Digital Cold Chain Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

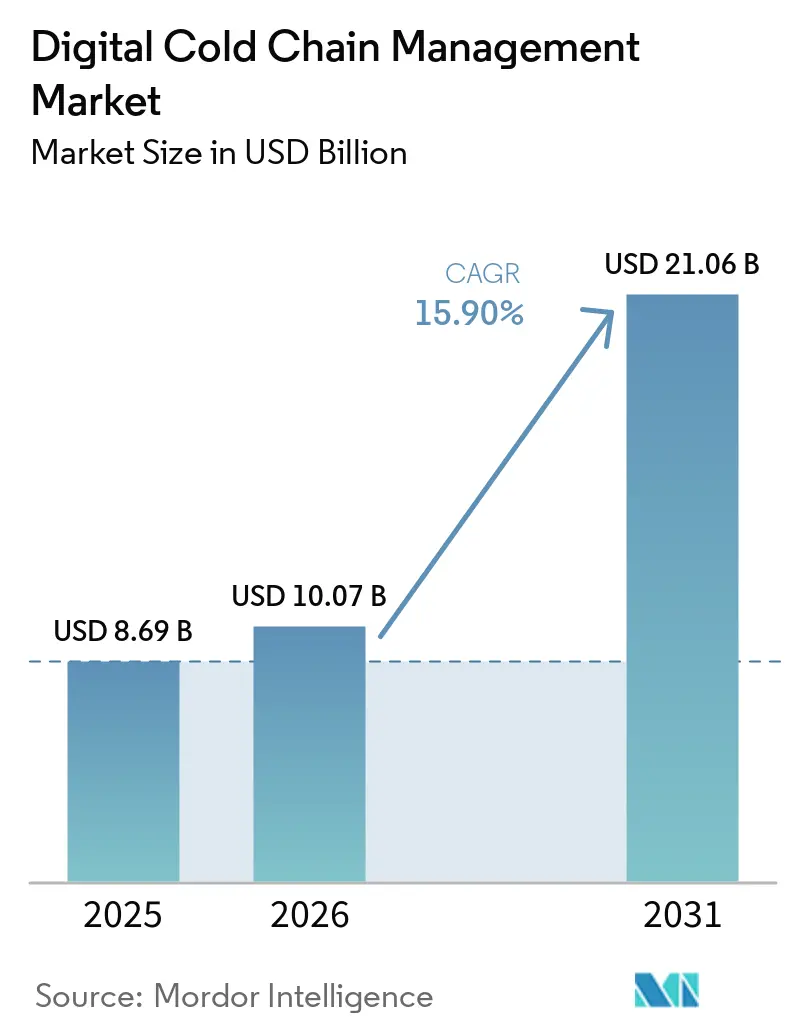

| Market Size (2026) | USD 10.07 Billion |

| Market Size (2031) | USD 21.06 Billion |

| Growth Rate (2026 - 2031) | 15.90% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Cold Chain Management Market Analysis by Mordor Intelligence

The Digital Cold Chain Management Market size is expected to increase from USD 8.69 billion in 2025 to USD 10.07 billion in 2026 and reach USD 21.06 billion by 2031, growing at a CAGR of 15.90% over 2026-2031.

Scaling demand for always-connected sensors, edge gateways, and cloud analytics is reshaping temperature-controlled logistics, replacing manual data logging with real-time visibility networks that capture temperature, humidity, shock, and geolocation data every few minutes. Uptake is strongest where regulators now require auditable electronic records, insurers condition coverage on validated excursion logs, and biologics producers demand proof of thermal integrity for high-value therapies. Hardware shipments remain the largest spending category, yet competitive differentiation has shifted decisively to software platforms that predict excursions, automate corrective workflows, and generate compliance documentation on demand.

Key Report Takeaways

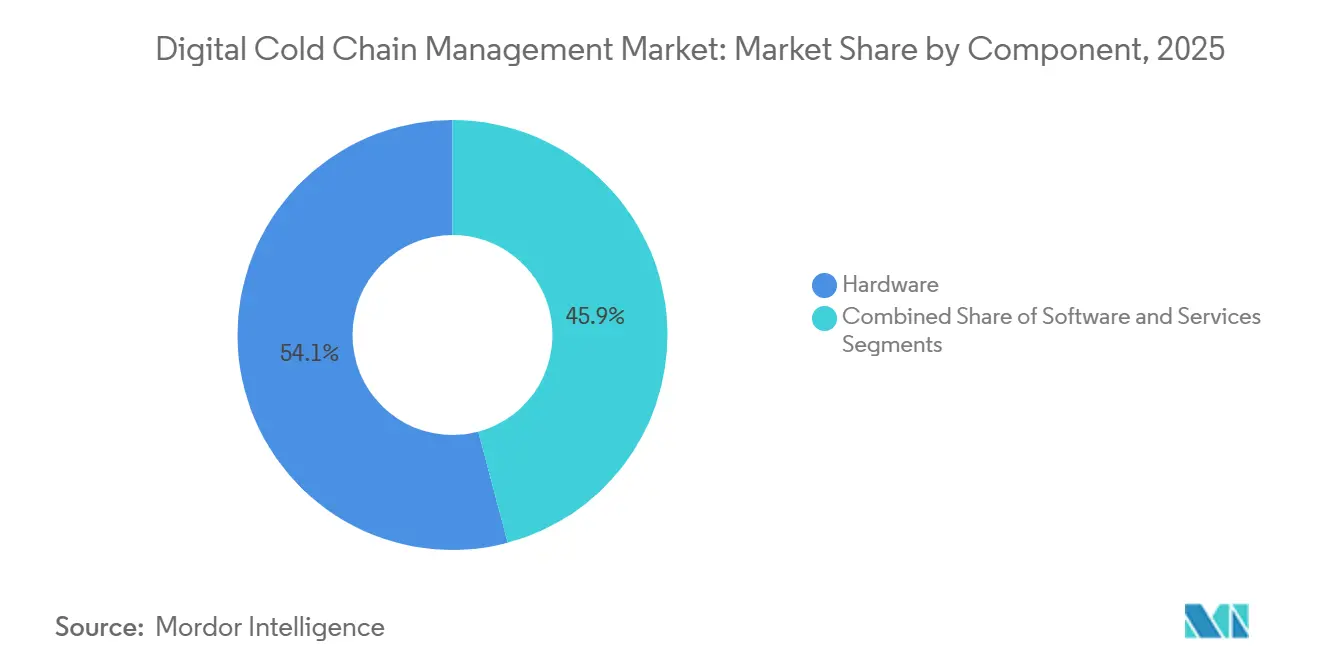

- By component, hardware led with 54.13% of the digital cold chain management market share in 2025, while software is expected to expand at a 16.6% CAGR through 2031, closing the gap between data collection and analytics-driven value creation.

- By temperature range, frozen products accounted for 61.55% of the digital cold chain management market size in 2025, and chilled is projected to advance at a 16.15% CAGR between 2026 and 2031.

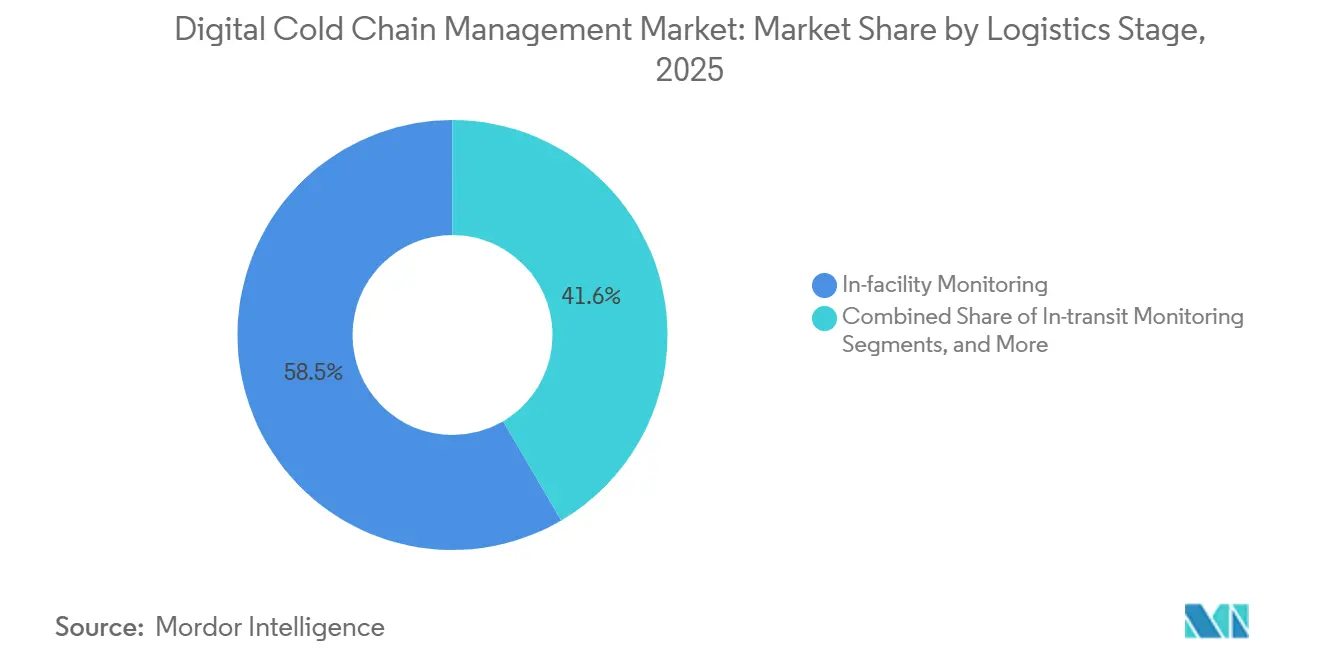

- By the logistics stage, In-facility monitoring held 58.45% of the digital cold chain management market share in 2025, whereas In-transit monitoring is expected to grow at 17.2% CAGR over 2026-2031.

- By end user, pharmaceuticals and healthcare commanded 40.45% of the digital cold chain management market size in 2025 and are expected to post the fastest segment CAGR of 16.95% through 2031.

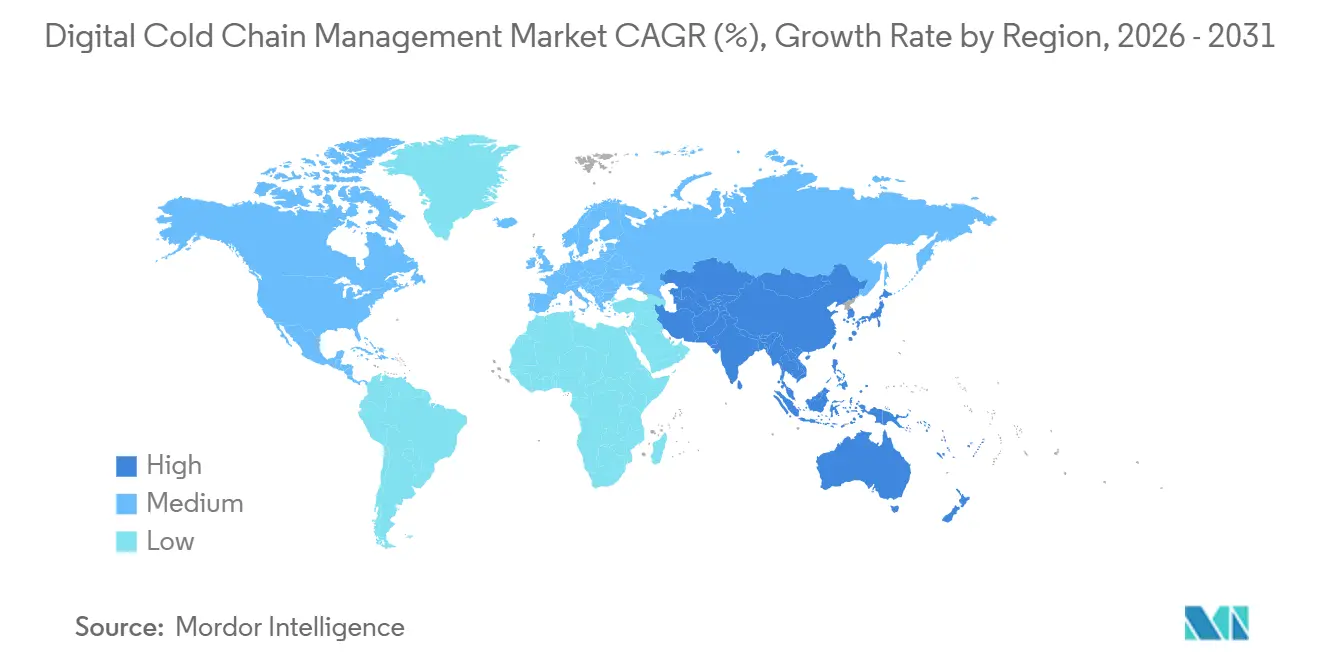

- By geography, North America captured 38.40% of the global digital cold chain management market share in 2025, while Asia-Pacific is projected to grow 17.25% CAGR during 2026-2031 on the back of rapid cold-storage and fleet expansion.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Digital Cold Chain Management Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Compliance-led traceability digitization | +3.2% | Global, peak in NA & EU | Short term (≤ 2 years) |

| Growth in biologics, vaccines, and CGT | +3.5% | Global focus in NA, EU, APAC | Medium term (2-4 years) |

| Food waste and spoilage reduction mandates | +2.4% | Global, EU priority | Short to medium term |

| Cloud analytics and exception automation | +2.0% | Global, fast in NA & APAC | Medium term (2-4 years) |

| Insurer demand for defensible records | +1.2% | NA, EU core | Medium to long term |

| Detached-asset visibility across handoffs | +1.0% | NA, EU spill-over to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Compliance-Led Traceability Digitization

Regulatory timelines have shifted traceability from a best practice to a statutory requirement. The United States Drug Supply Chain Security Act enforced its electronic-data phase in 2025, penalizing up to USD 500,000 for missing serialized records.[1]U.S. Food and Drug Administration, “Food Traceability Rule Key Data Elements,” fda.gov This move spurred enterprises to adopt cloud-connected temperature sensors. Concurrently, the FDA's Food Safety Modernization Act, under "for-cause" inspections since January 2026, mandates that covered foods provide key data within 24 hours, making real-time data acquisition legally essential. The European Union mirrors this urgency, with the General Food Law and the revised Waste Framework Directive endorsing digital record-keeping for verification.[2]European Commission, “Revised EU Waste Framework Directive Targets,” europa.eu These collective mandates amplify compliance risks, bolstering investments in the digital cold chain management market.

Growth in Biologics, Vaccines, and Cell & Gene Therapy Monitoring

Advanced therapeutics are broadening the scope for ultralow and precision-temperature logistics. In 2025, over 4,000 cell and gene therapy candidates were in clinical development, with autologous CAR-T treatments needing temperatures below 135 °C during transit. Given that single doses can surpass USD 500,000, sponsors demand chain-of-identity and chain-of-custody documentation, a feat beyond legacy data loggers. This rigor extends to mRNA vaccines and monoclonal antibodies, which are transported in the 2–8 °C range. Consequently, pharmaceutical shippers are gravitating towards multi-sensor devices that relay data to 24/7 command centers. The combination of high product value, strict stability requirements, and a global trial presence fuels the momentum of the digital cold chain management market.

Food Waste and Spoilage Reduction Mandates

Temperature monitoring is becoming integral to national food-waste goals. The European Union has set binding targets for 2030: a 10% reduction in food waste at production and a 30% cut at retail and household levels. This policy directly promotes real-time spoilage prevention technologies.[3]IntuitionLabs, “Cell & Gene Therapy Logistics Clinical Trial Guide,” intuitionlabs.ai Spain’s Law 1/2025 mandates supply-chain actors to adopt loss-prevention plans by April 2026, with similar laws emerging in South America and Asia.[4]Federal Register, “Traceability Records Compliance Date Extension,” federalregister.gov Continuous telemetry empowers processors and retailers to identify hot spots, reroute at-risk loads, and document preventive measures. This creates a compelling ROI narrative, extending beyond the pharmaceutical sector. As food chains strive to meet waste-reduction targets, the adoption of digital cold chain management solutions accelerates.

Cloud Analytics and Exception Automation

The competitive focus has shifted from mere sensor accuracy to automated decision-making. Cloud-native platforms now aggregate data from various vendors, employing machine-learning models that consider route history, ambient weather, and equipment age. These platforms can autonomously trigger actions. For instance, if predictive engines detect a potential issue, they can direct a carrier to divert a trailer, quarantine specific pallets, or send a technician, reducing response time from hours to mere minutes. Furthermore, automated report generation aids in compliance with GMP, GDP, and FSMA standards, lightening the load for shippers in highly regulated environments. This expansive functionality boosts software subscription value, propelling rapid revenue growth in the digital cold chain management market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High integration and validation costs | -2.1% | Global, acute in EM & SMEs | Short to medium term |

| Legacy-system interoperability gaps | -1.6% | Global, notable in APAC & SA | Medium term (2-4 years) |

| Airline tracker approval blind spots | -0.8% | Global air corridors | Long term (≥ 4 years) |

| Reusable-device return friction | -0.5% | Global, higher in EM last mile | Medium to long term |

| Source: Mordor Intelligence | |||

High Integration and Validation Costs

Enterprise-grade deployments require capital investments exceeding USD 50,000 per distribution center for hardware alone, with additional costs for software validation, such as 21 CFR Part 11 or EU GMP Annex 11. Small and mid-sized distributors often delay full rollouts to avoid penalties for partial compliance, a trend particularly evident in emerging markets where IT budgets fall short of global standards. Legal risks are significant, as demonstrated by a 2025 European court ruling that fined a freight forwarder USD 1.042 million for inadequate temperature records. Despite these risks, the complexity of validation continues to deter adoption. Up-front costs, therefore, moderate the otherwise strong growth potential of the digital cold chain management market.

Legacy-System Interoperability Gaps

Warehouses, carriers, and shippers rely on diverse warehouse management, transport management, and enterprise resource planning platforms that were not designed to handle real-time IoT inputs. This creates data silos, increasing manual reconciliation efforts and the likelihood of errors. The FDA acknowledged these interoperability challenges when extending its FSMA 204 compliance deadline, highlighting a systemic bottleneck. Additionally, the lack of finalized GS1 standards for temperature data exchange forces operators to develop costly custom interfaces. This fragmentation adds 15–20% to IT and compliance costs in multi-vendor sensor environments, presenting significant hurdles to the adoption of digital cold chain management solutions despite the market's growth trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Gains Ground on Hardware

In 2025, hardware accounted for 54.13% of the digital cold chain management market share as operators equipped warehouses, vehicles, and last-mile assets with sensors, RFID tags, and GPS trackers. A 7% annual decline in average sensor prices encouraged widespread adoption, even among cost-sensitive food shippers. Ultra-compact wireless sensors, measuring 19 × 19 × 3.5 mm with 15-year battery lives, reduced total ownership costs. Despite hardware's scale, revenue growth is shifting toward software, expanding at a 16.6% CAGR from 2026 to 2031. Subscription platforms transform raw data into excursion forecasts, auto-generate GDP or FSMA certificates, and integrate route optimization modules that cut fuel costs by up to 8%. As buyers demand deeper analytics, software providers bundle validation services, cybersecurity audits, and carbon-emission dashboards to enhance client retention.

By Temperature Range: Frozen Leads, Chilled Gains Ground

In 2025, the Frozen segment dominated the digital cold chain management market with a 61.55% share, driven by global shipments of frozen proteins, ice cream, and ready meals. Sea freight handled over half of perishable cargo tonnage, and initiatives like Move-to-15 °C aim to save 5% energy by monitoring and enforcing new set-points. The Chilled segment is projected to grow at a 16.15% CAGR, driven by biologics requiring 2 °C to 8 °C storage and rapid-commerce grocers offering one-hour delivery of fresh produce. Chilled loads are riskier due to lower thermal mass, leaving less margin for error. Consequently, pharmaceutical shippers increasingly use redundant multi-probe devices with real-time cloud connectivity, driving demand.

By Logistics Stage: In-Transit Monitoring on the Rise

In 2025, in-facility monitoring held a 58.45% share of the digital cold chain management market, reflecting two decades of warehouse validation regulations. Automated storage and retrieval systems now integrate embedded temperature networks, reducing retrofitting costs. However, in-transit monitoring is expected to grow at a 17.2% CAGR as 25% of temperature excursions occur during transit, with last-mile deliveries contributing significantly to spoilage. Telemetry devices that switch between cellular and satellite links ensure coverage across cold-chain "black holes" like transoceanic air routes. Regulators increasingly require shipment-level data, driving unit volumes. Carriers adopting dynamic ETA models that use real-time sensor inputs to adjust routes proactively are boosting device installations across trucks, containers, and boxes, benefiting the digital cold chain management market.

By End User: Pharmaceuticals Drive Scale and Growth

In 2025, Pharmaceuticals and Healthcare accounted for 40.45% of the digital cold chain management market, reflecting the sector's stringent compliance requirements and high-value stakes. Annual losses from temperature excursions, estimated at USD 35 billion, drive investment in validated monitoring systems. This segment is projected to grow at a 16.95% CAGR through 2031. The commercialization of cell and gene therapies, biosimilar launches, and home-delivery expansion demand greater visibility. While the Food and Beverage sector leads in device volume due to time-temperature indicators on supermarket pallets, its revenue per unit is lower than pharmaceuticals. The rise of direct-to-patient prescription models and decentralized clinical trials expands the market for small, high-value shipments, reinforcing the pharmaceutical sector's dominance in the digital cold chain management market.

Geography Analysis

In 2025, North America commanded a dominant 38.40% share of the digital cold chain management market. Strict regulations, such as DSCSA and FSMA, require serialized and temperature-verified records from manufacturers to dispensers, driving rapid sensor adoption in pharmaceuticals and high-risk food sectors. Leading cold-storage operators are investing in AI-driven yard management systems to ensure pallets on docks remain within required specifications. Europe, holding the second position, integrates traceability with sustainability. The resumption of on-site GDP inspections in 2025, coupled with national food waste laws, is pushing distributors toward unified monitoring platforms that streamline cross-border compliance. In January 2025, the United Kingdom updated its GDP guidance under the Windsor Framework to align with EU standards, ensuring continuity for pan-European logistics providers.

Asia-Pacific is set to surge at a robust 17.25% CAGR from 2026 to 2031, driven by large-scale infrastructure projects and supportive policies. By 2025, China's cold storage capacity exceeded 277 million m³, and its refrigerated truck fleet grew 19% year-on-year to 587,900 units, reflecting rising demand for in-vehicle telematics. In India, government funding through the Pradhan Mantri Kisan SAMPADA Yojana is modernizing rural cold storage facilities. Southeast Asian e-commerce grocers are investing in last-mile sensor networks to ensure product freshness. Latin American exporters, particularly in avocados, berries, and seafood, are increasingly adopting measures to comply with U.S. FSMA requirements, especially for export lanes. In the Middle East, IoT-enabled reefer parks near port free zones are safeguarding perishables destined for Africa, highlighting the global scope of opportunities in the digital cold chain management market.

Competitive Landscape

In 2025, the seven largest vendors in the digital cold chain management market collectively accounted for about 24% of the revenue, highlighting a moderately fragmented landscape. With sensor commoditization accelerating, hardware margins are shrinking. To counter this, device manufacturers are bundling cloud dashboards and analytics subscriptions tied to warranties. Software-centric companies command premium valuations due to recurring revenue models and high switching costs associated with platforms validated to standards like 21 CFR Part 11, EU Annex 11, and ISO 27001.

Competitive energy flows into insurance-technology convergence. For instance, Zebra Technologies partnered with Overhaul in April 2025 to integrate environmental sensors into a risk-management system capable of automatically initiating cargo-insurance claims after verified incidents. This demonstrates a growing revenue opportunity in the digital cold chain management market. Vendors differentiate through edge analytics that maintain cold box compliance during connectivity gaps and multi-modal tracking that seamlessly transitions data from warehouses to vehicles and parcel lockers. Strategic acquisitions and alliances drive growth. Examples include ORBCOMM's debt-funded expansion of its VIACHAIN platform and the 2026 partnership between SpotSee and Controlant, reflecting active capital deployment to secure first-mover advantages in niche software markets. As customer expectations shift from compliance to carbon reporting and shelf-life forecasting, suppliers capable of managing data across the entire custody chain are best positioned to lead the next phase of growth in the digital cold chain management market.

Digital Cold Chain Management Industry Leaders

ORBCOMM

DeltaTrak

Zebra Technologies

Cold Chain Technologies

Berlinger & Co. AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: SpotSee and Controlant launched a joint solution combining real-time trackers with indicator labels to cut pharmaceutical returns by up to 90%.

- February 2026: Kaleris released ColdLink, fusing TMS, YMS, and IoT data to automate “hot moves” for temperature-at-risk trailers and generate FSMA-compliant documentation.

- February 2026: DeltaTrak introduced FlashLink NOW loggers integrated with UBQ Network to provide cargo insurance triggers, carbon metrics, and shelf-life prediction in a single device.

- January 2026: ORBCOMM closed a USD 460 million refinancing with Carlyle, Bain Credit, and Morgan Stanley Private Credit to scale its VIACHAIN supply-chain intelligence platform.

Global Digital Cold Chain Management Market Report Scope

As per the scope of the report, digital cold chain management is the technology-driven process of ensuring the integrity, safety, and temperature control of sensitive products (foods, pharmaceuticals) throughout the supply chain. It utilizes IoT sensors, real-time data analytics, and automated alerts to monitor, track, and maintain specific environments from production to final delivery.

The digital cold chain management market is segmented by component, temperature range, logistics stage, end-user, and geography. By component, the market includes hardware, software, and services. By temperature range, the market is segmented into chilled, frozen, ultra-low and cryogenic, and controlled ambient. By logistics stage, the market is categorized into in-facility monitoring, in-transit monitoring, last-mile monitoring, and returnable asset and packaging monitoring. By end-user, the market is segmented into food and beverage, pharmaceuticals and healthcare, chemicals and specialty materials, third-party logistics and cold storage operators, and retail, e-grocery, and quick commerce. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Hardware |

| Software |

| Services |

| Chilled |

| Frozen |

| Ultra-low and Cryogenic |

| Controlled Ambient |

| In-facility Monitoring |

| In-transit Monitoring |

| Last-mile Monitoring |

| Returnable Asset and Packaging Monitoring |

| Food and Beverage |

| Pharmaceuticals and Healthcare |

| Chemicals and Specialty Materials |

| Third-party Logistics and Cold Storage Operators |

| Retail, E-grocery, and Quick Commerce |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Temperature Range | Chilled | |

| Frozen | ||

| Ultra-low and Cryogenic | ||

| Controlled Ambient | ||

| By Logistics Stage | In-facility Monitoring | |

| In-transit Monitoring | ||

| Last-mile Monitoring | ||

| Returnable Asset and Packaging Monitoring | ||

| By End User | Food and Beverage | |

| Pharmaceuticals and Healthcare | ||

| Chemicals and Specialty Materials | ||

| Third-party Logistics and Cold Storage Operators | ||

| Retail, E-grocery, and Quick Commerce | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the digital cold chain management market be by 2031?

The digital cold chain management market size is projected to reach USD 21.06 billion by 2031, reflecting a 15.9% CAGR over 2026-2031.

Which component of the digital cold chain management market is growing fastest?

Software is expected to register the highest component CAGR at 16.6%, thanks to demand for predictive analytics, automated reporting, and integration with route optimization engines.

Why is pharmaceuticals the leading end user for digital cold chain solutions?

Pharmaceuticals and Healthcare controlled 40.45% of the market size in 2025 and are projected to have the fastest growth because biologics, vaccines, and cell-and-gene therapies require validated, always-on temperature monitoring.

What is driving Asia-Pacific growth in digital cold chain management?

Rapid expansion of cold storage capacity, a 19% rise in China's refrigerated truck fleet, and government incentives such as India's SAMPADA program support a 17.25% CAGR in the region.

How are regulations influencing technology adoption?

U.S. DSCSA and FSMA rules, along with EU waste-reduction mandates, now require digitized temperature and traceability records, pushing companies to adopt real-time IoT monitoring platforms.

What emerging feature sets differentiate leading vendors?

Platforms offering chain-of-custody validation, AI-based excursion prediction, automated insurance claims, and carbon-emission analytics are gaining competitive advantage within the digital cold chain management market.

Page last updated on: