Digital Printing For Tableware Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

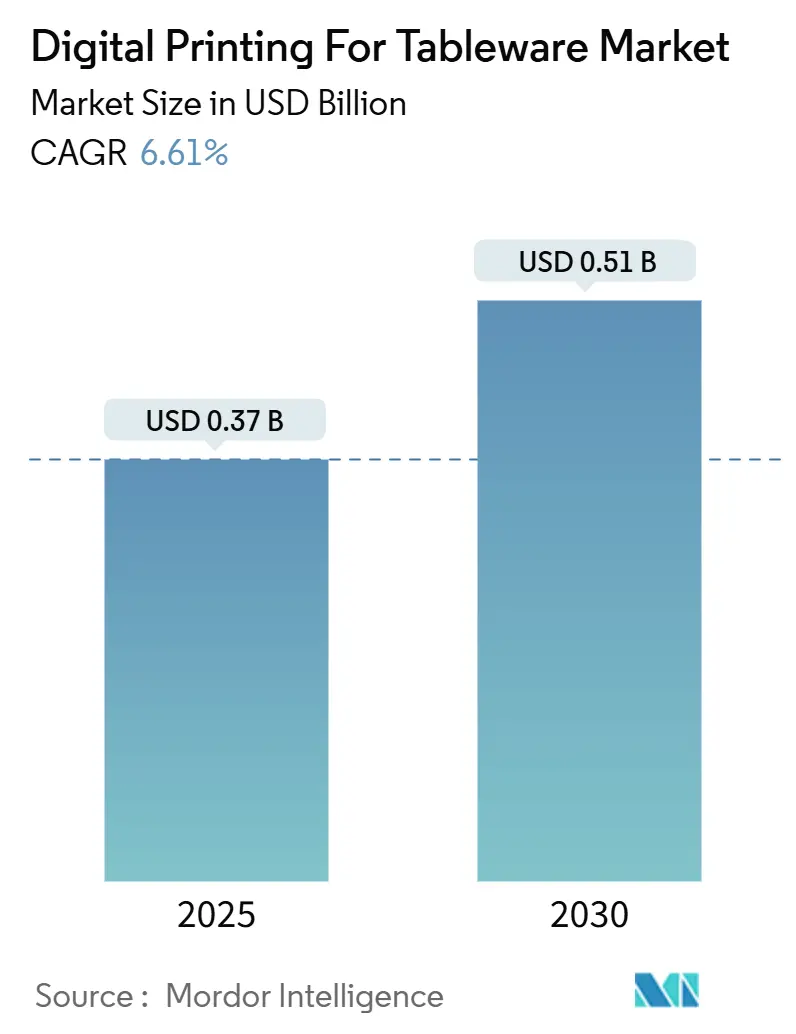

| Market Size (2025) | USD 0.37 Billion |

| Market Size (2030) | USD 0.51 Billion |

| Growth Rate (2025 - 2030) | 6.61% CAGR |

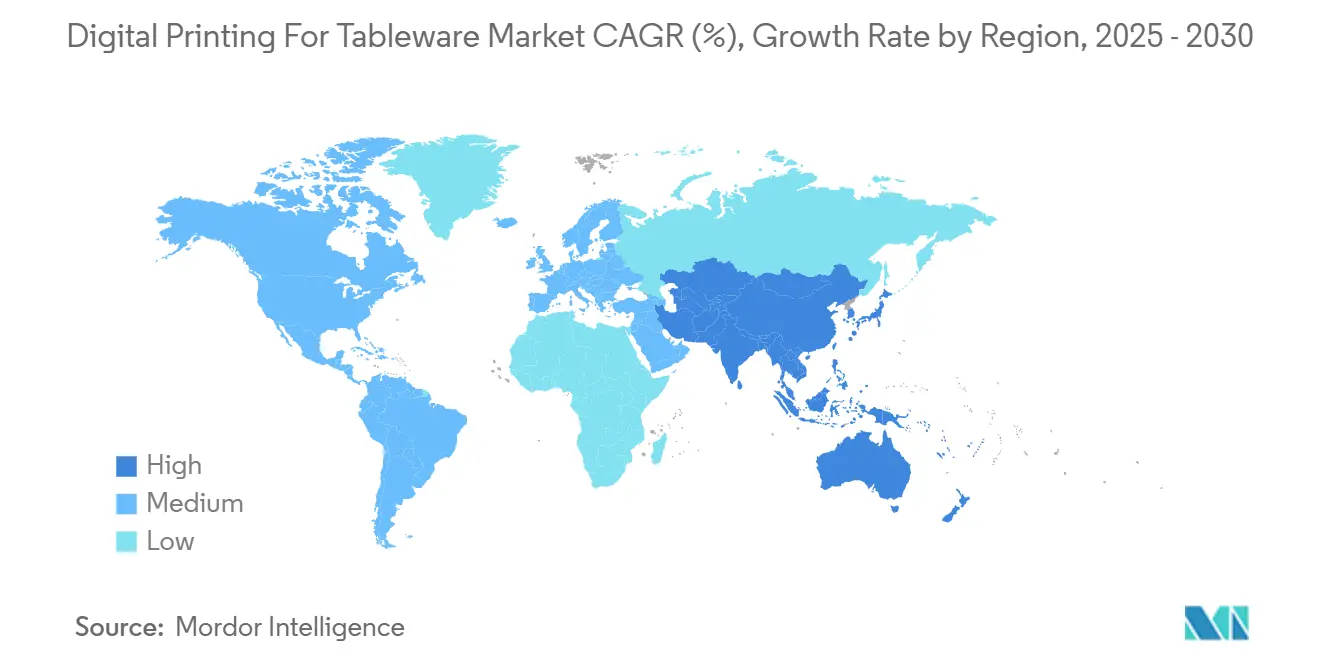

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

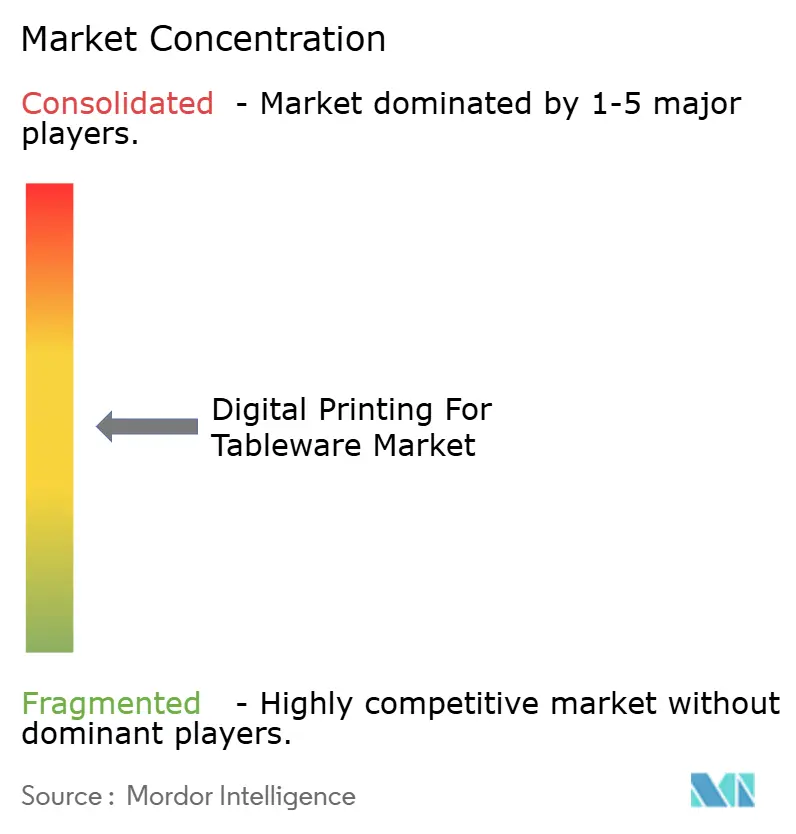

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Printing For Tableware Market Analysis by Mordor Intelligence

The digital printing for tableware market size is estimated at USD 0.37 billion in 2025 and is projected to reach USD 0.51 billion by 2030, representing a 6.61% CAGR over the forecast period. The demand for short-run customization in hospitality, rapid technology upgrades in ceramic inkjet heads, and stricter sustainability mandates are combining to drive digital adoption across tableware plants. Operators of ghost kitchens now require on-demand branded plates and cups that eliminate the tooling and inventory burdens associated with screen printing, while regulations in the United States and Europe clarify safety limits for UV-curable food-contact inks, alleviating liability concerns. Equipment vendors respond by integrating UV LED curing and automated vision systems, which speed up changeovers and reduce energy use by approximately 60% compared to thermal ovens. A widening range of water-based and low-migration formulations enables corporate buyers to match their emissions pledges, while manufacturers discover new premium niches, such as augmented-reality tableware, emerging from the same platform capability.

Key Report Takeaways

- By product type, plates led with 39.76% revenue share in 2024; glasses are projected to expand at a 7.23% CAGR to 2030.

- By printing technology, multi-pass inkjet accounted for 47.63% of the digital printing for tableware market share in 2024, while UV LED direct-to-object is growing at the fastest rate, with a 7.19% CAGR through 2030.

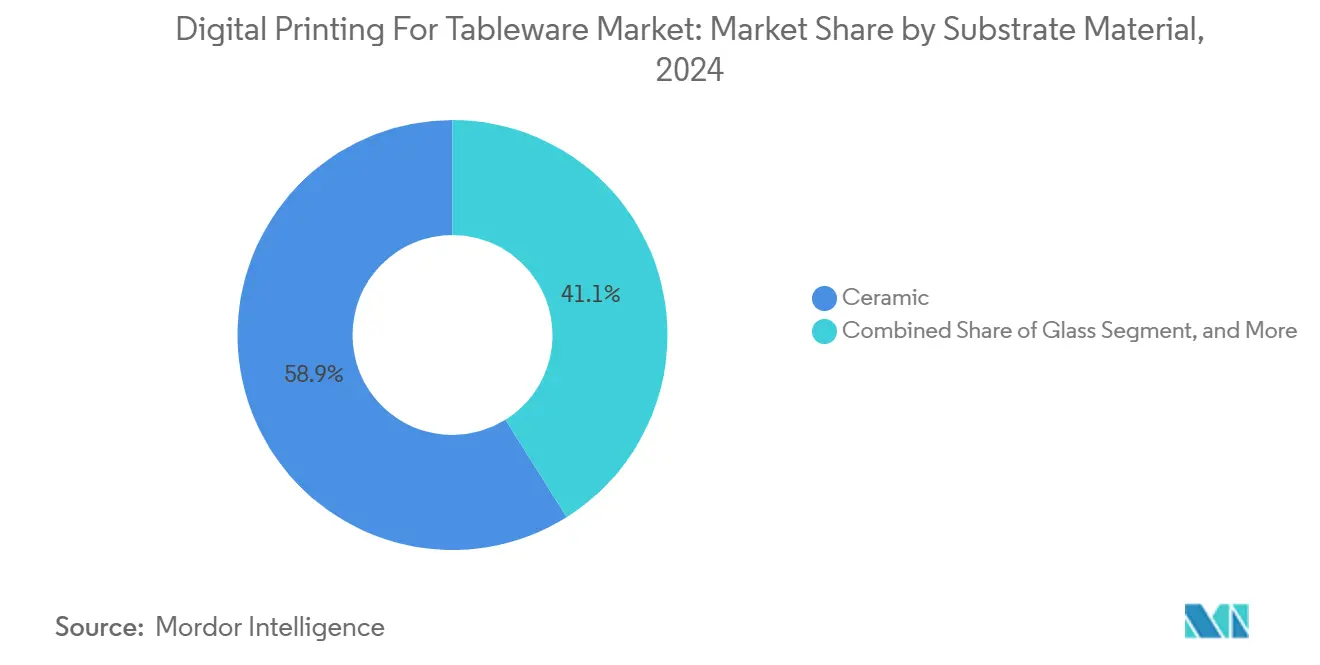

- By substrate, ceramics captured a 58.91% share of the digital printing for tableware market size in 2024, and glass is advancing at a 7.31% CAGR to 2030.

- By end user, commercial foodservice held a 42.37% share of the digital printing for tableware market size in 2024; promotional and corporate gifting is projected to rise at a 7.06% CAGR through 2030.

- By geography, Europe dominated with a 33.67% share in 2024, whereas the Asia-Pacific region recorded the highest CAGR at 7.11% through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Digital Printing For Tableware Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for personalized tableware in hospitality sector | +1.2% | North America and Europe, global spill-over | Medium term (2-4 years) |

| Rising adoption of short-run production among tableware manufacturers | +0.9% | Europe and Asia-Pacific, emerging in North America | Short term (≤ 2 years) |

| Improvements in ceramic inkjet head resolution and speed | +0.8% | Global, led by Germany and Japan technology hubs | Long term (≥ 4 years) |

| Eco-friendly inks driving brand sustainability initiatives | +0.7% | Europe and North America, spreading to Asia-Pacific | Medium term (2-4 years) |

| Emergence of augmented reality enabled interactive tableware | +0.4% | North America and select European markets | Long term (≥ 4 years) |

| On-demand dining ware production for ghost kitchens | +0.6% | Asia-Pacific and North America urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Personalized Tableware in the Hospitality Sector

Hotels and restaurants are transforming their table settings into brand assets by commissioning seasonal or location-specific motifs that enhance the guest experience and increase social media visibility. Digital workflows enable operators to refresh designs without the minimums of 1,000 units or more required by screen printing, thereby aligning inventory with occupancy fluctuations. U.S. Food and Drug Administration migration protocols for food-contact substances provide clear test paths, giving hospitality chains confidence to deploy digitally printed plates even for hot beverage service. Promotional tableware also leverages this capability, with corporate gifting volumes growing at a rate of more than 7% annually, as marketers favor reusable branded objects over single-use items. The upshot is a pull-through effect for equipment, consumables, and design services across the digital printing market for tableware.

Rising Adoption of Short-Run Production Among Tableware Manufacturers

European ceramic makers, faced with stringent waste directives, are adopting agile production models that minimize excess stock. Digital imaging removes screens, meshes, and chemical developers, slashing preparation times from days to minutes and supporting batches as small as 50 units. Canon’s industrial division reported a 40% jump in ceramic printing inquiries during 2024, while average order sizes halved, confirming the structural pivot toward make-to-order workflows.[1]CANON INC., “Canon Announces New Industrial UV LED Printing System for Ceramic Applications,” canon.com Asia-Pacific factories are following suit, installing modular UV LED lines that switch artwork through software rather than mechanical change parts. The resulting reduction in obsolescence and energy use is adding 0.9 percentage points to the forecast CAGR of the digital printing for tableware market.

Improvements in Ceramic Inkjet Head Resolution and Speed

Next-generation piezoelectric heads now achieve 1,200 dpi while sustaining throughputs near 150 m² per hour, erasing the historic trade-off between quality and productivity. Durst’s latest platform combines multi-lane image streams with real-time drop-watch cameras that correct jetting deviations in real-time, ensuring tone consistency across extended runs. Higher native resolution lets decorators reproduce photographic imagery and micro-text, expanding addressable segments such as luxury hotelware and commemorative porcelain. As these heads scale, they are expected to contribute 0.8 percentage points to industry growth.

Eco-Friendly Inks Driving Brand Sustainability Initiatives

Water-based and low-migration UV formulations eliminate heavy metals and volatile solvents, directly supporting corporate carbon and health targets. The European Food Safety Authority caps residual bisphenol compounds in coatings, prompting brands to list ink chemistries in procurement scorecards.[2]European Food Safety Authority, “Technical Guidance on Food Contact Materials,” efsa.europa.eu Early adopters publicize carbon-saving claims, citing lifecycle analyses that show digital printing can reduce process water use by more than 80% compared to analog methods. As sustainable sourcing becomes a bid requirement for institutional buyers, compliant ink sets are tipping purchase decisions and nudging volumes toward digital lines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of industrial direct-to-object printers | -1.4% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Limited durability of digitally printed graphics under commercial dishwashing | -0.8% | Global, focus in commercial foodservice | Medium term (2-4 years) |

| Supply chain volatility in specialty ceramic pigments | -0.6% | Global, highest in Asia-Pacific | Short term (≤ 2 years) |

| Regulatory uncertainty around food-contact safe UV inks | -0.5% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Industrial Direct-to-Object Printers

Full-format UV LED machines cost USD 200,000–800,000, a hurdle for small regional potteries. Financing tools, such as equipment-as-a-service, lower upfront outlays but raise unit costs, thereby diluting margins in price-sensitive segments. Regional development banks in the European Union offer digitization loans; however, comparable support is limited in many emerging economies, which slows down the diffusion.[3]European Investment Bank, “Digital Transformation Advisory Services,” eib.org

Limited Durability Under Commercial Dishwashing

Industrial dishwashers can reach temperatures of 82 °C with caustic detergents, and field tests have shown that some digitally printed plates fade after 800 cycles, compared to 2,000 cycles for traditional glazes. Manufacturers respond by adding clear overglazes or switching to high-cross-link UV inks, but these steps increase material costs and can negate part of the environmental benefit.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Plates Maintain Scale Advantage While Glasses Surge

Plates represent the largest volume in the digital printing for tableware market, with a 39.76% share in 2024, tied to standardized foodservice specifications. That dominance provides plate production with favorable economies of scale, allowing decorators to amortize printhead wear across high uptimes. Steady demand from quick-service restaurant chains reinforces base-load throughput, keeping plate lines near capacity for much of the year. The glasses sub-segment, although smaller, is projected to grow at a 7.23% CAGR through 2030. UV LED direct-to-glass systems bond ink without primers, simplifying curved-surface jobs and opening premium beverage branding opportunities. Stemware with vineyard-specific QR codes exemplifies how digital imaging adds value beyond aesthetics by embedding traceability and interactive experiences. Cups, bowls, and serveware post mid-single-digit growth, largely driven by promotional gift programs and the expansion of casual dining.

In commercial kitchens, plates must endure thermal shocks from heat lamps and dishwashers. Multi-layer digital inks that flex with ceramic substrates help meet these durability tests, and ISO 6486 leach testing validates compliance with food-contact regulations. On the glass side, adhesion promoters matched to soda-lime compositions keep chipping rates low in high-throughput bar settings. Suppliers package these chemistries with cloud-linked press profiles, letting decorators replicate Pantone matches at remote sites without trial-and-error runs.

By Printing Technology: Multi-Pass Holds Share as UV LED Accelerates

Multi-pass inkjet technology controlled 47.63% of the digital printing market share for tableware in 2024, leveraging its mature supply chain and proven color management workflows. Plants values its ability to switch quickly between CMYK and spot colors and to process mixed product heights on a single bed. Continuous software updates extend head life and ink compatibility, making multi-pass a safe capital choice for risk-averse operators. UV LED direct-to-object printing, however, is the rising star, with a forecast 7.19% CAGR. The technology combines one-pass imaging with instant curing, eliminating the need for conveyors and ovens, reducing floor space by as much as 30%, and halving electricity consumption. LED arrays running below 60 °C also enable decoration of thin-wall glassware without heat distortion.

Single-pass inkjet players target very high-volume SKUs such as hotel plate sets, where line speed outruns multi-pass but color-gamut limits remain an obstacle for intricate designs. Dye-sublimation serves polymer dinnerware and coated metals used in outdoor catering, while laser-toner transfer finds niches in boutique studios seeking photographic reproduction on limited editions. Integration middleware aligns all these print streams with ERP order queues, routing each job to the best-fit technology.

By Substrate Material: Ceramic Dominance, Faces Glass Innovation

Ceramic remains the backbone of the digital printing for tableware market, capturing 58.91% share in 2024, thanks to its thermal stability, scratch resistance, and well-established sintering processes. ISO 6486 migration limits for lead and cadmium have been part of quality audits for decades, giving ceramic suppliers clear compliance roadmaps. Yet, glass is the fastest climber, growing at 7.31% annually, as UV LED curing eliminates the need for primer layers and enables low-temperature processing. Premium hotels now commission glass plates etched with location coordinates and augmented reality markers, experiences that ceramic cannot deliver as seamlessly.

Metal substrates, mainly stainless blends, serve a niche market in transport catering where weight and breakage risk outweigh design flexibility. Digitally printed bamboo and wood bowls appeal to eco-lodges; however, adhesion challenges and moisture absorption constraints limit their scalability. Research consortia are exploring plasma-treated biopolymers as alternative surfaces that accept water-based inks while composting at the end of their life cycle, yet commercial release lies beyond the current forecast horizon.

By End User: Foodservice Core, Gifting Upswing

The commercial foodservice channel accounted for 42.37% of the digital printing for tableware market size in 2024. Chain restaurants and contract caterers prioritize brand consistency across hundreds of outlets, which digital workflows deliver without the tooling delays of analog processes. Cloud-connected printers enable synchronized menu rollouts by date, ensuring seasonal motifs launch simultaneously worldwide. Corporate gifting is the fastest riser, with a 7.06% CAGR, as marketers replace plastic trinkets with durable, fully customized mugs and plates bearing QR-linked campaign content. Hotels continue to invest in statement table settings to differentiate premium dining, while institutional operators such as airlines focus on ruggedness and weight reduction, fields in which metal and high-impact polymers retain an edge.

Household demand remains more sporadic, tied to wedding registries and boutique e-commerce sellers offering monogrammed sets. As desktop UV printers fall below USD 20,000, micro-studios enter the market, yet many lack the certification infrastructure to guarantee food-contact safety, limiting their penetration into mainstream retail.

Geography Analysis

Europe commands 33.67% of current revenue, anchored by dense networks of ceramic producers in Italy, Spain, and Germany. Sustainability policies such as the EU Green Deal incentivize water-based inks and energy-efficient curing, aligning digital platforms with regulatory goals. Germany also acts as a technology incubator, housing leading printhead OEMs that iterate velocity and drop-placement algorithms, accelerating local adoption. Southern European design houses leverage centuries-old artisan reputations to launch digitally printed, limited-edition pieces that fetch premium price points.

Asia-Pacific is the momentum engine, delivering a 7.11% CAGR through 2030. China’s consolidation of kilns in Guangdong and Jiangxi provinces creates clusters where shared firing and glazing lines reduce cost per unit. Provincial subsidies for high-efficiency equipment further tilt investment toward digital presses. India’s hotel pipeline includes hundreds of four- and five-star properties, all of which require uniquely branded dinnerware as part of their guest-experience packages. Japan and South Korea, with mature electronics sectors, provide R&D support for next-gen printhead materials and AI-driven nozzle monitoring.

North America holds steady mid-single-digit growth. Quick-service restaurant chains lead demand, applying corporate sustainability scorecards that favor low-VOC inks and traceable supply chains. However, higher labor and energy costs keep some manufacturing offshore, so imports from Mexico and Asia serve a portion of North American demand. The Middle East and Africa experience sporadic but high-value orders linked to luxury resorts, while South America’s growth is closely tied to economic cycles but benefits from local glassware production hubs in Brazil and Argentina.

Competitive Landscape

The digital printing for tableware market is moderately fragmented. Durst, Mimaki, and Canon utilize their industrial inkjet portfolios to provide turnkey ceramic lines, bundling presses, RIP software, and approved ink sets. Specialized firms like Dip-Tech focus exclusively on direct-to-glass systems, while newcomers integrate augmented reality tags that layer digital content over physical plates. Strategic alliances are common: Mimaki’s tie-up with Villeroy & Boch allows for the co-development of hotelware collections that combine heritage ceramic forms with digital motifs. Consolidation trends include Roland’s acquisition of Nazdar’s ceramic ink division, strengthening vertical control over consumables.

R&D pipelines concentrate on low-migration photoinitiators and printheads optimized for curved surfaces. Patent filings for ceramic inkjet climbed 35% in 2024, with Japan and the United States accounting for over half of applications. As the market matures, service models shift toward subscription ink and remote diagnostics to lock in lifetime value. Despite these moves, the top five vendors together hold under 50% of the revenue, signaling ongoing room for regional specialists to exploit niche substrates or localized design languages.

Platform differentiation increasingly hinges on compliance evidence. Vendors submit migration test data against FDA 21 CFR and EFSA thresholds to shorten customer certification cycles. Cloud dashboards aggregate machine telemetry to predict head-cleaning intervals, thereby minimizing downtime for foodservice suppliers operating 24-hour dishroom schedules. White-space areas such as biodegradable substrates and interactive QR-enabled storytelling remain lightly contested, presenting entry points for startups.

Digital Printing For Tableware Industry Leaders

Koenig & Bauer Kammann GmbH

Dip-Tech Digital Printing Technologies Ltd.

Durst Phototechnik AG

Electronics For Imaging Inc.

KERAJET S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: HP released cloud-based predictive-maintenance software for its tableware printers that forecasts head replacement needs 72 hours in advance, cutting unplanned downtime for foodservice suppliers by 25%.

- June 2025: Canon’s Industrial Printing division opened a ceramic ink R&D center in Aichi, Japan, focused on next-generation low-migration photoinitiators compliant with both FDA and EFSA limits.

- April 2025: Mimaki introduced a 10-color UV LED direct-to-glass system rated at 300 m² per hour, geared toward high-volume beverage glass customization in Asia-Pacific breweries.

- February 2025: Durst unveiled its Hawk Eye AI print-quality module for tableware lines, enabling real-time nozzle compensation that reduces scrap by 18% during commercial plate runs.

Global Digital Printing For Tableware Market Report Scope

| Plates |

| Bowls |

| Cups and Mugs |

| Glasses |

| Serveware and Others |

| Inkjet - Single Pass |

| Inkjet - Multi Pass |

| Dye-Sublimation |

| UV LED Direct-to-Object |

| Laser Toner Transfer |

| Ceramic |

| Glass |

| Metal |

| Plastic |

| Bamboo or Wood |

| Household or Residential |

| Commercial Foodservice |

| Hotels and Hospitality |

| Institutional (Airlines, Railways, etc.) |

| Promotional and Corporate Gifting |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Product Type | Plates | ||

| Bowls | |||

| Cups and Mugs | |||

| Glasses | |||

| Serveware and Others | |||

| By Printing Technology | Inkjet - Single Pass | ||

| Inkjet - Multi Pass | |||

| Dye-Sublimation | |||

| UV LED Direct-to-Object | |||

| Laser Toner Transfer | |||

| By Substrate Material | Ceramic | ||

| Glass | |||

| Metal | |||

| Plastic | |||

| Bamboo or Wood | |||

| By End User | Household or Residential | ||

| Commercial Foodservice | |||

| Hotels and Hospitality | |||

| Institutional (Airlines, Railways, etc.) | |||

| Promotional and Corporate Gifting | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of global digital printing for tableware in 2030?

The digital printing for tableware market size is expected to reach USD 0.51 billion by 2030.

Which region shows the fastest growth in adoption of digital tableware printing?

Asia-Pacific posts the highest CAGR at 7.11% through 2030, driven by Chinese and Indian manufacturing and hospitality expansion.

Why are UV LED systems gaining traction in tableware plants?

UV LED direct-to-object printers cure instantly at low temperatures, cut energy use by up to 60%, and enable single-step workflows, boosting productivity for customized glass and ceramic items.

How does digital printing support sustainability targets for hospitality brands?

Water-based and low-migration inks eliminate volatile organic compounds and heavy metals, align with EU and U.S. food-contact regulations, and reduce waste by printing on demand.

What is the main barrier for small potteries to adopt digital printing?

The capital cost of industrial-grade printers, ranging from USD 200,000 to USD 800,000, remains the biggest hurdle, although leasing and equipment-as-a-service models are emerging.

Which product category is growing fastest within digital tableware printing?

Glasses lead growth with a 7.23% CAGR, thanks to UV LED printing that decorates curved surfaces for premium beverage branding.

Page last updated on: