Digital PR Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

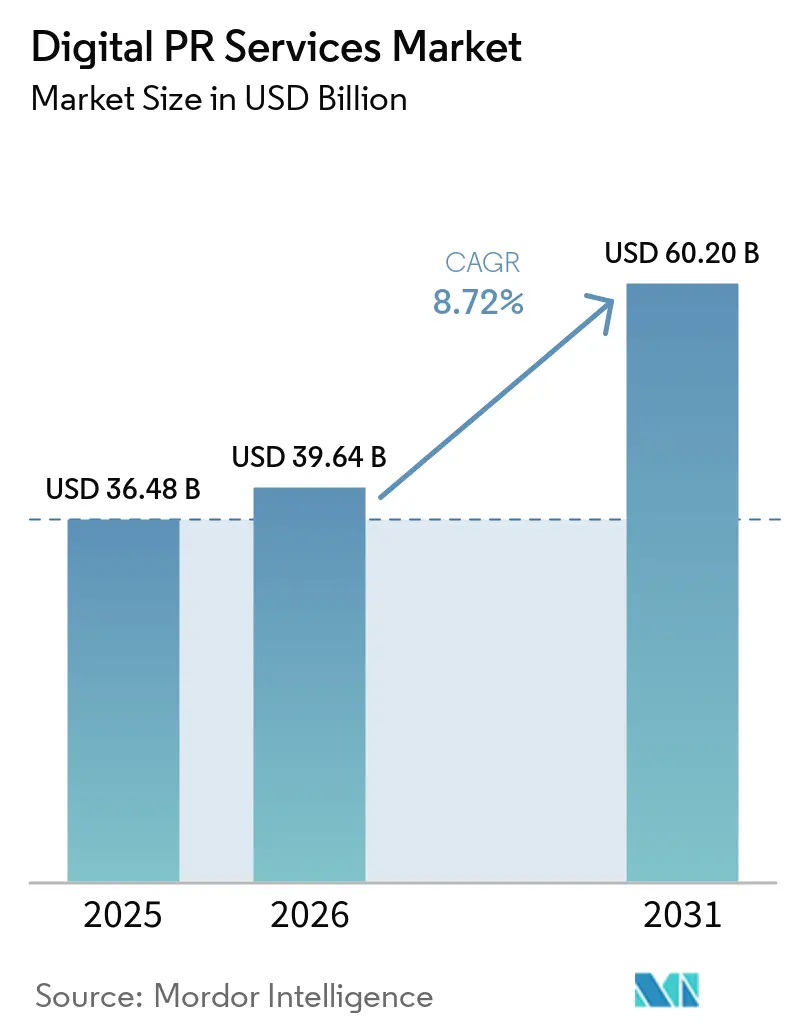

| Market Size (2026) | USD 39.64 Billion |

| Market Size (2031) | USD 60.20 Billion |

| Growth Rate (2026 - 2031) | 8.72% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital PR Services Market Analysis by Mordor Intelligence

The digital PR services market size is projected to be USD 36.48 billion in 2025, USD 39.64 billion in 2026, and reach USD 60.20 billion by 2031, growing at a CAGR of 8.72% from 2026 to 2031. The market is being reshaped by a broad change in how brand authority is built, as earned media, reputation management, and digital visibility now influence discovery across both traditional search and AI-generated answers. Clients are also demanding clearer proof of business value, which is pushing agencies to expand analytics, attribution, and sentiment intelligence instead of relying on legacy retainer logic tied mainly to coverage volume. Competitive behavior is changing at the same time, as large holding companies scale AI and data investments through acquisitions while independent specialists defend their position through vertical expertise, crisis readiness, and GEO-focused delivery models. Regulatory scrutiny around reviews, endorsements, and platform integrity is increasing the value of compliant online reputation management and higher-authority placements. The opportunity set remains broad, but premium growth is moving toward services that combine editorial credibility, measurable outcomes, and faster response to digital trust risks.

Key Report Takeaways

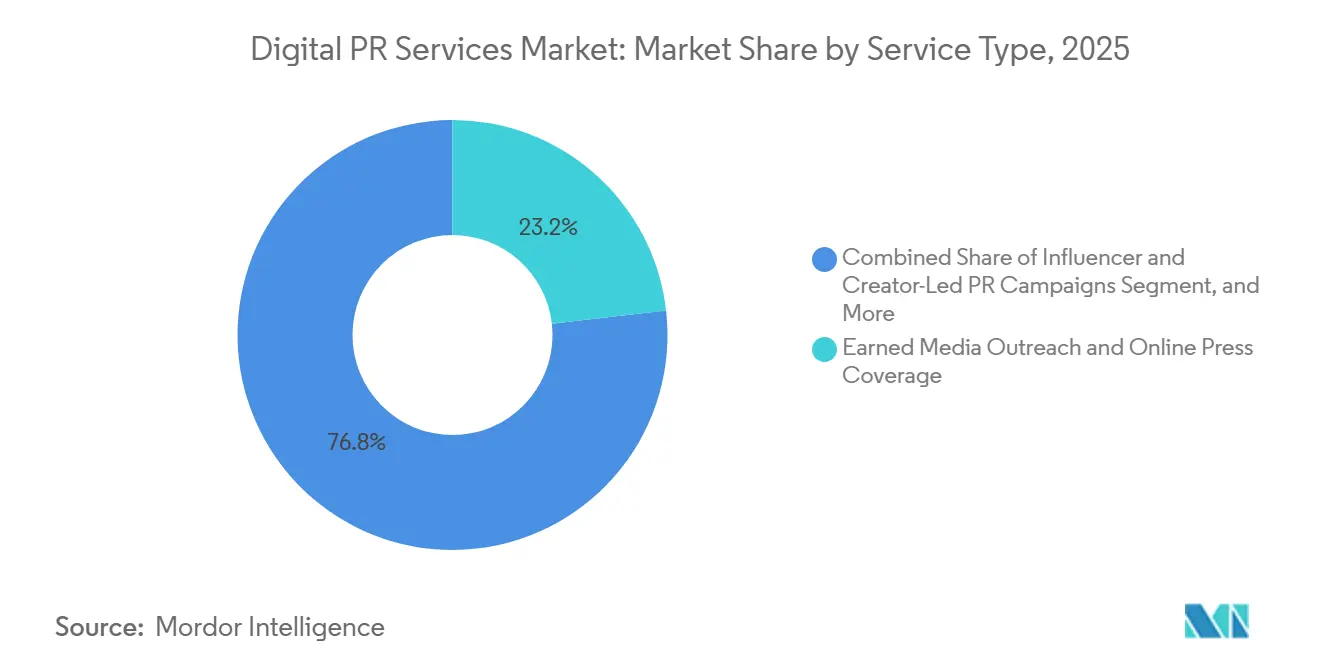

- By service type, Earned Media Outreach and Online Press Coverage held a 23.19% share in 2025, while Measurement, Analytics, and Sentiment Intelligence is projected to expand at a 13.28% CAGR through 2031.

- By client organization size, Large Enterprises held 61.84% share of the digital PR services market in 2025, while Small and Medium Enterprises are projected to expand at an 11.74% CAGR through 2031.

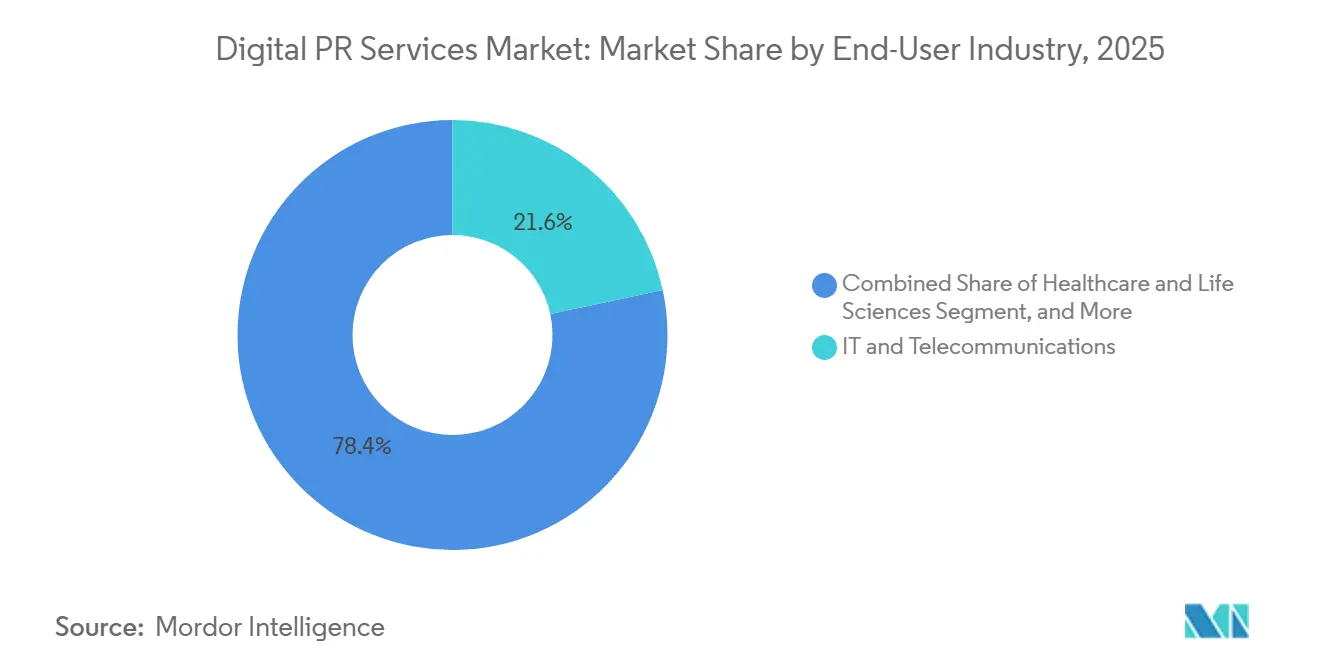

- By end-user industry, IT and Telecommunications accounted for 21.64% share in 2025, while Healthcare and Life Sciences are projected to grow at a 12.19% CAGR through 2031.

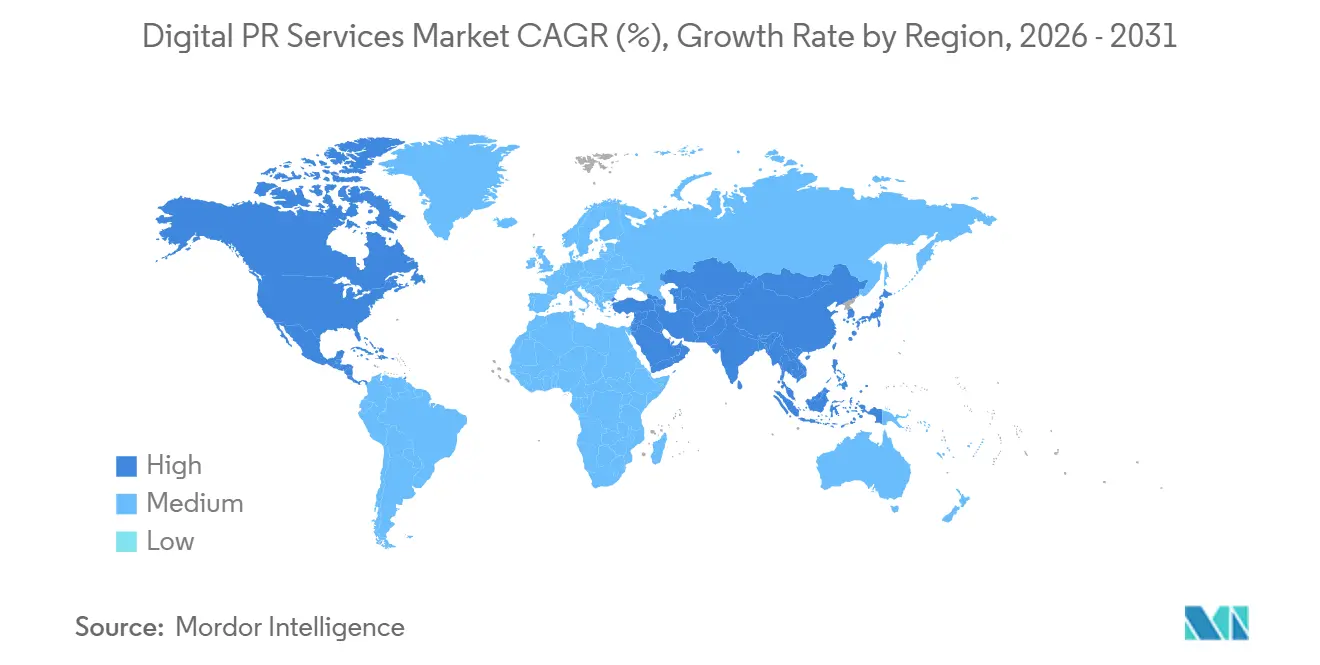

- By geography, North America held 38.32% share of the digital public relations (PR) services market in 2025, while the Asia-Pacific is projected to expand at a 9.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Digital PR Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Online Reputation Management | +1.8% | Global, with strongest pull in North America, Asia-Pacific, and Western Europe | Medium term (2-4 years) |

| Shift of PR Budgets to Digital and Social Channels | +1.6% | Global, led by North America and Europe, accelerating in LATAM and SEA | Short term (≤ 2 years) |

| Growing Influencer and Creator-Led Earned Media Spend | +1.3% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Need for Measurable PR Analytics and Attribution | +1.0% | Global, with highest urgency in North America and Western Europe | Medium term (2-4 years) |

| AI Search and Answer Engine Visibility Becoming a PR Budget Line | +1.2% | Global, most advanced in North America and UK, building in DACH and ANZ | Short term (≤ 2 years) |

| Reddit and Community-Led Discovery Reshaping Earned Media Planning | +0.5% | North America, UK, Australia, with spillover to Asia-Pacific and Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Online Reputation Management

Online reputation management has moved from a discretionary line item to a core operating need across the digital PR services market. The FTC's 2024 anti-fake-review rule made review authenticity a compliance issue, underscoring the need for verified monitoring, documentation, and remediation processes across digital channels.[1]Federal Trade Commission, “FTC Finalizes Rule Banning Fake Reviews,” Federal Trade Commission, ftc.gov That change matters because negative review events now affect not only brand trust but also discoverability on commerce and search platforms. The digital PR services market is therefore seeing stronger demand for always-on monitoring, faster response workflows, and cleaner audit trails that can withstand scrutiny. This pressure is even higher for digital-first brands, where a sudden reputational issue can simultaneously affect traffic, conversions, and visibility. As more brand interaction shifts to social commerce and platform-led buying journeys, the digital PR services market continues to benefit from the expansion of reputation-sensitive surfaces that require constant oversight.

Shift of PR Budgets to Digital and Social Channels

Budget allocation has continued to shift toward digital channels, supporting the digital PR services market. In the IPRN PR Business Survey 2026, 67% of PR agency principals expected business growth in 2026, while AI integration and client budget pressure were cited together as the leading concern by 28% of respondents. That pattern shows that clients are not pulling back evenly across media channels, but are instead protecting digital communications work that can support visibility, engagement, and reputation at once. The launch of WPP Media in 2025 also reflected this broader shift toward AI-powered, integrated media execution, which closely aligns with how large clients now expect communications and performance functions to work together. In the digital PR services market, this creates greater pressure on agencies to deliver stronger content operations, faster workflow speeds, and more precise targeting, rather than relying on legacy pitch volume. It also raises the value of agency relationships and editorial relevance, because inbox competition rises as more budgets move into the same digital channels.

Growing Influencer and Creator-Led Earned Media Spend

Influencer and creator activity now sits closer to mainstream communications planning, widening the scope of the digital public relations (PR) services market. The FTC's updated Endorsement Guides made clear that disclosure expectations apply across a broad set of endorsement formats, including content that uses AI-generated or synthetic personas. This has pushed brands to treat creator-led PR programs less like isolated social experiments and more like managed communications programs that require review, approvals, and documented compliance. The digital PR services market benefits from that shift because agencies can now add disclosure governance, briefing discipline, and creator screening into their service scope. At the same time, creator-led storytelling is blending with executive positioning and thought leadership, especially in sectors where trust and expertise matter more than broad reach alone. That makes the creator's work more valuable when it is tied to message control, sector knowledge, and reputation protection, rather than sold only as audience access.

AI Search and Answer Engine Visibility Becoming a PR Budget Line

AI visibility is becoming a recognized line of work, creating a new demand layer within the digital PR services market. The IPRN PR Business Survey 2026 showed that 41% of PR agencies were building knowledge and running GEO tests, while 15% were already generating revenue from GEO-related work. This change matters because AI-generated answers reward clear entity signals, high-authority references, and consistent third-party coverage, all of which align closely with traditional PR strengths. The digital PR services market is therefore expanding beyond media relations into narrative consistency, source placement quality, and AI-aware reputation architecture. Google's tighter action against site reputation abuse also reinforces the value of stronger editorial quality, because low-trust distribution tactics have become less reliable for achieving visibility. As agencies formalize GEO workflows, the digital PR services market is moving toward a model in which earned visibility and AI discoverability are planned together from the start.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ROI Measurement Fragmentation Across Earned, Social, and Search Outcomes | -1.2% | Global, most acute in North America and Europe where attribution standards are most contested | Medium term (2-4 years) |

| Data Privacy and Influencer Disclosure Compliance Burden | -0.9% | North America, Europe, Australia, with spillover to emerging markets via multinational clients | Short term (≤ 2 years) |

| Google Site Reputation Abuse Rules Weakening Legacy Backlink-First Tactics | -0.7% | Global, concentrated in markets where parasite SEO was most prevalent | Short term (≤ 2 years) |

| AI-Generated Misinformation and Deepfake Crises Raising Verification Costs | -0.8% | Global, with crisis verification costs highest in North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

ROI Measurement Fragmentation Across Earned, Social, and Search Outcomes

Measurement remains a structural challenge for the digital PR services market because earned outcomes, social performance, and search effects still sit in separate reporting systems. This makes it harder for agencies and clients to connect editorial placement with pipeline, conversion, or retention in a way that finance teams consider complete. The digital PR services market is also dealing with a new layer of complexity, as AI-generated answers create another visibility surface that most reporting stacks do not yet measure well. Publicis reinforced its focus on predictive measurement and connected data through major platform investments in 2025 and 2026, demonstrating how seriously large groups are taking this problem. Even so, the digital PR services market still lacks a universal standard that converts reputation, coverage, engagement, and AI presence into one accepted ROI model. Until that gap narrows, some clients will continue to favor channels with cleaner last-click attribution, even when earned strategies offer stronger long-term value.

Data Privacy and Influencer Disclosure Compliance Burden

Compliance obligations are raising delivery costs across the digital PR services market, especially where creator work, user-generated content, and paid amplification overlap. The FTC's revised Endorsement Guides clarified that disclosure rules extend to modern creator formats, including AI-generated and synthetic influencer content.[2]Federal Trade Commission, “Guides Concerning the Use of Endorsements and Testimonials in Advertising,” Federal Trade Commission, ftc.gov That means brands, agencies, and creators all face greater shared risk when disclosures are weak or inconsistent. The digital PR services market now has to account for more legal review, more content checks, and slower campaign deployment, which used to move much faster. The FTC's broader enforcement attention on endorsements and reviews has also made multinational campaign design more complex, because compliance expectations increasingly affect how briefs, approvals, and archiving are handled across markets. This creates barriers for smaller providers and favors agencies that can embed compliance controls into campaign operations without sacrificing speed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Analytics Mandates Change How Agencies Define Value

Earned Media Outreach and Online Press Coverage accounted for 23.19% of the digital PR services market in 2025, making it the largest service block. That position reflects the continued value of credible editorial placement, especially when brands need third-party validation rather than self-published claims. Measurement, Analytics, and Sentiment Intelligence is projected to grow at a 13.28% CAGR from 2026 to 2031, making it the fastest-growing service area in the digital PR services market. This shows a shift away from output-only reporting and toward proof of impact across campaigns, channels, and stakeholder groups. The digital PR services industry is therefore moving from counting placements to linking reputation work with demand signals, AI visibility, and real-time narrative tracking. Search-led digital PR and authority building are benefiting from the same change, because clients want agencies that can explain not only where a story landed but also why it mattered in search and AI environments.

Influencer and Creator-Led PR Campaigns are becoming increasingly integrated with thought leadership and executive positioning in the digital PR services market. That convergence matters because brands increasingly use trusted individuals, not only corporate channels, to carry authority into online discussions and earned media formats. The FTC's updated endorsement rules add a stronger compliance layer to this work, increasing the value of agencies that can manage process discipline alongside creative execution. Social Media PR and Engagement Amplification remains an important operating layer, but platform differences now shape how agencies allocate effort and measure outcomes. In practice, the digital public relations (PR) services market rewards firms that can integrate outreach, creator programs, crisis readiness, and analytics into a single service architecture rather than selling them as isolated tasks.

By Client Organization Size: SME Demand Deepens the Lower End of the Market

Large Enterprises accounted for 61.84% of the digital PR services market share in 2025, indicating that the largest clients still set the spending base for the market. Enterprise demand remains strong because large organizations need multiple service lines at once, including earned media, crisis response, executive positioning, social amplification, and AI-aware visibility work. They also operate across more geographies and stakeholder groups, which makes agency scale, governance, and reporting depth more important. As a result, the digital PR services market continues to give large agencies and networked specialists an advantage in complex, multi-market assignments.

Small and Medium Enterprises are projected to expand at a 11.74% CAGR from 2026 to 2031, making them the fastest-growing client group in the digital PR services market. This change reflects a lower access barrier to monitoring and measurement tools, which lets smaller firms justify ongoing PR spend more easily than before. The digital PR services industry is therefore widening at the lower end, not only through cheaper agency packages but through better software support and more modular delivery models. The result is a larger, more durable addressable base for agencies that can standardize workflows without sacrificing strategic judgment. This also creates a profitability challenge, because SME growth expands volume in the digital PR services market while putting pressure on per-client revenue and making automation more important to delivery economics.

By End-User Industry: Healthcare Adds Premium Demand Through Regulation and Trust

IT and Telecommunications accounted for 21.64% of the digital PR services market in 2025, making it the largest end-user segment. Telecom operators, cloud vendors, software companies, and infrastructure providers all operate in high-noise media environments where brand narratives need constant reinforcement. This keeps PR spending elevated because product launches, policy issues, service disruptions, and competitive messaging all unfold in real time across digital channels. The sector also places high value on thought leadership, executive authority, and sustained analyst and media visibility. For that reason, the digital PR services market continues to draw steady demand from IT and telecom buyers even as service needs become more measurement-driven.

Healthcare and Life Sciences is projected to grow at a 12.19% CAGR from 2026 to 2031, which makes it the fastest-growing end-user segment in the digital PR services market. Growth in this area stems from the growing role of digital channels in healthcare communications and the premium placed on accuracy, trust, and review discipline. The digital PR services industry benefits from this, as healthcare clients often need more specialized process design, stronger approvals, and closer coordination between communications and regulatory teams. That raises the value of agencies with experience in validated messaging and sector-specific crisis workflows rather than broad generalist coverage. It also supports higher retainer levels because the cost of error is higher in health-related communications than in many other end markets.

Geography Analysis

North America held 38.32% of the digital PR services market share in 2025, making it the largest regional bloc. The region benefits from dense agency infrastructure, mature enterprise demand, and faster commercialization of GEO-related services than most other markets. The IPRN survey showed that 15% of agencies were already generating revenue from GEO in 2026, while 41% were still building knowledge and testing, which supports North America's lead in monetizing AI visibility services. The United States remains the center of that shift because it combines large enterprise communications budgets with an advanced ecosystem of analytics, software, and platform partnerships. Canada and Mexico add different strengths to the regional mix, with bilingual communications requirements in Canada and expanding strategic hub activity in Mexico.

Europe remains a large and important part of the digital public relations (PR) services market because agency depth, cross-border brand activity, and digital compliance pressures support sustained demand. The region's regulatory environment places greater emphasis on transparency, governance, and platform responsibility, thereby enhancing the advisory value of PR work focused on reputation, disclosures, and data handling. This tends to favor agencies that can combine communications execution with legal awareness and documented process controls. Europe also matters because it offers mature demand across multiple major economies, rather than relying on a single national center.

Asia-Pacific is projected to grow at a 9.81% CAGR from 2026 to 2031, which makes it the fastest-growing region in the digital PR services market. The region's growth is supported by mobile-first commerce, platform diversity, and the need for multilingual reputation management across very different media systems. In Japan, influencer-driven communications and video production ranked as the top 2 demand-growth categories among PR firms in the PR Companies Report 2025, which shows how quickly digital formats have moved into core communications planning.[3]Public Relations Society of Japan, “PR Companies Report 2025,” Public Relations Society of Japan, prsj.or.jp China, India, and South Korea are also important because each market requires local platform fluency rather than a simple adaptation of Western PR playbooks. That increases the value of local execution depth and makes regional fragmentation a source of demand rather than a barrier.

Competitive Landscape

The digital PR services market is a fragmented specialist tier, and that structure defines the current competitive pattern. Omnicom completed its acquisition of Interpublic Group in November 2025, creating a combined company with pro forma revenue above USD 25 billion and materially increasing scale at the top end of the digital PR services market.[4] Omnicom Group, “Omnicom Completes Acquisition of Interpublic,” Omnicom Group, omc.com That deal strengthened buying power, operating breadth, and the ability to fund shared AI, analytics, and workflow infrastructure across multiple networks. The digital PR services market is therefore seeing a sharper divide between firms that can spread platform costs across very large client books and those that cannot. At the same time, fragmentation persists because clients still value specialist knowledge, fast decision-making, and sector-specific execution that large networks do not always deliver as quickly.

Publicis Groupe continued to build its data and measurement stack through strategic moves tied to connected identity, predictive measurement, and broader AI enablement, including the LiveRamp agreement and the Microsoft expansion announced in 2026. WPP also deepened its operating platform through WPP Media and broader AI deployment, which showed how closely media, analytics, and communications are starting to overlap in the digital PR services market. These moves show that the largest firms are no longer competing only on creative reputation or client rosters. They are increasingly competing on data architecture, AI tooling, and the ability to unify communications with broader marketing intelligence. In the digital PR services market, this raises the bar for enterprise procurement because platform capability is becoming part of agency selection, not just a background advantage.

Independent and mid-market specialists are responding by building narrower, yet more defensible, positions in the digital PR services market. FINN Partners advanced proprietary tools, such as AIristotle and Canary, to strengthen GEO-oriented narrative work and crisis simulation capabilities. Brunswick Group launched its Algorithmic Relations practice, reflecting growing demand for advice that links AI presence, search behavior, and reputation management under one umbrella. MikeWorldWide expanded its reputation advisory capabilities through the HudsonLake acquisition, which added greater depth in organizational change and workforce communications. These moves suggest that the digital PR services market still leaves room for specialists to win by bringing vertical fluency, faster productization, and better alignment with regulated or high-trust sectors. The main white space remains at the intersection of GEO-native earned media, compliance-heavy communications, and premium advisory models that are harder to standardize or automate.

Digital PR Services Industry Leaders

Omnicom Group Inc.

WPP Plc

BlueFocus Intelligent Communications Group Co., Ltd.

Publicis Groupe S.A.

The Interpublic Group of Companies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: MikeWorldWide acquired HudsonLake, a strategic communications firm specializing in organizational change and workforce communications, expanding its corporate reputation advisory across stakeholder groups, including employees and boards; the firm also appointed a Chief Integrated Media and Innovation Officer to unify research, analytics, and creative capabilities.

- May 2026: 5W PR launched a dedicated Defense Practice anchored to GEO and AI citation-share metrics for defense primes, venture-backed defense-tech companies, and aerospace firms, marking the first explicit positioning of AI search visibility as a primary defense-sector PR deliverable.

- April 2026: WPP integrated Google Earth AI into its WPP Open agentic marketing platform, enabling hyper-local demand prediction and automated marketing activation using planetary-scale geospatial intelligence, extending earned media targeting capabilities beyond content and into environmental and behavioral context.

- April 2026: Publicis Groupe and Microsoft expanded their strategic partnership to embed Microsoft Copilot Studio and Microsoft Azure across 114,000+ Publicis employees globally, accelerating the deployment of AI agents across creative production, media planning, and communications workflows.

Global Digital PR Services Market Report Scope

The Digital PR Services Market comprises professional communication, media relations, content promotion, and reputation management services delivered through digital channels to enhance brand visibility, credibility, audience engagement, and online authority. Digital PR services help organizations secure media coverage, improve search engine visibility, strengthen stakeholder relationships, manage brand perception, and support business growth across digital platforms.

The Global Digital PR Services Report is Segmented by Service Type (Earned Media Outreach and Online Press Coverage, Search-Led Digital PR and Authority Building, Thought Leadership Content and Executive Positioning, Influencer and Creator-Led PR Campaigns, Online Reputation Management and Brand Monitoring, Crisis Communication and Reputation Repair, Social Media PR and Engagement Amplification, and Measurement, Analytics, and Sentiment Intelligence), Client Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (Retail and E-commerce, IT and Telecommunications, BFSI, Healthcare and Life Sciences, Media and Entertainment, Travel and Hospitality, Manufacturing and Industrials, Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Earned Media Outreach and Online Press Coverage |

| Search-Led Digital PR and Authority Building |

| Thought Leadership Content and Executive Positioning |

| Influencer and Creator-Led PR Campaigns |

| Online Reputation Management and Brand Monitoring |

| Crisis Communication and Reputation Repair |

| Social Media PR and Engagement Amplification |

| Measurement, Analytics, and Sentiment Intelligence |

| Large Enterprises |

| Small and Medium Enterprises |

| Retail and E-commerce |

| IT and Telecommunications |

| BFSI |

| Healthcare and Life Sciences |

| Media and Entertainment |

| Travel and Hospitality |

| Manufacturing and Industrials |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Service Type | Earned Media Outreach and Online Press Coverage | |

| Search-Led Digital PR and Authority Building | ||

| Thought Leadership Content and Executive Positioning | ||

| Influencer and Creator-Led PR Campaigns | ||

| Online Reputation Management and Brand Monitoring | ||

| Crisis Communication and Reputation Repair | ||

| Social Media PR and Engagement Amplification | ||

| Measurement, Analytics, and Sentiment Intelligence | ||

| By Client Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By End-User Industry | Retail and E-commerce | |

| IT and Telecommunications | ||

| BFSI | ||

| Healthcare and Life Sciences | ||

| Media and Entertainment | ||

| Travel and Hospitality | ||

| Manufacturing and Industrials | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the digital PR services space?

The digital PR services market stood at USD 39.64 billion in 2026 and is forecast to reach USD 60.20 billion by 2031 at an 8.72% CAGR.

Which service area is expanding the fastest in digital PR services?

Measurement, Analytics and Sentiment Intelligence is the fastest-growing service type, projected to grow at a 13.28% CAGR from 2026 to 2031.

Which client group drives the most spending on digital PR services?

Large enterprises led spending with a 61.84% share in 2025, supported by broader needs across earned media, crisis response, analytics, and AI visibility.

Which end-user sector offers the strongest growth opportunity?

Healthcare and Life Sciences is the fastest-growing end-user segment, projected to expand at a 12.19% CAGR through 2031.

Which region leads global demand for digital PR services?

North America held the largest share at 38.32% in 2025, while Asia-Pacific is expected to post the fastest growth at a 9.81% CAGR.

What is changing competition among agencies and holding companies?

Competition is shifting toward AI tools, data platforms, GEO capabilities, and sector specialization, while large groups such as Omnicom, Publicis, and WPP continue to scale through acquisitions and platform investment.

Page last updated on: