Dental Plaster Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

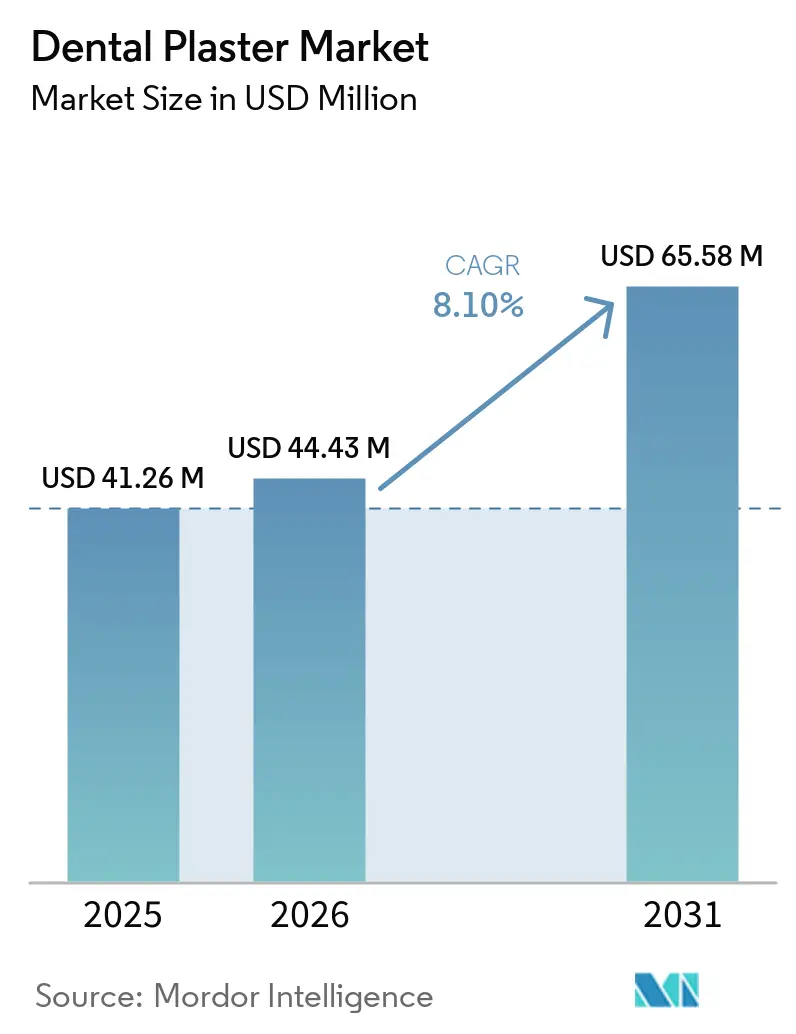

| Market Size (2026) | USD 44.43 Million |

| Market Size (2031) | USD 65.58 Million |

| Growth Rate (2026 - 2031) | 8.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Plaster Market Analysis by Mordor Intelligence

The Dental Plaster Market size is projected to be USD 41.26 million in 2025, USD 44.43 million in 2026, and reach USD 65.58 million by 2031, growing at a CAGR of 8.10% from 2026 to 2031.

Demographic aging, expanding prosthodontic workloads, and the material’s sub-20-micron detail fidelity sustain gypsum demand even as intraoral scanners and resin printing capture routine indications. Implantology remains a gypsum stronghold because technicians rely on the material’s tactile feedback when seating zirconia or metal frameworks prior to final sintering. ISO 6873 tolerance tightening reinforces premium Type IV and Type V adoption, while dental-tourism corridors in the Asia–Pacific and Latin America accelerate rush-turnaround orders that still favor fast-setting stones. At the same time, coal phase-out policies in Europe threaten flue-gas-desulfurization gypsum supply, prompting long-term sourcing contracts and recycled-gypsum pilots.

Key Report Takeaways

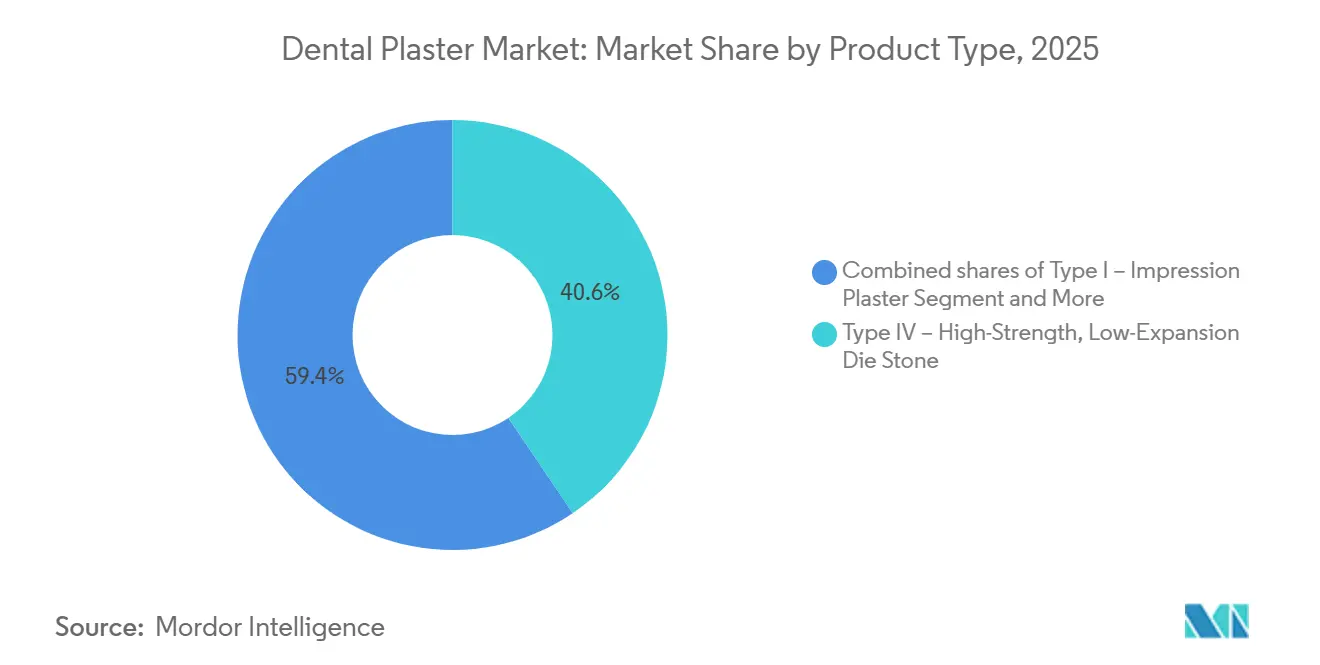

- By product type, Type IV high-strength, low-expansion stone captured 40.56% of the dental plaster market share in 2025 and is forecast to post a 9.1% CAGR through 2031.

- By application, restorative and prosthodontics held 47.81% of the dental plaster market size in 2025, while implantology & CAD/CAM dies are projected to expand at a 10.16% CAGR to 2031.

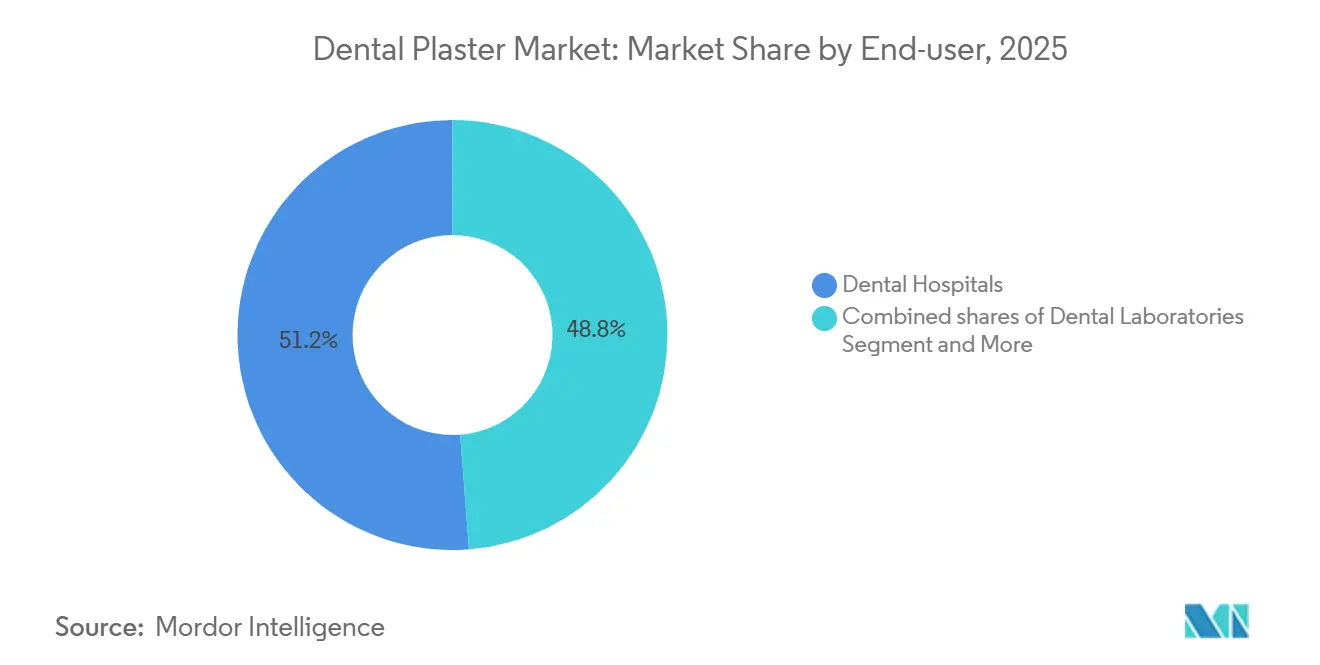

- By end user, dental hospitals commanded 51.23% revenue in 2025, yet dental clinics are advancing at a 10.39% CAGR through 2031.

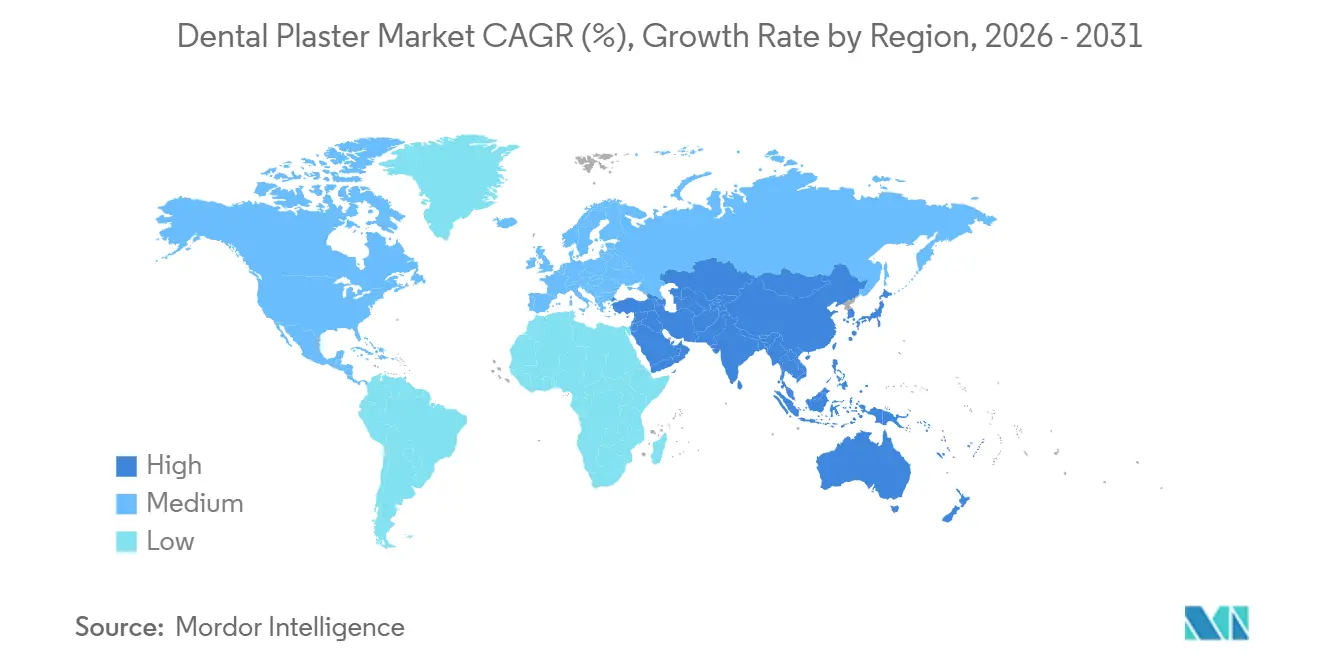

- By geography, North America led with 40.67% share in 2025, whereas the Asia–Pacific is expected to grow at a 10.05% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dental Plaster Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising oral disease burden boosts restorative and prosthodontic case volumes | +1.8% | Global, with concentration in aging OECD economies and emerging middle-class cohorts in India, Brazil, Indonesia | Medium term (2-4 years) |

| Expansion of dental clinics/labs and dental tourism (especially APAC) increases model fabrication | +2.1% | APAC core (Thailand, Vietnam, India), spill-over to Mexico, Turkey, Hungary | Short term (≤ 2 years) |

| Product innovations: low-expansion, scannable Type IV/V stones enabling hybrid digital workflows | +1.4% | North America, Western Europe, urban APAC hubs (Seoul, Tokyo, Singapore) | Medium term (2-4 years) |

| Aging populations and edentulism drive dentures and implant-supported prostheses | +1.6% | Global, acute in Japan, Germany, Italy, and US sunbelt states | Long term (≥ 4 years) |

| ISO 6873 tolerance tightening and QA traceability spur premium, consistent stones | +0.9% | EU and North America, gradual adoption in GCC and Latin America | Long term (≥ 4 years) |

| Gypsum's accuracy and stability keep it as verification/reference standard in hybrid workflows | +1.2% | Global, particularly high-value implant and full-arch cases in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Oral Disease Burden Boosts Restorative And Prosthodontic Case Volumes

Global caries and periodontitis prevalence ensures a steady pipeline of crowns, bridges, and dentures that rely on dimensionally stable casts[1]Centers for Disease Control and Prevention, “Oral Health Surveillance Report,” cdc.gov. In the United States, 15.2% of adults aged 65+ were edentulous in 2024, and the absolute cohort is climbing as baby boomers age. High-poverty segments record edentulism rates near 30%, concentrating prosthodontic workloads in safety-net clinics. Each complete denture consumes at least two gypsum casts, and implant-retained overdentures often require separate soft-tissue masters plus individual abutment dies, doubling stone use per case. This procedural intensity underpins sustained demand for premium Type IV stones that minimize remake risk when margins are thin.

Expansion Of Dental Clinics/Labs And Dental Tourism Increases Model Fabrication

Cross-border dentistry moved roughly 7 million patients in 2025, generating USD 5.2 billion in revenue as travelers sought 40-70% cost savings[2]Vietnam Investment Review, “Dental Tourism Growth,” vir.com.vn. Thailand, India, Mexico, Vietnam, Hungary, and Turkey anchor this network and rely on fast-setting stones that laboratories can turn around in 48-72 hours. Vietnam’s XDENT LAB opened a 1,500 m² denture plant in February 2025 to serve tourism inflows and domestic demand. Major manufacturers are following the chair count: Envista pledged RMB 1.0 billion for a Suzhou implant hub in July 2025, betting on China’s clinic buildout. Clinics themselves are adding cone-beam CT and chairside mills, yet still outsource multi-unit restorations that need gypsum verification, enlarging the dental plaster market footprint among private practices.

Product Innovations: Low-Expansion, Scannable Type IV/V Stones Enabling Hybrid Digital Workflows

Manufacturers now blend nano-sized calcium-sulfate hemihydrate with polymer modifiers to hit sub-0.1% expansion while boosting one-hour compressive strength beyond 60 MPa. The denser, smoother surface reflects structured light efficiently, letting desktop scanners capture sub-50-micron fidelity without spray. Whip Mix and Rapid Shape validated complete resin-and-gypsum ecosystems in April 2026, giving laboratories a single pipeline from pour to STL to printed prototype. Such hybrid paths keep the tactile verification technicians' trust, yet accelerate iteration loops, safeguarding gypsum relevance within digital dentistry’s rise. Premium pricing is justified as abrasion falls 70% versus legacy powders, cutting die replacement frequency in high-volume labs

Aging Populations And Edentulism Drive Dentures And Implant-Supported Prostheses

The global 60-plus cohort will double by 2050, sending edentulous counts above 600 million. Japan, Germany, Italy, and the U.S. Sunbelt states already see elevated full-arch workloads. Implant-supported overdentures require periodic relines and attachment swaps, each demanding fresh master casts. Immediate-loading protocols compress chair time but add interim models for try-ins within 48 hours of surgery. Each implant abutment warrants an individual Type IV die to assure passive fit and avert screw loosening, multiplying gypsum consumption compared with removable partial dentures. Consequently, aging drives a compounding effect on the dental plaster market rather than a linear rise.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intraoral scanning and 3D-printed models displace stone casts in many indications | -2.3% | North America, Western Europe, urban APAC (Seoul, Tokyo, Singapore) | Short term (≤ 2 years) |

| Moisture sensitivity and handling/storage variability cause inaccuracies, remakes, and waste | -1.1% | Global, acute in humid tropical climates (Southeast Asia, coastal Latin America) | Medium term (2-4 years) |

| Environmental/disposal concerns for gypsum waste increase compliance costs | -0.6% | EU, California, select Canadian provinces with landfill-diversion mandates | Long term (≥ 4 years) |

| Coal phase-out reduces FGD gypsum availability, pressuring raw material costs (EMEA focus) | -0.8% | Germany, Poland, Czech Republic, and other coal-dependent EU states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intraoral Scanning And 3D-Printed Models Displace Stone Casts In Many Indications

Scanner penetration rose significantly in developed practices by 2025, and modern optics give 20-50 micron trueness that equals PVS impressions poured in Type IV stone[3]Dental Tribune International, “Intraoral Scanner Adoption,” dental-tribune.com. Orthodontic models and single crowns seldom touch plaster now; an STL travels straight to a milling center. Each scanner sold erases up to 300 gypsum casts annually, pulling volume from the dental plaster market. Resin printers amplify displacement as aligner workflows require 30-50 staging models per case and deliver them in under four hours. Laboratories pivoting to aligners report that 80% of new study models are printed resins, not poured stone. While implants and full-arch cases still rely on physical dies, the substitution pressure on lower-value indications is immediate and material.

Moisture Sensitivity And Handling Variability Cause Inaccuracies, Remakes, And Waste

Calcium-sulfate hemihydrate is hygroscopic; exposure to greater than 70% RH introduces 0.02-0.05% dimensional drift, enough to miss ISO 6873 limits. Southeast Asian labs shoulder year-round humidity, forcing climate-controlled storerooms that raise overhead by 10%. Operator errors—wrong water ratios, inadequate vacuum mixing—compound risk, with small labs posting 5% remake rates on gypsum workflows versus <2% digitally. Environmental mandates tighten disposal rules; EU directives classify waste plaster as construction debris subject to recycling targets. Labs must pay haulers or install in-house slurry separators, adding compliance cost and denting dental plaster market profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Precision Needs Propel Type IV Dominance

Type IV high-strength, low-expansion stone accounted for 40.56% of the dental plaster market share in 2025 and is forecast to grow at 9.1% CAGR through 2031. This segment’s compressive strength surpasses 35 MPa within one hour, allowing aggressive margin trimming without chipping, and premium nano-filled variants exceed 62 MPa at the same mark. Resin-modified Type IV powders launched since 2024 cut abrasion by up to 83%, lengthening die life inside high-throughput labs. Type V stones hold niches where 0.20-0.30% expansion helps offset alloy shrinkage, but adhesion-based ceramics limit their addressable volume. In contrast, the Type III model stone faces direct competition from printed resins favored by orthodontic aligner producers, curbing its growth to low single digits.

Scannable surface engineering is reinvigorating Type IV relevance within digital workflows. Calcium-sulfate crystals are coated with reflective agents that enhance structured-light capture, eliminating the need for scan spray and saving technicians two minutes per die. Whip Mix partnered with Rapid Shape in April 2026 to cross-validate stones, scanners, and printers under one warranty umbrella. Such alliances protect gypsum’s role as a verification standard and differentiate suppliers on software compatibility rather than just powder chemistry. Competitors are exploring antimicrobial additives aimed at academic settings where infection-control audits are stringent, signaling further refinement in an already specialized niche of the dental plaster market.

By Application: Implantology And CAD/CAM Dies Lead Growth Curve

Restorative and prosthodontics generated 47.81% of the dental plaster market size in 2025, reflecting volumes of crowns, bridges, and full dentures processed worldwide. Nonetheless, implantology and CAD/CAM dies are racing ahead at a 10.16% CAGR due to rising immediate-load protocols and the popularity of digitally guided surgery. Each implant case demands diagnostic, surgical-guide, and final-prosthetic casts, tripling stone consumption compared with single-tooth crowns. Guided-surgery software hit significant penetration in implant placements across OECD markets in 2025, and every template relies on a master cast for sleeve positioning. Orthodontic study models, once a gypsum mainstay, are pivoting to resins as aligner manufacturers relocate production near clinic clusters, hurting Type III volumes.

The implant surge has secondary ripple effects: laboratories invest in articulators capable of full-arch dynamic occlusion, which still require rigid stone mounting plates. This ancillary hardware purchase secures additional, though smaller, powder sales. Meanwhile, model-based casting for occlusal night guards remains relatively stable, as many dentists consider printed guards brittle when adjusted chairside. Overall, application dynamics illustrate that the dental plaster market continues to migrate toward complex, multi-step restorations where tactile verification and strength are indispensable.

By End User: Clinics Capture Growth While Hospitals Remain Volume Anchor

Dental hospitals held 51.23% revenue share in 2025 due to their caseload of maxillofacial reconstruction and teaching obligations. Private dental clinics, however, are forecast to register a 10.39% CAGR through 2031 as chairside mills and cone-beam CT units plunge below USD 50,000, lowering entry barriers for advanced procedures. Clinics still outsource intricate implant frameworks to off-site labs that insist on ISO-certified Type IV stones, pulling gypsum demand deeper into the fragmented clinic channel. Laboratories themselves remain the largest absolute purchasers, but will cede market share as vertical integration by dental-service organizations gains steam.

Academic institutes contribute a modest portion of the dental plaster market, yet they serve as opinion leaders. Curriculum emphasis on hybrid workflows trains new graduates to pour, scan, and trim Type IV casts, perpetuating material familiarity despite scanner ubiquity. Vendors courting universities often bundle education discounts with traceability software, seeding long-term brand loyalty. Net, decentralization shifts buying patterns from a handful of hospitals to thousands of clinics without shrinking total powder volumes, offering distributors an expanded but more complex logistics map.

Geography Analysis

North America commanded 40.67% revenue in 2025, aided by stringent FDA rules that favor premium, lot-certified powders and by a procedural mix rich in high-margin implant rehabilitations. The United States hosts over 200,000 active dentists, and demand clusters in full-arch restorations spur consistent Type IV consumption. Reimbursement linked to same-day dentistry accelerates digital impressions for single crowns, but laboratories keep gypsum in play for framework verification, anchoring regional sales.

Europe faces a moderate CAGR as its dental plaster market contends with impending FGD-gypsum shortages once coal plants are shuttered by 2038. Manufacturers are hedging with multi-year quarry leases in Spain and imports from North Africa, yet freight and environmental permit delays weigh on margins. ISO-driven quality audits in Germany and France push labs toward premium, traceable powders, partially offsetting volume softness. The EU’s landfill-diversion rules add handling costs that encourage some labs to trial resin models, dampening Type III demand more than Type IV.

Asia–Pacific is the clear growth engine, projected at a 10.05% CAGR from 2026 to 2031. China, India, Vietnam, and Indonesia are commissioning new clinics at a significant pace, and cross-border dental tourism funnels patients to Thailand and Vietnam, where a 48-hour turnaround favors stone over printed resins. Envista’s RMB 1.0 billion implant plant in Suzhou signals confidence in future caseloads, while localized denture mega-labs like XDENT cut freight times and anchor gypsum procurement in-country. The Middle East and Africa benefit from Gulf diversification schemes that subsidize clinic networks, whereas Latin America’s growth hinges largely on Brazil’s macro stability. Overall, regional momentum ensures the dental plaster market remains globally balanced yet opportunity-rich.

Competitive Landscape

The dental plaster market shows moderate concentration; GC Corporation, Kerr Dental (Envista), Kulzer, Zhermack, SHERA, and Whip Mix together hold about the majority of the share, leaving room for agile regional suppliers. Competitors differentiate on scannable-surface technology, abrasion resistance, and ISO-documented traceability. Whip Mix’s 2026 tie-up with Rapid Shape bundles stones, scanners, and printers in one validated loop, raising switching costs for laboratories. Amann Girrbach’s April 2026 Ceramill software upgrade extended design modules for cast partial dentures and introduced milling tools with 300% longer life, highlighting a pivot toward recurring consumable revenue.

Raw-material security is emerging as a strategic lever. European formulators are scouting quarry acquisitions to hedge against FGD-supply decline, which could trigger consolidation and lift barriers for smaller entrants. In high-growth APAC, distributors emphasize 24-hour delivery and in-person training to win loyalty among new clinic owners. Resin printer makers continue to court gypsum users with hybrid toolchains, but technicians favor powders that provide tactile margin feel, preserving a defensible moat. The next battleground may be antimicrobial or color-shifting stones that visually signal full set, reducing premature die trimming and associated remakes.

Dental Plaster Industry Leaders

GC Corporation

Kulzer GmbH

Zhermack SpA

SHERA Werkstoff-Technologie GmbH

Kerr Dental (Envista)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The Oral Health Foundation endorsed the government's plan to establish new neighborhood health centers across England. However, it emphasizes that these centers should not be perceived as a short-term solution to the systemic issues affecting NHS dentistry.

- November 2025: South Korean specialists have developed an innovative plaster designed to restore teeth naturally. Industry experts anticipate that this advancement could potentially replace traditional fillings, invasive surgeries, and high-cost dental procedures in the future. The plaster delivers the drug Tideglusib directly to the gum tissues through micro-needles.

Global Dental Plaster Market Report Scope

As per the scope of the report, dental plaster, chemically known as calcium sulfate hemihydrate, is a fundamental material in dentistry derived from the naturally occurring mineral gypsum. The primary uses of dental plaster centers are around their role as auxiliary material in dental laboratories and clinics.

The dental plaster market is segmented by product type, application, end users, and geography. Based on product type, the market is segmented into Type I - impression plaster, Type II - model/articulating plaster, Type III - dental stone (model stone), Type IV - high-strength, low-expansion die stone, and Type V - high-strength, high-expansion die stone. Based on application, the market is segmented into restorative & prosthodontics, orthodontics & study models, implantology & CAD/CAM dies, model base & articulation. By end users, the market is segmented into dental laboratories, dental hospitals, dental clinics, and academic & research institutes. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Type I - Impression Plaster |

| Type II - Model/Articulating Plaster |

| Type III - Dental Stone (Model Stone) |

| Type IV - High-Strength, Low-Expansion Die Stone |

| Type V - High-Strength, High-Expansion Die Stone |

| Restorative & Prosthodontics (crowns, bridges, dentures) |

| Orthodontics & Study Models |

| Implantology & CAD/CAM Dies |

| Model Base & Articulation |

| Dental Laboratories |

| Dental Hospitals |

| Dental Clinics |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type (ISO 6873) | Type I - Impression Plaster | |

| Type II - Model/Articulating Plaster | ||

| Type III - Dental Stone (Model Stone) | ||

| Type IV - High-Strength, Low-Expansion Die Stone | ||

| Type V - High-Strength, High-Expansion Die Stone | ||

| By Application | Restorative & Prosthodontics (crowns, bridges, dentures) | |

| Orthodontics & Study Models | ||

| Implantology & CAD/CAM Dies | ||

| Model Base & Articulation | ||

| By End-user | Dental Laboratories | |

| Dental Hospitals | ||

| Dental Clinics | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current dental plaster market size and its expected 2031 value?

The dental plaster market size stands at USD 44.43 million in 2026 and is projected to reach USD 65.58 million by 2031.

How fast is the market growing?

Between 2026 and 2031 the market is forecast to expand at an 8.1% CAGR, driven mainly by implantology and Asia–Pacific clinic growth.

Which product type holds the largest share?

Type IV high-strength, low-expansion die stone commanded 40.56% market share in 2025 and remains the precision benchmark for implants and CAD/CAM frameworks

Why is Asia–Pacific the fastest-growing region?

Rapid clinic buildouts, thriving dental tourism in Thailand and Vietnam, and rising middle-class procedure uptake push the region toward a 10.05% CAGR to 2031.

Page last updated on: