Digital Marketing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.76 Trillion |

| Market Size (2031) | USD 1.27 Trillion |

| Growth Rate (2026 - 2031) | 10.91% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Marketing Market Analysis by Mordor Intelligence

The Digital Marketing Market size is projected to expand from USD 0.67 trillion in 2025 and USD 0.76 trillion in 2026 to USD 1.27 trillion by 2031, registering a CAGR of 10.91% between 2026 and 2031. The digital marketing market is moving into a phase where growth is coming from better data use, wider AI deployment, and stronger links between media, content, and commerce. Brands are shifting budgets toward measurable digital formats because campaign planning, audience targeting, and creative testing are now faster and more automated than before. The digital marketing market is also being reshaped by agency consolidation, as larger groups are combining media scale, identity assets, and cloud-based workflow systems to protect margins and deepen enterprise relationships. At the same time, privacy constraints are forcing marketers to rebuild measurement models, which is increasing demand for server-side tracking, incrementality testing, and first-party data services. The digital marketing market, therefore, offers room for both scaled incumbents and AI-enabled challengers, especially where managed services can improve campaign efficiency without matching headcount growth.

Key Report Takeaways

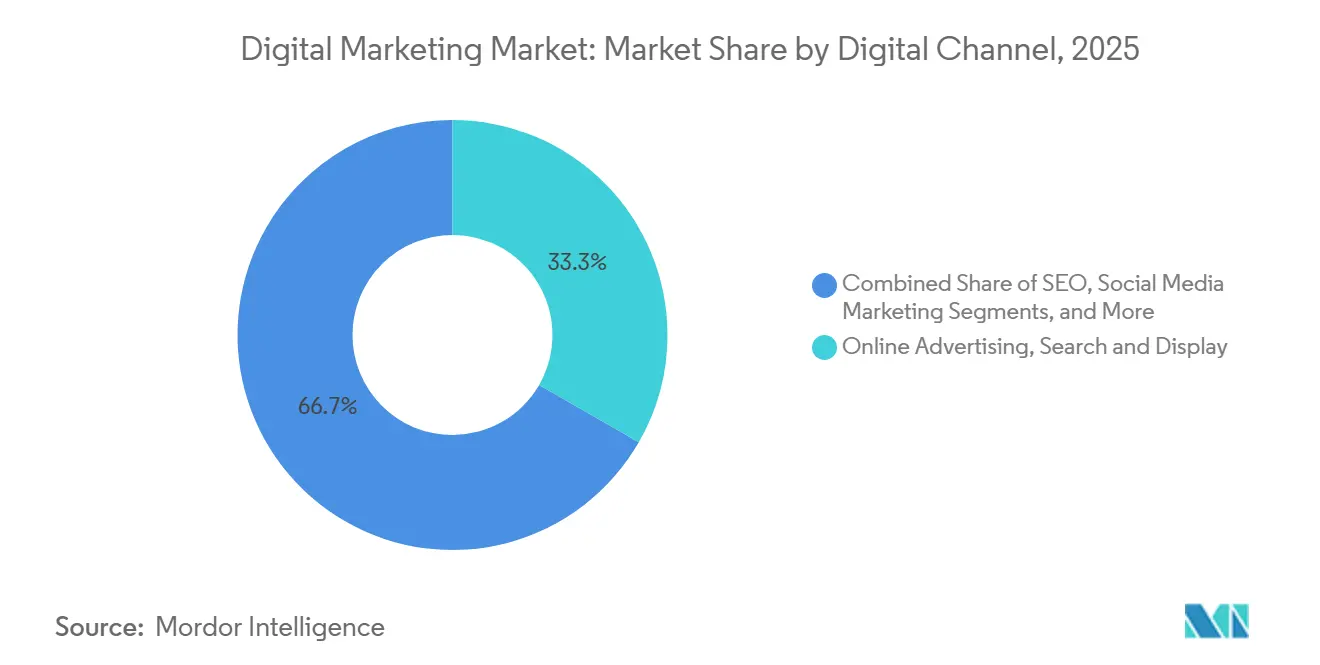

- By Digital Channel, Online Advertising, Search and Display held 33.32% share in 2025, while Influencer Marketing is projected to expand at a 15.13% CAGR through 2031.

- By Enterprise Size, Large Enterprises held 61.64% of the digital marketing market share in 2025, while Small and Medium Enterprises are projected to record the highest CAGR at 15.58% through 2031.

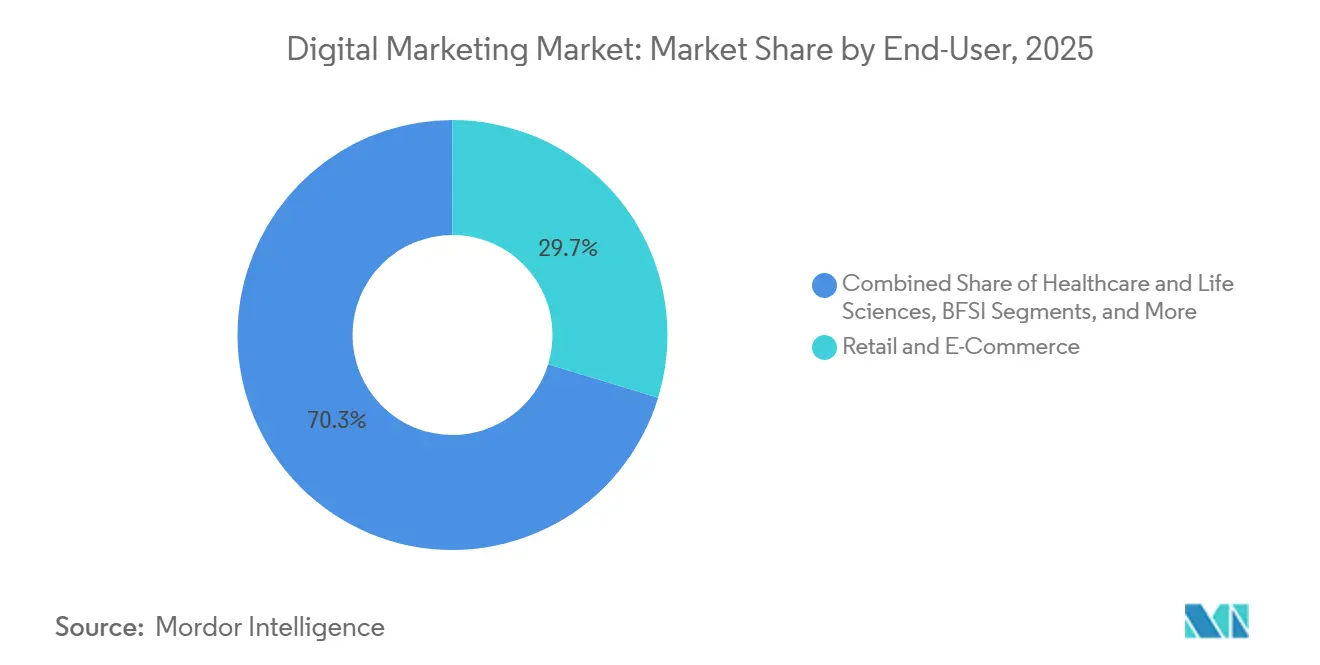

- By End-User Industry, Retail and E-Commerce accounted for 29.71% share in 2025, while Healthcare and Life Sciences are expected to expand at a 14.63% CAGR through 2031.

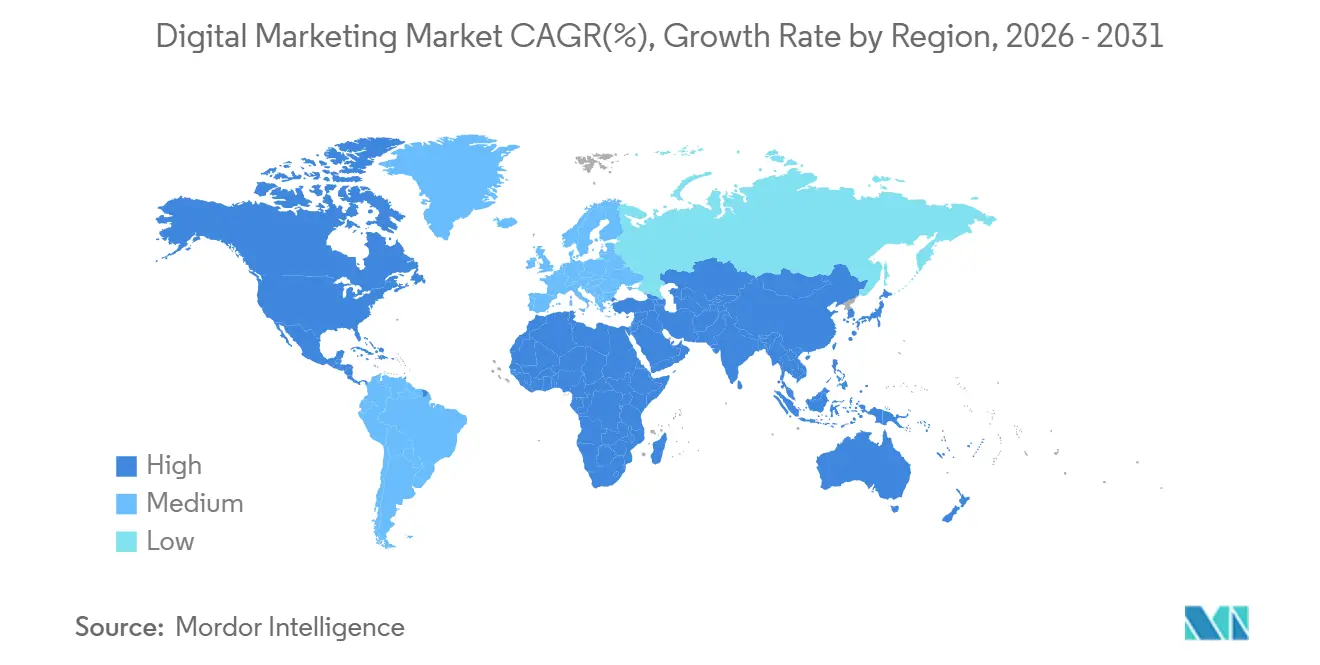

- By Geography, North America held 36.68% share in 2025, while Asia-Pacific is projected to advance at a 16.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Digital Marketing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Shift to AI-Assisted Campaign Planning and Optimization | +2.5% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Rising First-Party Data Adoption Across Walled Gardens | +1.8% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Expansion Of Commerce-Led Social and Creator Marketing | +1.6% | Asia-Pacific core, strong spill-over to North America and EMEA | Short term (≤ 2 years) |

| Growth Of Privacy-Resilient Measurement and Incrementality Testing | +1.2% | North America and EU, emerging across Asia-Pacific | Medium term (2-4 years) |

| Increasing Demand for Vertical-Specific MarTech Workflows | +1.0% | Global, with early adoption in healthcare and BFSI clusters | Long term (≥ 4 years) |

| Convergence Of Marketing Automation With CRM and Customer Data Platforms | +0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift to AI-Assisted Campaign Planning and Optimization

AI-assisted campaign services are changing how the digital marketing market operates because agencies can now deliver planning, testing, and optimization with less manual effort. Large holding groups moved early to scale this shift across their operating systems and client workflows. WPP signed a five-year USD 400 million partnership with Google in October 2025 to integrate generative and agentic AI tools into WPP Open, which strengthened automation across creative and campaign delivery.[1]WPP and Google, “WPP and Google Forge Groundbreaking Partnership to Redefine Marketing with AI,” PR Newswire, prnewswire.com Publicis Groupe expanded its partnership with Microsoft in April 2026 and deployed Microsoft 365 Copilot across more than 114,000 employees while naming Azure as its preferred cloud infrastructure.[2]Microsoft and Publicis Groupe, “Microsoft and Publicis Groupe Expand Their Strategic Partnership to Power the Future of Agentic Marketing for Businesses Worldwide,” Microsoft Source, news.microsoft.com This shift matters in the digital marketing market because service speed, workflow consistency, and data connectivity are becoming as important as traditional creative execution. It also raises entry barriers, since smaller firms can adopt tools, but they still struggle to match enterprise-grade infrastructure, model governance, and integrated client data environments.

Rising First-Party Data Adoption across Walled Gardens

The digital marketing market is seeing stronger demand for first-party data work because brands want more control over targeting, measurement, and customer intelligence. This need has grown as more media spend moves into closed platforms where measurement is strong inside the platform but weaker across channels. IAB reported that digital advertising revenue approached USD 300 billion globally in 2025, and commerce media, the fastest-growing programmatic category, rose 18.0% year over year to USD 63.4 billion. That environment rewards agencies in the digital marketing market that can connect customer data platforms, clean-room workflows, and server-side data pipelines into usable campaign systems. It also changes the client relationship, because advisory work around data ownership now sits closer to budget decisions than standard media execution. As a result, the digital marketing market is capturing more service demand in data architecture, identity resolution, and closed-loop reporting.

Expansion Of Commerce-Led Social and Creator Marketing

Commerce-led creator activity has become a direct growth engine for the digital marketing market, especially where content can move users from discovery to purchase in the same environment. IAB projected that U.S. creator economy advertising spend would rise from USD 37.1 billion in 2025 to USD 43.9 billion in 2026. CreatorIQ also reported that creator content accounted for 44% of brands' paid media creative assets on average, while average creator marketing investment reached USD 6.6 million, and more than 8 in 10 respondents achieved at least 2 times return on investment. These changes are pushing the digital marketing market toward more measurable creator programs rather than one-off brand awareness campaigns. The strongest demand is moving to managed-service models that can source creators, test content, monitor outcomes, and connect conversion data back to media budgets. This shift is especially important in the digital marketing market, where social commerce and retail media are starting to work as connected performance systems.

Growth Of Privacy-Resilient Measurement and Incrementality Testing

The digital marketing market is placing greater value on measurement methods that still work when user-level identifiers are weaker or incomplete. Traditional attribution models have become less reliable as privacy controls reduce the volume and quality of observable conversion signals across devices and platforms. Research published in Future Business Journal in 2026 found that incrementality testing grounded in causal inference outperformed observational attribution in measuring true marketing lift under conditions of identity signal degradation. The Kellogg School of Management also reported that its Predicted Incrementality by Experimentation framework, tested on 2,226 Meta ad experiments, achieved an out-of-sample R² of 0.88 compared with 0.19 for standard seven-day last-click attribution.[3]Kellogg School of Management, “Predicted Incrementality by Experimentation for Ad Measurement,” Northwestern University, kellogg.northwestern.edu That evidence is helping the digital marketing market shift budget authority toward agencies and partners that can run geo-lift tests, model causal outcomes, and validate incremental return with more confidence. It also supports higher-value service engagements because measurement advisory now influences strategy, reporting, and budget allocation across the full campaign cycle.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Signal Loss from Cookie Deprecation and Mobile Privacy Controls | -1.8% | Global, highest impact in North America and Europe | Short term (≤ 2 years) |

| MarTech Stack Fragmentation and Integration Debt | -1.4% | Global, concentrated in enterprises with legacy infrastructure | Medium term (2-4 years) |

| Rising Content, Talent, and Paid Media Costs | -1.1% | North America and Western Europe | Medium term (2-4 years) |

| Measurement Complexity Across Cross-Device and Multi-Touch Interactions | -0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Signal Loss From Cookie Deprecation and Mobile Privacy Controls

Signal loss remains one of the clearest operational limits on the digital marketing market because it reduces visibility across customer journeys and weakens standard attribution setups. Privacy controls across browsers, mobile operating systems, and consent frameworks have made deterministic tracking harder to maintain at scale. The practical effect is that the digital marketing market must spend more on server-side integration, identity stitching, and experimental measurement just to preserve reporting confidence. This adds cost for agencies and clients, and it can slow optimization when data flows are incomplete or delayed. It also creates uneven performance across regions, since compliance requirements and consent behaviors differ by market. Until privacy-resilient measurement becomes more widely standardized, the digital marketing market will continue to face friction in proving campaign impact with older tracking methods.

MarTech Stack Fragmentation and Integration Debt

The digital marketing market also faces a structural drag from fragmented technology stacks that were built over many years through separate point solutions and disconnected workflows. When campaign tools, analytics systems, CRM environments, and data platforms do not work well together, service delivery becomes slower and reporting becomes less consistent. This matters more now because AI-driven campaign systems depend on clean data movement and stable rules across the stack. In the digital marketing market, agencies are often asked to fix these integration issues while also meeting performance targets, which raises delivery complexity and stretches implementation timelines. Clients increasingly prefer partners that can rationalize systems and manage outcomes in one engagement rather than coordinate multiple vendors. That raises the value of transformation-oriented service models, but it also keeps shorter-term execution costs elevated across the digital marketing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Digital Channel: Programmatic Scale Anchors Search And Display While Creator Formats Lead Growth

Online Advertising, Search and Display accounted for 33.32% share of the digital marketing market size in 2025, which kept it as the largest channel in this market. The segment remains central to the digital marketing market because it sits closest to direct response, audience targeting, and measurable conversion activity. Its position is supported by the continued rise of retail media networks and programmatic buying systems that tie exposure to purchase intent. IAB noted that commerce media reached USD 62 billion in 2026 and remained the fastest-growing programmatic subsegment. That pattern supports agency demand in search management, display optimization, retail media activation, and closed-loop reporting. Social Media Marketing and SEO still carry meaningful weight in the digital marketing market because they complement paid acquisition with ongoing traffic capture and content visibility.

SEO is also changing within the digital marketing market as answer-engine behavior pushes agencies to adapt content strategies for AI-led discovery environments. HubSpot stated in April 2026 that customer organic traffic had declined 27% year over year while AI referral traffic tripled, which supported the launch of HubSpot AEO as a distinct service capability. Influencer Marketing is projected to expand at a 15.13% CAGR through 2031, making it the fastest-growing digital channel in the digital marketing market. IAB projected U.S. creator economy ad spend at USD 43.9 billion in 2026, which shows how quickly this channel is moving into core media planning. CreatorIQ added that creator content already represented 44% of paid media creative assets on average, which suggests that creators now influence both media mix and asset production. As a result, the digital marketing industry is allocating more resources to creator sourcing, content testing, and attribution-ready partnership models.

By Enterprise Size: Large Enterprise Spending Anchors the Base as SME Budgets Expand at Speed

Large Enterprises held 61.64% of the digital marketing market share in 2025, which reflects their budget depth, broader data assets, and ability to fund long-term managed-service relationships. Large accounts continue to anchor the digital marketing market because they need multi-country execution, integrated measurement, and shared workflows across paid, owned, and earned channels. Omnicom completed its USD 13.5 billion acquisition of Interpublic in November 2025, creating a larger network with combined revenues above USD 25 billion and deeper media and data capabilities.[4]Omnicom Group, “Omnicom Completes Acquisition of Interpublic, Forming the World’s Leading Marketing and Sales Company,” Omnicom Newsroom, omc.com That move matters in the digital marketing market because it concentrates enterprise budgets within fewer scaled agency relationships. It also reinforces the value of identity assets, centralized buying, and AI-enabled delivery systems for multinational clients.

Small and Medium Enterprises are projected to record a 15.58% CAGR through 2031, which makes them the fastest-growing enterprise-size segment in the digital marketing market. This rise is closely tied to lower-cost automation and easier access to campaign management tools that once favored larger clients. HubSpot expanded its Breeze agent suite and broader AI workflow capabilities in 2026, which signals how platform-led automation is widening access to advanced digital execution. That shift is changing the digital marketing market by moving some SME demand away from classic retainers and toward managed-platform or performance-led service models. SMEs in Asia-Pacific and the Middle East remain especially attractive because they pair growing online commerce activity with expanding digital adoption. This is also one of the clearest areas where the digital marketing industry can add volume growth even as pricing pressure rises in the mid-market.

By End-User Industry: E-Commerce Anchors Structural Spend While Healthcare Attracts Premium Performance Budgets

Retail and E-Commerce held 29.71% of end-use demand in 2025, which made it the largest vertical in the digital marketing market. That leadership reflects the close link between digital spend and transactional outcomes in online retail environments. The U.S. Census Bureau reported that U.S. retail e-commerce reached a USD 326.7 billion quarterly run rate in the first quarter of 2026, up 9.8% year over year. This supports sustained service demand across paid search, shoppable social, retail media, and retention-focused lifecycle marketing. IT and Telecommunications, BFSI, and Media and Entertainment also remain important to the digital marketing market because each relies on data-driven acquisition and channel-specific customer engagement. Their channel choices differ, but they all reward agencies that can combine performance measurement with sector-aware messaging and compliance control.

Healthcare and Life Sciences is expected to expand at a 14.63% CAGR through 2031, making it the fastest-growing end-use vertical in the digital marketing market. The segment is drawing premium budgets because outreach is becoming more targeted, digital-first, and closely measured against patient or prescriber actions. Specialized service models matter more here, since privacy rules and promotional controls raise the cost of generic execution. This creates room in the digital marketing market for agencies that can combine regulated content handling with audience targeting and reporting discipline. Travel and Hospitality, Manufacturing and Industrials, and other end-user industries are also expanding their digital budgets, though at a more moderate pace. Over time, the digital marketing market is likely to see stronger differentiation by vertical expertise rather than by channel capability alone.

Geography Analysis

North America held 36.68% share of the digital marketing market size in 2025, which kept it as the leading regional contributor. The region remains the largest part of the digital marketing market because it combines mature platform adoption, large enterprise budgets, and early investment in AI-enabled campaign systems. The Interactive Advertising Bureau reported that U.S. digital advertising revenue approached USD 300 billion in 2025, while commerce media reached USD 63.4 billion. Canada and Mexico add regional depth, with Mexico benefiting from a growing digitally native consumer base and rising SME use of social and search channels.

Asia-Pacific is projected to grow at a 16.12% CAGR through 2031, making it the fastest-growing geography in the digital marketing market. Dentsu reported that digital media represented 70% of total APAC ad spend, while programmatic grew 24% and outpaced global benchmarks. Dentsu also noted that India’s digital media advertising grew 20% in 2025, while China’s top six platforms posted 6.7% year-over-year growth, led by Douyin or TikTok at 11%. These trends show why the digital marketing market is scaling quickly in mobile-first commerce environments with strong platform integration. In the Middle East, IAB MENA reported that digital advertising reached USD 8.185 billion in 2025, up 17.8% year over year, and that Egypt recorded 23.1% growth.

Europe continues to contribute a material share to the digital marketing market, but growth is shaped by stricter compliance requirements than in most other regions. GDPR enforcement and the EU AI Act are pushing agencies and brands toward more privacy-aware campaign design, consent management, and measurement frameworks. South America is anchored by Brazil, where digital commerce and mobile-led ad activity are supporting broader adoption across performance channels. Africa remains smaller in scale, but the digital marketing market is gaining momentum there as South Africa and Nigeria continue to attract most of the region’s digital advertising investment.

Competitive Landscape

The digital marketing market is moderately consolidated at the top tier, but it remains fragmented across specialists, independent agencies, and regional service providers. Large holding companies compete on media scale, identity assets, and AI-enabled workflow infrastructure rather than on execution capacity alone. Omnicom completed its acquisition of Interpublic in November 2025, creating the world’s largest marketing and sales organization and combining Interpublic’s Acxiom data infrastructure with Omnicom’s Omni intelligence platform. That deal strengthened Omnicom’s position in the digital marketing market by deepening enterprise data access and increasing buying leverage. It also raised pressure on mid-sized firms that do not control comparable data or workflow systems.

WPP and Publicis have responded with platform-led partnerships that show how competition in the digital marketing market is moving closer to cloud, AI, and identity integration. WPP’s five-year USD 400 million partnership with Google in October 2025 expanded access to generative and agentic AI tools across WPP Open. In April 2026, WPP also integrated Google Earth AI geospatial intelligence into WPP Open to support demand prediction and hyper-local campaign execution. Publicis and Microsoft expanded their strategic partnership in April 2026 by combining Copilot deployment, Azure infrastructure, and Epsilon’s identity graph in a full-stack agentic marketing setup.

The digital marketing market is also seeing pressure from consulting-led transformation providers and AI-native service models that compete for workflow redesign, data integration, and automated execution budgets. Adobe reinforced this direction in June 2026 by extending its agentic AI partnerships across AWS, Anthropic, Google Cloud, Microsoft, and OpenAI, with Accenture, Omnicom, WPP, and Code and Theory among the deploying partners. WPP further signaled its competitive intent in June 2026 when it became the first advertising partner to pilot Meta’s AI creative solution inside WPP Open. In this setting, the digital marketing market favors firms that can combine proprietary data, measurable lift, and AI-driven operating efficiency in one client proposition.

Digital Marketing Industry Leaders

Google LLC

Meta Platforms, Inc.

Adobe Inc.

Salesforce, Inc.

WPP plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Adobe announced at Cannes Lions an expansion of its CX Enterprise Coworker and Adobe Marketing Agent across leading AI platforms including AWS, Anthropic, Google Cloud, Microsoft, and OpenAI. Accenture, Omnicom, WPP, and Stagwell's Code and Theory began deploying Adobe's content, data, and AI platforms to transform brand experience creation and measurement at scale, marking a multi-partner activation of cross-platform agentic creative infrastructure.

- April 2026: Publicis Groupe and Microsoft announced an expanded strategic partnership to build a full-stack agentic marketing solution unifying legacy systems, AI agents, and identity-based data. As part of the deal, Publicis deployed Microsoft 365 Copilot across all 114,000-plus employees worldwide, adopted Microsoft Azure as its preferred cloud infrastructure, and integrated Epsilon's consumer identity graph with Microsoft's AI agent layer to deliver personalization at scale.

- April 2026: WPP integrated Google Earth AI geospatial models and datasets into WPP Open, its agentic marketing platform, following its October 2025 Cloud and AI partnership with Google. The integration enables brands to predict demand and automate hyper-local marketing based on planetary-scale geospatial intelligence, representing one of the first commercial applications of Earth AI models in marketing services.

- November 2025: Omnicom Group completed its USD 13.5 billion acquisition of the Interpublic Group of Companies, forming the world's largest marketing and sales organization. The combined entity retained six flagship media networks, OMD, PHD, UM, Initiative, Mediahub, and Hearts and Science, and integrated Interpublic's Acxiom data infrastructure with Omnicom's proprietary Omni AI intelligence platform.

Global Digital Marketing Market Report Scope

The Digital Marketing Market Report is segmented by Digital Channel (SEO, Social Media Marketing, Online Advertising Search and Display, Content Marketing, Email Marketing, Influencer Marketing, Marketing Automation, Digital Customer Engagement Solutions, Analytics and Reporting Tools, and Other Digital Channels), Enterprise Size (Large Enterprises and Small and Medium Enterprises), End-User Industry (Retail and E-Commerce, IT and Telecommunications, BFSI, Healthcare and Life Sciences, Media and Entertainment, Travel and Hospitality, Manufacturing and Industrials, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value in USD.

| Search Engine Optimization (SEO) |

| Social Media Marketing |

| Online Advertising, Search and Display |

| Content Marketing |

| Email Marketing |

| Influencer Marketing |

| Marketing Automation |

| Digital Customer Engagement Solutions |

| Analytics and Reporting Tools |

| Other Digital Channels |

| Large Enterprises |

| Small and Medium Enterprises |

| Retail and E-Commerce |

| IT and Telecommunications |

| BFSI |

| Healthcare and Life Sciences |

| Media and Entertainment |

| Travel and Hospitality |

| Manufacturing and Industrials |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Digital Channel | Search Engine Optimization (SEO) | |

| Social Media Marketing | ||

| Online Advertising, Search and Display | ||

| Content Marketing | ||

| Email Marketing | ||

| Influencer Marketing | ||

| Marketing Automation | ||

| Digital Customer Engagement Solutions | ||

| Analytics and Reporting Tools | ||

| Other Digital Channels | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By End-User Industry | Retail and E-Commerce | |

| IT and Telecommunications | ||

| BFSI | ||

| Healthcare and Life Sciences | ||

| Media and Entertainment | ||

| Travel and Hospitality | ||

| Manufacturing and Industrials | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of digital marketing?

The digital marketing market stood at USD 0.76 trillion in 2026 and is projected to reach USD 1.27 trillion by 2031, growing at a 10.91% CAGR.

Which digital channel leads revenue generation?

Online Advertising, Search and Display led all channels with a 33.32% share in 2025, supported by strong programmatic and retail media demand.

Which channel is growing the fastest through 2031?

Influencer Marketing is projected to post the fastest growth at a 15.13% CAGR, helped by creator-led media and commerce-driven content formats.

Why are first-party data services becoming more important?

Brands need stronger control over targeting and measurement as media spend concentrates inside closed platforms, which is increasing demand for data integration and owned measurement systems.

Which customer group is creating the strongest growth opportunity?

Small and Medium Enterprises are expected to expand the fastest at a 15.58% CAGR, as AI-led tools lower the cost of running advanced campaigns.

Page last updated on: