Dental Putty Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

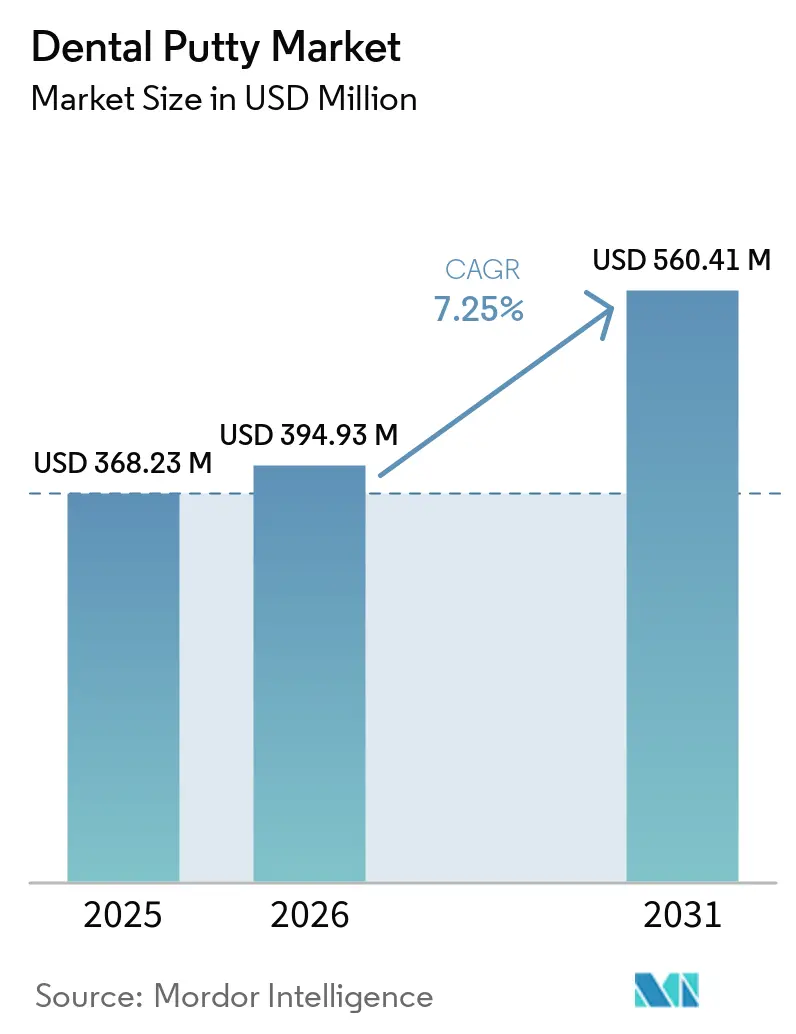

| Market Size (2026) | USD 394.93 Million |

| Market Size (2031) | USD 560.41 Million |

| Growth Rate (2026 - 2031) | 7.25% CAGR |

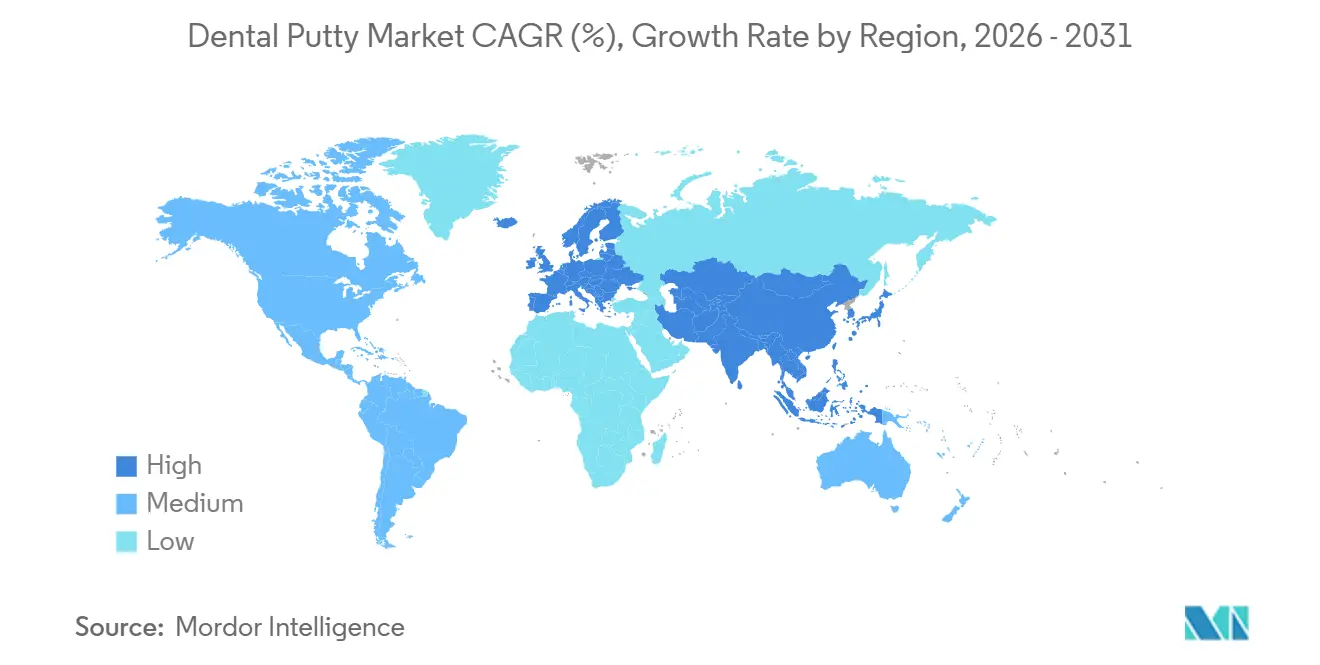

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Putty Market Analysis by Mordor Intelligence

The Dental Putty Market size is projected to expand from USD 368.23 million in 2025 and USD 394.93 million in 2026 to USD 560.41 million by 2031, registering a CAGR of 7.25% between 2026 to 2031.

Analog impression materials continue to hold a firm footing even as digital scanning gains ground, since many multi-unit and full-arch cases still rely on physical impressions for fit verification. North America led in 2025, supported by standardized clinical workflows and strong consumables purchasing. Asia-Pacific is the growth leader through 2031 as dental tourism expands, middle-income patient pools rise, and large clinics scale their capacity. In material chemistry, VPS retains a durable position due to handling ease and reliable dimensional stability, while polyether accelerates in complex cases that benefit from hydrophilicity and higher rigidity. Applications reflect this clinical reality, with prosthodontics anchoring volume and implantology advancing faster on the back of more demanding protocols where analog verification remains common.

Key Report Takeaways

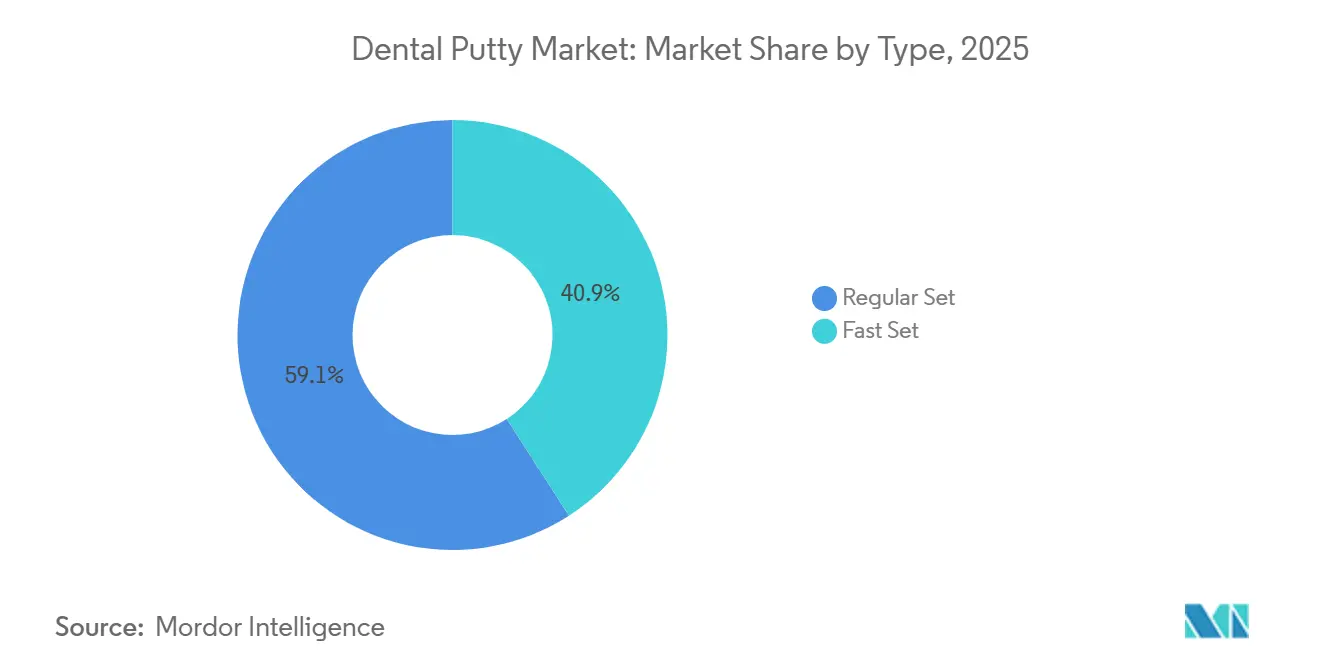

- By type, regular-set putties held 59.12% share in 2025, while fast-set formulations are set to grow at 7.98% CAGR through 2031 in the dental putty market.

- By product type, VPS led with 58.91% revenue share in 2025, while polyether is projected to expand at an 8.13% CAGR through 2031.

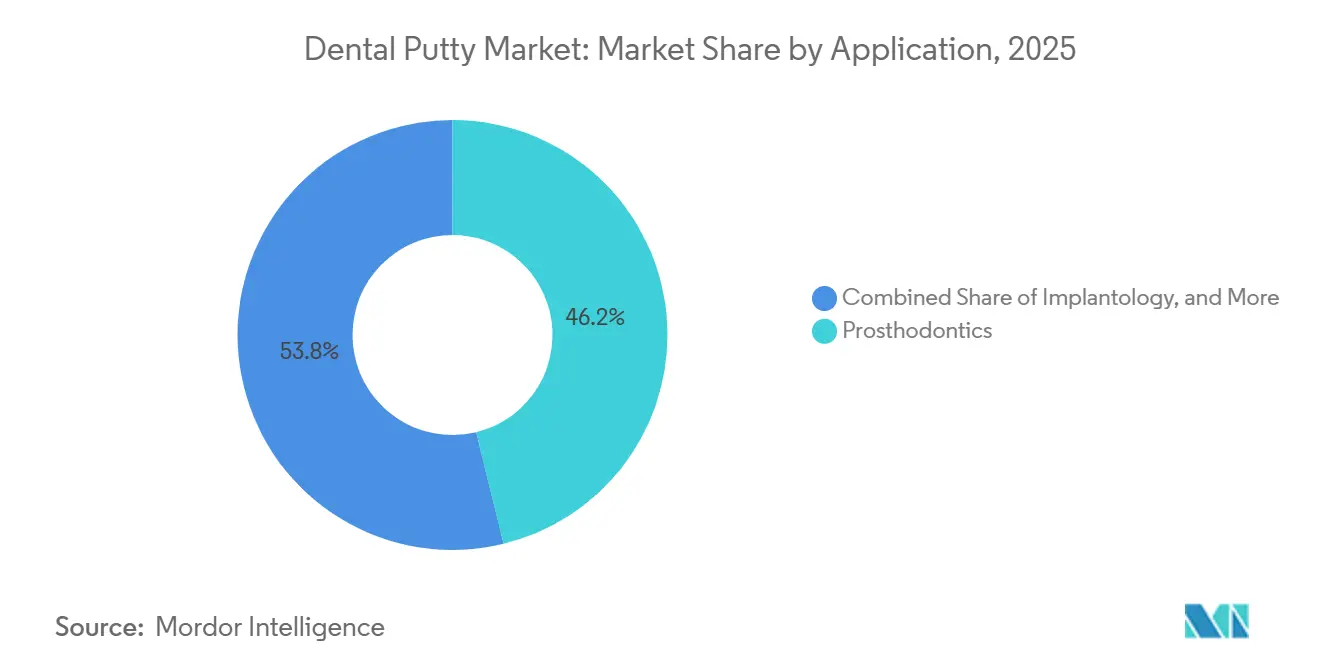

- By application, prosthodontics accounted for a 46.18% share in 2025, while implantology is forecast to be the fastest-growing application at an 8.95% CAGR through 2031 in the dental putty market.

- By delivery form, automix cartridges accounted for 51.32% share in 2025 in the dental putty market, while hand-mix jars are projected to grow at a 7.65% CAGR through 2031.

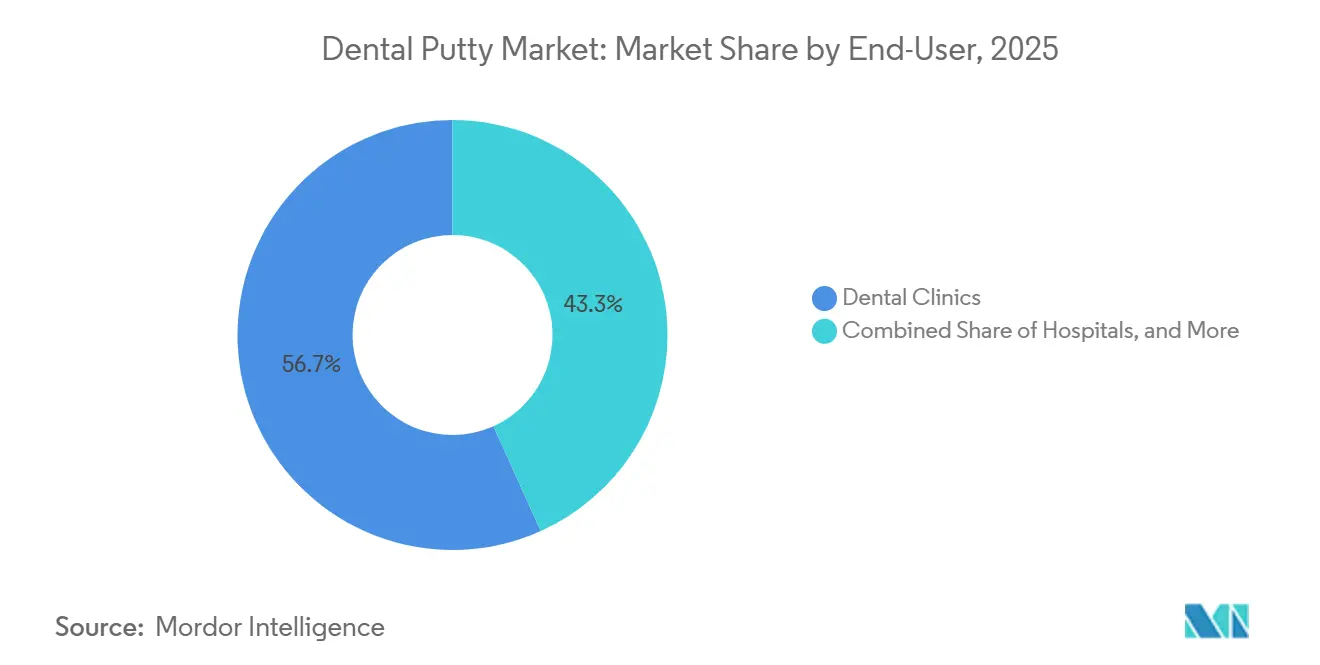

- By end-user, clinics held 52.76% share in 2025, while dental laboratories are anticipated to record the fastest growth at an 8.48% CAGR through 2031.

- By geography, North America held 36.74% of the market share in 2025, while Asia-Pacific recorded the highest projected CAGR at 9.73% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dental Putty Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Oral Diseases and Edentulism | +1.8% | Global, pronounced in South Asia (17.57% periodontitis prevalence), Latin America (7.39% edentulism rate) | Medium term (2-4 years) |

| Growing Demand for Restorative and Prosthodontic Procedures | +1.6% | North America and Europe, Asia-Pacific growth corridors | Long term (≥ 4 years) |

| Advancements in VPS/Polyether Putty Performance | +1.4% | Global, early adoption in clinical research centers across Germany, Japan, U.S. | Short term (≤ 2 years) |

| Aging Demographics Increasing Complex Indirect Cases | +1.9% | Asia-Pacific core markets and select Middle East and Africa geriatric segments | Long term (≥ 4 years) |

| Analog Impressions Remain Preferred for Challenging Cases (Full-Arch, Subgingival) | +0.9% | National, with early gains in specialized implant clinics including Chilean urban centers and globally dispersed hubs | Medium term (2-4 years) |

| Capital Constraints Slowing Scanner Adoption in Cost-Sensitive Clinics | +0.7% | Asia-Pacific, Latin America, Sub-Saharan Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Oral Diseases and Edentulism

The dental putty market benefits from a sustained clinical need that tracks the global burden of oral disease. According to the Journal of Periodontal Research, periodontitis remains one of the most prevalent global diseases, calling the newest global data a “serious wake-up call.” It emphasized that severe periodontitis affects ~11% of the world’s population, consistent with Global Burden of Disease (GBD) estimates, moving edentulism higher among conditions that drive disability, which sustains indirect restorative demand for precision impressions in complex rehabilitations.[1]University of BirminghamThe latest global disease data for Periodontitis: a serious wake-up call! China is expected to account for 130.23 million edentulous individuals by 2050, or 19.67% of the global total, reinforcing the need for accurate impression capture across large treatment volumes. In the United States, surveillance data for 2017 to early 2020 show untreated caries in 21% of adults aged 20 to 64 and 13% of seniors, with much higher rates among high-poverty groups and current smokers, which underpins steady indirect case flow and periodic full-arch rehabilitations.[2]Centers for Disease Control and Prevention, “Oral Health Surveillance Report: Dental Caries, Tooth Retention, and Edentulism, United States, 2017–March 2020,” U.S. Department of Health and Human Services Manufacturers also cite edentulism trends to justify investments in denture and overdenture workflows, such as the Dentsply Sirona partnership with Formlabs that aligns materials, printers, and validation to scale digital denture production while maintaining analog intake when clinically appropriate. Analyses from global disease-burden programs have recorded minimal progress in reducing the total population affected by oral conditions, which continues to reinforce the dental putty market across prosthodontics and implantology.

Growing Demand for Restorative and Prosthodontic Procedures

The dental putty market tracks long-term restorative needs shaped by aging cohorts who retain more natural teeth yet require complex indirect treatments. U.S. adults aged 65 and older retain a mean of 19.8 permanent teeth compared with 27 among those aged 20 to 34, a pattern that concentrates multi-unit bridges, overdentures, and precision partial frameworks in senior populations who often need accurate margin capture and stable occlusal records. Digital technologies are accelerating in labs and clinics, yet verification steps for intricate multi-unit cases often remain analog, especially for subgingival margins or full-arch passive fits, which sustain routine use of putty-wash techniques within hybrid workflows. Partnerships that integrate materials with validated production routes, such as Dentsply Sirona’s collaboration with Formlabs on printable denture systems, further normalize hybrid protocols where analog impressions feed digital design and manufacture. North American group practices and integrated lab networks also standardize restorative pathways, where analog and digital complement each other rather than displace, supporting steady demand for premium putty chemistries that reduce rework and remakes. European markets maintain broad reimbursement for essential restorative services in many countries, and clinics invest in fit-critical materials to reduce chairside adjustments and follow-up visits. Together these procedural and payment dynamics maintain a stable restorative base that underpins long-run visibility for the dental putty market.

Advancements in VPS/Polyether Putty Performance

Continuous formulation updates improve handling, accuracy, and chairside efficiency, which keeps the dental putty market relevant within digital ecosystems. Polyether products with intrinsic hydrophilicity, such as Solventum’s Impregum line, are engineered to displace moisture in subgingival settings while delivering “snap-set” kinetics that balance workable time with a fast, predictable set, which is valuable in hemostasis-sensitive fields.[3]Solventum, “3M Impregum Polyether Impression Materials VPS materials also advance in bite registration and occlusal accuracy, as seen in GC America’s EXABITE II, which brings thixotropic stacking, rapid intraoral set, and high post-set hardness designed to resist distortion during articulation and transport to the lab.[4]GC America, “EXABITE II,” GC America Delivery systems evolve in parallel, with 50 ml cartridge improvements that simplify viscosity selection and reduce dispensing errors across multi-viscosity, double-mix techniques that many clinics routinely deploy. Adjacent consumables also reduce pre-impression steps, such as VOCO’s retraction paste with a two-viscosity aluminum chloride formulation that targets sulcular conditioning while claiming significant procedural time savings in cases where cord placement can be avoided.These material-science and delivery gains compress workflow times, extend detail capture in moisture-rich sites, and improve consistency for putty-wash approaches that are still common in complex indirect procedures. As labs and clinics co-deploy CAD software and printers, these analog inputs remain easy to digitize through desktop scanning, preserving practical flexibility for teams that want the assurance of a physical master.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Intraoral Scanners in Selected Specialties | -1.2% | North America and Europe for orthodontics and single-crown workflows | Short term (≤ 2 years) |

| Higher Cost of Premium Putties Vs Alginate and Technique Sensitivity | -0.7% | Global, with cost pressure acute in Eastern Europe and Southeast Asia | Medium term (2-4 years) |

| EU MDR Compliance Costs and SKU Rationalization in Europe | -0.5% | Europe including Germany, France, Italy | Short term (≤ 2 years) |

| Lab Digitalization Steering Clinicians Toward Scan-First Workflows | -0.9% | Asia-Pacific growth corridors and North American DSO networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU MDR Compliance Costs and SKU Rationalization in Europe

European regulations continue to shape investment and portfolio choices for impression-material suppliers, which modestly weighs on the dental putty market. The European Commission’s targeted MDR revision proposal in December 2025 pursued selective simplifications for custom-made devices, yet standard off-the-shelf impression materials remain subject to strict clinical evaluation, documentation, and ongoing surveillance requirements, keeping regulatory workloads elevated. The required Summary of Safety and Clinical Performance documentation, equivalence assessments, or de novo clinical evidence, and notified-body cycles extend timeframes for updates and new variants, which can slow the refresh cadence for smaller SKUs that serve narrow use cases. Larger incumbents can absorb these fixed costs more easily by spreading them across wider catalogs, which can reinforce their position in core markets as smaller players rationalize portfolios. Company disclosures in 2025 reported measured portfolio streamlining in Europe, consistent with a focus on core chemistries and high-velocity formats in the face of regulatory friction. Multinational suppliers with multi-brand ecosystems and integrated distribution have highlighted resilience in this environment, which points to a steady supply of key putty families rather than a proliferation of micro-variants. The overall effect is a modest dampener on near-term innovation breadth in Europe, yet market access for major VPS and polyether systems remains unchanged.

Lab Digitalization Steering Clinicians Toward Scan-First Workflows

Laboratory investment in CAD software, integrated milling, and 3D printing continues to reshape intake preferences in ways that lean toward digital scans, which is a mild restraint for the dental putty market. Cloud platforms and workflow suites in large group practices encourage standardized case routing and file sharing that can shorten lab turnaround when inputs are already in digital formats. Desktop scanners, updated scan modes, and support for articulator capture help labs ingest both physical impressions and restorations for reliable digitization, which creates a bridge for clinics that operate hybrid protocols. Scan ecosystems also expand with connectors and integrations that simplify handoffs between acquisition and design environments, which incrementally reduce friction to go digital-first in single-unit and orthodontic cases. That said, for full-arch and immediate-load situations, many labs still outline workflows that include an analog verification step to support passive fit and detail in moisture-prone sites. The practical reality is a hybrid model where digital gains speed while analog preserves accuracy for the most challenging cases, gently tilting intake toward scans without displacing putty-wash protocols wholesale. The net effect is a small drag on growth that is partially offset by stable analog demand in complex rehabilitations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Fast-Set Formulations Narrow Regular-Set’s Historical Lead

Regular-set dental putty held 59.12% share in 2025, reflecting consistent use in multi-step protocols that benefit from longer workable time. Fast-set variants are projected to grow at 7.98% CAGR, helped by clinicians' focus on efficient chairside timing and streamlined case progression in implant and multi-unit indications. Clinical users adopt fast-set to reduce intraoral time while sustaining margin fidelity, which reduces adjustments and remakes in cases that still need analog verification. Vendor portfolios have been updated to bring shorter set times without sacrificing flow into subgingival areas, as seen in polyether families that emphasize predictable kinetics and handling control. Labs that accept both digital files and physical impressions remain attentive to impression surface quality, which supports sustained use of proven regular-set chemistries in crown-and-bridge work. The result is a gradual shift toward faster options where case complexity allows them, rather than a sharp pivot away from longer sets.

Fast-set progress reflects product design aimed at faster intraoral set while protecting detail capture at the margin. In time-sensitive protocols such as immediate posterior work or retakes, fast-set putties can keep total chair time low, while regular-set options remain the default for precise tray seating and wash capture. Advanced families with robust flow control and rapid final set times are designed to protect sulcular landmarks where moisture or blood can obscure lines. Training and team familiarity also play a role, since the step sequence and tray management in fast-set variants can differ from legacy routines. Over the forecast period, both sets remain in broad use, with fast-set growth outpacing the category as more clinics pursue shorter appointments and higher daily throughput.

By Product Type: VPS Dominance Persists, Polyether Gains in Implant Niches

VPS putty accounted for 58.91% share in 2025, supported by a stable cost-to-performance balance and wide availability across delivery formats. Polyether is set to grow faster at 8.13% CAGR as implantologists and prosthodontists prioritize intrinsic hydrophilicity and higher post-set rigidity for multi-unit, moisture-challenged cases that benefit from minimal elastic recovery during model work. Field evidence and product specifications emphasize polyether’s ability to capture subgingival margins with fewer voids while maintaining the snap-set behavior that helps manage hemostasis windows. VPS remains the workhorse in general practice, given familiar handling, ease of mixing in cartridges, and consistent elastic recovery that many teams have built into their tray and wash combinations. Manufacturers continue to position complementary viscosities that support double-mix approaches for crown-and-bridge care, which is where VPS shows resilient traction.

Multi-brand portfolios that include both chemistries allow clinics and labs to match material choice to case needs without switching vendors, which reduces training time and supports consistency in lab communication. For challenging implant impressions, polyether’s rigidity helps maintain coping stability during master-cast fabrication and tower alignment, while VPS remains favored for many single- and multi-unit tooth-borne cases due to handling speed and familiarity. The long-term picture shows durable co-existence, with VPS anchoring broad indications and polyether expanding in demanding sites where marginal fidelity under moisture is non-negotiable. Overall, the dental putty market advances through chemistry choice rather than displacement, reflecting case-by-case selection inside hybrid analog-digital workflows.

By Application: Implantology Velocity Offsets Prosthodontics’ Volume

Prosthodontics held 46.18% share in 2025, reflecting the sustained need for fixed bridges, removable dentures, and full-arch rehabilitations that lean on putty-wash accuracy for subgingival landmarks and interarch records. Implantology is forecast to grow fastest at 8.95% CAGR as more clinics expand treatment offerings, shorten appointment cycles with integrated lab support, and maintain analog verification to secure passive fits. Global burden data indicate that edentulism remains elevated in several regions and could rise substantially in absolute terms as populations age, which stabilizes volume for denture and overdenture workflows that retain analog impression steps. Manufacturers that support digital denture manufacture while validating materials and processes reflect this hybrid reality, where analog intake precedes CAD design and milling. As implant therapy expands, clinical teams continue to rely on polyether and advanced VPS formulations to manage sulcular moisture and to stabilize components during work-up, particularly in full-arch and immediate-load cases.

Restorative disciplines such as indirect crown-and-bridge remain stable users of VPS for familiar double-mix approaches, while implant surgeons and prosthodontists lean into polyether for its hydrophilicity and rigidity during post-set handling. Lab systems that speed denture and bridge production also maintain straightforward pathways to ingest physical impressions, which supports clinics that want a simple analog capture followed by digital design. These dynamics yield an application mix where volume-leading prosthodontics coexists with a faster-rising implantology segment, each with clear material preferences that sustain category breadth in the dental putty market.

By Delivery Form: Automix Cartridges Lead, Yet Hand-Mix Defies Obsolescence

Automix cartridges held 51.32% share in 2025, reflecting ergonomic advantages for base-catalyst ratios, reduced void formation, and consistent chairside delivery. Hand-mix jars, often expected to fade, maintain relevance and are projected to grow at 7.65% CAGR as cost-sensitive clinics and experienced technicians value lower upfront costs and tactile control. Unit-dose packs remain a smaller niche that serves infection-control priorities, though higher per-impression costs limit adoption in high-throughput settings. Equipment ecosystems that integrate automated mixing also reinforce cartridge use, particularly in clinics with multi-operatory turnover and labs that standardize double-mix viscosity pairings. As portfolio updates improve visibility of cartridge contents and compatibility of mixing tips, single-practice teams can cut dispensing errors and improve reproducibility.

Despite the rise of automix, hand-mix jars continue to serve practitioners balancing cost control with reliable performance in established protocols. Hand-mix selection also aligns with local supply dynamics and technician familiarity, anchoring a steady base even as larger practices lean into automix systems. Manufacturers that support both delivery forms preserve flexibility for clinics to match format to procedure complexity while remaining with a single brand family. Automated mixing units align with team training, predictable extrusion rates, and clinic or lab productivity plans, which helps maintain the leading role of automix in settings that optimize throughput. Over time, both delivery forms will remain in use, reflecting the everyday practicality of analog capture alongside digital design in the dental putty market.

By End-User: Clinics Dominate, Labs Accelerate via Digital Integration

Dental Clinics accounted for 52.76% share in 2025, reflecting their central role as the point of impression capture across prosthodontic, implant, and restorative pathways. Laboratories are projected to grow at 8.48% CAGR as they invest in integrated software, scanning, and printing that increase throughput and make hybrid intake easier for referring clinics. Data from large vendors show that consumables that include impression materials maintain a durable contribution to regional results, which underscores the resilience of chairside analog steps in daily practice. Labs often lead digitization while continuing to accept physical impressions, then scan and process them for CAD production, which allows clinics to bridge analog capture with modern fabrication tools. Hospitals and academic centers contribute smaller volumes yet serve as proving grounds for advanced materials and workflows, influencing training and future practice norms.

Clinics’ material choices are shaped by case complexity, time targets, and payer constraints, which sustain a range of chemistries and set times in daily use. Laboratories amplify product development with real-world feedback on flow behavior, snap-set reliability, and dimensional stability, which helps vendors optimize variants that reduce remakes. As more labs scale digital dentures and bridges, they continue to outline straightforward ways to digitize analog impressions for advanced production while keeping options open for full-arch verification and occlusal validation. This division of roles maintains clinics as the principal end-user today while laboratories grow faster, each anchoring complementary positions within the dental putty market.

Geography Analysis

North America held 36.74% share in 2025, supported by mature procurement in group practices, access to advanced materials, and integrated lab relationships. Asia-Pacific is the fastest-growing region with a 9.73% projected CAGR to 2031 as clinics add capacity, dental tourism scales, and middle-income patient pools expand in China, India, and Southeast Asia. Europe held a significant position in 2025, though companies continue to navigate MDR-driven regulatory workloads for consumables and updates, which adds cost and time without changing access to core impression-material families. Latin America carries a high edentulism prevalence, which creates structural tailwinds for prosthodontics and implant-supported solutions that rely on accurate impression capture. In North America and Western Europe, clinical workflows often combine analog and digital steps, using analog verification when case complexity rises, which sustains premium putty use in multi-unit and full-arch work. These patterns align with a hybrid model that favors fit accuracy while absorbing lab productivity gains.

Across the Asia-Pacific region, aging populations and rising oral-health awareness create a persistent demand for indirect treatments that depend on accurate impressions. Disease-burden research indicates the global count of people affected by oral conditions remains large and shows minimal improvement, which supports continued consumption of precision materials in high-volume markets. North American group practices continue to standardize case routing and material choice through digital platforms and shared procurement, which keep consumables demand steady across locations. In Canada, recent cycles document measurable edentulism prevalence, reinforcing steady prosthodontic volume, while U.S. surveillance highlights higher untreated decay rates in certain adult subgroups, translating into stable indirect case flows 150. European suppliers report portfolio streamlining under MDR alongside continued access to flagship putty ranges, indicating steady supply within a more focused set of variants.

In the Middle East and Africa, investment in clinics and training expands access to advanced materials, though dentist-to-population ratios still limit procedural throughput in many countries. Latin America’s high edentulism prevalence underpins prosthodontic care, with studies documenting shifts in age-standardized rates but growth in absolute case counts that keep restorative demand visible. In Europe’s largest economies, vendors focus on core catalogues that meet stringent documentation standards, supported by diversified brand families that can amortize regulatory costs. Overall regional dynamics point to a stable demand profile in developed markets, a faster rise in Asia-Pacific, and steady case growth in Latin America that together support the long-run outlook for the dental putty market.

Competitive Landscape

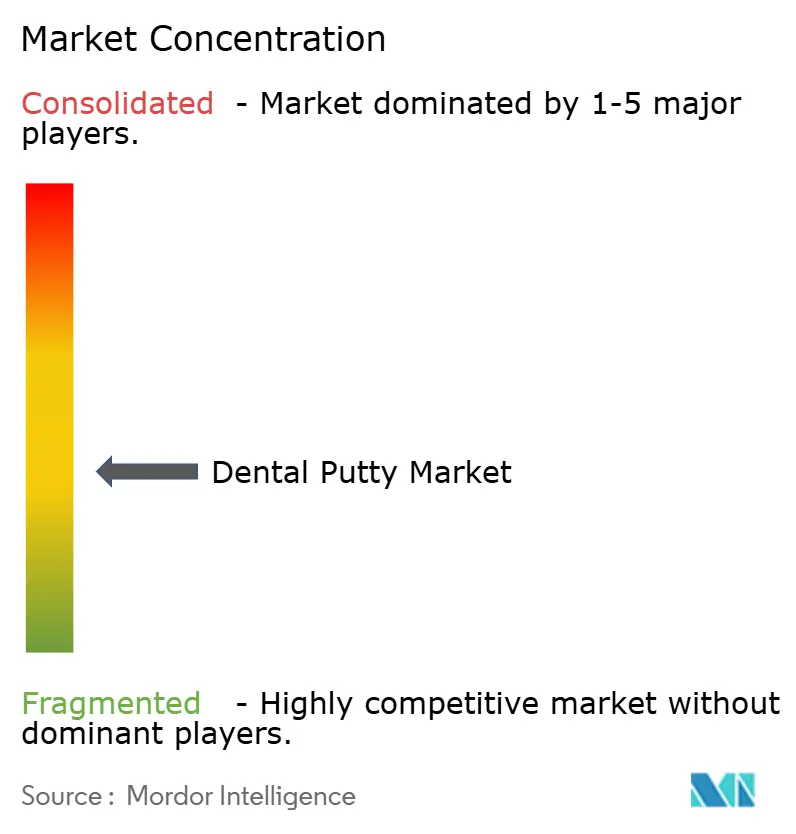

The dental putty market is fragmented, with no single company exceeding a mid-teens global share, which reflects proven legacy chemistries and training-based brand loyalty. Multinational incumbents provide breadth across chemistries, viscosities, and delivery forms, alongside distribution and digital ecosystems that help clinics align materials with workflows. Several European specialists maintain strong regional positions with focused portfolios and close lab relationships, while regional manufacturers and distributors serve localized demand. Integrated vendors that pair consumables with equipment and software can reinforce adoption through validated workflows that blend analog capture with digital design and manufacture. Suppliers also invest in clinical education and training that highlight handling, hydrophilicity, and set-time differences, which matter for subgingival margins and multi-implant stability. Together, these factors create a competitive pattern where product performance and portfolio completeness carry weight alongside distribution reach and service.

Recent strategic moves demonstrate how leading players sustain relevance in hybrid analog-digital environments. Dentsply Sirona expanded distribution partnerships across technology portfolios in early 2026, signaling a focus on enterprise-grade platforms that support standardized case management while accommodating analog verification where needed. Kettenbach introduced an improved 50 ml cartridge system in 2025 to simplify dispensing, viscosity identification, and mixing across its impression portfolio, which speaks to steady product-cycle refinement in ergonomics and consistency. VOCO launched a retraction paste that seeks to reduce time and variability in tissue management, addressing a pre-impression step that influences final impression quality in subgingival sites. These steps illustrate a mix of ecosystem building, delivery updates, and procedure-adjacent innovation that supports clinical reliability.

Competitive positioning also reflects investment in validated digital denture routes and lab integrations that accept physical impressions for subsequent scanning. Dentsply Sirona’s partnership with Formlabs on printable denture systems shows direct alignment between material validation and production equipment, which makes it easier for clinics to keep analog intake while adopting digital manufacture. Desktop scanning and lab software updates from major equipment vendors reinforce hybrid pathways by ingesting physical impressions and articulator settings that practitioners rely on during case planning. In this environment, product families that combine hydrophilicity, quick set, and stable rigidity remain attractive for complex indications, while VPS variants keep broad coverage in tooth-borne restorations. The result is a competitive cycle that emphasizes incremental improvements, verified interoperability, and service models that meet clinics at their current stage of digital adoption, which sustains ongoing demand in the dental putty market.

Dental Putty Industry Leaders

COLTENE Holding AG

Dentsply Sirona Inc.

GC Corporation

Ivoclar Vivadent AG

Kerr Corporation (Envista Holdings Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Ivoclar and Benco Dental expanded their two-decade partnership to distribute Ivoclar’s complete CAD/CAM block portfolio for the Dentsply Sirona CEREC system across the United States, broadening access for chairside milling workflows that can integrate with analog-impression verification for multi-unit cases

- December 2025: GC Corporation launched a new dental putty product line, G-C Putty Pro, in 2025 to expand its portfolio in Asia-Pacific markets. The product was positioned for improved handling and dimensional stability in crown and bridge impressions. It was targeted at clinics shifting toward faster impression workflows. The launch reinforced GC’s competitive position in silicone-based impression materials.

- July 2025: Kettenbach Dental introduced an improved 50 ml cartridge dispensing system across its impression-material portfolio, enhancing mixing accuracy, workflow efficiency, and material consistency for VPS-based systems used in dental putty applications.

Global Dental Putty Market Report Scope

As per the scope of the report, dental putty is a viscous, elastomeric impression material used in dentistry to create accurate molds of teeth and oral structures. It is typically based on polyvinyl siloxane (PVS) or polyether materials, offering high dimensional stability and precision. Dentists use it primarily in crowns, bridges, implants, and prosthodontic procedures to capture detailed impressions. It serves as a key component in two-step or single-step impression techniques for restorative dentistry.

The dental putty market is segmented by type, product type, application, delivery form, end user, and geography. By type, the market is segmented into regular set and fast set. By product type, the market is segmented into VPS (A-silicone) putty, polyether putty, and condensation silicone (C-silicone) putty. By application, the market is segmented into prosthodontics (fixed and removable), implantology, restorative dentistry (indirect), and orthodontics and occlusal records. By delivery form, the market is segmented into hand-mix jars, automix cartridges, and unit-dose / preportioned packs. By end-user, the market is segmented into dental clinics, hospitals, dental laboratories, and academic & research institutes. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Regular Set |

| Fast Set |

| VPS (A-silicone) Putty |

| Polyether Putty |

| Condensation Silicone (C-silicone) Putty |

| Prosthodontics (fixed and removable) |

| Implantology |

| Restorative Dentistry (indirect) |

| Orthodontics and Occlusal Records |

| Hand-mix Jars |

| Automix Cartridges |

| Unit-dose / Preportioned Packs |

| Dental Clinics |

| Hospitals |

| Dental Laboratories |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Regular Set | |

| Fast Set | ||

| By Product Type | VPS (A-silicone) Putty | |

| Polyether Putty | ||

| Condensation Silicone (C-silicone) Putty | ||

| By Application | Prosthodontics (fixed and removable) | |

| Implantology | ||

| Restorative Dentistry (indirect) | ||

| Orthodontics and Occlusal Records | ||

| Delivery Form | Hand-mix Jars | |

| Automix Cartridges | ||

| Unit-dose / Preportioned Packs | ||

| End-User | Dental Clinics | |

| Hospitals | ||

| Dental Laboratories | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the dental putty market growth outlook to 2031?

The dental putty market size is forecast to rise from USD 368.23 million in 2025 to USD 560.41 million by 2031 at 7.25% CAGR over 2026-2031.

Which regions lead and which are growing fastest in dental putty?

North America led with 36.74% share in 2025, while Asia-Pacific is projected to post the fastest growth at 9.73% CAGR through 2031.

Which material chemistry will dominate dental putty demand?

VPS remains the volume leader with 58.91% share in 2025, while polyether is the fastest-growing due to hydrophilicity and rigidity suited for complex implant cases.

How will applications shift within dental putty usage?

Prosthodontics holds the largest share at 46.18% in 2025, and implantology is set to grow fastest at 8.95% CAGR due to expanding complex, multi-unit protocols.

What delivery forms and set types are preferred in practice?

Automix cartridges lead with 51.32% share, and hand-mix jars are growing at 7.65% CAGR, while fast-set formulations are advancing at 7.98% CAGR alongside regular-set’s large installed base.

Why do analog impressions continue alongside digital scanners?

Full-arch, subgingival, and immediate-load cases still benefit from analog verification for margin fidelity and passive fit, so clinics and labs operate hybrid analog-digital workflows.

Page last updated on: