Dermatology Contract Research Organization (CRO) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

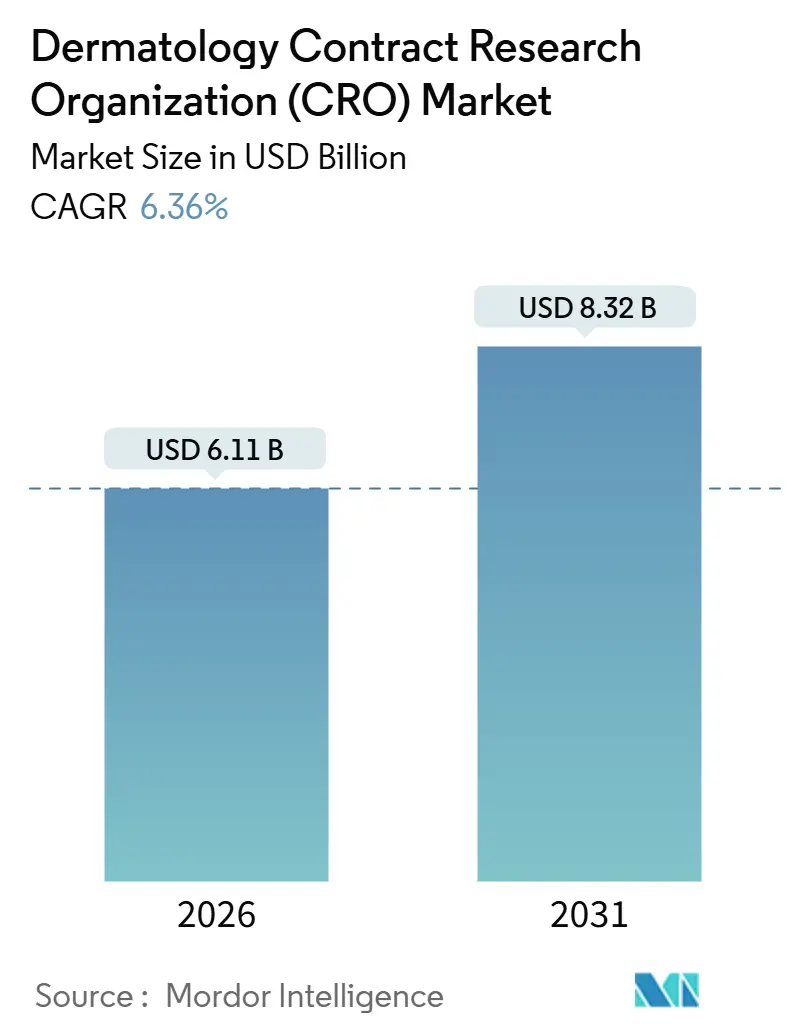

| Market Size (2026) | USD 6.11 Billion |

| Market Size (2031) | USD 8.32 Billion |

| Growth Rate (2026 - 2031) | 6.36% CAGR |

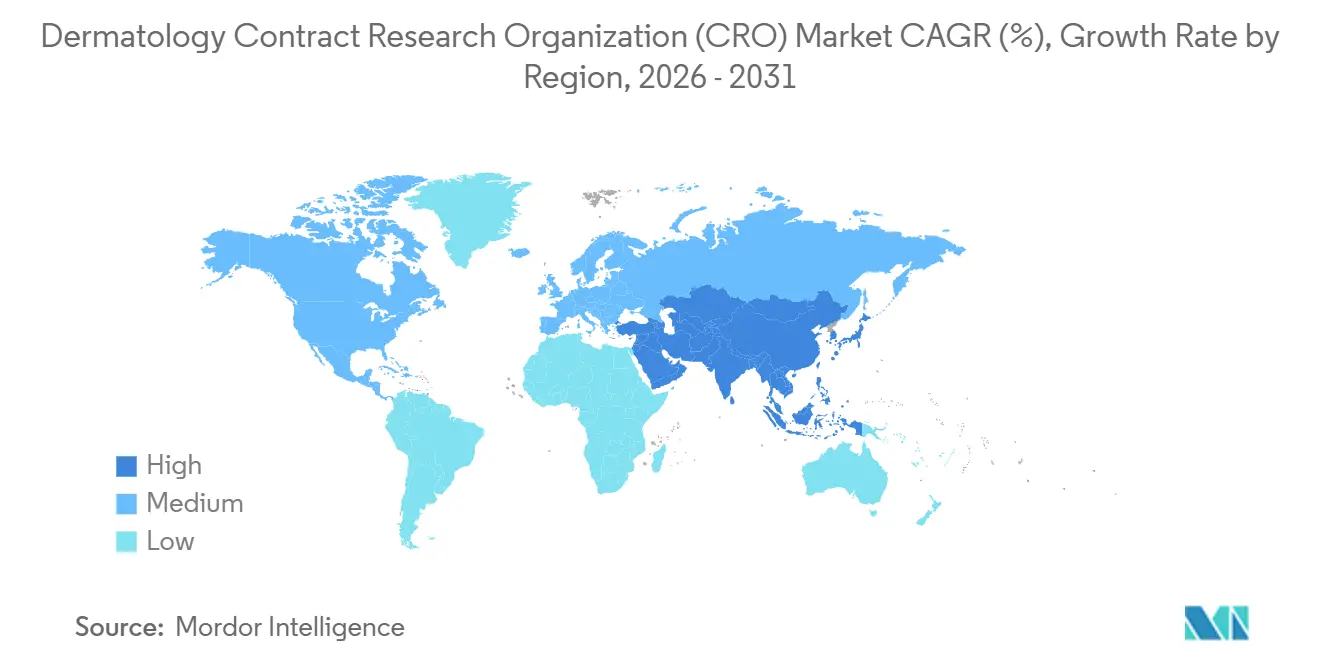

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dermatology Contract Research Organization (CRO) Market Analysis by Mordor Intelligence

The Dermatology Contract Research Organization Market size is estimated at USD 6.11 billion in 2026, and is expected to reach USD 8.32 billion by 2031, at a CAGR of 6.36% during the forecast period (2026-2031).

Rising reliance on specialist contract research organizations, the FDA’s readiness to accept rigorously validated imaging and patient-reported endpoints, and steady biologics launches in psoriasis, atopic dermatitis, and vitiligo keep the Dermatology CRO market on a robust growth path. Sponsors now favor external partners that bring pre-negotiated investigator networks, disease-specific electronic data-capture templates, and global regulatory know-how. Strategic partnerships such as LEO Pharma’s 2023 deal with ICON plc allow innovators to embed CRO competencies directly into their development roadmaps, shaving three to six months off pivotal-trial timelines. Regulatory tailwinds are equally decisive: the FDA’s April 2025 approval of ZEVASKYN gene therapy for recessive dystrophic epidermolysis bullosa, granted after a 31-patient single pivotal study, showcased how credible endpoints can shorten reviews, strengthening the business case for outsourcing to niche CROs that master protocol design.

Key Report Takeaways

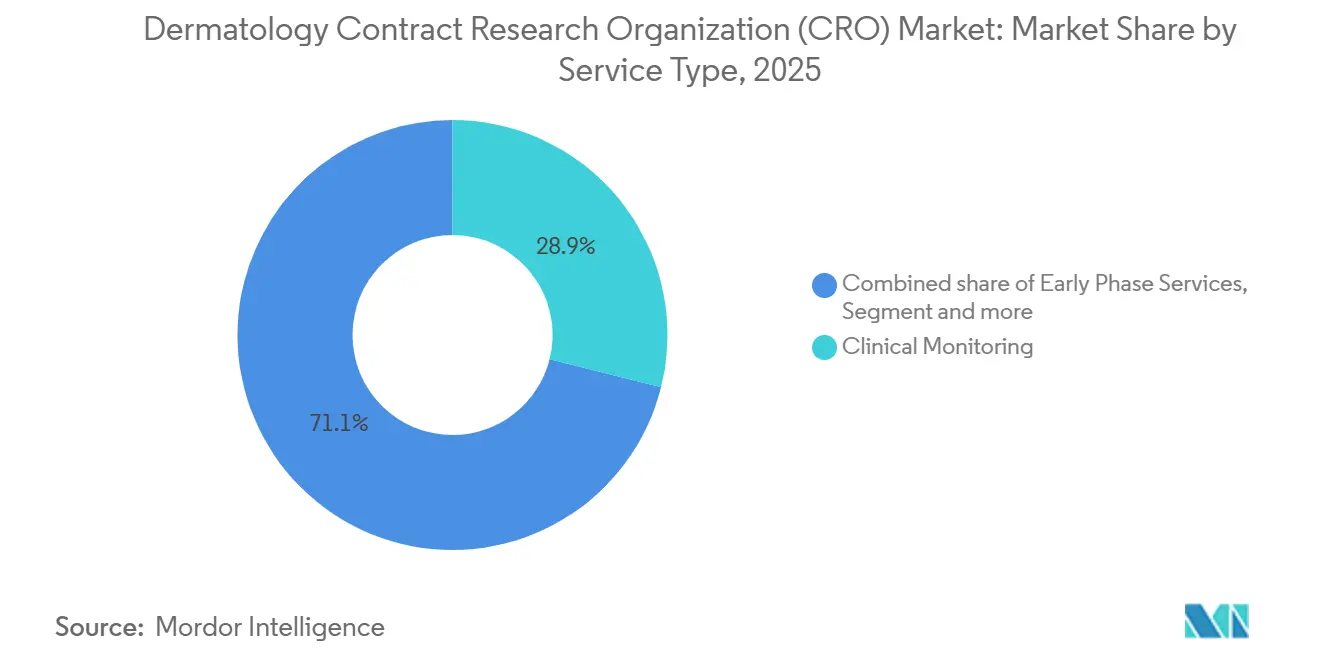

- By service type, Clinical Monitoring led with 28.9% revenue share in 2025, whereas Pharmacovigilance is expected to expand at a 6.78% CAGR to 2031.

- By clinical phase, Phase III accounted for 37.8% of the Dermatology Contract Research Organization (CRO) market share in 2025, while Phase I is forecast to grow at a 6.88% CAGR through 2031.

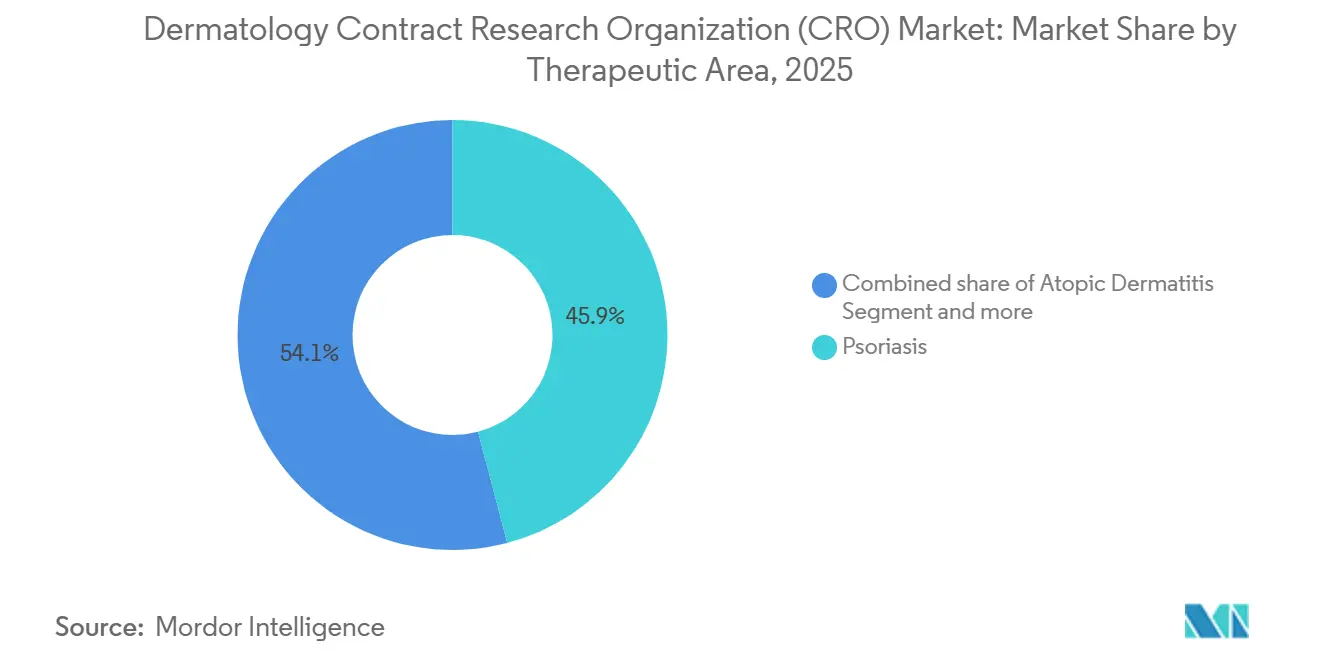

- By therapeutic area, psoriasis retained 45.9% share in 2025, but vitiligo is projected to advance at a 6.98% CAGR during the same horizon.

- By sponsor type, pharmaceutical companies captured 46.8% share in 2025, while medical device and diagnostic companies are set to post the fastest 7.09% CAGR to 2031.

- By geography, North America commanded 46% of 2025 revenue, yet Asia-Pacific is on track for a 7.50% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dermatology Contract Research Organization (CRO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outsourcing Surge Among Dermatology Drug Sponsors | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Rising Global Prevalence of Chronic Skin Diseases | +1.5% | Global, particularly APAC and MEA due to underdiagnosis | Long term (≥ 4 years) |

| Regulatory Incentives for Novel Dermatology Drugs | +0.9% | North America & EU, spill-over to APAC | Short term (≤ 2 years) |

| Cost-Reduction Via Specialist CRO Partners | +1.0% | Global, early gains in North America | Medium term (2-4 years) |

| Decentralized & Hybrid Dermatology-Trial Adoption | +0.8% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| AI-Powered Digital-Imaging Endpoints Standardization | +0.7% | North America & EU core, APAC adoption accelerating | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Outsourcing Surge Among Dermatology Drug Sponsors

Pharmaceutical developers are dismantling fixed clinical-operations teams and pivoting to flexible outsourcing models. LEO Pharma’s multiyear alliance with ICON plc illustrates how sponsors blend operational execution with therapeutic-area insight to de-risk late-stage psoriasis and atopic dermatitis pipelines [1]ICON plc, “LEO Pharma Strategic Partnership,” iconplc.com. Gilead’s 2025 collaboration with LEO Pharma on a STAT6 inhibitor shows that co-development deals also transfer shared CRO networks, compressing start-up times. Even consumer-health players such as Beiersdorf now rely on academic-CRO consortia to tackle prescription dermatology opportunities. As talent migrates from in-house teams to CRO employers, specialized providers deepen expertise, reinforcing the outsourcing cycle. The Dermatology CRO market, therefore, benefits from a virtuous loop in which sponsors shed overhead while CROs scale capabilities.

Rising Global Prevalence of Chronic Skin Diseases

Worldwide psoriasis cases have risen to roughly 60 million, and vitiligo affects an estimated 28.5 million people, with Asia-Pacific recording the steepest growth as diagnostic infrastructure expands. Atopic dermatitis incidence has climbed 30% in major APAC cities since 2020, broadening trial-eligible cohorts for systemic biologics and topical Janus kinase inhibitors. GLOBOCAN logged more than 1.5 million annual non-melanoma skin cancer cases in 2024, fueling post-approval safety-study demand. Large, underserved populations give CROs fertile ground for multi-regional enrollment strategies that blend cost-efficient Asia-Pacific sites with U.S. and EU pivotal centers. Heightened disease prevalence, therefore, adds at least 1.5 percentage points to the Dermatology CRO market CAGR through 2031.

Regulatory Incentives for Novel Dermatology Drugs

The FDA’s orphan designation and subsequent approval in 2025 cut typical review times by up to 12 months, slashing development budgets by nearly one-third. Cosibelimab won clearance for cutaneous squamous-cell carcinoma in 2024 via a single-arm Phase II study, illustrating flexibility for immuno-oncology dermatology assets. EMA alignment on vitiligo, shown by its 2024 ruxolitinib endorsement, signals converging regulatory expectations that simplify global filings. CROs with permanent FDA-EMA liaison teams command premium fees for shepherding expedited pathways. Resulting sponsor savings feed back into higher outsourcing volumes, reinforcing Dermatology CRO market expansion.

Cost-Reduction Via Specialist CRO Partners

Dermatology-focused CROs cut per-patient costs significantly versus generalists through pre-negotiated site rates, reusable ePRO templates, and disease-specific imaging algorithms. ICON reports a 40% faster site-activation cycle within its dermatology center of excellence. Innovaderm’s registries drop screen-failure rates below 20%, yielding six-figure savings per pivotal trial. Savings are largest in Phase III, where site payments dominate budgets, making cost leadership a durable driver for the Dermatology CRO market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Pressure from Intense CRO Competition | -0.6% | Global, most acute in North America & Europe | Short term (≤ 2 years) |

| Complex, Region-Specific Topical-Trial Regulations | -0.4% | EU & APAC, fragmented national requirements | Medium term (2-4 years) |

| Scarcity Of Validated Dermatology Biomarkers | -0.5% | Global, limiting precision-medicine trials | Long term (≥ 4 years) |

| Patient-Privacy Concerns Over Remote Skin Images | -0.3% | EU (GDPR) & North America (HIPAA), emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Pressure from Intense CRO Competition

Sponsors today canvass five to seven bids for mid-size dermatology studies, trimming average CRO gross margins to around 23%. IQVIA’s late-2024 purchase of Citeline is a strategic move to bundle regulatory intelligence with execution, helping justify premium quotes. Phase III projects remain margin-protective because switching providers mid-trial is risky, but early-phase work has commodity-type pricing. CROs are responding with multiyear, end-to-end packages that trade reduced unit economics for guaranteed volume, yet the tactic drags EBITDA and moderates Dermatology CRO market growth by roughly 0.6%.

Complex, Region-Specific Topical-Trial Regulations

The EMA’s demand for dermatopharmacokinetic tape-stripping studies, China’s 50% local-subject quota, and India’s tropical stability testing add USD 200,000–400,000 and six to nine months to program timelines [2]European Medicines Agency, “Topical Bioequivalence Guidance,” ema.europa.eu. Japan’s mandatory photosafety tests further fragment global development paths. Sponsors with limited capital restrict their geographic scope, lowering CRO addressable revenue and shaving 0.4 percentage points off the Dermatology CRO market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Pharmacovigilance Gains as Biologics Mature

Clinical Monitoring generated the largest slice of 2025 revenue, representing 28.95% of the Dermatology Contract Research Organization (CRO) market size, because Phase III protocols require frequent on-site visits and source-data verification. Pharmacovigilance, however, is projected to outpace all other services at a 6.78% CAGR as regulators demand decade-long safety registries for IL-17 and IL-23 inhibitors, driving sustained outsourcing demand. Specialist CROs leverage harmonized MedDRA coding and pooled-database analytics to detect rare events faster, creating clear differentiation.

Data Management and Biostatistics are moving up the value chain as AI-graded imaging and ePRO data expand raw-data volumes by double-digit rates. Laboratory and Analytical Services see renewed interest because EMA-mandated tape-stripping bioequivalence tests for topicals can only be executed by a handful of labs worldwide. Over time, low-margin site-management functions risk being disintermediated by direct sponsor-site platforms, prompting CROs to emphasize higher-value pharmacovigilance and regulatory consulting.

By Clinical Phase: Phase I Accelerates as Novel Mechanisms Enter Clinic

Phase III retained the greatest Dermatology Contract Research Organization (CRO) market share at 37.89% in 2025, thanks to high-enrolling psoriasis and atopic dermatitis programs, yet Phase I is set for the fastest 6.88% CAGR as gene therapies and novel JAK inhibitors reach first-in-human studies. Biotech clients, often without internal clinical-ops teams, outsource end-to-end study management, pushing CROs to build specialized toxicology and photosafety capabilities.

Phase II remains the operational “sweet spot.” Cohorts of 150–200 patients allow proof-of-concept without Phase III expenditure but still require sophisticated monitoring, data, and pharmacovigilance services. Post-marketing Phase IV studies expand steadily as payers demand comparative-effectiveness data, enabling CROs to generate recurring, lower-volatility revenue.

By Therapeutic Area: Vitiligo Surges on Repigmentation Endpoint Validation

Psoriasis anchored 45.97% of 2025 revenue, but vitiligo is forecast to lead growth with a 6.98% CAGR, reflecting renewed sponsor interest after ruxolitinib’s success. Dermatology CRO market size for vitiligo studies is expected to double by 2031 as additional JAK inhibitors and melanocyte-stimulating therapies enter late-stage trials.

Atopic dermatitis trials remain plentiful due to the blockbuster performance of dupilumab, tralokinumab, and lebrikizumab, while alopecia areata studies scale up following baricitinib’s approval. Rare genodermatoses, despite small populations, command premium budgets because orphan-drug incentives fund intensive monitoring and decentralized-trial structures that specialist CROs can monetize.

By Sponsor Type: Device Firms Drive Diagnostic-Trial Demand

Pharmaceutical companies still account for 46.82% of the Dermatology CRO market revenue, but medical device and diagnostic sponsors will clock a 7.09% CAGR through 2031 as AI-based imaging tools and companion diagnostics seek validation. Device developers rely on CROs to coordinate dual regulatory submissions for the test and therapeutic components, heightening complexity and billable hours.

Academic groups provide steady, smaller contracts funded by NIH and EU grants. These projects often serve as proof-of-concept feeders for future industry partnerships but pressure CRO pricing. The sponsor landscape is converging as pharma acquires device firms to build integrated platforms and device makers license therapeutic molecules, broadening the Dermatology CRO market opportunity.

Geography Analysis

North America commanded 46% of 2025 revenue owing to the FDA’s acceptance of digital-imaging endpoints and the density of more than 180 academic dermatology centers that rapidly enroll in pivotal trials. The region’s robust payer systems support post-approval evidence generation, although site competition lengthened recruitment times from eight to 11 months between 2023 and 2025. Canada’s streamlined ethics approvals and Mexico’s lower site costs create tactical Phase II advantages, but the United States still absorbs the bulk of late-stage budgets.

Asia-Pacific is on track for the fastest 7.5% CAGR through 2031 as China’s NMPA and India’s CTRI log double-digit increases in protocol submissions [3]National Medical Products Administration, “Dupilumab Approval,” nmpa.gov.cn. Japan’s PMDA, though stringent on photosafety, offers high-compliance patient pools critical for long-term safety follow-ups. South Korea’s MFDS accelerates biosimilar trials, Australia remains a popular first-in-human venue thanks to its R&D tax incentive, and Southeast Asian countries offer cost-effective bioequivalence options, expanding investigator networks for future pivotal projects.

Europe presents regulatory complexity yet yields cost arbitrage. EMA harmonization is improving, evidenced by its 2024 vitiligo approval aligning with the FDA timeline. Southern and Eastern European sites deliver 30%–40% cost savings versus Germany and the UK, though CROs must invest in local language project management. The Middle East and Africa are nascent but growing; the UAE approved 12 dermatology studies in 2025, and Turkey’s treatment-naive demographics appeal to biosimilar developers despite regulatory unpredictability. In South America, Brazil and Argentina drive activity, yet currency volatility requires CRO contracts to carry inflation clauses.

Competitive Landscape

No single provider has a dominant share, underscoring a fragmented Dermatology CRO market where therapeutic specialization trumps scale. IQVIA’s 2024 acquisition of Citeline brings real-time regulatory intelligence under one roof, helping sponsors benchmark competitor trial designs at the proposal stage. Labcorp’s purchase of Invitae’s genomic assets the same year adds companion-diagnostic capabilities, enabling bundled proposals that include biomarker testing and protocol execution.

Specialists such as Innovaderm Research and Proinnovera own proprietary patient registries and AI-certified imaging endpoints but face capital constraints for international expansion. Emerging disruptors like Science 37 and TrialSpark circumvent conventional site-based models with direct-to-patient platforms, cutting recruitment timelines by up to 50% and forcing incumbents to invest in hybrid-trial technologies.

Scale players respond with vertical integration, combining lab, logistics, pharmacovigilance, and real-world evidence services, to lock in multi-program agreements. Compliance with ICH E6(R3), ISO 14155, and GDPR raises entry barriers but also piles on operating costs, squeezing mid-tier generalist CROs that lack either deep specialization or diversified service breadth.

Dermatology Contract Research Organization (CRO) Industry Leaders

IQVIA Holdings Inc.

ICON plc

Thermo Fisher Scientific Inc. (PPD)

Labcorp Drug Development

Syneos Health Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Silo Pharma has chosen Allucent to steer its Phase I trials, illustrating how small, dermatology-focused biotechs are increasingly turning to seasoned contract researchers rather than building the expertise in-house.

- July 2025: Novotech received the 2025 Global Biotech CRO Company of the Year award, spotlighting APAC-centric execution strengths

- March 2025: Jeeva Clinical Trials expanded its CRO Partnership Program, adding AI-supported patient-engagement modules for dermatology protocols.

Global Dermatology Contract Research Organization (CRO) Market Report Scope

As per the scope of the report, Dermatology Contract Research Organization (CRO) is a specialized service provider that manages clinical trials and research for pharmaceutical, biotechnology, and medical device companies, focusing on skin-related conditions. These organizations are essential partners in navigating the complex drug development lifecycle.

The Dermatology Contract Research Organization (CRO) Market is segmented by service type, clinical phase, therapeutic area, sponsor type, and geography. By service type, the market is categorized into early phase services, clinical monitoring, regulatory & medical affairs, data management & biostatistics, site management, patient recruitment & retention, pharmacovigilance, laboratory / analytical services, and others. By clinical phase, it is segmented into Pre-clinical, Phase I, Phase II, Phase III, and Phase IV. By therapeutic area, the market is divided into psoriasis, atopic dermatitis, acne & rosacea, skin cancer, alopecia, vitiligo, wound healing & ulcers, and other inflammatory skin diseases. By sponsor type, the segmentation includes pharmaceutical companies, academic & research institutes, and medical device / diagnostic companies. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Early Phase Services |

| Clinical Monitoring |

| Regulatory & Medical Affairs |

| Data Management & Biostatistics |

| Site Management |

| Patient Recruitment & Retention |

| Pharmacovigilance |

| Laboratory / Analytical Services |

| Others |

| Pre-clinical |

| Phase I |

| Phase II |

| Phase III |

| Phase IV |

| Psoriasis |

| Atopic Dermatitis |

| Acne & Rosacea |

| Skin Cancer |

| Alopecia |

| Vitiligo |

| Wound Healing & Ulcers |

| Other Inflammatory Skin Diseases |

| Pharmaceutical Companies |

| Academic & Research Institutes |

| Medical Device / Diagnostic Companies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Early Phase Services | |

| Clinical Monitoring | ||

| Regulatory & Medical Affairs | ||

| Data Management & Biostatistics | ||

| Site Management | ||

| Patient Recruitment & Retention | ||

| Pharmacovigilance | ||

| Laboratory / Analytical Services | ||

| Others | ||

| By Clinical Phase | Pre-clinical | |

| Phase I | ||

| Phase II | ||

| Phase III | ||

| Phase IV | ||

| By Therapeutic Area | Psoriasis | |

| Atopic Dermatitis | ||

| Acne & Rosacea | ||

| Skin Cancer | ||

| Alopecia | ||

| Vitiligo | ||

| Wound Healing & Ulcers | ||

| Other Inflammatory Skin Diseases | ||

| By Sponsor Type | Pharmaceutical Companies | |

| Academic & Research Institutes | ||

| Medical Device / Diagnostic Companies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Dermatology CRO market?

The Dermatology CRO market size is expected to reach USD 6.11 billion in 2026 and is forecast to reach USD 8.32 billion by 2031

Which service grows fastest in outsourced dermatology trials?

Pharmacovigilance is projected to post the quickest 6.78% CAGR through 2031 because regulators demand long-term safety surveillance for biologics.

Why is Asia-Pacific attracting more dermatology studies?

Faster NMPA approvals and a growing pool of treatment-naive patients lift Asia-Pacific revenue at a 7.5% CAGR, outpacing all regions.

What is driving demand from device sponsors?

AI-powered imaging and companion diagnostics require validation studies, pushing medical device and diagnostic companies to outsource multi-component protocols.

How are decentralized trials changing dermatology research?

Smartphone imaging, telemedicine visits, and home phlebotomy cut dropout rates and accelerate recruitment, now appearing in 18% of dermatology protocols.

Page last updated on: