Depyrogenated Sterile Empty Vials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

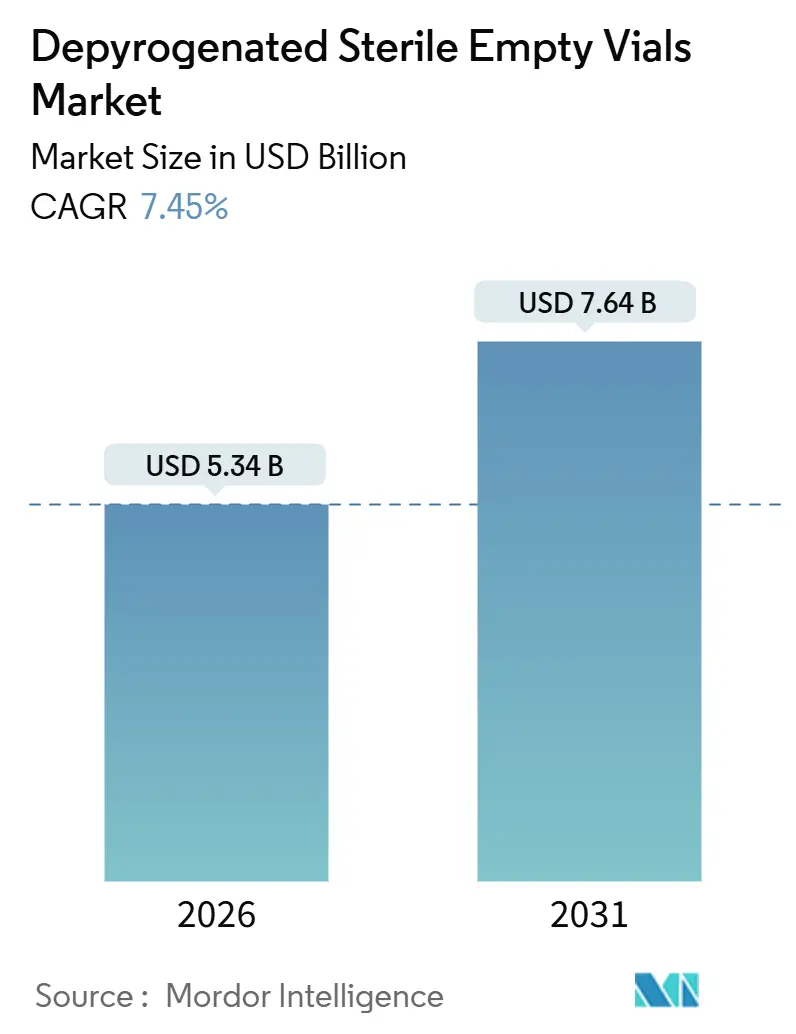

| Market Size (2026) | USD 5.34 Billion |

| Market Size (2031) | USD 7.64 Billion |

| Growth Rate (2026 - 2031) | 7.45% CAGR |

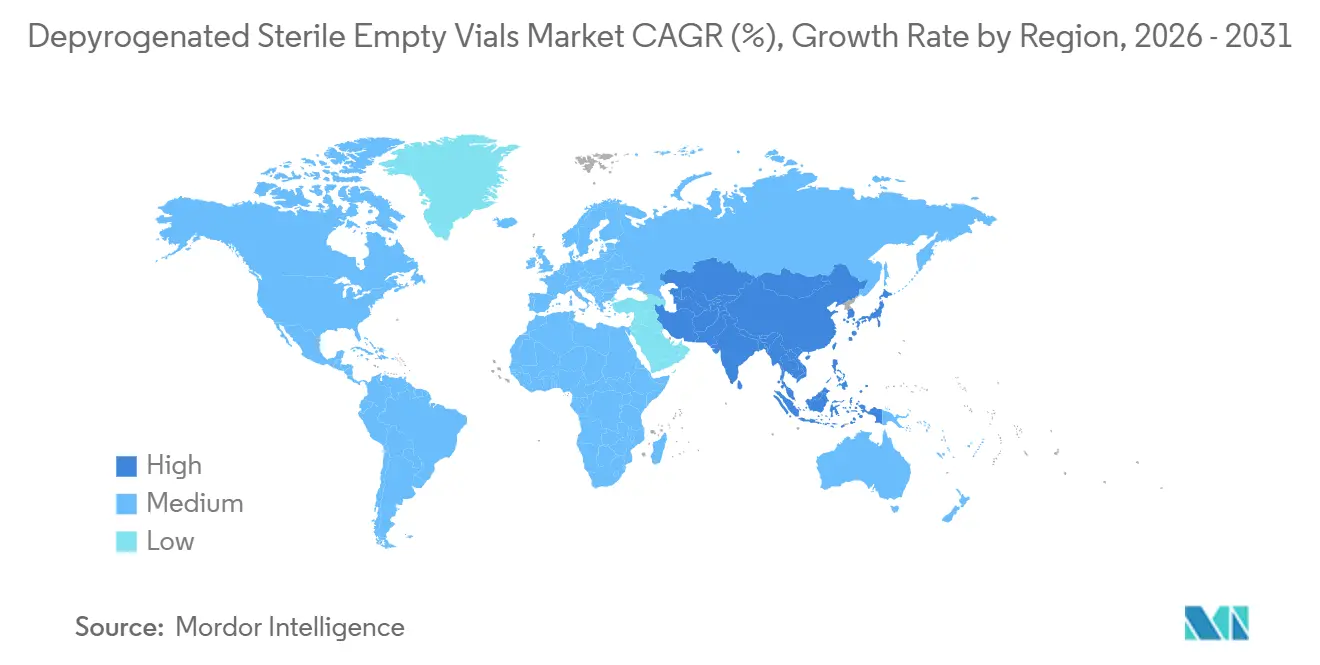

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Depyrogenated Sterile Empty Vials Market Analysis by Mordor Intelligence

The Depyrogenated Sterile Empty Vials Market size is estimated at USD 5.34 billion in 2026, and is expected to reach USD 7.64 billion by 2031, at a CAGR of 7.45% during the forecast period (2026-2031).

This expansion reflects structural shifts rather than simple volume gains, as injectable pipelines tilt toward biologics, personalized therapies, and next-generation vaccines that demand pyrogen-free primary packaging. Contract development and manufacturing organizations (CDMOs) now provide almost two-fifths of global injectable capacity, so they increasingly specify validated, ready-to-use (RTU) vials to avoid in-house depyrogenation downtime. Regulatory bodies have tightened endotoxin limits and documentation requirements, pushing manufacturers to replace legacy washing tunnels with pre-sterilized containers. Meanwhile, lingering glass-tubing constraints give vertically integrated suppliers pricing power, even as cyclic olefin polymer (COP) and cyclic olefin copolymer (COC) formats post the fastest growth. Collectively, these dynamics keep the depyrogenated, sterile, empty vial market on a resilient, mid-single-digit growth trajectory.

Key Report Takeaways

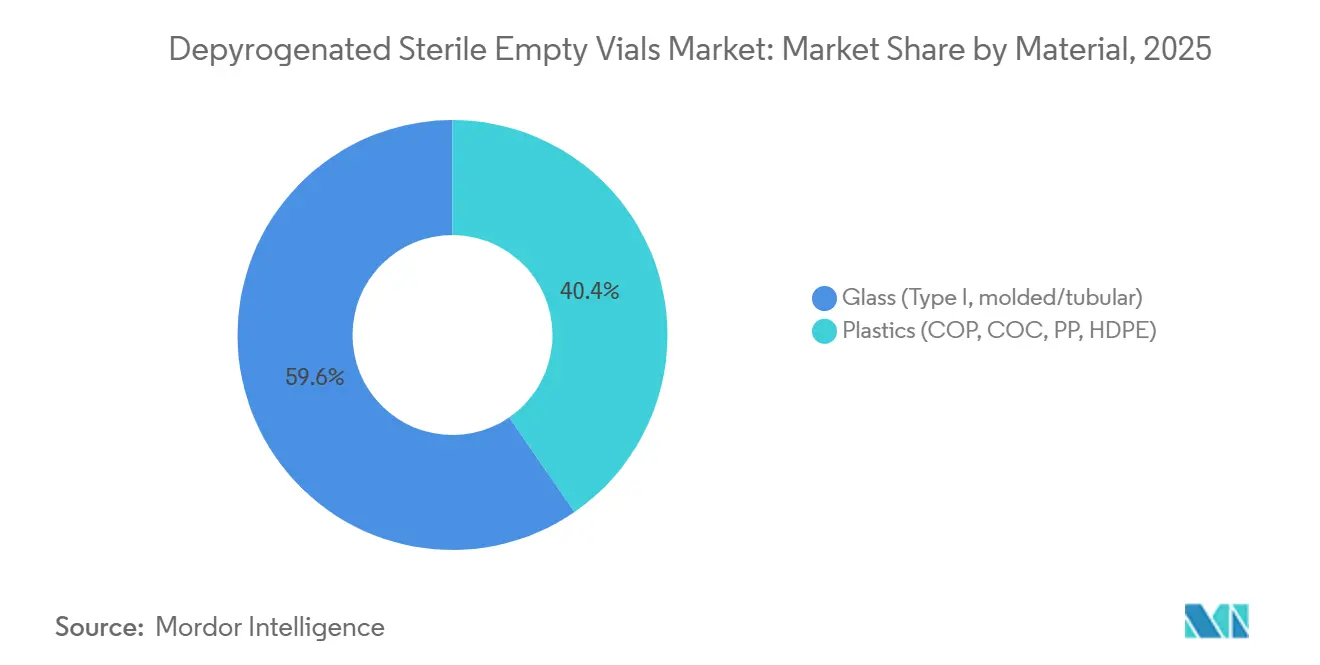

- By material, Type I borosilicate glass led with 59.55% revenue share in 2025, while polymer vials are forecast to post the quickest 8.25% CAGR through 2031.

- By vial volume, the 10mL –20 mL range captured 32.53% of the depyrogenated, sterile, empty vials market share in 2025; vials under 5 mL are projected to expand at an 8.85% CAGR to 2031.

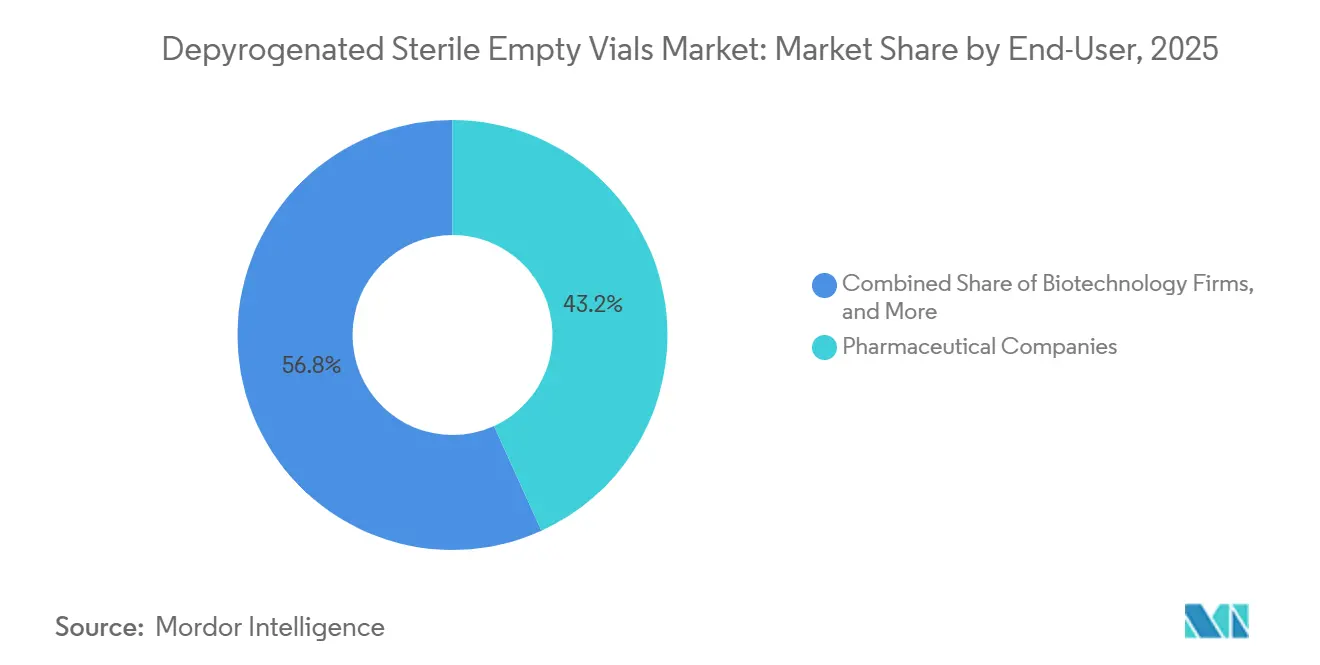

- By end user, pharmaceutical companies commanded 43.23% of the depyrogenated sterile empty vials market size in 2025, yet clinical and compounding laboratories represent the fastest-growing segment at an 8.15% CAGR.

- By geography, North America generated 39.25% of 2025 revenue, whereas Asia-Pacific is slated to grow at an 8.21% CAGR, the swiftest pace worldwide.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Depyrogenated Sterile Empty Vials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-COVID Surge in Biologics & Personalized Therapies | +1.8% | North America, Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| Heightened Global Sterility & Endotoxin Regulations | +1.5% | Global | Long term (≥ 4 years) |

| CDMO Outsourcing & Rapid Line Changeovers | +1.4% | North America, Europe, India, China | Medium term (2-4 years) |

| Expansion of Vaccine Manufacturing Infrastructure | +1.2% | North America, Europe, India | Short term (≤ 2 years) |

| Energy-Cost Shift to Outsourced Depyrogenation | +0.6% | Europe, North America | Medium term (2-4 years) |

| Smart RTU Vials with RFID And Data-Matrix Codes | +0.5% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-COVID Surge in Biologics & Personalized Therapies

Biologics now represent 40% of global pipelines, and messenger RNA, CAR-T, and gene-edited therapies all require cryogenic-compatible containers with ultra-low endotoxin levels. Moderna’s pipeline of 45 programs, 31 already in clinical trials, locks in multi-year RTU vial contracts, while BioNTech’s Marburg expansion to 750 million annual doses further stretches supply. As batch sizes splinter across hundreds of stock-keeping units, suppliers able to validate depyrogenated runs as small as 10,000 vials capture premium demand. The depyrogenated, sterile, empty vial market, therefore, gains critical mass from high-value biologics rather than commodity injectables.

Heightened Global Sterility & Endotoxin Regulations

Revised FDA guidance from July 2024 requires prior-approval supplements for any change to sterilization temperature profiles or hold times, increasing the compliance burden for in-house tunnels[1]U.S. Food and Drug Administration, “Container Closure Systems for Packaging Human Drugs and Biologics,” fda.gov. Europe’s Annex 1 now mandates documented three-log endotoxin reduction, and WHO’s Technical Report 1039 harmonizes testing worldwide[2]European Medicines Agency, “Annex 1: Manufacture of Sterile Medicinal Products,” ema.europa.eu. Together, these rules push risk-averse manufacturers toward validated RTU formats, thereby sustaining the market for depyrogenated, sterile, empty vials.

CDMO Outsourcing & Rapid Line Changeovers

Pharma divestitures and biotech asset-light models mean CDMOs already handle up to 40% of injectable output. Operators such as Pfizer CentreOne and Aenova invest in RTU filling lines because same-day changeovers lift asset utilization by roughly 20%. Consequently, CDMO purchasing establishes a strong floor for the depyrogenated, sterile, empty vial market.

Expansion of Vaccine Manufacturing Infrastructure

Public funding exceeding USD 8 billion between 2021 and 2025 added green-field mRNA capacity in Canada, India, and Africa. Each site specifies 2 mL–10 mL depyrogenated vials that meet USP <85> endotoxin criteria, amplifying demand over the short term.

Restraints Impact Analysis*

| Restraint | ( ~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium Pricing of RTU Depyrogenated Vials | -0.8% | Global, price-sensitive generics | Medium term (2-4 years) |

| Substitution Threat from Pre-Filled Syringes & Cartridges | -0.6% | North America, Europe | Long term (≥ 4 years) |

| Borosilicate Furnace Capacity Constraints | -0.5% | Global | Short term (≤ 2 years) |

| Validation Hurdles for Polymer Vials | -0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium Pricing of RTU Depyrogenated Vials

RTU formats carry a 40%–60% markup versus bulk-washed glass. Margins on generic injectables often run below 12%, so Medicare Part B reimbursement fails to offset the higher cost, discouraging upgrades and shaving growth from the depyrogenated sterile empty vials industry.

Substitution Threat from Pre-Filled Syringes & Cartridges

Needle-safe syringes, wearable injectors, and patient-centric delivery devices bypass vials for chronic therapies, particularly in Europe and North America. As Gerresheimer, BD, and West post double-digit syringe growth, some small-volume vial demand migrates to alternative containers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Glass Holds Ground as Polymers Accelerate

Type I borosilicate glass dominated 59.55% of 2025 revenue thanks to universal regulatory acceptance, high-temperature tolerance, and well-understood leachables profiles. Corning’s Valor and Viridian lines add break resistance and lower embodied carbon, reinforcing glass as the mainstream substrate[3]Corning Incorporated, “Corning Launches Viridian Vials,” corning.com. Yet plastics such as COP and COC are projected to compound at 8.25% through 2031, the fastest growth rate in the depyrogenated sterile empty vials market. Polymer vials weigh less, resist shattering, and integrate with pre-filled syringe platforms, giving contract fillers ergonomic and safety wins.

Momentum in polymers carries strategic significance. SiO2’s barrier-coated containers show extractables parity with glass, while newly published silicon-oxynitride research cuts aluminum release tenfold[4]SiO2 Materials Science, “Technology Overview,” sio2ms.com. Still, validation cycles stretching 12–24 months keep absolute volumes modest. Overall, glass should retain the majority stake, but incremental shifts in share to polymer create new competition and pricing corridors.

By Vial Volume: Mid-Sizes Lead, Ultra-Small Surge

The 10 mL–20 mL cohort captured 32.53% of 2025 sales, supplying bulk-fill monoclonal antibodies and multi-dose vaccines. High-speed lines running 400–600 vials per minute favor these mid-sizes, and Gerresheimer’s RTF and Stevanato’s EZ-fill offerings shorten validation timelines by four weeks or more. At the same time, vials under 5 mL are forecast to post an 8.85% CAGR, the sharpest rise in the depyrogenated sterile empty vials market size, as cell-and-gene therapies and high-potency oncology drugs demand single-dose precision.

Manufacturers who can deliver depyrogenated runs at prices below 2,000 units per run win outsized margins. Nipro’s D2F platform, for instance, guarantees endotoxin levels below 0.03 EU/mL for advanced-therapy batches. Conversely, vials over 20 mL remain a mature niche as hospitals migrate irrigation solutions to flexible bags.

By End User: Pharma Heavyweights, Labs Accelerate

Pharmaceutical companies still accounted for 43.23% of 2025 demand, leveraging large campuses such as Pfizer's McPherson and AbbVie's North Chicago sites, which run multiple fill-finish lines. However, clinical and compounding laboratories are advancing at an 8.15% CAGR, the fastest of any buyer group inside the depyrogenated sterile empty vials market. Decentralized trials need small, sterile batches shipped to community sites, while Section 503B outsourcing facilities must meet USP <71> sterility and endotoxin specifications. This decentralized model widens the addressable base beyond Big Pharma.

Geography Analysis

North America generated 39.25% of 2025 revenue, buoyed by strong biologics pipelines and early RTU adoption. FDA SOPP 8506 obliges six-month shortage notifications, motivating redundant inventories and multi-supplier strategies that channel steady orders to vial makers. Significant capex by West Pharmaceutical and Corning secures future feedstock and components within the region.

Europe follows with entrenched demand and new policy tailwinds. The December 2025 Critical Medicines Act earmarks EUR 5 billion for local production of 200 essential drugs, locking in multiyear contracts for regional tubing and RTU capacity. SCHOTT’s Hungarian expansion and Stevanato’s Italian build-out position incumbents to backfill reshored volumes.

Asia-Pacific is projected to grow at 8.21% through 2031, the fastest worldwide. India’s Production Linked Incentive (PLI) program alone allocates USD 840 million to bulk-drug plants and USD 1.8 billion to finished formulations, spurring Serum Institute and Biological E to add 1.5 billion vaccine doses of annual capacity. Corning-SGD’s Hyderabad tubing plant shortens lead times from a year to eight weeks, undergirding a regionally integrated supply chain. China and Japan contribute incremental demand as each harmonizes with ICH guidelines and invests in low-extractables formats.

The Middle East & Africa, as well as South America, are smaller today but rising. South Africa’s Biovac and Brazil’s ANVISA reforms embed higher sterility standards that favor depyrogenated RTU vials. As local fill-finish hubs proliferate, baseline requirements for validated, pyrogen-free containers will expand accordingly.

Competitive Landscape

The depyrogenated sterile empty vials market is moderately concentrated: the top five suppliers, SCHOTT, Gerresheimer, Stevanato Group, West Pharmaceutical Services, and Corning, command a sizable yet not dominant share. Each pursues vertical integration to lock in glass tubing, geographic dispersion to serve reshoring clients, and technology differentiation through smart IDs, barrier coatings, or sustainability branding. SCHOTT’s EUR 1 billion multi-region tubing program exemplifies feedstock control, while Gerresheimer’s Peachtree City site and Stevanato’s Piombino Dese line illustrate regional reach. Polymer innovators such as SiO2 aim at niche, high-value therapies, leveraging more than 300 patents and break-resistant designs.

White-space growth focuses on ultra-small (<1 mL) cryogenic-ready formats for mRNA and cell-therapy products, hybrid glass-polymer constructs, and depyrogenation-as-a-service offerings for resource-limited pharma plants. Start-ups that integrate RFID, blockchain, and predictive analytics into vial tracking stand to attract digital-first biotechs. Nonetheless, FDA guidance mandating full extractables studies for any process change grants incumbents with validated portfolios a timing advantage.

Depyrogenated Sterile Empty Vials Industry Leaders

SCHOTT AG

Corning Inc.

Gerresheimer AG

Stevanato Group

West Pharmaceutical Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Sharp Sterile Manufacturing committed USD 28 million to double filling capacity at its Lee, Massachusetts, site by adding a fully automated IMA Life isolated line for RTU vials.

- September 2025: Medisca entered a long-term partnership with Stevanato Group to distribute EZ-fill RTU glass vials to sterile compounding pharmacies worldwide.

Global Depyrogenated Sterile Empty Vials Market Report Scope

As per the report's scope, depyrogenated sterile empty vials are pharmaceutical‑grade glass containers that have been rigorously treated to remove pyrogens, heat‑stable endotoxins that can cause fever or adverse reactions. After depyrogenation, the vials are sterilized and packaged to maintain aseptic integrity. They are used for filling sterile drug products, injectables, vaccines, and diagnostic reagents. Their preparation ensures they meet strict regulatory standards for sterility and endotoxin limits.

The depyrogenated, sterile, empty vials market segmentation includes material, vial volume, end user, and geography. By material, the market is segmented into glass (Type I, molded/tubular) and plastics (COP, COC, PP, HDPE). By vial volume, the market is segmented into < 5 mL, 5–10 mL, 10–20 mL, and > 20 mL. By end user, the market is segmented into pharmaceutical companies, biotechnology firms, contract manufacturing/CDMOs, and clinical & compounding labs. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report covers estimated market sizes and trends for 17 countries across major regions worldwide. The report offers the value (in USD) for the above segments.

| Glass (Type I, molded/tubular) |

| Plastics (COP, COC, PP, HDPE) |

| 5 mL |

| 5-10 mL |

| 10-20 mL |

| 20 mL |

| Pharmaceutical Companies |

| Biotechnology Firms |

| Contract Manufacturing / CDMOs |

| Clinical & Compounding Labs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material | Glass (Type I, molded/tubular) | |

| Plastics (COP, COC, PP, HDPE) | ||

| By Vial Volume | 5 mL | |

| 5-10 mL | ||

| 10-20 mL | ||

| 20 mL | ||

| By End-User | Pharmaceutical Companies | |

| Biotechnology Firms | ||

| Contract Manufacturing / CDMOs | ||

| Clinical & Compounding Labs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the depyrogenated sterile empty vials market?

The depyrogenated sterile empty vials market size reached USD 5.34 billion in 2026.

How fast is the market expected to grow by 2031?

It is projected to expand at a 7.45% CAGR, reaching USD 7.64 billion by 2031.

Which material dominates sales today?

Type I borosilicate glass leads with 59.55% revenue share.

Which vial size is growing the quickest?

Vials under 5 mL are forecast to post an 8.85% CAGR from 2026 to 2031.

Why are CDMOs important to future demand?

CDMOs control up to 40% of injectable capacity and favor RTU vials to shorten line changeovers, bolstering overall consumption.

Which region will see the highest growth rate?

Asia-Pacific is expected to record the fastest regional CAGR at 8.21% through 2031.

Page last updated on: