Dental Rapid Prototyping Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

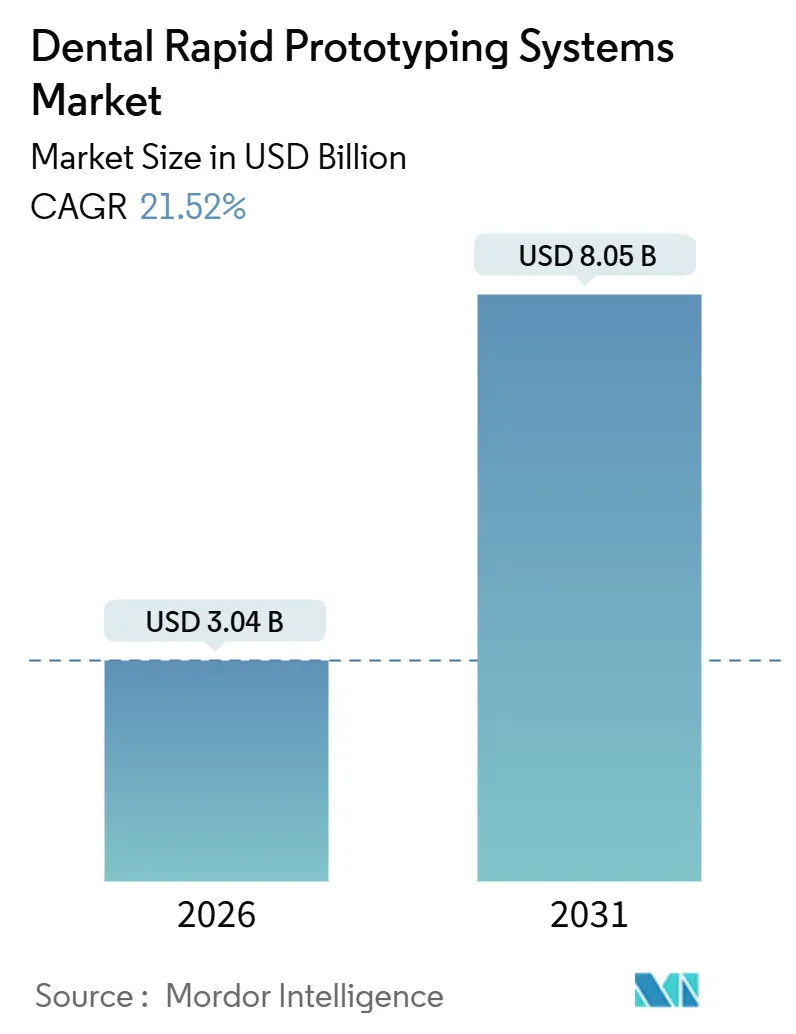

| Market Size (2026) | USD 3.04 Billion |

| Market Size (2031) | USD 8.05 Billion |

| Growth Rate (2026 - 2031) | 21.52% CAGR |

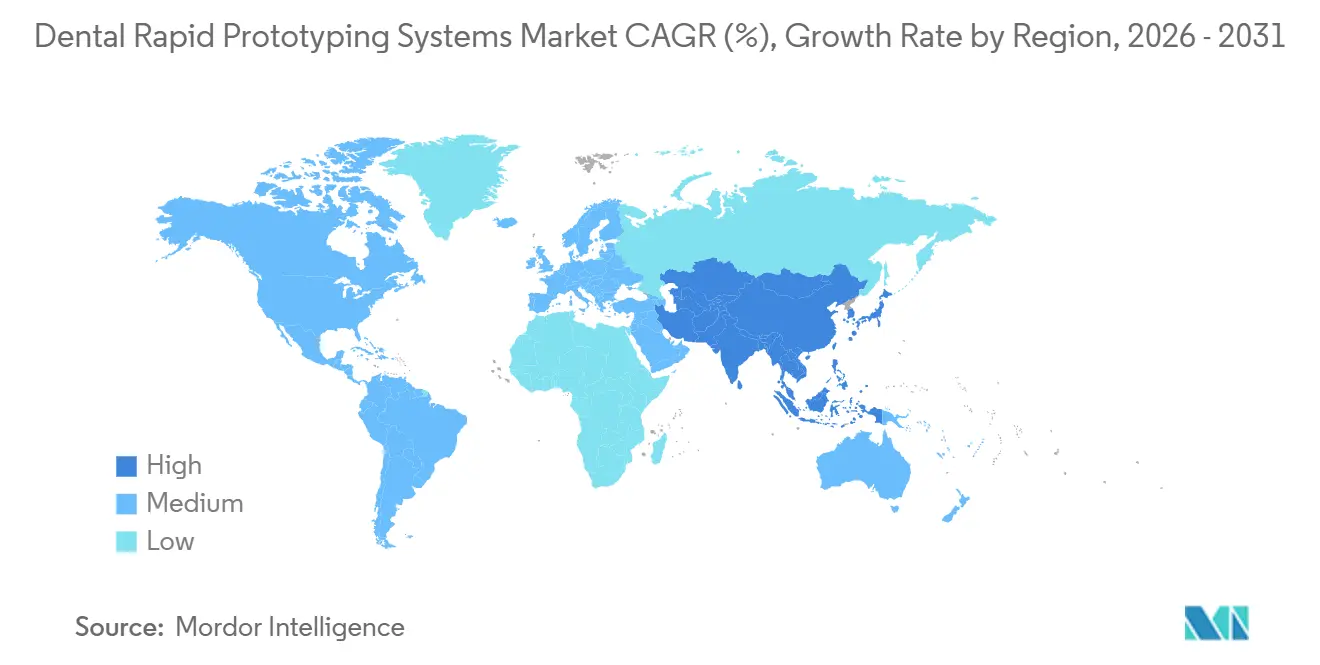

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

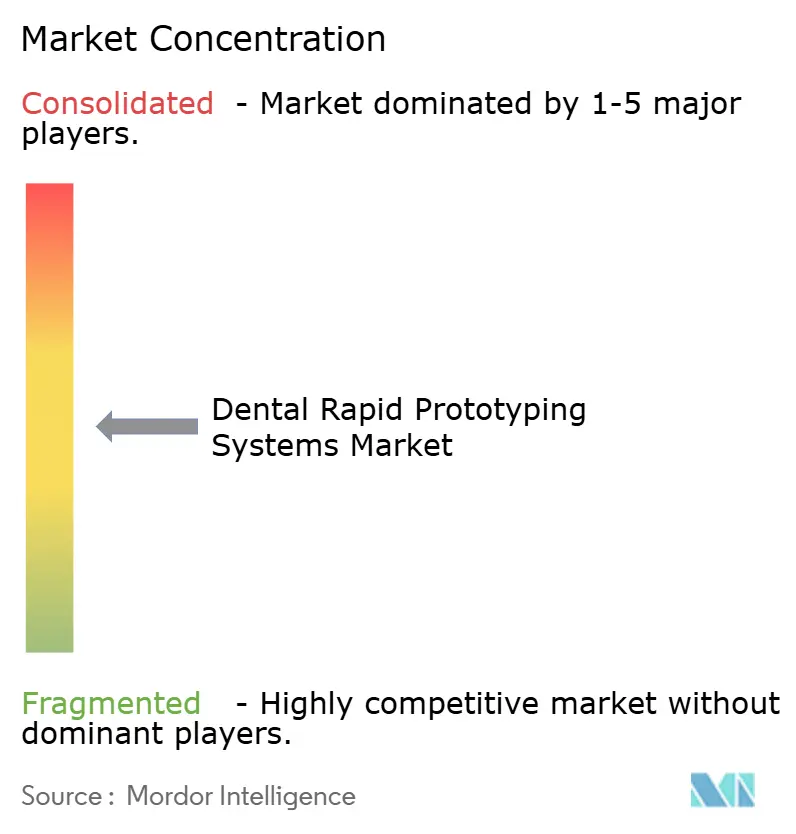

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Rapid Prototyping Systems Market Analysis by Mordor Intelligence

The dental rapid prototyping systems market size is estimated at USD 3.04 billion in 2026, and is projected to reach USD 8.05 billion by 2031, advancing at a 21.52% CAGR over the forecast period. Sustained double-digit growth reflects falling desktop printer prices, a widening menu of FDA-cleared biocompatible resins, and maturing AI design automation that collectively reduce payback for in-house production to well under one year for high-volume practices[1]U.S. Food and Drug Administration, “510(k) Premarket Notification Database,” fda.gov . Platform vendors now emphasize subscription bundles that roll hardware, software, and maintenance into flat monthly fees, converting capital purchases into predictable operating expenses. Rapid material innovation is also expanding the addressable use case set beyond study models toward crowns, bridges, and denture bases, compressing lead times from 5 days to same-day delivery. Competitive dynamics favor vertically integrated companies that control hardware, resins, and cloud design engines, enabling stickier recurring revenue and faster regulatory filings. Despite the momentum, regulatory complexity, cybersecurity threats, and the ongoing shortage of digitally skilled dental technicians, the dental rapid prototyping systems market's trajectory is tempered.

Key Report Takeaways

- By technology, stereolithography commanded a 45.55% revenue share in 2025, while Digital Light Processing is forecast to record a 22.25% CAGR through 2031.

- By material, photopolymer resins accounted for 81.53% of 2025 revenue, and metals are expected to expand at a 21.85% CAGR through 2031.

- By application, clear aligners and orthodontic models led with 36.23% of 2025 revenue, whereas surgical guides are projected to grow at a 22.55% CAGR.

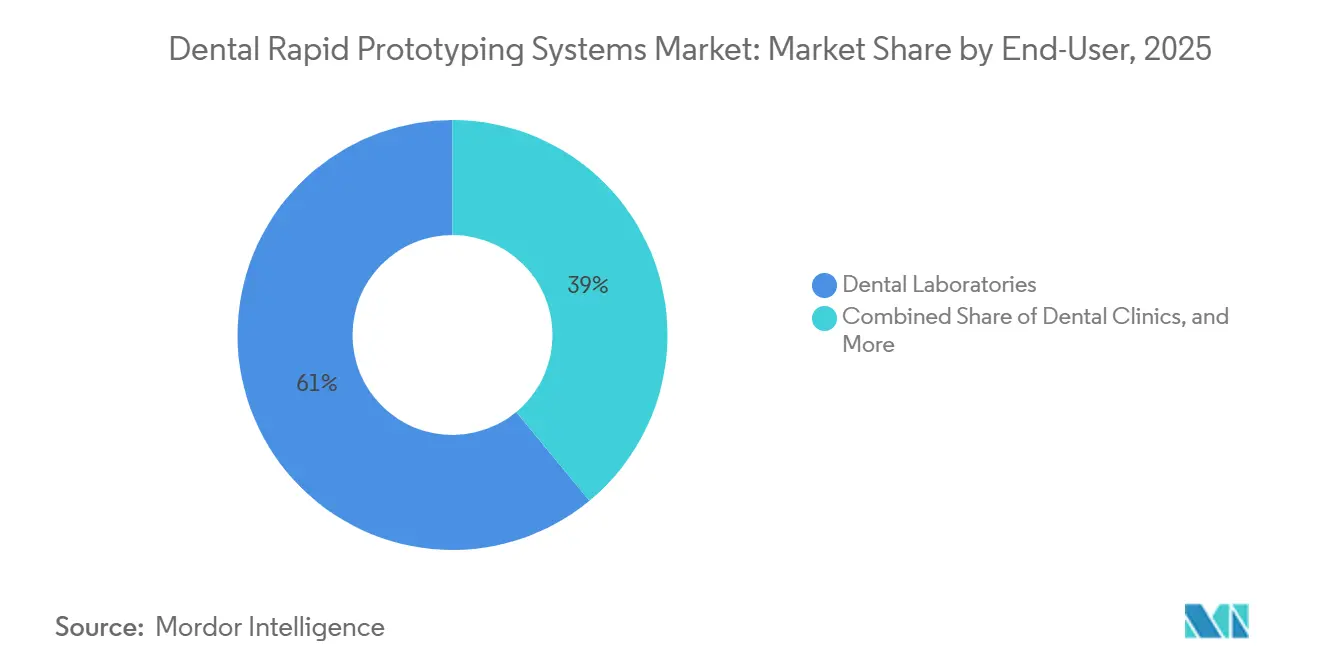

- By end user, dental laboratories captured 61.03% of 2025 revenue, and clinics are poised to grow at a 23.11% CAGR.

- By geography, North America accounted for 38.13% of 2025 revenue, yet Asia-Pacific is projected to register a 21.81% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dental Rapid Prototyping Systems Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining Vat-Polymerization Printer Costs | +4.2% | Global, with accelerated adoption in APAC and Latin America | Short term (≤ 2 years) |

| Biocompatible Resin Regulatory Approvals | +3.8% | North America & EU, with spillover to APAC | Medium term (2-4 years) |

| Demand for Customized Clear Aligners | +5.1% | Global, led by North America and APAC urban centers | Medium term (2-4 years) |

| Subscription-Based Hardware-as-a-Service Models | +2.9% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| AI-Assisted Workflow Automation | +3.6% | Global, with early gains in North America and Western Europe | Medium term (2-4 years) |

| Dental-Tourism Hub Investments | +1.9% | MEA (Turkey, UAE), Latin America (Mexico, Costa Rica), Southeast Asia (Thailand) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining Vat-Polymerization Printer Costs

List prices for desktop stereolithography and DLP units have fallen to the USD 6,000–8,000 range, roughly two-thirds below 2016 levels as component commoditization and regional manufacturing scale take hold[2]Formlabs, “Form 4 Launch,” formlabs.com. Formlabs’ Form 4, launched in 2024, pairs a sub-USD 4,000 entry price with 50% faster print speeds, enabling orthodontic and oral-surgery specialists to amortize the investment in four to six months when replacing outsourced night-guard or guide jobs. Chinese manufacturers such as Shining 3D offer DLP platforms priced under USD 5,000, further lowering the barrier for emerging-market clinics[3]Shining 3D, “Affordable DLP Platforms for Asia-Pacific,” shining3d.com . Low-volume general dentists still face longer payback periods due to throughput constraints. Yet, multi-application practices break down rapidly when aligner, model, splint, and provisional workflows share the same hardware. This price compression directly widens the installed base, underpinning the near-term expansion of the dental rapid prototyping systems market.

Biocompatible Resin Regulatory Approvals

The FDA cleared seven new Class II intraoral resins during 2024–2025, including Formlabs Premium Teeth Resin and Carbon FP3D, after each material satisfied ISO 10993 cytotoxicity, sensitization, and accelerated-aging tests. These clearances extend digital production from diagnostic models to definitive prosthetics, unlocking higher-value indications and accelerating subscription uptake in which resins and printers ship as integrated packages. Carbon’s FP3D showcases flexural strength above 65 MPa and elongation at break exceeding 20%, matching injection-molded thermoplastics while enabling chairside denture frameworks. In Europe, the Medical Device Regulation demands post-market surveillance files for 10 years, lengthening development cycles and favoring larger firms with dedicated regulatory teams. Once approvals are secured, validated material libraries become durable competitive moats that reinforce recurring revenue from consumables.

Demand for Customized Clear Aligners

Align Technology shipped 1.1 million Invisalign cases in Q3 2024, and Carbon’s L1 system produces up to 1,000 aligner models daily, with 40% resin savings compared with earlier SLA workflows, bringing the per-model cost close to USD 5. The ability to control design, nesting, and production in-house lets dental service organizations recapture margin previously lost to external labs and compress turnaround time to less than 24 hours. DLP hardware cures entire layers in under 10 seconds, making it the architecture of choice for high-throughput aligner workflows. SprintRay’s Pro 2 couples 4K projection with RayWare 3.0’s one-click nesting, cutting setup time to 2 minutes and boosting batch efficiency. Research into direct 3D-printed elastomeric aligners remains experimental but signals the next wave of workflow simplification for the dental rapid prototyping systems market.

AI-Assisted Workflow Automation

3Shape Automate processed more than 2.5 million cases in 2024, trimming design time per orthodontic model from 30 minutes to 90 seconds while achieving a 94% clinician acceptance rate. Convolutional neural networks segment teeth, predict occlusal contacts, and delineate margin lines, routing anomalous scans to human technicians only when needed. Subscription fees align with design volume, USD 0.99 per case for large labs versus USD 14.99 for single-location practices, eliminating the USD 25,000 upfront license cost typical of legacy CAD platforms. Straumann’s CARES ecosystem embeds AI for implant planning, auto-positioning fixtures based on bone density and nerve proximity, cutting surgical complications by roughly 15% in early trials. AI also accelerates post-processing; Carbon’s AO Backpack

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Expenditure for Industrial Systems | -2.7% | Global, with acute impact in price-sensitive APAC and Latin America markets | Medium term (2-4 years) |

| Regulatory Complexity & Approval Costs | -3.4% | EU (MDR), North America (FDA 510(k)), with cascading delays in APAC | Long term (≥ 4 years) |

| Cybersecurity Risks in Cloud Workflows | -1.8% | Global, concentrated in North America and EU where cloud adoption is highest | Short term (≤ 2 years) |

| Digital-Skills Shortage among Dental Technicians | -2.3% | Global, with severity in rural North America, Southern Europe, and emerging APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for Industrial Systems

Powder-bed metal platforms, such as the EOS M 100 Dental, list between USD 150,000 and USD 400,000, limiting adoption to high-throughput labs and hospital departments. While practices producing 15 or more crowns a month can break even within six months when replacing USD 100 outsourcing fees, general dentists fabricating fewer than eight units per month face multiyear payback horizons. Subscription models mitigate some barriers. Carbon bundles hardware, software, and repair guarantees into a single operating fee, but material costs for cobalt-chrome and zirconia powders remain steep, adding 15% to per-unit expenses. Desktop Metal targets the mid-market with Flexcera, a USD 50,000 hybrid resin-ceramic platform, though sintering for zirconia crowns still requires 12-hour furnace cycles. Until price parity narrows, the capital hurdle will restrain full penetration of the Dental rapid prototyping systems market.

Regulatory Complexity and Approval Costs

Submitting a Class II resin under the FDA 510(k) pathway typically takes 12–18 months and costs USD 80,000–120,000 for biocompatibility and accelerated-aging studies. The European Union’s Medical Device Regulation adds periodic safety updates and 10-year technical-file retention, inflating compliance outlays by an additional EUR 50,000–150,000 per formulation. Smaller material startups often lack the infrastructure to navigate multi-jurisdictional filings, ceding share to vertically integrated incumbents that amortize regulatory overhead across broader portfolios. ISO 13485 quality system certification requires annual audits, and any nonconformity can stall product launches for up to 1 year. Fragmented frameworks in Asia add further complexity; China’s tiered approval scheme now recognizes FDA or CE marks, yet India still requires country-specific clinical data, which splinters supply chains and delays market entry. These headwinds collectively shave momentum from the Dental rapid prototyping systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: DLP Gains on SLA’s Installed Base

Digital Light Processing is projected to expand at a 22.25% CAGR through 2031, narrowing the gap with stereolithography’s current 45.55% revenue share thanks to superior throughput in aligner-model production. SprintRay Pro 2 nests 42 full-arch models in a 10-hour shift and completes each print in under 15 minutes, enabling batch aligner workflows that laser-based SLA systems cannot match.

SLA remains the preferred choice for crown margins and implant analogs that demand sub-25-micron accuracy, a niche that helps maintain its lead within the Dental rapid prototyping systems market. Fused Deposition Modeling remains a prototyping option, but its visible layer lines and limited biocompatible filaments limit its use to academic research. Selective Laser Sintering and material jetting together account for a small slice of revenue due to capital investments exceeding USD 200,000 and narrow material catalogs. However, Desktop Metal’s multi-material powder-bed roadmap could disrupt the status quo by 2027.

By Material: Metals Ascend as Regulatory Barriers Fall

Photopolymer resins delivered 81.53% of 2025 material revenue, anchored by FDA-cleared options such as Carbon FP3D and Formlabs Premium Teeth Resin. Metals are forecast to expand at a 21.85% CAGR, buoyed by cobalt-chrome and titanium frameworks printed on systems like EOS M 100 Dental, which achieves 99.5% part density at 50-micron layers.

Plastics such as PEEK and ULTEM fill temporary restoration niches, while ceramics remain constrained by long sintering cycles and high per-kilogram costs, despite Lithoz CeraFab’s 1,200 MPa flexural strength crowns. Desktop Metal’s Flexcera combines ceramic and resin chemistries on a single USD 50,000 platform, targeting mid-sized labs that cannot justify separate kilns. As ISO- and ASTM-aligned standards for additive powder quality mature, metals will claim a larger share of the Dental rapid prototyping systems market, particularly in full-arch implant applications.

By Application: Surgical Guides Outpace Aligners on Implant Volume

Clear aligners and orthodontic models generated 36.23% of 2025 revenue, underpinned by Invisalign’s 1.1 million unit shipments and Carbon’s high-throughput resin workflows[4]Align Technology, “Q3 2024 Results,” aligntech.com. Looking ahead, surgical guides are predicted to grow at a 22.55% CAGR, benefiting from cone-beam CT integration that delivers implant placement within 1.5 mm of plan and trims chairtime by 20%.

Crown and bridge models continue to serve as master dies for investment casting, yet direct 3D-printed restorations threaten to erode this share as biocompatible resins receive more clearances. Denture bases remain a smaller niche, though Flexcera’s elongation-at-break above 20% positions it to capture same-day partial frameworks. Momentum in surgical guides underscores the versatility of resin platforms and is poised to lift the market share of dental rapid prototyping systems held by implant-focused specialists.

By End-User: Clinics Disrupt Labs’ Outsourcing Model

Dental laboratories retained 61.03% of 2025 revenue, but clinics are on track for a 23.11% CAGR, as sub-USD 8,000 desktop printers enable chairside fabrication of night guards, provisional restorations, and guides. High-volume orthodontic and implant practices recoup printer investments in as little as 4 months by replacing USD 100+ outsourced units, while also cutting delivery from 5 days to same-day.

Labs retain an edge in complex multi-unit and metal frameworks that require industrial powder-bed systems, yet their traditional outsourcing role is narrowing as clinics vertically integrate. Hospitals and academic centers occupy modest shares, focusing on maxillofacial reconstruction guides and biomaterial research, respectively. Subscription bundles that shift expenditure from capital to operating costs further accelerate clinic uptake, reinforcing the structural shift within the dental rapid prototyping systems market.

Geography Analysis

North America generated 38.13% of 2025 revenue, driven by mature CAD/CAM adoption and 14,800 iTero scanner installations in Q3 2024. Early FDA clearances foster rapid resin deployment, and reimbursement pathways favor digital workflows. Europe follows, yet the Medical Device Regulation’s stringent surveillance obligations extend time-to-market by up to 18 months, nudging some vendors to prioritize faster-moving regions. Germany, France, and the United Kingdom dominate regional demand, supported by dense lab networks and high implant volumes.

Asia-Pacific is the fastest-growing region, projected at a 21.81% CAGR through 2031. Dental-tourism hubs in Thailand and South Korea, plus sub-USD 10,000 DLP systems from Shining 3D, democratize access for price-sensitive clinics. China’s tiered approval scheme recognizes FDA or CE marks, compressing regulatory timelines and expediting launches for Formlabs and Stratasys. South America and the Middle East & Africa trail, hampered by import tariffs and lower purchasing power, yet pockets such as Dubai’s implant centers invest aggressively in industrial metal printers.

Competitive Landscape

The dental rapid prototyping systems market is moderately fragmented. Dentsply Sirona reported USD 267 million in digital equipment revenue during Q3 2024, illustrating CAD/CAM incumbents’ continued scale. Straumann’s USD 204 million haul in digital solutions in H1 2024 reflects its end-to-end ecosystem spanning intraoral scanning to aligner fulfillment.

Pure-play additive firms emphasize recurring revenue. Carbon’s subscription model bundles over-the-air firmware updates every eight weeks, predictive maintenance, and 48-hour repair guarantees, boosting customer lifetime value and lowering churn. Formlabs champions open-material validation to widen resin choices, while SprintRay targets chairside workflows with software-led automation.

Desktop Metal’s USD 27 million Aerosint buyout augments its multi-material powder spreading IP, which could disrupt metal frameworks by 2027. Patent filings concentrate on resin chemistry and AI-based support generation, with the USPTO recording 12 new Desktop Metal applications in 2024. Regulatory expertise

Dental Rapid Prototyping Systems Industry Leaders

Dentsply Sirona

Planmeca Oy

3D Systems Corporation

Straumann Group

Rapid Shape GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Rapid Shape unveiled RS VIVO, a dental resin portfolio covering permanent crowns, temporaries, and splints, broadening chairside restorative options.

- September 2025: SprintRay acquired the EnvisionTEC/ETEC dental portfolio, including patents and trademarks, to deepen its material and hardware IP stack.

Global Dental Rapid Prototyping Systems Market Report Scope

As per the report's scope, dental rapid prototyping systems are advanced digital manufacturing technologies used to create precise dental models, surgical guides, crowns, bridges, and aligners directly from digital scans. These systems use techniques such as 3D printing and CAD/CAM to produce customized dental components rapidly. They improve accuracy, reduce turnaround time, and support efficient, patient-specific dental treatments.

The dental rapid prototyping systems market segmentation includes technology, material, application, end-user, and geography. By technology, the market is segmented into stereolithography (SLA), digital light processing (DLP), fused deposition modeling (FDM), selective laser sintering (SLS), and material/binder jetting. By material, the market is segmented into photopolymer resins, plastics (thermoplastics), metals, and ceramics & glass-ceramics. By application, the market is segmented into clear aligners & orthodontic models, crown & bridge models, surgical guides, denture bases & teeth, and dental implants & frameworks. By end-user, the market is segmented into dental laboratories, dental clinics, hospitals, and academic & research institutes. By geography, the global market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Stereolithography (SLA) |

| Digital Light Processing (DLP) |

| Fused Deposition Modeling (FDM) |

| Selective Laser Sintering (SLS) |

| Material / Binder Jetting |

| Photopolymer Resins |

| Plastics (Thermoplastics) |

| Metals |

| Ceramics & Glass-Ceramics |

| Clear Aligners & Orthodontic Models |

| Crown & Bridge Models |

| Surgical Guides |

| Denture Bases & Teeth |

| Dental Implants & Frameworks |

| Dental Laboratories |

| Dental Clinics |

| Hospitals |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Stereolithography (SLA) | |

| Digital Light Processing (DLP) | ||

| Fused Deposition Modeling (FDM) | ||

| Selective Laser Sintering (SLS) | ||

| Material / Binder Jetting | ||

| By Material | Photopolymer Resins | |

| Plastics (Thermoplastics) | ||

| Metals | ||

| Ceramics & Glass-Ceramics | ||

| By Application | Clear Aligners & Orthodontic Models | |

| Crown & Bridge Models | ||

| Surgical Guides | ||

| Denture Bases & Teeth | ||

| Dental Implants & Frameworks | ||

| By End-User | Dental Laboratories | |

| Dental Clinics | ||

| Hospitals | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is global adoption of Dental rapid prototyping systems?

The Dental rapid prototyping systems market is advancing at a 21.52% CAGR, fueled by falling printer prices and expanding FDA-cleared resin libraries.

Which technology is growing quickest?

Digital Light Processing is forecast to expand at 22.25% CAGR through 2031 thanks to its throughput advantage in aligner-model production.

Why are clinics bringing production in-house?

Sub-USD 8,000 desktop printers and subscription bundles cut payback to under 12 months, letting clinics recapture lab margins and offer same-day appliances.

What materials dominate current usage?

Photopolymer resins account for 81.53% of 2025 revenue due to multiple FDA-cleared biocompatible formulations for crowns, bridges, and dentures.

Which region will lead growth through 2031?

Asia-Pacific is projected to grow at 21.81% CAGR, supported by dental tourism and locally manufactured low-cost DLP systems.

Page last updated on: