Although financing options are improving and are expected to reduce this barrier, it remains a short-term challenge to growth[1]United Nations Conference on Trade and Development, “World Investment Report 2025,” unctad.org.

Integration Complexity with PLC/MES and Need for Skilled Programming/Commissioning

Setting up a servo press requires 200–400 engineering hours to calibrate force sensors, configure industrial networks, and connect quality databases. In talent-scarce regions, this increases budgets by 20–30%. ASEAN plants face difficulties in hiring engineers skilled in EtherCAT, PROFINET, and OPC-UA, causing ramp-up delays of up to six months. Turnkey packages from Delta and AIDA help simplify commissioning, but tasks such as custom profiles, vision alignment, and multi-axis synchronization still need OEM field service, costing USD 20,000–40,000 per installation. North American integrators handle this complexity, but price-sensitive emerging markets often delay projects until they improve their skills pipeline. Workforce upskilling programs and vendor-hosted training centers are essential to support the growth of the digital servo press market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Capacity: Automotive-Scale Loads Dominate, Benchtop Units Lead Growth

Systems above 200 kN captured 40.1% of 2024 revenue because automotive body-in-white, powertrain press-fit, and heavy appliance assemblies require multi-ton loads that only large straight-side frames can handle. This segment benefits from synchronized dual-servo drives that keep bed deflection below 0.1 mm under eccentric loads, a specification demanded by tier-1 suppliers to hold tolerances across large weldments. Automotive electrification programs in Germany and the United States prefer 300–400 kN models for battery busbar and motor-stator insertion, balancing force requirements, and floor-space constraints. In parallel, >500 kN systems remain limited to niche applications because of steep motor-torque demands that inflate capex.

Sub-100 kN presses, often benchtop or small C-frame units, are forecast to grow at 7.34%, the highest CAGR across capacity tiers, as medical-device and electronics plants prioritize cleanroom compatibility and 1 N force accuracy. Janome’s JP-S2 delivers 0.5–10 kN in a 300 mm-square footprint and logs every stroke over Ethernet, a feature suite popular with contract manufacturers making pacemakers and smartphone camera modules. The 100–200 kN band serves mid-range tasks such as brake-caliper riveting and e-motor stator pressing, and faces intensifying price competition as mechanical-press incumbents retrofit electromechanical drives to existing frames. Across all tiers, compliance with ISO 16092 safety standards adds USD 5,000–15,000 per unit, yet customers increasingly view certified safety circuits as non-negotiable for operator protection.

By Application: Automotive Still Leads, Medical Devices Sets the Pace

Automotive and auto-component uses held 44.3% revenue in 2024, anchored by electric-vehicle battery modules that demand hundreds of press-fit joints per unit and require force tracking for each insertion. Tier-1 suppliers in China’s Guangdong and Jiangsu provinces procure high-capacity frames to synchronize multi-axis movement and hit takt times under 2 s per cycle. North American electric-pickup programs also invest in servo presses to assemble aluminum battery enclosures, leveraging regenerative-braking energy recapture to improve plant sustainability metrics. Despite dominance, growth moderates as the installed base matures and long automotive capex cycles slow repeat orders.

Medical devices are projected to expand at 7.67%, the fastest CAGR, fueled by implantable-device assembly, orthopedic screw insertion, and surgical stapler riveting that must meet FDA data-logging requirements. Servo presses samples at 20 kHz and creates tamper-proof records, making them the preferred choice for ISO 13485 audits. Electronics applications, ranging from connector insertion to transformer-core stacking, benefit from multi-stage force profiles that reduce scrap to below 0.5%, appealing to high-volume consumer-device lines in Vietnam and Malaysia. Aerospace and defense projects deploy servo presses for composite panel riveting to curb delamination under cyclic loads, preserving aircraft structural integrity. These diverse use cases collectively reinforce the growth outlook for the digital servo press market.

By Frame Type: Rigid Straight-Side Structures Hold Share, Benchtop Designs Accelerate

Straight-side and H-frame structures amassed 42.8% of 2024 revenue because they keep parallelism across large beds and withstand eccentric forces in multi-ton operations. Automotive chassis plants rely on 4-post guidance to keep ram skew under 0.1 mm when pressing oversized suspension arms. These frames accept dual or quad servo motors, distributing load evenly and extending ball-screw life, yet they occupy significant floor space and carry high acquisition costs. European appliance makers combine straight-side rigidity with quick-change platens to shorten setup times across product variants.

Benchtop and tabletop designs, occupying less than 0.5 m², are forecast to grow at 7.98%, propelled by medical-device startups and university R&D labs that need clean, oil-free, and software-defined presses. Janome’s JP-Series integrates with LabVIEW and MATLAB, allowing researchers to visualize force curves in real time and tweak parameters without mechanical tooling. C-frames offer three-sided access for oversized workpieces and vision-system integration, advantageous in appliance motor-stator pressing. Custom in-line frames combine servo presses, robots, and conveyors in turnkey cells, achieving sub-5-second cycles, essential for lights-out factories in Japan and Germany. CE and UL certifications extend product-development timelines by up to 12 months, favoring incumbents that already maintain compliance portfolios, yet demand for agile footprint solutions keeps new entrants innovating on modular design[2]Janome Industrial Equipment, “JP Series 5 Cleanroom Servo Press,” janome.co.jp.

Geography Analysis

Asia-Pacific accounted for 57.4% of 2024 installations and is projected to post an 8.20% CAGR to 2030, the highest regional momentum. China’s 9.5 million EV output in 2024 translates to thousands of servo presses across battery, busbar, and cooling-plate lines, especially in Guangdong and Zhejiang provinces, where government incentives favor energy-efficient equipment. ASEAN drew USD 31 billion in electronics greenfield investment that same year, spawning 12 smart factories with fully networked servo-press lines operating under Manufacturing Execution System oversight. Japan’s subsidy scheme covering 30% of Industry 4.0 capex helped IIoT adoption climb from 11% to 18% in two years, boosting domestic demand for servo-equipped assembly cells. India is gaining traction as smartphone OEMs and EV component suppliers deploy sub-100 kN benchtop models, yet skills shortages and financing gaps temper near-term penetration[3]Board of Investment Thailand, “Smart Factory Incentive Program 2024,” boi.go.th.

North America benefits from reshoring trends and strict traceability mandates. AIDA’s Dayton, Ohio center supports proof-of-concept trials that reduce project risk and has already underpinned more than 300 regional installations. U.S. medical-device makers require FDA-compliant data logs for every press stroke, a regulation that positions servo technology as the de facto standard. Mexican tier-1 automotive suppliers in Guanajuato and Nuevo León integrate servo presses to meet OEM carbon-reduction pledges while lowering energy spend amid volatile power tariffs. Canada’s aerospace hubs employ servo presses for composite fuselage riveting, keeping force variance within 5% to avoid micro-cracks under fatigue loads, a performance unattainable with pneumatic riveters.

Europe follows closely with electric-vehicle initiatives that produced 1.2 million battery EVs in 2024, infusing demand for servo presses in German, French, and Italian assembly plants. ANDRITZ Schuler’s 2025 rebrand heralds a combined push into battery production and lightweight-forming lines, leveraging an existing mechanical-press footprint to accelerate servo upgrades. Eastern Europe lures appliance and electronics OEMs with skilled labor and EU proximity, yet adoption rates lag because local integrators are still building expertise in EtherCAT and OPC-UA connectivity. The Middle East and Africa pursue servo presses in Vision 2030 industrialization agendas, but high capex and limited financing slow deployments, while South America faces currency volatility and skills gaps that lengthen ROI timelines.

Competitive Landscape

The Digital Servo Press Market concentration is moderately fragmented. Japanese incumbents—Janome, AIDA, Sintokogio, THK, Sanyo Machine Works, and ESTIC—leverage decades of servo-motor proficiency and robotics integration to dominate Asia-Pacific installations. Their portfolios span benchtop to 3,500-ton frames, allowing one-stop sourcing for tier-1 suppliers that operate across multiple capacity bands. European specialists, notably TOX PRESSOTECHNIK, SCHMIDT Technology, and Kistler Group, focus on precision assembly, supplying modular frames and 0.1%-accuracy force sensors that attract German automotive and Italian medical-device plants. These firms maintain application-engineering teams that calibrate force profiles onsite, reinforcing customer lock-in through value-added services.

Traditional mechanical-press OEMs—ANDRITZ Schuler, Komatsu, Amada, and Stamtec—are retrofitting electromechanical drives into existing frames to enter the digital servo press market. ANDRITZ’s acquisition of Schuler in March 2025 consolidates European share and brings battery-line expertise under one banner. Komatsu and Amada partner with servo-motor suppliers to bundle drive kits that convert hydraulic C-frames into semi-servo hybrids, narrowing price gaps in the 100–200 kN band and eroding pure-play specialists’ margins. Atlas Copco, Promess, and Intelligent Actuator cross-sell presses with fastening systems and robots, easing integration complexity for OEMs that prefer single-invoice procurement strategies.

Market white space includes ultra-compact benchtops for medical-device startups, cloud-based force-profile libraries for predictive maintenance, and energy-storage add-ons for regions with grid instability. AIDA’s 2024 purchase of HMS Products extends service coverage across the American Midwest, combining hydraulic know-how with servo expertise for hybrid systems above 500 kN, a niche still resistant to full electric conversion. Regulatory compliance remains a moat: ISO 16092 and CE Mark reviews run 6-12 months, deterring new entrants and sustaining incumbents’ pricing power, particularly in Europe and North America.

Digital Servo Press Industry Leaders

Janome Industrial Equipment

Promess Inc.

Kistler Group

TOX PRESSOTECHNIK

IAI (Intelligent Actuator)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ANDRITZ acquired Schuler AG and rebranded the entity as ANDRITZ Schuler, integrating servo-press technology into battery-production lines and lightweight-forming applications to serve European automotive OEMs' electrification programs. The acquisition expands ANDRITZ's metal-forming portfolio and positions the combined entity to compete with Japanese servo-press incumbents in Asia-Pacific markets.

- February 2025: AIDA Engineering announced the expansion of its Dayton, Ohio facility to 180,000 square feet, adding application-development labs and customer-training programs to support North American manufacturers adopting servo-press technology for electric-vehicle battery assembly and medical-device production. The facility has supported over 300 servo-press installations across automotive, aerospace, and electronics sectors.

- January 2025: Delta Electronics launched the AM-ESP series servo-press controller in Thailand, integrating human-machine interfaces, programmable logic controllers, and servo motors in pre-configured packages that reduce commissioning time by 30% and simplify integration with manufacturing execution systems. The product targets ASEAN electronics contract manufacturers and automotive tier-2 suppliers.

- December 2024: Kistler Group introduced the maXYmos TL force-monitoring system with 0.1% measurement accuracy and 20-kilohertz sampling rates, enabling real-time process control and traceability for medical-device and automotive press-fitting applications. The system integrates with Ethernet/IP and OPC-UA industrial networks to support Industry 4.0 deployments.

Global Digital Servo Press Market Report Scope

| < 100 kN |

| 100 – 200 kN |

| > 200 kN |

| Automotive & Auto Components |

| Electrical & Electronics (incl. Motors) |

| Aerospace & Defense |

| Medical Devices & Equipment |

| Consumer Appliances & Power Tools |

| Metalworking & General Industrial |

| Other Industries |

| C-Frame (Gap Frame) |

| Straight-Side / H-Frame |

| 2-Post / 4-Post (Column) Frame |

| Benchtop / Table-Top Presses |

| Custom / In-line Frames |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Capacity | < 100 kN | |

| 100 – 200 kN | ||

| > 200 kN | ||

| By Application | Automotive & Auto Components | |

| Electrical & Electronics (incl. Motors) | ||

| Aerospace & Defense | ||

| Medical Devices & Equipment | ||

| Consumer Appliances & Power Tools | ||

| Metalworking & General Industrial | ||

| Other Industries | ||

| By Frame Type | C-Frame (Gap Frame) | |

| Straight-Side / H-Frame | ||

| 2-Post / 4-Post (Column) Frame | ||

| Benchtop / Table-Top Presses | ||

| Custom / In-line Frames | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What CAGR is forecast for the digital servo press market to 2030?

The market is projected to grow at a 6.74% CAGR from 2025 to 2030 based on Mordor Intelligence estimates.

Which region currently leads installations of digital servo presses?

Asia-Pacific held 57.4% of all installations in 2024 and is predicted to maintain leadership through an 8.20% CAGR.

Why are medical-device manufacturers adopting servo presses rapidly?

FDA traceability rules require force-displacement data on every joint, and servo presses capture this information in real time, driving a 7.67% CAGR in medical applications.

How do servo presses lower operating costs compared with hydraulic units?

Electric drives draw energy only during the press stroke, cut maintenance intervals fourfold, and eliminate oil-related clean-room contamination, trimming total cost of ownership despite higher capex.

What is the main technical limit preventing the full replacement of hydraulic presses?

Tasks above 500 kN still demand force density that servo motors cannot yet deliver cost-effectively, so deep drawing and hot forging remain hydraulic domains.

Page last updated on: