Dental Suction Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

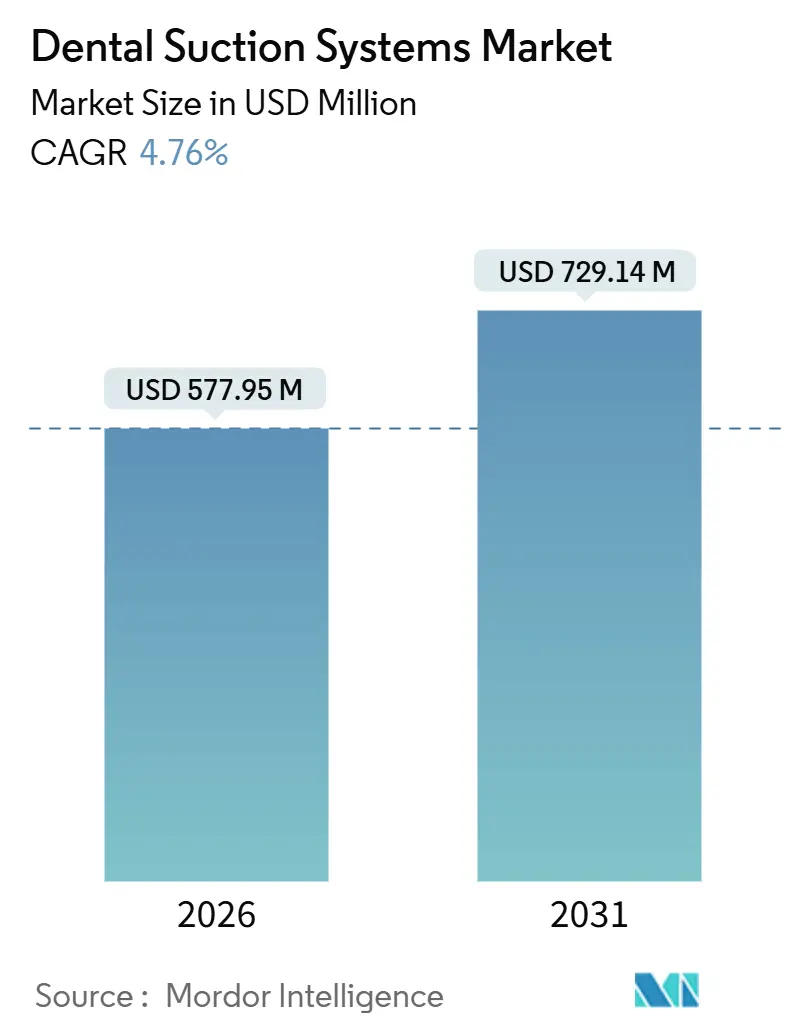

| Market Size (2026) | USD 577.95 Million |

| Market Size (2031) | USD 729.14 Million |

| Growth Rate (2026 - 2031) | 4.76% CAGR |

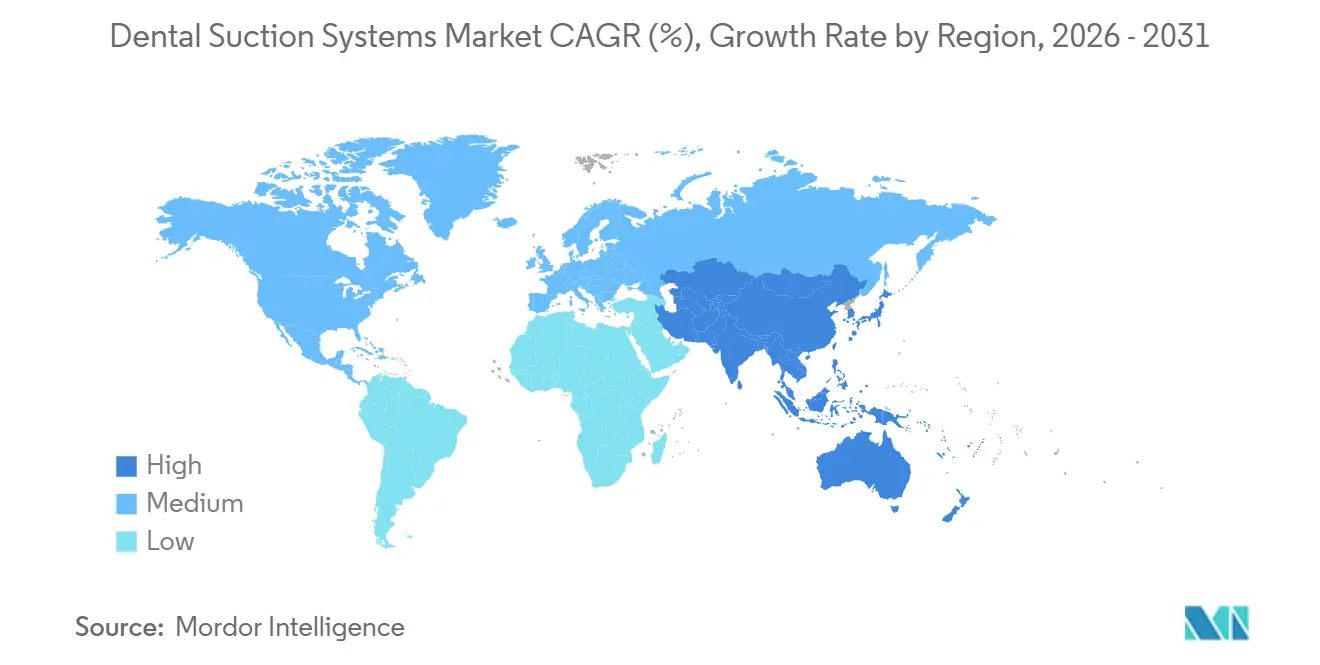

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Suction Systems Market Analysis by Mordor Intelligence

The Dental Suction Systems Market size is estimated at USD 577.95 million in 2026, and is expected to reach USD 729.14 million by 2031, at a CAGR of 4.76% during the forecast period (2026-2031).

Market growth is driven by the adoption of energy-efficient dry vacuum platforms, stricter infection-control regulations, and the rapid expansion of multi-chair Dental Service Organizations (DSOs). Key factors influencing adoption include the mandatory implementation of amalgam-separators, the integration of variable-frequency-drive (VFD) motors that reduce electricity consumption by 30-40%, and cloud-enabled pumps that provide predictive failure alerts 72 hours in advance. Hospitals are increasingly incorporating oral-surgery suites requiring 24/7 suction redundancy, while urban clinics are investing in sub-55 dB(A) pumps to comply with municipal noise standards. Furthermore, the rise of online procurement channels and subscription-based “equipment-as-a-service” models is enhancing market accessibility, particularly for start-ups with limited initial capital.

Key Report Takeaways

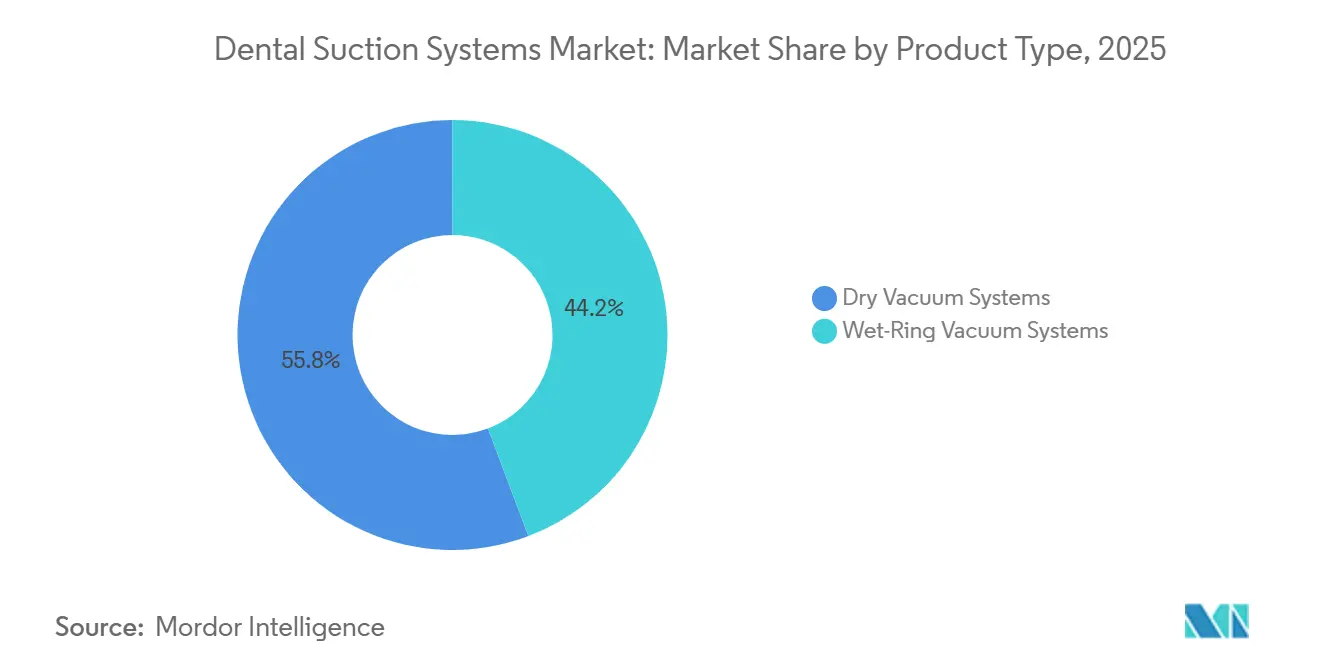

- By product, dry vacuum systems led with 55.76% of 2025 revenue; wet-ring variants are forecast to expand at a 6.43% CAGR through 2031.

- By installation type, chairside units captured a 58.65% share in 2025, whereas centralized platforms are growing at a 6.75% CAGR to 2031.

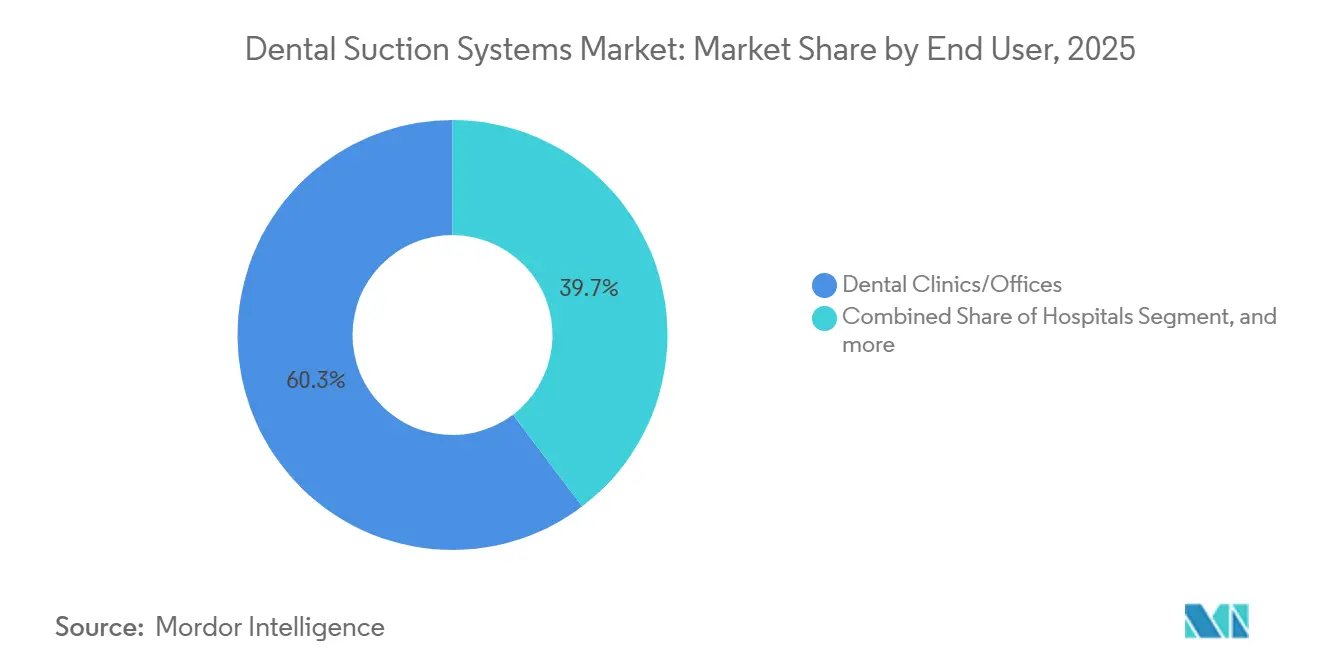

- By end user, dental clinics commanded 60.32% of the dental suction systems market share in 2025, while hospitals showed the fastest growth at 7.11% CAGR.

- By sales channel, direct OEM routes accounted for 52.45% of 2025 sales; online channels are projected to grow at a 7.54% CAGR.

- By geography, North America retained 42.67% revenue share in 2025; Asia-Pacific is advancing at a 5.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dental Suction Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened infection prevention and aerosol management protocols | +0.8% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Regulatory compliance for mercury and wastewater discharge | +0.7% | North America, Europe, China, India, Brazil | Medium term (2–4 years) |

| Expanding multi-chair clinics and DSOs | +1.2% | North America, Asia-Pacific, Latin America | Long term (≥ 4 years) |

| Sustainability initiatives favoring energy-efficient dry vacuums | +0.6% | Europe, North America, Australia | Medium term (2–4 years) |

| Digitization and remote monitoring | +0.5% | North America, Western Europe, urban Asia-Pacific | Medium term (2–4 years) |

| Urban facility design constraints | +0.4% | Dense cities worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Heightened Infection Prevention and Aerosol Management Protocols

The Centers for Disease Control and Prevention recommends high-volume evacuators capable of sustaining flows above 100 CFM within 6 inches of the operative field, effectively steering clinics toward centralized dry pumps that can support continuous multi-hour surgical loads. OSHA guidance reinforces the requirement, while the EPA’s dental effluent rule mandates amalgam separators achieving 99% particulate capture, with fines reaching USD 37,500 per violation in 2024. Manufacturers responded: Cattani’s Aspi-Aero 25, launched in 2024, integrates HEPA filtration and trimmed room turnover times by 30%. ISO 23402-3:2024 further standardizes mobile-unit performance, obliging battery-powered pumps to deliver 80 L/min for 45 minutes, a prerequisite for U.S. federal grants[1]International Organization for Standardization, “ISO 23402-3:2024 Dentistry—Portable Suction Equipment,” iso.org.

Regulatory Compliance Requirements for Mercury and Wastewater Discharge

The EPA rule obliges all U.S. practices discharging to municipal sewers to install ISO 11143-compliant separators that attain 95% mercury capture. California’s water board levies fines starting at USD 10,000 for non-compliance, and New York demands biennial third-party certification[2]California State Water Resources Control Board, “Dental Amalgam Program,” waterboards.ca.gov. Dry vacuums, which avoid the dilution inherent to wet-ring pumps, cut sludge-handling costs by 20-25%. Europe’s Urban Waste Water Treatment Directive encourages a full shift to dry systems, and ISO 22052:2024 harmonizes global test methods, shaving 6–9 months off CE-mark and FDA pathways.

Expanding Multi-Chair Clinics and DSOs Requiring Centralized Vacuum Infrastructure

DSO affiliation increased roughly 50% between 2017 and 2022, and these groups may account for 40% of overall dental spend by 2030. Centralized pumps slash per-chair costs 15-20% in 8-to-12-chair setups and feed remote dashboards that predict faults 72 hours in advance, curbing unplanned downtime 40%. China’s National Health Commission counted an 18% annual rise in 6-plus-chair clinics from 2020-2024, prompting bulk orders for centralized units.

Sustainability Initiatives Driving Adoption of Energy-Efficient Dry Vacuum Systems

VFD-equipped dry platforms cut electricity consumption 30-40% and trim water use to zero, securing ENERGY STAR labels and utility rebates in several U.S. states. Midmark’s Smart G-Vacuum powers down after 15 minutes of inactivity, powering down the standby draw to 85%. The EU’s Fit for 55 package, targeting a 55% carbon cut by 2030, is pushing clinics to replace wet-ring pumps that consume up to 500 L/day of water.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure for upgrading legacy equipment | -0.9% | Independent practices in mature markets | Short term (≤ 2 years) |

| Technical challenges retrofitting older buildings | -0.5% | Pre-2000 construction in North America and Europe | Medium term (2–4 years) |

| Rising total ownership cost from hazardous-waste rules | -0.3% | North America, Europe, selected Asian markets | Long term (≥ 4 years) |

| Space and vibration limits in mixed-use real estate | -0.2% | Dense urban markets worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for Upgrading Legacy Utility-Room Equipment

Switching a four-chair clinic from wet-ring to dry suction commonly costs USD 25,000-35,000, a hurdle for independents whose median net income fell 16-22% from 2010-2023[3]American Dental Association, “Survey of Dental Practice 2024,” ada.org. Leasing spreads payments over five to seven years, but rural practitioners face higher interest rates. DSOs enjoy 20-25% volume discounts, widening the affordability gap. Subscription “vacuum-as-a-service” plans, such as Dürr Dental’s 2025 German launch, eliminate upfront spend while reducing the 10-year outlay by 15-20%.

Technical Challenges of Retrofitting Suction Systems in Older Buildings

Centralized pumps require 208-240 V three-phase circuits at 30-50 A. Upgrading panels costs USD 5,000-10,000 and may require transformer swaps, adding 10-12 weeks. Routing waste lines through load-bearing walls or asbestos-containing materials inflates labor. Wood-frame vibration demands spring mounts and elastomer pads costing USD 2,000-3,000, and historic districts often ban exterior venting, forcing recirculating filters that increase the footprint by 30%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Dry Vacuum Systems Lead, Wet-Ring Variants Gain in Water-Rich Regions

Dry platforms accounted for 55.76% of 2025 revenue in the dental suction systems market. Premium price tags of USD 8,000-15,000 per operatory are offset by 30-40% energy savings from VFD motors, a decisive benefit for DSOs tracking utility bills across hundreds of sites. Wet-ring pumps, costing USD 4,000-7,000, remain favored in water-abundant locales because single-phase 120 V service suffices for small practices and maintenance requires no oil changes. Wet-ring demand is rising 6.43% annually through 2031, underpinned by clinics in Southeast Asia and Brazil that prioritize lower upfront costs. METASYS’s 2025 EXCOM hybrid blurs categories, bundling 95% amalgam capture with a 60% noise cut. Regulatory frameworks like ISO 10637 continue to steer buyers toward technologies that simplify separator certification.

Second-generation dry pumps incorporate EC motors and predictive telemetry. Dürr Dental’s Dental Vortex Blue reaches 92% efficiency and 52 dB(A) operation, unlocking ENERGY STAR rebates. Cattani’s Turbo SMART TS couples inverter control with cloud diagnostics, trimming energy by 35% and servicing costs by 25%. Such innovations reinforce the dental suction systems market as sustainability regulations tighten.

By Installation Type: Chairside Units Dominate, Centralized Systems Scale with DSOs

Chairside units commanded 58.65% of 2025 revenue, driven by 2-to-4-chair practices that need flexible, low-commitment setups. Units can be installed in under three hours and cost USD 2,000-4,000 per operatory, making them attractive for leased spaces that lack three-phase power. Centralized systems, expanding at a 6.75% CAGR, lower per-chair spending by 15-20% once clinics exceed eight chairs. Heartland Dental remotely monitors vacuum pressure across 1,800 offices, cutting downtime 40%. The dental suction systems market size for centralized platforms is projected to widen as DSOs consolidate procurement and landlords allow utility-room retrofits.

A-dec’s QuietCore+ extends mean time between failures to 12,000 hours, while Midmark’s Smart G-Vacuum powers down during idle periods, cutting standby draw by 85%. Retrofitting older buildings still adds 20-30% to capital due to electrical and structural reinforcements, factors that keep chairside units entrenched in vintage real estate.

By End User: Dental Clinics Lead, Hospitals Accelerate With Ambulatory Surgery Integration

Dental clinics generated 60.32% of the 2025 demand, reflecting more than 200,000 active U.S. practices. Hospitals, however, are the fastest-growing segment, with a 7.11% CAGR, because ambulatory surgery centers now incorporate oral-maxillofacial suites that require redundant pumps and 24/7 readiness. Centralized hospital installations raise capital by 30-40% but satisfy Joint Commission infrastructure criteria. The dental suction systems market size generated by hospitals is expected to grow steadily as outpatient surgical volumes rise.

Mobile and outreach units grow by 5.2% annually, thanks to USD 127 million in HRSA grants that require ISO 23402-3 compliance. Academic centers demand modular suction that can vary flow from 50 CFM student stations to 150 CFM implantology labs, reinforcing premium multi-mode pump sales within the dental suction systems industry.

By Sales Channel: Direct OEM Channels Prevail, Online Platforms Surge With Digital Procurement

Direct OEM transactions accounted for 52.45% of 2025 sales, as DSOs and hospitals prefer bundled service contracts and certified installation. Online marketplaces, rising 7.54% annually, now enable specification comparisons and 48-hour credit approval, a boon for start-ups. Subscription plans such as Dürr Dental’s “Vacuum-as-a-Service” exchange upfront savings for a 15-20% higher 10-year cost.

Dealer networks still serve independents who need local techs and same-day parts, though consolidation means the top three U.S. distributors handle 75% of the throughput. Refurbished-equipment portals offer certified dry vacuums at 40-60% discounts, supporting rural clinics but accounting for less than 7% of the overall dental suction systems market.

Geography Analysis

North America accounted for 42.67% of 2025 revenue, driven by EPA separator mandates and a mature DSO penetration projected to reach 40% of spend by 2030. Utility rebates in California, New York, and Massachusetts absorb 10-15% of dry-vacuum capex. Canadian clinics pursue province-level carbon credits that pay CAD 2,000-3,000 per operatory for ENERGY STAR pumps, while Mexico’s dental-tourism hubs retrofit suction rooms to reassure U.S. patients. Growth moderates as independent practitioners postpone upgrades amid net-income compression.

Asia-Pacific is advancing at a 5.89% CAGR through 2031, led by China’s 18% annual expansion in 6-plus-chair clinics and India’s Ayushman Bharat-funded builds that specify ISO 10637-compliant pumps. Thailand and South Korea cater to dental tourists who demand visible infection-control measures, thereby fueling the growth of centralized installations. Japan’s aging population pushes clinics toward ultra-quiet pumps to aid hearing-impaired elders, and Australia mandates amalgam separators nationwide by 2026.

Europe contributes 28% of revenue, with stringent Fit for 55 carbon goals accelerating the take-up of dry-vacuum technology. Germany enforces mercury limits that are 10 times stricter than U.S. rules, prompting the adoption of dual-stage separators. Britain’s NHS reimburses gear that cuts energy 25%, spurring 12% annual centralized-pump growth since 2023. France obliges biomedical-waste segregation, adding EUR 1,000-2,000 yearly to operating costs, yet aligning clinics with EU Waste directives. South America and MEA jointly account for about 17% of demand, with Brazil upgrading private practices and the UAE outfitting medical-tourism clinics with ISO 13485 gear.

Competitive Landscape

The dental suction systems market remains moderately fragmented. A-dec, Dürr Dental, Cattani, METASYS, Midmark, and Planmeca collectively hold close to 38% share. Each embeds IoT dashboards, noise-reduction engineering, and ENERGY-STAR-level efficiency. A-dec charges USD 50-75 per month for cloud analytics tied to its QuietCore+ pumps, boosting customer lifetime value by 30-40%. Takara Belmont touts ISO 13485 certification and 10-year durability tests spanning 108,000 chair cycles to win hospital contracts.

Regional rivals in China and South Korea underprice wet-ring systems for cost-sensitive buyers, while U.S. distributors launch private-label lines that dilute OEM margins. Subscription models address capital barriers but heighten lifetime cost, fostering recurring revenue for manufacturers. Product differentiation now coalesces around hybrid dry-wet pumps, active vibration damping, and factory-certified separator installation services that command 10-15% price premiums.

Dental Suction Systems Industry Leaders

A-Dec, Inc.

METASYS Medizintechnik GmbH

Midmark Corporation

Dürr Dental SE

Cattani S.P.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Planmeca debuted ProX GO wireless X-ray units aligned with mobile-clinic constraints

- December 2024: Patterson Companies was acquired for USD 4.1 billion by Patient Square Capital, accelerating e-commerce and private-label rollouts

Global Dental Suction Systems Market Report Scope

As per the scope of the report, dental suction systems are devices used to remove saliva, blood, and debris from a patient's mouth during dental procedures. They help maintain a clear working area and ensure patient comfort and safety. These systems typically include a suction tip, hose, and a vacuum unit to generate the necessary suction power.

The Dental Suction Systems Market is Segmented by Product (Dry Vacuum Systems and Wet-Ring Vacuum Systems), Installation Type (Chairside/Individual Operatory and Centralized Utility-Room Systems), End User (Dental Clinics/Offices, Hospitals, Mobile/Outreach Dental Units, and Academic & Research Institutes), Sales Channel (Direct OEM, Distributor/Dealer, and Online), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East & Africa). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Dry Vacuum Systems |

| Wet-Ring Vacuum Systems |

| Chairside/Individual Operatory |

| Centralized Utility-Room Systems |

| Dental Clinics/Offices |

| Hospitals |

| Mobile/Outreach Dental Units |

| Academic & Research Institutes |

| Direct (OEM) |

| Distributor/Dealer |

| Online |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| france | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product | Dry Vacuum Systems | |

| Wet-Ring Vacuum Systems | ||

| By Installation Type | Chairside/Individual Operatory | |

| Centralized Utility-Room Systems | ||

| By End User | Dental Clinics/Offices | |

| Hospitals | ||

| Mobile/Outreach Dental Units | ||

| Academic & Research Institutes | ||

| By Sales Channel | Direct (OEM) | |

| Distributor/Dealer | ||

| Online | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| france | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the dental suction systems market?

The market generated USD 577.95 million in 2026 and is forecast to reach USD 729.14 million by 2031.

Which product type leads global demand?

Dry vacuum systems hold 55.76% of 2025 revenue, thanks to energy savings and compliance benefits.

How fast is Asia-Pacific demand growing?

Asia-Pacific sales are advancing at a 5.89% CAGR through 2031, driven by urban clinic expansion and government subsidies.

Why are hospitals adopting new suction platforms?

Ambulatory surgery integration and Joint Commission rules require redundant, 24/7-rated pumps.

How are subscription models changing equipment procurement?

“Vacuum-as-a-service” plans shift costs from capex to opex, removing upfront spend but increasing 10-year ownership costs about 15-20%.

Page last updated on: