Dental Lights Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.36 Billion |

| Market Size (2031) | USD 1.85 Billion |

| Growth Rate (2026 - 2031) | 6.35% CAGR |

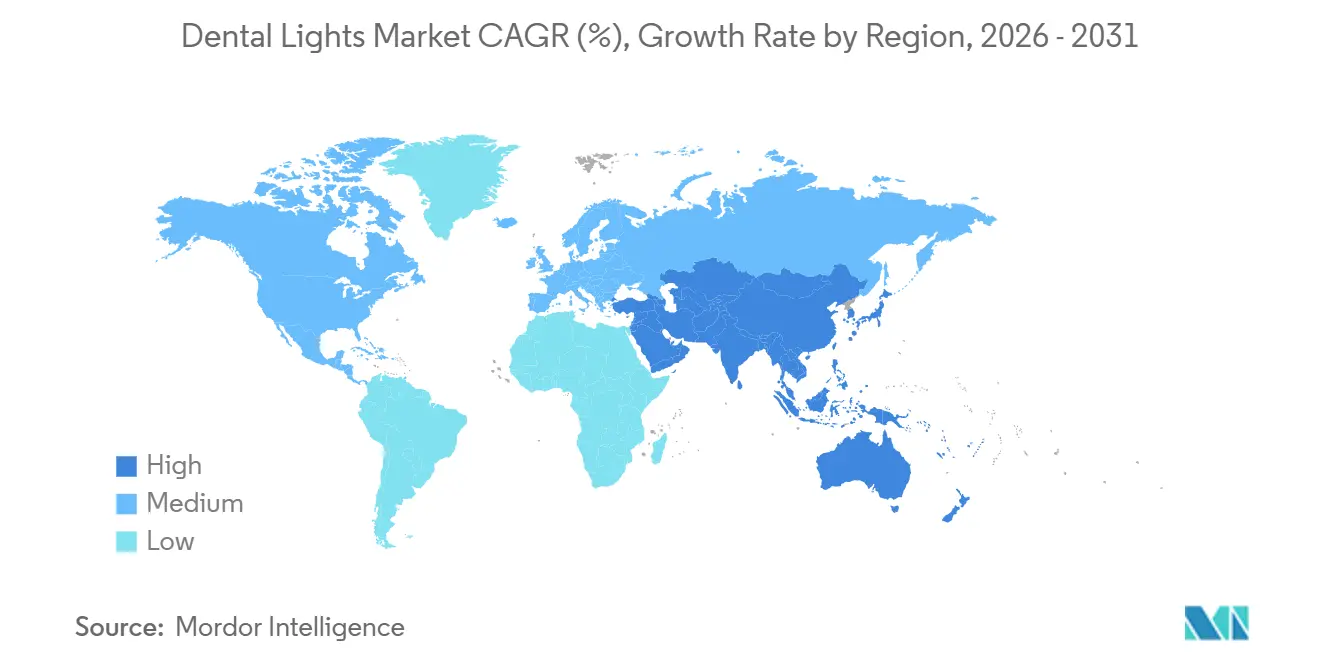

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

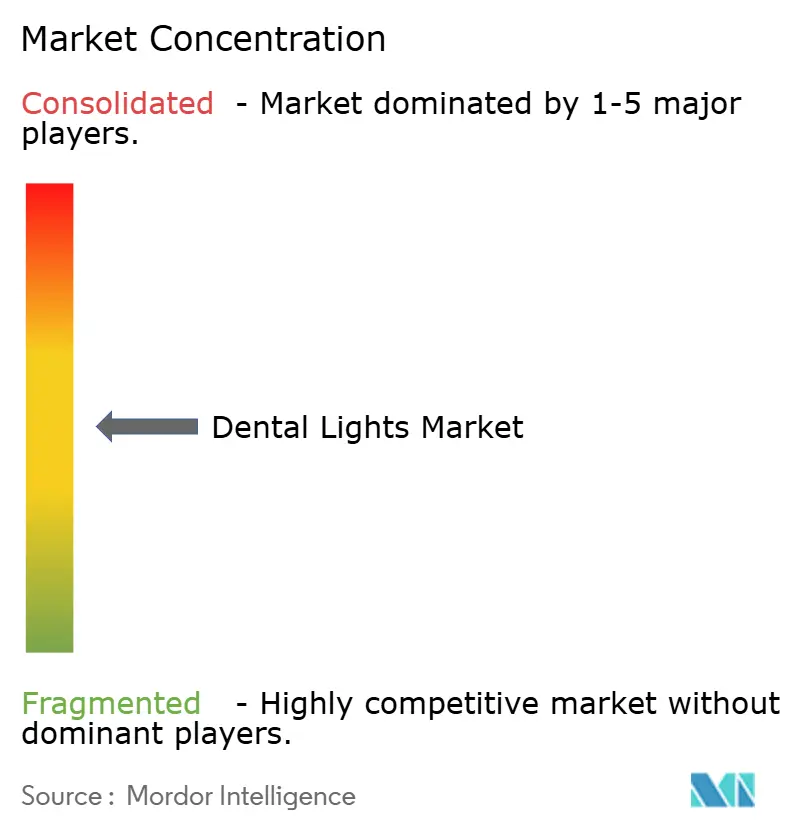

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Lights Market Analysis by Mordor Intelligence

The Dental Lights Market size was valued at USD 1.29 billion in 2025 and is estimated to grow from USD 1.36 billion in 2026 to reach USD 1.85 billion by 2031, at a CAGR of 6.35% during the forecast period (2026-2031).

LED systems already dominate unit volumes, yet a resilient halogen niche grows even faster because restorative dentists prize the technology’s consistent color-rendering index above 95. Ceiling-mounted fixtures remain the mainstream choice for large multi-chair operatories, while demand for mobile and portable lights accelerates in geographies where infrastructure flexibility matters more than floor-plan uniformity. Regional dynamics are diverging: North America retains its revenue lead on the back of dental service organization (DSO) consolidation, whereas Asia-Pacific records the quickest unit expansion as China’s domestic-production mandate and India’s new National Dental Commission stimulate equipment renewal. Competitive intensity stays moderate; integration strategies by the leading manufacturers tie illumination to delivery units, imaging, and data platforms, helping them defend share against smaller specialists that differentiate on spectral fidelity or portability.

Key Report Takeaways

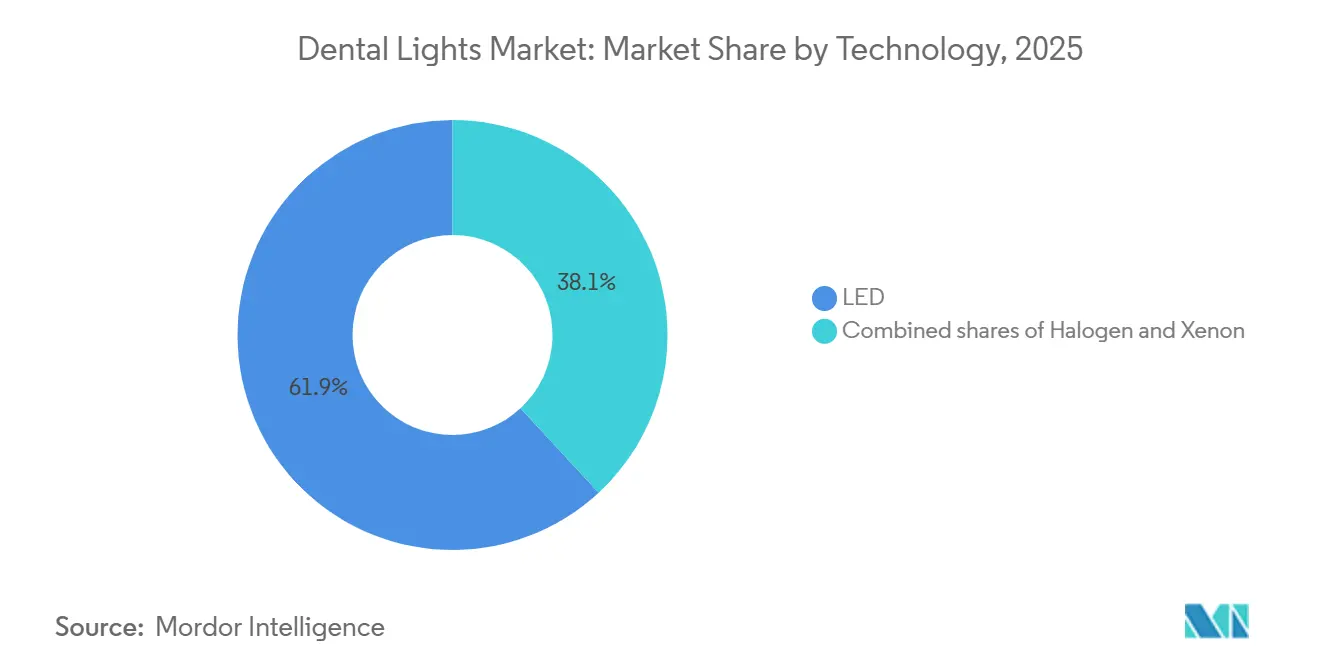

- By technology, LED captured 61.90% of the Dental lights market share in 2025, while halogen is forecast to expand at an 8.10% CAGR through 2031.

- By mounting type, ceiling-mounted lights held 48.93% revenue share in 2025; mobile and portable units are projected to climb at an 8.04% CAGR to 2031.

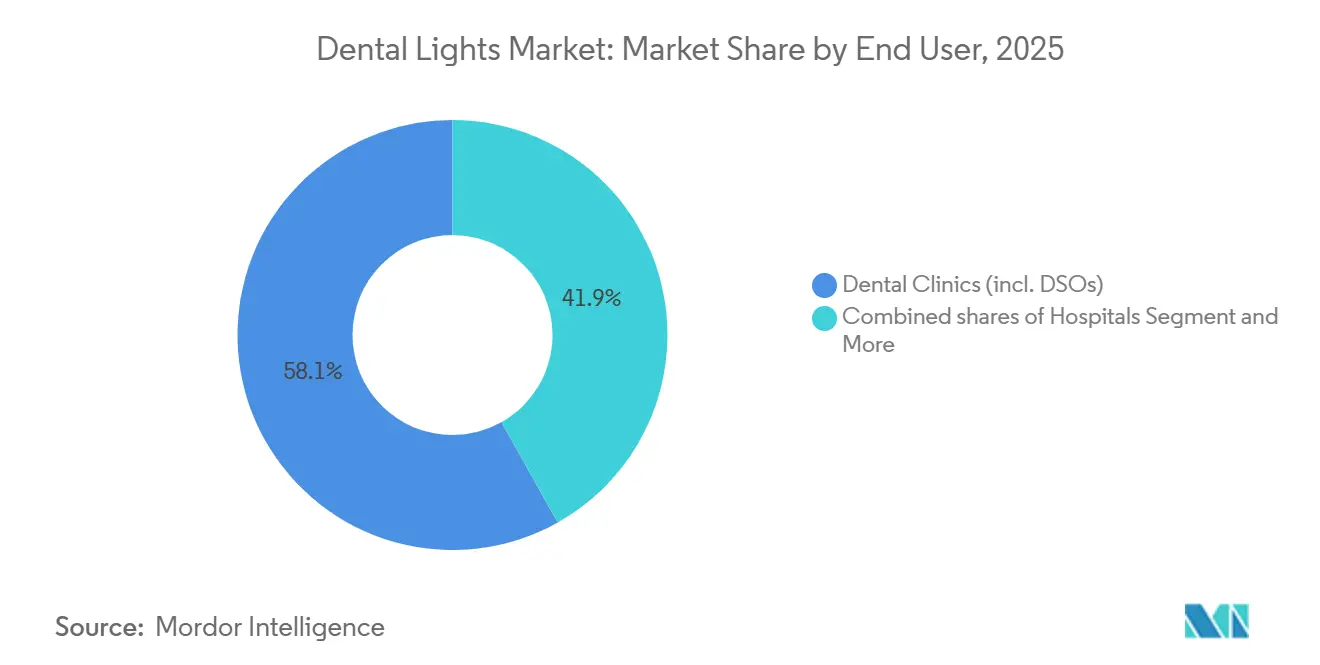

- By end user, dental clinics accounted for 58.14% of the Dental lights market size in 2025 and are advancing at a 9.67% CAGR through 2031.

- By geography, North America commanded 42.10% share of the Dental lights market size in 2025, whereas Asia-Pacific is advancing at an 8.13% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dental Lights Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| LED transition for efficiency, longevity, and heat reduction | +1.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Infection-control and touchless workflows | +1.2% | Global, notably North America and Asia-Pacific cities | Short term (≤2 years) |

| Expansion of DSOs and multi-operatory buildouts | +1.5% | North America core, spillover to Europe and Australia | Medium term (2-4 years) |

| Rising cosmetic and restorative procedure volumes | +1.0% | Global, concentrated in high-income urban hubs | Long term (≥4 years) |

| Regulatory/ecodesign shifts accelerating LED retrofits | +0.6% | Europe and North America; emerging in Asia-Pacific | Medium term (2-4 years) |

| Digital imaging integration with tunable CCT/CRI | +0.7% | Premium segments in North America, Europe, Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

LED Transition for Efficiency, Longevity, and Heat Reduction

LED operatory lamps cut energy use by up to 80% and last 15,000-50,000 hours versus halogen’s 500-2,000-hour bulbs, eliminating frequent replacements and the associated labor burden. They also generate minimal radiant heat, improving patient comfort and letting sealed housings withstand aggressive disinfectants. Despite those advantages, practitioners who perform complex shade-matching still migrate slowly because only premium multi-wavelength arrays reach CRI 95 or higher, a benchmark halogen meets with ease. The American Dental Association reported that LED multi-wave light-curing units already represented a significant portion of units in clinical use, underscoring momentum behind the solid-state shift.

Infection-Control and Touchless Operatory Workflows

The pandemic cemented touchless activation as a new normal. Motion or proximity sensors now accompany most mid- and high-tier lights, minimizing cross-contamination risk and satisfying stricter hygiene protocols in DSO networks. These features pair naturally with connected ecosystems that log usage hours and automate maintenance reminders. A related occupational-health question has emerged: a 2026 Nature study found that 22.4% of dentists exhibit vision issues linked to prolonged blue-light exposure, roughly double the rate of non-dentists. If regulators translate such findings into tougher blue-hazard limits than ISO 9680:2021’s current illuminance threshold, vendors will need adaptive dimming or spectral-filtering upgrades.

Expansion of DSOs and Multi-Operatory Buildouts

PDS Health passed 1,000 affiliated offices and Dentalcorp operated 575 clinics by 2025, giving DSOs formidable purchasing power. Standardized ceiling-mounted LED systems with integrated delivery units help these chains streamline training, inventory, and service contracts, making DSOs the single largest growth engine for the Dental lights market. The model is replicating, albeit slowly, in Western Europe and Australia.

Regulatory/Ecodesign Shifts Accelerating LED Retrofits

EU Ecodesign Regulation 2019/2020 pushes for CRI ≥80, strict flicker limits, and ≤0.5 W standby draw, while ISO 9680:2021 requires 15,000 lux minimum illuminance and CRI/Rf ≥85. Even though dental lights integrated into medical devices enjoy certain exemptions, the direction of travel is clear: efficient, modular LED designs gain compliance advantages and lower lifecycle costs [1]ISO, “ISO 9680:2021 Dentistry — Operating light,” iso.org.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Upfront cost pressure for small practices | -0.9% | Global, acute in emerging Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Compliance burden under ISO 9680:2021 and MDR | -0.5% | Europe and North America; emerging in Asia-Pacific | Medium term (2-4 years) |

| LED/optics component supply variability | -0.4% | Global, concentrated in North America and Europe manufacturing hubs | Short term (≤ 2 years) |

| Retrofit constraints in low-ceiling/legacy operatory rooms | -0.3% | North America and Europe legacy practices; select Asia-Pacific urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Upfront Cost Pressure for Small Practices

Integrated LED packages cost USD 7,000-15,000. Although 80% of practices rely on financing, credit access remains uneven and monthly payments compete directly with staff and consumables budgets. Refurbished halogen units therefore stay attractive, particularly in clinics serving lower-income populations or rural catchments.

Compliance Burden Under ISO 9680:2021 and MDR

Full photometric, flicker, and biocompatibility testing can cost USD 50,000-200,000 per product line. Large multinationals amortize the outlay across broad portfolios, but smaller firms either retreat to niche geographies or accept buy-outs. The EU’s Medical Device Regulation further tightens post-market surveillance, spurring defensive mergers and acquisitions to pool regulatory expertise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Halogen’s Niche Defies LED Dominance

LED products commanded 61.90% Dental lights market share in 2025, yet halogen posts an 8.10% CAGR. Halogen remains indispensable for specialist clinics where CRI 95-plus color fidelity is non-negotiable. Premium LEDs with multi-wavelength chips are closing the gap, but their price premium sustains a dual-technology landscape. The Dental lights market size for LED platforms will keep expanding, but a loyal halogen customer base guarantees parallel demand through at least 2031.

Second-generation LEDs win favor with DSOs due to 80% lower energy consumption and 15,000-50,000-hour lifespans. Manufacturers reinforce that advantage by bundling lights with imaging and power modules, locking customers into proprietary ecosystems. Meanwhile, xenon stays peripheral, confined to surgical suites that prioritize instant-on brightness over maintenance convenience.

By Mounting Type: Portable Units Gain as Flexibility Trumps Standardization

Ceiling-mounted configurations retained 48.93% Dental lights market share in 2025 due to ergonomic reach and clutter-free floors, but mobile and portable units are forecast to grow 8.04% annually. Rural outreach clinics, humanitarian missions, and emerging-market practitioners value battery operation and wheelbase mobility more than architectural aesthetics. The Dental lights market size contributed by mobile variants remains smaller than ceiling systems, yet their faster growth signals a structural pivot toward flexible care models.

Chair- or unit-mounted lights appeal to single-operator practices seeking integrated delivery systems, while wall-mounted variants shrink as building codes and ceiling installations improve. Product development reflects these preferences: high-end ceiling models now feature sensor activation and tunable spectra, whereas portable units emphasize rugged frames, quick-swap batteries, and simplified maintenance.

By End User: Dental Clinics Dominate as DSOs Drive Standardization

Dental clinics—including corporate DSOs—held 58.14% of the Dental lights market size in 2025 and will rise at a 9.67% CAGR to 2031. Large networks exploit scale to secure volume discounts and standardize LED setups across multi-chair locations, reinforcing ceiling-mounted leadership. Hospitals and academic institutes buy fewer lights and replace them less often because capital-budget cycles are slower and procurement hurdles higher. Dental laboratories fall outside routine operatory use and represent a marginal share.

Independent private practices still populate most developing regions, yet even they gravitate gradually to LED once financing terms improve, illustrating how end-user dynamics amplify the Dental lights market’s broader LED transition.

Geography Analysis

North America generated 42.10% of global revenue in 2025, fueled by DSO expansion and a high density of cosmetic procedures that demand advanced lighting. Nevertheless, replacement cycles lengthen as early adopters reach saturation, tempering regional growth below the global CAGR.

Asia-Pacific is the fastest-growing zone at 8.13% per year. China mandates that the majority of dental chairs be locally made by 2026, driving domestic lamp manufacturing and import partnerships. India’s 2026 National Dental Commission seeks to close severe care gaps—fewer than one in four primary health centers employ a dentist—thereby lifting demand for portable units and entry-level LED kits. Japan’s aging society and Australia’s budding DSO sector add premium demand layers, while Southeast Asia adopts a mixed value-premium profile.

Europe exhibits moderate growth underpinned by strict compliance. Northern and Western countries upgrade to tunable LED systems, whereas Southern Europe leans on entry-level LEDs and refurbished halogen models to control costs. The Middle East invests in dental-tourism hubs equipped with high-CRI ceiling lights, and Africa sees sporadic but rising outreach and university purchases. South America’s demand concentrates in Brazil and Argentina, where currency swings complicate import affordability yet urban cosmetic practices mirror global LED preferences.

Competitive Landscape

A-dec, Dentsply Sirona, Planmeca, Midmark, and Takara Belmont anchor a top tier that bundles lighting with chairs, imaging, and asset-tracking software. Their integration playbooks raise switching barriers and protect margins. Planmeca’s 2025 launch of the Pro50 S, Pro40, and Solanna Vision—each ISO- and CE-compliant—exemplifies vertical-integration leverage. FARO and BPR Swiss compete on spectral accuracy; FARO’s B75 delivers CRI 98 with tunable 2,700-5,700 K output, targeting cosmetic specialists who will not trade optical fidelity for ecosystem lock-in.

Portable-segment activity is brisk, with Chinese and U.S. mid-caps supplying battery-operated kits to outreach programs and small clinics. Regulatory burdens drive consolidation: Röko AB’s 2026 majority stake in Lambda S.p.A. pooled resources for photometric testing and MDR submissions. Data-centric offerings emerge as differentiators; Midmark’s connected ecosystem logs lamp usage and integrates RFID instruments, signaling a shift toward analytics-driven operatory management.

Dental Lights Industry Leaders

Dentsply Sirona

A‑dec Inc.

Planmeca Oy

Midmark Corporation

Takara Belmont Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: A-dec and Dentsply Sirona integrated the Midwest Motor System into A-dec’s 500 Pro and 300 Pro chairs, uniting LED lighting, delivery, and imaging in a single platform.

- February 2026: Midmark unveiled a connected operatory suite that links LED lights, RFID-tagged handpieces, and cloud analytics for real-time asset management.

- February 2026: DentalEZ introduced the Forest 5400 chair package, bundling a value-priced LED light with U.S.-made upholstery for cost-sensitive independents.

Global Dental Lights Market Report Scope

As per the scope of the report, dental lights, technically known as dental operating or operatory lights, are specialized high-intensity lighting systems designed to illuminate a patient's oral cavity with focused, clear, and shadow-free light. These fixtures are essential for providing practitioners with the visibility needed to perform intricate procedures, such as diagnostic exams and restorative work, while reducing eye strain and fatigue. Modern operatory lights are typically mounted to the dental chair, ceiling, wall, or a delivery system and feature adjustable swing arms and swivel joints that allow for precise positioning.

The dental lights market is segmented by technology, mounting type, end users, and geography. Based on technology, the market is segmented into LED, Halogen, and Xenon. Based on mounting type, the market is segmented into ceiling-mounted, chair-/unit-mounted, wall-mounted, and mobile/portable. By end users, the market is segmented into dental clinics, hospitals, academic & research institutes, and dental laboratories. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| LED |

| Halogen |

| Xenon (niche) |

| Ceiling-mounted |

| Chair-/Unit-mounted |

| Wall-mounted |

| Mobile/Portable |

| Dental Clinics and DSOs |

| Hospitals |

| Academic & Research Institutes |

| Dental Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology (Light Source) | LED | |

| Halogen | ||

| Xenon (niche) | ||

| By Mounting Type | Ceiling-mounted | |

| Chair-/Unit-mounted | ||

| Wall-mounted | ||

| Mobile/Portable | ||

| By End User | Dental Clinics and DSOs | |

| Hospitals | ||

| Academic & Research Institutes | ||

| Dental Laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast value of the Dental lights market by 2031?

The Dental lights market is projected to reach USD 1.85 billion by 2031.

How fast is the Dental lights market expected to grow?

It is set to register a 6.35% CAGR between 2026 and 2031.

Which technology segment is growing quickest within operatory lighting?

Halogen lights, driven by cosmetic specialists, are forecast to grow at 8.10% annually through 2031.

Why are DSOs important for equipment vendors?

DSOs consolidate purchasing, enabling large-scale LED standardization and multi-year service contracts that boost vendor retention

Page last updated on: